hedge funds in a modern portfolio · 5 hedge funds in a modern portfolio 1 the best of both worlds...

TRANSCRIPT

Hedge funds in a modern portfolio

Hedge funds in a modern portfolioPortfolioConstruction Conference 2006

Patrick TuohyAsia Head

Alternative Investments Group24 August 2006

Hedge funds in a modern portfolio2

1

2

3

4

5

6

7

8

The Past – Where are we today and why did we get here? 3

The Present – Absolute returns are all relative 11

The Future – The evolution continues 15

Contents

1. The Past

Hedge funds in a modern portfolio4

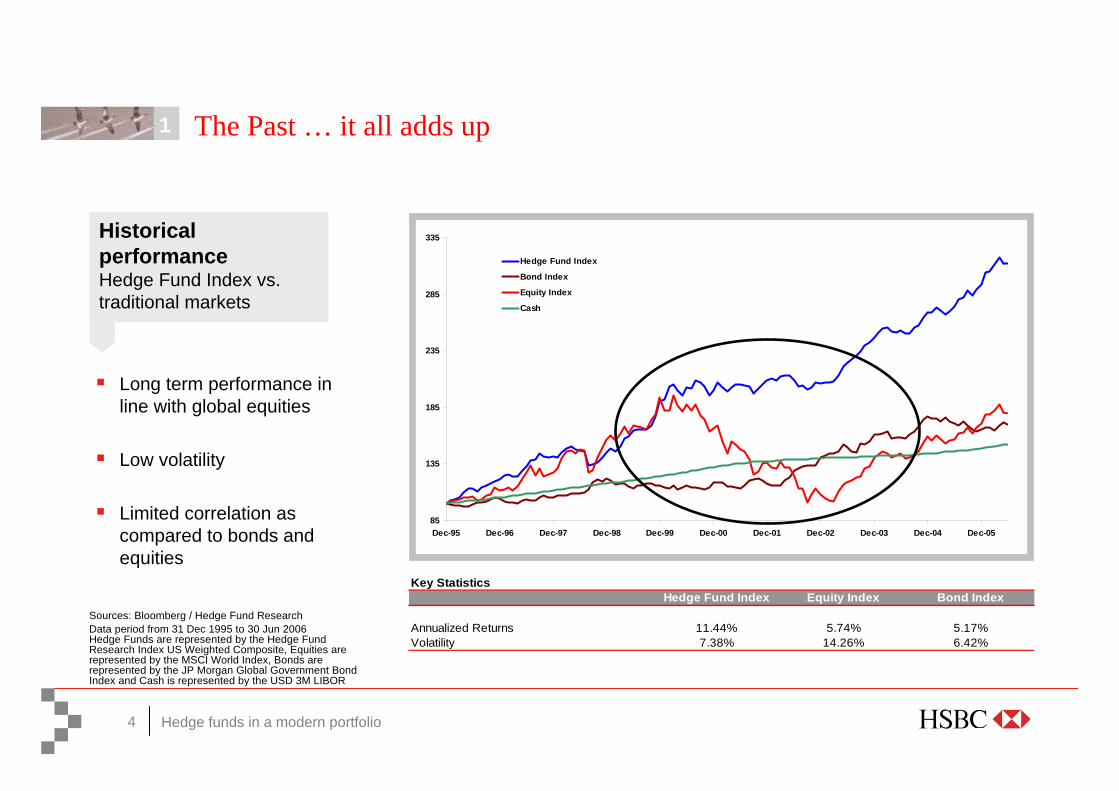

1 The Past … it all adds up

85

135

185

235

285

335

Dec-95 Dec-96 Dec-97 Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05

Hedge Fund Index

Bond Index

Equity Index

Cash

Long term performance in line with global equities

Low volatility

Limited correlation as compared to bonds and equities

Historical performanceHedge Fund Index vs. traditional markets

Key StatisticsHedge Fund Index Equity Index Bond Index

Annualized Returns 11.44% 5.74% 5.17%Volatility 7.38% 14.26% 6.42%

Sources: Bloomberg / Hedge Fund Research Data period from 31 Dec 1995 to 30 Jun 2006Hedge Funds are represented by the Hedge Fund Research Index US Weighted Composite, Equities are represented by the MSCI World Index, Bonds are represented by the JP Morgan Global Government Bond Index and Cash is represented by the USD 3M LIBOR

Hedge funds in a modern portfolio5

1 The best of both worlds

Sources: Bloomberg / Hedge Fund ResearchHedge Funds are represented by the Hedge Fund Research Index US Weighted Composite, Equities are represented by the MSCI World Index, Bonds are represented by the JP Morgan Global Government Bond Index and Cash is represented by the USD 3M LIBOR

Jan 2000 – Dec 2002

Demonstrates cash like returns in equity down periods

50

70

90

110

130

150

Dec-99 Jun-00 Dec-00 Jun-01 Dec-01 Jun-02 Dec-02

Hedge Fund IndexEquity IndexBond IndexCash

Jan 2003 – Jun 2006

Demonstrates growth in line with equity trends

60

80

100

120

140

160

180

200

Dec-02 Jun-03 Dec-03 Jun-04 Dec-04 Jun-05 Dec-05 Jun-06

Hedge Fund IndexEquity IndexBond IndexCash

Hedge funds in a modern portfolio

80

130

180

230

280

330

380

430

Dec-93 Dec-94 Dec-95 Dec-96 Dec-97 Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05

Hedge Fund Research Index US Weighted CompositeMSCI World IndexJP Morgan Global Gov't Bond Index

6

1 Protection against major market events

Event Period HFRIFWI MSCI Event Period HRFIFWI MSCI

Fed raised rates Feb - Dec 1994 2.13% -1.47% Tech bubble-burst & market down cycle Jan 2000 - Dec 2002 8.26% -44.24%

Mexican Peso crisis Dec 1994 -0.08% 0.80% “9/11” terror attack Sept 2001 -2.83% -8.92%

Collapse of LTCM Jul -Aug 1998 -8.70% -13.45% The Iraq War Mar 2003 0.14% -0.56%

Sources: Bloomberg / Hedge Fund Research Data period from 31 Dec 1993 to 31Jun 2006

FED rate hikes / Peso crisis Technology bubble burst

LTCM crisis

9/11 Terror attack

Iraq War

Hedge funds in a modern portfolio7

1 Hedge fund strategies – Change over time (1990)

Source: Hedge Fund Research

Hedge funds in a modern portfolio8

1 Hedge fund strategies – Change over time (Q2 2006)

Source: Hedge Fund Research

Hedge funds in a modern portfolio

Hedge funds in a modern portfolio10

1 The experience to date

Sources: Bloomberg / Hedge Fund Research Data period from 31 Dec 1995 to 30 Jun 2006 Hedge Funds are represented by the Hedge Fund Research Index US Weighted Composite, Equities are represented by the MSCI World Index, and Bonds are represented by the JP Morgan Global Government Bond Index

Without hedge fund

90

110

130

150

170

190

210

230

Dec

-95

Apr

-96

Aug-

96

Dec

-96

Apr

-97

Aug-

97

Dec

-97

Apr

-98

Aug-

98

Dec

-98

Apr

-99

Aug-

99

Dec

-99

Apr

-00

Aug-

00

Dec

-00

Apr

-01

Aug-

01

Dec

-01

Apr

-02

Aug-

02

Dec

-02

Apr

-03

Aug-

03

Dec

-03

Apr

-04

Aug-

04

Dec

-04

Apr

-05

Aug-

05

Dec

-05

Apr

-06

60% Equity 40% Bond

MSCI World

Traditional Portfolio

With hedge fund

90

110

130

150

170

190

210

230

Dec

-95

Apr

-96

Aug

-96

Dec

-96

Apr

-97

Aug

-97

Dec

-97

Apr

-98

Aug

-98

Dec

-98

Apr

-99

Aug

-99

Dec

-99

Apr

-00

Aug

-00

Dec

-00

Apr

-01

Aug

-01

Dec

-01

Apr

-02

Aug

-02

Dec

-02

Apr

-03

Aug

-03

Dec

-03

Apr

-04

Aug

-04

Dec

-04

Apr

-05

Aug

-05

Dec

-05

Apr

-06

33% Eq 33% Bond 33% Hedge Fund

MSCI World

Portfolio inclusive of Hedge Funds

2. The Present

Hedge funds in a modern portfolio12

2 Absolute return is all relative

Sources: Bloomberg, Hedge Fund Research 32% 21% 31% 4% 22% 21% 17% 3% 31% 5% 5% -1% 20% 9% 9% 6%

Hedge Fund Research Index Weighted Composite Performance

Net Asset Flow of Global Hedge Funds / Hedge Fund Index Performance / MSCI World Index Performance (1991 - YTD Q2 2006)

-25,000

0

25,000

50,000

75,000

100,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 YTDQ2

2006

Net

Ass

et F

low

of H

edge

Fun

ds (U

S$m

m) /

Hed

ge F

und

Res

earc

h In

dex

Perf

orm

ance

100

150

200

250

300

350

400

MSC

I World Index Perform

ance

Hedge Fund Net Asset Flow

MSCI World Index Performance

Hedge funds in a modern portfolio13

2 Demographics dictate returns

Source: 2005 Deutsche Bank Alternative Investment SurveyBased on over 1,000 representatives from 650 firms, representing US$645bn in direct hedge fund assets

Fund of Funds are the dominant player in the market

Institutions represent one third of investors

Appetite for risk has reduced

Hedge fund investors 2005

Funds of funds43%

Family Offices/High

Net Worth Individuals

15%

Pensions11%

Endowments,

Foundations7%

Corporations

4%

Consultants2%

Other6%

Insurance Companies

3%

Banks9%

Hedge funds in a modern portfolio

2 Urban myth busting

Major allocation changes driven by new fund inflows, NOT strategy views

Great quality managers in out-of-favour strategies are very often retained

Illiquid managers are avoided regardless of investment potential

Funds are (over) diversified to satisfy institutional risk appetite

14

3. The Future

Hedge funds in a modern portfolio16

3 The shape of things to come

Less liquid strategiesThe rise of the event-driven activists

Strategy and geographically focused fundsA more focused, flexible, tactical approach

Structured productsHedge fund annuities plus managed leverage

Emerging manager and incubator fundsDiamonds in the rough

ItIt’’s all about s all about higher return higher return

(and risk)(and risk)

Hedge funds in a modern portfolio

3

17

Growing trends:Move toward single country funds, specifically, Japan, Europe and AsiaMove toward strategy specific funds, principally, equity long/short, macro and CTAs

Multi-strategy funds have become more diversified and less attractive

Building blocks enabling investors to focus their portfolio allocations to achieve better returns. i.e. more tactical allocations

More likely to generate higher alpha due to managers’specialization in strategies and local expertises

Capacity has made strategy allocation increasingly more important

Strategy and geographically focused funds

Multi manager

Multi strategy

Asia & Emerging Markets

Macro

Managed Futures

Event DrivenEuropean

Core and Satellite Approach

Hedge funds in a modern portfolio

3 CTAs … a case study in diversification

18

Fed Rate Hike Feb - Dec 1994 (11 months)

-2.54%

11.26%

-5.00%

0.00%

5.00%

10.00%

15.00%

1

Managed Futures Index

MSCI World

Russian Default May - Aug 1998 (4 months)

12.99%

-12.84%-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

1

Managed Futures Index

MSCI World

LTCM Collapse - July - Sept 1998 (3 months)

15.70%

-12.10%-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

1

Managed Futures Index

MSCI World

Tech Bubble Downturn Jan 2000 - Dec 2003 (3 Yrs)

35.29%

-60.46%-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

1

Managed Futures Index

MSCI World

911 September 11th 2001 (1 month)

3.65%

-8.92%-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

1

Managed Futures Index

MSCI World

Sources: CSFB Tremont Hedge Index and Bloomberg – January 1994 to August 2005

Asian Crisis July - Oct 1997 (4 months)

1.32%

-2.42%-3.00%-2.50%-2.00%-1.50%-1.00%-0.50%0.00%0.50%1.00%1.50%2.00%

1

Managed Futures Index

MSCI World

Hedge funds in a modern portfolio

3

19

The price of liquidity

Source: Hedge Fund Research

3-year Total Return

35%44%

89%

HFRI WeightedComposite

HFRI Event DrivenIndex

HFRI DistressedIndex

Outperform by 154%

10-year Total Return

174%214% 205%

HFRI WeightedComposite

HFRI Event DrivenIndex

HFRI DistressedIndex

Outperform by 18%

5-year Total Return

53%63%

95%

HFRI WeightedComposite

HFRI Event DrivenIndex

HFRI DistressedIndex

Outperform by 79%

Represents performance of HFRI Distressed Index over HFRI Weighted Composite

Hedge funds in a modern portfolio

3

20

Emerging managers outperform veteran managers

Emerging managers (managers with less than two year track record) represent nearly 10% of the hedge fund universe based on AUM.

This counterintuitive phenomenon is mainly driven by:Greater incentive of young managers to outperform their peers to attract assetsThe nimble nature of smaller funds to focus on their best investment ideasThe application of specific expertise to niche exposures

Hedge funds in a modern portfolio

3

21

Incubator funds

PositivesStatistically start up funds enjoy the “rookie effect”Establish long-term relationship and resultant capacity

NegativesHigher operational and investment riskQuestionable sustained long term successLack of infrastructureFund of funds forced to invest rather than wait to discover the next Soros

Hedge funds in a modern portfolio

3

22

Structured products … hedge fund annuities

Out of favor in low interest rate environment but now a viable investment option

Managed leverage

Improved financial techniques and models allow for more advanced and tailored structured products

The flexibility of:Portfolio leverageLIBOR plus linked couponVariable tenorMulti-currency options

CS Tremont Hedge Fund Index versus USD 3M LIBOR +0.5% (Jan 1996 - Jun 2006)

50

100

150

200

250

300

350

Dec-95 Oct-96 Aug-97 Jun-98 Apr-99 Feb-00 Dec-00 Oct-01 Aug-02 Jun-03 Apr-04 Feb-05 Dec-05

CS Tremont Hedge Fund Index

USD 3M LIBOR + 0.5%

Source: Bloomberg; Credit Suisse Tremont Hedge Index

Hedge funds in a modern portfolio

3

23

The Future … it’s all about capacity

Hedge fund industry is capacity constrainedThere will be limited great managers with limited opportunities There will be new opportunities that will evolve

The industry will polarise into “capacity rich” players and boutiques with a niche

InvestorsWill become more tacticalWill add less liquid strategiesMay embrace emerging managersMay use managed leverage through structured products

Advisors will have more opportunity to add value

Hedge funds in a modern portfolio

3

24

Hard times for hedge funds?

Hedge funds are estimated to represent only 2% by assets compared to US mutual funds

Rapid growth in the number of funds offered

Investors disappointed by poor returns in recent bear market

Stock exchange concerns over perceived heavy impact of hedge-fund trading on some stocks

SEC scrutinising the sector

“Hard Times Come to Hedge Funds”. 1970.

Hedge funds in a modern portfolio25

This document has been issued by HSBC Republic Investments Limited on behalf of the Alternative Investment Group (“AIG”) for information purposes only. AIG and HSBC Republic Investments Limited are part of the HSBC Group, providing hedge fund advisory services to institutional and private investors.. The contents of this document are not and should not be construed as an offer to sell any investment, instrument or service. Furthermore, this document does not constitute the solicitation of an offer to purchase or subscribe for any investment, instrument or service in any jurisdiction where, or from any person in respect of whom, such a solicitation of an offer is unlawful.

This document is intended for Professional Investors only.

© Copyright. HSBC Republic Investments Limited 2006, whose office is at 78 St. James’s Street, London, SW1A 1JB. ALL RIGHTS RESERVEDNo part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of HSBC Republic Investments Limited.