2014: commercial real estate houston commercial real estate dan bellow president – houston jones...

TRANSCRIPT

2014: Commercial Real Estate

Dan BellowPresident – Houston

Jones Lang LaSalle Americas, Inc.

Houston

Houston 2nd Hottest Real Estate Market for 2014HBJ – January 16, 2014

Fortune Names Houston Companies Among 100 Best to Work for in U.S.Fortune – January 16, 2014

Houston # 1 U.S. City for JobsForbes – September 10, 2013

Most Robust Economy in North AmericaBrookings Institute – August 2013

Largest Export Market in the U.S.Department of Commerce – June 2013

Most Multifamily ConstructionAXIOMetrics Inc – January 30, 2013

Top U.S. Manufacturing CitiesManufacture’s News – January 23, 2013

Houston’s Rankings

2

MSA New Construction Starts thru November 2013*

Houston 46,462New York 35,360

Dallas 35,113

Washington DC 22,716

Atlanta 22,447

Los Angeles 21,245

Austin 19,049

Miami 19,032

Houston’s Housing Market: Constant Growth

*Single & MultifamilySource: Bureau of Labor and Statistics

3

December 20135,813 Units

Single Family Home Sales10,0009,0008,0007,0006,0005,0004,0003,0002,000

Houston’s Housing Market: Constant Growth

4

Houston’s Retail Market: Reflective of Economy’s Boom

• 265 MSF of rentable area

• 2013 absorption of 1.7 MSF

• 1 MSF of construction entering 2014

• Rental rates up 2.8% Y-Y from Q4 2012

• Premiere sites (Uptown, Woodlands) averaging $40.00 to $70.00 PSF

• Neighborhood center rentals averaging $25.00 to $35.00 PSF

• $180 PSF average sale price; 6.7% average cap rate

5

Houston’s Office Market: Metro Comparison

Gross Rental Rate Growth (4Q 2012 – 4Q 2013)

6

Key Market IndicatorsSupply

2013Year End

2014Forecast

Supply 152,083,838 SF

Direct market vacancy 11.4%

Total market vacancy 12.3%

Under construction (70% preleased) 6.8 MSF

Houston’s Office Market: Unprecedented Growth

7

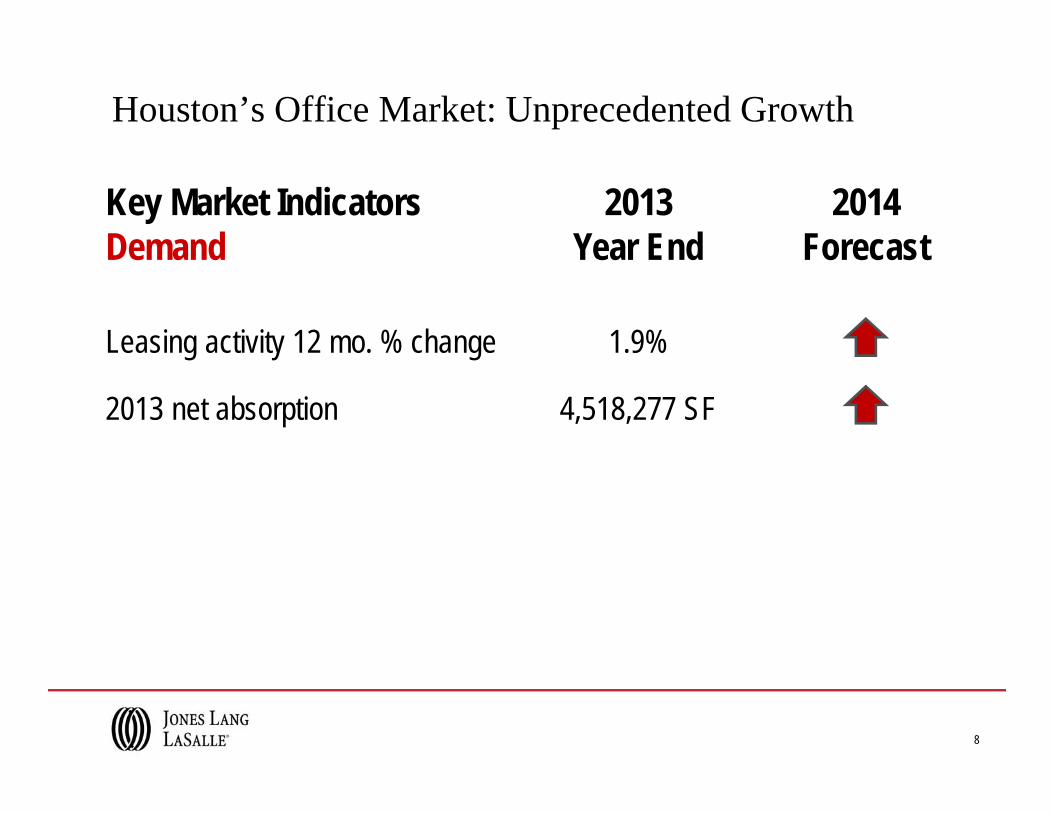

Key Market IndicatorsDemand

2013Year End

2014Forecast

Leasing activity 12 mo. % change 1.9%

2013 net absorption 4,518,277 SF

Houston’s Office Market: Unprecedented Growth

8

Key Market IndicatorsPricing

2013Year End

2014Forecast

Overall rent 12 mo. % change 4.2%

Class A overall asking rent $34.14 PSF

Class B overall asking rent $21.00 PSF

Houston’s Office Market: Unprecedented Growth

9

10

Houston Office Market

74%76%78%80%82%84%86%88%90%92%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Overall Occupancy Class A&B (%) CBDSuburban

1. Central Business District: KBR, United, Rosetta Resources, Transcanda

2. Galleria: Stewart, BBVA, Alliant, Williams Co., Blue Cross Blue Shield

3. Greenway Plaza: ExxonMobil, Occidental, UHY, Seahawk Drilling

Houston Office Market: 6 Submarkets Driving Houston

11

4. Katy Freeway (Energy Corridor):BP, Murphy Oil, Nexen, Technip

5. Westchase District: Halliburton, ABB, National Oilwell Varco

6. The Woodlands (“New” Energy Corridor): ExxonMobil, Southwestern Energy, Nexeo Solutions, Newfield

Houston Office Market: 6 Submarkets Driving Houston

12

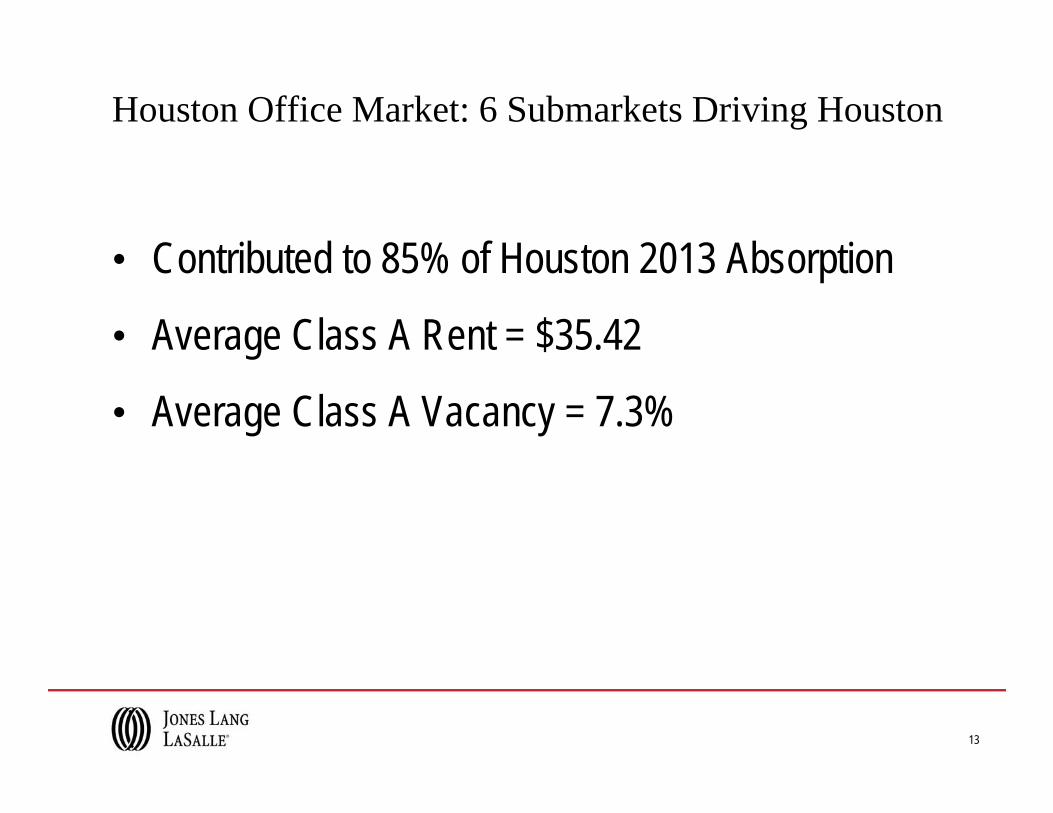

• Contributed to 85% of Houston 2013 Absorption

• Average Class A Rent = $35.42

• Average Class A Vacancy = 7.3%

Houston Office Market: 6 Submarkets Driving Houston

13

Activity / Absorption

Prices / Rental Rates

Supply / Vacancy

Market Condition 2013 Year End4.5 MSF absorbed in 2013; 8 MSF in past 2 years

4.4% Rent Growth YOY 2012 to 2013 in Class A space; $40 PSF Gross Rates in CBD

Overall vacancy decreased 2.8% YOY from 2012; 7 submarkets with single digit overall vacancy

Houston Office Market Conclusions

14

Activity / Absorption

Prices / Rental Rates

Supply / Vacancy

Tenant leverage in Big 6 submarkets to diminish; Demand and absorption will increase

Growth to continue with increased demand particularly West Houston, The Woodlands and CBD

New projects are preleased, will increase supply but decrease vacancy rates

Market Condition 2014 Forecast

Houston Office Market Outlook

15

Houston Industrial Market: Metro Comparison

Gross Rental Rate Growth (4Q 2012 – 4Q 2013)

16

Key Market IndicatorsSupply

2013 Year End

2014Forecast

Supply 389,478,498 SF

Direct market vacancy 4.8%

Total market vacancy 4.9%

Under construction (65% preleased) 5.8 MSF

Houston’s Industrial Market: Continued Growth

17

Key Market IndicatorsDemand

2013 Year End

2014Forecast

Leasing activity 12 mo. % change 2.2%

2013 net absorption 3,213,308 SF

Houston’s Industrial Market: Continued Growth

18

Key Market IndicatorsPricing

2013 Year End

2014Forecast

Overall rent 12 mo. % change 7.3%

Warehouse/distribution asking rent $5.28 PSF

Manufacturing asking rent $5.16 PSF

Houston’s Industrial Market: Continued Growth

19

Activity / Absorption

Prices / Rental Rates

Supply / Vacancy

Market Condition 2013 Year End

4.3% rent growth overall Q-Q; $6.00 PSF asking rates in North and Northwest markets

Vacancy decreased in most submarkets; Over 50% of new supply is speculative

Majority of activity in North, Northwest, and Port of Houston; Build-to-suit construction strong

Houston Industrial Market Conclusions

20

Activity will remain strong in North & Northwest; Big Box users continue to take space

Lease rates to increase as Build-to-suit market expands

Vacancy rates will continue to decrease throughout much of market, possibly to below 4.5%

Activity / Absorption

Prices / Rental Rates

Supply / Vacancy

Market Condition 2014 Forecast

Houston Industrial Market Outlook

21

Houston’s Capital Markets 2013 Conclusions:Shifting from Secondary to Primary Market

• Allowing for portfolio diversification for investors

• Growth of offshore investors

• Large scale transactions dominated market

• Lack of small to medium sized offerings

• Class A transaction volume increased 54% Y-Y

• Suburban price PSF breaks pricing record 3x in 2013

• 6.9% average cap rate is 50 basis point reduction from 2012

22

Houston’s Capital Markets 2013 Conclusions:Shifting from Secondary to Primary Market

• Williams Tower in the Galleria traded at $278 PSF and 5.75% cap rate (Trophy Class A building)

• BG Group Place in the CBD traded at $493 PSF and 5.75% cap rate (Trophy Class A building)

• Greenway Plaza (10 buildings in Houston) traded at $218 PSF and 7.6% cap rate (Class A buildings)

23

More large entity-level transactions and partial interest offerings on the way

Suburban price PSF to increase, likely to $400 PSF;Westchase & Greenway cap rates to compress

Supply of traded buildings to tieto vacancy of buildings; 90% occupied buildings preferred

Activity / Absorption

Prices / Rental Rates

Supply / Vacancy

Market Condition 2014 ForecastHouston’s Capital Markets Outlook

24

Q & A

Dan BellowPresident – Houston

Jones Lang LaSalle, Americas Inc.