2017 – 2021 strategic plan - ago.gov.zm · 2017 – 2021 strategic plan ... 17 2.4 stakeholders...

TRANSCRIPT

Prepared by:

The Office of the Auditor GeneralIn collaboration with

Management Development DivisionCabinet Office

June, 2017

2017 – 2021 Strategic Plan

OFFICE OF THE AUDITOR GENERAL

TABLE OF CONTENTS

ACRONYMS ................................................................................................................................................................................ ii

FOREWORD ............................................................................................................................................................................... iii

ACKNOWLEDGEMENTS ............................................................................................................................................................ iv

EXECUTIVE SUMMARY............................................................................................................................................................... v

1.0 INTRODUCTION ............................................................................................................................................................1

1.1 Background .................................................................................................................................................................................1

1.2 Functions .....................................................................................................................................................................................1

1.3 Organizational Structure ..........................................................................................................................................................2

1.4 Strategic Operational Linkages ...............................................................................................................................................2

1.5 Rationale for Developing the 2017-2021 Strategic Plan ....................................................................................................3

1.6 Methodology ..............................................................................................................................................................................3

1.7 Plan Coverage .............................................................................................................................................................................4

2.0 ENVIRONMENTAL ANALYSIS ........................................................................................................................................6

2.1 External Environmental Analysis .............................................................................................................................................6

2.2 Internal Environmental Analysis ...........................................................................................................................................14

2.3 Clients Analysis .........................................................................................................................................................................17

2.4 Stakeholders Analysis ..............................................................................................................................................................17

2.5 Strategic/ Core Issues ..............................................................................................................................................................20

3.1 Vision ..........................................................................................................................................................................................20

3.2 Mission .......................................................................................................................................................................................20

3.3 Goal .............................................................................................................................................................................................21

3.4 Values .........................................................................................................................................................................................21

4.0 OBJECTIVES, STRATEGIES AND PERFORMANCE INDICATORS ................................................................................. 22

5.0 PRE- CONDITIONS ..................................................................................................................................................... 34

6.0 GENERAL ASSUMPTIONS .......................................................................................................................................... 35

7.0 LINKING THE STRATEGIC PLAN TO THE BUDGETING PROCESS ............................................................................... 35

8.0 MONITORING AND EVALUATION OF THE STRATEGIC PLAN .................................................................................... 35

9.0 STRUCTURAL IMPLICATIONS .................................................................................................................................... 36

Appendix I - Indicative Core Functional Structure for OAG ................................................................................................. 37

Appendix ii - Summary of the SWOT Analysis ...................................................................................................................... 38

ACRONYMS

AFROSAI African Organisation of Supreme Audit Institutions

AFROSAI-E African Organisation of Supreme Audit Institutions – English Speaking

CAATs Computer Aided Audit Techniques

CPs Cooperating Partners

HRA Human Resource and Administration

IA Institutional Assessment

ICBF Institutional Capacity Building Framework

ICT Information Communication Technology

IFMIS Integrated Financial Management Information System

INCOSAI International Congress of Supreme Audit Institutions

ISSAIs International Standards of Supreme Audit Institutions

M&E Monitoring and Evaluation

MDD Management Development Division

MPSAs Ministries, Provinces and other Spending Agencies

NAO National Audit Office

OAG Office of the Auditor General

PESTEL Political Economic Social and Technological

PF Patriotic Front

PMS Performance Management System

SAIs Supreme Audit Institutions

SAI PMF Supreme Audit Institution Performance Measurement Framework

7NDP Seventh National Development Plan

SAC State Audit Commission

SWOT Strengths Weaknesses Opportunities Threats

FOREWORD

I am pleased to present the 2017 to 2021 Strategic Plan for the Office of the Auditor General (OAG). This Plan provides a strategic framework for improved audit service delivery.

With the expansion of the mandate of OAG in accordance with the Constitution (Amendment) Act No. 2 of 2016, the Office through this Plan will ensure that public resources are used for national development and wellbeing of citizens. The Office will remain committed to promoting accountability and prudent management of public resources.

The Strategic Plan outlines the priorities of the Office for the period 2017 to 2021. It is my sincere hope and trust that my Office will continue receiving the much needed support from all our esteemed stakeholders for its effective and efficient implementation.

I, therefore, implore my staff to remain committed to ensure successful implementation of the 2017 to 2021 Strategic Plan.

Ron M. Mwambwa Acting Auditor General

ACKNOWLEDGEMENTS

The development of this Strategic Plan would not have been possible without technical support from Management Development Division-Cabinet Office, the Cooperating Partners and other stakeholders. I am grateful for their support. I would also like to thank all members of staff for their commitment and valuable contributions during the consultative process.

Finally, I am grateful to the energetic Core Team that spearheaded the whole strategic planning process from the review of the performance of the Office during the 2014 to 2016 Strategic Plan period to the formulation of this new Plan covering 2017 to 2021.

Davison K. MendamendaDeputy Auditor General – Corporate Services

EXECUTIVE SUMMARY

The Office of the Auditor General (OAG) is the Supreme Audit Institution (SAI) of Zambia and draws its mandate from the Constitution (Amendment) Act No. 2 of 2016 under Article 250 and the Public Audit Act No. 29 of 2016. The Office engaged Management Development Division (MDD) - Cabinet Office to provide technical support to review the performance of the Office during the period 2014 to 2016 and to develop the 2017 to 2021 Strategic Plan due to the following reasons:

• Expiry of the Office of the Auditor General 2014 to 2016 Strategic plan;• Need to take on board national priorities outlined in the Seventh National Development Plan and

the aspirations of the current administration in the revised 2017 to 2021 Patriotic Front Manifesto;• Need to align all national programmes and activities to the electoral cycle; and• Non-attainment of the targets to reduce irregular payments, which instead increased from K26

million in 2014 to K115 million in 2015.

According to the Public Audit Act No. 29 of 2016, the Office of the Auditor-General (OAG) is to be established as the National Audit Office (NAO). The transformation is aimed at enhancing the financial and administrative autonomy of the Office, and strengthening its functions by expanding the mandate to include the auditing of Local Authorities as provided for under the Constitution (Amendment) Act No. 2 of 2016, Article 250 among others. However, the change of the name from OAG to NAO, the operationalisation of the State Audit Commission Act and the Public Audit Act, which are key for the Office to attain administrative and financial autonomy, await the issuing of the Statutory Instruments.

The main function of the OAG is to audit the accounts of State organs, State institutions, provincial administration and local authorities; and other institutions financed from public funds. In this respect, the OAG conducts external audit on these institutions to examine whether the funds appropriated by Parliament or raised by the Government and disbursed have been applied for the purposes for which they were appropriated or raised.

The assessment of the Office‘s performance during 2014 to 2016 and development of the 2017 to 2021 Strategic Plan took a consultative process involving stakeholders namely: staff, management, clients and other stakeholders. The stakeholders were consulted to provide feedback on the performance of the Office and to suggest areas for improvement. The assessment showed an average overall performance of 50% during the period under review although there was exceptional performance in other areas of auditing. The average overall performance was largely attributed to support from Government and Cooperating partners; technical support from regional audit bodies such as AFROSAI-E and the INTOSAI and staff commitment towards work.

This Strategic Plan was developed with a focus on addressing the main challenges faced by the Office and consolidating some of the gains recorded. Against this background, OAG’s strategic direction for the period 2017 to 2021 is illustrated in the following statements:

Vision: “A dynamic audit institution that promotes transparency, accountability and prudent management of public resources.”

Mission:“To independently and objectively provide quality auditing services in order to assure our stakeholders that public resources are being used for national development and wellbeing of citizens.”

Goal: To give assurance that at least 80% of public resources are applied towards development outcomes.

Values:To independently and objectively provide quality auditing services, OAG shall uphold the values of Integrity, Professionalism, Objectivity, Team-work, Confidentiality, Excellence, Innovation and Respect.

Objectives:

In the next five years, OAG will pursue the following objectives:

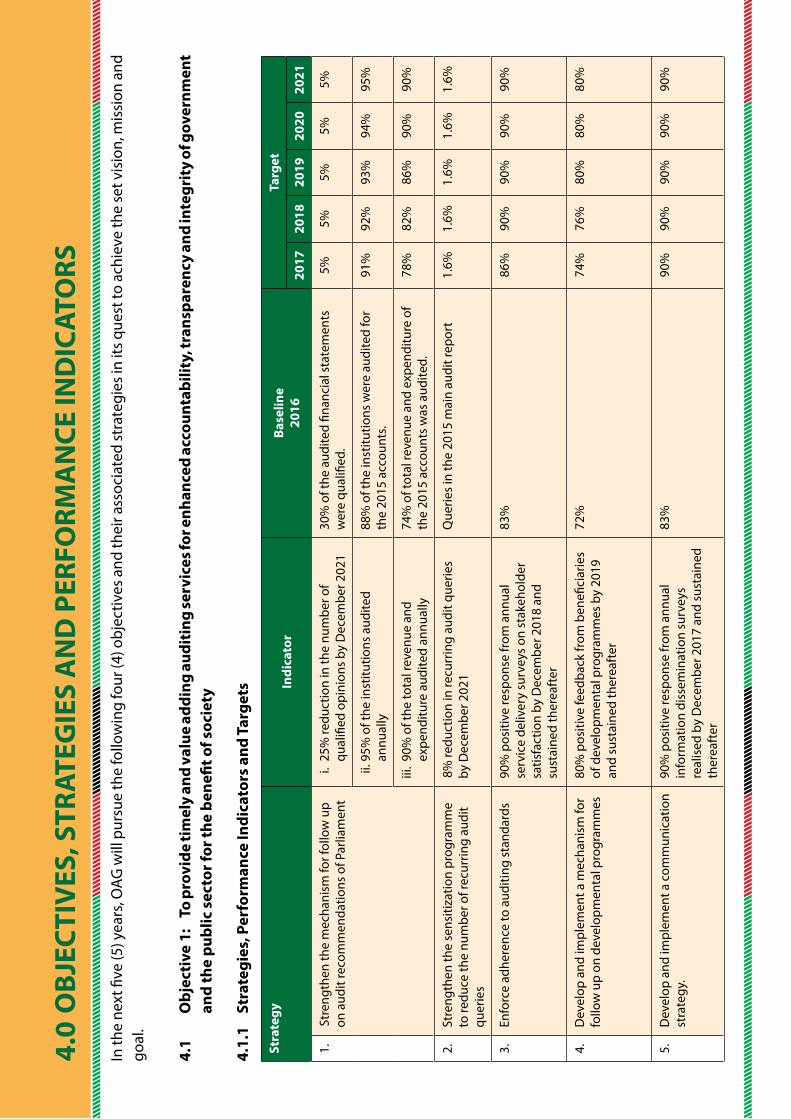

i. To provide timely and value adding auditing services for enhanced accountability, transparency and integrity of government and the public sector for the benefit of society.

ii. To effectively plan, execute, monitor and evaluate programmes and provide management information for timely decision making and attainment of set objectives.

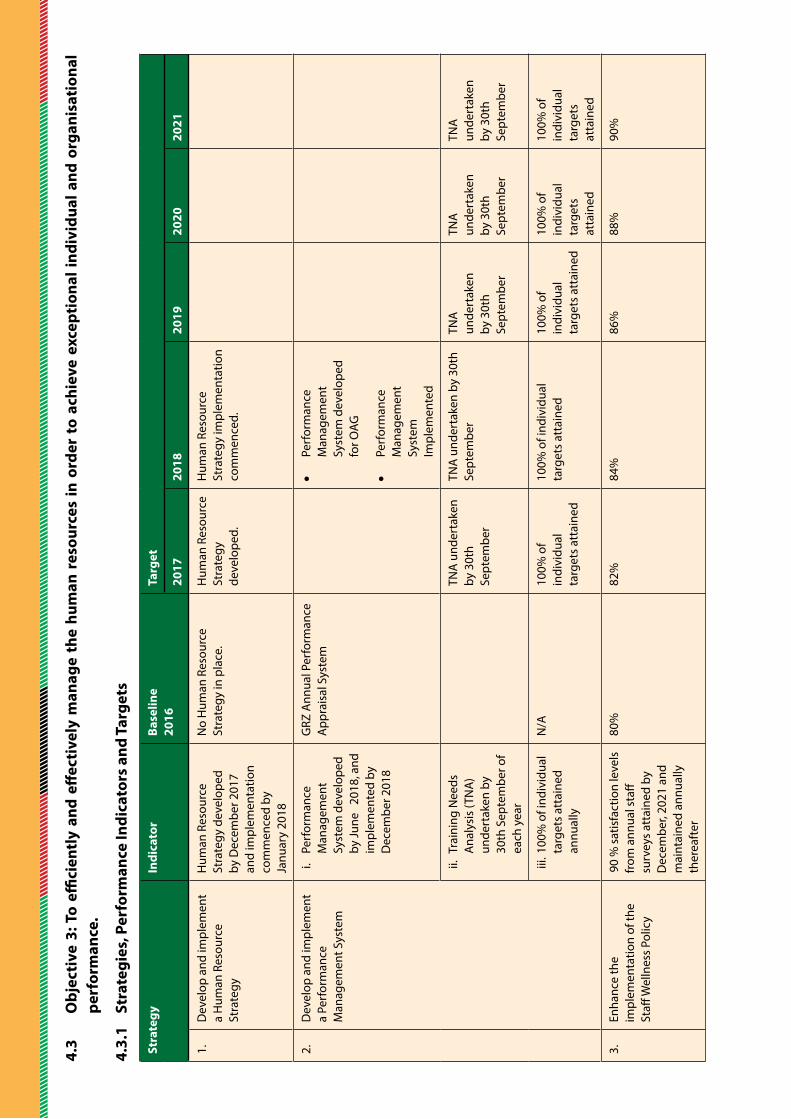

iii. To efficiently and effectively manage the human resources in order to achieve exceptional individual and organisational performance.

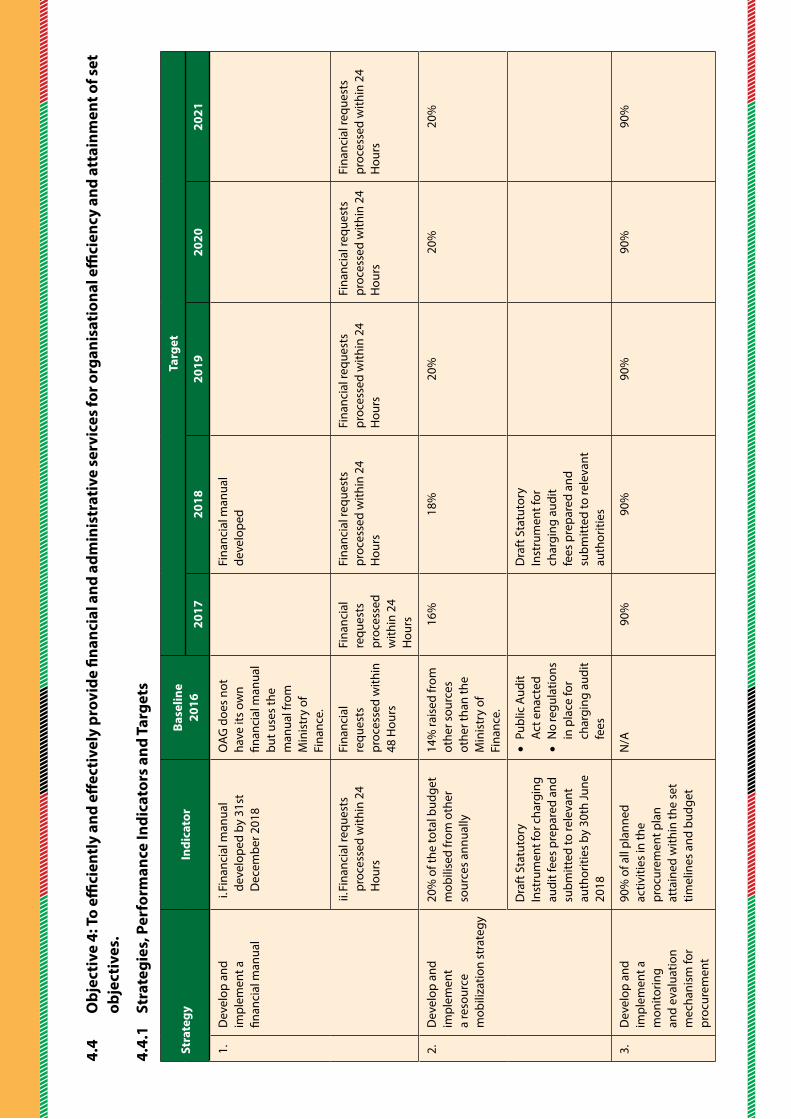

iv. To efficiently and effectively provide financial and administrative services for organisational efficiency and attainment of set objectives.

Key Strategies:

Among the key strategies to realise the objectives are:i. Strengthen the mechanism for follow up on audit recommendations of Parliament;ii. Strengthen the sensitization programme to reduce the number of recurring audit queries; iii. Enforce adherence to auditing standards; iv. Develop and implement a communication strategy;v. Develop and implement a mechanism for follow up on developmental programmes; vi. Develop and implement a Human Resource Strategy;vii. Develop and implement a Performance Management System;viii. Review and operationalise the organisation structure and job Descriptions; ix. Develop and implement a resource mobilization strategy; andx. Develop and implement a monitoring and evaluation mechanism for procurement.

These strategies will result in the following among others:

i. Reduction in the number of qualified opinions and recurring audit queries, demonstrating improvements in the management of public resources;

ii. Improved information management and organizational efficiency, demonstrating enhanced internal processes and organisational capacity;

iii. Positive response from clients and stakeholders, demonstrating a high level of satisfaction; and

iv. Improved positive image of the Office.

1.0 INTRODUCTION

1.1 Background

The Office of the Auditor General (OAG) is a government institution charged with the responsibility of providing audit services to Ministries, Provinces and other Spending Agencies (MPSAs) as well as private institutions which receive government subvention in any financial year. The Office plays an oversight role in the use of public resources appropriated by Parliament or raised by Government.

According to the Public Audit Act No. 29 of 2016, the Office of the Auditor-General (OAG) is to be established as the National Audit Office (NAO). The Auditor-General is the Chief Executive Officer of NAO appointed under Article 249 (1) of the Constitution. The transformation is aimed at enhancing the financial and administrative autonomy of the Office, and strengthening its functions by expanding the mandate to include the auditing of Local Authorities as provided for under the Constitution (Amendment) Act No. 2 of 2016, Article 250 among others. However, the change of the name from OAG to NAO, the operationalisation of the State Audit Commission Act and the Public Audit Act, which are key for the Office to attain administrative and financial autonomy, await the issuing of the Statutory Instruments.

The timelines for submitting audit reports at the end of each financial year have been reduced from twelve months to not later than nine (9) months after the end of each financial year.

The role of OAG in ensuring prudent management and utilisation of public resources is well underscored in the Seventh National Development Plan, which has prioritized enhancing domestic resource mobilisation, reforecasting of public spending and restoring budget credibility to contribute to the well-being of the Nation and achievement of the Vision 2030.

1.2 Functions

The functions of OAG as provided for under the Constitution (Amendment) Act No. 2 of 2016 Article 250 and the Public Audit Act No. 29 of 2016 are as follows:

a) audit the accounts of State organs, State institutions, Provincial Administration and Local Authorities as well as institutions financed from public funds;

b) audit the accounts that relate to the stocks, shares and stores of the Government;

c) conduct financial and value for money audits, including forensic audits and any other type of audit, in respect of any project that involves the use of public funds;

d) Carry out special, environmental, procurement and contract audits or reviews of the state organs, state institutions and private institutions;

e) Ascertain that money appropriated by Parliament or raised by the Government and disbursed has been applied for the purpose for which it was appropriated or raised; was expended in conformity with the authority that governs it; and was expended economically, efficiently and effectively; and

f) Recommend to the Director of Public Prosecutions or a law enforcement agency any matter within the competence of the Auditor-General that may require to be prosecuted.

1.3 Organizational Structure

The OAG is headed by the Auditor General who is assisted by two Deputy Auditors General in charge of the Audit Division and Corporate Services Division. There are seven directorates, of which five (5) are under the Audit Division and two (2) under the Corporate Services Division. The operations are required to be decentralized to all the provinces and progressively to the districts as provided for under the Constitution (Amendment) Act No. 2 of 2016 Article 249 (2).

1.4 Strategic Operational Linkages

In executing its functions, OAG closely collaborates with institutions, such as, the National Assembly, National Prosecution Authority, Drug Enforcement Commission (DEC), Anti-Corruption Commission (ACC), Ministries, Provinces and other Spending Agencies (MPSAs). The NAO also values strategic alliances with stakeholders including, the Cooperating Partners (CPs), Civil Society Organisations (CSOs) and Supreme Audit Institutions, such as, International Organisation of Supreme Audit Institutions (INTOSAI), African Organisation of Supreme Audit Institutions (AFROSAI), African Organisation of Supreme Audit Institutions- English Speaking Countries ( AFROSAI-E) and INTOSAI Development Initiative (IDI).

1.5 Rationale for Developing the 2017-2021 Strategic Plan

The development of the 2017 to 2021 Strategic Plan was necessitated by the national priorities including improving transparency and accountability for enhanced public service delivery and growth in the economy as outlined in the Seventh National Development Plan, and recognition of the role of the Office in ensuring accountability and transparency in the use of public funds from taxes and donors in the revised Patriotic Front Manifesto, the expiry of the 2013 to 2016 Strategic Plan, and challenges faced by the Office during the implementation of the 2013 to 2016 Strategic Plan. The challenges included non-attainment of set targets such as reducing irregularities in the use of public funds. The 2015 Auditor General’s Report for instance, indicated an increase in irregular payments from K26 million in 2014 to K115 million in 2015. Further, the development of the Plan was necessitated by the need to align all national programmes and activities to the electoral cycle.

1.6 Methodology

The OAG engaged Management Development Division (MDD) - Cabinet Office to provide technical support to review the 2014 to 2016 Strategic Plan and develop the 2017 to 2021 Strategic Plan. A Core Team was constituted to spearhead the process, which involved a two pronged approach, that is, Institutional Assessment (IA) and Organisational Development (OD).

The IA involved determination of the performance of the Office during the period 2014 to 2016 and its internal capabilities. Various stakeholders were engaged to solicit for information on the performance and suggest areas for improvement. The views of stakeholders were obtained through a self-completion questionnaire and one-day engagement sessions to allow for free expression of views and building consensus on key issues respectively. The internal capabilities were determined using a number of tools including, the McKinsey 7s Model, Lewin’s Simple Change Management Model, Objective and Problem Trees, SWOT and PESTEL Analyses.

The information gathered informed the determination of the strategic direction for OAG for the next five years in terms of the Vision, Mission, and Goal, Objectives and their related strategies and Performance Indicators. The Plan was validated by various stakeholders.

1.7 Plan Coverage

The rest of the Plan is laid out as follows:

(i) Environmental Analysis

This Section analyses the internal and external environments within which OAG has been operating during the period 2014 to 2016 and provides an outlook for the next five (5) years. Specifically, the Section highlights some key developments that have taken place in the recent past, which have had or might have an impact on OAG’s operations and, therefore, may be of significance in future. These developments relate to political/policy, economic, social,, technological, legal and environmental (PESTEL). In addition, the Section gives some highlights on the performance of the Office during the period 2014 to 2016.

In the process, the Office’s Strengths, Weaknesses, Opportunities and Threats (SWOT) are highlighted. Further, the Section identifies OAG’s clients and stakeholders and their needs and concerns/interests respectively. The Section concludes with the identification of the policy and/or legal challenges (core issues) that need to be addressed for the Office to effectively and efficiently execute its mandate.

(ii) Vision, Mission, Goal and Value Statements

The Vision, Mission, Value and Goal Statements of the Office are articulated under this Section. The Vision statement illustrates the Office’s desired future successful state of being, while the Mission statement defines the Office’s fundamental purpose for its continued existence in the next five (5) years. The Goal statement projects strategically OAG’s broad but realistic targets to be achieved within the Plan period.

Finally, the Section outlines the Values that the Office shall uphold in the execution of its mandate in order to live up to the expectations of its clients, stakeholders and the Nation as a whole.

(iii) Objectives and Performance Indicators

The objectives of OAG to be pursued in the next five (5) years are outlined under this section. The objectives have been developed in line with the Vision, Mission and Goal Statements of the Office and taking into account the outcome of the SWOT, PESTLE, Clients and Stakeholders analyses. The objectives are accompanied by Performance indicators which are variables by which the achievement of the set objectives will be measured.

(iv) Strategies

Strategies, which are the most feasible courses of action to be taken by OAG to achieve the set objectives, and ultimately, the Goal, Mission and Vision, are outlined under this Section.

(v) Pre-Conditions

The critical success factors within the control of OAG that need to be in place for successful implementation of the Strategic Plan are presented under this Section.

(vi) Assumptions

The critical success factors outside the control of the Office that need to be in place for successful implementation of the Strategic Plan are presented under this Section.

(vii) Strategic Plan – Budget Linkage

The success of the Strategic Plan depends on how resources are planned, mobilised and allocated for the implementation of all the activities associated with the identified strategies to contribute to the achievement of the set objectives. Such activities and associated costs will be outlined in OAG’s Annual Operational Plans.

Accordingly, this Section provides general guidelines and underscores the importance of linking the Strategic Plan to the annual budgeting process to ensure that adequate resources are mobilised timely and made available for implementation of the Strategic Plan.

(viii) Monitoring and Evaluation

Monitoring and Evaluation (M&E) is crucial to ensuring successful implementation of the Plan and achievement of the desired impact. This Section, therefore, provides general guidelines and underscores the importance of an M&E Mechanism/Framework to the successful implementation of the Strategic Plan and the realization of the desired impact.

(ix) Structural Implications of the Strategic Plan

This section highlights what the structural implications are in terms of core functions or core business of OAG arising from the Strategic Plan developed. There may be inevitable structural changes that might come about as a result of the desire to address the challenges affecting the Office and achieve the objectives that have been set by the time the Plan expires.

2017 – 2021 STRATEGIC PLAN

2.0 ENVIRONMENTAL ANALYSIS

The performance of OAG during the period under review was impacted by both internal and external factors as follows:

2.1 External Environmental Analysis

The external environment was analysed using the PESTEL tool and the findings were as follows:

a) Political/ Policy developments

(i) Continuity of the Patriotic Front (PF) in Government

Following the 2016 general elections in which the PF retained the trust of the people of Zambia, there has been continued support to enhance the operations of OAG by the PF Government. During the period 2014 to 2016, the PF Government pledged to and adequately funded the Office to enable it effectively execute its mandate. Government support is further evidenced by granting the Office Autonomy as provided for in the Constitution (Amendment) Act No.2 of 2016.

OAG’s administrative and financial independence will, therefore, be strengthened in line with International Standards for Supreme Audit Institutions (ISSAI 1 and 10). OAG will continue to engage Government to fulfil its commitment to adequately fund the Office. The Office will also put measures in place to ensure prudent utilisation of the resources. In addition, the Office will operationalise the State Audit Commission Act No. 27 of 2016 and the Public Audit Act No. 29 of 2016.

(ii) Creation of New Ministries and Districts

The creation of new ministries and districts has increased the scope and coverage for OAG. The Office will engage Government for increased funding and staffing to enable it carry out its mandate. A resource mobilisation strategy will also be developed for alternative support and the structure of OAG will be reviewed to cater for the new districts.

(iii) Approval of the National Climate Change policy

The approval of the National Climate Change Policy in April 2016 requires commitment from all the institutions to mainstream climate change issues. In this regard, OAG will engage Cooperating Partners for financial and technical support, engage the SAI community to develop an Environmental Audit Manual and increased audit coverage to include issues related to Climate Change.

(iv) Developments in the INTOSAI Community

The OAG is a member of INTOSAI as well as its regional bodies AFROSAI and AFROSAI-E. Over the years, these bodies have adopted various standards and guidelines providing guidance on operations of SAIs. The adoption of ISSAI 12 on the value and benefits of SAIs provides a new framework to understand the uniqueness of the role of SAIs in their respective environments. In addition, the professionalization agenda adopted during the 2016 International Congress of Supreme Audit Institutions (INCOSAI) suggests a path Supreme Audit Institutions should follow to improve Public Financial Management in their country context. At the same meeting, the adoption of the SAI PMF and ICBF also provide useful analytical tools to assist SAIs evaluate their performance.

b) Economic Developments

(i) Increase in Exchange and Inflation Rates

During the period under review, Zambia experienced volatility in the exchange rate which saw the exchange rates increase from $1 = K6.2 in August 2015 to $1 = K15 by January 2016, before averaging to between K9 and K10 at close of 2016. The inflation rate also increased from 7.9% in January 2015 to 21.1% in December 2015 before declining to single digit of 7.2% at end of December 2016. This negatively affected OAG as evidenced by the funding of 64% of the 2016 budget.

To mitigate the above challenges, Office will develop a resource mobilisation plan and prioritise implementation of programmes.

c) Technological Developments

(i) E-Government Initiative and Social Media

The advancements in technology have resulted in the introduction of the E-Government Initiative, which includes Integrated Financial Management Information System (IFMIS), Treasury Single Account (TSA), Smart Zambia Institute, Big Data and Mobile computing. The advancements have also resulted in increased use of the social media, such as, Facebook, Twitter, WhatsApp, Instagram, LinkedIn and Imo. These developments have positively impacted and likely to continue impacting on the operations of OAG. The following have been the major benefits:

• Improved efficiency in the accounting and auditing processes;

• Increase in Audit coverage;

• Savings on hardware and software costs;

• Easy access to information; and

• Increased productivity arising from virtual work environment.

To optimise the developments, the Office will take the following measures:

• Build adequate capacity of staff to make use of the technology;

• Continuously collaborate with Smart Zambia Institute for technical support;

• Maintain the systems and put in place security measures to safe guard the information;

• Strengthen the performance management system to ensure maximum staff commitment to duty; and

• Develop and implement the ICT policy and Plan to guide ICT operations and use in the Office.

d) Ecological/ Environmental Developments

(i) Effects of global warming/industrial pollution

With the effects of global warming/ industrial pollution, the OAG will promote environmental audits which are not currently pronounced. This is in line with the adoption of the United Nations 2030 Agenda for sustainable development which is currently the benchmark against which progress in the area of sustainable development will be measured. This will result in increased audit coverage and

generation of revenue through the SI. The Office will develop and implement a resource mobilisation Plan for funds to increase awareness and recruitment of specialized staff. The Office will also regularly produce up to date reports to gain stakeholder confidence.

e) Legal Developments

(i) Enactment of the State Audit Commission Act No 27 of 2016

The enactment of the State Audit Commission Act No 27 of 2016 established the State Audit Commission and provided for the administrative and financial autonomy of OAG. The Office will develop and implement systems and procedures that will ensure efficient and effective service delivery. The wrong referencing of Article 234(2) (a) to Article 249(2)m, however, has a potential to conflict with the provisions of Article 250 (2) with regard to the independence of the OAG. The Office will, therefore, engage the Ministry of Justice to correct the referencing.

(ii) Amendment of the Constitution of Zambia

The Constitution (Amendment) Act No. 2 of 2016, has provided OAG with the following, among others:

• Reduced timelines for submitting audit reports at the end of each financial year from twelve months to not later than nine (9) months after the end of each financial year - Article 211 & 212;

• Expansion of the mandate to Audit Local Authorities - Article 250;

• Introduction of New Commissions - Part XVIII;

• Decentralization to Provinces & Districts - Article 249(2).

• Powers to recommend prosecution to the DPP or any other law enforcement agency - Article 250(e).

• Appointment of the Auditor General (AG) by SAC; and

• Expansion of types of Audits (procurement audit) - clause 14.

To optimize the developments, OAG will take the following measures:

• Enhance the auditing systems and procedures;

• Sensitize clients on the new audit period;

• Promote transparency in the appointment of the AG;

• Develop and implement a succession plan;

• Recognise deserving staff;

• Enrich jobs to motivate staff; and

• Strictly enforce accounting and audit standards.

(iii) Enactment of the Public Audit Act No. 29 of 2016

The Public Audit Act No. 29 of 2016 provides for the establishment of the Office of the Auditor General under Article 4(1) and for the following:

• Mandate to Charge and Collect audit fees - Clause 32(b);

• Surcharging and Disallowance of expenditure - Clause 26;

• Stipulation of Auditing Standards to follow - Clause 28;

• Appointment of External Auditors by State Audit Commission to audit OAG - Clause 34(2);

• Mandate to make regulation using Statutory Instruments (Sis) - Clause 39;

• Power to examine bank accounts for suspicious transactions - (Part 5-General provisions Clause 36(1);

• Expansion of types of Audits (procurement audit) - Clause 14; and

• Revenue generation

These will result in saving of public resources and reduced misappropriation, production of quality audits, enhanced Transparency and Accountability and positive image of the Office.

OAG will take advantage of the developments by developing regulations on charging of audit fees and modalities to surcharge and disallow expenditure. The Office will also enhance audit procedures and standards and develop and implement capacity building programmes in auditing standards for audit staff

2.1.1 Opportunities

Arising from the external environmental analysis, the following are some of the opportunities that OAG should take advantage of in executing its mandate in the five years:

a) Government support

The Government recognises the important role the Office plays in promoting transparency and accountability (prudent management) in the use of public resources. The Government has, therefore, continued to strengthen governance institutions such as OAG through provision of enabling legislation and funding as well as creating platforms for constructive engagements. OAG will continue engaging government for support.

b) Good Working Relationship with Strategic Institutions

The Office has a good working relationship with Cabinet Office. In this regard, there is efficient provision of administrative services such as facilitating the reorganisation of OAG and management of staff matters. The Ministry of Justice has also been supportive in providing technical support on legal matters. Further, the good working relationship with Ministry of Finance and Ministry of Justice ensures that the Public Accounts Committee (PAC) recommendations made on audits are resolved. In addition, the Ministry of Finance has continued to allow dialogue on issues of funding to OAG whenever need arises. The Office will strengthen collaboration with these stakeholders.

c) Support from Cooperating Partners

Cooperating Partners (CPs) have continued to provide both technical and financial support to the Office in carrying out its mandate. OAG will continue to leverage on this support to mitigate some of its challenges and ensure that all the support provided is put to good use or intended purpose.

d) Availability of SMART Zambia Institute

The SMART Zambia Institute is available to provide technical support in the implementation of ICT strategies in OAG in line with the E-Government initiative which is aimed at enhancing ICT utilisation in the provision of services in the Public Sector. The Office will engage the Institute to improve its ICT infrastructure and skills.

2.1.2 Threats

The opportunities above notwithstanding, there are also a number of threats that have had a negative impact on the operations of the Office and are likely to be of concern during the period 2017 to 2021 unless measures are taken to mitigate the effects. The threats include the following:

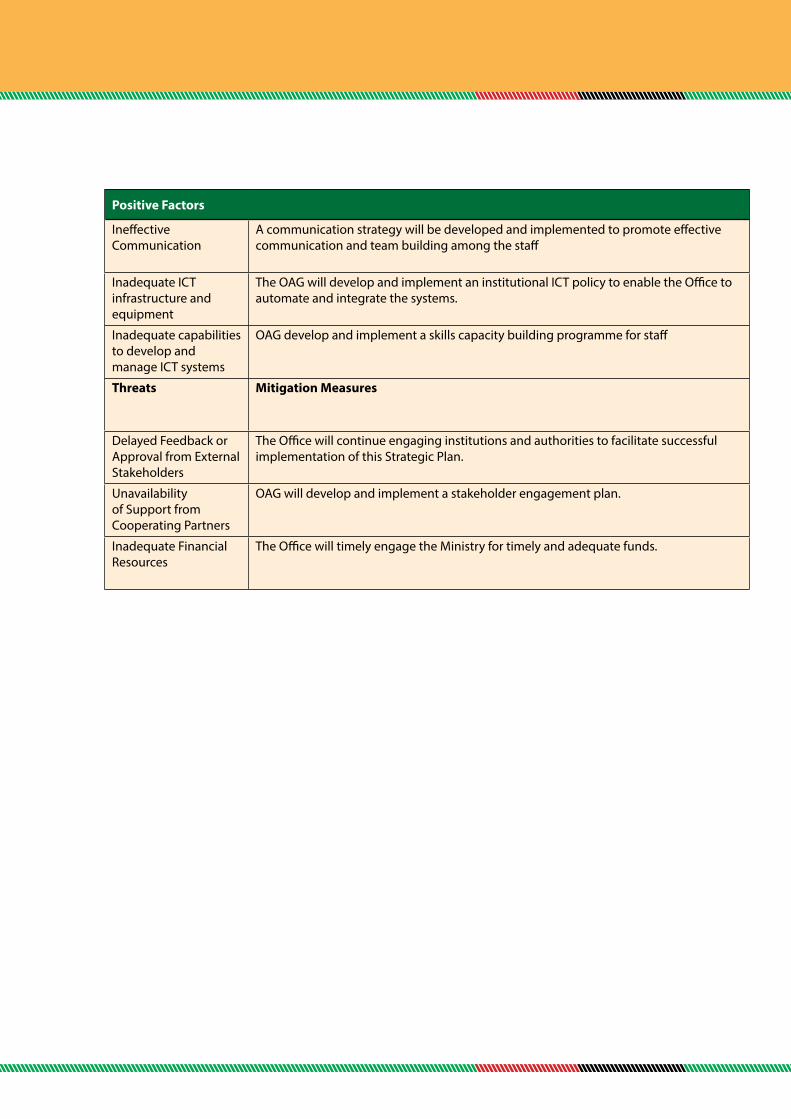

a) Delayed Feedback or Approval from External Stakeholders

The timeframe in which feedback or approval from external stakeholders is expected to be received is not within the control of the OAG. This can result in delays in implementation of vital work processes and subsequently fail to deliver the expectations of the citizenry. For example, the operationalisation of the State Audit Commission Act and the Public Audit Act, which are key for the Office to attain administrative and financial autonomy, await the issuing of the Statutory Instruments. The Office will continue engaging institutions and authorities to facilitate successful implementation of this Strategic Plan.

b) Unavailability of Support from Cooperating Partners

Cooperating Partners play a key role in execution of OAG mandate through technical and financial support. In the event that CPs are not available to support the Office, given adverse global economic development, the operations of the Office may be affected. The Office will develop and implement a stakeholder engagement plan.

c) Inadequate and Untimely Funding

Ministry of Finance sets the budget ceiling for the Office according to the national resource envelope and disburses the resources according to the revenue collections. The extent to which the annual work plan of the Office is executed is, therefore, largely dependent on the Treasury. The Office will timely engage the Ministry for timely and adequate funds.

2.2 Internal Environmental Analysis

2.2.1 Performance Against the 2014 to 2016 Strategic Plan

The overall performance of OAG during the period under review was rated as average, at 50%. However, the audit coverage in terms of institutions audited was exceptional at 95%, while expenditure was at 87% with revenue audit coverage being the lowest at 80%. The average overall performance was largely attributed to support from Government and Cooperating Partners, technical support from regional audit bodies, such as, AFROSAI-E and the INTOSAI; and staff commitment towards work among others.

The implementation of the Strategic Plan resulted in improved capacity to carry out more audits in line with ISSAIs, leading to improved quality of audit reports; effectiveness in conducting audits, leading to improved audit scope and coverage and increased number of reports being

published; and enhanced contribution to public awareness in particular, on matters relating to accountability and transparency in the management of public resources.

The major challenges, however were delays in the operationalisation of the SAC and inadequate and intermittent funding. The Office also saw an increase in irregular payments from K26 million in 2014 to K115 million in 2015.

2.2.2 Institutional Assessment

The assessment also revealed a number of strengths and weaknesses that the Office should optimise and mitigate respectively. The following are the strengths, and weaknesses identified:

a) Strengths

(i) Support from Management and Leadership

The management and Leadership of OAG is visionary and committed to ensuring that Office operations are effectively and efficiently carried out. The continuation of this support will enable the office to improve its operations in tandem with the evolving external environment, the national development priorities and to meet the expectations of stakeholders. The Staff will continue engaging management and the leadership for their support and guidance in implementing programmes of the Office.

(ii) Availability of Qualified and Competent Staff

The Office has qualified and competent staff in various disciplines of auditing. As of December 2016, the Office had fully qualified accountants which included ACCA-99, CIMA-8, ZICA-24, Bachelor in Accountancy-35 and other Degrees-25. This has enabled the Office to execute its mandate in a professional manner. OAG will continue building the capacity of staff and set specific individual targets to ensure timely implementation of programmes.

(iii) Availability of the Learning and Innovation Centre

The Office has a Learning and Innovation Centre used for conducting in-house training programmes. This has enabled the Office to save training costs. The Office will build the capacity of the Center and develop tailor made programmes for OAG staff.

(iv) Legal Provisions to Mobilise Resources

The Constitution (Amendment) Act No. 2 of 2016 and the Public Audit Act No. 29 of 2016 have provided the Office with opportunities of raising revenue through charging of audit fees in addition to the funding from the Treasury. Currently, funding to the Office has been erratic and not adequate. Consequently, the audit coverage has been negatively affected. Therefore, the opportunity to generate own revenue will enable the Office to increase its audit scope. The Office will, therefore, develop relevant regulations to facilitate revenue generation.

(v) Availability of the Integrity Committee

The Office has in place an Integrity Committee (IC) whose role is to deter corrupt activities and maladministration in the institution. The availability of the Committee promotes ethical values in the Institution. In this regard, the Office will actively engage the Committee to ensure adherence to the ethical values.

a) Weaknesses

(i) Resistance to change

The Office has in the recent past been undergoing change in all its work processes. However, instances of resistance to change have been observed during the transition period. As a result, this has negatively affected the pace of implementation of certain activities in the Office.

The Office will develop and implement a change management programme to enable staff understand and appreciate the importance of the changes taking place in the institution.

(ii) Lack of Understanding of the Role of the Integrity Committee

Despite the availability of the Integrity Committee in the Office, there is little understanding of the role of the Committee. As a result, the Office is not benefiting fully from the work of the Committee which promotes ethical behaviour among staff. There is need, therefore, for the Committee to actively engage the staff by sensitising them on the role of the Committee.

(iii) Ineffective Communication

There are instances of ineffective communication among the staff and this has led to misinterpretation of information. A communication strategy will be developed and implemented to promote effective communication and team building among the staff.

(iv) Inadequate ICT infrastructure and equipment

The Office lacks adequate Information Communication Technology (ICT) infrastructure and equipment to sustain the ICT needs, such as, the automation of audit processes and the integration of operational systems. This has contributed to the delayed completion of audit assignments and challenges to access information within the Office and outside. The OAG will develop and implement an institutional ICT policy to enable the Office to automate and integrate the systems.

(v) Inadequate capabilities to develop and manage ICT systems

There are inadequate skills amongst the staff to develop ICT systems. This has made it difficult for the Office to implement some of its ICT strategies and the e-Government initiatives that are aimed at enhancing the efficiency and effectiveness in the operations of the Office. OAG will develop and implement a skills capacity building programme for staff. A summary of the SWOT Analysis is at Appendix ii.

2.3 Clients Analysis

Ministries Provinces and other Spending Agencies that receive or manage public funds were identified as OAG clients. The client survey undertaken identified the following as their needs:

a) Quality Audit Services

The clients expect to receive quality audit services by:

• Actively interacting with clients during the audit process;

• Timely completion of audits;

• Widening the audit scope;

• Rotating staff on audit assignments;

• Exhibiting ethical behaviour; and

• Carrying out value for money audits.

b) Provision of Advisory

The clients indicated that the Office should be able to offer advisory services in addition to the audit services they are currently receiving. This will assist in resolving a number of audit queries.

2.4 Stakeholders Analysis

The Office identified sixteen (16) stakeholders whose interests/concerns are presented in the table below.

S/N Stakeholder Inter est/ Concerns

Parliament • Timely production of quality and value adding Audit reports

• Timely production of PAC status reports

Cabinet Office Timely production of the OAG administrative report.

Ministry of Finance • Timely certification of accounts and production of PAC status reports

• Timely production of performance audit reports• Prudent utilisation of funds

Media Institute of Southern Africa – Zambia Timely production of quality Audit Reports and the impact

Drug Enforcement Commission • Timely production of Financial and Forensic Reports• Effective collaboration • Provision of expert witnesses

Zambia Information Communication Authority • Adherence to ICT regulations and Standards • Adherence to professional ethics

Transparency International Zambia Timely production of quality Audit Reports and the impact

Jesuit Centre for Theological Reflection Timely production of quality Audit Reports and the impact

Anti-Corruption Commission • Timely production of Financial and Forensic Reports• Effective collaboration • Provision of expert witnesses

S/N Stakeholder Inter est/ Concerns

Zambia Public Procurement Authority • Enhanced quality of procurement audits• Effective collaboration

Cooperating Partners • Enhanced provision of audit services to Government and donor funded projects

• Prudent utilisation of funds and the impact

Policy Monitoring and Research Centre • Timely production of quality Audit Reports and the impact

• Effective collaboration

Professional Bodies (ACCA, ZIHRM, ZICA, CIMA, ZIPS, ICTSZ e.t.c)

Adherence to professional ethics and standards

Financial Intelligence Centre • Timely production of Financial and Forensic Reports• Effective collaboration

Civil Society for Poverty Reduction Timely production of quality Audit Reports and the impact

Supreme Audit Institutions Community (INTOSAI, AFROSAI, AFROSAI-E, IDI)

• Timely production of quality Audit Reports and the impact

• Adherence to professional ethics and standards• Effective collaboration and active participation in various

programmes.• SAI Zambia has contributed significantly in various

forums e.g the INTOSAI Working Group on Public Debt, and the OAG has been the External Auditor of AFROSAI for the last three years.

General Public • Timely production of quality and value adding Audit reports and the impact.

• An accountable Office of the Auditor General• Prosecution of offenders

2.5 Strategic/ Core Issues

The analysis identified two challenges that require legal intervention. These are, non-operationalization of the SAC because the Office cannot appoint Commissioners, Auditor General & Deputy Auditor Generals and non-operationalization of the Public Audit Act due to the absence of Commencement Orders. The effects have been perceived lack of commitment of the Office to enhance good governance. In addition, the Office has not been able to mobilize resources and surcharge and disallow expenditure by the OAG resulting in the loss of public funds.

The Office will engage relevant authorities on the issuance of Statutory Instrument (SI).

2017 – 2021 STRATEGIC PLAN

3.0 STRATEGIC DIRECTION

In the next five years, OAG will pursue the following strategic direction:

3.1 Vision

The Office shall, in the next five years, strive to be:

“A dynamic audit institution that promotes transparency, accountability and prudent management of public resources”.

Through this vision statement, OAG has committed itself to overcoming its limitations and accordingly, strategically reposition itself to respond to the concerns of its stakeholders, the needs of its clients and the economy in general. In this regard, the vision will serve as a standard guide in the Office’s promotion of transparency and accountability in the use of public resources appropriated by Parliament or raised by Government.

3.2 Mission

For the next five (5) years the Office has committed itself:

“To independently and objectively provide quality auditing services in order to assure our stakeholders that public resources are being used for national development and wellbeing of citizens”.

Through this Mission Statement, OAG commits enhancing the image of the Office by professionally providing audit services to its clients.

3.3 Goal

In line with the Vision and Mission statements, coupled with the need to further refocus the operations and provide overarching performance benchmarks, OAG has set for itself the goal below to be pursued in the next five (5) years as follows:

“To give assurance that at least 80% of public resources are applied towards development outcomes.”

3.4 Values

To independently and objectively provide quality auditing services, and ensuring attainment of the vision, mission and goals, the Office shall uphold the following core values:

(a) Integrity: Putting the obligations of OAG above one’s personal interests, and conducting oneself in a manner that is beyond reproach;

(b) Professionalism: Exhibiting competence, skills, good judgement, conduct and behaviour.

(c) Confidentiality: Being trustworthy by not revealing or disclosing privileged information to unauthorised persons;

(d) Team Work: Willing to cooperate and effectively contribute and participate as part of the team;

(e) Excellence: Commitment to being the best and/or delivering the best service;

(f) Innovation: Introducing new ideas and methods of delivering our services; and

(g) Respect: Considerate to one another, recognising each other’s differences and understanding the stakeholder’s needs and expectations.

4.0

OBJ

ECTI

VES

, STR

ATEG

IES

AN

D P

ERFO

RMA

NCE

IND

ICAT

ORS

In th

e ne

xt fi

ve (5

) yea

rs, O

AG w

ill p

ursu

e th

e fo

llow

ing

four

(4) o

bjec

tives

and

thei

r ass

ocia

ted

stra

tegi

es in

its q

uest

to a

chie

ve th

e se

t vis

ion,

mis

sion

and

go

al.

4.1

Obj

ecti

ve 1

: To

pro

vide

tim

ely

and

valu

e ad

ding

aud

itin

g se

rvic

es fo

r enh

ance

d ac

coun

tabi

lity,

tran

spar

ency

and

inte

grit

y of

gov

ernm

ent

and

the

publ

ic s

ecto

r for

the

bene

fit o

f soc

iety

4.1.

1 St

rate

gies

, Per

form

ance

Indi

cato

rs a

nd T

arge

ts

Stra

tegy

Indi

cato

rBa

selin

e 20

16Ta

rget

2017

2018

2019

2020

2021

1.St

reng

then

the

mec

hani

sm fo

r fol

low

up

on a

udit

reco

mm

enda

tions

of P

arlia

men

ti.

25%

redu

ctio

n in

the

num

ber o

f qu

alifi

ed o

pini

ons

by D

ecem

ber 2

021

30%

of t

he a

udite

d fin

anci

al s

tate

men

ts

wer

e qu

alifi

ed.

5%5%

5%5%

5%

ii. 9

5% o

f the

inst

itutio

ns a

udite

d an

nual

ly88

% o

f the

inst

itutio

ns w

ere

audi

ted

for

the

2015

acc

ount

s.91

%92

%93

%94

%95

%

iii. 9

0% o

f the

tota

l rev

enue

and

ex

pend

iture

aud

ited

annu

ally

74%

of t

otal

reve

nue

and

expe

nditu

re o

f th

e 20

15 a

ccou

nts

was

aud

ited.

78%

82%

86%

90%

90%

2.St

reng

then

the

sens

itiza

tion

prog

ram

me

to re

duce

the

num

ber o

f rec

urrin

g au

dit

quer

ies

8% re

duct

ion

in re

curr

ing

audi

t que

ries

by D

ecem

ber 2

021

Que

ries

in th

e 20

15 m

ain

audi

t rep

ort

1.6%

1.6%

1.6%

1.6%

1.6%

3.En

forc

e ad

here

nce

to a

uditi

ng s

tand

ards

90%

pos

itive

resp

onse

from

ann

ual

serv

ice

deliv

ery

surv

eys

on s

take

hold

er

satis

fact

ion

by D

ecem

ber 2

018

and

sust

aine

d th

erea

fter

83%

86%

90%

90%

90%

90%

4.

Dev

elop

and

impl

emen

t a m

echa

nism

for

follo

w u

p on

dev

elop

men

tal p

rogr

amm

es80

% p

ositi

ve fe

edba

ck fr

om b

enefi

ciar

ies

of d

evel

opm

enta

l pro

gram

mes

by

2019

an

d su

stai

ned

ther

eaft

er

72%

74%

76%

80%

80%

80%

5.D

evel

op a

nd im

plem

ent a

com

mun

icat

ion

stra

tegy

.90

% p

ositi

ve re

spon

se fr

om a

nnua

l in

form

atio

n di

ssem

inat

ion

surv

eys

real

ised

by

Dec

embe

r 201

7 an

d su

stai

ned

ther

eaft

er

83%

90%

90%

90%

90%

90%

4.2

Obj

ecti

ve 2

: To

effec

tive

ly p

lan,

exe

cute

, mon

itor

and

eva

luat

e pr

ogra

mm

es a

nd p

rovi

de m

anag

emen

t in

form

atio

n fo

r ti

mel

y de

cisi

on

mak

ing

and

atta

inm

ent o

f set

obj

ecti

ves

4.2.

1 St

rate

gies

, Per

form

ance

Indi

cato

rs a

nd T

arge

ts

Stra

tegy

Indi

cato

rBa

selin

e 20

16

Targ

et

2017

2018

2019

2020

2021

1.D

evel

op a

nd im

plem

ent

an a

utom

ated

and

in

tegr

ated

Man

agem

ent

Info

rmat

ion

Syst

em.

Aver

age

stan

dard

aud

it du

ratio

n re

duce

d fr

om

55 to

45

days

by

202

55 d

ays

53 d

ays

51 d

ays

49 d

ays

47 d

ays

45 d

ays

2.St

reng

then

the

M&

E Fu

nctio

n an

d th

e Fr

amew

ork

for m

onito

ring

all

prog

ram

mes

.

100%

of p

lann

ed

activ

ities

att

aine

d w

ithin

the

set t

imel

ines

an

d bu

dget

;

85%

90%

95%

100%

100%

100%

3.D

evel

op a

nd im

plem

ent

an in

stitu

tiona

l IC

T po

licy

and

Stra

tegy

to g

uide

th

e im

plem

enta

tion

and

use

of a

utom

ated

In

form

atio

n Sy

stem

s.

Inst

itutio

nal I

CT

Polic

y an

d St

rate

gy d

evel

oped

an

d im

plem

ente

d by

Ju

ne, 2

018

No

Inst

itutio

nal

ICT

Polic

y or

St

rate

gy

•In

stitu

tiona

l IC

T Po

licy

and

Stra

tegy

•

Impl

emen

tatio

n co

mm

ence

d

Man

agem

ent

Info

rmat

ion

Syst

em

inte

grat

ed a

nd

oper

atio

nalis

ed b

y D

ecem

ber,

2018

•IF

MIS

•PM

EC•

Hum

an R

esou

rce

Man

agem

ent

Syst

em

•Au

dit M

anag

emen

t Sy

stem

(AM

S)

•Li

brar

y

•H

elp

Des

k In

form

atio

n Sy

stem

•Fl

eet M

anag

emen

t•

Ass

et M

anag

emen

t In

form

atio

n

Inte

rnet

con

nect

ivity

at

all t

imes

N/A

Inte

rnet

con

nect

ivity

re

stor

ed w

ithin

1 h

our.

Inte

rnet

con

nect

ivity

re

stor

ed w

ithin

1 h

our.

Inte

rnet

co

nnec

tivity

re

stor

ed w

ithin

1

hour

.

Inte

rnet

co

nnec

tivity

re

stor

ed

with

in 1

hou

r.

Inte

rnet

co

nnec

tivity

re

stor

ed w

ithin

1

hour

.

4.D

evel

op a

nd

oper

atio

nalis

e an

ICT

disa

ster

reco

very

pla

n.

Lost

info

rmat

ion

reco

vere

d w

ithin

24

hour

s

N/A

Dat

a re

cove

red

with

in 2

4 ho

urs

Dat

a re

cove

red

with

in 2

4 D

ata

reco

vere

d w

ithin

24

Dat

a re

cove

red

with

in 2

4

Dat

a re

cove

red

with

in 2

4

5.D

evel

op a

nd im

plem

ent

a ris

k m

anag

emen

t st

rate

gy.

Risk

man

agem

ent

stra

tegy

dev

elop

ed a

nd

impl

emen

ted

by Ju

ne

2018

.

No

Risk

m

anag

emen

t st

rate

gy in

pl

ace.

Risk

man

agem

ent

stra

tegy

dev

elop

ed a

nd

impl

emen

ted

4.3

Obj

ecti

ve 3

: To

effici

entl

y an

d eff

ecti

vely

man

age

the

hum

an r

esou

rces

in o

rder

to

achi

eve

exce

ptio

nal i

ndiv

idua

l and

org

anis

atio

nal

perf

orm

ance

.

4.3.

1 St

rate

gies

, Per

form

ance

Indi

cato

rs a

nd T

arge

ts

Stra

tegy

Indi

cato

rBa

selin

e 20

16Ta

rget

2017

2018

2019

2020

2021

1.D

evel

op a

nd im

plem

ent

a H

uman

Res

ourc

e St

rate

gy

Hum

an R

esou

rce

Stra

tegy

dev

elop

ed

by D

ecem

ber 2

017

and

impl

emen

tatio

n co

mm

ence

d by

Ja

nuar

y 20

18

No

Hum

an R

esou

rce

Stra

tegy

in p

lace

.H

uman

Res

ourc

e St

rate

gy

deve

lope

d.

Hum

an R

esou

rce

Stra

tegy

impl

emen

tatio

n co

mm

ence

d.

2.D

evel

op a

nd im

plem

ent

a Pe

rfor

man

ce

Man

agem

ent S

yste

m

i. Pe

rfor

man

ce

Man

agem

ent

Syst

em d

evel

oped

by

June

20

18, a

nd

impl

emen

ted

by

Dec

embe

r 201

8

GRZ

Ann

ual P

erfo

rman

ce

App

rais

al S

yste

m

•Pe

rfor

man

ce

Man

agem

ent

Syst

em d

evel

oped

fo

r OAG

•Pe

rfor

man

ce

Man

agem

ent

Syst

em

Impl

emen

ted

ii. T

rain

ing

Nee

ds

Ana

lysi

s (T

NA

) un

dert

aken

by

30th

Sep

tem

ber o

f ea

ch y

ear

TNA

und

erta

ken

by 3

0th

Sept

embe

r

TNA

und

erta

ken

by 3

0th

Sept

embe

rTN

A

unde

rtak

en

by 3

0th

Sept

embe

r

TNA

un

dert

aken

by

30t

h Se

ptem

ber

TNA

un

dert

aken

by

30t

h Se

ptem

ber

iii. 1

00%

of i

ndiv

idua

l ta

rget

s at

tain

ed

annu

ally

N/A

100%

of

indi

vidu

al

targ

ets

atta

ined

100%

of i

ndiv

idua

l ta

rget

s at

tain

ed

100%

of

indi

vidu

al

targ

ets

atta

ined

100%

of

indi

vidu

al

targ

ets

atta

ined

100%

of

indi

vidu

al

targ

ets

atta

ined

3.En

hanc

e th

e im

plem

enta

tion

of th

e St

aff W

elln

ess

Polic

y

90 %

sat

isfa

ctio

n le

vels

fr

om a

nnua

l sta

ff su

rvey

s at

tain

ed b

y D

ecem

ber,

2021

and

m

aint

aine

d an

nual

ly

ther

eaft

er

80%

82%

84%

86%

88%

90%

Stra

tegy

Indi

cato

rBa

selin

e 20

16Ta

rget

2017

2018

2019

2020

2021

4.Re

view

and

op

erat

iona

lise

the

orga

nisa

tion

stru

ctur

e an

d jo

b D

escr

iptio

ns

i. O

rgan

isat

ion

stru

ctur

e re

view

ed

by D

ecem

ber 2

017

2010

Res

truc

turin

g re

port

Org

anis

atio

n st

ruct

ure

revi

ewed

ii. J

ob D

escr

iptio

ns

revi

ewed

by

Dec

embe

r 201

7

2004

job

desc

riptio

ns

curr

ently

in u

seA

ll jo

b de

scrip

tions

re

view

ed

iii. 1

00%

of t

he s

taff

esta

blis

hmen

t fille

d at

all

times

84%

90%

95%

100%

100%

100%

5.En

hanc

e th

e op

erat

ions

of

the

Lear

ning

and

in

nova

tion

Cent

re

Lear

ning

and

in

nova

tion

Cent

re

(LIC

) enh

ance

d an

d op

erat

iona

lised

by

Dec

embe

r 201

8

•Th

e LI

C ha

s no

eq

uipm

ent s

uch

as c

ompu

ters

, pr

ojec

tors

and

oth

er

pres

enta

tion

faci

litie

s.

•N

o sp

ecifi

c tr

aini

ng

cale

ndar

in p

lace

.

•Tr

aini

ng

cale

ndar

in

plac

e

•Co

mpu

ters

, pr

ojec

tors

and

oth

er

pres

enta

tion

faci

litie

s pr

ocur

ed a

nd

inst

alle

d

4.4

Obj

ecti

ve 4

: To

effici

entl

y an

d eff

ecti

vely

pro

vide

fina

ncia

l and

adm

inis

trat

ive

serv

ices

for o

rgan

isat

iona

l effi

cien

cy a

nd a

ttai

nmen

t of s

et

obje

ctiv

es.

4.4.

1 St

rate

gies

, Per

form

ance

Indi

cato

rs a

nd T

arge

ts

Stra

tegy

Indi

cato

rBa

selin

e 20

16

Targ

et

2017

2018

2019

2020

2021

1.D

evel

op a

nd

impl

emen

t a

finan

cial

man

ual

i. Fin

anci

al m

anua

l de

velo

ped

by 3

1st

Dec

embe

r 201

8

OAG

doe

s no

t ha

ve it

s ow

n fin

anci

al m

anua

l bu

t use

s th

e m

anua

l fro

m

Min

istr

y of

Fi

nanc

e.

Fina

ncia

l man

ual

deve

lope

d

ii. Fi

nanc

ial r

eque

sts

proc

esse

d w

ithin

24

Hou

rs

Fina

ncia

l re

ques

ts

proc

esse

d w

ithin

48

Hou

rs

Fina

ncia

l re

ques

ts

proc

esse

d w

ithin

24

Hou

rs

Fina

ncia

l req

uest

s pr

oces

sed

with

in 2

4 H

ours

Fina

ncia

l req

uest

s pr

oces

sed

with

in 2

4 H

ours

Fina

ncia

l req

uest

s pr

oces

sed

with

in 2

4 H

ours

Fina

ncia

l req

uest

s pr

oces

sed

with

in 2

4 H

ours

2.D

evel

op a

nd

impl

emen

t a

reso

urce

m

obili

zatio

n st

rate

gy

20%

of t

he to

tal b

udge

t m

obili

sed

from

oth

er

sour

ces

annu

ally

14%

rais

ed fr

om

othe

r sou

rces

ot

her t

han

the

Min

istr

y of

Fi

nanc

e.

16%

18%

20%

20%

20%

Dra

ft S

tatu

tory

In

stru

men

t for

cha

rgin

g au

dit f

ees

prep

ared

and

su

bmitt

ed to

rele

vant

au

thor

ities

by

30th

June

20

18

•Pu

blic

Aud

it Ac

t ena

cted

•

No

regu

latio

ns

in p

lace

for

char

ging

aud

it fe

es

Dra

ft S

tatu

tory

In

stru

men

t for

ch

argi

ng a

udit

fees

pre

pare

d an

d su

bmitt

ed to

rele

vant

au

thor

ities

3.D

evel

op a

nd

impl

emen

t a

mon

itorin

g an

d ev

alua

tion

mec

hani

sm fo

r pr

ocur

emen

t

90%

of a

ll pl

anne

d ac

tiviti

es in

the

proc

urem

ent p

lan

atta

ined

with

in th

e se

t tim

elin

es a

nd b

udge

t

N/A

90%

90%

90%

90%

90%

Stra

tegy

Indi

cato

rBa

selin

e 20

16

Targ

et

2017

2018

2019

2020

2021

4.Co

nstit

ute

and

oper

atio

nalis

e an

Au

dit C

omm

ittee

90%

of r

ecom

men

datio

ns

from

the

Inte

rnal

Aud

it Re

port

impl

emen

ted

No

Audi

t Co

mm

ittee

in

plac

e

Audi

t Co

mm

ittee

Co

nstit

uted

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al A

udit

Repo

rt im

plem

ente

d

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al

Audi

t Rep

ort

impl

emen

ted

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al

Audi

t Rep

ort

impl

emen

ted

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al

Audi

t Rep

ort

impl

emen

ted

5.St

reng

then

ad

min

istr

ativ

e su

ppor

t sys

tem

s

90%

sta

ff sa

tisfa

ctio

n le

vel i

n pr

ovis

ion

of

adm

inis

trat

ive

serv

ices

at

tain

ed b

y 20

19 a

nd

sust

aine

d th

erea

fter

N/A

80%

85%

90%

sta

ff sa

tisfa

ctio

n le

vel i

n pr

ovis

ion

of a

dmin

istr

ativ

e se

rvic

es

90%

sta

ff sa

tisfa

ctio

n le

vel

in p

rovi

sion

of

adm

inis

trat

ive

serv

ices

90%

sta

ff sa

tisfa

ctio

n le

vel i

n pr

ovis

ion

of a

dmin

istr

ativ

e se

rvic

es

Stra

tegy

Indi

cato

rBa

selin

e 20

16

Targ

et

2017

2018

2019

2020

2021

4.Co

nstit

ute

and

oper

atio

nalis

e an

Au

dit C

omm

ittee

90%

of r

ecom

men

datio

ns

from

the

Inte

rnal

Aud

it Re

port

impl

emen

ted

No

Audi

t Co

mm

ittee

in

plac

e

Audi

t Co

mm

ittee

Co

nstit

uted

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al A

udit

Repo

rt im

plem

ente

d

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al

Audi

t Rep

ort

impl

emen

ted

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al

Audi

t Rep

ort

impl

emen

ted

90%

of

reco

mm

enda

tions

fr

om th

e In

tern

al

Audi

t Rep

ort

impl

emen

ted

5.St

reng

then

ad

min

istr

ativ

e su

ppor

t sys

tem

s

90%

sta

ff sa

tisfa

ctio

n le

vel i

n pr

ovis

ion

of

adm

inis

trat

ive

serv

ices

at

tain

ed b

y 20

19 a

nd

sust

aine

d th

erea

fter

N/A

80%

85%

90%

sta

ff sa

tisfa

ctio

n le

vel i

n pr

ovis

ion

of a

dmin

istr

ativ

e se

rvic

es

90%

sta

ff sa

tisfa

ctio

n le

vel

in p

rovi

sion

of

adm

inis

trat

ive

serv

ices

90%

sta

ff sa

tisfa

ctio

n le

vel i

n pr

ovis

ion

of a

dmin

istr

ativ

e se

rvic

es

5.0 PRE- CONDITIONS

The following factors which are within the control of OAG will be critical for the successful implementation of the Strategic Plan.

i. Adequate, skilled and committed staff

The effective implementation of the Strategic Plan will depend largely on recruiting the right people, placing them in the right positions and retaining them over a long period of time. The staff should possess the right skills, knowledge and experience. Commitment from employees will also be important to achieve the strategic goals.

ii. Availability of operational tools and information

Effective implementation of the plan requires availability of essential operational tools and equipment for the staff.

iii. Support from leadership and management

Senior management sets the direction for the organisation, energises creativity and innovation and drives the effective implementation of the strategies. The support of leadership and management will be key to the successful implementation of the Strategic Plan.

iv. Operationalization of the Learning and Innovation Centre

The Learning and Innovation Centre is intended to provide in-house training for the staff to enable them expand their knowledge and skill base. For successful implementation of the plan, a fully operational Learning and innovation Centre should be in place.

v. Adequate Office Accommodation

The decentralisation of the operations of OAG will require that the securing of adequate and conducive office accommodation for the officers who will be deployed to the district offices for operations.

6.0 GENERAL ASSUMPTIONS

The following factors though outside the control of OAG will be critical for successful implementation of the Strategic Plan.