2019 community investment workshops

TRANSCRIPT

DATE: PRESENTED BY:

2019 Community Investment Workshops

2019 Community Investment Department

Affordable Housing Program

Homeownership InitiativesHOP, NIP, and AMP

Community Investments Program and Elevate

Today’s Agenda

O V E RV I E W

• Cooperatives created by Congress in 1932

• 11 regional banks with over $1 trillion in total assets

• Member owned – only members can access products/services

• Each FHLBank independently managed

• 10% of yearly net earnings from each bank are reinvested into communities

Federal Home Loan Bank System

F E D E R A L H O M E L O A N B A N K S Y S T E M

Where are we?

A S O F 1 / 3 1 / 1 9

What is FHLBank Indianapolis?

• Regional Wholesale Bank o Serving member financial

institutions throughout Indiana and Michigan since 1932.

• Our Missiono To provide a reliable source of

liquidity to members to support housing finance, asset-liability management, and community lending.

o To provide grants and low-cost loans to our members that help support affordable housing and economic development initiatives.

Credit Unions

34%

Insurance Companies

14%

CDFI's1%

Banks & Thrifts

51%

• The Community Investment Department illustrates the mission of FHLBI:

What we do is valuable!

• Our goal is to be good stewards of our AHP allocation by disbursing funds to quality requests and projects

• We strive to provide excellent customer service, operate efficiently, and be proactive

• In the end, people and communities are helped

Guiding Principles

Homeownership Initiatives (HOP: NIP: AMP): 35% = $7.9 Million in 2019First-come, first served grant funding programs that match each step in the lifecycle of home ownership.

A L L O C AT I O N S

Community Investment Programs

Affordable Housing Program (AHP): 65% = $14.7 Million in 2019Competitive grants awarded to members to support the creation of rental and homeownership opportunities for low- and moderate-income households.

Community Investment Program (CIP) Targeted $150 Million in 2019Discounted advances and letters of credit available to members on an ongoing basis to support targeted housing and economic development.

Elevate Small Business Grant Program – $375,000 in 2019Competitive grants awarded to members to help stimulate local economic development, workforce development and job creation through small businesses in the states of Indiana and Michigan.

DATE: PRESENTED BY:

CompetitiveAffordable Housing Program (AHP)

March 2019 MaryBeth Wott, FVP, Community Investment Officer

T H E B A S I C S

• Provides direct grants for the acquisition, rehabilitation, or construction of affordable housing.

• Only FHLBI members may apply for AHP grant funding.

• Maximum grant is $500,000.

• Project sponsors are housing developers (either for profit or nonprofit) that partner with an FHLBI member to complete the project.

Affordable Housing Program (AHP)

AHP: Competitive grants awarded to FHLBI members to support the

creation of rental and homeownership opportunities for low- and moderate-

income households.

Competitive AHP o Funded 29 projects

(3 alternates)o Total of $13 million o Created 1,066

affordable units

Highlights of 2018 Program Year

L I M I T E D TO H O U S I N G

• Eligible Project Types• Single family – single or

scattered site• Multi-family – single or multi-site• Domestic violence shelters• Homeless and emergency

housing shelters• Transitional housing• Permanent supportive housing• Group homes and congregate

living plans

Flexible Development Funding Source

Grants of up to $500,000 per

project!

• Ineligible Project Types• Nursing homes• Assisted living facilities• Echo or cottage housing

units for the elderly

M I N I M U M R E Q U I R E M E N T S

• Thresholds• Need for subsidy• Readiness to proceed• Reasonable & realistic• Capacity• Minimum requirements for targeting• Housing costs must be affordable

• Incomes must be validated with third-party documentation• AHP subsidy must be used for eligible purpose• AHP subsidy per unit limit is $50,000• Demonstrated market need for housing type

Eligibility Thresholds

A H P I S C O M P E T I T I V E –1 O F E V E R Y 2 A P P L I C AT I O N S I S A W A R D E D

• 5 pts Donated Property• 7 pts Non Profit Sponsorship• 20 pts Targeting• 5 pts Housing for Homeless• 8 pts Empowerment Initiatives• 8 pts Member Involvement • 3 pts Rural Housing• 9 pts Opportunity Targeting• 8 pts Desirable Sites• 5 pts Readiness to Proceed• 15 pts Subsidy per Unit• 7 pts Community Stability

AHP Scoring Summary - 2019

New Changes in 2019

New Changes in 2019

New Changes in 2019

New Changes in 2019

A H P R E Q U I R E S A N F H L B I M E M B E R PA RT N E R

• Member Role• Underwrites the projects • Maintains relationship with sponsor• Oversees construction and disbursement of AHP funds• May require additional reporting beyond AHP requirements• May be required to repay AHP subsidy • May require security instrument in addition to Retention Agreement• Provides compliance reports and disbursement requests to FHLBI

• Sponsor Role• Assemble a well documented realistic AHP Application• Inform the Member and FHLBI when things change• Prepare and assemble well documented compliance reports and

disbursement requests• Treat the AHP grant like a loan – the Member is! (AHP Agreement)• Understand requirements to remain in compliance with AHP Regulations• Understand repayment obligation

Roles & Expectations

W H AT M A K E S A G R E AT PA RT N E R ?

• Develop a relationship before you have a financial ask• Provide volunteer opportunities for employees• Research member website for their area of focus• Offer board seats to financial institution employees • Share success stories

Community financial institutions need the community to thrive in order to thrive!

Roles & Expectations

Awarded Application2019

Stage I –Development

Phase (1-3 yrs)2019-2022

Stage II –Project Completion

(3 yrs)2022

Completion Monitoring

(1 yr from completion)2023

Stage III – Long term monitoring

(for 15 yrs post-completion)

2037

Life Cycle of AHP Rental Project

FHLBI is involved in each AHP Rental Project for up to 18 years

2 0 1 9 P R O G R A M Y E A R

AHP Application Timeline

JanuaryImplementation Plan

2019 Released

MarchPre-application and Quick Smart Tools released

June 14, 2019Pre-Application Due

Date

JuneOn-Site Technical

Assistance

August 14Applications are due

at 5 PM ET

November 16Awards announced

G E T T I N G S TA RT E D F O R 2 0 1 9

• 2019 Implementation Plan• Review Threshold

Requirements• Quick Smart Score• Identify Partners• Technical Assistance On

Demand

Competitive AHP Program

• AHP Application Files –(excel format)• Getting Started Instructions• Pre- Application & Final

Application Assembly• Financial Workbook• Exhibit Cover Pages• Certification / Authorized

Signatures

• 2019 Implementation Plan• AHP Training Guide• AHP Application Tips & Tools• Notification of Intent • Technical Assistance on

Demand• AHP Training Webinars

(recorded)• Quick Smart Score• AHP Pre-Application & Final

Application Files• Awardee lists / Statistics

Available on our Website

Join us for an Underwriting Affordable Housing Workshop!• Affordable housing experts walk

you through the different layers of funding for affordable housing projects.

Check fhlbi.com/training for updates on future trainings and workshops.

Underwriting Affordable Housing

May 21, 2019

Detroit, MI

June 4, 2019

Indianapolis, IN

(800) 688.6697 (TOLL FREE)

AFFORDABLE HOUSING PROGRAM STAFF

VP, AHP Portfolio ManagerTrish Lewis – [email protected]

AHP Production ManagerMike Recker – [email protected]

Senior Compliance AnalystDevin Day – [email protected]

Senior Compliance AnalystErica Petty-Saunders – [email protected]

Compliance Analyst IAshlen Nisley- [email protected]

Federal Home Loan Bank of Indianapolis

DATE: PRESENTED BY:

Federal Housing Finance Agency AHP Final Rule

March 2019 MaryBeth Wott, FVP, Community Investment Officer

P U B L I S H E D I N T H E F E D E R A L R E G I S T E R N O V. 2 8 , 2 0 1 8

• Provides the FHLBanks additional authority to allocate their funds

• Authorizes the FHLBanks to establish separate competitive funds that target specific affordable housing needs in their districts

General

• Provides additional flexibility to design project selection scoring systems

• Aligns certain monitoring requirements with those of other federal funding programs

• Streamlines and reorganizes the regulation

P R O V I S I O N S M U S T B E I M P L E M E N T E D B Y J A N . 1 , 2 0 2 1

• FHLBank must establish a General Fund

• FHLBanks can establish up to three Targeted Funds

• Does not include previously proposed “outcome requirements” –thank you for your comments!!

• Five-year retention agreement eliminated for homeownership transactions involving only rehabilitation (must be implemented by January 1, 2020)

• Final Rule adopts Proposed Rule requirement for “cure first” provision

Competitive AHP

P R O V I S I O N S M U S T B E I M P L E M E N T E D B Y J A N . 1 , 2 0 2 1

Competitive AHP

• Statutory Scoring Priorities:– Donated property (5 points)– Nonprofit sponsorship (5 points)– Home purchase by low-income

household (5 points)• Regulatory Scoring Priorities:

– Targeting to Lower Income Households (20 points)

– Underserved Communities and populations (5 points)

– Creating economic opportunity (5 points)– Community Stability (5 points)

• FHLBank Optional Priorities:– Housing needs identified by FHLBanks

(0 – 50 points)

P R O V I S I O N S M U S T B E I M P L E M E N T E D B Y J A N . 1 , 2 0 2 1

• Maximum grant increased from $15,000 to $22,000 and can adjust upward based on FHFA’s House Price Index

• Five-year retention agreement required for purchase transactions

• Five-year retention agreement eliminated for transactions involving only rehabilitation (must be implemented by January 1, 2020)

• When calculating pro rata repayment, will use “net proceeds” instead of current requirement to use “net gain”

• If required repayment is $2,500 or less, the repayment is forgiven

Homeownership Initiatives (Set-asides)

P L E A S E R E T U R N TO Y O U R S E AT S B Y 1 0 : 4 5

Here are a few questions you can ask to help ‘break the ice’ with your new acquaintance:

1. What brings you to today’s workshop?

2. What are you currently working on that you are the most excited about?

3. What would you be doing right now if you were not at this workshop?

Networking Opportunity

DATE: PRESENTED BY:

Homeownership InitiativesG R A N T P R O G R A M S F O R T H E L I F E -

C Y C L E O F H O M E O W N E R S H I P

March 2019 Rori Chaney, Ronna Edwards

AVA I L A B L E TO A N Y F H L B I M E M B E R

• Down payment and closing cost assistance for eligible first-time homebuyers ($500,000 per member cap)

HOP – Homeownership Opportunities Program

• Owner-occupied rehabilitation for eligible homeowners ($300,000 per member cap)

NIP – Neighborhood Impact Program

• Accessibility modifications and rehabilitation for eligible senior or disabled households ($300,000 per member cap)

AMP – Accessibility Modifications Program

Homeownership Initiatives

T Y P I C A L P R O G R A M T I M E L I N E

Q1 2019Implementation

Plan and program forms

are updated and available for

review

MarchCID Workshops

are held throughout IN

and MI (6 total)

March/AprilProgram

specific training takes place (webinars)

April/MayFunding round typically opens

when HUD announces

income limits

Funding round will close when

all funds are exhausted

Homeownership Initiative Programs

• Members are the gatekeepers of the programs, households can only participate with member assistance

• Understand the requirements of each program• Ensure partnering organizations understand the

program requirements as well• Manage the transaction: Establish a process• Exercise due-diligence in the process

– Worthy situations of the grant funds

Member Role and Responsibilities

C H A N G E S TO T H E I - P L A N

What’s New In 2019?

Changes for Homeownership InitiativesHOP• There is no longer a requirement for matched funds when a non-member

originates the mortgage ($1,000 home-buyer contribution remains)• Return of funds of $2,500 or less are not required on sale or refinance.

NIP• Plumbing is removed as an eligible expense• Electrical now only applies to replacement of knob-and-tube wiring

AMP• Maximum disbursement amount per household is reduced to $12,000• Amount allowed to go toward CAP certified agency for inspection of the

home is reduced to $250

F O R M S

Additional Changes for 2019

Changes for Homeownership Initiatives

NIP and AMP• The Real Estate Retention Agreement is no longer required.

All existing NIP and AMP retention agreements are now null and void and can be removed from the recipient’s property.

• Title Requirements: Titles that include adult children for estate planning purposes

are now allowed Homeowners must have owned and resided in the subject

property for at least 6 months prior to enrollment (previous requirement was 18 months)

W E B I N A R S

• Only NEW users, those members who have not received a disbursement in the previous two years, are required to view the training webinars

• All others are free to view webinars at your leisure. We highly recommend taking advantage of the information provided!

fhlbi.com/training

HOP/NIP/AMP - Training

A P R I L 1 7 – J U N E 2 7

2018 YEAR IN REVIEW

$6.4 Million disbursed, serving 820 households

2018 HOP Profile

245 Total Households Assisted

$1.8M Total Funds Disbursed

$7,670 Average Grant Size

$35,251 Average Household Income

26% Households Considered Very Low Income <50% AMI

468 Total Households Assisted

$3.2M Total Funds Disbursed$6,772 Average Grant Size$23,081 Average Household

Income 57% Households Considered

Very Low Income <50% AMI

2018 NIP Profile

2018 AMP Profile

98 Total Households Assisted

$1.2M Total Funds Disbursed

$12,874 Average Grant Size

$20,169 Average Household Income

58% Households Considered Very Low Income <50% AMI

Why Participate?

Opportunity

MEMBER

O P P O RT U N I T Y

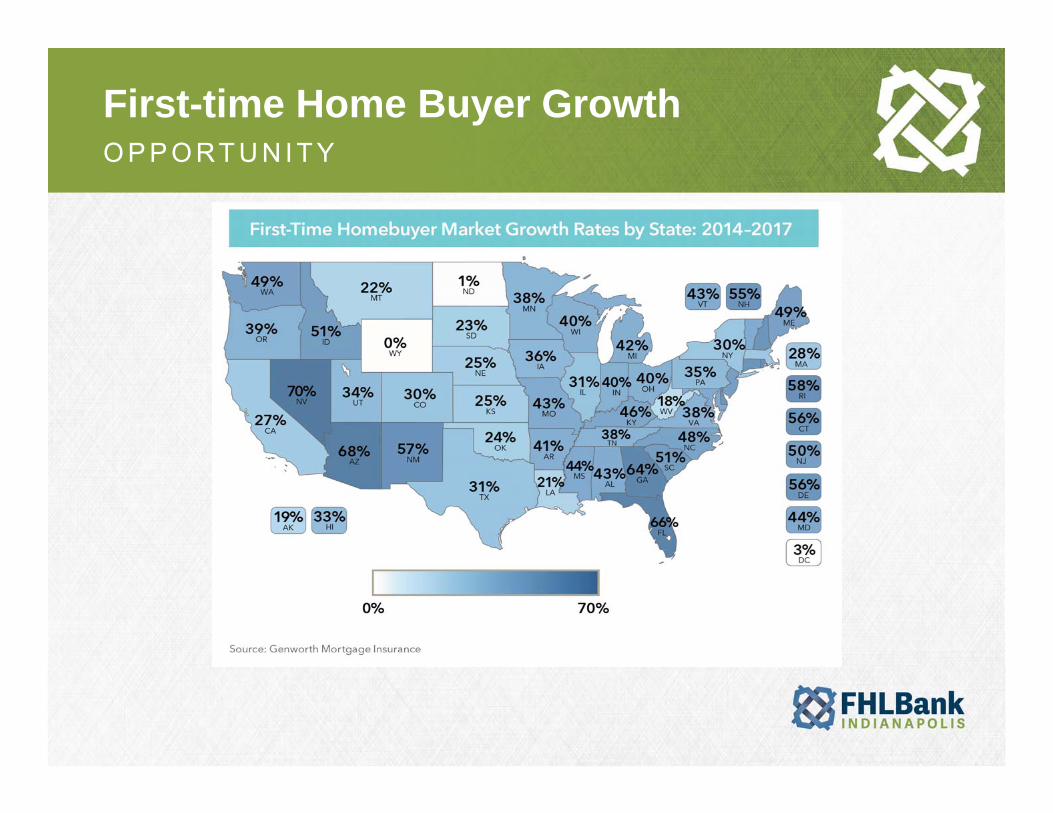

First-time Home Buyer Growth

O P P O RT U N I T Y

• In 2017, 65% of home buyers age 37 and younger, were first-time home buyers

– 24% of those age 38-52 were first-time home buyers.

First-time Home Buyer

S O C I A L R E S P O N S I B I L I T Y

Support & Responsibility

Joint Center for Housing Studies of Harvard University, 2016

Why Participate?

Opportunity Economic Impact

MEMBER

Why Participate?

Opportunity Economic Impact

Social Responsibility

MEMBER

Why Participate?

Opportunity Economic Impact

Social Responsibility Legacy

MEMBER

H O P - D O W N P A Y M E N T A N D C L O S I N G C O S T A S S I S T A N C EF O R F I R S T - T I M E H O M E B U Y E R S

Homeownership Opportunities Program

F I R S T- T I M E H O M E B U Y E R S O N LY

First-time homebuyer(s):• Person(s) who has not had ownership in a principal

residence during a three year period ending on the date of the purchase of the property.

• A single parent who has only owned a home with a spouse while married

• Person(s) who has only owned a principal residence not permanently affixed to a permanent foundation in accordance with applicable regulations.

Who can access HOP funds?

H O P : D O W N PAY M E N T A N D C C A S S I S TA N C E

1) Member Originated First Mortgage• $8,000 in HOP funds

2) Non-member Originated First Mortgage• $4,000 in HOP funds

Homeownership Opportunities Program

M U S T B E O W N E R O C C U P I E D

• Single-Family Detached (1-4 family)• Condominiums• Duplexes• Townhomes• Modular and Manufactured Homes

– All properties must be titled as real estate and be permanently affixed to a permanent foundation

Non-eligible Properties Member REO Properties

Eligible Properties

• Loan origination fees• Doc prep fees• Credit report• Closing fees• Attorney fees• Appraisal fee• Title Insurance• Recording Fees

See Implementation Plan for full list of eligible closing costs

Eligible Closing Costs

• 30 days prepaid interest• Up to 10 months of escrow

– Taxes and/or HO insurance– Flood Insurance

• Final mortgage payment: PITI <35% of gross household income• Minimum $1,000 cash contribution (borrower’s own funds)• Must have 12 months of continuous employment• Homebuyer may not receive more than $250 cash back at closing• Homebuyer counseling required ($150 of HOP funds toward this)• Minimum loan term 5 years• Minimum amortization 15 years• Rehab costs must be paid by 3rd party or outside of closing• No non-arm’s length transactions • No construction-perm transactions• Other assistance funds are allowed (cannot be other FHLBank

grants)

See the Implementation Plan for further details www.fhlbi.com/communitiesandhousing

HOP Requirements

N I P : D E F E R R E D M A I N T E N A N C E R E PA I R S

Neighborhood Impact Program

R E PA I R S F O R O W N E R - O C C U P I E D P R O P E RT I E S

Each homeowner can request up to $7,500 for qualified repairs

Each repair must be supported by at least two independent bids*

Owner-occupants must have resided in the home for at least 6 months prior to enrollment

Must be current on mortgage and taxes

Household income must be ≤80% AMI

Funds can only be used for eligible repairs

NIP Grant Details

W H AT R E PA I R S A R E E L I G I B L E ?

• HVAC repair/replacement• Water heater replacement• Windows• Soffits and Fascia• Siding• Roofing• Gutters and downspouts• Exterior doors

NIP Repairs

• Electrical – replace knob-and-tube wiring

• Weatherization needs– Caulking– Weather stripping– Insulation

A M P : H E L P I N G K E E P FA M I L I E S I N T H E I R H O M E S

Accessibility Modification Program

W H O I S E L I G I B L E

1) Households where all members are age 62 or older

2) Households where all members are age 62 or older and age 17 or younger

3) Households with a member of any age who has a permanent disability (must be receiving disability benefits)

Only households in IN and MI

AMP

P R O G R A M D E TA I L S

• Each household can request up to $12,000 for eligible repairs

• Two independent bids must be obtained*

• If the agency supplying the assessment is also bidding on the project, there needs to be two (2) additional bids: 3 total bids.

• Owner-occupants must have resided in the home for at least 6 months prior to enrollment

Up to 50% of amount requested for AMP eligible repairs can be requested for NIP eligible repairs within the same request– If AMP repairs = $8,000 then can request up to $4,000 for NIP

repairs

AMP

M O D I F I C AT I O N S A N D R E PA I R S

• Ramps or zero step entries• Hand rails• Levered door handles• Widened doorways• Bathroom modifications

– Walk/roll-in showers– Grab bars– ADA approved toilets– Roll under vanity– Lower level ½ bath conversions

AMP

• Installation of smoke detectors

• Universal floor coverings• Relocation of laundry facilities

to the main floor• Internal chair lifts

C I D : 8 0 0 - 6 8 8 - 6 6 9 7

Rori ChaneyCommunity Lending [email protected]

Ronna EdwardsCompliance Analyst [email protected]

Mark StermerCompliance Analyst [email protected]

Anastasia WeinreichCompliance Analyst [email protected]

Contact Information

DATE: PRESENTED BY:

Community InvestmentProgram - CIP

3/6/19 Rori Chaney, AVP, Community Lending Manager

• FHLBI’s lowest-cost funding• Available at FHLBI’s cost of

funds, plus a nominal administrative fee (non-competitive)

• Flexible terms/structure• Variable and fixed rates to 20

years• Up to 30-year amortization

• Same collateral, prepayment terms, and activity-based stock requirements as traditional advances.

Community Investment Program

CIP includes discounted advances and letters of credit, available to members on

an on-going basis to support targeted housing and economic development.

Community Investment Program• Advances: $357.6 Million for 29 projects• Letters of Credit: $12.5 Million for 5 projects

Project Types• Housing: $327.4 Million• Economic Development: $42.7 Million

Highlights of 2018 Program Year

Q U A L I F I C AT I O N

CIP Housing Project

Ownership Residentialo Individual owner-occupied units owned or purchasedo All household incomes ≤ 115% of Area Median

Income (AMI)o REQUIRED Documentation: List of originated

mortgages

Rental Residentialo Financing of rental units and cooperativeso At least 51% of resident incomes ≤ 115% of AMI oro Rents affordable to at least 51% of residents whose

incomes are ≤ 115% AMIo REQUIRED Documentation: Rent roll, FHLBI Rent

Schedule, or Income Roll

CIP can be used to support ownership or rental projects.

Q U A L I F I C AT I O NCIP: Commercial/Economic Development

CIP can be used to support the establishment of small business or projects that

create jobs in communities.

Small Business ConcernSmall Business revenue/size standards (NAICS code)

Job creation/retention at qualified wage levelsAt least 51% of job salaries ≤ 115% AMI for rural At least 51% of job salaries ≤ 100% AMI for urban

I N C O M E R E Q U I R E M E N T SCIP: Commercial Economic Development

≤ 115% AMI for rural areas

Provides services or benefits to urban or rural area

≤ 100% AMI for urban areas

Project located in a targeted area (income exemption)

Rural/urban Champion Community, Empowerment Zone, or Enterprise Community

State of Michigan Renaissance Zone

Native American area

State of Indiana Enterprise Zone

Area affected by a federal military base closing or realignment

Federal Brownfield Tax Credit

Federally declared disaster area

C I P A P P L I C AT I O N S O R Q U E S T I O N S

Rori ChaneyAVP, Community Lending Manager317.465.0428 : [email protected]

Contact Information

DATE: PRESENTED BY:

ELEVATESMALL BUSINESS GRANT

3.2019 Rori Chaney, AVP, Community Lending Manager

P U R P O S E

The Federal Home Loan Bank of Indianapolis created the Elevate grant to help stimulate local economic development, business expansion, workforce development, and job creation through small businesses in the Bank’s district states of Indiana and Michigan.

Elevate Small Business Grant

2 0 1 8 S TAT I S T I C S

Elevate Small Business Grant

• The Bank will target to award $375,000 in Elevate grants in 2019

• Maximum request amount per application is $25,000

• Applicants are limited to one application per year• Members may ‘sponsor’ more than one

applicant/small business

Elevate Small Business Grant

W H O I S E L I G I B L E ?

Elevate was developed to help businesses and communities in the Bank’s district.

Therefore, only small businesses in the states of Indiana and Michigan are eligible who:

• Have been in business for at least 12 months;• Have annual revenue less than $1 Million;• Are a for-profit business; • Provide a complete budget of sources and uses of funds

involved with the qualifying expense.

Elevate Small Business Grant

W H AT C A N I T B E U S E D F O R ?

• Acquisition of real property

• Acquisition of buildings, office space, warehouse space etc.

• Facility expansion• Acquisition of machinery

or equipment

Elevate Small Business Grant

• Workforce development or training

• Business loan closing costs

• Other technology enhancements

The following are the permitted uses of Elevate:

D E C I S I O N S , D E C I S I O N S …

Applications that, in the Bank’s judgment, best meet the objectives of the ELEVATE Grant: To make positive contributions toward:

a) local economic development,b) business expansion,c) workforce development, or d) job creation.

Evaluation Factors:

A P P L I C AT I O N P R O C E S S

• All applications must be submitted by a member institution

• Applications will be made available on the Bank’s website (www.fhlbi.com) by May 1, 2019

• Applications are due to FHLBI no later than July 15, 2019

• Awards will be announced no later than August 16, 2019

Applying for the Grant

C H A R A C T E R I S T I C S O F A S T R O N G A P P L I C AT I O N

Inform:– Let us know who you are and what your business is

about:• When and why did you start this business• Provide your mission/vision statement• Provide a link to your website

– Who is your customer base– What products/services do you provide– What does your past growth look like

• Employees• Revenues

Elevate Small Business Grant

C H A R A C T E R I S T I C S O F A S T R O N G A P P L I C AT I O N

Detail the need:– What is the need or problem to be solved?

• Give details of Who? What? Where? When? Why?• What is the impact:

– Impact on people (employees, customers, community)– Impact on the business– Impact on local economy

– Be clear and realistic• Provide supportive, realistic data

– Don’t give the funder reason to doubt your information

Elevate Small Business Grant

S U B M I T TA L T I P S

• Submit a typed application, not handwritten

• Include photos– Current location– Before and after of what’s already been done– Photos of the equipment/machinery/item to be funded

• Submit the application early!

Elevate Small Business Grant

Q U E S T I O N S ?

Contact an Elevate team member at: [email protected]

Elevate Small Business Grant

DATE: PRESENTED BY:

AUTOMATIONPROJECTS

3.2019 Mark Stermer

G O A L S

Automation Project

Automation Goals

Provide functionality and ease of use to Members

Automate existing paper-burdened processes and accept onlineapplications

Continue to provide services in a manner that meets regulatory expectations

Create operational efficiencies

T I M E L I N E

Automation Project

Current StageIT Development, QA,

User Acceptance Testing

Summer 2019Member Beta Group

2020 CID Workshops

Member Training

2020 RoundSystem is in Production

• Will begin no earlier than July• Need approximately 15 members to

be a Beta group

A N E W TO O L

• What is the Secure Portal?– A tool to send and receive files with FHLBank Indianapolis

• Who should be using the Secure Portal?– Any member or organization partnering with a member on

an AHP funded project that is responsible for sending files to FHLBank

• When do I get to use the Secure Portal?– Projects awarded in 2018 are currently using the Secure

Portal. Throughout 2019, previously awarded projects will be added

AHP Secure Portal

A N E W TO O L

• How do I know when to submit documents on the Secure Portal?– You will be emailed by FHLBank when you should be

using the Secure Portal

AHP Secure Portal

A C C E S S I N G P O RTA L

Secure Portal Access• Login button on fhlbi.com• https://fhlbi.moveitcloud.com• fhlbi.com/secureportal

AHP Secure Portal

R E S O U R C E S

www.fhlbi.com/secureportal– Quick Start Guide– FAQ– Webinar– Forms

AHP Secure Portal

Q U E S T I O N S ?

System Navigation Issues

Contact the Community Investment Department for questions regarding

navigating the system.

800-688-6697

AHP Secure Portal

Account Administration Issues

Contact the FHLBank Indianapolis Service Desk for account issues.

800-442-2568

Questions?

Thank you for joining us!Please complete your survey!!

Closing Comments and Next Steps