2014 state of the nonprofit sector survey arts & culture · pdf...

TRANSCRIPT

0 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

2014 State of the Nonprofit Sector Survey Arts & Culture

http://nff.org/survey

Filter the results yourself at http://survey.nff.org

Based on a nationwide survey of nonprofit cultural leaders conducted by Nonprofit Finance Fund, January-February 2014.

1 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Table of Contents

About Nonprofit Finance Fund & the Survey

Program Trends: Demand, Engagement, & Competition

Financial Health & Management Actions Taken

Grantmaking Trends: Dynamics of Private & Public Funding

Measuring Impact

Conclusion: Looking Ahead & Tips for Cultural Nonprofits

2 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

About Nonprofit Finance Fund (NFF): Tailored Investments, Strategic Advice, Accessible Insights

Since 1980, we’ve helped funders, nonprofits, and other mission-driven organizations connect money to mission. Our services help great organizations stay in balance, so that they’re able to adapt to changing financial circumstances and grow and innovate when they’re ready. As a leading community development financial institution, NFF has provided over $287 million in loans and access to additional financing via grants, tax credits, and capital to support over $1.4 billion in projects for thousands of organizations.

Since our founding, NFF has been helping arts and cultural organizations solve their financial challenges and plan for a more vibrant, healthy future. We have worked with more than 1,300 arts organizations across the country, from small neighborhood-based community centers to large performing arts organizations and museums.

3 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

NFF’s Annual Survey: Linking Practice, Data, and Action

Support systemic change

Provide practical advice and facilitate dialogue among funders, NPOs, advocates, gov’t

Deeper analysis of subsets of survey data

Share what we learn with the field

High-level analysis of results

Test hypotheses through data collection

Develop hypotheses of NPO experiences through on-the-ground work Phase 1: Building on NFF’s

Advisory & Lending practice, we develop survey content, collect unbiased data, and share what we learn with the field.

Phase 2: Our data analysis informs our Advisory & Lending practice, in a feedback loop of learning.

Phase 3: We work with experts, advocates, funders and others to put the data in service of systems-level change.

4 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

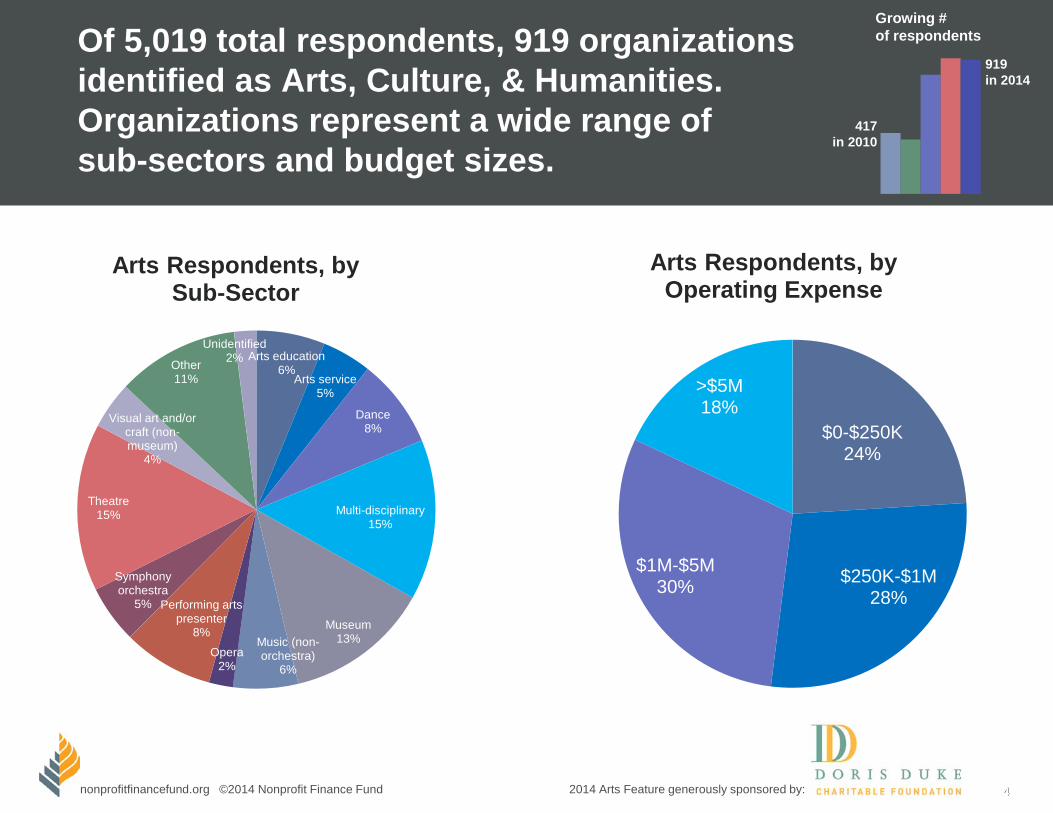

Of 5,019 total respondents, 919 organizations identified as Arts, Culture, & Humanities. Organizations represent a wide range of sub-sectors and budget sizes.

4

$0-$250K 24%

$250K-$1M 28%

$1M-$5M 30%

>$5M 18%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

Arts Respondents, by Operating Expense

Growing # of respondents

919 in 2014

417 in 2010

Arts education 6%

Arts service 5%

Dance 8%

Multi-disciplinary 15%

Museum 13% Music (non-

orchestra) 6%

Opera 2%

Performing arts presenter

8%

Symphony orchestra

5%

Theatre 15%

Visual art and/or craft (non-museum)

4%

Other 11%

Unidentified 2%

Arts Respondents, by Sub-Sector

5 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Table of Contents

About Nonprofit Finance Fund & the Survey

Program Trends: Demand, Engagement, & Competition

Financial Health & Management Actions Taken

Grantmaking Trends: Dynamics of Private & Public Funding

Measuring Impact

Conclusion: Looking Ahead & Tips for Cultural Nonprofits

6 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

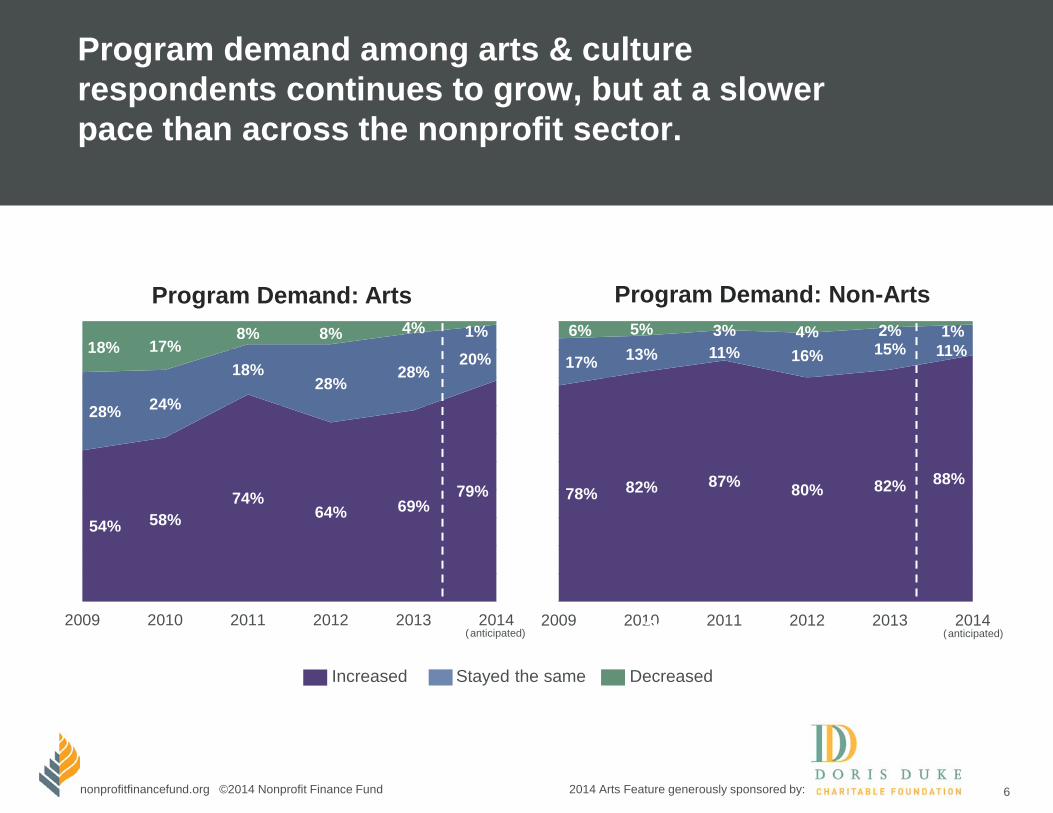

78% 82% 87% 80% 82% 88%

17% 13% 11% 16% 15% 11% 6% 5% 3% 4% 2% 1%

2009 2010 2011 2012 2013 2014

Program demand among arts & culture respondents continues to grow, but at a slower pace than across the nonprofit sector.

2012

54% 58% 74%

64% 69% 79%

28% 24%

18% 28%

28% 20%

18% 17% 8% 8% 4% 1%

2009 2010 2011 2012 2013 2014

Program Demand: Arts Program Demand: Non-Arts

Increased Stayed the same Decreased

(anticipated) (anticipated)

7 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

A majority of cultural organizations are keeping up with rising demand for their programs.

7

Yes 67%

No 33%

Were you able to meet demand?

Yes 38% No

62%

Organizations Met Demand (excluding arts)?

8 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Organizations report increasing demand for programming that is interactive, affordable, and appealing to all ages.

8

“Audiences are demanding free programs that contain social components and interactive elements. They want programs that cater to a variety of age ranges, so that they are able to bring their family.” - Museum, Florida

“Audiences want programming that is participatory and affordable. Trends are the same everywhere: reduced reliance on the ‘experts’ and increased self-propelled activity.” - Arts service nonprofit, California

“Participatory programs are in high demand. People want to be actively involved. I think it's an extension of the fact that everyone can participate in everything (YouTube, Facebook, Twitter). The power of authoritative institutions is being called into question.” - Museum, Georgia

9 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Arts & culture organizations are pursuing a range of strategies (e.g., program adaptation, data collection, targeted marketing) to build and engage their audience/visitor base.

How are arts organizations developing and engaging audiences/visitors?

71%

59%

56%

53%

53%

46%

29%

26%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Developing programs that are relevant for targetaudiences or visitor segments

Collecting data on audience/visitor preferences andbehaviors

Implementing new marketing strategy(ies)

Engaging audiences/visitors through technology

Offering participatory programming

Offering cultural experiences in unconventional spaces

Implementing new pricing model(s)

Involving audiences/visitors in program planning

We did not make a meaningful investment indevelopment or engagement strategies

10 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

65%

47%

44%

33%

33%

25%

14%

8%

5%

5%

0% 10% 20% 30% 40% 50% 60% 70%

Our audience/visitor base grew

Our donor base grew

We attracted younger audiences/visitors

We attracted an audience/visitor segment that is morerepresentative of our community

Our ticket revenue grew

Our surplus/deficit improved

Our financial results have not improved

The number and composition of audiences/visitors hasnot changed

We saw some audience/visitor segments decline

Don’t know

65% of arts respondents report growth in their audience/visitor base as a result of engagement strategies. However, far fewer report positive financial return on their investments.

Results from audience/visitor development

11 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Organizations do not feel overly threatened by competition from other arts and non-arts experiences. Of those who did experience competition, <15% reported financial ramifications.

11

How has increased competition impacted your organization? (selected all that apply)

11%

7%

11%

13%

12%

6%

37%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Decline in overall attendance

Decline in repeat attendance

Downward pricing pressure

Lower earned revenue

Lower contributed revenue

Declining bottom line

We have not experienced increasedcompetition

12 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Arts & culture organizations cite some of the positive effects of competition: stronger programs, a more engaged audience, and opportunity for collaboration.

12

“A rising tide raises all boats. If people are interested in experiencing the arts, that helps us.” - Theatre, California

“As we become the dominant cultural organization in our community, we experience the inverse of competition–opportunities to be generous to struggling organizations.” - Museum, California

“More activity in the field of experimental arts only strengthens our programs and builds a more open & educated audience.” - Theatre, New York

“We cooperate with other organizations to build audiences for all of us.” - Orchestra, Utah

13 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Table of Contents

About Nonprofit Finance Fund & the Survey

Program Trends: Demand, Engagement, & Competition

Financial Health & Management Actions Taken

Grantmaking Trends: Dynamics of Private & Public Funding

Measuring Impact

Conclusion: Looking Ahead & Tips for Cultural Nonprofits

14 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

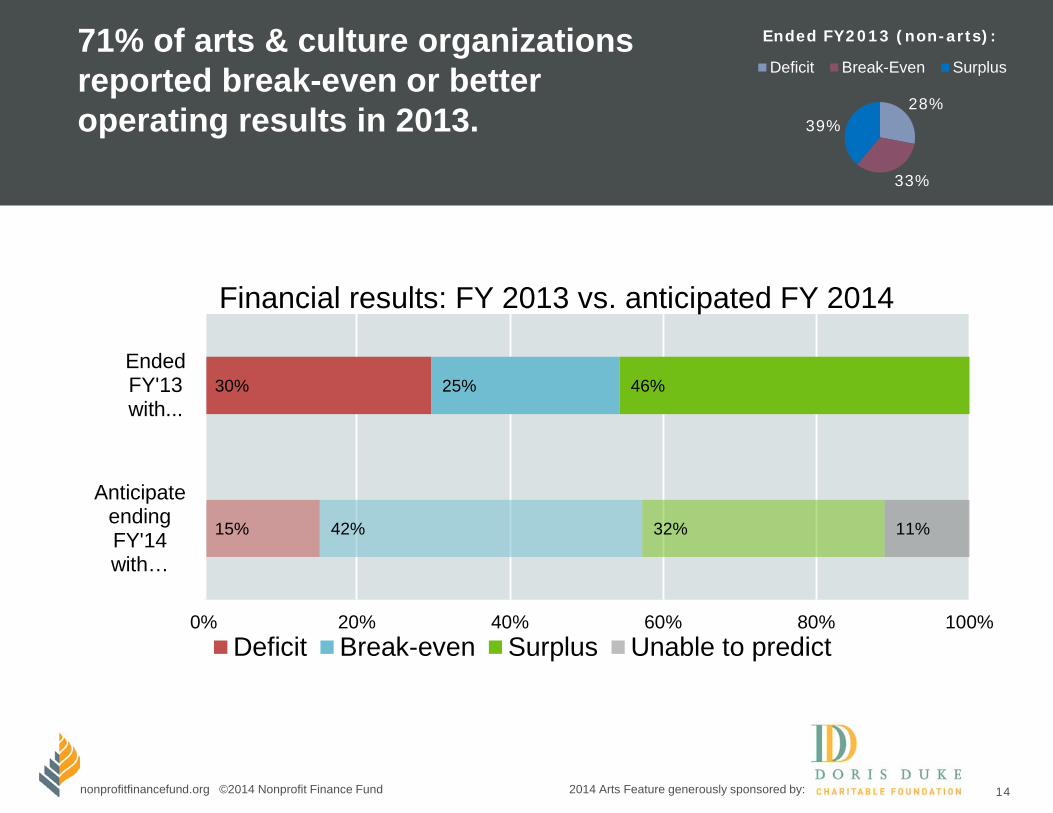

71% of arts & culture organizations reported break-even or better operating results in 2013. 28%

33%

39%

Ended FY2013 (non-arts):

Deficit Break-Even Surplus

15%

30%

42%

25%

32%

46%

11%

0% 20% 40% 60% 80% 100%

Anticipate ending FY'14 with…

EndedFY'13with...

Financial results: FY 2013 vs. anticipated FY 2014

Deficit Break-even Surplus Unable to predict

15 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Trend data show declines in the percentage of arts organizations reporting deficits.

36% 33% 30% 28% 28%

28% 22% 25% 32% 33%

36% 44% 44% 40% 39%

2009 2010 2011 2012 2013

Arts Respondents: ended the year with…

Non-arts Respondents: ended the year with…

Deficit Break-even Surplus

37% 38% 34% 31% 30%

31% 21%

23% 26% 25%

32% 42% 44% 42% 46%

2009 2010 2011 2012 2013

16 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Despite improving annual results, 41% of arts & culture groups persistently report having fewer than 3 months of cash.

Cash may be restricted or earmarked to future programs or time periods. NFF strongly recommends that organizations also calculate months of liquid net assets to understand the funds actually available to pay the bills:

Unrestricted net assets – (property & equipment – associated debt) / (total expenses / 12)

16%

25%

38%

21%

<1Month

1-2Months

3-6Months

>6Months

Months of cash (non-arts): 11%: <1 month 22%: 1-2 months 46%: 3-6 months 21%: >6 months

25% say they added to reserve funds, while 17% said they drew down reserves.

17 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

55%

27%

35%

44%48%

45%

0%

10%

20%

30%

40%

50%

60%

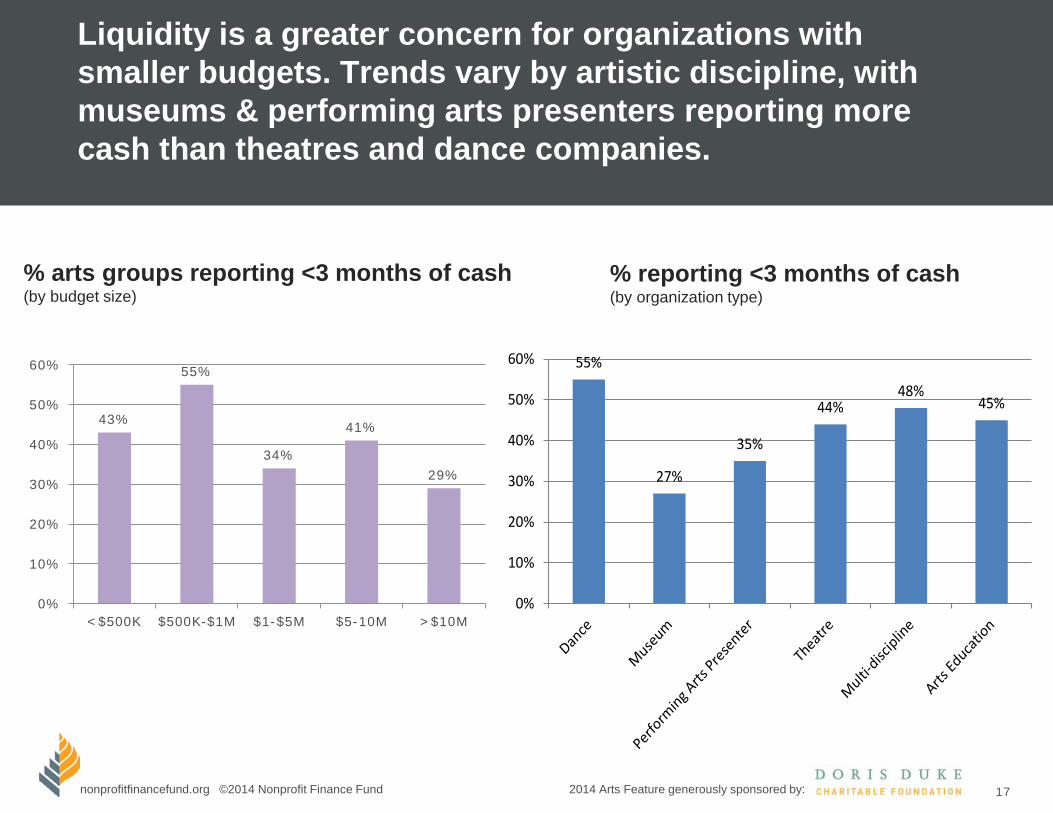

Liquidity is a greater concern for organizations with smaller budgets. Trends vary by artistic discipline, with museums & performing arts presenters reporting more cash than theatres and dance companies.

% arts groups reporting <3 months of cash (by budget size)

% reporting <3 months of cash (by organization type)

43%

55%

34%

41%

29%

0%

10%

20%

30%

40%

50%

60%

<$500K $500K-$1M $1-$5M $5-10M >$10M

18 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Nearly 50% of arts respondents cite “achieving long-term financial sustainability” as their greatest challenge.

"The local economy is still struggling. This will make it a challenge for us to balance our need for additional revenue for long-term sustainability with our wish to keep prices low for our customers who can't afford much for entertainment.” - Theatre, Oregon

Greatest Challenges Arts Respondents are Facing (respondents chose up to 3)

47%

22%

21%

19%

16%

14%

13%

13%

11%

11%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Achieving long-term financial sustainability

Not enough staff

Marketing, outreach, and community engagement

Diversifying funding sources

Developing cash reserves

Raising unrestricted revenue

Managing or pursuing growth

Raising funding that covers full costs

Having regular, reliable cash flow

Measuring impact

19 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Financial challenges notwithstanding, program and audience expansion continued apace for many. (Notably, collaboration is less prominent in the arts than other sectors.)

50%

46%

44%

25%

20%

16%

12%

11%

53%

44%

50%

30%

19%

26%

15%

18%

0% 10% 20% 30% 40% 50% 60%

Add or expand programs or services

Increase the number of people served or audience reached

Collaborate with another organization to improve/increase programs or services offered

Upgrade hardware or software to improve service or program delivery

Expand geographies served

Use, purchase, or upgrade software specifically to capture data on program impact

Increase amount of service per client or programs per visitor/audience member

Reduce or eliminate programs or services

Program-related Actions Taken in 2013

Arts Non-arts

20 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

However, arts & culture nonprofits invested less in personnel (through hiring, salaries & professional development) than the greater nonprofit sector.

44%

39%

36%

36%

35%

32%

25%

20%

52%

44%

50%

49%

36%

32%

31%

30%

0% 10% 20% 30% 40% 50% 60%

Hire staff for new positions

Give raises

Invest money or time in professional development for staff

Make replacement hires

Engage more closely with your board through more frequent reports and meetings

Retain all existing personnel

Rely more on volunteers

Invest money or time in coaching or training for executive leadership

Arts Non-arts

Personnel-related Actions Taken in 2013

21 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

What top management strategies did arts & culture groups undertake to improve their situation? Many focused on planning. Few launched capital campaigns or purchased/renovated facilities.

37%

36%

23%

22%

21%

16%

11%

8%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Conduct long-term strategic or financial planning

Upgrade hardware or software to improve organizational efficiency

Use outside help to improve financial knowledge or capacity

Collaborate with another organization to reduce administrative expenses

Pursue an earned revenue venture

Undergo organizational restructuring

Launch a capital campaign

Purchase a facility, or renovate a facility you own

22 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Table of Contents

About Nonprofit Finance Fund & the Survey

Program Trends: Demand, Engagement, & Competition

Financial Health & Management Actions Taken

Grantmaking Trends: Dynamics of Private & Public Funding

Measuring Impact

Conclusion: Looking Ahead & Tips for Cultural Nonprofits

23 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Addressing unhealthy finances will require more candid grantmaker-grantee dialogue. Respondents report comfort in talking to funders about program expansion, but not long-term financial needs.

My organization can have open dialogue with funders about…

“We launched a special campaign dedicated to risk capital. It is a hard case to make, and fundraising has been slow but steady. But it's really proving to be a game changer. The case is that we need support that works outside the bounds of our annual budget so we can say 'yes' to different kinds of projects.” - Theatre, Washington, DC

53%

36%

22%

21%

12%

12%

11%

9%

9%

3%

2%

0% 10% 20% 30% 40% 50% 60%

Expanding programs

General operating support

Acquiring or renovating a facility

Multi-year funding

I do not feel that my funders are willing toengage in open dialogue about these topics

Developing reserves for operating needs(money for rainy day)

Working capital (cash flow needs)

Developing reserves for long-term facility /fixed asset needs

Flexible capital for change/growth(including impact investing products)

Other reserves or topics

Paying off loans

24 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

General operating support & grants for expanding programs were the most common types of funding received. Far fewer organizations received funding for flexible capital and reserves.

58%

44%

30%

18%

11%

8%

8%

5%

5%

2%

0% 10% 20% 30% 40% 50% 60% 70%

General operating support

Expanding programs

Multi-year funding

Acquiring or renovating a facility

Working capital (cash flow needs)

Flexible capital for organizationalchange/growth

Developing reserves for operating needs(money for a rainy day)

Developing reserves for artistic risk-taking

Developing reserves for long-termfacility or fixed asset needs

Paying off loans

Funding received in the past year “The most helpful funding is multi-year, significant general operating support with partners that have a committed relationship with our institution.” - Theatre, New York

25 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

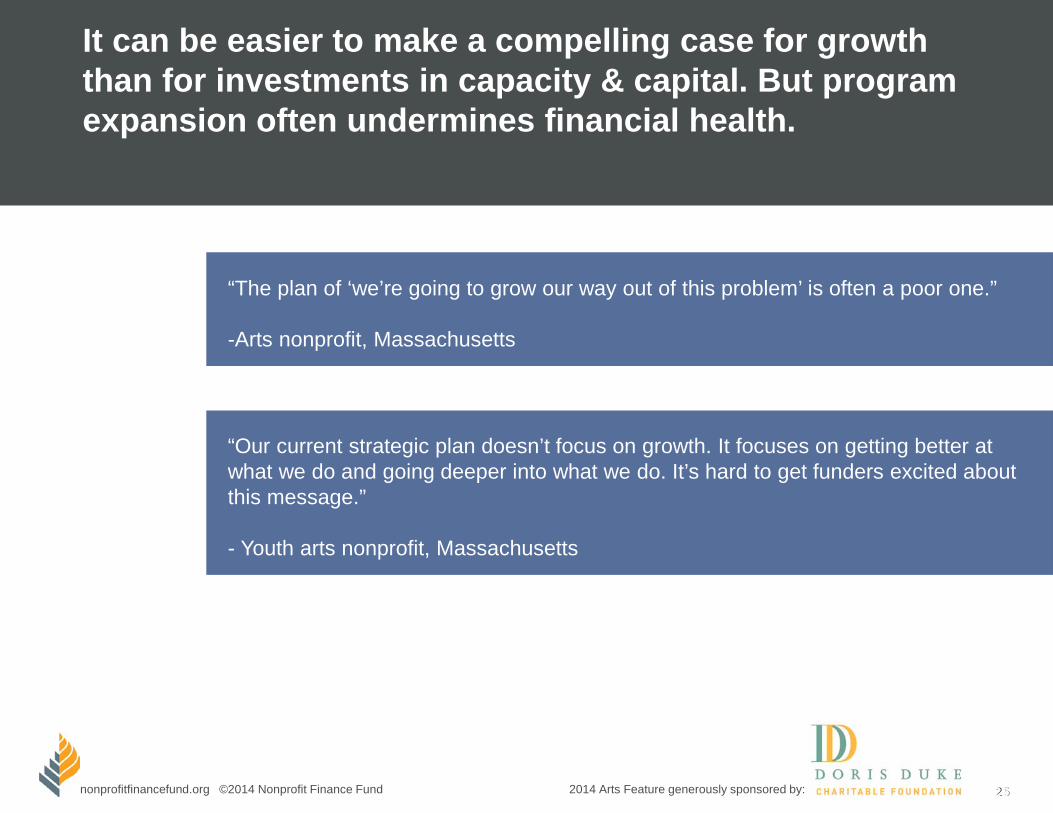

It can be easier to make a compelling case for growth than for investments in capacity & capital. But program expansion often undermines financial health.

25

“The plan of ‘we’re going to grow our way out of this problem’ is often a poor one.” -Arts nonprofit, Massachusetts

“Our current strategic plan doesn’t focus on growth. It focuses on getting better at what we do and going deeper into what we do. It’s hard to get funders excited about this message.” - Youth arts nonprofit, Massachusetts

26 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

42%

33%

29%

21%

21%

15%

13%

3%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Faced reporting requirements that were outsized relative to thesize of the grant

Benefited from a funder’s non-monetary resources or knowledge (e.g., convenings, network-building, referrals)

Applied for a grant that restricted allowable overhead rate

Invited by a funder to openly discuss financial health and long-term financial needs

Benefited from a funder’s decision to streamline application and/or due diligence process

Told by a funder that a grant award was approved because ofa track record of strong financial management and surpluses

Invited to give input on a funder’s strategy

Told by a funder that a grant award was denied because of atrack record of surpluses and savings

Cultural organizations report experiencing grantmaking practices both conducive to, and disruptive of, effective planning and management.

Grantmaking practices experienced in the past year

27 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

While more than 40% of respondents say private philanthropists rarely or never pay full program costs, government is even less likely to offer full cost coverage.

How often do funders cover the full costs of programs they intend to support?

“We have not generated adequate unrestricted operating support to maintain our operations. More and more gifts and grants have restrictions, and some even prohibit any indirect or overhead support. Collectively, we have to help the donor community know that programs cannot be offered [if they don’t] contribute to our indirect costs.” - Science center, Washington

54%

63%

60%

31%

36%

33%

14%

14%

15%

17%

23%

19%

13%

10%

10%

28%

19%

23%

8%

5%

8%

14%

11%

14%

9%

5%

4%

5%

3%

9%

3%

3%

3%

5%

9%

3%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Local gov't

State gov't

Federal gov't

Private/communityfoundations

Corporations/corporate foundations

Individuals

Never Rarely Sometimes Often Always N/A

28 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

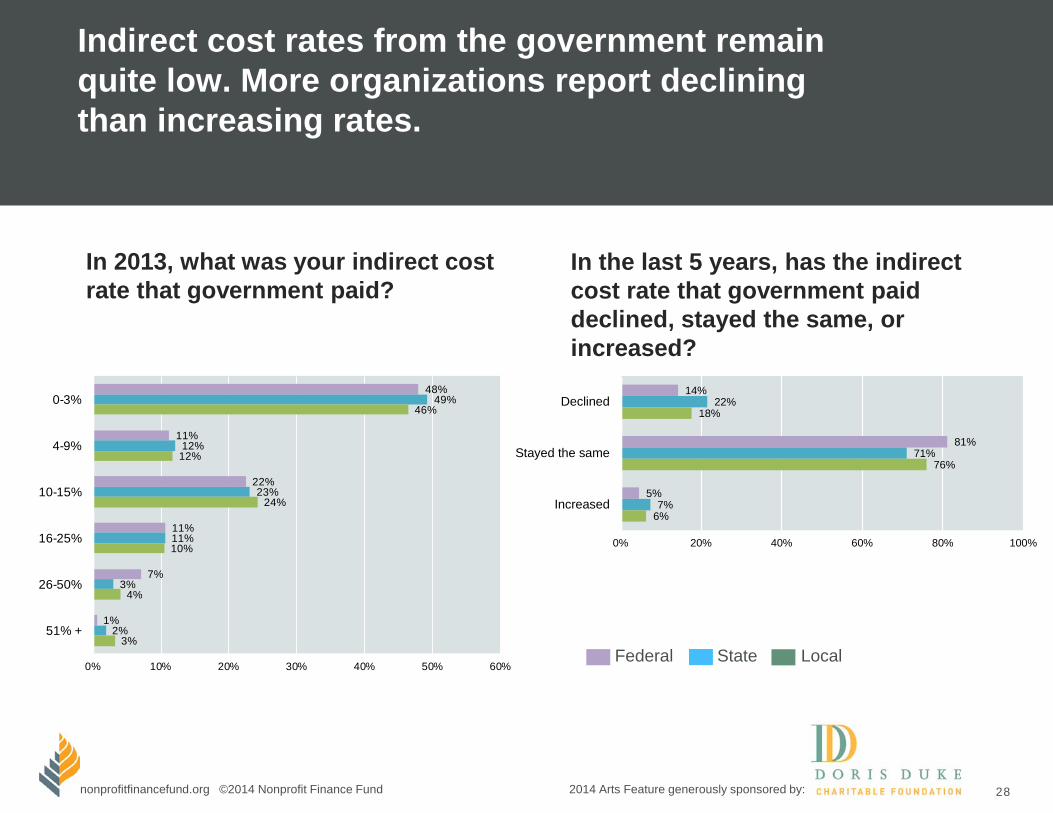

Indirect cost rates from the government remain quite low. More organizations report declining than increasing rates.

In 2013, what was your indirect cost rate that government paid?

In the last 5 years, has the indirect cost rate that government paid declined, stayed the same, or increased?

Federal State Local

48%

11%

22%

11%

7%

1%

49%

12%

23%

11%

3%

2%

46%

12%

24%

10%

4%

3%

0% 10% 20% 30% 40% 50% 60%

0-3%

4-9%

10-15%

16-25%

26-50%

51% +

14%

81%

5%

22%

71%

7%

18%

76%

6%

0% 20% 40% 60% 80% 100%

Declined

Stayed the same

Increased

29 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

More than 40% of organizations report that government funding at the state and local levels arrives late.

29

2%

67%

13%

11%

5%

2%

52%

15%

15%

16%

3%

56%

16%

16%

9%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Ahead of scheduledpayment date

On scheduledpayment date

1-30 days late

31-90 days late

> 90 days late

Federal gov't

State gov't

Local gov't

When do you receive payments from the government?

30 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

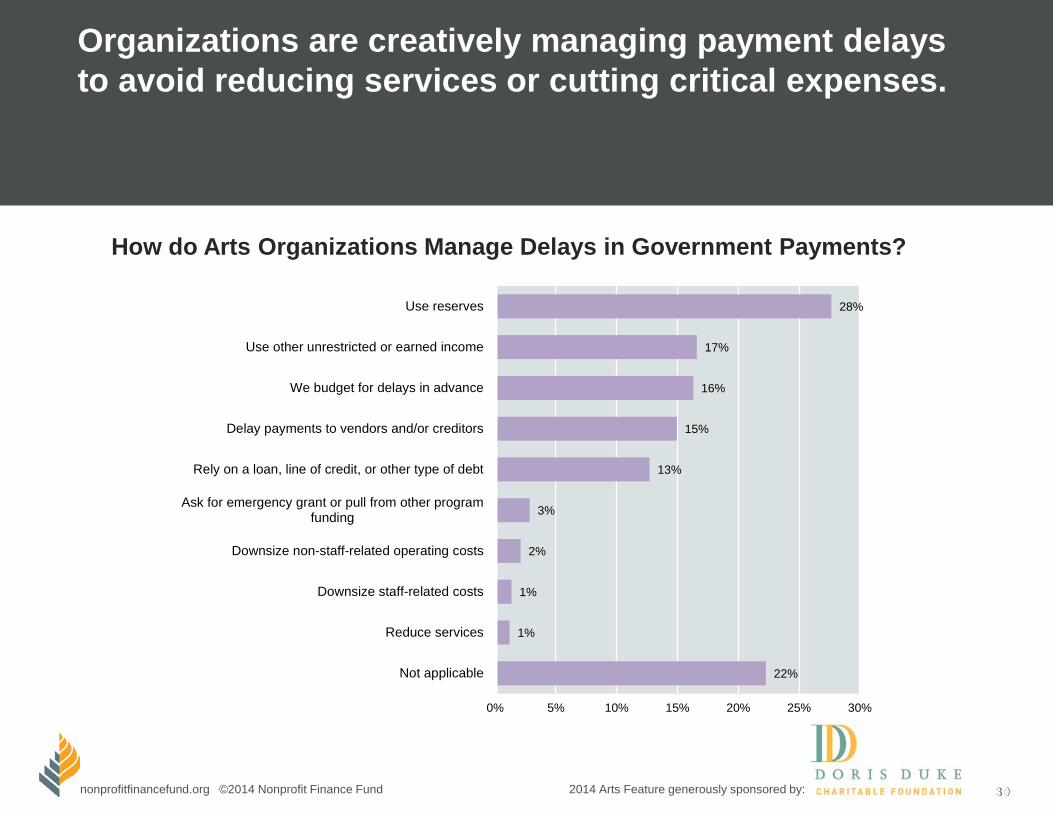

Organizations are creatively managing payment delays to avoid reducing services or cutting critical expenses.

30

How do Arts Organizations Manage Delays in Government Payments?

28%

17%

16%

15%

13%

3%

2%

1%

1%

22%

0% 5% 10% 15% 20% 25% 30%

Use reserves

Use other unrestricted or earned income

We budget for delays in advance

Delay payments to vendors and/or creditors

Rely on a loan, line of credit, or other type of debt

Ask for emergency grant or pull from other programfunding

Downsize non-staff-related operating costs

Downsize staff-related costs

Reduce services

Not applicable

31 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Table of Contents

About Nonprofit Finance Fund & the Survey

Program Trends: Demand, Engagement, & Competition

Financial Health & Management Actions Taken

Grantmaking Trends: Dynamics of Private & Public Funding

Measuring Impact

Conclusion: Looking Ahead & Tips for Cultural Nonprofits

32 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Proving impact becomes increasingly important in an uncertain philanthropic marketplace. The arts & culture sector measures outcomes data less frequently than the broader nonprofit sector.

How often does your organization pursue the following (related to program impact)?

32%

4%

22%

22%

30%

6%

30%

31%

31%

21%

34%

32%

7%

69%

15%

14%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Use an external evaluator to assess the effectiveness of our programsor services

Collect program data on productivity, such as the number of clients orsize of audience served

Collect long-term data on how our services change the lives of ourclients or audience members

Collect long-term data on how our services or programs affect thecommunity in which we live

Never Rarely Sometimes Regularly

33 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

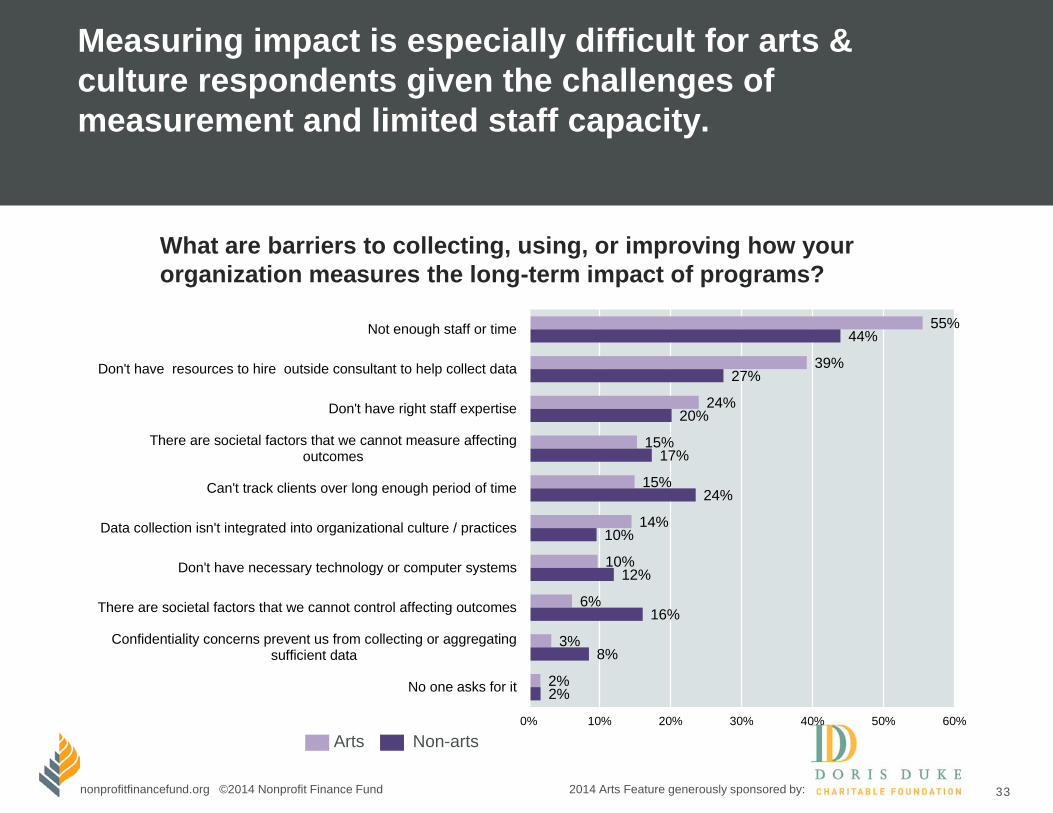

Measuring impact is especially difficult for arts & culture respondents given the challenges of measurement and limited staff capacity.

55%

39%

24%

15%

15%

14%

10%

6%

3%

2%

44%

27%

20%

17%

24%

10%

12%

16%

8%

2%

0% 10% 20% 30% 40% 50% 60%

Not enough staff or time

Don't have resources to hire outside consultant to help collect data

Don't have right staff expertise

There are societal factors that we cannot measure affectingoutcomes

Can't track clients over long enough period of time

Data collection isn't integrated into organizational culture / practices

Don't have necessary technology or computer systems

There are societal factors that we cannot control affecting outcomes

Confidentiality concerns prevent us from collecting or aggregatingsufficient data

No one asks for it

What are barriers to collecting, using, or improving how your organization measures the long-term impact of programs?

Arts Non-arts

34 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

78% say funders rarely or never cover the costs associated with impact measurement.

40%

38%

18%

3%

0%

0% 10% 20% 30% 40% 50%

Never

Rarely

Sometimes

Often

Always

How often do funders cover the costs associated with impact measurement?

35 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Table of Contents

About Nonprofit Finance Fund & the Survey

Program Trends: Demand, Engagement, & Competition

Financial Health & Management Actions Taken

Grantmaking Trends: Dynamics of Private & Public Funding

Measuring Impact

Conclusion: Looking Ahead & Tips for Cultural Nonprofits

36 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Looking Ahead: Steps cultural nonprofits & their funders can take to propel change

Nonprofits: Develop strategies that integrate financial planning with operational and program

planning, Understand and seek funding for the full costs of projects/programs, Budget and manage to operating surpluses, Prioritize working capital and savings for periodic risk-taking and change, and Clearly communicate your financial goals, priorities and timeline in the context of

your art-making.

Funders: Encourage integrated planning that links program, operations, and finances to

strategy, Fund projects and programs at full costs, Reward rather than penalize surpluses, Seed reserves for liquidity, risk-taking, and change, and Engage in dialogue with your staff, grantees, and peer funders about

capitalization principles as a means to artistic freedom.

37 nonprofitfinancefund.org ©2014 Nonprofit Finance Fund 2014 Arts Feature generously sponsored by:

Nonprofit Finance Fund Where Money Meets Mission ®

Learn more at: http://nff.org/survey [email protected]

Interact with the data yourself at: survey.nff.org

Visit our Arts Resource Page:

http://nonprofitfinancefund.org/partnerships/artsandculture

Stay connected: Twitter.com/nff_news Facebook.com/nonprofitfinancefund

37