2015 annual report - kuke.com.pl · kuke finance s.a. | 2015 annual report 7 on 22 december 2014,...

TRANSCRIPT

2015 AnnuAl RepoRt

2 2015 AnnuAl RepoRt

letteR FRoM the pResident oF the MAnAgeMent BoARd

MAcRoeconoMic conditions in 2015

doMestic deMAnd

eXpoRt

doMestic MARket

oRgAnisAtion

shAReholdeRs And shARe cApitAl

MAnAgeMent BoARd

supeRvisoRy BoARd

kuke FinAnce s.A.

peRFoRMAnce oF kuke s.A.in specific business areas

geneRAl Results

geogRAphic stRuctuRe

AgReeMents

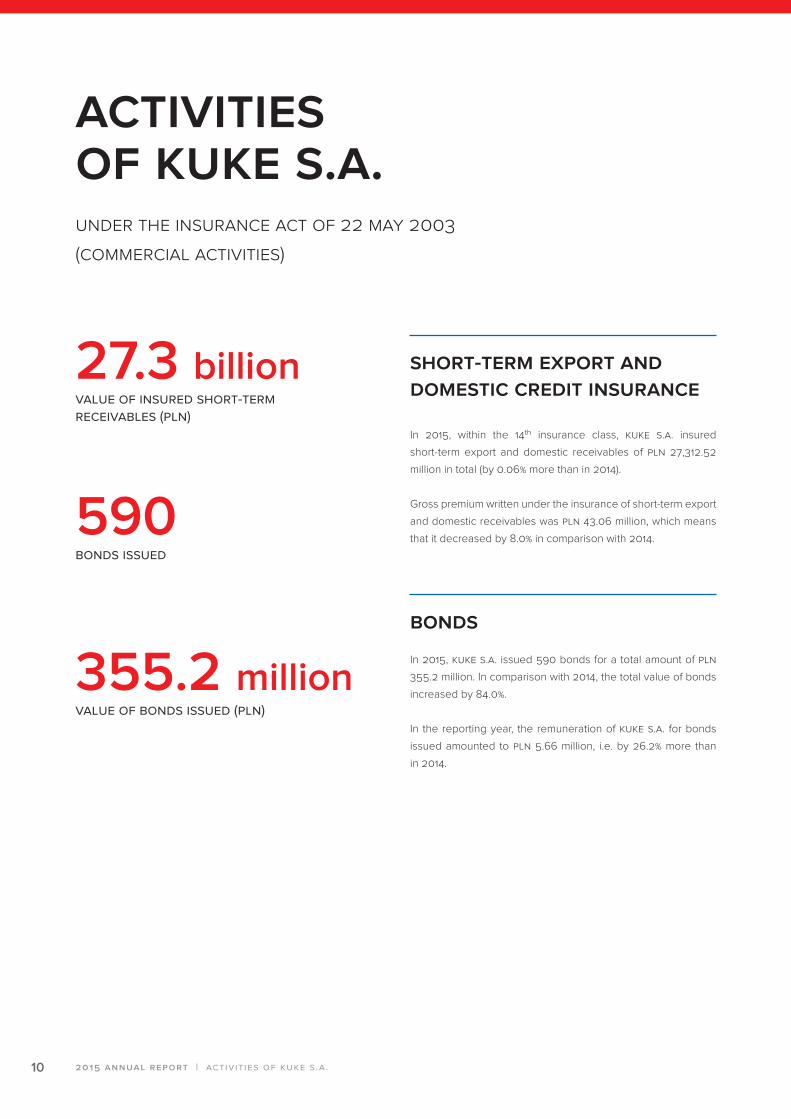

Activities oF kuke s.A. under the insurance act of 22 May 2003

(coMMercial activities)

shoRt-teRM eXpoRt And doMestic cRedit insuRAnce

Bonds

Activities oF kuke s.A. under the act on export insurance backed

by the state treasury of 7 July 1994

FinAnciAl Results

AnAlysis oF the BAlAnce sheet

Assets

equity And liABilities

AnAlysis oF technicAl insuRAnce Account And oveRAll pRoFit And loss Account

dAtA tABles

Assets

equity And liABilities

technicAl Account oF pRopeRty And cAsuAlty insuRAnce

geneRAl pRoFit And loss Account

stAteMent oF cAsh FloWs

solvency pARAMeteRs

tABle oF contents

32015 AnnuAl RepoRt

Dear Sirs and Madams,

It is my great pleasure to present to you the Annual Report

of the Export Credit Insurance Corporation Joint Stock

Company (KUKE S.A.), where you will find the effects of

our work and the results we have achieved in 2015.

As a Polish company and a national insurer of receiva-

bles, we have been supporting the effective trade ex-

change of entrepreneurs on both foreign and domestic

markets for 25 years now. Our insurance facilities meet

the highest international standards while the compre-

hensiveness of our offer is comparable with that of other

export credit agencies around the world.

Summing up 2015, let me mention that the Export Credit

Insurance Corporation has been recognised as an im-

portant pillar of the system of support of Polish exports

under the government Plan for Responsible Develop-

ment, the most important elements of which are being

intensively implemented as of 2016.

Thus, KUKE has ambitious plans to become an effective

business partner of all Polish enterprises, irrespective of

their size and capital possibilities, whose acquisition tar-

gets extend beyond the frontiers of our country.

Yours faithfully,

Marek Czerski

President of the Management Board of kuke s.a.

4 2015 AnnuAl RepoRt | MacroeconoMic conditions in 2015

MAcRoeconoMic conditions in 2015

The growth in 2015 was mainly driven, similarly to 2014, by do-

mestic demand. This time, however, the impact of turnover with

abroad was also positive. Although it was not that significant as

in 2013, it differed substantially from the results of 2014, when

the balance of turnover with abroad materially deteriorated

GDP growth.

The high growth of domestic demand in 2015 derived from

increased consumption (in the household and public sectors)

and accumulation (including gross expenses for fixed assets

and a change in inventories). As regards consumption, the

significant re-improvement of financial standing of households

was particularly important because headcount and real value of

wages and salaries increased. Expenses for public consump-

tion were also increasing in a dynamic way, although slightly

less intensively than in the previous year. Expenses connected

with investment processes were also high. They were higher in

the first six months of the year and turned up less dynamic in

the second part. Similarly to the previous year, projects related

to the modernisation and expansion of production facilities

of enterprises played a special role. The scale of growth was

diminished by a decline in inventories, which was particularly

intensive at the beginning of the year.

Despite of high consumer demand, the rate of growth of import

decreased visibly because of a reduced growth of investments

and a drop in inventories. In turn, export was increasing at a rate

similar to that recorded in 2014.

In 2015, the rate of economic growth in Poland was 3.6% in comparison with

3.3% in 2014 and 1.3% in 2013. The rate of growth in particular quarters was

similar and clearly exceeded 3%. Thus, for two years in a row, enterprises

were operating in the environment of quite fast increasing demand, which

had a positive impact on the financial standing of their business partners.

doMestic deMAnd

5MacroeconoMic conditions in 2015 | 2015 AnnuAl RepoRt

Situation in the domestic market remained good. Consumer

and business sentiment was improving. This was substantially

influenced by in-depth moderation of the monetary policy since

autumn 2012, which was additionally strengthened with a cor-

rection of interest rates in autumn 2014 and spring 2015. An

easier and cheaper access to loans for enterprises favoured

a return to investment planning, but mainly contributed to an

improvement in liquidity and a reduction in financing expenses.

Households also felt an improvement in access to financing,

which additionally strengthened consumer demand.

As a consequence, the rate of economic growth of Poland in

subsequent quarters was high (respectively from 3.7% through

3.3% and 3.5% to 3.9%). In the whole year of 2015, it was 3.6% and

was by 3.3% greater than in 2014.

An improvement in economic situation for the second year in a

row contributed to a further drop in corporate bankruptcies in

Poland. In 2015, 737 bankruptcies were recorded in comparison

with 818 in 2014. In the same time, the intensity of bankruptcies

of commercial companies dropped from 1.15% as at the end of

2014 to 1.05% as at the end of 2015.

7.8%total GroWth of polish exports

10.3%GroWth of exports to countries of the eu

3.6% rate of econoMic GroWth

As regards export, sales to EU states improved. Foreign ex-

change rates had a special impact on 2015 results. EUR/USD

rate turned up to be much smaller than in summer 2014. As a

consequence, goods produced in EU states started being very

competitive in terms of prices in relation to goods produced

in other countries of the world. This improved export from the

EU, including the euro zone, as well as demand for supplies

necessary for production and consumer goods (bought by per-

sons employed in export industries). In the same time, goods

produced in Poland turned up to be more competitive in terms

of prices than goods produced in countries whose currencies

are correlated with the dollar (e.g. far east countries). The rate

of growth of sales to other developed markets was relatively

small. But sales to developing countries in 2015 were very

good. The growth turned up to be much greater than in the pre-

vious year. Export decline was recorded again in terms of sales

to countries of Central and Eastern Europe. This was an effect

of strongly limited demand as a result of tense economic and

political relationships between Kiev and Moscow. This stemmed

from a significant decrease in purchasing power of customers.

In the case of Ukraine, military actions constituted an essential

factor. A drop of sales to Russia also resulted from an embargo

enforced on our foodstuff.

Preliminary statistics based on customs reporting kept in euro

indicate that Polish export in 2015 grew by 7.8%. Export of goods

to the euro zone countries increased by 10.1% and mainly result-

ed from a progress in sales to Germany (11.2%), Italy (13.2%) and

the Netherlands (14.4%). The scale of growth of export calcu-

lated for all EU countries was better and constituted 10.3%. Sales

to non-euro zone countries, e.g. the UK (14.4%), the Czech Re-

public (10.1%) and Hungary (8.3%) improved. Export to countries

of Central and Eastern Europe decreased by 21.1%. In the case

of developing countries, the growth was estimated at 12.6%. In

2015, export to other developed countries grew by 3.9%.

eXpoRt doMestic MARket

6 2015 AnnuAl RepoRt | orGanisation

oRgAnisAtion

shAReholdeRs And shARe cApitAl

The structure of the share capital as at 31 December 2015 was

as follows:

shAReholdeR

nuMBeR oF

shARes

pAR vAlue

oF shARes

(pln) shARe (%)

State Treasury represented by the Minister of Finance 700,828 70,082,800 63.31

Bank Gospodarstwa Krajowego bp 406,201 40,620,100 36.69

totAl 1,107,029 110,702,900 100.00

supeRvisoRy BoARd

From 1 January 2015 to 21 December 2015, the Supervisory

Board of KUKE S.A. was composed of:

☐ Wojciech Rząsiecki – Chairman

☐ Michał Gruba – Vice-Chairman

☐ Ryszard Frączek

☐ Michał Kempa

☐ Katarzyna Przewalska

☐ Maria Szymańska

☐ Arkadiusz Zabłoński

☐ Jacek Zieliński

On 21 December 2015, Ryszard Frączek filed his resignation

from the Supervisory Board of KUKE S.A.

As at 31 December 2015, the Supervisory Board of KUKE S.A.

was composed of:

☐ Wojciech Rząsiecki – Chairman

☐ Michał Gruba – Vice-Chairman

☐ Michał Kempa

☐ Katarzyna Przewalska

☐ Maria Szymańska

☐ Arkadiusz Zabłoński

☐ Jacek Zieliński

MAnAgeMent BoARd

From 1 January 2015 to 8 December 2015, the Management

Board of KUKE S.A. was composed of:

☐ Dariusz Poniewierka – President of the Management Board

☐ Piotr Stolarczyk – Vice-President of the Management Board

☐ Aleksandra Hanzel – Vice-President of the Management Board

On 8 December 2015, Aleksandra Hanzel filed her resignation

from the Management Board of KUKE S.A.

Therefore, as at 31 December 2015, the Management Board of

KUKE S.A. was composed of:

☐ Dariusz Poniewierka – President of the Management Board

☐ Piotr Stolarczyk – Vice-President of the Management Board

As at 31 December 2015, the share capital of KUKE S.A. amount-

ed to PLN 110,702,900 and was divided into 1,107,029 registered

ordinary shares of a par value of PLN 100 each. The share capi-

tal was paid in full.

7kuke finance s.a. | 2015 AnnuAl RepoRt

On 22 December 2014, the Extraordinary Meeting of Sharehold-

ers of KUKE S.A. adopted a resolution on increasing the share

capital of KUKE Finance S.A. by PLN 10,300,000.00, i.e. to PLN

25,000,000.00, through the issue of 103,000 new registered

shares of C class of a par value of PLN 100 each. The share

capital was increased through closed subscription in accord-

ance with Art. 431 § 2.2 of the Code of Commercial Compa-

nies, and the shares were offered to KUKE S.A., which held a

pre-emptive right.

The share capital was paid in full on 12 January 2015. On 20

January 2015, the District Court for the capital city of Warsaw,

12ʰ Commercial Division of the National Court Register, regis-

tered the increase in the share capital of KUKE Finance S.A. As

a result, the share capital of KUKE Finance S.A. increased from

PLN 14,700,000 to PLN 25,000,000. The share capital was paid

in full.

At present, KUKE S.A. owns 250,000 registered shares of KUKE

Finance S.A. in total, i.e. 100% of the share capital of its sub-

sidiary. The company commenced its operating activities in

November 2014.

kuke FinAnce s.A.

The core activity of KUKE Finance S.A. covers financing foreign and domes-

tic receivables through all forms of factoring that are available in the market,

particularly within the framework of non-recourse factoring i.e. where the

factor assumes the risk of non-payment by his client’s buyer.

8 2015 AnnuAl RepoRt | perforMance of kuke s.a.

peRFoRMAnce oF kuke s.A.iN SPEcific bUSiNESS AREAS

geneRAl Results

In 2015, KUKE S.A. insured a total turnover of PLN 30,721.91 mil-

lion, i.e. by 1.7% less than in the previous year.

31,670.3

28,884.9

30,018.8

31,245.0

30,721.9

In 2015, insured export turnover dropped by 5.3% in comparison

with 2014. Insured export turnover amounted to PLN 12,901.89

million, including PLN 9,847.69 million of commercial export in-

surances (growth of the volume by 1.5%) and PLN 3,054.20 mil-

lion of export insurances backed by the State Treasury (drop of

the volume by 21.9%).

Under the insurance of short-term domestic receivables and

commercial bonds, KUKE S.A. covered transactions of PLN

17,820.02 million, which means a 1.1% growth in comparison

with 2014.

vAlue oF insuRed eXpoRt And doMestic tuRnoveR

in pln Million (All insuRAnce FAcilities)

30.7 billionvalue of insured turnover (pln)

2,390active insurance policies and bonds

12 billionexposure (pln)

2011

2012

2013

2014

2015

9perforMance of kuke s.a. | 2015 AnnuAl RepoRt

30.7 billionvalue of insured turnover (pln)

geogRAphic stRuctuRe

AgReeMents

geogRAphicAl stRuctuRe oF insuRed eXpoRt

tuRnoveR (All insuRAnce FAcilities)

Germany

Russia

Czech Republic

Canada

UK

Belarus

Switzerland

Netherlands

Lithuania

Italy

Others

The geographic structure of export turnover covered by KUKE

was dominated by Germany (21.3%), Russia (8.3%) and the Czech

Republic (5.7%), similarly to 2014. The share of EU countries was

65.9% (64.8% in 2014) and the share of ciS countries was 16.6%

(21.2% in 2014).

In 2015, KUKE S.A. concluded 1,114 new insurance agreements

and bond agreements, including 768 in terms of commercial ac-

tivities and 346 in terms of activities backed by the State Treas-

ury. In addition, 1,231 policies from previous years were renewed

(421 in terms of commercial activities and 810 in terms of activi-

ties backed by the State Treasury). In 2015, 2,345 policies were

signed and renewed in total, i.e. by 12.88% more than in 2014.

As at the end of 2015, there were 2,390 active policies, which

meant an increase by 13.3% in comparison with the previous

year (1,096 in terms of commercial activities: 21.5% growth

and 1,294 in terms of activities backed by the State Treasury:

7.2% growth).

1,848

1,960

2,057

2,109

2,390

nuMBeR oF Active insuRAnce policies And Bonds

issued (All insuRAnce FAcilities)

21.3%

8.3%

5.7%

4.7%

4.0%3.9%3.5%3.4%

3.4%

38.4%

3.3%

2011

2012

2013

2014

2015

10 2015 AnnuAl RepoRt | activit ies of kuke s.a.

shoRt-teRM eXpoRt And doMestic cRedit insuRAnce

Bonds

In 2015, within the 14ʰ insurance class, KUKE S.A. insured

short-term export and domestic receivables of PLN 27,312.52

million in total (by 0.06% more than in 2014).

Gross premium written under the insurance of short-term export

and domestic receivables was PLN 43.06 million, which means

that it decreased by 8.0% in comparison with 2014.

In 2015, KUKE S.A. issued 590 bonds for a total amount of PLN

355.2 million. In comparison with 2014, the total value of bonds

increased by 84.0%.

In the reporting year, the remuneration of KUKE S.A. for bonds

issued amounted to PLN 5.66 million, i.e. by 26.2% more than

in 2014.

Activities oF kuke s.A. UNDER thE iNSURANcE Act of 22 MAy 2003

(coMMERciAL ActivitiES)

27.3 billionvalue of insured short-terM receivables (pln)

590bonds issued

355.2 million value of bonds issued (pln)

11activit ies of kuke s.a. | 2015 AnnuAl RepoRt

In 2015, the total value of export contracts covered under me-

dium- and long-term export credit insurance facilities (credits

with repayment terms of two and more years) amounted to

PLN 861.57 million, including PLN 1.32 million due to increasing

amendments to insurance contracts of 2008, 2013 and 2014.

KUKE S.A. entered into 16 insurance agreements covering 18 ex-

port contracts worth PLN 930.52 million.

Within the framework of the Government Export Support Pro-

gram in 2015 KUKE S.A. concluded 6 insurance agreements for a

total sum of PLN 250.40 million.

During the reporting period premium written under medium-

and long-term export credit insurance amounted to PLN 28.32

million. As loans insured under 4 insurance contracts from pre-

vious years were repaid before their maturity, KUKE S.A. made

premium refunds in the amount of PLN 11.70 million in total. Pre-

mium written under medium- and long-term export credit insur-

ance deducted by the above amount came to PLN 16.62 million.

In 2015, as part of its state backed insurance activities, KUKE S.A.

issued 208 bonds for a total value of PLN 231.93 million. This

included 13 contract bonds for a total of PLN 32.54 million and

195 bonds concerning letters of credit amounting to PLN 199.40

million. Remuneration for bonds issued and the extension of the

terms of bonds granted in previous years was PLN 4.70 million.

In 2015, 119 turnover policies and 3 individual policies were

signed under short-term export credit insurance backed by the

State Treasury (credit terms of less than two years). 810 policies

were renewed. As at the end of the year, there were 924 active

policies, i.e. 10.9% more than in the previous year.

Total insured turnover amounted to PLN 1.96 billion, i.e. 29.4%

less than in 2014.

Premium written signed under short-term export credit insur-

ance backed by the State Treasury amounted to PLN 16.41

million.

In 2015, KUKE S.A. paid out 76 indemnities for a total amount of

PLN 145.88 million, including:

☐ 72 indemnities concerning short-term export credit insur-

ance amounting to PLN 15.20 million;

☐ 4 indemnities concerning medium- and long-term export

credit insurance amounting to PLN 130.68 million.

No indemnities were paid and no payments were made under

remaining insurance facilities backed by the State Treasury.

During that period, within the framework of its Treasury-backed

export business, KUKE was able to recover in the process of

subrogation the total amount of PLN 0.93 million, of which 0.36

million pertained to short-term contracts and 0.58 million con-

cerned medium- and long-term insurance.

Activities oF kuke s.A. UNDER thE Act oN ExPoRt iNSURANcE bAcKED

by thE StAtE tREASURy of 7 JULy 1994

12 2015 AnnuAl RepoRt | financial results

In the financial year 2015, KUKE S.A. changed its accounting principles and

started to settle in time the reinsurance commission within the 15ʰ insur-

ance class. To provide for the comparability of data in the income state-

ment and balance sheet for 2014, a deferred reinsurance commission within

the 15ʰ insurance class had to be calculated as at 31 December 2014 and

31 December 2013.

Assets

In 2015, intangibles increased from PLN 0.63 million in 2014 to

PLN 0.51 million.

Investments constituted 69.5% of the balance sheet total. In

comparison with the end of 2014, they increased by 1.6% and

reached PLN 237.56 million as at 31 December 2015.

Receivables as at the end of 2015 were PLN 38.27 million and

constituted 11.2% of total assets. In comparison with 2014, re-

ceivables increased by 5.5%, including:

☐ receivables under direct insurances (mainly premium settle-

ments) decreased by 2.3% from PLN 21.62 million in 2014 to

PLN 21.12 million in 2015;

☐ reinsurance receivables grew by 1.4% from PLN 12.87 million

in 2014 to PLN 13.05 million in 2015;

☐ other receivables grew by 127.0% from PLN 1.81 million in

2014 to PLN 4.11 million in 2015; their growth resulted from

settlements connected with a commission charged by KUKE

S.A. for insurances backed by the State Treasury.

Other assets as at 31 December 2015 amounted to PLN 60.68

million and were 40.2% smaller than as at 31 December 2014.

Funds deposited on a separate bank account for insurance

business backed by the State Treasury which is used to carry

out settlements regarding activities entrusted to KUKE S.A. on

the basis of the Act on Export Insurances Backed by the State

Treasury of 7 July 1994 constituted 90.5% of the above amount,

i.e. PLN 54.93 million.

FinAnciAl Results

AnAlysis oF the BAlAnce sheet

KUKE S.A.’s balance sheet total as at the end of 2015 was PLN

341.66 million and was 9.2% smaller than as at the end of 2014.

The drop in the balance sheet total resulted mainly from a de-

crease in funds deposited on a separate bank account for insur-

ance business backed by the State Treasury (by 44.0%, i.e. PLN

43.24 million), which is used to carry out settlements regarding

activities entrusted to KUKE S.A. on the basis of the Act on Export

Insurances Backed by the State Treasury of 7 July 1994.

13financial results | 2015 AnnuAl RepoRt

KUKE S.A.‘s equity as at the end of 2015 was PLN 204.27 million

and was 1.0% greater than as at the end of the previous year. The

equity constituted 59.8% of the balance-sheet total (2014: 53.8%).

As at 31 December 2015, liabilities and special funds dropped

by 33.2% in comparison with the previous year. Their constituted

24.0% of total equity and liabilities. As at the end of 2015, they

amounted to PLN 81.86 million, including funds deposited on a

separate bank account for insurance business backed by the

State Treasury which is used to carry out settlements regarding

activities entrusted to KUKE S.A. on the basis of the Act on Export

Insurances Backed by the State Treasury, which amounted to

PLN 54.93 million.

As at the end of the reporting period, technical and insurance

provisions (including reinsurers’ share and estimated recourses)

amounted to PLN 42.95 million, which means that they increased

by 4.8% in comparison with the end of 2014. They constituted

12.6% of total equity and liabilities.

The following table presents net provisions established in 2015.

1) including estimated recourses.

Differences in checksums result from roundings.

type oF pRovision

As At

31.12.2014

(pln Million)

2014

shARe

(%)

As At

31.12.2015

(pln Million)

2015

shARe

(%)

chAnge

2015/2014

(%)

Provision for unexpired risk 24.23 59.10 24.72 57.50 2.00

Provision for unpaid indemnities and benefits 1) 11.42 27.90 6.28 14.60 −45.10

Equalisation provision 1.71 4.20 9.23 21.50 439.80

Provision for bonuses and rebates

for the insured

3.63 8.90 2.74 6.40 −24.70

totAl 41.00 100.00 42.95 100.00 4.80

equity And liABilities

237.6 millioninvestMents (pln)

42.9 milliontechnical insurance provisions (pln)

81.9 millionother payables and special funds (pln)

204.3 millioneQuity (pln)

14

AnAlysis oF technicAl insuRAnce Account And oveRAll pRoFit And loss Account

In 2015, revenues from net premium earned (including a change

in the provision for unexpired risk) amounted to PLN 25.95 mil-

lion, i.e. 6.2% more (PLN 1.51 million) than in 2014. A gross pre-

mium written was PLN 48.72 million and decreased by 5.0%, i.e.

PLN 2.58, in comparison with 2014.

In 2015, indemnities and benefits paid net of reinsurance

amounted to PLN 10.64 and were 47.4% smaller than in 2014.

The provision for unpaid indemnities and benefits net of rein-

surance, including estimated recourses, dropped by PLN 5.15

million (similarly to 2014, when they dropped by PLN 8.14 million).

Costs of insurance operations (costs of administration and ac-

quisition and reinsurance commissions received) decreased

by 8.3% in comparison with 2014 and amounted to PLN 10.84

million. Costs of administration and acquisition increased in

comparison with 2014 by 1.4% to PLN 19.97 million. Revenues

from reinsurance commissions (which decrease the costs of in-

surance activity) increased by 15.9% in comparison with 2014 to

PLN 9.13 million.

Other revenues and technical expenses net of reinsurance

amounted to PLN 0.29 million.

Technical result before the establishment of the equalisation

provision was pln 9.92 million. Given its positive technical

result in the 14ʰ insurance class, KUKE S.A. released the equali-

sation provision of PLN 7.52 million. Ultimately, technical insur-

ance result in 2015 was pln 2.40 million in comparison with

the loss of PLN 1.62 million in 2014.

In 2015, the balance of investment income and expenses (cal-

culated as total income from investments, unrealised profits and

losses from investments and investment expenses) was PLN

4.42 million. It was by 31.9% smaller than in 2014. Result from

investments in 2015 was reduced by PLN 1.90 million by unreal-

ised loss from the shares of KUKE Finance S.A.

The balance of other operating income and expenses was neg-

ative and amounted to PLN −4.05 million, including the balance

of commissions and expenses connected with handling export

insurances backed by the State Treasury of PLN −4.03 million (in

comparison with PLN 1.15 million in 2014), and resulted from the

commission which was smaller than in 2014 and derived from

gross premium written under those insurances.

In 2015 KUKE S.A. recorded gross profit of PLN 2.77 in compari-

son with PLN 5.98 million in the previous year. Including current

and deferred income tax of PLN 0.39, the net profit stood at

pln 2.38 million (2014: PLN 5.04 million).

2.4 milliontechnical result (pln)

10.6 millionclaiMs and benefits paid (pln)

2.4 millionnet profit (pln)

2015 AnnuAl RepoRt | financial results

15

As at 31 December 2015, KUKE S.A. recorded a surplus of own

assets to cover the solvency margin and the compulsory guar-

antee capital by PLN 196.90 million and PLN 185.95 million

respectively.

Assets used to cover technical and insurance provisions

amounted to PLN 142.92 million and technical insurance provi-

sions amounted to PLN 66.21 million. As at the end of 2015, the

assets to technical insurance provisions coverage level stood

at 216%.

As at 31 December 2015, KUKE S.A. met all legally required pru-

dential standards for insurance activity.

For presentation purposes, negative items are marked with “-”.

selected iteMs oF the technicAl Account

And pRoFit And loss Account

2014

(pln Million)

2015

(pln Million)

Gross premiums 51.30 48.72

Net premiums 24.45 25.95

Claims and benefits −12.09 −5.49

Bonuses and rebates, net of reinsurance −1.24 0.01

Balance of other technical income and expenses 0.79 0.29

Costs of insurance operations −11.82 −10.84

Change in equalisation provision −1.71 −7.52

technicAl Result −1.62 2.40

Balance of investment income and expenses 6.49 4.42

Balance of other operating income and expenses 1.11 −4.05

gRoss pRoFit (loss) 5.98 2.77

Income tax −0.94 −0.39

net pRoFit (loss) 5.04 2.38

18.7

−8.3

4.1

5.0

2.4

net pRoFit/loss in pln Million

2011

2012

2013

2014

2015

financial results | 2015 AnnuAl RepoRt

16

(pln thousAnd) 31.12.2014 31.12.2015

Intangible assets 631 508

Investments 233 769 237 562

Investments in subordinated undertakings 13 114 46 560

Shares in subordinated undertakings 13 114 21 510

Loans to subordinated undertakings and debt securities

issued by those undertakings

0 25 050

Other financial investments 220 655 191 002

Other loans 0 0

Debt securities and other fixed income securities 196 166 171 687

Deposits with credit institutions 24 489 19 315

Receivables 36 293 38 274

Direct insurance receivables 21 618 21 119

Receivables from policyholders 21 249 20 769

Other receivables 369 350

Reinsurance receivables 12 866 13 049

Other receivables 1 809 4 106

Receivables from the State budget 71 842

Other receivables 1 738 3 264

Other assets 101 398 60 676

Tangible fixed assets 1 501 1 770

Cash and cash equivalents 99 897 58 906

incl.: cash on separate bank account for insurance business

guaranteed by the State Treasury

98 170 54 928

Deferred expenses and accrued income 4 131 4 639

Deferred tax assets 1 411 1 874

Deferred acquisition costs 2 291 2 401

Other deferred expenses and accrued income 429 364

totAl Assets 376 222 341 659

Assets(AFteR tRAnsFoRMAtion)

2015 AnnuAl RepoRt | financial results

17

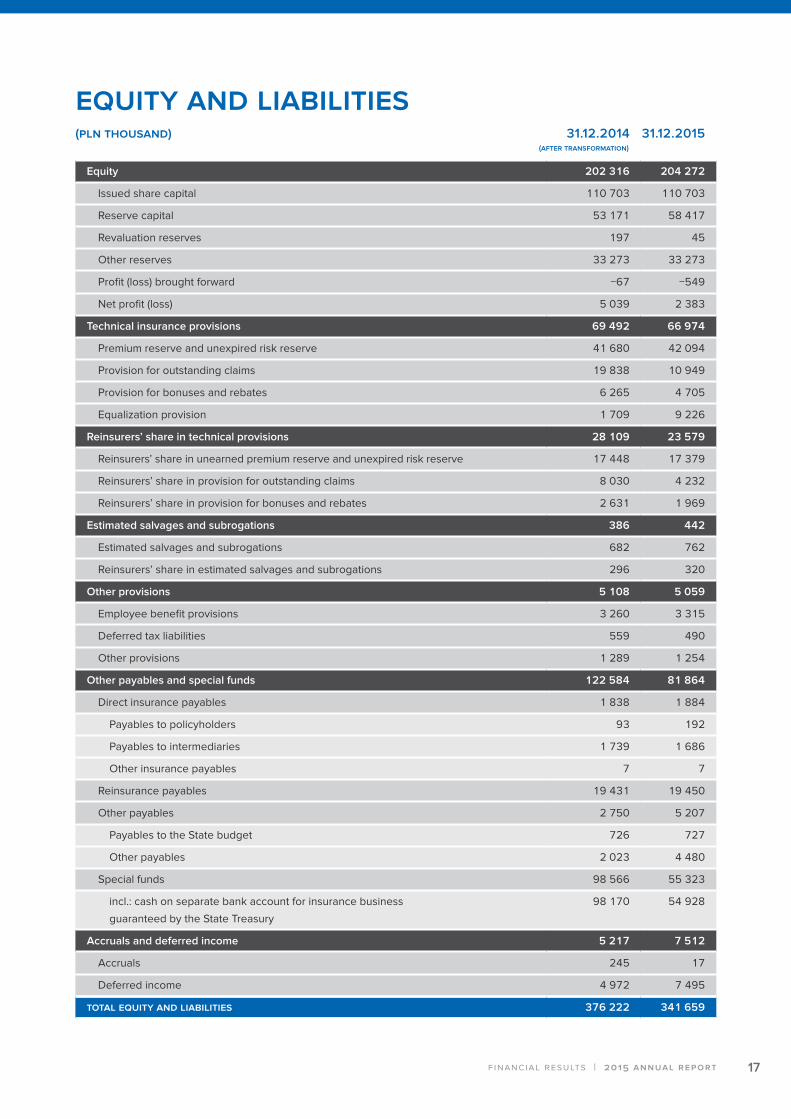

(pln thousAnd) 31.12.2014 31.12.2015

Equity 202 316 204 272

Issued share capital 110 703 110 703

Reserve capital 53 171 58 417

Revaluation reserves 197 45

Other reserves 33 273 33 273

Profit (loss) brought forward −67 −549

Net profit (loss) 5 039 2 383

Technical insurance provisions 69 492 66 974

Premium reserve and unexpired risk reserve 41 680 42 094

Provision for outstanding claims 19 838 10 949

Provision for bonuses and rebates 6 265 4 705

Equalization provision 1 709 9 226

Reinsurers’ share in technical provisions 28 109 23 579

Reinsurers’ share in unearned premium reserve and unexpired risk reserve 17 448 17 379

Reinsurers’ share in provision for outstanding claims 8 030 4 232

Reinsurers’ share in provision for bonuses and rebates 2 631 1 969

Estimated salvages and subrogations 386 442

Estimated salvages and subrogations 682 762

Reinsurers’ share in estimated salvages and subrogations 296 320

Other provisions 5 108 5 059

Employee benefit provisions 3 260 3 315

Deferred tax liabilities 559 490

Other provisions 1 289 1 254

Other payables and special funds 122 584 81 864

Direct insurance payables 1 838 1 884

Payables to policyholders 93 192

Payables to intermediaries 1 739 1 686

Other insurance payables 7 7

Reinsurance payables 19 431 19 450

Other payables 2 750 5 207

Payables to the State budget 726 727

Other payables 2 023 4 480

Special funds 98 566 55 323

incl.: cash on separate bank account for insurance business

guaranteed by the State Treasury

98 170 54 928

Accruals and deferred income 5 217 7 512

Accruals 245 17

Deferred income 4 972 7 495

totAl equity And liABilities 376 222 341 659

(AFteR tRAnsFoRMAtion)

equity And liABilities

financial results | 2015 AnnuAl RepoRt

18

(pln thousAnd)

01.01.2014-

-31.12.2014

01.01.2015-

-31.12.2015

Premiums 24 446 25 954

Gross written premiums 51 302 48 722

Reinsures’ share in written premiums 24 236 22 285

Change in unearned premium reserve and unexpired risk reserve 4 543 414

Reinsures’ share in change in reserves 1 922 −69

Other net technical income 3 546 3 420

Claims and benefits 12 092 5 491

Net claims and benefits paid 20 231 10 637

Claims and benefits paid gross 33 326 16 674

Reinsurers’ share in claims and benefits paid 13 095 6 038

Net change in outstanding claims provision −8 139 −5 146

Gross change in outstanding claims provisions −13 377 −8 969

Reinsurers’ share in change in outstanding claims provision −5 238 −3 823

Net premiums and benefits incl. change in provisions 1 241 −9

General insurance expenses 11 819 10 841

Acquisition costs 8 546 8 692

incl. change in deferred acquisition costs −585 −110

Administrative expenses 11 148 11 279

Reinsurance commissions and shares in profit 7 875 9 131

Other net technical expenses 2 753 3 132

Change in equalization reserve 1 709 7 517

technicAl Result −1 623 2 403

technicAl Account oF pRopeRty And cAsuAlty insuRAnce

(AFteR tRAnsFoRMAtion)

2015 AnnuAl RepoRt | financial results

19

(pln thousAnd)

01.01.2014-

-31.12.2014

01.01.2015-

-31.12.2015

Technical result −1 623 2 403

Investment income 8 254 6 990

Income from investments in subordinated undertakings 0 195

Income from other financial investments 7 998 6 779

Realized gains on investments 255 16

Unrealized gains on investments 173 0

Investment management expenses 354 562

Unrealized losses on investments 1 586 2 012

Other operating income 14 402 9 528

incl.: income due to insurance activity guaranteed by the State Treasury 13 767 8 926

Other operating expenses 13 290 13 578

incl.: expenses due to insurance activity guaranteed by the State Treasury 12 615 12 954

Gross profit (loss) 5 976 2 769

Income Tax 936 386

net pRoFit (loss) 5 039 2 383

(AFteR tRAnsFoRMAtion)

geneRAl pRoFit And loss Account

financial results | 2015 AnnuAl RepoRt

20

(pln thousAnd)

01.01.2014-

-31.12.2014

01.01.2015-

-31.12.2015

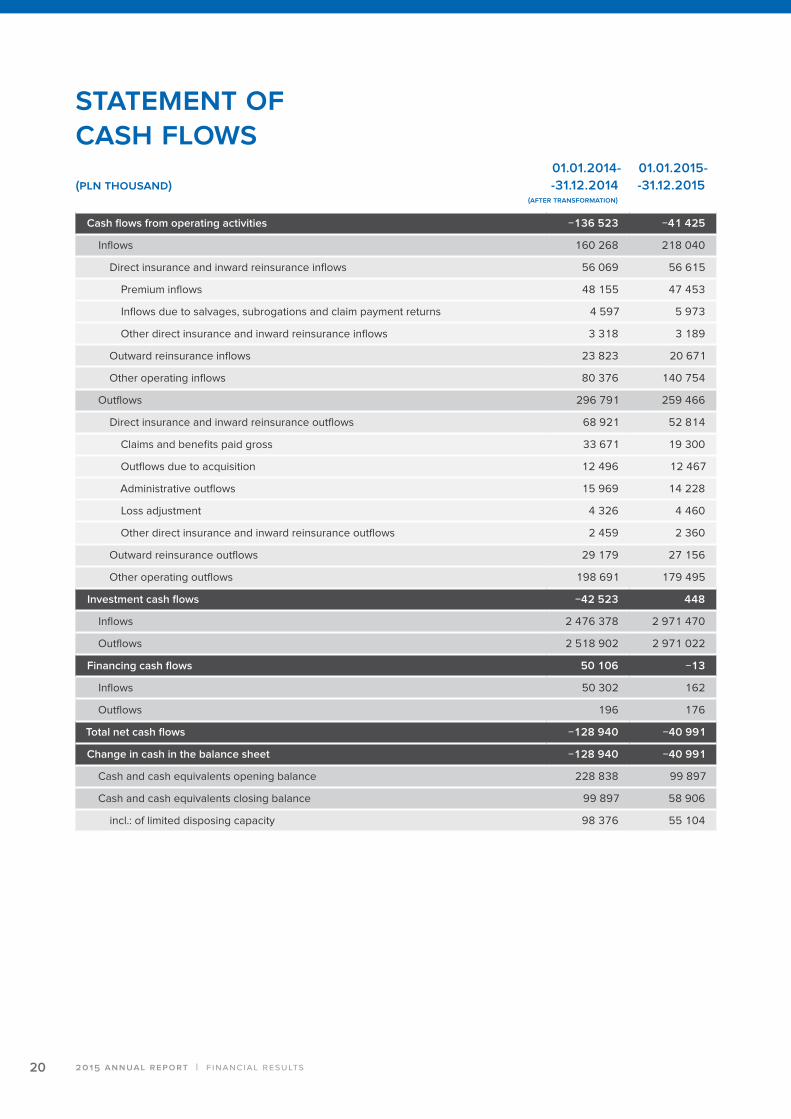

Cash flows from operating activities −136 523 −41 425

Inflows 160 268 218 040

Direct insurance and inward reinsurance inflows 56 069 56 615

Premium inflows 48 155 47 453

Inflows due to salvages, subrogations and claim payment returns 4 597 5 973

Other direct insurance and inward reinsurance inflows 3 318 3 189

Outward reinsurance inflows 23 823 20 671

Other operating inflows 80 376 140 754

Outflows 296 791 259 466

Direct insurance and inward reinsurance outflows 68 921 52 814

Claims and benefits paid gross 33 671 19 300

Outflows due to acquisition 12 496 12 467

Administrative outflows 15 969 14 228

Loss adjustment 4 326 4 460

Other direct insurance and inward reinsurance outflows 2 459 2 360

Outward reinsurance outflows 29 179 27 156

Other operating outflows 198 691 179 495

Investment cash flows −42 523 448

Inflows 2 476 378 2 971 470

Outflows 2 518 902 2 971 022

Financing cash flows 50 106 −13

Inflows 50 302 162

Outflows 196 176

Total net cash flows −128 940 −40 991

Change in cash in the balance sheet −128 940 −40 991

Cash and cash equivalents opening balance 228 838 99 897

Cash and cash equivalents closing balance 99 897 58 906

incl.: of limited disposing capacity 98 376 55 104

stAteMent oF cAsh FloWs

2015 AnnuAl RepoRt | financial results

(AFteR tRAnsFoRMAtion)

21

(pln thousAnd)

01.01.2014-

-31.12.2014

01.01.2015-

-31.12.2015

Assets of the insurance company 376 222 341 659

Assets to cover all expected liabilities 173 906 137 387

technical insurance provisions 40 997 42 953

other provisions 5 108 5 059

other payables and special funds 122 584 81 864

accruals and deferred income 5 217 7 512

Intangible assets 631 508

Deferred tax assets 1 411 1 874

Amount of own assets 200 274 201 890

Solvency margin 5 173 4 989

Minimum guarantee capital 15 403 15 939

1/3 of the solvency margin 1 724 1 663

Surplus of own assets to cover the solvency margin 195 101 196 901

Guarantee capital 15 403 15 939

Surplus of own assets to cover the guarantee capital 184 871 185 951

solvency pARAMeteRs

financial results | 2015 AnnuAl RepoRt

(AFteR tRAnsFoRMAtion)

The Polish original should be referred to in matters of interpretation.Translation of auditor’s report originally issued in Polish.

1/2

THE INDEPENDENT AUDITORS’ REPORT ON THE SUMMARY FINANCIALSTATEMENTS

To the General Meeting and Supervisory Board of Korporacja Ubezpieczeń KredytówEksportowych Spółka Akcyjna

We have audited the financial statements for the year ended 31 December 2015 of KorporacjaUbezpieczeń Kredytów Eksportowych Spółka Akcyjna (‘the Company‘) located in Warsaw, at Sienna39 (‘the unabridged financial statements’), from which the attached summarized financial statementsfor the year ended 31 December 2015 were derived by the Company’s Management Board (‘thesummarized financial statements’). The unabridged financial statements have been prepared inaccordance with the accounting principles specified in the Accounting Act dated 29 September 1994(Journal of Laws 2013.330 with subsequent amendments – ‘the Accounting Act’) and regulationsissued based on that Act and based on properly maintained accounting records.We conducted our audit of the unabridged financial statements, from which the summarized financialstatements were derived, in accordance with the chapter 7 of the Accounting Act and the NationalAuditing Standards issued by the National Council of Statutory Auditors. On 20 April 2016 we issuedan unqualified opinion on the unabridged financial statements of the Company. The unabridgedfinancial statements of the Company, as well as the attached summary financial statements of theCompany do not reflect the effects of events which occurred subsequent to the date of issuance of theabove opinion.

Summary financial statements do not contain all the elements and disclosures required for thepreparation of the unabridged financial statements. For a better understanding of the Company’sfinancial position as at 31 December 2015 and the results of its operations for the period from 1January 2015 to 31 December 2015 and of the scope of our audit, the attached summarized financialstatements should be read in conjunction with the unabridged financial statements from which thesummarized financial statements were derived and our auditors’ report relating to these financialstatements.

Responsibility of the Company’s Management Board for the attached summary financial statementsof the Company

The Management Board of the Company is responsible for the preparation and publication of theattached summary financial statements of the Company with the auditors’ report on the attachedsummary financial statements in the Annual Report of the Company.

Auditors’ Responsibility

Our responsibility was to express an opinion on the attached summary financial statements of theCompany based on our procedures, which were conducted in accordance with National AuditingStandard No. 3, guided by the principles contained in International Standard on Auditing 810‘Engagements to Report on Summary Financial Statements’.

2/2

OpinionIn our opinion the attached summarized financial statements, in all material respects, are consistentwith the unabridged financial statements, from which they were derived.

on behalf ofErnst & Young Audyt Polska spółka

z ograniczoną odpowiedzialnością sp. k.Rondo ONZ 1, 00-124 Warsaw

Reg. No. 130

Key Certified Auditor

(-)Arkadiusz Krasowski

Certified AuditorNo. 10018

Warsaw, 2 November 2016

koRpoRAcjA uBezpieczeń

kRedytóW ekspoRtoWych

spółkA AkcyjnA

ul. Sienna 39

00-121 Warszawa

tel.: 22 356 83 00

infolinia: 801 805 853

WWW.kuke.coM.pl