2014 mba guide to hiring in the private equity, venture capital and hedge fund industries

TRANSCRIPT

MBA Hiring Outlook

for the Buyside

GLOCAP

Q4 2014

GLOCAP

Glocap Search – at a glanceEstablished in 1997 and headquartered in New York City, Glocap Search is a

recruiting firm focused on helping the buyside; Glocap has placed over 1000

investment professionals into investment management firms ranging from start-

ups to PE mega-funds, leading VCs and the world’s largest hedge funds; given

this, Glocap is one of the world’s largest and longest-serving buyside recruiters

3 offices nationwide, 40+ staff

Over 1 million candidates

Client retention rate of >90%, with deep penetration (for example, having placed people at 30 of the 40 largest HFs, and most of the top VCs)

Chiefly staffed by ex-industry professionals, top college grads and MBAs

Focus on pre- and post-MBA recruiting into investment professional roles (and other roles like strategy positions, marketing, COO/CFO roles)

GLOCAP

Some Key Points about MBA Hiring

The MBA market for buyside recruiting remains competitive; it’s hard to transition into the industry (for 1st years, a relevant summer internship is key, regardless of prior experience)

Be proactive with funds as early as possible and stay in close contact with them throughout the year as their needs become clearer; be patient, do homework on opportunities and network

Recruiters can be a useful part of a job search: sign up on glocap.com and request to receive post-MBA roles now so that you may see opportunities that we start working on throughout the year

GLOCAP

A Few Stats to Consider

LEAVING B-SCHOOL WITHOUT A JOB?

At the top business schools, up to 25% of students don’t have job

offers by graduation; by the fall, this drops to below 10% - but many

settle (taking offers that aren’t always ideal)

WHAT TOOLS TO USE TO JOB SEARCH?

At the top business schools, while 50% - 75% of job acceptances come

from school facilitated opportunities (campus recruiting, internships

through school, etc.) it means 25-50% came from student facilitated

opportunities (networking, recruiters, summer internships found by the

student, etc.) – it’s very important to do both!

WHAT ARE THE OPPORTUNITIES OFF-CAMPUS?

Most funds don’t come to campus; many are not actively looking for MBAs. In the Hedge Fund space for example, bschools rarely have more than 30 HFs coming to campus, though the universe of registered HFs is now over 10,000

GLOCAP

Agenda

State of the PE/VC/Hedge Fund Industry

The Job Market and the Competition

Getting a Job on the Buyside

Compensation

GLOCAP

State of the Industry

GLOCAP

U.S. PE Deal Flow by Quarter

Source: PitchBook, as of 6/30/14

Deal-making has held fairly steady over the last few quarters$51

$28

$34

$55

$76

$86

$78

$135

$96

$86

$95

$120

$89

$91

$93

$178

$83

$101

$120

$151

$108

409366 365

443

535493 504

700

612 595 578

632610

563 557

814

547 552

678633

589

0

100

200

300

400

500

600

700

800

900

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2009 2010 2011 2012 2013 2014

Capital Invested ($B) # of Deals Closed

GLOCAP

U.S. VC Deal Flow by QuarterCapital invested hit a post dot-com boom record in 2Q 2014

$6.5

$7.8

$6.6

$6.7

$10.6

$9.8

$10.2

$9.1

$9.1

$10.3

$8.7

$8.4

$8.8

$9.3

$9.1

$9.8

$12.5

$16.4

9541,003

938993

1,2771,2021,229

1,175

1,4841,469

1,3551,301

1,4371,383

1,294

1,1621,1551,117

0

200

400

600

800

1,000

1,200

1,400

1,600

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2010 2011 2012 2013 2014

Capital Invested ($B) # of Deals ClosedSource: PitchBook

GLOCAP

Hedge Fund Industry Assets

Industry Assets remain at record

levels, now estimated at $2.8T

GLOCAP

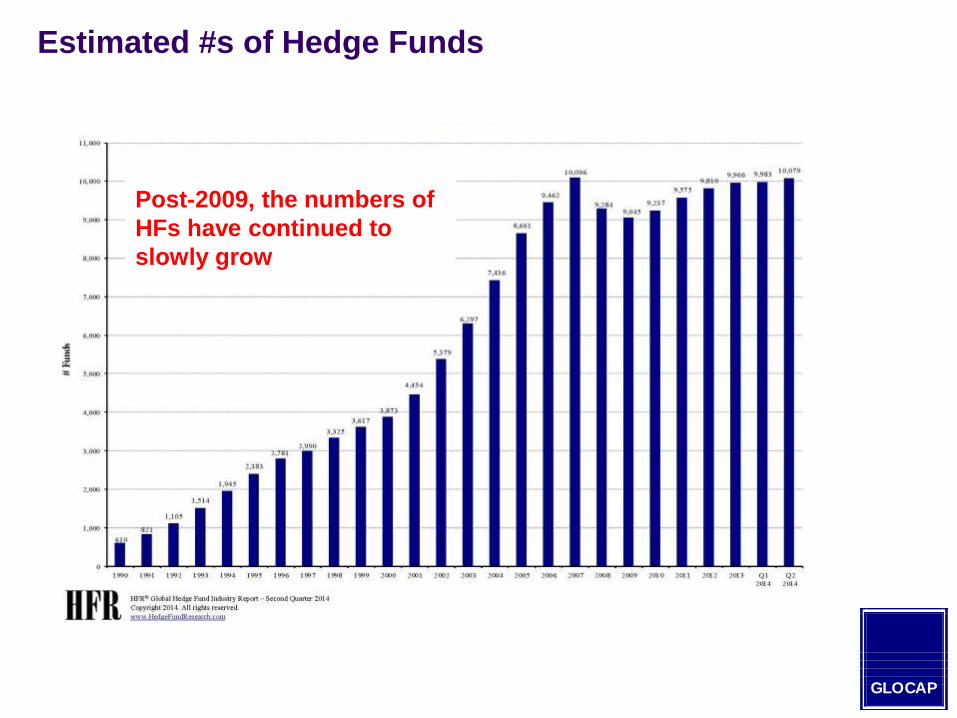

Post-2009, the numbers of

HFs have continued to

slowly grow

Estimated #s of Hedge Funds

GLOCAP

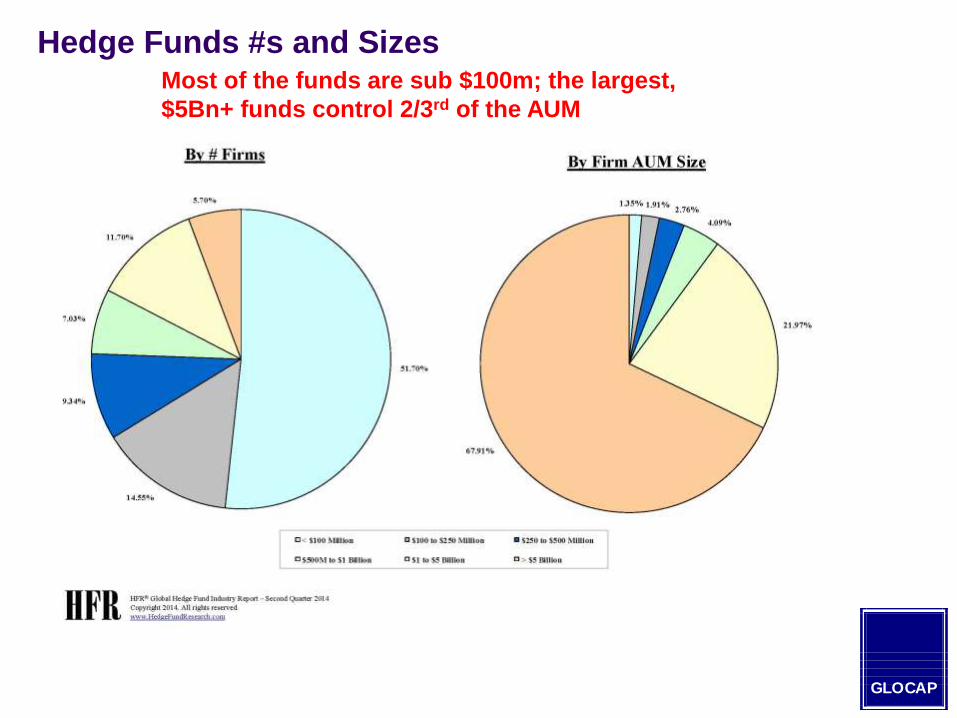

Most of the funds are sub $100m; the largest,

$5Bn+ funds control 2/3rd of the AUM

Hedge Funds #s and Sizes

GLOCAP

The Job Market &

The Competition

GLOCAP

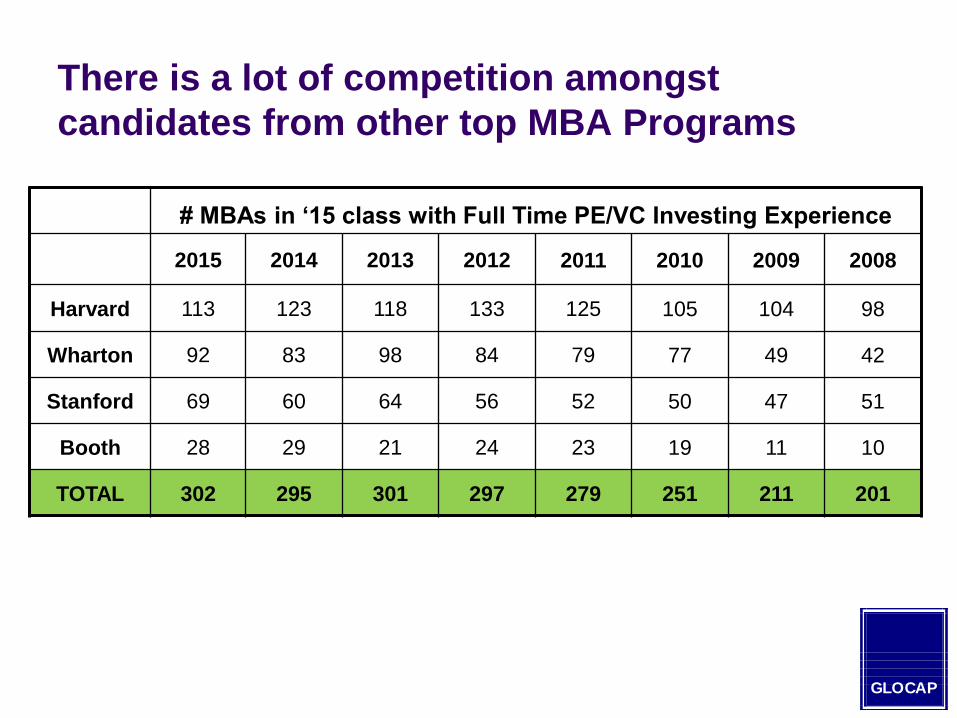

There is a lot of competition amongst

candidates from other top MBA Programs

# MBAs in ‘15 class with Full Time PE/VC Investing Experience

2015 2014 2013 2012 2011 2010 2009 2008

Harvard 113 123 118 133 125 105 104 98

Wharton 92 83 98 84 79 77 49 42

Stanford 69 60 64 56 52 50 47 51

Booth 28 29 21 24 23 19 11 10

TOTAL 302 295 301 297 279 251 211 201

GLOCAP

Recruiting Perspective on PE

Only a subset of MBAs with prior PE experience return to the buyside. As a result, more candidates are going the operating, consulting or entrepreneurial routes. Two schools reported ~55% of 2013 MBAs returned to the buyside after graduation

In 2012, 65% of MBAs returned to the buyside

These numbers are down from 85+% who returned to the buyside prior to the downturn in 2008/9.

For MBAs with previous PE experience

PE internship opportunities seem to be decreasing over the past few years, although there are

still funds using them as an extended interview process

MBAs are increasingly looking to diversify their experiences over the summer with internships in

operations/consulting rather than more PE investing opportunities

For MBAs without previous PE experience

For those who broke into the industry after graduation, specifically those with two to four yrs of

investment banking/consulting experience plus a summer PE internship fared best

There aren’t many of them, but a small number of these summer internships do turn into full time

offers

GLOCAP

While still highly valued, having an MBA is not as much of a pre-requisite for

obtaining or staying in VC long-term, unlike the PE job market

Venture capital firms are increasingly looking at people with more varied

backgrounds

People accepting post-MBA VC jobs are those who have typically two

years of banking or consulting followed by a few years of VC, start-up or

operating experience within a technology firm (for example, Dropbox,

Google, Facebook or Microsoft)

VC firms are looking for candidates with strong networks and a

willingness to source

Firms are looking for more specific tech knowledge and vertical expertise

Those recruiting for post-MBA VC jobs are often recruiting against laterals

(people with four to five years of post-MBA experience without an MBA) as well

as people who have one to two years post-MBA

Recruiting Perspective on VC

GLOCAP

Recruiting Perspective on Hedge Funds

Tailwinds:

The majority of hiring at hedge funds is at the junior and mid-levels (i.e. 2-8 years of experience, where most MBAs are) These hires are relatively cheap, come in trained and do the majority of the heavy

lifting

Junior bench is typically the first to see rebound in demand

Hedge funds are showing a growing interest in MBA talent Larger, more established platforms increasingly on campus

Broader MBA skills and perspectives are being valued, in addition to investment/trading skills, as are fundamental PE skills Big picture perspectives, risk considerations, extensive research experience

2014 showed instances of successfully negotiated comp packages by MBA graduates Including guarantees and sign-ons

Some 2015 MBAs have already received offers from their summer internships at hedge funds

GLOCAP

An MBA still does not provide a SIGNIFICANT competitive

advantage to hedge fund candidates

Despite increasing interest from select hedge funds for MBA talent, the vast

majority still do not place a premium on the degree

There are instances in which MBA candidates are selected against (attitude,

financial expectations, time out of the market)

The competition is as fierce as ever. You are up against:

Lateral hedge fund candidates

PE / VC candidates who want to move to the public markets

CFA / Master’s candidates

Majority of candidates who transition to a hedge fund from b-school

have previous buy-side experience (HF, PE, long-only)

Few candidates with only investment banking, consulting, industry or “other”

backgrounds successfully make the transition (summer internship is key)

Bottom line: you have to REALLY want it

Recruiting Perspective on Hedge Funds

Headwinds:

GLOCAP

Getting a Job on the Buyside

GLOCAP

Tips on Career TransitioningIn our experience, you can typically only change one element of your career

path at a time. For example, thinking about GEOGRAPHY, INDUSTRY and

STRATEGY/SECTOR…

STARTING

EXPERIENCE

TRANSITION TRANSITION

US, HF, Credit London, HF, Credit US, HF, Cross-Asset

US, PE, Industrials US, PE, Energy/Power US, HF, Industrials

Japan, PE, Tech US, HF, L/S Equity

generalist

OR

OR

Reasonable

Reasonable

Challenging

GLOCAP

General Tips on Getting a Buyside Job

CLARIFY GOALS AND IDENTIFY TARGETS

Know what you want, and be efficient with your time

Identify industry focus/expertise, investment stage and size of fund

Research funds that have hired MBAs in the past and know what they look for

DO YOUR HOMEWORK

Know what your strengths are; identify and convey your edge to show

differentiation

Know your deals, speak to your roles

Prepare investment ideas

DEMONSTRATE YOUR PASSION

Offer to do project work/ consult (perhaps for free if you can do that)

Don’t rely on your resume for them to be impressed; it’s a door-opener at best

The best positioning is you’re not ‘looking for a job’; you’re looking to invest on their

platform and add to their team which will improve that firm’s performance

GLOCAP

Then…NETWORK

Undergrad

Bschool

Alumni

Former

Employer

Recruiters

People like to help their own . . . the worst they

can do is say no

Fraternity /

Sorority

Industry

events

GLOCAP

International Perspective RETURNING NATIONALS ARE OFTEN IN DEMAND

You have the language, the cultural understanding and the network, plus the US

experience

IF YOU WANT TO STAY IN THE US

How does your background differentiate you? E.g. you’re from Asia and want to

stay in the US and focus on Consumer sector investments, you can make the case

you’re well-placed to understand the drivers of global consumer demand given your

background

If you have family/ties to the US, play them up – firms want to see a commitment

that you’re here for the long-term

NEW H1B VISAS ARE IN SHORT SUPPLY

But use OPT time

H1B transfers are pretty straightforward (be ready to educate firms not familiar with

the process, and offer to pay and handle the paperwork)

If you’re a US citizen or Green card holder but this wouldn’t be obvious from your

background, then highlight this in your resume! Firms aren’t allowed to ask about

this, and generally look to hire the best regardless of citizenship status, but it can

only help you

GLOCAP

Hedge Fund and Venture Capital hiring occurs less systematically and more often occurs in Q1/Q2 of your second year

For Hedge Funds, many people graduate without a job and pick up a strong position over the summer, in the fall

The PE MBA Recruiting Cycle

1st Semester

Aug – early Oct:

Mega/Large PE

Funds

Oct – Dec:

Large and middle

market funds

2nd Semester

Middle market

and smaller

funds

Post Grad

Just in time

hiring needs

Most larger funds

with predictable

annual hiring needs

and a focus on

pedigree come to

market first – but

there are more

exceptions to that

rule each year

Large/ Upper Middle

Market funds with

unfilled spots and

mid-size funds

whose hiring needs

have become

apparent by later in

the 1st semester

Mid-size and smaller

funds that may not have

known needs prior to the

new year and that are not

as anxious about specific

candidate characteristics

Typically smaller

funds with unforeseen

hiring needs, although

there have been

notable exceptions in

recent years

Start of hiringEnd of hiring

GLOCAP

Compensation

GLOCAP

Compensation Data – PE/VC Overall compensation has remained flat since the 2008/2009 downturn

Generally speaking, fund size drives buyside fund compensation for post-MBA graduates

PE PE compensation for recent MBA graduates

Many but not all PE funds offer MBAs carry within the first year of employment

VC

More variance in the total compensation figures in VC

Typically pay at a discount to traditional PE funds (sometimes as much as 30%+ lower

Usually structure comp for a higher base and lower target bonus

PE firms are more likely to give a sign on bonus than VC firms but it does vary

Many Investment Banks have announced they will increase Analyst comp (i.e. GS plans to increase base by 20%), we expect this to cause firms to revaluate compensation in the near term

GLOCAP

<$300M $300 - $750M $750M to $2B $2B to $5B Megafund

Base $100K - $125K $110K - $135K $135K - $165K $140K - $175K

$150K -

$200K+

Bonus 75% - 125% 90% - 150% 100% - 150% 100% - 150% 125% - 200%+

Total $200 - $275k $225 - $300k $275 - $375k $315 - $425k $400 - $525k+

GLOCAP

Compensation Data – Hedge Funds

For the MBA class of 2014, base packages were typically in the $125k-$175k range and all-in compensation expectation $240k-$450k

Several instances of successfully negotiated packages to include a sign-on (often $25-30k)

BUT typically few instances of bonus guarantees, more typically ‘bonus guidance’

GLOCAP

Small <$500M Mid $500M - $4Bln Large $4Bln+

Base $125K - $175K $150K - $225K $150K - $275K

Bonus $125K - $400K $250K - $850K $340K - $1.4M

Total $250K - $575k $400K - $1.1M $490K - $1.7M

*Compensation data for a “Level II” professional or ‘Idea Generator’ at mid-performing funds, based on 2014

comp data

2014 Compensation data for “Idea Generators”*

On average,

5-10% up on

2013 for top

performers

GLOCAP

The Key Points in Conclusion

The MBA market for buyside recruiting remains competitive; it’s hard to transition into the industry (for 1st years, a relevant summer internship is vital)

Be proactive with funds as early as possible and stay in close contact with them throughout the year as their needs become clearer; be patient, do homework on opportunities and network

Recruiters can be a useful part of a job search: sign up on glocap.com and request to receive post-MBA roles now so that you may see opportunities that we start working on throughout the year

GLOCAP

MBA Recruiting Contacts

HEDGE FUNDS

Anthony Keizner (NY), [email protected]

Kristin Sartorius (MBA coordinator), [email protected]

PE/VC

Diane Tseng (SF), [email protected]

Sarah Moffet (SF), [email protected]

Pamela Lang (NY), [email protected]

Kelley Finlayson (NY), [email protected]

212.333.6400

JOB SEEKERS – CREATE A CONFIDENTIAL

PROFILE AT www.glocap.com

AND SIGN UP TO RECEIVE NEW BUYSIDE JOB

POSTINGS