2018-2019 park hill school district budget

TRANSCRIPT

43

ORGANIZATIONAL SECTION

The Organizational Section of the school budget document describes the districts organizational and management structure as well as the policies and procedures governing its administrative and financial operations. In many ways, this section describes the district’s mission and how it is achieved.

Eight of 16 students from Plaza Middle School that earned Glory of Missouri awards

from the Missouri House of Representatives.

PARK HILL SCHOOL DISTRICT

7703 NW Barry Road

Kansas City, Missouri 64153

(816) 359-4000

www.parkhill.k12.mo.us

44

This Page Left Intentionally Blank

45

PARK HILL SCHOOL DISTRICT OVERVIEW

INTRODUCTION

The Park Hill School District is a place where students, parents, teachers, administrators, staff, and community

members are Building Successful Futures • Each Student • Every Day!

The Park Hill School District was established under the Statutes of the State of Missouri. The District operates as a

"six director" District (with seven members of the Board of Education) as described in RSMo Chapter 162. Park Hill

School District operates as fiscally independent of the State of Missouri or any other jurisdiction in the county or

local townships in which it operates. The district is a legal corporate body and a political subdivision of the State of

Missouri and may levy and collect taxes within the guidelines and limitations of Missouri state statutes.

The Park Hill School District, formally organized in 1951 under the provisions of Missouri’s School Reorganization

Statute of 1948, encompasses 71 square miles located in the southern third of Platte County, located just north of

downtown Kansas City, Missouri. Park Hill is a public school district, with pre‐kindergarten (pre-K) programs through

grade 12. As of the Spring of 2017, the district includes ten elementary schools, three middle schools (including a

sixth grade center), two high schools, a day treatment

school (Russell Jones Education Center), and the Gerner

Family Early Education Center. Other support facilities

include a district Aquatic Center, Underground Support

Services (leased), and the District Office. Beginning in

2017-2018, the district began the use of a leased office

building to support the LEAD Innovation Studio and

professional studies programs to supplement high school

programming.

The district is planning to open a fourth middle

school, Walden Middle School, and an eleventh

elementary, Hopewell Elementary School, in the

Fall, 2019. The district will open the Support

Services and Transportation facility in October,

2019, and open a permanent facility for LEAD

Innovation Studio in August, 2020.

Predominantly rural‐oriented in the past, Park Hill

has steadily changed to a more suburban district,

blending both residential and commercial growth.

Approximately 43% of the school district lies within

the city limits of Kansas City, Missouri. There are seven other incorporated communities including Riverside,

46

Parkville, Houston Lake, Lake Waukomis, Weatherby Lake, Platte Woods, and Northmoor, as well as the

unincorporated communities of Waldron and Platte County.

The Missouri River forms the southern and western boundaries of the district and also delineates the state line

between Missouri and Kansas. The northern boundary gerrymanders in stair-step fashion from Northwest 76th

Street and the Clay County line to Northwest 120th Street, the northern most point of the district. The northern

boundary divides the Kansas City International Airport, with one of the three airport terminals lying within district

boundaries, and the remaining portions of the airport lying within the Platte County R-3 School District, the

neighboring district to the north.

GENERAL AND DEMOGRAPHIC INFORMATION

COMMERCE

Platte County, Missouri (“Platte County”) is the home of one of the general purpose foreign trade zones in the Kansas

City, Missouri (“Kansas City”) area. A foreign trade zone encourages international commerce by permitting foreign

goods to be held duty-free and quote-free in a specific area. Goods brought into a zone may be stored, manipulated,

mixed with domestic and/or foreign materials, used in the manufacturing process, or exhibited for sale without

paying the duty.

MEDICAL AND HEALTH FACILITIES

There are many general practitioners and specialists who provide medical care in the area served by the District. St.

Luke’s Northland Hospital – Barry Road Campus is located in Platte County. District residents have access to all the

medical and health facilities in metropolitan Kansas City. These include, among others, St. Luke’s Northland Hospital

– Smithville Campus, Liberty Hospital and North Kansas City Hospital, which are located in Clay County, Missouri near

the District.

RECREATIONAL, CULTURAL AND RELIGIOUS FACILITIES

Many recreational facilities are easily accessible to residents of the District, including several lakes, parks and athletic

facilities. District residents have access to all the cultural activities in metropolitan Kansas City. Nearly every major

religious organization is represented in or near the District.

MUNICIPAL SERVICES AND UTILITIES

Various cities within the District provide municipal services to the District. City-owned utilities consist of the water

and sewer systems, except in Parkville, Missouri and Riverside, Missouri where water is provided by Missouri

American Water Company. Electricity is provided by Kansas City Power & Light. Natural gas service is provided by

Kansas Gas Service.

TRANSPORTATION AND COMMUNICATION FACILITIES

Residents have access to all transportation systems serving Kansas City. This includes Amtrak Railroad and the

Kansas City International Airport. A portion of the airport is located within the District. Rail service in Platte County

47

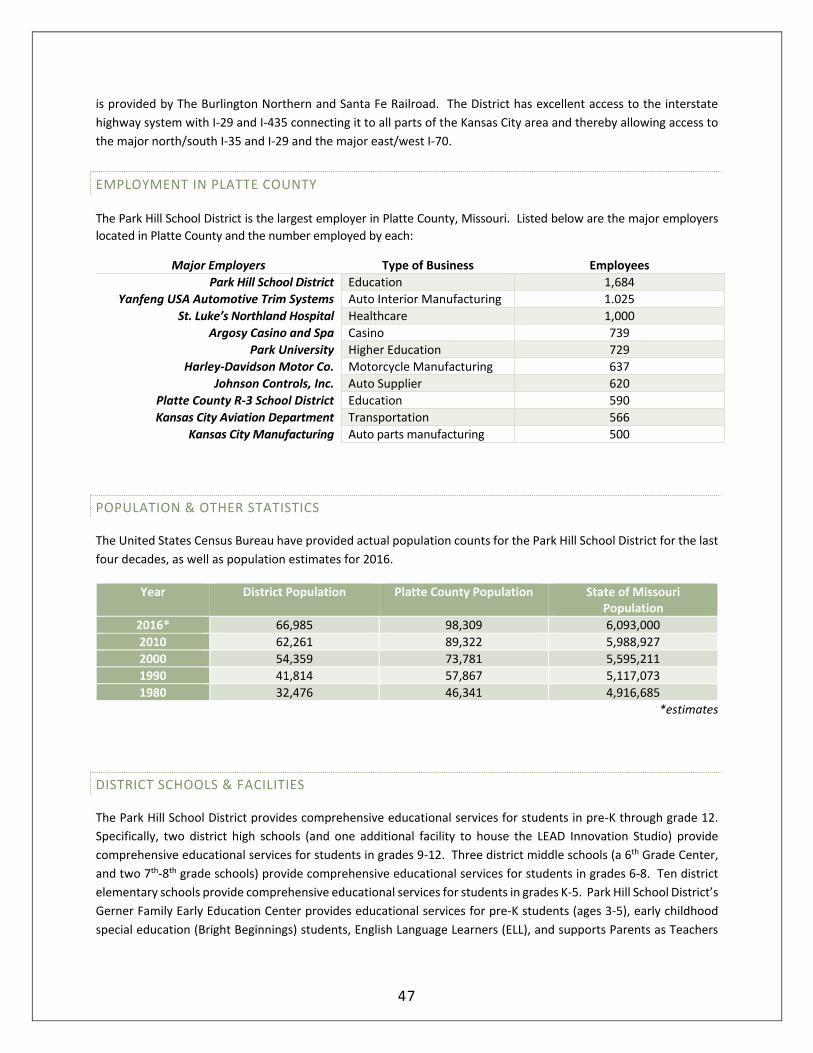

is provided by The Burlington Northern and Santa Fe Railroad. The District has excellent access to the interstate

highway system with I-29 and I-435 connecting it to all parts of the Kansas City area and thereby allowing access to

the major north/south I-35 and I-29 and the major east/west I-70.

EMPLOYMENT IN PLATTE COUNTY

The Park Hill School District is the largest employer in Platte County, Missouri. Listed below are the major employers

located in Platte County and the number employed by each:

Major Employers Type of Business Employees

Park Hill School District Education 1,684

Yanfeng USA Automotive Trim Systems Auto Interior Manufacturing 1.025

St. Luke’s Northland Hospital Healthcare 1,000

Argosy Casino and Spa Casino 739

Park University Higher Education 729

Harley-Davidson Motor Co. Motorcycle Manufacturing 637

Johnson Controls, Inc. Auto Supplier 620

Platte County R-3 School District Education 590

Kansas City Aviation Department Transportation 566

Kansas City Manufacturing Auto parts manufacturing 500

POPULATION & OTHER STATISTICS

The United States Census Bureau have provided actual population counts for the Park Hill School District for the last

four decades, as well as population estimates for 2016.

Year District Population Platte County Population State of Missouri Population

2016* 66,985 98,309 6,093,000

2010 62,261 89,322 5,988,927

2000 54,359 73,781 5,595,211

1990 41,814 57,867 5,117,073

1980 32,476 46,341 4,916,685

*estimates

DISTRICT SCHOOLS & FACILITIES

The Park Hill School District provides comprehensive educational services for students in pre-K through grade 12.

Specifically, two district high schools (and one additional facility to house the LEAD Innovation Studio) provide

comprehensive educational services for students in grades 9-12. Three district middle schools (a 6th Grade Center,

and two 7th-8th grade schools) provide comprehensive educational services for students in grades 6-8. Ten district

elementary schools provide comprehensive educational services for students in grades K-5. Park Hill School District’s

Gerner Family Early Education Center provides educational services for pre-K students (ages 3-5), early childhood

special education (Bright Beginnings) students, English Language Learners (ELL), and supports Parents as Teachers

48

(PAT). The district’s Adventure Club program provides before- and after-school day care services. The Russell Jones

Education Center provides educational services in a day treatment setting for K-12 students with special needs.

The district projects a K-12 enrollment of 11,650 students in 2018-2019, which will make the Park Hill School District

the 16th largest school district in the state of Missouri (522 school districts total).

ELEMENTARY SCHOOLS

Thomas B. Chinn Elementary School Principal, Lee Heinerikson 7100 N. Chatham Road Kansas City, MO 64151 2018-2019 Projected Enrollment (K-5): 476

English Landing Elementary School Principal, Kerry Roe

6500 NW Klamm Drive Kansas City, MO 64151

2018-2019 Projected Enrollment (K-5): 515

Graden Elementary School Principal, Dr. LuAnn Halverstadt 8804 NW 45 Highway Parkville, MO 64152 2018-2019 Projected Enrollment (K-5): 560

Hawthorn Elementary School Principal, Brooke Renton

8200 N. Chariton Kansas City, MO 64152

2018-2019 Projected Enrollment (K-5): 554

49

Line Creek Elementary School Principal, Robin Davis 5801 NW Waukomis Kansas City, MO 64151 2018-2019 Projected Enrollment (K-5): 578

Prairie Point Elementary School Principal, Jay Niceswanger

8101 NW Belvidere Parkway Kansas City, MO 64151

2018-2019 Projected Enrollment (K-5): 460

Alfred E. Renner Elementary School Principal, Dr. Melissa Hensley 7401 NW Barry Road Kansas City, MO 64152 2018-2019 Projected Enrollment (K-5): 446

Southeast Elementary School Principal, Terri Deayon

5701 NW Northwood Kansas City, MO 64151

2018-2019 Projected Enrollment (K-5): 506

Tiffany Ridge Elementary School Principal, Dr. Desiree Rios 5301 NW Old Tiffany Springs Road Kansas City, MO 64154 2018-2019 Projected Enrollment (K-5): 656

Union Chapel Elementary School Principal, Dr. Steven Archer

7100 NW Hampton Road Kansas City, MO 64152

2018-2019 Projected Enrollment (K-5): 520

50

Hopewell Elementary School (Projected Opening Fall, 2019)

Principal, Dr. Melissa Hensley NW 68th Street Kansas City, MO 64151

MIDDLE SCHOOLS

Plaza Middle School (6th Grade Center) Principal, Dr. Tressa Wright 6501 NW 72nd Street Kansas City, MO 64151 2018-2019 Projected Enrollment (6th): 928

Congress Middle School Principal, Dr. Tim Todd

8150 N. Congress Kansas City, MO 64152

2018-2019 Projected Enrollment (7-8): 958

51

Lakeview Middle School Principal, Kirsten Clemons 6720 NW 64th Street Kansas City, MO 64151 2018-2019 Projected Enrollment (7-8): 818

Walden Middle School Projected Opening Fall, 2019

Principal, Keelie Stucker 4701 NW 56th Street

Kansas City, MO 64151

52

HIGH SCHOOLS

Park Hill High School Principal, Dr. Brad Kincheloe 7701 NW Barry Road Kansas City, MO 64153 2018-2019 Projected Enrollment (9-12): 1,866

Park Hill South High School Principal, Dr. Dale Longenecker

4500 NW River Park Drive Kansas City, MO 64150

2018-2019 Projected Enrollment (9-12): 1,512

LEAD Innovation Studio Principal, Dr. Ryan Stanley 10150 N. Ambassador Drive Kansas City, MO 64153 2018-2019 Projected Enrollment (9-12): 296

53

OTHER SCHOOLS AND FACILITIES

Russell Jones Education Center Principal, Dr. Tara Kalis 7642 N. Green Hills Road Kansas City, MO 64151 2018-2019 Projected Enrollment (K-12): 46

Gerner Family Early Education Center Principal, Rachel Ward

8100 N. Congress Kansas City, MO 64151

2018-2019 Projected Enrollment (Pre-K): 450

District Central Office 7703 NW Barry Road Kansas City, MO 64153

Community Services 7703 NW Barry Road

Kansas City, MO 64153

Support Services 8500 NW River Park Drive, Pillar 116 Parkville, MO 64152

Aquatic Center 8152 N. Congress

Kansas City, MO 64152

54

PARK HILL STUDENT ENROLLMENT

The Missouri Department of Elementary and Secondary Education has established the annual official enrollment

count as the number of students in grades K-12 enrolled on the last Wednesday in September of each year. The

enrollment information throughout the budget document uses this value to represent annual enrollment.

HISTORICAL ENROLLMENT GROWTH (GRAPH)

The following graph depicts the 25-year enrollment history of the Park Hill School District. The district has seen

steady enrollment growth over three decades, at a rate of about 1.0% annually. The 2017-2018 enrollment for the

district was 11,458 students which was 1.5% growth from the prior year. The district also hosts pre-school programs

with additional 452 students.

-

2,000

4,000

6,000

8,000

10,000

12,000

K-1

2 E

nro

llmen

t

55

GOVERNANCE STRUCTURE

PARK HILL BOARD OF EDUCATION

The District is a reorganized school district formed pursuant to Chapter 162 of the Revised Statutes of Missouri, as

amended (“RSMo”). Park Hill School District operates as fiscally independent of the State of Missouri or any other

jurisdiction in the county or local townships in which it operates. The district is a legal corporate body and a political

subdivision of the State of Missouri and may levy and collect taxes within the guidelines and limitations of Missouri

state statutes.

The District is governed by a seven-member Board of Education. The members of the Board are elected by the

voters of the District for three year staggered terms. All Board members are elected at large and serve without

compensation. The Board is responsible for all policy decisions. The President of the Board is elected by the Board

from among its members for a term of one year and has no regular administrative duties. The Secretary and

Treasurer are appointed by the Board and may or may not be members of the Board.

A listing of the current Board of Education follows, photographs are available on page 13:

President, Bart Klein Vice President, Susan Newburger

Treasurer, Kimberlee Ried Member, Janice Bolin Member, Todd Fane

Member, Scott Monsees Member, Kyla Yamada

Superintendent of Schools, Dr. Jeanette Cowherd

Secretary to the Board, Opal Hibbs

56

ADMINISTRATIVE STAFF

The Board of Education appoints the Superintendent of Schools who is the chief administrative officer of the District

responsible for carrying out the policies set by the Board. Additional members of the administrative staff are

appointed by the Board of Education upon recommendation by the Superintendent.

The organizational structure for the district operations effective July 1, 2018 appears below. This organizational

chart lists the district level administrative staff by position and title.

Park Hill School DistrictBoard of Education

Superintendent of Schools

Dr. Jeanette Cowherd

Secretary to the Superintendent & Board of

Education Ms. Opal Hibbs

Assistant Superintendent for Business &

Technology Dr. Paul Kelly

Assistant Superintendent for Human Resources

Dr. Bill Redinger

Assistant Superintendent for Academic Services

Dr. Jeff Klein

Executive Director of Quality & Evaluation

Dr. Mike Kimbrel

Director of CommunicationsMs. Nicole Kirby

Director of Student ServicesDr. Josh Colvin

Director of Special Services

Dr. Chris Daniels

Director Elementary Education

Dr. Jasmine Briedwell

Director of Secondary Education

Dr. Jamie Dial

Director of Food Services

Ms. Ronda McCullick

Director of Technology

Mr. Derrick Unruh

Director of OperationsMr. Jim Rich

Director of Human Resources

Dr. Linda Kaiser

Director of Instructional Technology

Dr. Susan Rizzo

Director of Safety & Safety

Mr. Chad Phillips

57

MISSION AND GOALS OF THE ORGANIZATION

MISSION, VISION AND VALUES

Park Hill School District’s culture of high expectations and continuous improvement is guided by the tenets of a

professional learning community with a shared vision, mission, and values. The district focuses upon identified

strategic focus areas and articulated goals within a five-year strategic plan that are aligned with student and

stakeholder requirements/expectations. Staff members utilize collective inquiry, collaborative teams, and an action

orientation to accomplish the goals of the district.

The Board of Education and senior leaders have defined the vision, mission, and values of the school district.

The vision of the district is:

Building Successful Futures • Each Student • Every Day

The mission is:

Through the expertise of an engaged staff, the Park Hill School District provides a relevant education in a safe,

caring environment to prepare each student for success in life.

The values of the district have been identified as:

Student Focus Integrity

High Expectations Continuous Improvement

Visionary Leadership Equity

The Missouri Department of Elementary and Secondary Education (DESE) requires a five-year strategic plan for each

public school district in Missouri. These plans are called Comprehensive School Improvement Plans (CSIP). The

current five-year plan was adopted by the Board of Education in Spring, 2018 with goals/objectives/actions to take

place through the 2022-2023 school year. The goals of the 2018-2023 CSIP are monitored bi-annually by the Board

of Education with revisions occurring as a result of input from the CSIP team based upon results or progress toward

goals.

The 2018-2023 CSIP (strategic planning) process included a review of the current vision, mission, values and strategic

perspectives of the Park Hill School District; a review of stakeholders needs and expectations; an evaluation of

current performance; an examination of environmental shifts; and SWOT (Strengths, Weaknesses, Opportunities

and Threats) analysis; the articulation of strategic focus area goals and objectives; and the completion of district

action plans to achieve the goals and objectives.

58

STRATEGIC PERSPECTIVES

During the 2016-2017 academic year, the Park Hill School District administered the Key Requirements Survey to

Parents, Students, and Stakeholders. Survey participants were asked about a variety of items and how critical they

were for the school to provide. Participants could respond whether they thought the item was critical, very

important, important or nice to have. Respondents were then asked to prioritize and choose their first choice, second

choice, and third choice in order of importance.

The Board of Education also participated in a similar process to identify key requirements they felt were important

for the district to consider and include in the Comprehensive School Improvement Plan.

Additionally, feedback from school personnel, the Platte County Economic Development Council, and the National

Association for College Admissions Counseling and the Regional Workforce Intelligence Network of Greater Kansas

City survey results of soft skills and workplace competencies were used to identify key student and stakeholder

needs. Following the identification of key student and stakeholder needs, the Superintendent’s cabinet articulated

key performance indicators.

The Park Hill School District Balanced Scorecard tracks key performance indicators and associated measures in the

following Strategic Perspectives:

Group Key Requirements (STRATEGIC PERSPECTIVE)

Students (customer) Provide a Safe Environment Readiness

Respectful Environment

Caring Environment

Parents (customer) Safe and Orderly Environment Well Qualified Teachers Caring Environment

Readiness

Stakeholders Well Qualified Teachers Safe and Orderly Environment Caring Environment

Financial Responsibility and Integrity

Following the identification of organizationally-wide goal areas, teams identified a variety of activities that could be

utilized to accomplish the objectives. An effort/benefit matrix and other forced choice ranking processes were used

to prioritize each activity based upon the benefit provided and the effort (people, time, and money) needed to

accomplish the activity. This process of prioritization enhances the district’s long-term organizational stability and

ability to execute the strategic plan.

STRATEGIC ADVANTAGES

Strong Financial Condition

Continuous Improvement

Culture High Expectations

Academic Performance

59

Well-Qualified Staff

Engaged Staff

Rigorous Curriculum

Community Support

In previous versions of the CSIP, Strategic Focus Areas were determined (Financial – Academic – Climate – Employee)

with goals and objectives for each. Using our SWOT analysis, Strategic Advantages, and Strategic Challenges, the

team moved to a more integrated model. Thus, all Strategic Perspectives are working on the same organizationally-

wide goals. Further, this was built upon the integration of our Vision statement: Building Successful Futures ∙ Each

Student ∙ Every Day.

ACTION PLANS

Each district action plan includes the following element:

• Park Hill CSIP Goal: organizational-wide goal.

• Objective: a measurable indicator of progress (Specific, Measureable, Attainable, Realistic, and

Timely).

• Annual Targets: benchmarks used to gauge annual progress.

• Description of Strategy: a succinct description of why the proposed actions/activities are relevant.

• Completion Date: the date the action/activity will be completed.

• Description of Action/Activity (Long- and Short-Term): a succinct statement of an action/activity used

to enhance the identified objective.

MAJOR GOALS AND OBJECTIVES

Goals of the 2018-2023 CSIP have been identified as:

COLLEGE, CAREER, and LIFE READINESS: All students will graduate college, career, and life-ready.

ACCESS and OPPORTUNITY: Ensure success for ALL students regardless of background.

KEYS TO EXCELLENCE: Park Hill School District will leverage its Keys to Excellence for sustainability into

the future.

Objectives, annual targets, description of strategies, completion dates and descriptions of action and activities are

detailed within the CSIP posted and updated on the district’s website at https://www.parkhill.k12.mo.us/.

60

FINANCIAL GOALS AND OBJECTIVES

The 2018-2023 CSIP includes the following financial and resource strategies that directly support the organizational-

wide goals of the district. The financial strategies are highlighted in yellow. Other non-financial strategies have not

been detailed in this list which causes the numbering of the strategies to appear incomplete.

1.0. GOAL. Each student will graduate college, career, and life-ready.

1.1. OBJECTIVE. 80% of Park Hill students will meet readiness benchmark as measured by the CCR Index.

1.1.6. ORGANIZATIONAL STRATEGY. Ensure adequate resources and evaluate cost/ROI to assure

students are college, career, and life ready.

1.2. OBJECTIVE. Park Hill students will meet SEL benchmark as measured by the SEL Index.

1.2.4. ORGANIZATIONAL STRATEGY. Ensure adequate resources and evaluate cost/ROI to assure

students have afforded mental health supports to promote college, career, and life readiness.

1.3. OBJECTIVE. 80% of Park Hill students will be proficient or advanced on the 21st Century Skills

Assessment.

1.3.6. ORGANIZATIONAL STRATEGY. Ensure adequate resources and evaluate cost/ROI to assure

students are afforded 21st Century/Professional skills to promote college, career, and life

readiness.

2.0. GOAL. Ensure success for ALL students regardless of background.

2.1. OBJECTIVE. Decrease the Access and Opportunity Gap as measured by the Access and Opportunity

Index.

1.2.4. ORGANIZATIONAL STRATEGY. Ensure adequate resources and evaluate cost/ROI to assure

students in every demographic group have access and opportunity.

2.2. OBJECTIVE. Decrease the CCR Index gap between student demographic groups to 15%.

2.2.8. ORGANIZATIONAL STRATEGY. Ensure adequate resources and evaluate cost/ROI to assure

students in every demographic group are college, career, and life ready.

3.0 GOAL. Park Hill School District will leverage its Keys to Excellence for sustainability into the future

3.4. OBEJCTIVE. Strategic resource allocation.

3.4.1. ORGANIZATIONAL STRATEGY. Facility planning through deployment of the Long-Range

Facility Plan and annual Capital Improvement Plan.

Further detail of the Long-Range Facility Plan can be found on page 149 of the budget document. The Capital

Improvement Plan is detailed on page 145 of this budget document.

61

The district’s Comprehensive School Improvement Plan and the goals, objectives and activities within it serve as the

foundation for the financial budget document. As evidenced within the district’s values and goals, the Park Hill

School District has created an expectation of continuous improvement throughout the organization; improvement

is expected from individual students, classrooms, schools, programs/departments and the district as a whole via a

comprehensive evaluation and improvement planning process. Funds are included to support the work necessary to

review and enhance school and program improvement plans, for school-site allocations as well as professional

development needs.

FIDUCIARY AND BUDGETARY GOALS

The Financial Focus Area Collaborative Team (FACT) has developed a scorecard, District Financial Scorecard (DFS), to

track twelve key financial measures outlined in the CSIP on a bi-annual basis. The DFS is a management tool to guide

the actions of the FACT toward the targets established by the Board of Education and FACT team representatives.

A snapshot of the DFS appears on the following page with quantitate scores and targets assigned to 12 criteria.

62

63

GOAL COSTS

The deployment of the 2018-2023 CSIP begins in July, 2018. The financial strategies (as listed on page 60) emphasize

collaboration with the district team to evaluate costs and Return on Investment (ROI) for the strategies to support

the objectives and goals within the CSIP. Hence, an accounting has not been conducted for the current strategies as

this work will begin with the deployment of the strategies during the 2018-2019 school year.

The process the district will use is similar to the current process in which goal area leaders propose plans that support

the CSIP goals in the Fall of each school year including proposing new or shifted costs. The Financial Area

Collaborative Team (FACT) will conduct an analysis of proposal and report back on the feasibility of the strategy to

support in future year budgets with a focus on sustainability. These proposals are integrated into “Budget

Assumptions” in the winter of each school year and are presented to the Board of Education as a road-map for the

development of the next fiscal year’s budget.

Through the Spring of each year, budget assumptions become integrated into the financial and staffing plans and

are detailed within the district’s budget system. This budget is presented to the Board of Education periodically

through the Spring to ensure Board support of the district’s direction and match with the mission of the school

district. The Board is asked to officially approve the next fiscal year’s budget at the last public Board meeting in June

of each year.

DISTRICT OPERATING EXPENDITURES BY FUNCTION

In lieu of goal costs that are to be developed during the 2018-2019 school year, below depicts the district budgeted

operating expenditures by function and the percentage of these expenditures relative to the overall operating

expenditure budget. A function describes the activity for which a service or material object is acquired.

District Function 2018-2019 % of Operating

Expenditures

1000-Instruction 83,295,171 50.8%

1100-Regular Programs 57,920,388 35.3%

1200-Special Programs 20,227,181 12.3%

1300-Career Education Programs 107,078 0.1%

1400-Student Activities 3,814,778 2.3%

1900-Payments to Other Districts 1,225,746 0.7% 2000-Support Services 76,108,015 46.4%

2100-Support Services - Pupils 5,785,415 3.5%

2200-Support Services - Instructional Staff 12,553,593 7.7%

2300-Support Services - General Administration 6,918,000 4.2%

2400-Support Services - School Administration 8,218,006 5.0%

2500-Support Services - Business 39,658,192 24.2%

2600-Support Services - Central Office 2,974,809 1.8% 3000-Community Services 4,524,117 2.8%

3100-Community Services 2,410,880 1.5%

64

District Function 2018-2019 % of Operating

Expenditures

3200-Community Recreation Services 278,824 0.2%

3500-Early Childhood Program 1,738,141 1.1%

3700-Non-Public School Pupils’ Services 13,756 0.0%

3800-Custody and Care of Children Services 55,679 0.0%

3900-Other Community Services 26,837 0.0% 4000-Facilities Acquisition and Construction Services 100,000 0.1%

4000-Facilities Acquisition and Construction Services 100,000 0.1%

Grand Total 164,027,303

65

SIGNIFICANT BUDGET AND FINANCIAL COMPONENTS

BUDGET POLICIES AND PROCEDURES

The Park Hill School District Board of Education has adopted the policies that govern the financial management of

the school district. These policies are modeled after the Missouri School Board Association's policy manual and are

reviewed and edited by the district policy committee prior to review by the Board of Education. Each policy and

corresponding regulations and forms can be viewed by the public by accessing the district web site at

https://www.parkhill.k12.mo.us/district_information/district_policy .

Code Policy Title

DA Fiscal Responsibility

DB Annual Budget

DBB Fiscal Year

DC Taxing and Borrowing Authority-Limitations

DCB Political Campaigns

DD Grants

DEA Revenues from Tax Sources

DFA Revenues from Investments-Use of Surplus Funds

DG Depository of Funds

DGA Authorized Signatures

DH Bonded Employees and Officers

DI Fiscal Accounting and Reporting-Accounting System

DIE Audits

DJB Petty Cash Accounts

DJF Purchasing

DJFA Federal Programs and Projects

DK Payment Process

DLB Salary Deductions

DLC Expense Reimbursements

DLCA Travel Expenses

DN Surplus District Property

Policies are updated by the district policy committee and Board of Education on a regular basis. Specific budget

policies are provided below – any changes and corresponding regulations can be accessed via the school district

website at https://www.parkhill.k12.mo.us/district_information/district_policy .

BOARD POLICY DB – ANNUAL BUDGET

One of the primary responsibilities of the Park Hill Board of Education is to secure adequate funds to conduct a

quality program of education in the school district. The annual school budget represents a written document

presenting the Board's plan for allocation of the available financial resources into an explicit expenditure plan to

sustain and improve the educational function of the school district. It is a legal document describing the programs

to be conducted during the fiscal year and is the basis for the establishment of tax rates for the district.

66

The planning and preparation of the budget is a continuing process. It must involve a number of people who have

knowledge of the educational needs of the community and who can provide accurate data in regard to the financial

potential of the district. Members of the Board, citizens, students, and professional and support staff members

should be involved in the planning process, which culminates in the preparation of the budget document. The

Superintendent will establish procedures which seek input from the appropriate people on budgetary needs and

who consider the priorities established by the Board.

The Board designates the Superintendent to serve as the budget officer of the district. As budget officer, the

Superintendent will direct the planning and preparation of the budget and will submit it to the Board for approval.

The Superintendent will present to the Board a tentative budget proposal for the following year and will present the

final budget proposal before the new fiscal year begins, as provided by law.

The Board may revise the items contained therein and will, at that meeting, adopt the portion of the budget dealing

with the salary schedule and the needed tax rate for the district. Should the adopted budget require an increase in

the tax levy above the authorized level that the Board may levy, the tax levy increase shall be presented to the voters

for approval. The budget shall be appropriately adjusted if the voters fail to pass the tax levy increase. The Board

will conduct at least one (1) public hearing regarding the proposed budget and taxation rate. 2 The annual budget

document shall present a completed financial plan for the ensuing fiscal year and shall include at least the following

statutory requirements:

• A budget message describing the important features of the budget and major changes from the

preceding year.

• Estimated revenues to be received from all sources for the fiscal year, with a comparative statement

of actual or estimated revenues for the two (2) years next preceding, itemized by year, fund and source.

• Proposed expenditures for each department, office and other classification for the fiscal year, with a

comparative statement of actual or estimated expenditures for the two (2) years preceding, itemized

by year, fund, activity and object.

• The amount required for the payment of interest, amortization and redemption charges on the debt

of the school district.

• A general budget summary.

In no event shall the total proposed expenditures from any fund exceed the estimated revenues to be received plus

any unencumbered balance or less any deficit estimated for the beginning of the fiscal year. Upon the

recommendation of the superintendent, the Board will approve a system of internal accounting to ensure proper

financial accounting of revenues and expenditures.

The adopted budget of the Park Hill School District serves as the control to direct and limit expenditures in the

district. Overall responsibility for assuring control rests with the Superintendent, who will establish procedures for

budget control and reporting throughout the district.

The total amounts that may be expended during the fiscal year for the operation of the school district are set forth

in the budget. The total budgeted expenditure for each program is the maximum amount that may be expended for

67

that classification of expenditures during the school year unless a budget transfer is recommended by the

superintendent and is approved by the Board.

The Board will review the financial condition of the district monthly and shall require the Superintendent to prepare

a monthly reconciliation statement. This statement will show the amount expended during the month, total (to date)

for the fiscal year, receipts and remaining balances in each fund. This statement will be used as a guide for projected

purchasing and as a guide for budget transfers.

During the fiscal year, the Superintendent or his/her designee may transfer any unencumbered balance or portion

thereof from the expenditure authorization of one (1) account to another, subject to limitations provided by state

laws and approval by the Board. 3

All moneys received by the school district shall be disbursed only for the purposes for which they are levied, collected

or received.

BOARD POLICY DBB – FISCAL YEAR

The fiscal year is defined as beginning annually on the first day of July and ending on the thirtieth day of June

following.

The district treasurer shall not draw any check or issue any order for payment that is in excess of the income and

unencumbered revenue of the school district for the fiscal year beginning on the first day of July and ending on the

thirtieth day of June following.

BOARD POLICY DI – FISCAL ACCOUNTING AND REPORTING/ACCOUNTING SYSTEM

The Park Hill School District's accounting system shall conform to requirements established by state statutes,

regulations of the Missouri Department of Elementary and Secondary Education (DESE), the current version of the

Missouri Financial Accounting Manual, and statements issued by the Governmental Accounting Standards Board

(GASB).

The Superintendent or his/her designee shall be responsible for receiving and properly accounting for all funds of

the school district and implementing the accounting system. As specified in state law, the Park Hill Board of

Education shall establish funds for the accounting of all school moneys in the district. The treasurer of the district

shall open an account for each fund, and all monies received by the district shall be deposited in the appropriate

fund account. All financial transactions shall be recorded in the revenue and expenditure records, and appropriate

entries from the adopted budget shall be made in the records for the respective funds.

The Board shall receive monthly financial statements from the Superintendent or his/her designee showing the

financial condition of the district. In addition, other financial statements determined necessary by either the Board

or the Superintendent or his/her designee shall be presented to the Board for review. The superintendent or his/her

designee shall also be responsible for pupil-related accounting and shall file enrollment, attendance, Nutrition

Services and transportation reports as required by DESE.

68

REGULATIONS THAT GOVERN THE BUDGET PROCESS

STATE AID

The amount of State Aid for school districts in Missouri has typically been calculated using a complex formula. The

impact of Senate Bill (SB) 287 in 2006 was to transition the state away from a local-tax-rate-based formula to a

formula that is primarily student-needs-based. The formula was phased in over a seven-year period, which began

in the 2006-2007 fiscal year and ended with the 2012-2013 school year. Since the 2013-2014 school year, State Aid

has been calculated solely using the student-needs-based formula.

PROPERTY TAX LEVY REQUIREMENTS

The sum of a district’s local property tax levies in its Incidental and Teachers’ Funds must be at least $2.75 per $100

assessed valuation in order for the district to receive increases in State Aid above the level of State Aid it received in

the 2005-2006 fiscal year. Levy reductions required as a result of a “Hancock rollback” will not affect a district’s

eligibility for State Aid increases.

THE FORMULA

A district’s State Aid is determined by first multiplying the district’s weighted average daily attendance (“Weighted

ADA”) by the state adequacy target (“State Adequacy Target”). This figure may be adjusted upward by a dollar value

modifier (“DVM”). The product of the Weighted ADA multiplied by the State Adequacy Target multiplied by the

DVM is then reduced by a district’s local effort (“Local Effort”) to calculate a district’s final State Aid amount. The

State Aid amount is distributed to the districts on a monthly basis.

WEIGHTED ADA

Weighted ADA is based upon regular term ADA plus summer school ADA, with additional weight assigned in certain

circumstances for students who qualify for free and reduced price lunch (“FRL”), receive special education services

(“IEP”), or possess limited English language proficiency (“LEP”). These FRL, IEP and LEP students are weighted to the

extent they exceed certain thresholds (based on the percentage of students in each of the categories in certain high

performing districts (“Performance Districts”)), which thresholds can change every two years. For fiscal years 2017

and 2018, DESE has revised the thresholds downward as required under SB 586, which modified the definition of

State Adequacy Target to require that a future recalculation of the State Adequacy Target never result in a decrease

from the State Adequacy Target as calculated for fiscal years 2017 and 2018. This lowering of the thresholds means

more FRL, IEP and LEP students will be included in Weighted ADA. The District’s State Aid revenues would be

adversely affected by decreases in its Weighted ADA resulting from decreased enrollment generally and, specifically,

decreased enrollment of FRL, IEP and LEP students.

69

STATE ADEQUACY TARGET

The State Aid formula requires DESE to calculate a “State Adequacy Target,” which is intended to be the minimum

amount of funds a school district needs in order to educate each student. DESE’s calculation of the State Adequacy

Target is based upon amounts spent, excluding federal and state transportation revenues, by Performance Districts.

Every two years, using the most current list of Performance Districts, DESE will recalculate the State Adequacy Target.

The recalculation can never result in a decrease from the State Adequacy Target as calculated for fiscal years 2017

and 2018 and any State Adequacy Target figure calculated subsequent to fiscal year 2018. For fiscal years 2017 and

2018, the State Adequacy Target is $6,241 per pupil. For fiscal year 2017, the State Adequacy Target was at an

adjusted level because education funding was not fully funded.

For fiscal year 2019, the foundation formula is expected to be fully funded with a SAT of $6308, but the Governor

still has the ability to withhold money throughout the year.

DOLLAR VALUE MODIFIER

The DVM is an index of the relative purchasing power of a dollar in different areas of the state. The DVM is calculated

as one plus 15% of the difference of the regional wage ratio (the ratio of the regional wage per job divided by the

state median wage per job) minus one. The law provides that the DVM can never be less than 1.000. DESE revises

the DVM for each district on an annual basis.

The DVM for the District for 2015-2016 and 2016-2017 was 1.080 and 1.084, respectively. The DVM for the District

for 2017-2018 was 1.081 and is budgeted to increase to 1.084 in 2018-2019.

LOCAL EFFORT

For the 2006-2007 fiscal year, the Local Effort figure utilized in a district’s State Aid calculation was the amount of

locally generated revenue that the district would have received in the 2004-2005 fiscal year if its operating levy was

set at $3.43. The $3.43 amount is called the “performance levy.” For all years subsequent to the 2006-2007 fiscal

year, a district’s Local Effort amount has been frozen at the 2006-2007 amount, except for adjustments due to

increased locally collected fines or decreased assessed valuation in the district. Growth in assessed valuation and

operating levy increases will result in additional local revenue to the district, without affecting state aid payments.

CATEGORICAL-SOURCE ADD-ONS

In addition to State Aid distributed pursuant to the formula as described above, the formula provides for the

distribution of certain categorical sources of State Aid to school districts. These include (1) 75% of allowable

transportation costs, (2) the vocational education entitlement and (3) educational and screening program

entitlements.

70

CLASSROOM TRUST FUND (GAMBLING REVENUE) DISTRIBUTION

A portion of the state aid received under the formula will be in the form of a distribution from the “Classroom Trust

Fund,” a fund in the state treasury containing a portion of the state’s gambling revenues. This money is distributed

to school districts on the basis of ADA (versus Weighted ADA, which applies to the basic formula distribution). The

funds deposited into the Classroom Trust Fund are not earmarked for a particular fund or expense and may be spent

at the discretion of the local school district except that, beginning with the 2010-11 fiscal year, all proceeds of the

Classroom Trust Fund in excess of amounts received in the 2009-10 fiscal year must be placed in the Teachers’ or

Incidental Funds.

For the 2017-2018 fiscal year, each school district received approximately $404 per pupil based on their 2016-2017

ADA. The $404 per ADA value has been budgeted for the 2018-2019 school year. Classroom Trust Fund dollars do

not increase the amount of State Aid.

MANDATORY DEPOSIT AND EXPENDITURES OF CERTAIN AMOUNTS IN THE TEACHERS’ FUND

The following state and local revenues must be deposited in the Teachers’ Fund: (1) 75% of basic formula State Aid,

excluding State Aid distributed from the Classroom Trust Fund (gambling revenues); (2) 75% of one-half of the

district’s local share of Proposition C revenues; (3) 100% of the career ladder state matching payments; and (4) 100%

of local revenue from fines and escheats based on violations or abandoned property within the district’s boundaries.

In addition to these mandatory deposits, school districts are also required to spend for certificated staff

compensation and tuition expenditures each year the amounts described in clauses (1) and (2) of the preceding

paragraph. Since the 2007-2008 fiscal year, school districts are further required to spend for certificated staff

compensation and tuition expenditures each year, per the second preceding year’s Weighted ADA, as much as was

spent in the previous year from local and county tax revenues deposited in the Teachers’ Fund, plus the amount of

any transfers from the Incidental Fund to the Teachers’ Fund that are calculated to be local and county tax sources.

This amount is to be determined by dividing local and county tax sources in the Incidental Fund by total revenue in

the Incidental Fund. Commencing with the 2006-2007 fiscal year, the formula provides that certificated staff

compensation now includes the costs of public school retirement and Medicare for those staff members. These

items were previously paid from the Incidental Fund.

Failure to satisfy the deposit and expenditure requirements applicable to the Teachers’ Fund will result in a

deduction of the amount of the expenditure shortfall from a district’s basic formula State Aid for the following year,

unless the district receives an exemption from the State Board of Education.

A school board may transfer any portion of the unrestricted balance remaining in the Incidental Fund to the

Teachers’ Fund. Any district that uses a transfer from the Incidental Fund to pay for more than 25% of the annual

certificated compensation obligation of the district, and has an Incidental Fund balance on June 30 in any year in

excess of 50% of the combined Incidental and Teachers’ Fund expenditures for the fiscal year just ended, will be

required to transfer the excess from the Incidental Fund to the Teachers’ Fund.

71

LIMITED SOURCES OF FUNDS FOR CAPITAL EXPENDITURES

School districts may only pay for capital outlays from the Capital Projects Fund. Sources of revenues in the Capital

Projects Fund are limited to: (i) proceeds of general obligation bonds such as the Bonds (which are repaid from a

Debt Service Fund levy) and lease financings; (ii) revenue from the school district’s local property tax levy for the

Capital Projects Fund; (iii) certain permitted transfers from the Incidental Fund; and (iv) a portion of the funds

distributed to school districts from the Classroom Trust Fund.

CAPITAL PROJECTS FUND LEVY

Prior to setting tax rates for the Teachers’ and Incidental Funds, each school district must annually set the tax rate

for the Capital Projects Fund as necessary to meet the expenditures of the Capital Projects Fund for capital outlays,

except that the tax rate set for the Capital Projects Fund may not be in an amount that would result in the reduction

of the equalized combined tax rates for the Teachers’ and Incidental Funds to an amount below $2.75.

The District’s Capital Projects Fund levy for 2017-2018 was $0.1800 per $100 of assessed valuation and is expected

to remain at this value for 2018-2019.

TRANSFERS FROM THE INCIDENTAL FUND TO THE CAPITAL PROJECTS FUND

In addition to money generated from the Capital Projects Fund levy, each school district may transfer money from

the Incidental Fund to the Capital Projects Fund for certain purposes, including: (1) the amount to be expended for

transportation equipment that is considered an allowable cost under the state board of education rules for

transportation reimbursements during the current year; (2) the amount necessary to satisfy obligations of the Capital

Projects Fund for state-approved area vocational-technical schools; (3) current year obligations for lease-purchase

obligations entered into prior to January 1, 1997; (4) the amount necessary to repay costs of one or more guaranteed

energy savings performance contracts to renovate buildings in the school district, provided that the contract

specified that no payment or total of payments shall be required from the school district until at least an equal total

amount of energy and energy-related operating savings and payments from the vendor pursuant to the contract

have been realized; and (5) to satisfy current year capital project expenditures, an amount not to exceed the greater

of (a) $162,326 or (b) seven percent (7%) of the State Adequacy Target.

The District transferred $4,567,800 from the Incidental Fund to the Capital Projects Fund under this provision during

the 2016-2017 fiscal year and $4,500,000 is estimated at the conclusion of the 2017-2018 fiscal year. The 2018-2019

budget reflects a $3,000,000 transfer.

72

TRANSFERS FROM INCIDENTAL FUND TO DEBT SERVICE FUND AND/OR CAPITAL PROJECTS

FUND

If a school district is not using the seven percent (7%) or the $162,326 transfer discussed in parts (5)(a) and (5)(b) of

the prior paragraph and is not making payments on lease purchases pursuant to Section 177.088, RSMo, then the

school district may transfer from the Incidental Fund to the Debt Service and/or the Capital Projects Fund the greater

of (1) the State Aid received in the 2005-2006 school year as a result of no more than eighteen (18) cents of the sum

of the Debt Service Fund levy and Capital Projects Fund levy used in the foundation formula and placed in the Capital

Projects Fund or Debt Service Fund, or (2) Five percent (5%) of the State Adequacy Target times the district’s

Weighted ADA.

Because the District typically makes transfers under the provision discussed in the prior paragraph, the District is

not eligible to make a transfer under this provision.

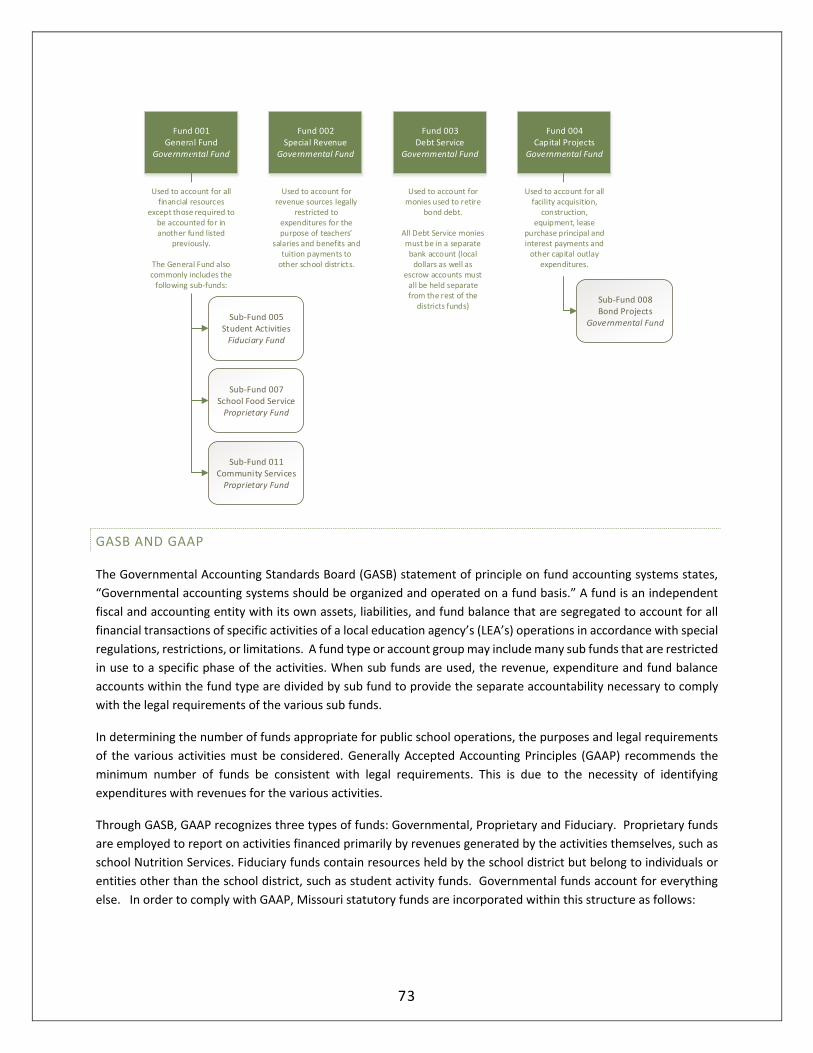

APPLICABLE FUND TYPES AND TITLES

Chapter 165, RSMo, provides that all school monies must be accounted for within a framework of four governmental

funds:

Fund 001 - General Fund (Incidental)

Fund 002 – Special Revenue Fund (Teachers Fund)

Fund 003 - Debt Service Fund

Fund 004 - Capital Projects Fund

In addition to these funds, the Park Hill School District also utilizes sub funds. Revenue and expenditures within sub

funds can be rolled into their governmental fund for reporting purposes.

73

GASB AND GAAP

The Governmental Accounting Standards Board (GASB) statement of principle on fund accounting systems states,

“Governmental accounting systems should be organized and operated on a fund basis.” A fund is an independent

fiscal and accounting entity with its own assets, liabilities, and fund balance that are segregated to account for all

financial transactions of specific activities of a local education agency’s (LEA’s) operations in accordance with special

regulations, restrictions, or limitations. A fund type or account group may include many sub funds that are restricted

in use to a specific phase of the activities. When sub funds are used, the revenue, expenditure and fund balance

accounts within the fund type are divided by sub fund to provide the separate accountability necessary to comply

with the legal requirements of the various sub funds.

In determining the number of funds appropriate for public school operations, the purposes and legal requirements

of the various activities must be considered. Generally Accepted Accounting Principles (GAAP) recommends the

minimum number of funds be consistent with legal requirements. This is due to the necessity of identifying

expenditures with revenues for the various activities.

Through GASB, GAAP recognizes three types of funds: Governmental, Proprietary and Fiduciary. Proprietary funds

are employed to report on activities financed primarily by revenues generated by the activities themselves, such as

school Nutrition Services. Fiduciary funds contain resources held by the school district but belong to individuals or

entities other than the school district, such as student activity funds. Governmental funds account for everything

else. In order to comply with GAAP, Missouri statutory funds are incorporated within this structure as follows:

Fund 001General Fund

Governmental Fund

Fund 002Special Revenue

Governmental Fund

Fund 003Debt Service

Governmental Fund

Fund 004Capital Projects

Governmental Fund

Sub-Fund 007School Food Service

Proprietary Fund

Sub-Fund 011Community Services

Proprietary Fund

Sub-Fund 005Student Activities

Fiduciary Fund

Sub-Fund 008Bond Projects

Governmental Fund

Used to account for all financial resources

except those required to be accounted for in another fund listed

previously.

The General Fund also commonly includes the

following sub-funds:

Used to account for revenue sources legally

restricted to expenditures for the purpose of teachers’

salaries and benefits and tuition payments to

other school districts.

Used to account for all facility acquisition,

construction, equipment, lease

purchase principal and interest payments and

other capital outlay expenditures.

Used to account for monies used to retire

bond debt.

All Debt Service monies must be in a separate bank account (local

dollars as well as escrow accounts must

all be held separate from the rest of the

districts funds)

74

Of these funds, only the General (Fund 001), Special Revenue (Teachers Fund) (Fund 002) and Capital Projects (non-

bond related) (Fund 004) allow the district flexibility to control expenditures. As a result, much of the district’s focus

is on these which are typically referred to as “Operating” funds. Funds maintained separate from the operating

budget include Debt Service (Fund 003), and Capital Projects activities supported by Bond Issue Proceeds (Fund 008).

CLASSIFICATION OF REVENUES AND EXPENDITURES

REVENUES

District revenues are received by fund and are also reported by fund and by source. Revenue sources include local,

county, state, federal, and other sources. Account codes are utilized to uniquely identify each revenue by its source.

SOURCES OF REVENUE

The District finances its operations through the local property tax levy, state sales tax, State Aid (as defined below),

federal grant programs and miscellaneous sources, including without limitation State Aid for transportation, a state

sales tax on cigarettes and a pro rata share of interest income from the counties in which each school district

operates. Debt service on general obligation bonds is paid from amounts in the District’s Debt Service Fund. The

primary source of money in the Debt Service Fund is local property taxes derived from a debt service levy. As

discussed below, the Debt Service Fund may, however, also contain money derived from transfers from the

Incidental Fund, from State Aid in the Classroom Trust Fund, and from certain other taxes or payments-in-lieu-of-

taxes that may be placed in the Debt Service Fund at the discretion of the Board.

State and federal revenue, as well as “Proposition C” sales tax revenue (included in the “Local Revenue”), are

received on a continuous monthly basis throughout the fiscal year. Local taxes, however, are received primarily in

January, over six months into a district’s fiscal year. Districts that receive a smaller percentage of revenue from state

and federal aid, and depend more on local revenues, will typically carry a larger fund balance than other districts

that may be receiving a larger percent of its revenue from state and federal aid amounts rather than local taxes.

LOCAL REVENUE

The primary sources of “local revenue” are (1) taxes upon real and personal property within a district, excluding

railroad and utility property taxes, which are more fully described below, and (2) receipts from a 1% state sales tax

(commonly referred to as “Proposition C revenues”) approved by the voters in 1982.

Proposition C revenues are deemed to be “local” revenues for school district accounting purposes. Proposition C

revenues are distributed to each school district based on the district’s weighted average daily attendance.

For the 2016-2017 fiscal year, each school district received approximately $979 per pupil from Proposition C

revenues based upon each district’s 2015-2016 Weighted ADA. For the 2017-2018 fiscal year, each school district

received approximately $964 per pupil from Proposition C revenues based upon each district’s 2016-2017 Weighted

ADA. The 2018-2019 budget includes anticipating $964 per WADA.

75

COUNTY REVENUE

For school taxation purposes, all state assessed railroad and utility property within a county is taxed uniformly at a

rate determined by averaging the tax rates of all school districts in the county. No determination is made of the

assessed value of the railroad and utility property that is physically located within the boundaries of each school

district. Such tax collections for each county are distributed to the school districts within that county according to a

formula based in part on total student enrollments in each district and in part on the taxes levied by each district.

County revenue also includes certain fines and forfeitures collected with respect to violations within the boundaries

of the school district.

STATE REVENUE

The primary source of state revenue or “State Aid” is provided under a formula enacted under Chapter 163, RSMo.

In its 2005 regular session, the Missouri General Assembly approved significant changes to the formula by adoption

of Senate Bill 287 (“SB 287”), which became effective July 1, 2006.

FEDERAL REVENUE

School districts receive certain grants and other revenue from the federal government that are required to be used

for the specified purposes of the grant or funding program.

The federal “No Child Left Behind” law required that every public school student must score at a “proficient” level

or higher in math and reading by 2014. Each state establishes its own proficiency levels. Federal sanctions for school

districts that fail to meet established proficiency standards include providing parents and students from

underperforming schools within a district the right to request a transfer to a school within the district that meets

proficiency standards. In addition, schools that continue to fail to meet proficiency standards must, in addition to

transfers and tutoring, make additional changes in staffing, curriculum and management. Federal sanctions apply

only to public schools that receive Title I federal money.

In July of 2012, the State earned a waiver from the No Child Left Behind law when the United States Department of

Education (the “DOE”) approved the State’s proposed accountability system aimed at replacing the existing

accountability measures of the No Child Left Behind law. This waiver expired August 1, 2016. The State’s proposed

system, Top 10 by 20, outlines a plan for the State to be in the top 10 states by 2020, with a focus on students

becoming college and career ready by graduation.

The federal “Every Student Succeeds Act” (“ESSA”) was signed into law on December 10, 2015. ESSA replaces the

“No Child Left Behind Act.” Each state education agency must develop a state accountability plan (“ESSA Plan”) that

incorporates testing based on challenging academic standards. The ESSA Plans must be submitted to the DOE by

either April 3 or September 18, 2017. Under ESSA, states can decide how much weight to give standardized tests in

their accountability systems and determine what consequences, if any, should attach to poor performance.

However, at least 95 percent of eligible students are required to take the state-chosen standardized test and federal

funding can be withheld if states fall below the 95 percent threshold. The transition to new ESSA Plans began during

the 2016-2017 school year, with full implementation expected in the 2017-2018 school year once a state’s ESSA Plan

is approved by the DOE. If a state’s ESSA Plan is not approved prior to the 2017-2018 school year then a state may

delay, until the 2018-2019 school year, implementation of certain aspects of the ESSA Plan.

76

The State of Missouri is in the process of designing an accountability system that will meet the parameters outlined

in ESSA. The State of Missouri plans to submit its plan to the DOE by the September 18, 2017 deadline. Under ESSA,

the State will continue to test students through the Missouri Assessment Program.

EXPENDITURES

Expenditures are approved by the Board of Education by fund and are reported by fund, function, object and

operational unit. Expenditures by function describe the action, purpose or program in which activities are

performed such as special education services. An expenditure’s object identifies the service or commodity obtained,

such as salaries, employee benefits, purchased services, supplies or capital projects. Expenditure units are utilized

to identify the program or school in which the expenditure is being made and approved.

Unique account codes are established to identify funds, functions, objects and units within the district accounting

system.

FUND BALANCE POLICIES

Financial statements prepared for school districts include the General/Incidental Fund, Special Revenue

Fund, Debt Service Fund, and the Capital Projects Fund.

GENERAL AND SPECIAL REVENUE FUND BALANCES

The General/Incidental and Special Revenue Funds are used for the day to day operation of the school district. The

combined fund balance carried in these funds is the primary indicator of a district’s financial viability and stability.

Fund balances will appropriately fluctuate based upon an individual school district’s primary source of revenue.

Some school districts receive 70 percent of their revenue from state and federal sources and 30 percent from local

sources. Other districts are just the reverse with 70 percent from local sources and 30 percent from state and federal

sources. Since state and federal revenues are received on a monthly basis throughout the fiscal year and local taxes

are received primarily in January, the timing of a district’s receipts is important when evaluating its fund balance.

According to state law, a school district shall not issue a check unless there is sufficient money in the treasury and in

the proper fund (Section 165.021(4), RSMo). At a minimum, a school district should carry a combined fund balance

in the General and Special Revenue Funds sufficient to make it through December without going negative on a fund

balance basis. School Districts have the option of borrowing money by entering into a tax anticipation note which

provides operating cash pending receipt of tax revenue.

DEBT SERVICE FUND BALANCE

The balance in the Debt Service Fund is highly predictable because expenditures usually consist of only two items

(principal and interest) and are known in advance. Debt Service Fund monies are to be placed in a separate bank

account and are not to be commingled with the district’s operating (General, Special Revenue, and Capital Projects

Funds) monies. The State Auditor’s Office monitors the fund balance in the Debt Service Fund when calculating the

77

maximum annual Debt Service Fund levy. For these reasons, the Debt Service Fund balance has been excluded from

the fund balance analysis.

CAPITAL PROJECTS FUND BALANCE

The Capital Projects Fund balance analysis has also been excluded because this fund is highly restricted in terms of

its usage and derivation. Capital Projects Fund money may be spent only for the erection of buildings or additions to

buildings, remodeling or reconstruction of buildings, furnishings for buildings, payment of lease purchase

obligations, purchases of real estate, and other capital outlay expenditures. Any expenditure for equipment that has

a unit cost of $1,000 or more and a useful life estimated at more than one year should be made from the Capital

Projects Fund. Current operating expenses (repairs, supplies, etc.) cannot be paid from the Capital Projects Fund.

BASIS OF ACCOUNTING FOR FINANCIAL REPORTING

The District presents its governmental activities in fund financial statements on the modified cash basis of

accounting, which is a comprehensive basis of accounting other than accounting principles generally accepted in the

United States of America, in conformity with the requirements of Missouri law and DESE. This basis recognizes

assets, liabilities, net assets/fund equity, revenues and expenditures when they result from modified cash

transactions.

The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise its assets,

liabilities, fund equity, revenues and expenditures. District resources are allocated to, and accounted for, individual

funds based upon the purposes for which they are to be spent and the means by which spending activities are

controlled. Transactions have been recorded in the following funds for the accounting of all District funds:

General/Incidental Fund: The General Fund is the primary operating fund of the District. It is used to

account for general activities of the District, including expenditures for noncertified employees, pupil

transportation costs, plant operation, fringe benefits, student body activities, community services, Nutrition

Services and any expenditures not required or permitted to be accounted for in other funds.

Special Revenue Fund: Accounts for expenditures for certificated employees involved in administration

and instruction. It includes revenues restricted by the state and the local tax levy for the payment of teacher

salaries and certain employee benefits.

Debt Service Fund: Accounts for the accumulation of resources for, and the payment of, principal, interest

and paying agent charges on, long-term debt.

Capital Projects Fund: Accounts for resources restricted for the acquisition or construction of specific

capital projects or items. It accounts for the proceeds of long-term debt, taxes and other receipts, including

the Bond proceeds, designated for construction of major capital assets and all other capital outlay.

The Treasurer of the District is responsible for handling all moneys of the District and administering the above funds.

All moneys received by the District from whatever source are credited to the appropriate fund. Moneys may be

disbursed from such funds by the Treasurer only for the purpose for which they are levied, collected or received and

78

only upon checks drawn by the Treasurer pursuant to orders of the Board or upon orders for payment issued by the

Treasurer pursuant to orders of the Board.

The financial records of the District are audited annually by an independent public accountant according to the

modified cash basis of accounting. The most recent annual audit has been performed by Daniel Jones & Associates,

P.C., Certified Public Accountants, Arnold, Missouri. The audited financial statements of the District for the fiscal

year ended June 30, 2016, together with the independent auditor’s report thereon, are included in this Official

Statement at Appendix B. A summary of significant accounting policies of the District is contained in the notes

accompanying the financial statements in Appendix B. The audited financial statements for earlier years with reports

by the certified public accountants are available for examination in the District’s office.

GENERAL ACCOUNTING POLICIES

A. Fund Accounting. The accounts of the district are organized on the basis of funds, each of which is considered

to be a separate accounting entity. The operations of each fund are summarized by providing a separate set of

self-balancing accounts that include assets, liabilities, and fund balances arising from revenues and expenditures.

The following funds used by the district are General/Incidental Fund, Special Revenue Fund, Debt Service Fund,

and Capital Projects Fund.

B. Basis of Accounting. The measurement focus and basis of accounting determine the accounting and financial reporting treatment applied to a fund. The district’s policy is to operate its financial statements on the cash basis of accounting. Revenues are recognized in the accounting period in which the revenue is received. Expenditures are recognized when the related fund liability is incurred and payment is made. Debt service resources are provided during the current year for payment of general long-term debt principal and interest; and therefore, the expenditures and related liabilities have been recognized in the Debt Service Fund.

C. Budgets and Budgetary Accounting. The district follows the procedures below in establishing the budgetary

data reflected in the financial statements:

1) In accordance with Chapter 67, RSMo, the district adopts a budget for each fund of the political subdivision.

2) Prior to July, the Assistant Superintendent for Business and Technology, who serves as the budget officer,

submits to the Board of Education a proposed cash basis budget for the fiscal year beginning on the following

July 1. The proposed budget includes estimated revenues and proposed expenditures for all district funds.

Budgeted expenditures cannot exceed beginning available monies plus estimated revenues for the year.

3) In June the budget is legally enacted by a vote of the Board of Education.

4) Subsequent to its formal approval of the budget, the Board of Education has the authority to make

necessary adjustments to the budget by formal vote. Adjustments made during the year are reflected in the

budget information included in the general-purpose financial statements. Budgeted amounts are finally

amended by the Board of Education.

D. Post-Employment Benefits.

79

COBRA Benefits – Under the Consolidated Omnibus Budget Reconciliation Act (COBRA), the district provides

healthcare benefits to eligible former employees and their eligible dependents. Certain requirements are

outlined by the federal government for this coverage. The premium is paid in full by the insured on or before the

first day of each month for the actual month covered. This program is offered for the duration of 18 to 36 months

after the termination date. There is no associated cost to the district under this program.

Retiree Benefits – Professional and support staff members participate in the Public School Retirement System

(PSRS) of the State of Missouri or in the Public Education Employee Retirement System (PEERS) as allowed by

law. Retired employees participating in PSRS or PEERS, as well as their dependents, surviving spouse and children,

are allowed to remain or become members in district health benefit programs. Certain requirements are outlined

by the state government for this coverage. The premium is paid in full by the insured on or before the first day

of each month for the actual month covered. There is no associated accrued obligation or cost to the district

under either program. The district prepares the initial COBRA or retiree enrollment forms and the former

employee makes the premium payment for the insurance carrier to the district. It is then remitted to the

insurance company with the district’s payment for active employees.

E. Compensated Absences. District twelve-month employees earn vacation time throughout the fiscal year and

can only accumulate a maximum of 40 days at the end of a fiscal year. Unused vacation beyond 40 days at the

end of a fiscal year is forfeited by the employee.

In addition, employees qualifying for sick leave are awarded between 9 and 12 days per year based upon their

employee classification. The days are earned throughout the fiscal year. Unused days may rollover to the

following year, and may accumulate up to a defined amount based upon employee classification. Unused days

are paid in to some employee groups on an annual basis. Remaining unused sick leave is payable to the employee

upon termination of employment at rates based on formulas utilizing years of service with the district.

F. Teachers’ Salaries. Payroll checks are written and dated in May for July and August payrolls and are included

in the financial statements as an expenditure paid in the month of May. This practice has been consistently

followed in previous years and is consistent with other Missouri school districts.

CASH AND TEMPORARY INVESTMENTS

Pooled Cash. Certain cash resources of the General, Special Revenue, and Capital Projects funds are combined

to form a pool of cash and investments, which is managed by the Board Treasurer. The pooled accounts consist

primarily of the bank checking account, bank money market accounts, and U.S. Government agency securities.

Cash and Investments. Cash resources of the individual funds are combined to form a pool of cash and

temporary investments (except the Debt Service Fund). State law requires that all deposits of the Debt Service

Fund be kept separate and apart from all other funds of the district. Each fund’s portion of this pool is displayed

on the combined balance sheet under each fund’s caption.

Missouri statutes require that all deposits with financial institutions be collateralized in an amount at least equal

to uninsured deposits.

80

TAXES

Property taxes attach as an enforceable lien on property as of January 1. Taxes are levied on November 30. All

unpaid taxes become delinquent January 1 of the following year. The county collects the property taxes and

remits them to the district on a monthly basis.

LONG-TERM DEBT

Article VI, Section 26(b), Constitution of Missouri, limits the outstanding amount of authorized general obligation

bonds of a district to 15% of the assessed valuation of a district (including state assessed railroad and utilities).

REFUNDED DEBT

Proceeds from Issues 2003, 2004, 2010, 2013 and 2016 General Obligation Refunding Bonds were used for the

refunding and refinancing of Issues 1997, 1999, 2001, 2004 and 2006 General Obligation Bonds. As a result of

the advanced refunding, the trust assets are shown as restricted in the district’s financial statements.

LEASES

The district currently has a variety of operating lease agreements. The agreements include warehouse space,

LEAD Innovation Studio, technology storage and logistics space, and various mobile classrooms. In addition, the

district leases a portion of the Gerner Family Early Education Center to Head Start for pre-school services.

PENSION PLANS

The Park Hill School District contributes to the Public School Retirement System of Missouri (PSRS), a cost sharing

multiple-employer defined benefit pension plan. PSRS provides retirement and disability benefits to certificated

employees and death benefits to members and beneficiaries. Positions covered by the Public School Retirement

System are not covered by Social Security. PSRS benefit provisions are set forth in Chapter 169.010.141 of the