2015 feb spe student summit presentation allen sinor

TRANSCRIPT

1

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

© 2015 BAKER HUGHES INCORPORATED. ALL RIGHTS RESERVED. TERMS AND CONDITIONS OF USE: BY ACCEPTING THIS DOCUMENT, THE RECIPIENT AGREES THAT THE DOCUMENT TOGETHER WITH ALL INFORMATION INCLUDED THEREIN IS THECONFIDENTIAL AND PROPRIETARY PROPERTY OF BAKER HUGHES INCORPORATED AND INCLUDES VALUABLE TRADE SECRETS AND/OR PROPRIETARY INFORMATION OF BAKER HUGHES (COLLECTIVELY "INFORMATION"). BAKER HUGHES RETAINSALL RIGHTS UNDER COPYRIGHT LAWS AND TRADE SECRET LAWS OF THE UNITED STATES OF AMERICA AND OTHER COUNTRIES. THE RECIPIENT FURTHER AGREES THAT THE DOCUMENT MAY NOT BE DISTRIBUTED, TRANSMITTED, COPIED ORREPRODUCED IN WHOLE OR IN PART BY ANY MEANS, ELECTRONIC, MECHANICAL, OR OTHERWISE, WITHOUT THE EXPRESS PRIOR WRITTEN CONSENT OF BAKER HUGHES, AND MAY NOT BE USED DIRECTLY OR INDIRECTLY IN ANY WAY DETRIMENTALTO BAKER HUGHES’ INTEREST.

Working Smarter, Not HarderThe Role of Innovation in Oil and Gas

Allen SinorVice President, Global AccountsBaker Hughes

4-6 February, 2015

SPE Gulf Coast Section2015 Student Summit

Draft O

nly

2

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

The Perfect HSE Day

Recordable injuries or incidents

Serious spills/releases

Motor vehicle incidents

Draft O

nly

3

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Our Purpose

Draft O

nly

4

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Industry Challenges

Increasing cost– We need to drive efficiencies

More remote areas– High end complex technologies to remote regions

Experience gap– 44% personnel <3years experience

Need to use unconventionalextraction methods

Technological challenges of drilling– Pressure, temperature and extreme weather conditions

Significant operational risks and environmental impact

Draft O

nly

5

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

The Current Oil “Crisis”

NORWAY PULPIT ROCK

Draft O

nly

6

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Global Demand and Complexity

Draft O

nly

7

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

The BIG Question

Why do we explore, drill and develop oil and gas wells?

To make profitable returns for our investors

Draft O

nly

8

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Decision Strategies Oilfield Breakfast Forum 5 April 2012, Helge Hove Haldorson

Up to $16 dollarsfor four bottles(280,000% MU)

Draft O

nly

9

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

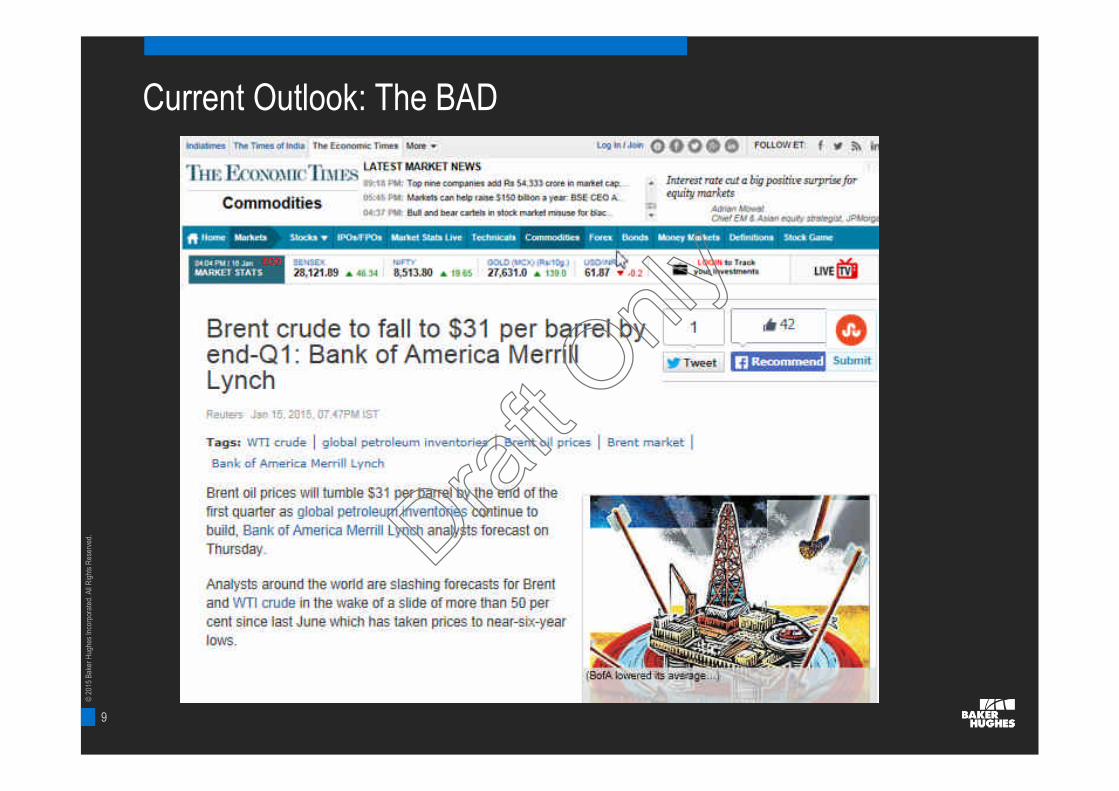

Current Outlook: The BAD

Draft O

nly

10

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

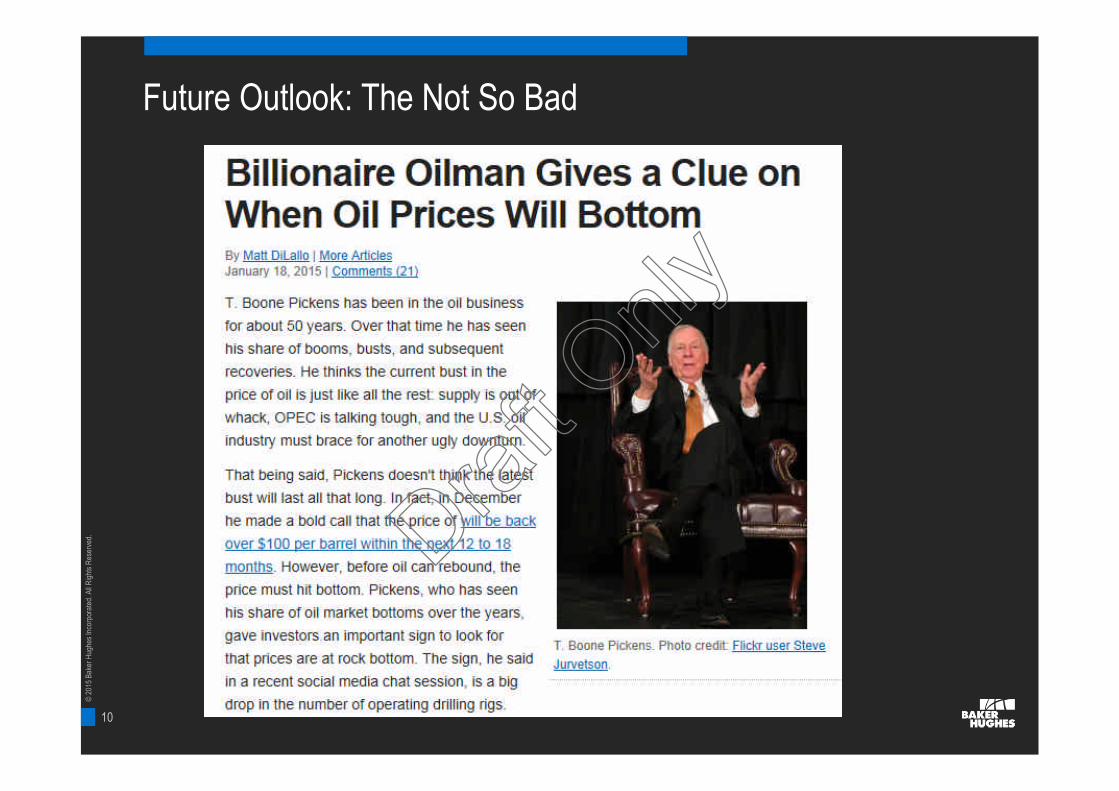

Future Outlook: The Not So Bad

Draft O

nly

11

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

700

800

1975 1980 1985 1990 1995 2000 2005 2010 2015E

Liqu

ids

Dem

and

/Liq

uids

Sup

ply

+O

PE

CS

pare

Cap

acity

(mm

bbl/d

)

Rea

lCap

ex($

B,2

013)

/Rea

lAvg

.WT

I(20

13$)

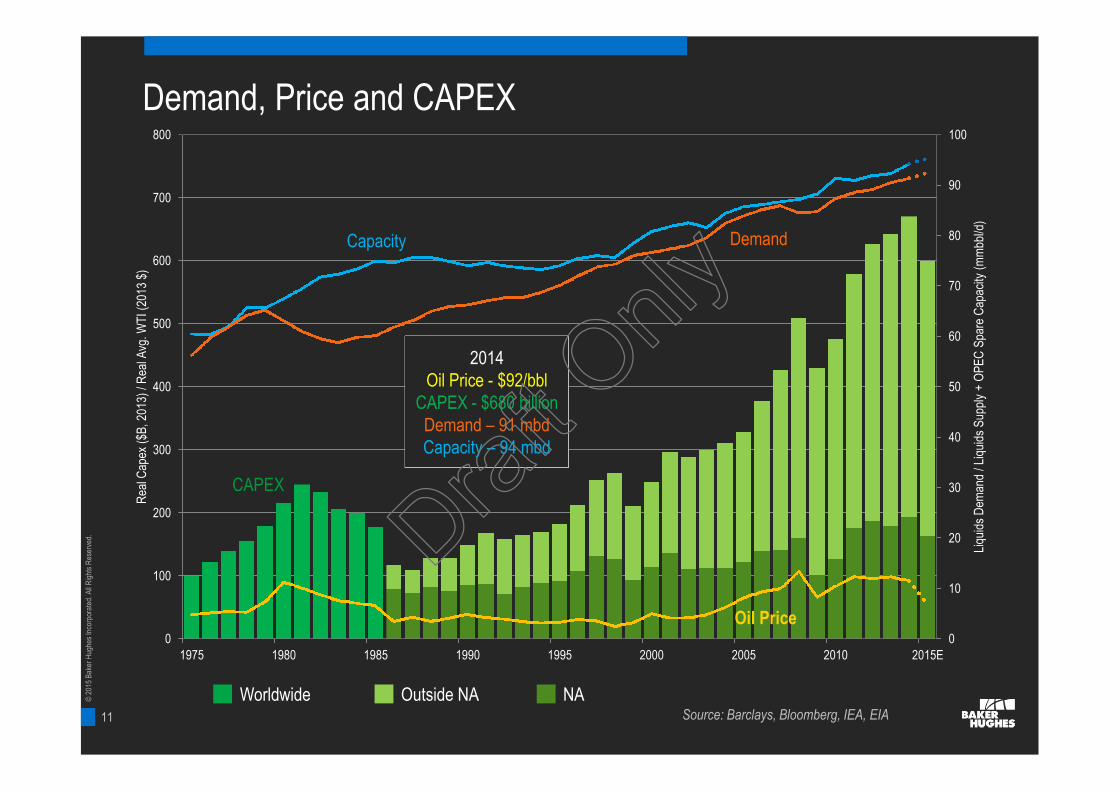

Source: Barclays, Bloomberg, IEA, EIA

CAPEX

Oil Price

DemandCapacity

Worldwide Outside NA NA

2014Oil Price - $92/bbl

CAPEX - $680 billionDemand – 91 mbdCapacity – 94 mbd

Demand, Price and CAPEX

Draft O

nly

12

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

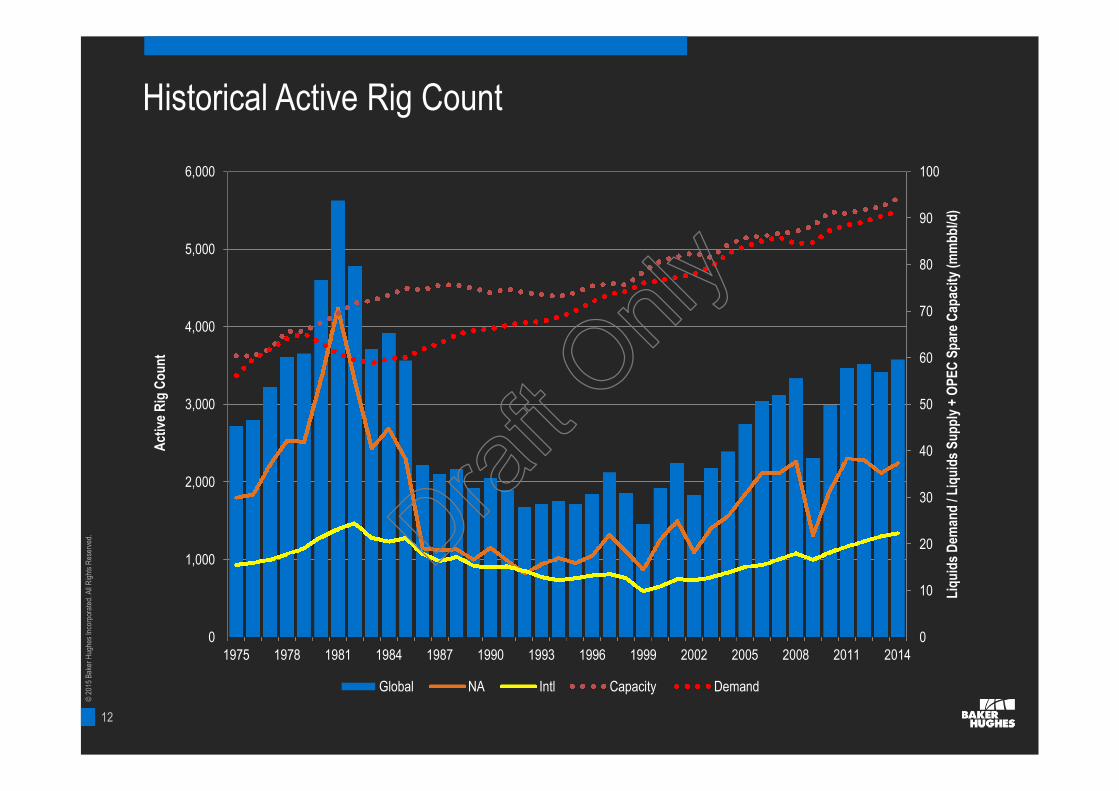

Historical Active Rig Count

0

10

20

30

40

50

60

70

80

90

100

0

1,000

2,000

3,000

4,000

5,000

6,000

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

Liq

uid

sD

eman

d/L

iqu

ids

Su

pp

ly+

OP

EC

Sp

are

Cap

acit

y(m

mb

bl/d

)

Act

ive

Rig

Co

un

t

Global NA Intl Capacity Demand

Draft O

nly

13

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

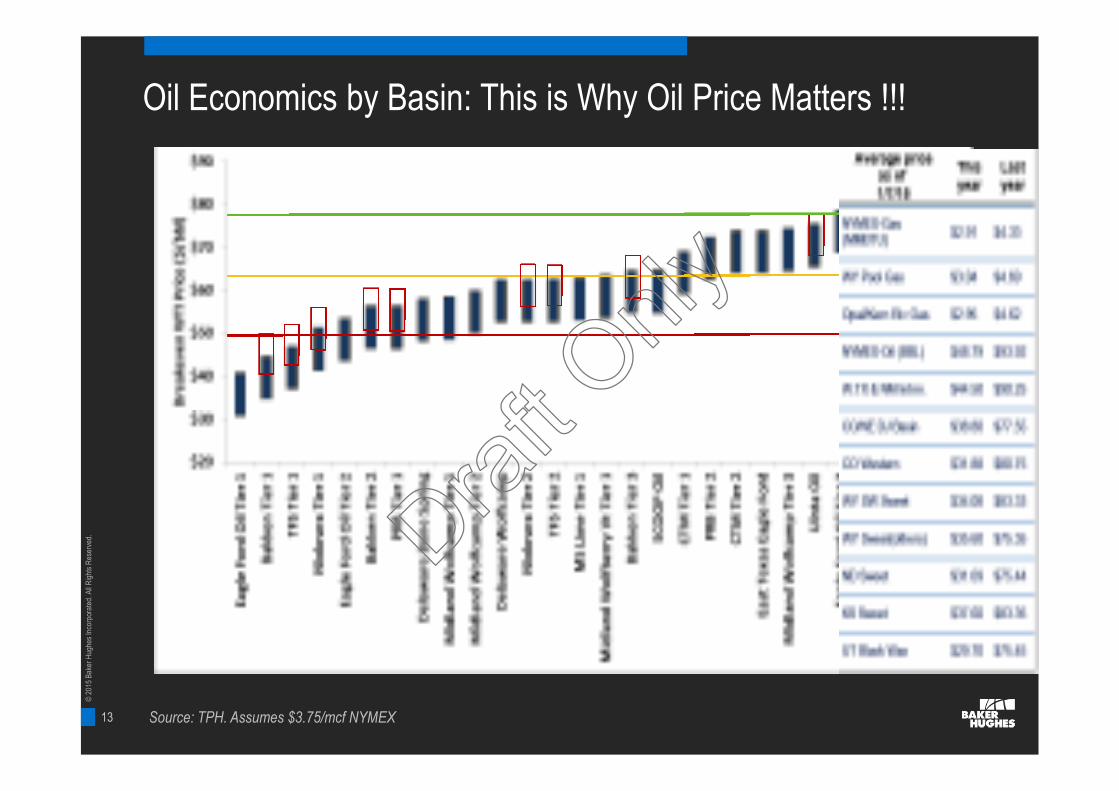

Oil Economics by Basin: This is Why Oil Price Matters !!!

Source: TPH. Assumes $3.75/mcf NYMEX

Draft O

nly

14

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

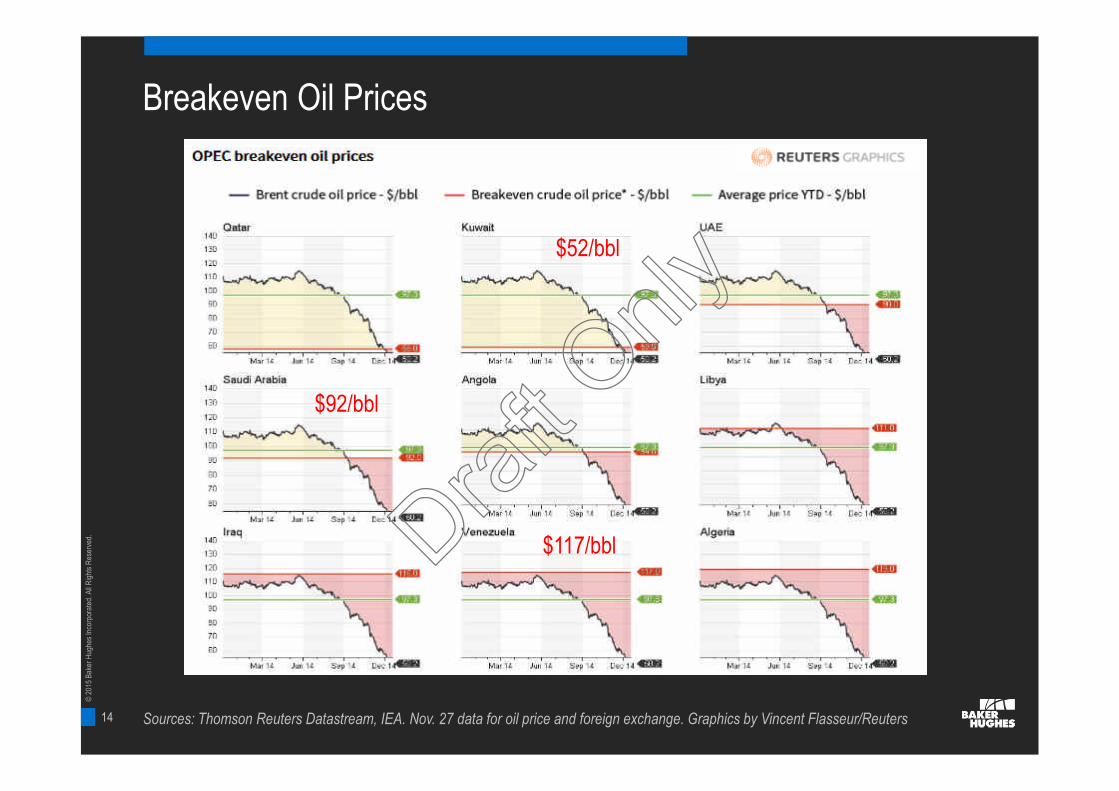

Sources: Thomson Reuters Datastream, IEA. Nov. 27 data for oil price and foreign exchange. Graphics by Vincent Flasseur/Reuters

Breakeven Oil Prices

$92/bbl

$117/bbl

$52/bbl

Draft O

nly

15

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Increasing Demand in a Changing World

15

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d. Draft O

nly

16

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

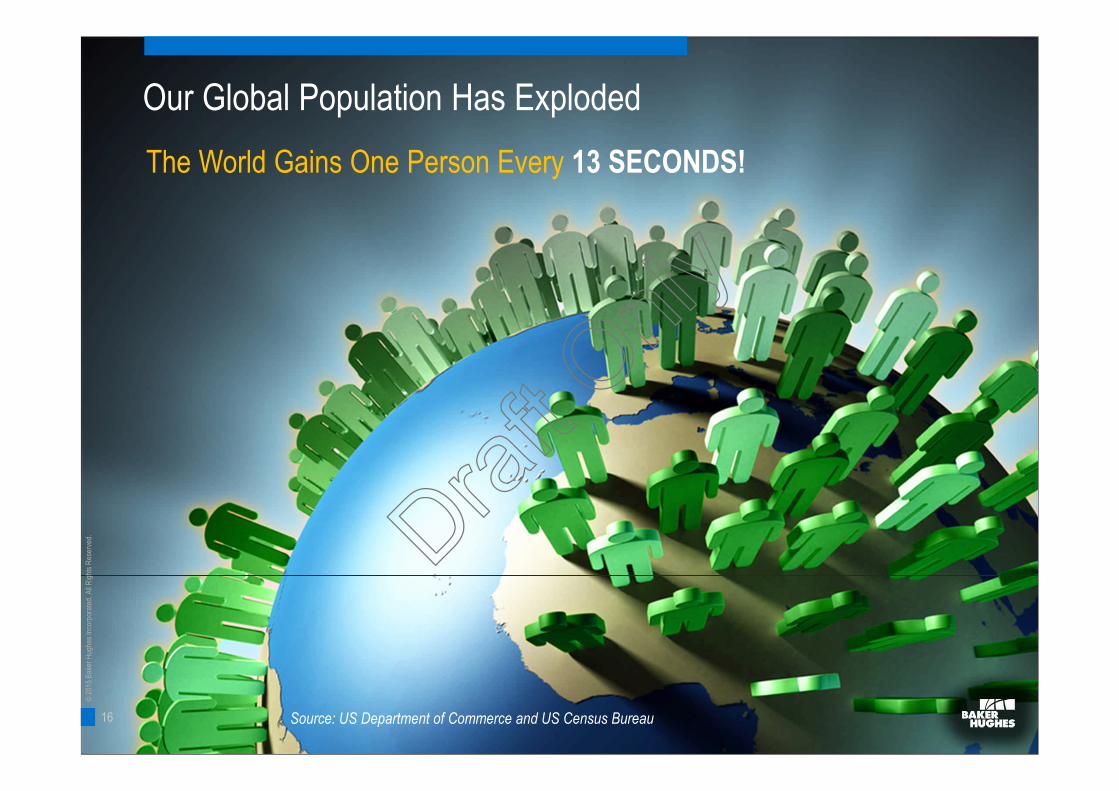

Our Global Population Has Exploded

Source: US Department of Commerce and US Census Bureau

The World Gains One Person Every 13 SECONDS!

16

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d. Draft O

nly

17

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Our Global Population Has Exploded

Source: U.S. Department of Commerce and U.S. Census Bureau

2014 – 7.3 Billion

Draft O

nly

18

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

18

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Beijing, China: 21,000,000 People

Draft O

nly

19

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

19

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

19

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Sao Paulo, Brazil: 12,000,000 People

Draft O

nly

20

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Source: Reuters, July 16, 201420

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

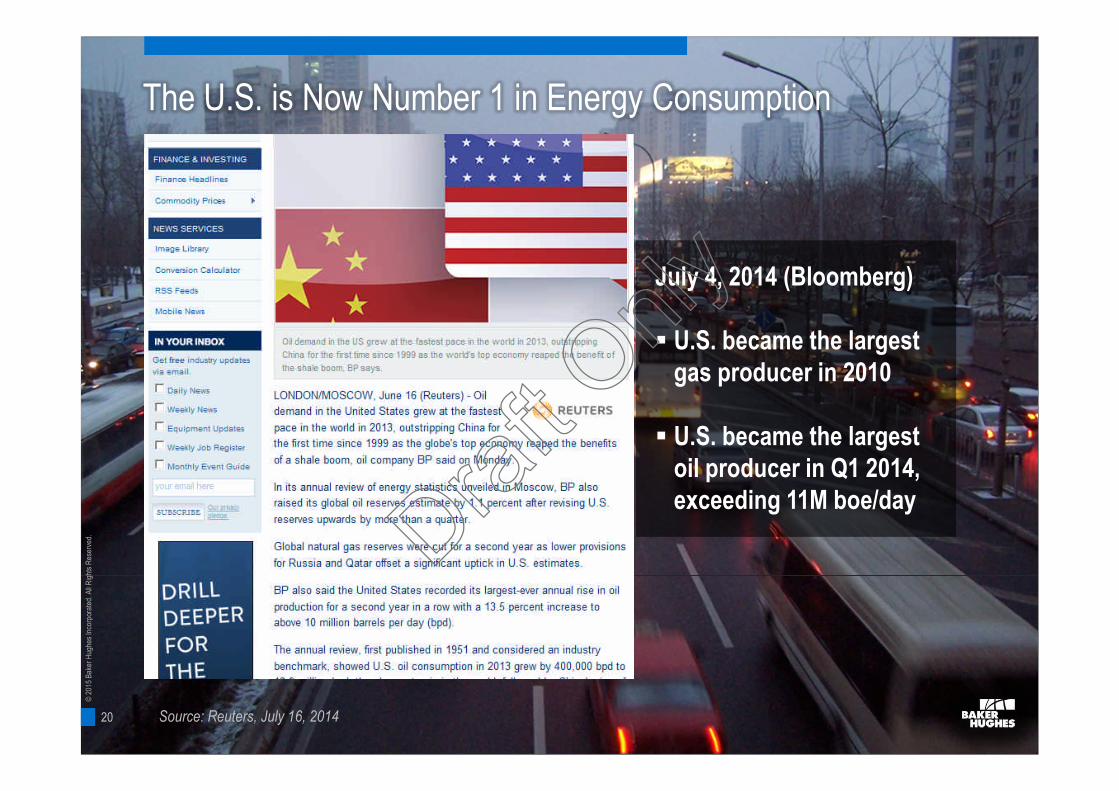

The U.S. is Now Number 1 in Energy Consumption

July 4, 2014 (Bloomberg)

U.S. became the largestgas producer in 2010

U.S. became the largestoil producer in Q1 2014,exceeding 11M boe/dayDraf

t Only

21

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

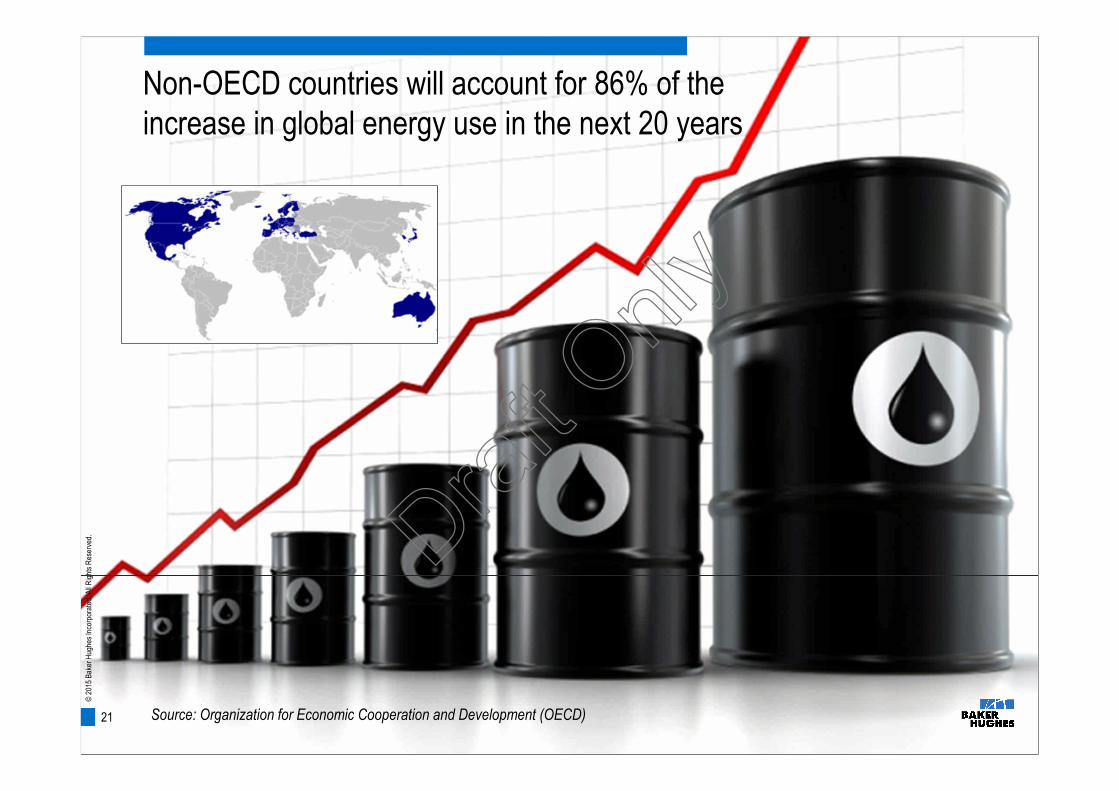

d.Non-OECD countries will account for 86% of theincrease in global energy use in the next 20 years

Source: Organization for Economic Cooperation and Development (OECD)21

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d. Draft O

nly

22

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

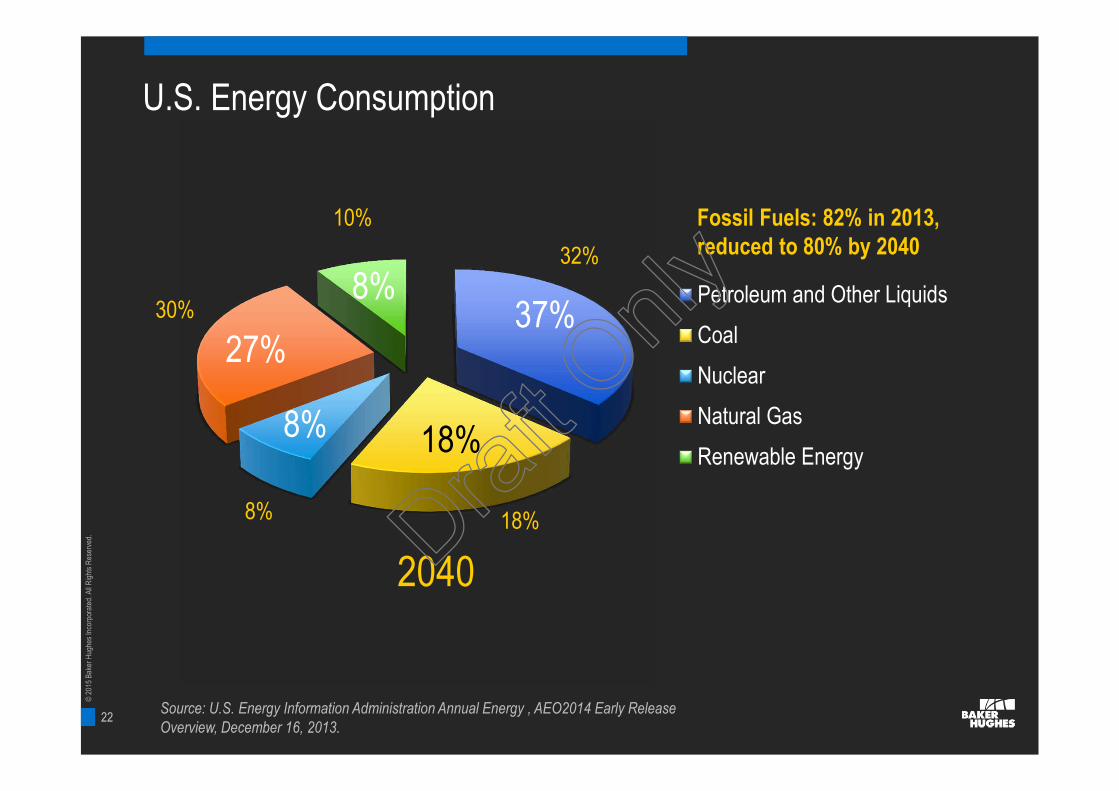

37%

18%8%

27%

8% Petroleum and Other Liquids

Coal

Nuclear

Natural Gas

Renewable Energy

Source: U.S. Energy Information Administration Annual Energy , AEO2014 Early ReleaseOverview, December 16, 2013.

U.S. Energy Consumption

2040

32%

18%8%

30%

10% Fossil Fuels: 82% in 2013,reduced to 80% by 2040

Draft O

nly

23

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Our Customer Base is Evolving

IOCIOC NOCNOC IndependentsIndependents

Draft O

nly

24

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

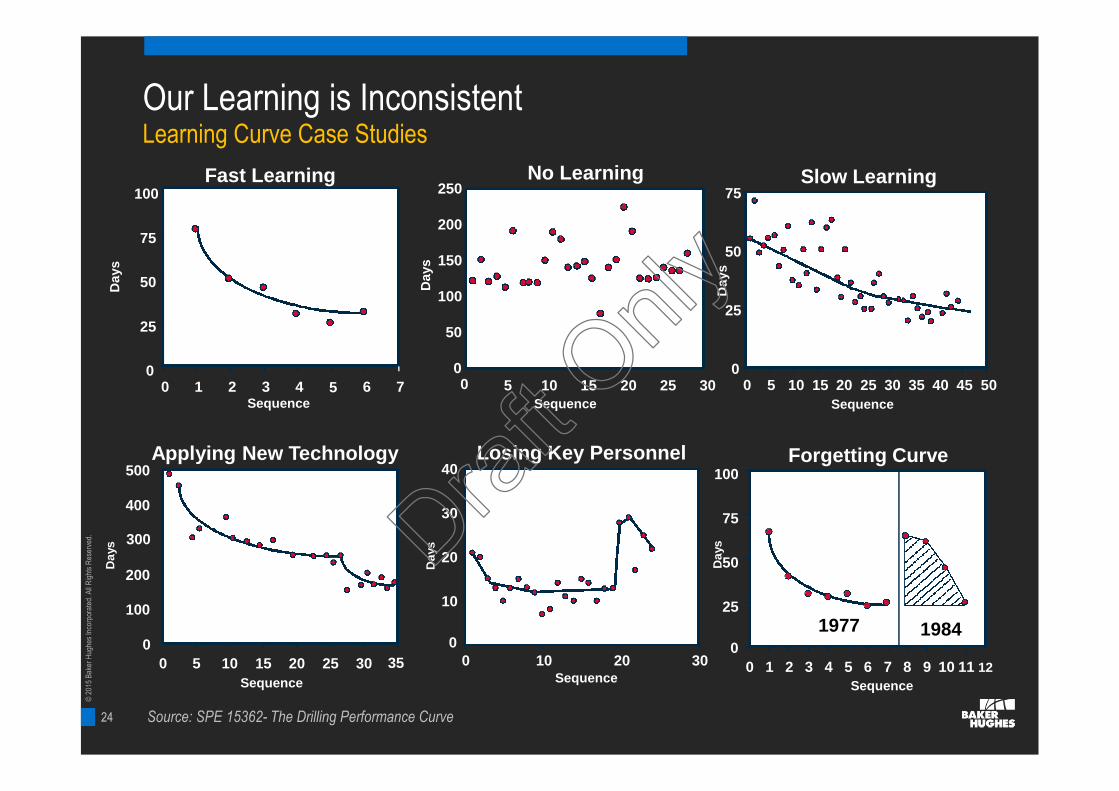

Our Learning is InconsistentLearning Curve Case Studies

35

Sequence

Da

ys

Applying New Technology Losing Key Personnel Forgetting Curve

Sequence

Days

0

50

100

150

200

250

0 5 10 15 20 25 30

No Learning

Days

Sequence

0

25

50

75

100

0 1 2 3 4 5 6 7

Fast Learning

Sequence

0

25

50

75

0 5 10 15 20 25 30 35 40 45 50

Slow Learning

Da

ys

1977 19840

25

50

75

100

0 1 2 3 4 5 6 7 8 9 10 11 12

Sequence

0

10

20

30

40

0 10 20 30Sequence

Days

Source: SPE 15362- The Drilling Performance Curve

0

100

200

400

500

0 5 10 15 20 25 30

Da

ys 300 Draf

t Only

25

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

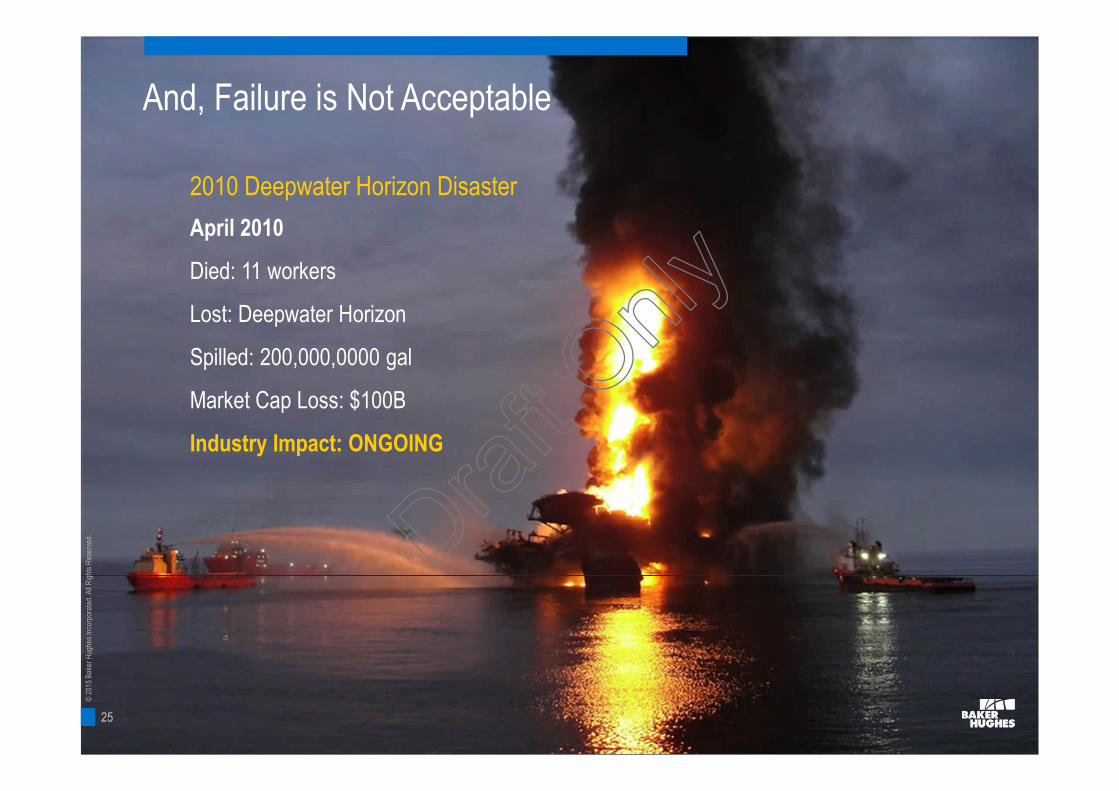

And, Failure is Not Acceptable

2010 Deepwater Horizon Disaster

April 2010

Died: 11 workers

Lost: Deepwater Horizon

Spilled: 200,000,0000 gal

Market Cap Loss: $100B

Industry Impact: ONGOING

25

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d. Draft O

nly

26

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

What Lies Ahead?

26

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d. Draft O

nly

27

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

The Future?

It is no longer about drilling “further and faster”

It is about Safety, Consistency and Cost of Ownership

Key Pathways

Reservoir

Digital

Materials

Automation

Science

Draft O

nly

28

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Reservoir Challenges

Even after all of these enhanced oil recovery steps (primary, secondary and tertiary)have been taken, it is still not uncommon for 60 – 70% of the original oil to be left in thereservoir. So, if you think about that, there are billions of barrels of discovered oil thatwe’re leaving in place. Unconventional reservoirs are worse, averaging 90%.

“In the past 100 years – in all of human history – we have consumed 1 trillion barrels ofoil. There are several times that much here,” said Roger Day, vice president foroperations for American Shale Oil (AMSO).

The oil shale deposits found on federal lands in Colorado, Utah and Wyoming containan estimated 4.285 trillion barrels of oil in place according to the U.S. GeologicalSurvey — enough to sustain America’s fuel needs for over a century.Draf

t Only

29

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Well Construction: With RSS or RNS

Draft O

nly

30

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

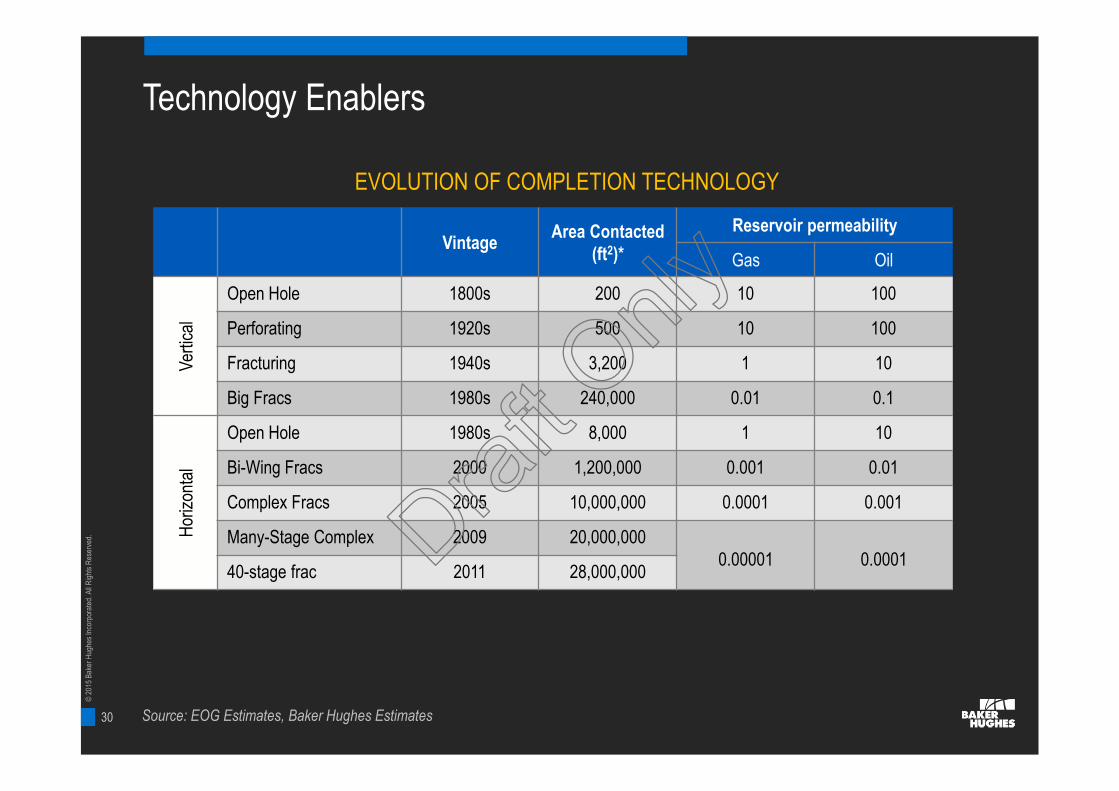

Technology Enablers

VintageArea Contacted

(ft2)*

Reservoir permeability

Gas Oil

Ver

tical

Open Hole 1800s 200 10 100

Perforating 1920s 500 10 100

Fracturing 1940s 3,200 1 10

Big Fracs 1980s 240,000 0.01 0.1

Hor

izon

tal

Open Hole 1980s 8,000 1 10

Bi-Wing Fracs 2000 1,200,000 0.001 0.01

Complex Fracs 2005 10,000,000 0.0001 0.001

Many-Stage Complex 2009 20,000,0000.00001 0.0001

40-stage frac 2011 28,000,000

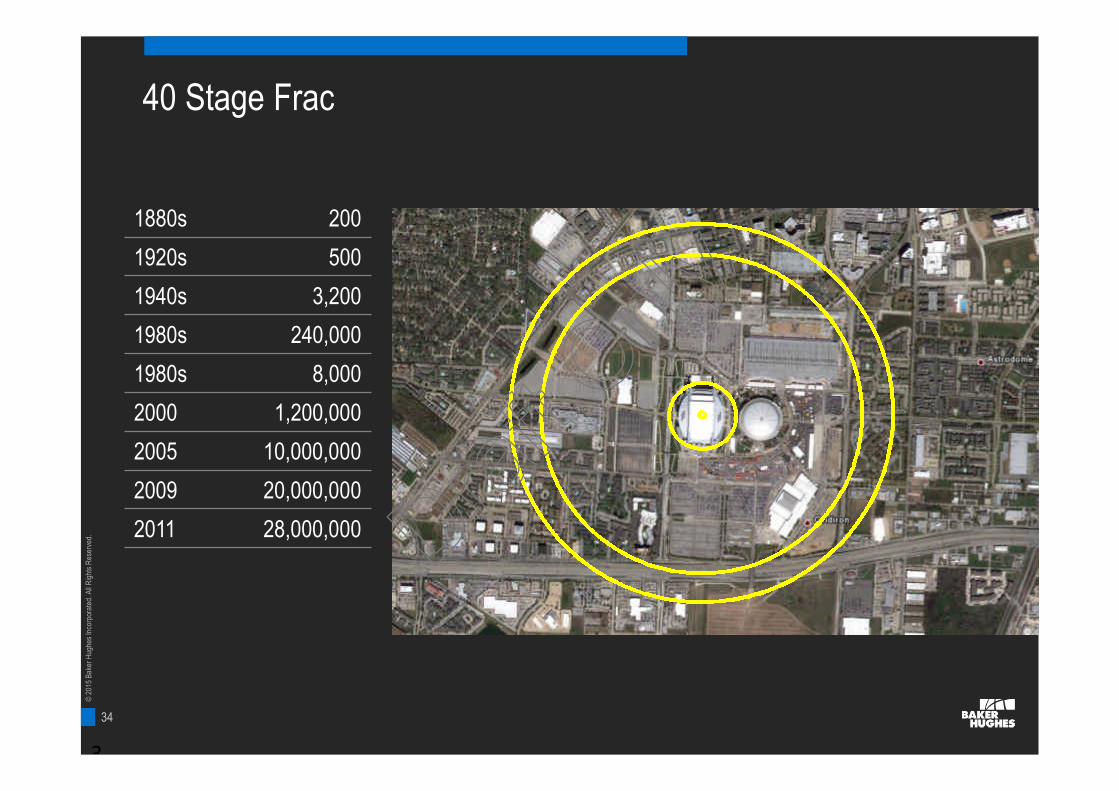

EVOLUTION OF COMPLETION TECHNOLOGY

Source: EOG Estimates, Baker Hughes Estimates

Draft O

nly

31

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

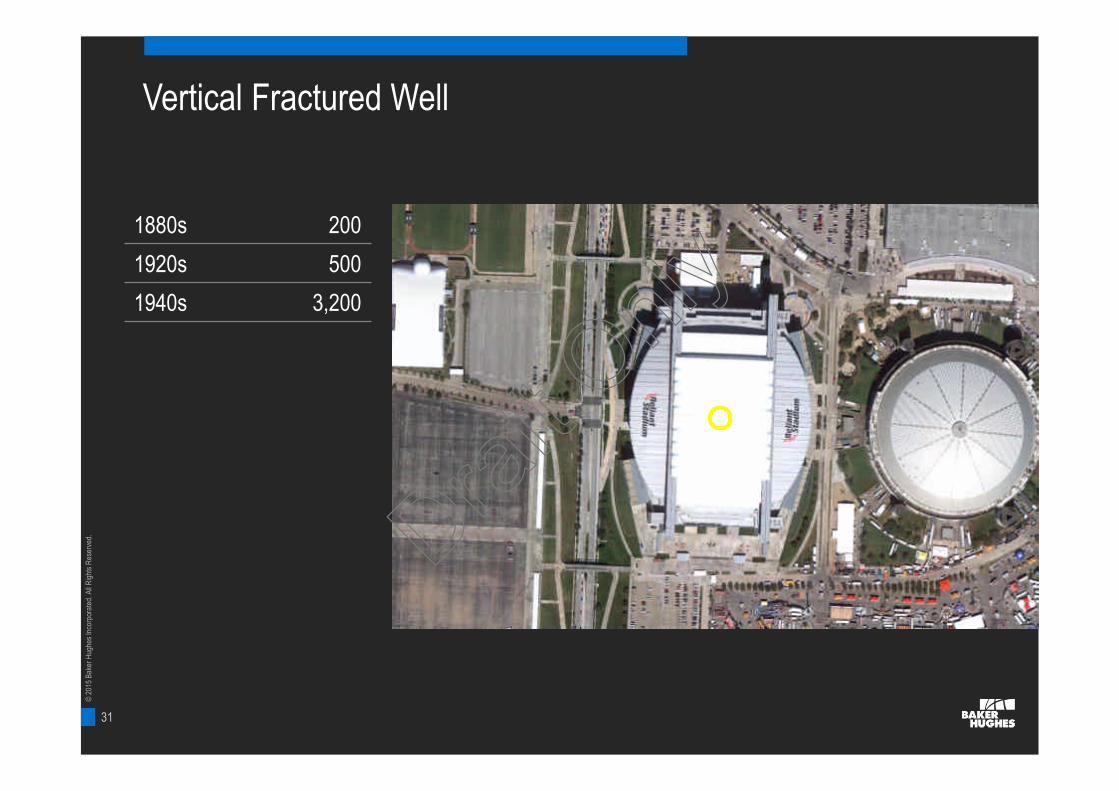

Vertical Fractured Well

1880s 200

1920s 500

1940s 3,200

Draft O

nly

32

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

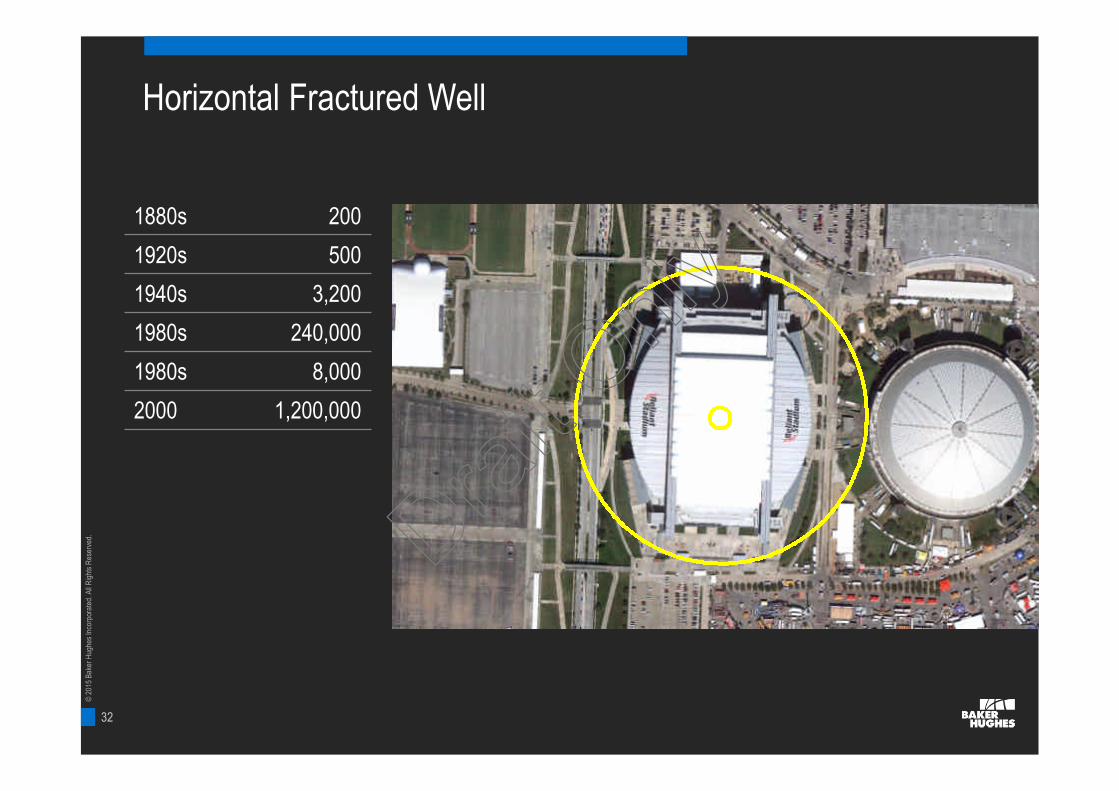

Horizontal Fractured Well

1880s 200

1920s 500

1940s 3,200

1980s 240,000

1980s 8,000

2000 1,200,000

Draft O

nly

33

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

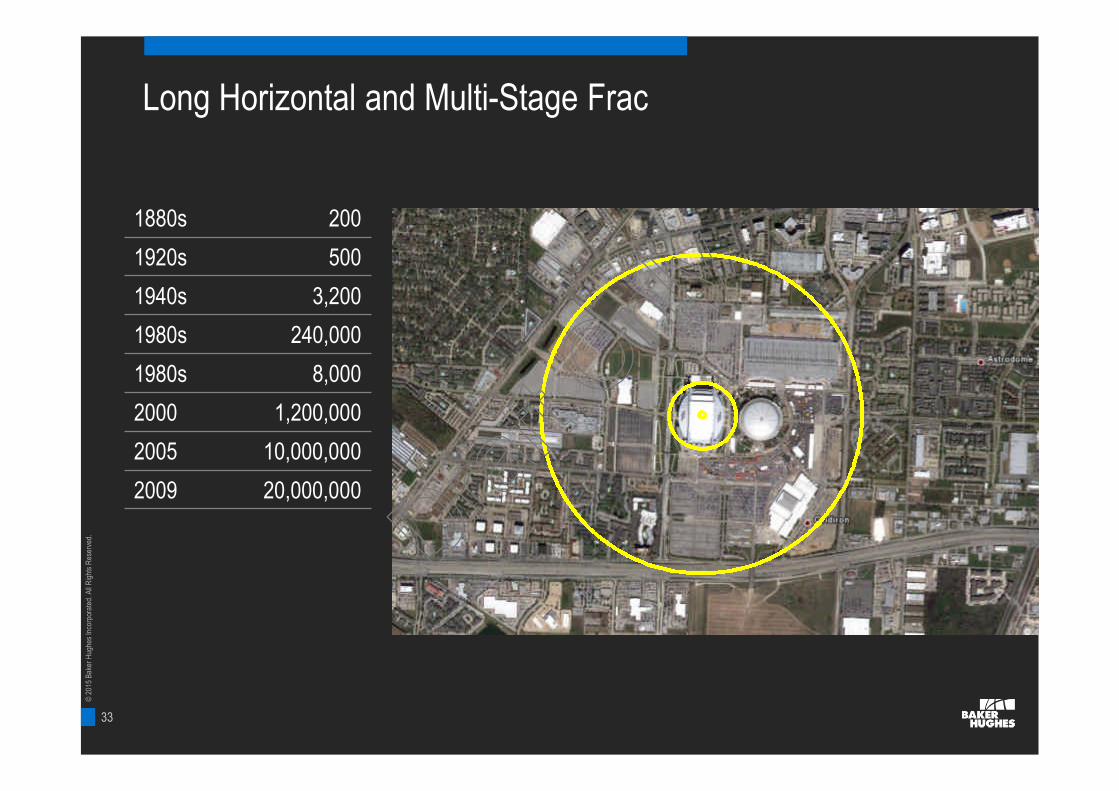

Long Horizontal and Multi-Stage Frac

1880s 200

1920s 500

1940s 3,200

1980s 240,000

1980s 8,000

2000 1,200,000

2005 10,000,000

2009 20,000,000

Draft O

nly

34

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

40 Stage Frac

3

1880s 200

1920s 500

1940s 3,200

1980s 240,000

1980s 8,000

2000 1,200,000

2005 10,000,000

2009 20,000,000

2011 28,000,000 Draft O

nly

35

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

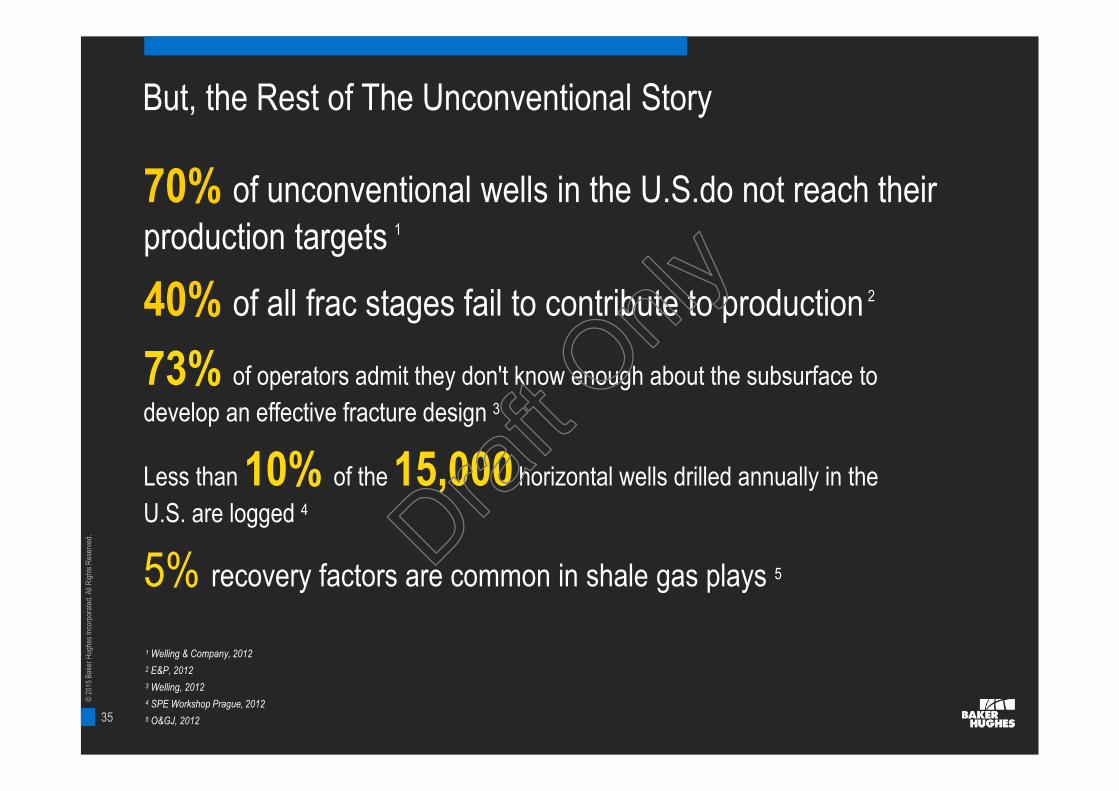

But, the Rest of The Unconventional Story

70% of unconventional wells in the U.S.do not reach their

production targets 1

40% of all frac stages fail to contribute to production 2

73% of operators admit they don't know enough about the subsurface to

develop an effective fracture design 3

Less than 10% of the 15,000 horizontal wells drilled annually in the

U.S. are logged 4

5% recovery factors are common in shale gas plays 5

1 Welling & Company, 2012

2 E&P, 2012

3 Welling, 2012

4 SPE Workshop Prague, 2012

5 O&GJ, 2012

Draft O

nly

36

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

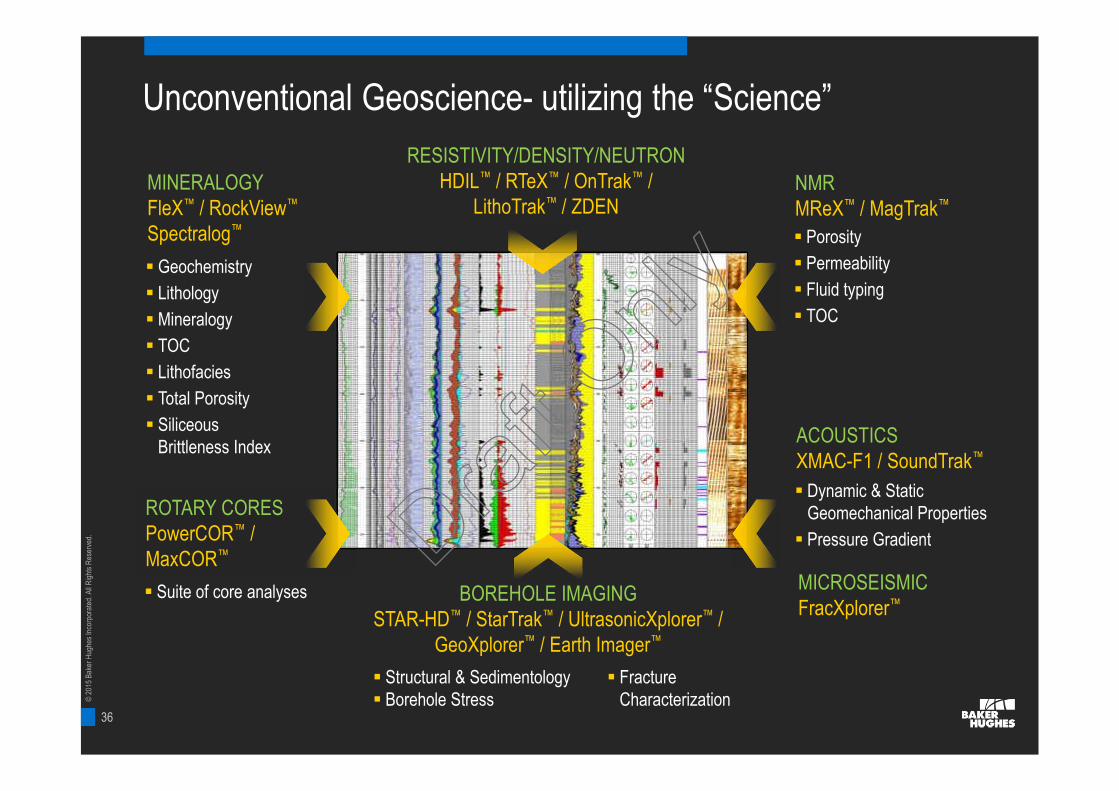

Unconventional Geoscience- utilizing the “Science”

Geochemistry

Lithology

Mineralogy

TOC

Lithofacies

Total Porosity

SiliceousBrittleness Index

Porosity

Permeability

Fluid typing

TOC

Dynamic & StaticGeomechanical Properties

Pressure Gradient

Suite of core analyses

ROTARY CORESPowerCOR™ /MaxCOR™

MINERALOGYFleX™ / RockView™

Spectralog™

MICROSEISMICFracXplorer™

ACOUSTICSXMAC-F1 / SoundTrak™

NMRMReX™ / MagTrak™

BOREHOLE IMAGINGSTAR-HD™ / StarTrak™ / UltrasonicXplorer™ /

GeoXplorer™ / Earth Imager™

RESISTIVITY/DENSITY/NEUTRONHDIL™ / RTeX™ / OnTrak™ /

LithoTrak™ / ZDEN

Structural & Sedimentology Borehole Stress

FractureCharacterization

Draft O

nly

37

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

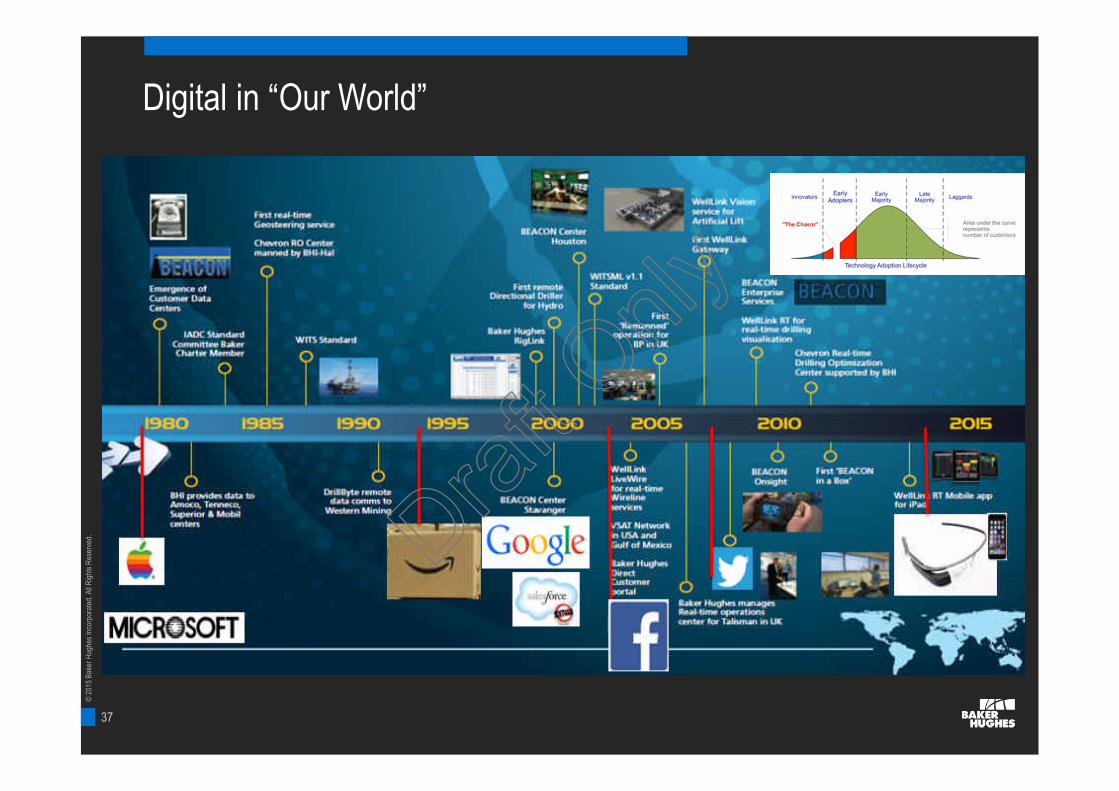

Digital in “Our World”

Draft O

nly

38

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

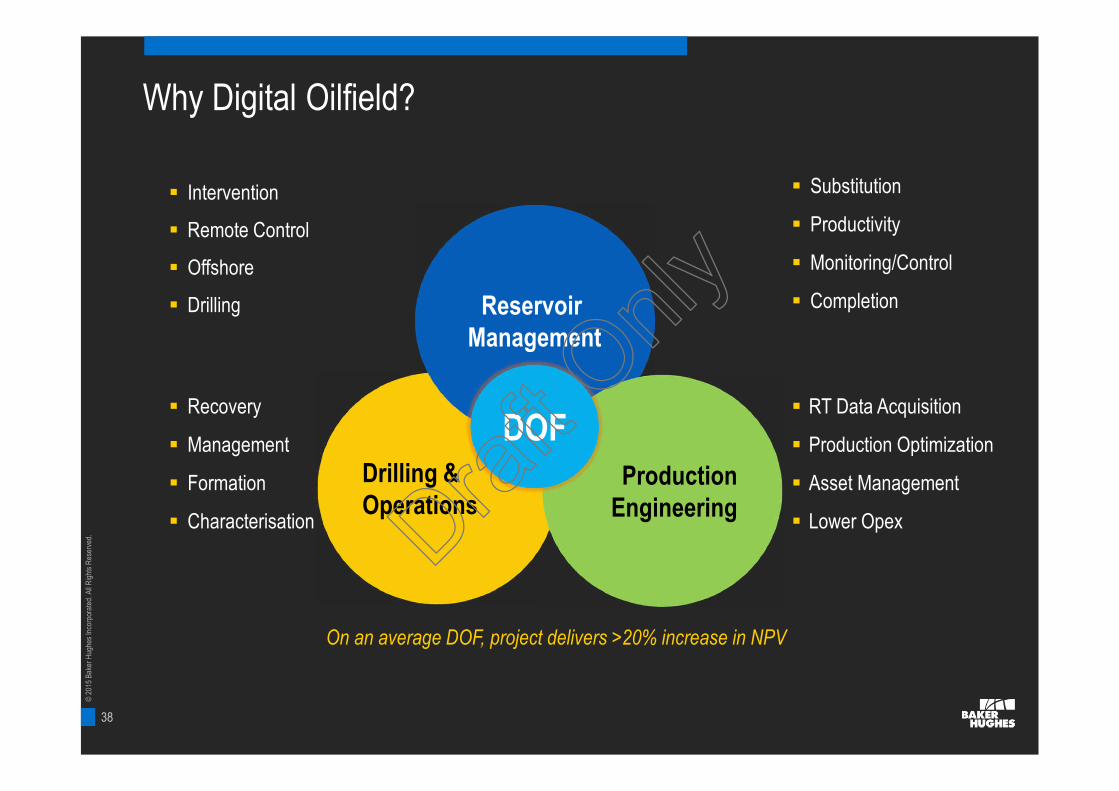

Why Digital Oilfield?

On an average DOF, project delivers >20% increase in NPV

Drilling &Operations

ReservoirManagement

ProductionEngineering

DOF

Intervention

Remote Control

Offshore

Drilling

Substitution

Productivity

Monitoring/Control

Completion

Recovery

Management

Formation

Characterisation

RT Data Acquisition

Production Optimization

Asset Management

Lower OpexDraft O

nly

39

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

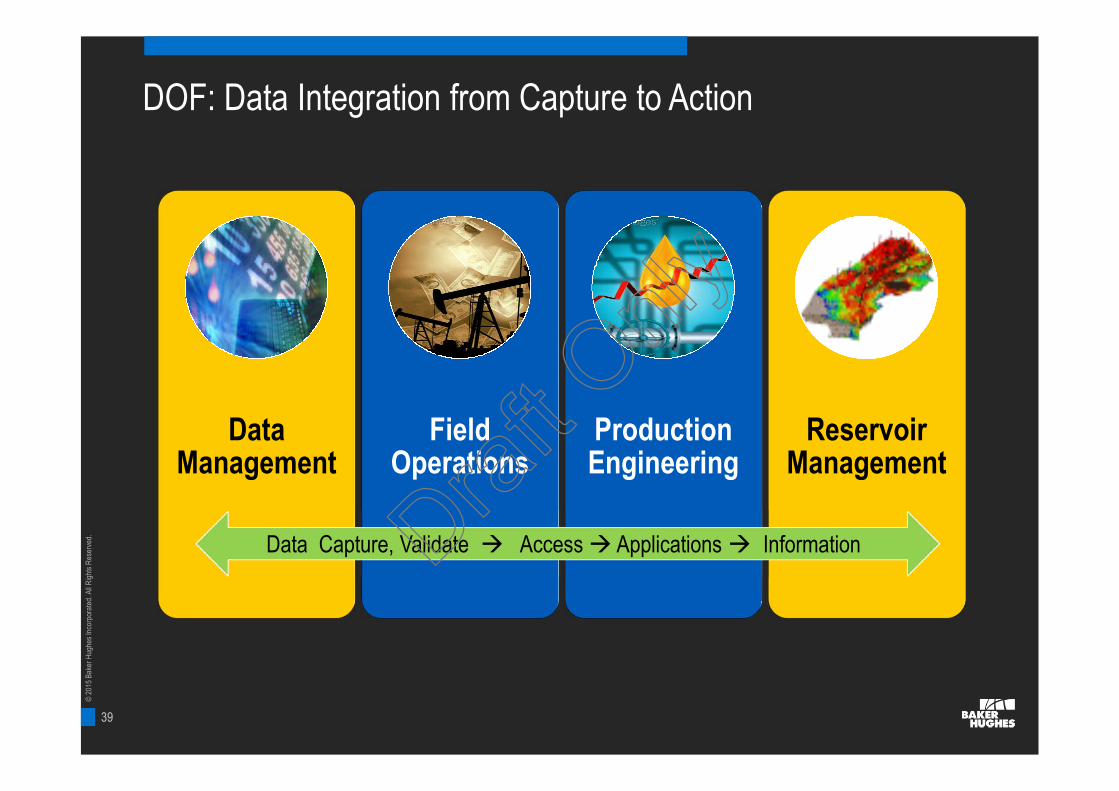

DOF: Data Integration from Capture to Action

DataManagement

FieldOperations

ProductionEngineering

ReservoirManagement

Data Capture, Validate Access Applications InformationDraft O

nly

40

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Moving from a Legacy of Data and Application Silos

3rd Parties3rd Parties Equipment VendorsEquipment Vendors

Shore SupportShore Support

OperatorOperator Rig OwnerRig Owner Service Company 1Service Company 1

Service Company 2Service Company 2

Sensors & SystemsSensors & Systems

Video

Fire &Safety

EGIS

MaintenanceSystems

Audio

WeatherAlerts

Radar

SCADA

Alarms

Access &Identity Mgmt.

PanicButton

LPR

Procedures

Draft O

nly

41

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

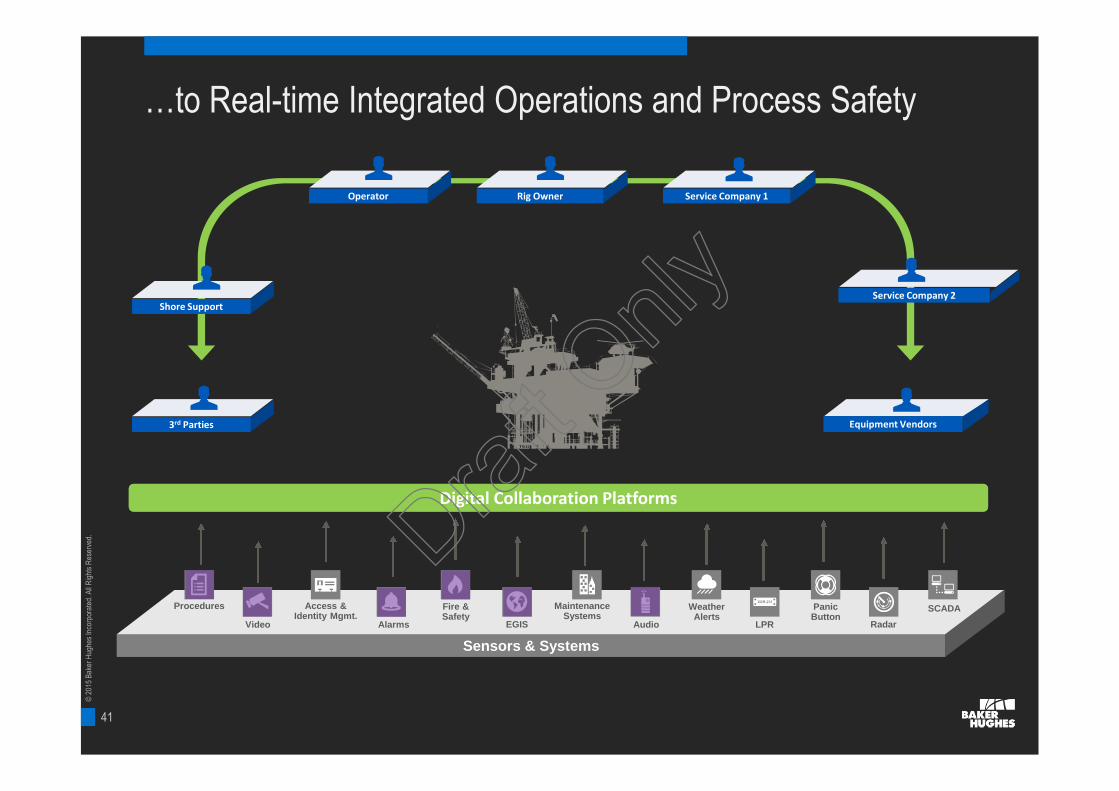

3rd Parties3rd Parties Equipment VendorsEquipment Vendors

Shore SupportShore Support

OperatorOperator Rig OwnerRig Owner Service Company 1Service Company 1

Service Company 2Service Company 2

Sensors & SystemsSensors & Systems

Video

Fire &Safety

EGIS

MaintenanceSystems

Audio

WeatherAlerts

Radar

SCADA

Alarms

Access &Identity Mgmt.

PanicButton

LPR

Procedures

Digital Collaboration PlatformsDigital Collaboration Platforms

…to Real-time Integrated Operations and Process Safety

Draft O

nly

42

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

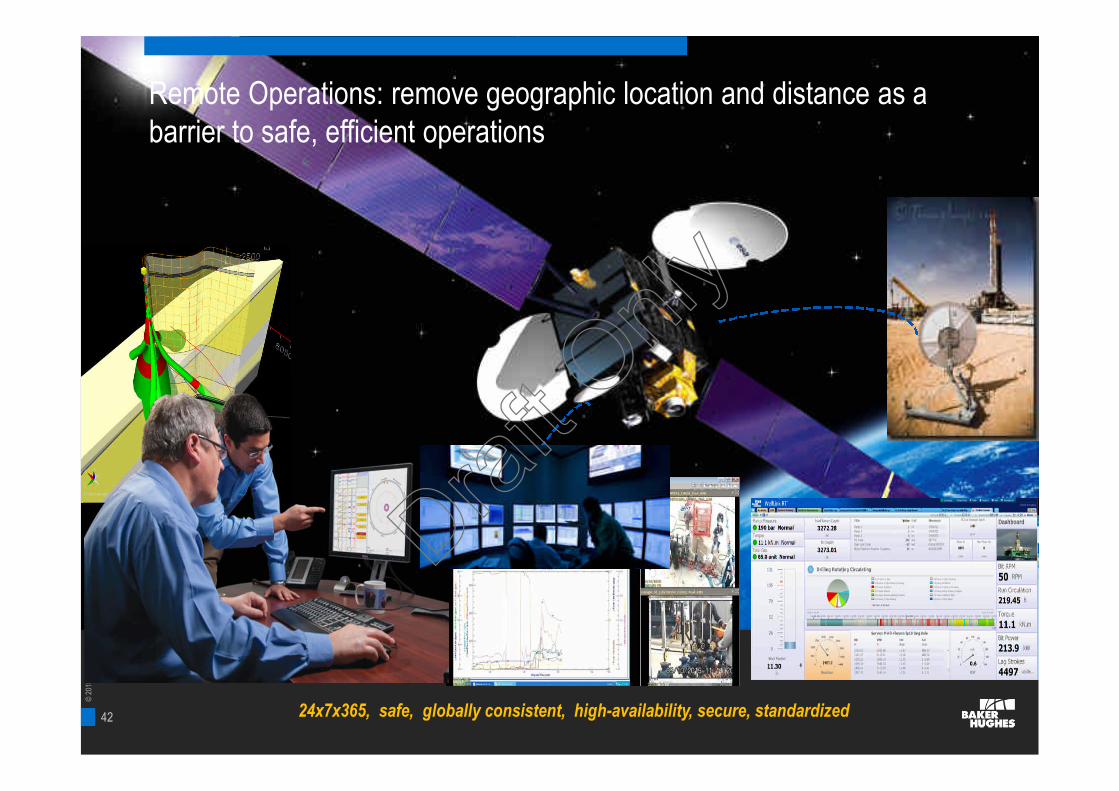

Remote Operations: remove geographic location and distance as abarrier to safe, efficient operations

24x7x365, safe, globally consistent, high-availability, secure, standardized

Draft O

nly

43

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

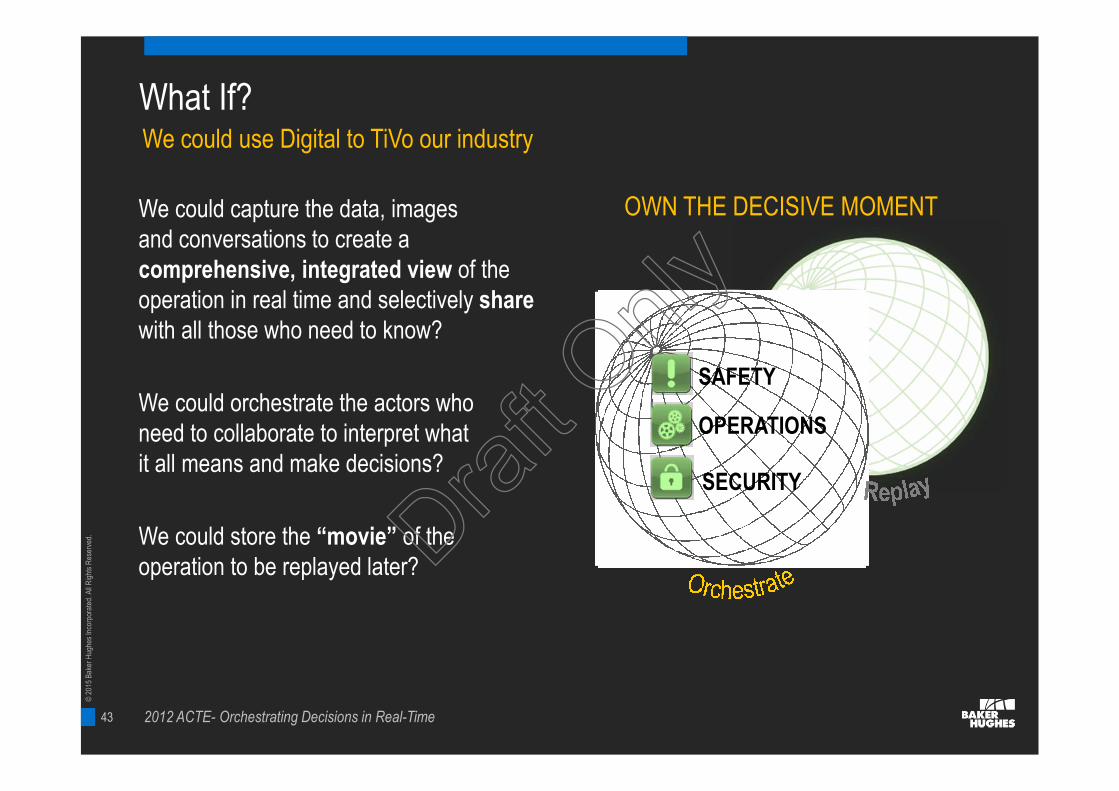

What If?

We could capture the data, imagesand conversations to create acomprehensive, integrated view of theoperation in real time and selectively sharewith all those who need to know?

We could orchestrate the actors whoneed to collaborate to interpret whatit all means and make decisions?

We could store the “movie” of theoperation to be replayed later?

We could use Digital to TiVo our industry

SAFETY

SECURITY

OPERATIONS

OWN THE DECISIVE MOMENT

2012 ACTE- Orchestrating Decisions in Real-Time

Draft O

nly

44

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Digital: Pathway to Global Knowledge

Knowledge

SkillsExperience

Behavior

What makes a person competent?

GOOGLE GLASS

Baker Hughes launched 160 new products in 2014.The pace of innovation is exponential.

A future of wearable “TECH”

How do we adopt digital enablement?

Draft O

nly

45

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

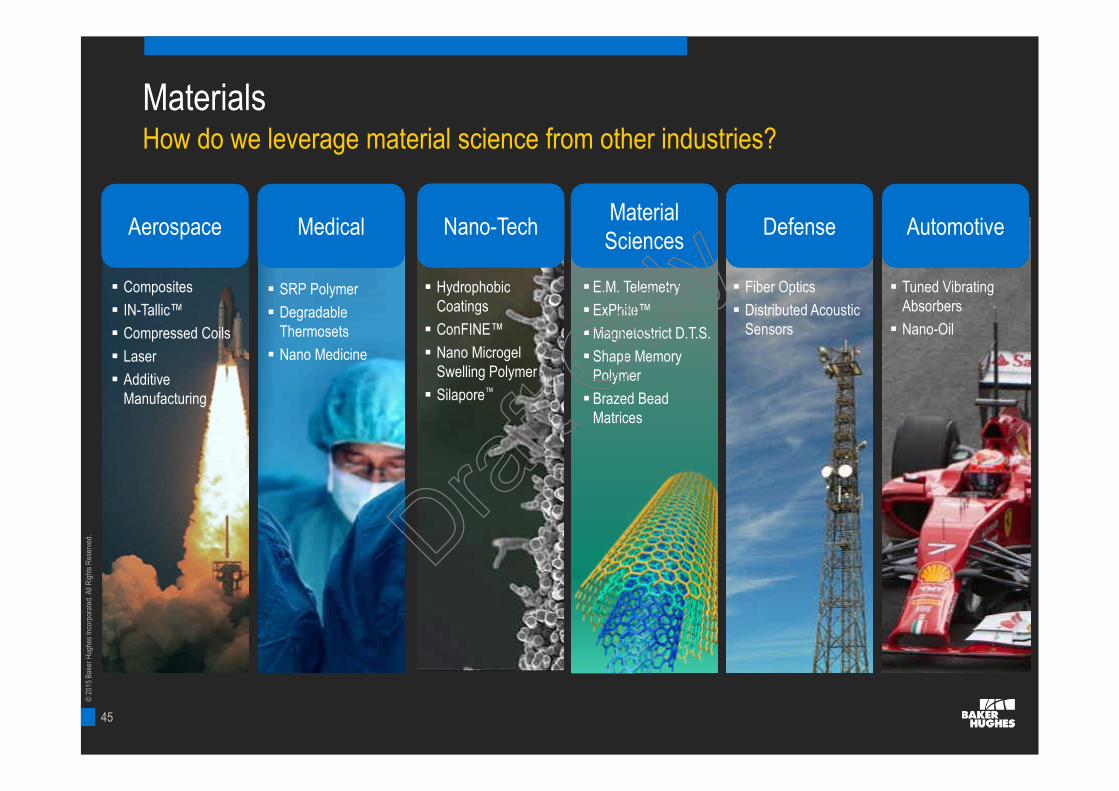

MaterialsHow do we leverage material science from other industries?

DefenseDefenseMaterialSciencesMaterialSciences

AerospaceAerospace

Composites

IN-Tallic™

Compressed Coils

Laser

AdditiveManufacturing

MedicalMedical

SRP Polymer

DegradableThermosets

Nano Medicine

Fiber Optics

Distributed AcousticSensors

E.M. Telemetry

ExPhite™

Magnetostrict D.T.S.

Shape MemoryPolymer

Brazed BeadMatrices

AutomotiveAutomotive

Tuned VibratingAbsorbers

Nano-Oil

Nano-TechNano-Tech

HydrophobicCoatings

ConFINE™

Nano MicrogelSwelling Polymer

Silapore™

Draft O

nly

46

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Materials

The next BIG game changers

High temperature electronics

Shape memory polymers

Wear resistant materials

Impact resistant materials

Nano engineered materials

– Sensors

– Chemicals

– Drilling materials

– Reservoir surveillance

The prefix nano, derived from the Latin word nanus for dwarf,means something very small. When we’re using it in metricterms, a nanometer is one-billionth of a meter. Think about that!Take a strand of hair and put at it between your fingers. Thewidth of that hair is 100,000 nanometers. A nanometer is abouthow much your fingernail grows every second. So a nanometeris really small.

Nanotechnology Helps 3-D TV Make a Comeback Without Glasses- Dexter Johnson post, Consumer Electronics Show

Draft O

nly

47

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

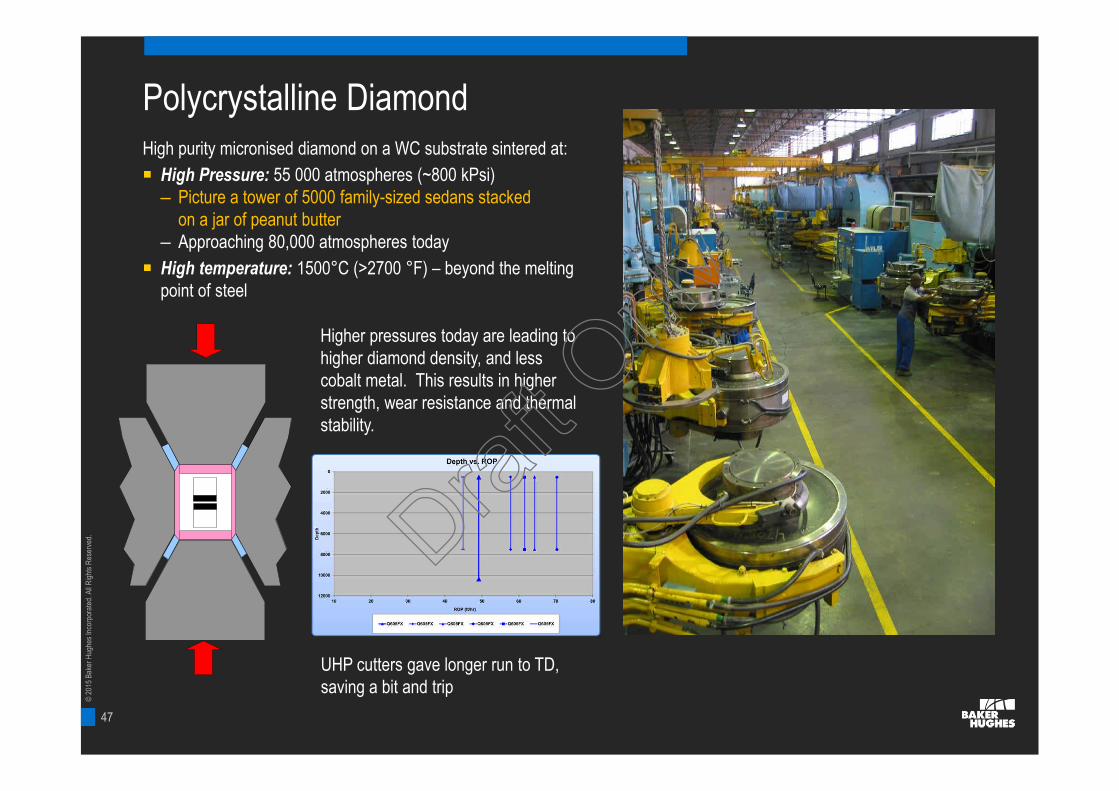

Polycrystalline DiamondHigh purity micronised diamond on a WC substrate sintered at:

■ High Pressure: 55 000 atmospheres (~800 kPsi)– Picture a tower of 5000 family-sized sedans stacked

on a jar of peanut butter– Approaching 80,000 atmospheres today

■ High temperature: 1500°C (>2700 °F) – beyond the meltingpoint of steel

Higher pressures today are leading tohigher diamond density, and lesscobalt metal. This results in higherstrength, wear resistance and thermalstability.

UHP cutters gave longer run to TD,saving a bit and trip

Draft O

nly

48

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

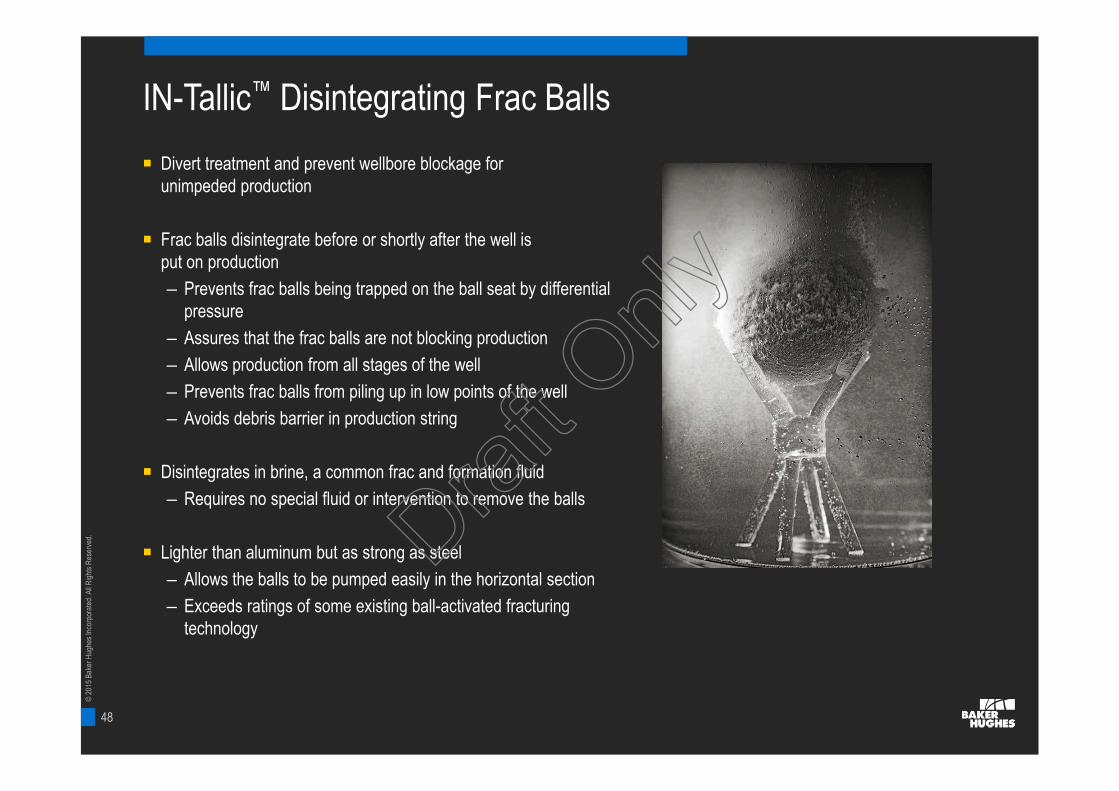

IN-Tallic™ Disintegrating Frac Balls

■ Divert treatment and prevent wellbore blockage forunimpeded production

■ Frac balls disintegrate before or shortly after the well isput on production

– Prevents frac balls being trapped on the ball seat by differentialpressure

– Assures that the frac balls are not blocking production

– Allows production from all stages of the well

– Prevents frac balls from piling up in low points of the well

– Avoids debris barrier in production string

■ Disintegrates in brine, a common frac and formation fluid

– Requires no special fluid or intervention to remove the balls

■ Lighter than aluminum but as strong as steel

– Allows the balls to be pumped easily in the horizontal section

– Exceeds ratings of some existing ball-activated fracturingtechnology

Draft O

nly

49

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

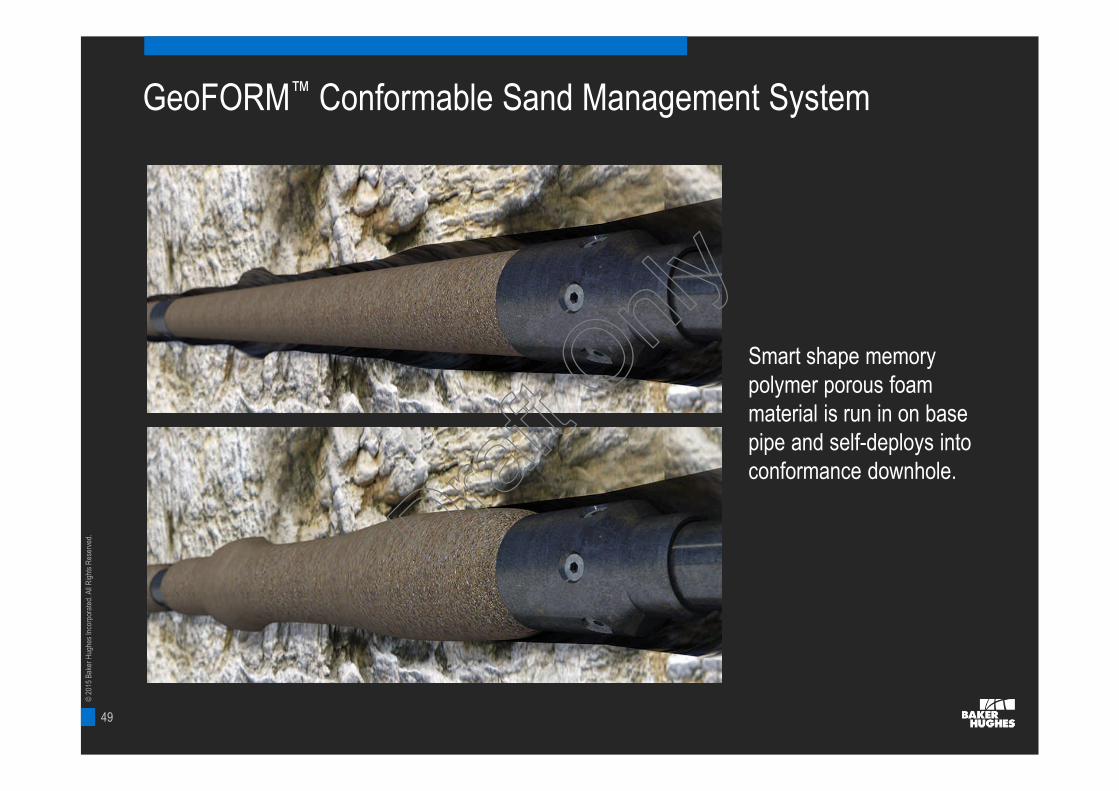

GeoFORM™ Conformable Sand Management System

Smart shape memorypolymer porous foammaterial is run in on basepipe and self-deploys intoconformance downhole.

Draft O

nly

50

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Automation

Many industries have acknowledged human limitations in managing repetitiveor complex tasks and they have turned to automation.

Automotive

Airline

Beverage and Food

Draft O

nly

51

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

Automation: The BIG Reason

We can train our brain

“Aoccdrnig to a rscheearch at Cmabrigde

Uinervtisy, it deosn't mttaer in waht oredr the

ltteers in a wrod are, the olny iprmoetnt tihng

is taht the frist and lsat ltteer be at the rghit

pclae. The rset can be a total mses and you

can sitll raed it wouthit porbelm. Thsi is

bcuseae the huamn mnid deos not raed ervey

lteter by istlef, but the wrod as a wlohe”

- But miss details due to routine

People make mistakes

Draft O

nly

52

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

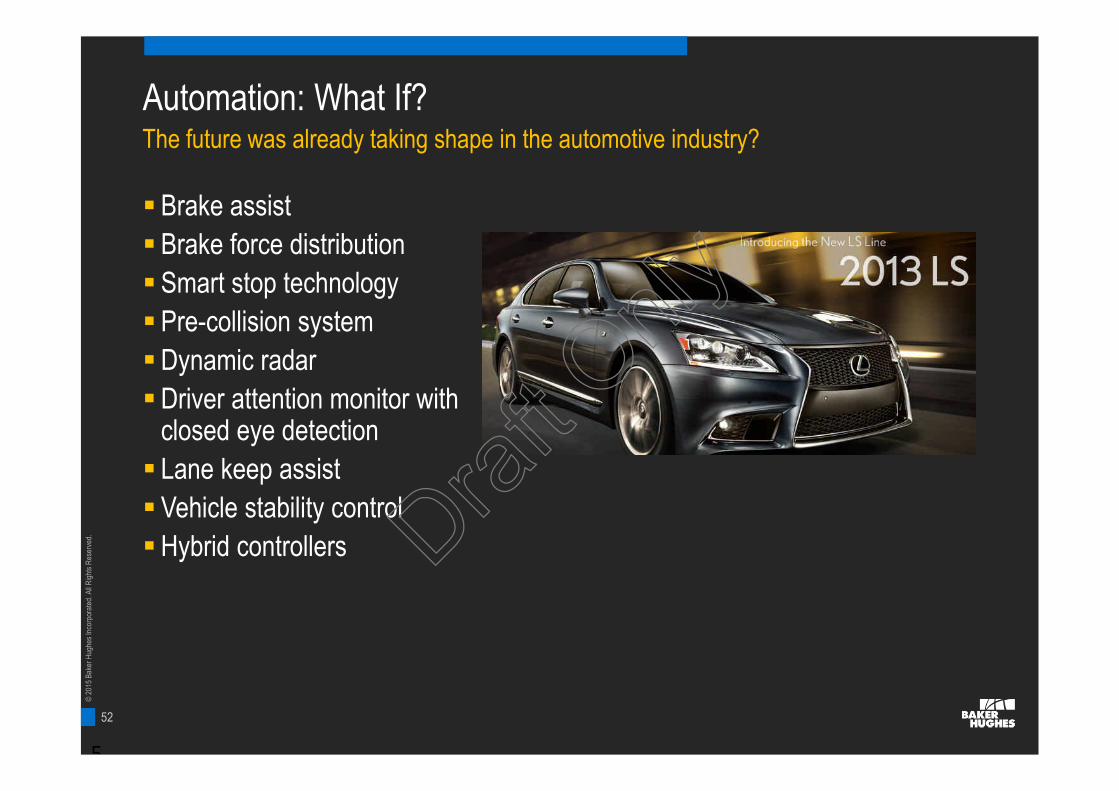

Automation: What If?

Brake assist

Brake force distribution

Smart stop technology

Pre-collision system

Dynamic radar

Driver attention monitor withclosed eye detection

Lane keep assist

Vehicle stability control

Hybrid controllers

5

The future was already taking shape in the automotive industry?

Draft O

nly

53

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

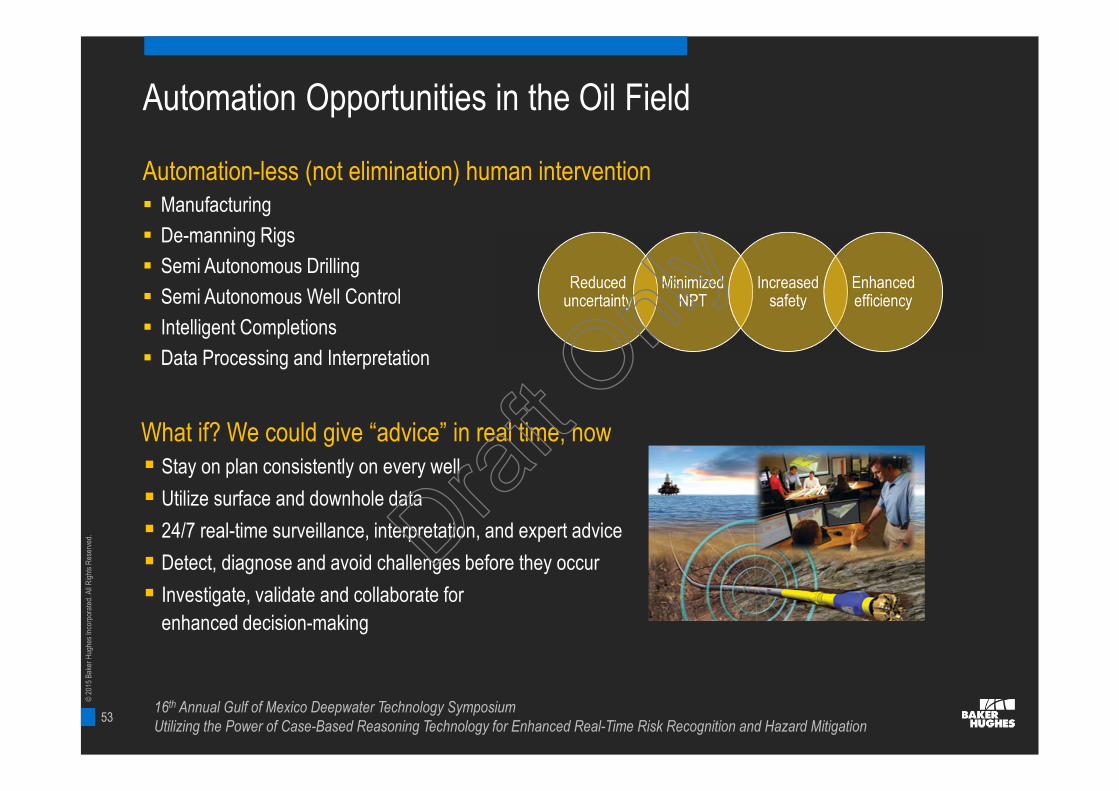

Automation Opportunities in the Oil Field

Automation-less (not elimination) human intervention Manufacturing

De-manning Rigs

Semi Autonomous Drilling

Semi Autonomous Well Control

Intelligent Completions

Data Processing and Interpretation

Stay on plan consistently on every well

Utilize surface and downhole data

24/7 real-time surveillance, interpretation, and expert advice

Detect, diagnose and avoid challenges before they occur

Investigate, validate and collaborate for

enhanced decision-making

What if? We could give “advice” in real time, now

16th Annual Gulf of Mexico Deepwater Technology SymposiumUtilizing the Power of Case-Based Reasoning Technology for Enhanced Real-Time Risk Recognition and Hazard Mitigation

Draft O

nly

54

©20

15B

aker

Hug

hes

Inco

rpor

ated

.All

Rig

hts

Res

erve

d.

© 2015 BAKER HUGHES INCORPORATED. ALL RIGHTS RESERVED. TERMS AND CONDITIONS OF USE: BY ACCEPTING THIS DOCUMENT, THE RECIPIENT AGREES THAT THE DOCUMENT TOGETHER WITH ALL INFORMATION INCLUDED THEREIN IS THECONFIDENTIAL AND PROPRIETARY PROPERTY OF BAKER HUGHES INCORPORATED AND INCLUDES VALUABLE TRADE SECRETS AND/OR PROPRIETARY INFORMATION OF BAKER HUGHES (COLLECTIVELY "INFORMATION"). BAKER HUGHES RETAINSALL RIGHTS UNDER COPYRIGHT LAWS AND TRADE SECRET LAWS OF THE UNITED STATES OF AMERICA AND OTHER COUNTRIES. THE RECIPIENT FURTHER AGREES THAT THE DOCUMENT MAY NOT BE DISTRIBUTED, TRANSMITTED, COPIED ORREPRODUCED IN WHOLE OR IN PART BY ANY MEANS, ELECTRONIC, MECHANICAL, OR OTHERWISE, WITHOUT THE EXPRESS PRIOR WRITTEN CONSENT OF BAKER HUGHES, AND MAY NOT BE USED DIRECTLY OR INDIRECTLY IN ANY WAY DETRIMENTALTO BAKER HUGHES’ INTEREST.

Working Smarter, Not HarderThe Role of Innovation in Oil and Gas

Allen SinorVice President, Global AccountsBaker Hughes

4-6 February, 2015

SPE Gulf Coast Section2015 Student Summit

Draft O

nly