2017 cpa exam changes

TRANSCRIPT

THE

2017CPA EXAM CHANGES

TABLE OF CONTENTS

Introduction

The Next CPA Exam: An Overview

Content Changes & Understanding

“Higher Order Skills”

Structure Changes

Administrative Changes

How Will These Changes Affect You?

Roger CPA Review Has Your Back!

Conclusion

3

4

8

19

27

28

30

31

INTRODUCTION

MANY CPA EXAM candidates haveprobably heard by now that thebiggest thing to happen to the

Uniform CPA Exam since it switched overto computerized testing is officiallyhappening: the 2017 changes. Due to theadvancement of technology, newlylicensed CPAs are now required toperform at higher levels earlier on intheir careers. In order to ensure that the

CPA Exam remains relevant and preparesnewly hired CPAs for such higherexpectations, the CPA Exam will undergosome drastic changes beginning Q2 of2017. Here at Roger CPA Review, we’llwalk you through what changes you canexpect to see in 2017, why these changesare happening, and how we’ll helpcandidates pass the next version of theCPA Exam.

THE NEXT CPA EXAM:AN OVERVIEW

● Why is the CPA Exam changing?

● How were the changes determined?

● When will the changes go into effect?

CHAPTER 1

ON SEPTEMBER 1, 2015, THE AMERICAN INSTITUTEOF CERTIFIED PUBLIC ACCOUNTANTS (AICPA)announced that there will be a new version of the Uniform CPA Exam. launching in thesecond quarter of 2017.

Many changes in the business world inconjunction with the advancement oftechnology have impacted the Accountingprofession. Whereas before the roles ofnewly licensed CPAs included tasks such aspreparing spreadsheets, leading schedules,and footing and crossfooting, theadvancement of technology has made suchtasks less relevant. Therefore, firms expecttoday’s newly licensed CPAs to demonstratea higher order skillset since they are now

required to perform at higher levels earlieron in their careers. In order to meet thisneed, there was a demand for the CPAExam to authentically test for the higherorder skills needed immediately in theworkplace. Therefore, the 2017 CPA Examchanges not only reflect the evolution ofthe profession, but also assurance of thepublic’s continued trust in CPAs’ judgmentand understanding of accountingstandards.

The AICPA routinely performs a PracticeAnalysis at least once every seven years. APractice Analysis is a systematic study of aprofession to describe the jobresponsibilities of those in practice. Thisinformation is then used to identify theknowledge and skills required to effectivelycarry out those responsibilities, and in turnshould be tested on the CPA Exam.

The AICPA began conducting a PracticeAnalysis in 2014, looking to ensure that thecontent and structure of the CPA Exam

were still relevant—and most importantly—reliable measures of the knowledge andskills required of a CPA to protect publicinterest. This led to the Research andDevelopment of an Exposure Draft: aninformed and thoughtful proposal for thenext version of the Uniform CPA Exambased on intensive research and inputfrom key stakeholders in the profession,such as boards of accountancy, accountingfirms, academia (including Roger CPAReview), and standards setters.

As information was collected throughmeans such as focus groups, interviews,surveys, meetings with CPAs from acrossthe profession, and an invitation tocomment with stakeholders, the AICPABoard of Examiners concluded that aconsensus was clear: due to advances intechnology and its ever-increasing use,CPAs new to the profession are now

expected to have the skills and knowledgeof a CPA with 2 years’ experience.Therefore, CPA Exam candidates need tobe tested with higher order skills toprepare them for the types of tasks andresponsibilities they can expect to performat the outset of their careers.

The Exposure Draft closed for commenting Q4 of 2015. The final Exposure Draft will bereleased to the public Q2 of 2016. The proposed changes to the CPA Exam are expectedto go into effect Q2 of 2017.

When will the changes go into effect?

CONTENT CHANGES

● Understanding “Higher Order Skills”

● Content Allocation

● New CPA Exam Blueprints

CHAPTER 2

UNDERSTANDING

WHILE THE NEXT version of the CPAExam is undergoing manyalterations, it’s important to keep

in mind that many of the topics andconcepts tested on the exam will essentiallyremain the same; what will be different is

the skill level and way in which candidateswill be tested on these concepts and topics.

Currently, the CPA Exam tests candidateson remembering & understanding andapplying their knowledge of concepts.

On the 2017 CPA Exam, this will change. Candidates won’t only be expected toremember, understand, and apply, but also analyze and evaluate concepts based ontheir knowledge.

Remembering &Understanding

ApplicationCurrent

CPA Exam+

+ + +2017

CPA ExamRemembering &Understanding Application Analysis Evaluation

The addition of these twocomponents, analysis andevaluation, are how the examis shifting toward higher orderskills which involves morecritical thinking andassessment. The graph to theright explains each skill leveldifficulty in depth. Sk

ill D

iffic

ulty

HOW WERE THESE SKILLS DETERMINED?

In order to determine what the higherorder skills tested would be, the AICPAadopted a version of Bloom’s Taxonomyof Educational Objectives. Initiallydeveloped by educational psychologists in1956 and later modified in 2001, Bloom’sTaxonomy classifies a continuum of skillsthat students can be expected to learnand demonstrate when acquiringknowledge.

As indicated in the chart below, theseskills include remembering,understanding, applying, analyzing,

evaluating, and creating. Candidates cansee that for the purposes of the currentCPA Exam, the only skills tested are“remembering & understanding” (whichhave been categorized as one), and“applying.” However in the 2017 CPAExam, the higher order skills that will beadded from Bloom’s Taxonomy are“evaluation” and “analysis”. Bloom’sTaxonomy has been widely used as abasis in educational and licensure testingto define the level of skills to be assessedand to guide the development of testquestions.

Bloom’s Taxonomy of Educational Objectives

Bloom’s Taxonomy ofEducational Objectives

2017 CPA Exam

Before 2017Changes

Remembering & Understanding

Application

Analysis

Evaluation

Remember

Understand

Apply

Evaluate

Create

CPA Exam Skill Levels

Here are some key words to help candidates understand the nature of the tasks theywill be expected to complete using these skill sets:

Understanding Skill Level

For example, if the skill tested is, the

question may ask candidates to ifsomething is current or non-current, or issomething an operating lease or a capitallease. For an question, theymay be asked to lease expenseor lease liability. Under anquestion, candidates may look at positiveand negative confirmations, or to

from one ledger to another. Andin questions, candidates couldbe presented with many documents and

whether the conclusion given byan assistant is correct or incorrect. Thesekeywords for each skill set can serve ashelpful identifiers for the skill difficultylevel candidates encounter.

While the analysis and evaluation components are definite game changers for the CPAExam, the area in which they will be tested is only in Task-Based Simulations. Here’s achart of the skill level tested by question type:

Skill Level Tested by Question Type

Notice that although evaluation is the difficult skill set, it will only be tested in asmall percentage of the Audit portion of the CPA Exam.

Here is skill level broken down by exam section, comparing the current exam to its2017 counterpart:

AUD

BEC

Skill level broken down by exam section, comparing the current exam to its 2017counterpart continued:

FAR

REG

THEREFORE, WHILE SOME portions of theexam will be more difficult, thepercentage in which candidates will

encounter them remains relatively small.Analysis will take anywhere from 15-35%.Evaluation will take anywhere from 15-35%. Application and remembering &understanding represent the skill setscandidates are normally tested on andused to and will still comprise a majority ofthe Exam.

Many candidates have asked whether ornot this will make the exam more difficult.Although analysis and evaluation comprisea small percentage of the exam, theassumption is that the increase in higherorder skills they will be testing will increasedifficulty to some extent. So it’s importantthat candidates are fully prepared forthese significant changes.

CONTENT

IN TERMS OF overall content allocation,candidates will notice that the exam willhave less specified areas of testing;

however, that doesn’t mean that thosetopics are necessarily going to disappearor that the exam will be any shorter.Instead, these areas are being integratedinto other areas. A good example of this isthe FAR section. In the graph below,

candidates can see that FAR will go fromhaving 5 areas to 4, and Non-profitaccounting will no longer be its own area.This is because Non-Profit accounting willbe integrated into sections I, II, and III.Because this topic is in reality accrual-based accounting, the AICPA decided it didnot make sense to test it separately.

In addition, because it’s been determinedthat the exam should only be testing whata person with 2 years’ experience in theaccounting industry should know, some ofthe more complicated topics are actuallybeing eliminated since these skills reflectthose who are most likely in a managerial

or partner role. By allocating contentinstead of segmenting it, the CPA Exambroadens candidates’ depth of knowledgeand integrates topics into several of thecategories in order to reflect theirportrayal in the real world.

The following is a breakdown of the content allocation for the remaining parts of the CPAExam, comparing the current version to its 2017 counterpart:

NEW CPA EXAM

TO ILLUSTRATE THE knowledge and skillsthat will be tested on the CPA Exam,the AICPA currently uses a Content

Specification Outline (CSO) to detail what isexpected on the CPA Exam in an outlineformat. Currently, the CSO lists the tasks acandidate will perform. However,

beginning in Q2 of 2016, the CSO will bereplaced with CPA Exam Blueprints.Blueprints provide a map of topics andtasks the candidate is expected to knowand perform, as well as what skill level(s)these tasks will assess.

Assist candidates in preparing for the exam by delineatingthe knowledge and skills that may be tested.

Provide assurance that the exam is properly designed totest such knowledge, skills, and tasks.

Apprise educators about the knowledge and skills candi-dates will need to function as newly licensed CPAs.

Guide the development of new exam questions.

The purpose of the blueprint will be to:

An example of the current CSO and new Blueprint is shown below:

With the introductionof blueprints, there’snow a greater level ofinformation availableto candidates on whatthey are expected toperform on the exam.This also helps us atRoger CPA Review sothat we can moreeffectively prepareour students forsuccess on the exam.

STRUCTURE CHANGES● Increasing Task-Based Simulations & Decreasing Multiple Choice Questions

● Document Review Simulations

● Time Allocation

CHAPTER 3

THE 2017 CHANGES will also introduce aseries of changes to the actualstructure of the exam. Such

changes include increasing the number ofTask-based Simulations (TBSs), decreasingthe number of Multiple Choice Questions(MCQs), and introducing a new type of

TBS: Document Review Simulations(DRSs). The only question type that willremain the same are WrittenCommunications (WCs). As a result, theexam will also see changes in scoring andtime allocation to accommodate thesestructural alterations.

INCREASING TASK-BASED SIMULATIONS &

Because TBSs are designed to test higherorder skills, the increase in TBSs persection has been well warranted. It iscurrently anticipated that BEC will include4-5 TBSs while AUD, FAR, and REG willeach include 8-9. Of course, the mostanticipated news regarding Task-Based

Simulations is the addition of a new type:Document Review Simulations (DRSs).We’ll talk more in depth about what DRSsare and what candidates need to know inthe following section, including why theywill be appearing on the CPA Exam earlierthan 2017.

While the number of TBSs are increasing,candidates can see from the chart thatMCQs for each section will actually bedecreasing by 12-20 questions,depending on the section. This is a direct

correlation to adding more TBSs to theexam since TBSs require more time toanswer and will be testing higher orderskills.

As can be seen in the graph below, the 2017 CPA Exam will include 2-3more TBSs in AUD, FAR, and REG. BEC will also include TBSs, which itnever has before.

As a result, the scoring weights of eachsection of the CPA Exam will also change.On AUD, FAR, and REG, MCQs willaccount for 50% of the total score whileTBSs will account for the other 50%.

Similarly, in BEC, MCQs will account for50% of the total score while TBSs accountfor 35%, and Written Communications(WCs) account for the last 15%:

By distributing the score weights this way,candidates will see that their final scoresare more balanced among MCQs, TBSs,and WCs. Whereas the current examallocates a majority of the score to MCQs,the 2017 version will test candidates

evenly across their abilities to remember& understand information in MCQs aswell as apply, analyze, and evaluate it inTBSs and WCs.

DOCUMENT REVIEW

IN AN OVERARCHING effort to help the CPAExam reflect what’s expected of newlylicensed CPAs on the job, DRSs are one

major change that will go into effectsooner than 2017. Candidates can expect

to see DRSs being tested on the CPAExam beginning July 1, 2016. Here, we’ll gointo further detail about what DRSs are,why they’re being added, and how theywill be tested on the CPA Exam.

DRSs have been added to the CPA Examto better prepare newly licensed CPAs forthe tasks they will be expected toperform. Such tasks will includemanagement and review of bankstatements, memos, and otherdocuments that are representative ofcommon business documents practicingCPAs normally encounter.

As a result, inclusion of DRSs play asignificant role in making the CPA Exammore authentic, informing future CPAs ofexpected job functions.

WHY IT’S BEING ADDED

WHAT IT WILL TEST

DRSs will start by testing candidates’ability to apply their knowledge ofdocumentation review, which involveslooking at related source documents(exhibits) and discerning what’simportant and what’s not importantfor solving the problem. In 2017, DRSswill also test higher order skills whichinclude analysis, and/or evaluation ofrealistic documents and relatedsource documents.

HOW IT WILL BE TESTED

An example of how DRSs will be tested can be seen below. The candidate will bepresented with highlighted phrases or sentences within the document that may ormay not be correct. They must then select the appropriate edit for that highlightedsection based on the relevant source documents, which will appear as categorizedtabs on the upper left hand corner.

For more detailed information about DocumentReview Simulations, please see our blog.

TIME

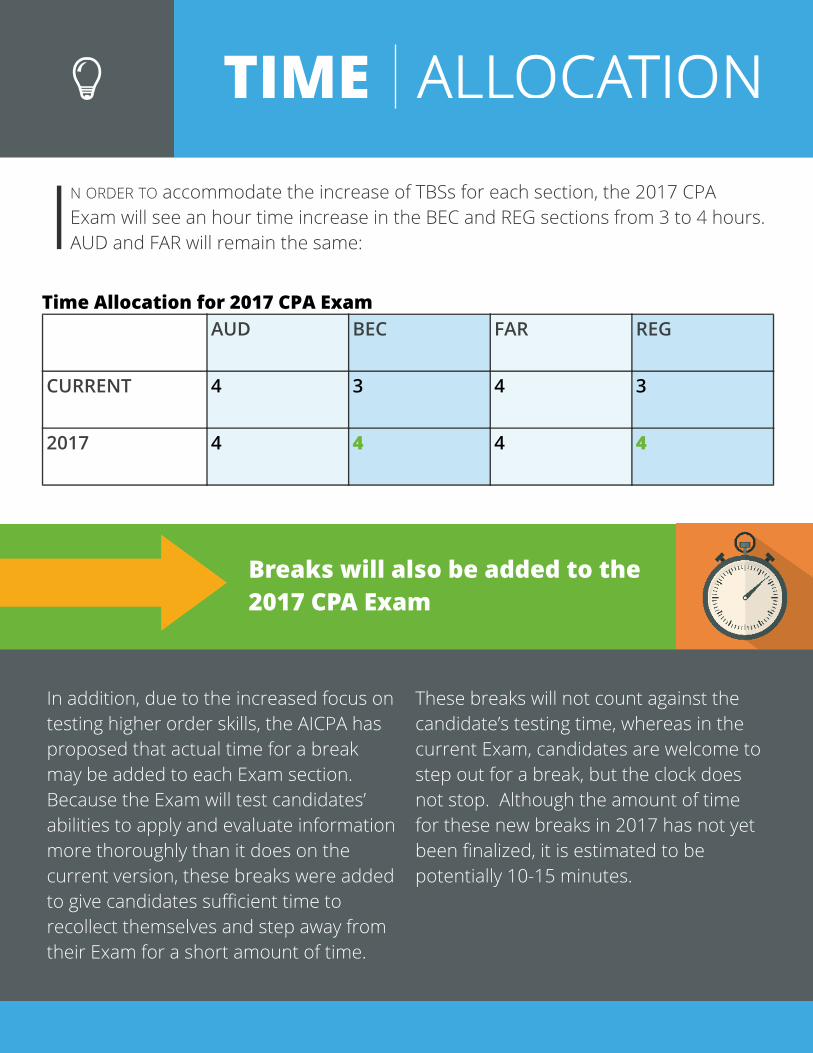

IN ORDER TO accommodate the increase of TBSs for each section, the 2017 CPAExam will see an hour time increase in the BEC and REG sections from 3 to 4 hours.AUD and FAR will remain the same:

AUD BEC FAR REG

CURRENT 4 3 4 3

2017 4 4 4 4

Time Allocation for 2017 CPA Exam

In addition, due to the increased focus ontesting higher order skills, the AICPA hasproposed that actual time for a breakmay be added to each Exam section.Because the Exam will test candidates’abilities to apply and evaluate informationmore thoroughly than it does on thecurrent version, these breaks were addedto give candidates sufficient time torecollect themselves and step away fromtheir Exam for a short amount of time.

These breaks will not count against thecandidate’s testing time, whereas in thecurrent Exam, candidates are welcome tostep out for a break, but the clock doesnot stop. Although the amount of timefor these new breaks in 2017 has not yetbeen finalized, it is estimated to bepotentially 10-15 minutes.

Breaks will also be added to the2017 CPA Exam

As with any major change within anorganization, the administrative side ofthe CPA Exam will be seeing somealterations as well. There will be a $20increase for both the BEC and REGsections as a result of the increasedtesting time from 3 to 4 hours.

The scoring timeline should not beimpacted with the 2017 CPA examchanges; however, the first window in

which the 2017 CPA exam changes firstemerge (Q2 and Q3 of 2017) mayexperience delays. Afterward, the scoringtimeline should return to normal.

In the future, they may also reduce theblackout periods to 10+ days or more,and are considering allowing candidatesto retest a failed section in the sametesting window.

POSSIBLE ADMINISTRATIVE

NOW THAT WE’VE provided in depthinformation about the 2017 CPAExam changes, here’s what we

recommend if you plan on taking the exambetween now and Q2 of 2017. If youanticipate on passing all 4 sections of theexam before Q1 of 2017, you will be less

affected with the exception of DRSs beingadded July 1, 2016. However, if youanticipate on becoming eligible to sit forthe exam in 2016 now or in the nearfuture, here’s how the 2017 changes willaffect you and our recommended courseof action for each scenario.

HOW WILL THE 2017 CHANGES

If you’re eligible to sit for the examnow, we recommend that you beginstudying for the exam and take all 4parts as soon as possible. This meansthat you have about 1 year and 2months to pass all 4 parts before thechanges go into effect Q2 of 2017.So if you haven’t already begunapplying for the exam, do so now since

it can take some time to go throughand complete the application process.Learn more about how to qualify andapply to the CPA Exam with our eBookhere. You can also begin studying forthe first section you plan on takingwhile you’re waiting for yourapplication to finalize to save time andget ahead of the game.

ELIGIBLE TO SIT NOW

If you will be eligible to sit for theexam sometime in 2016, werecommend that you get as manyparts done as possible before Q2 of2017. The idea is to strategically takethe more heavily impacted parts first,in an effort to get as many as you can

done before the changes take place.Our suggested order is the following:BEC, REG, AUD, and then FAR. Thisway, the less impacted parts will bethe ones you take when the changestake place.

If you’re going to eligible to sit for theexam in 2017, all you have to do is stayinformed and prepare accordingly. Asthe AICPA continues to finalize plansfor what the 2017 CPA Exam will looklike, you should continue to stayupdated and familiarize yourself withthe new exam’s overall content,structure, and format.

Another thing to keep in mind isbecause Audit & Attestation (AUD),Business Economics & Concepts (BEC),Financial Audit & Reporting (FAR), andRegulation (REG) still make up the 4parts of the CPA Exam, you will be ableto carry over any sections you passedbefore the 2017 changes take place.Just make sure they are within your 18month window.

ELIGIBLE TO SIT DURING 2016

ELIGIBLE TO SIT IN 2017

NO MATTER WHERE you are in your CPAExam journey, we understand theimportance of providing students

with the most up-to-date tools they needto confidently prepare for and pass theCPA Exam. At the crux of our coursemethodology, The Roger Method™ wasfundamentally designed to help studentsmake important connections, retaininformation, and apply what they havelearned to the CPA Exam. As always, theessential elements of this methodology—Learn, Practice, Support—were built toprovide students with a strong foundationof knowledge no matter what changes onthe CPA Exam may occur. So no matterhow students are tested, they will be fully

prepared on the concepts they need tolearn.

Additionally, our adaptive InteractivePractice Questions software is designed towithstand any and all exam changes with atesting environment that exactly mimicsthe CPA Exam. To ensure our students arefully prepared, we are expanding ourdatabase to include questions that assesshigher order skills and facilitate criticalthinking. Furthermore, the software willalso include samples of Document ReviewSimulations in time for the July 2016update. This evolution will not only preparestudents for the 2017 changes, but will alsoinstill confidence come exam day.

ROGER CPA REVIEW

IN

WE HOPE YOU found our coverage ofthe 2017 CPA Exam helpful andinformative. Stay tuned for our

upcoming Blogs, Webcasts, andNewsletters on the 2017 CPA Exam and

visit our page fordetailed info: rogerCPAreview.com/cpa-exam/changes. As always, please feel freeto reach out to us with any questions orcomments at [email protected].