2013 capital market days · 2013 capital market days 16,17, 18 september 2013 france, a region for...

TRANSCRIPT

2013 CAPITAL MARKET DAYS 16,17, 18 September 2013

FRANCE, A REGION FOR GROWTH

Hervé NAVELLOU

CPD President Western Europe

COUNTRY KEY FIGURES

3

France Key figures

GDP**

€2.032b

Inflation*

+2%

Rate of Unemployment*

10.6%

Purchasing Power*

-0.9%

Greatest Concerns *** 1. Unemployment 78% 2. Health 58% 3. Purchasing Power 54%

65.6 million people*

13% of European Union total population

2nd largest country in Western Europe

20 -64 y.old

20 y.old and less

17.7% 24.5%

57.8%

Sources: *Insee 2012- **Euromonitor Dec 2012- ***TNS SOFRES 2012

26/09/2013

65 y.old and more

THE FRENCH BEAUTY MARKET

5

2012 - French Beauty Market

26/09/2013

€ 6,969 M +1.1%

€ 6,983 M +0,2%

2010 2011 2012

MARKET SIZE & GROWTH

49.4M buyers 15 y.old and more

+ 415,000 buyers vs 2011

29.4 products purchased / year

Source: BMS L’ORÉAL- Sell in; Kantar World panel

6

2012 - French Beauty market €6.983 M (+0,2% vs 2011)

26/09/2013

Source: BMS L’ORÉAL

Styling

4% (-3.2%)

Haircolor

5% (+0.5%)

Haircare

10% (+2.1%)

Shower gels

11% (+1.4%)

Shaving

1% (-4.6%)

Deodorants

5% (+0.2%)

Oral Cosmetic

2% (-1.5%)

SKINCARE

32% (+1.0%)

MAKEUP

11% (+0.0%)

HAIR

19% (+0.6%)

TOILETRIES

17% (+0.7%)

FRAGRANCES

19% (-1.6%)

Face care

16% (+0.4%)

Cleansing

5% (-2.9%)

Body Care

8% (+4.2%)

Suncare

3% (+2.9%)

DISTRIBUTION

8 26/09/2013

French Distribution Landscape

7,520 hyper / supermarket stores

4,367 hard discounters stores

2,580 drive stores

MASS MARKET

77 department stores

2,300 perfumeries

SELECTIVE MARKET

58,000 hair salons 23,000 pharmacies

800 parapharmacies

PHARMACIES / PARAPHARMACIES HAIR SALONS

Source: IRI, IMS, NPD, FNC

9

2012 - French Beauty market €6.983 M (+0,2% VS 2011)

26/09/2013

MASS MARKET

37% (+0.5%)

PROFESSIONAL MARKET

10% (+0,9%)

PARA + PHARMACIES

18% (+3.9%)

DIRECT SALES

10% (-5.5%)

Source: BMS L’ORÉAL

SELECTIVE MARKET

25% (-0.6%)

SPLIT BY DISTRIBUTION CHANNEL

10

Complementary Distribution Channels

26/09/2013

Source: BMS L’ORÉAL

32% 11% 19% 19% 17% 2%

Mass Market

Professional market

Selective market

Direct sales

Category weight - Value

24%

37%

56%

9%

74%

25%

10%

3%

33%

17%

35%

82%

32%

6%

8% 1%

18%

75%

16% 19%

2% 8% 8%

SKINCARE MAKEUP HAIRCARE FRAGRANCES TOILETRIES ORALCOSMETICS

HAIR

Para pharmacies / Pharmacies

11

2012- Focus on Mass market distribution

26/09/2013

7,520 Hyper /

supermarkets

4,367

Hard discounters

37%

of total Beauty Value

SM

31.6%

HD

5.1%

HM

63.3%

Source: BMS L’ORÉAL, IRI

12 26/09/2013

Key facts Mass market distribution

Diversification of store formats (development of small stores, city-centre location, etc.)

Development of the Drive

Poorer performance of non-food and textile segments

Opportunity for beauty

13

2012- Focus on Pharmacies and parapharmacies

26/09/2013

Source: BMS L’ORÉAL, IMS

23,000 pharmacies

800 parapharmacies

71.5% pharmacies 18% of total Beauty Value 28.5% parapharmacies

14 26/09/2013

Key facts Pharmacies and parapharmacies

Priorisation of Dermocosmetics

Development of Consumer Experience, Service and Offer

Business potential for beauty brands

PARAPHARMACIES

PHARMACIES

Context • Change in Pharmacy : decrease in prescribed drugs affect the channel

• Pharmacies go towards news segments: OTC, Dermocosmetics (+4.6%)

• Growth is held by the biggest pharmacies (T.O > €2.2 M)

Driving growth of dermocosmetics

Huge development in the Mass market distribution

15

2012 -Focus on Hair dressing industry

26/09/2013

58,000 salons

€5.3 billion estimated turnover 2012 (including hairdresser services)

90% are independent… … and generate 65% of turnover

6,4% of total Beauty Value

HAIR PRODUCTS SOLD AND USED BY HAIRDRESSERS / SELL IN

TOTAL HAIR DRESSING INDUSTRY / SELL OUT

Sources: FNC, BMS

16

Key facts Hair dressing industry

26/09/2013

Stabilized consumers behaviour: 4.8 visits a year Atomised sector of small businesses: 90% are still independant salons Emergence of new categories: Color without ammonia, Instrumental cosmetic, Booming nailcare market

Opportunity for a new market dynamic

17

2012 -Focus on Selective Market

26/09/2013

2,300 Perfumeries

77 Department stores

25%

of total Beauty Value

Independant perfumeries+ others

15%

National channels + department stores

85% (65% in 2006)

Source: BMS L’ORÉAL, NPD

18

Key facts Selective Market

26/09/2013

Highly fragmented sector, where national brands + department stores account for nearly 85% of turnover

Independant stores account for only 10% of turnover

Growth of exclusive brands (Urban Decay, Clarisonic, Benefit, Make up for ever, Smashbox, Bare Mineral, etc.)

19

2012 -Focus on E-business

26/09/2013

Source: Intern Custagg based on panel data (IRI, NPD + IMS + KANTAR) – Sell Out

4% of total Beauty Value

Average

basket

Lancôme €95

Yves Saint Laurent €90

Kiehl’s €80

Biotherm €80

Sephora €51

The Body Shop €36

20

2012 -Focus on Retail stores

26/09/2013

FRENCH CONSUMERS

22

French Consumers Key facts 1st half of 2013

26/09/2013

2013

STILL UNDER PRESSURE …

BUT SOME GOOD NEWS IN EARLY 2013

Higher unemployment:

10.9%

Increased GDP (vol)

Increased Purchase Power:

+0.9% (Q1/2013)

Increased Household consumption:

+0.3% (vs -0.2% Q1/2013)

Inflation: +1.1% (annual base - July 2013)

Higher Taxes

26/09/2013 24

Source: Insee

23

French Consumer: The “Smart” Shopper

26/09/2013

Switches between

different distribution channels

Is watchful of prices

and promotion

Searches for

information, Compares online and

listens to WOM

Is Brand Loyal

24

Source: Intern

24

French Consumers: Colour as an antidote

26/09/2013

80% of women state that

colour is important to beauty

Sort of emotional pay-off from the use

of colour: feeling more attractive, more

feminine, or more confident

NAIL VARNISH BOOM:

+1,000,000 buyers vs y.a

Average basket: +12.6% units

Source: Intern, Kantar

25

Self-care as a core value

French Beauty market Key consumer trends

26/09/2013

Sensory perception: a major issue

26

Emergence of safety concerns

French Beauty market Key consumer trends

26/09/2013

Development of brands that have roots, their own history

The power of Nature

27 26/09/2013

New categories

Inspired technical

offers by professionals

Development of

“customised’’ offers

French Beauty market Key consumer trends

L’ORÉAL IN FRANCE

29

L’ORÉAL France

Source: Intern data

26/09/2013

FRENCH LEADER ON COSMETICS MARKET

Creation 1909

Sell In

€1,976 b Sponsorship €11.6M

Employees 12,255

Delivery sites

10 Plants 13

% of global l’Oréal sales

9.6%

Research centers 12

30

Market Share L’ORÉAL FRANCE total

26/09/2013

2011 2012 %value change

2012/2011

L’ORÉAL Total 27.0 28.3 +4.5%

Consumer Products Division 16.1 16.9 +5.1%

Luxury Division 4.7 4.9 +2.6%

Professional Products Division 3.3 3.3 +1.2%

Active Cosmetics Division 2.9 3.2 +8.3%

Source: BMS L’ORÉAL - Sell In

VALUE MARKET SHARE (%) - SELL IN

31

Consumer data L’ORÉAL FRANCE total

26/09/2013

NUMBER OF BUYERS (in millions)

2010 2011 2012

L’ORÉAL total 41.3 41.4 42.3

New buyers +420,000 +142,000 +836,000

Source: KANTAR

CPD: 41.0

ACD: 5.8

LD: 5.4

PPD: 3.0

32

Top 10 players Beauty market - France

26/09/2013

2010 2011 2012 % value change

2012/2011

L’ORÉAL total 28.8 28.8 29.5 +2.5%

LVMH 6.5 6.6 6.7 +1.2%

Yves Rocher* 5.4 5.9 5.6 -5.3%

Pierre Fabre 4.0 3.9 4.1 +5.6%

Unilever 3.4 3.4 3.5 +2.5%

Private Labels 3.6 3.5 3.4 -1.8%

Beiersdorf 4.0 3.6 3.3 -10.0%

Henkel 2.9 2.9 2.9 +0.0%

Chanel 2.8 2.9 2.8 -3.2%

Procter & Gamble 2.8 2.7 2.7 -0.4%

Source: Intern Custagg Panel IRI + Panel NPD + Panel IMS + Panel KANTAR - Hairsalons: excluding services. Perfume stores excluding own brand products

*= Brand Yves Rocher

VALUE MARKET SHARE (%) - SELL OUT

33

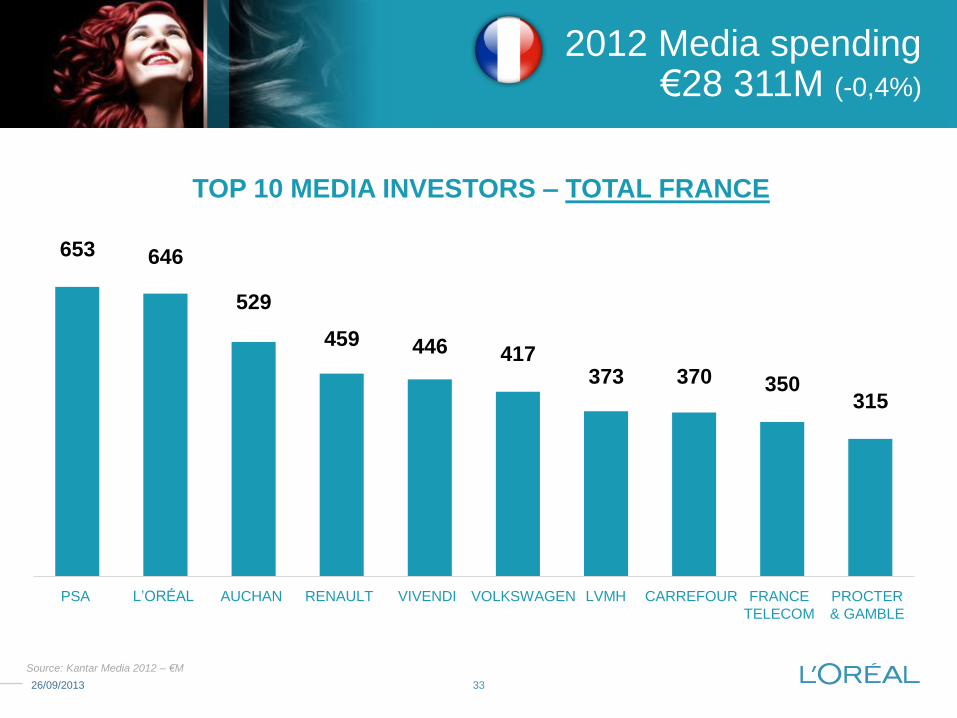

2012 Media spending €28 311M (-0,4%)

26/09/2013

653 646

529

459 446 417 373 370 350

315

PSA L’ORÉAL AUCHAN RENAULT VIVENDI VOLKSWAGEN LVMH CARREFOUR FRANCE

TELECOM

PROCTER

& GAMBLE

Source: Kantar Media 2012 – €M

TOP 10 MEDIA INVESTORS – TOTAL FRANCE

34

2012 Media spending- Beauty Total €2,056 M (+1.5%)

26/09/2013

642

-0.8%

186

+9.6% 184

+15% 125

+12.3% 96

-20.8% 66

+18.1% 57

+7.5 %

73

+12.3% 56

+36.8%

58

+12.9%

TOP 10 MEDIA INVESTORS – TOTAL BEAUTY

L’ORÉAL LVMH PROCTER

& GAMBLE

UNILEVER BEIERSDORF HENKEL JOHNSON

& JOHNSON

CHANEL

+ BOURJOIS

PUIG COLGATE

PALMOLIVE

Source: Kantar Media 2012 – €M

35

20.9% 18.5% 16.6%

53.1%

42.1%

SKINCARE FRAGRANCES TOILETRIES HAIRCARE MAKEUP

Market Share L’ORÉAL total - 2012

26/09/2013

L’ORÉAL IS LEADER WITH 28.3% VALUE MARKET SHARE (SELL IN)

BUT STILL HAS POTENTIAL FOR GROWTH

Source: BMS L’ORÉAL + DIM

L’ORÉAL

COMPETITION

€2,185 M

€1,357 M

€1,200 M

€1,356 M

€734 M

HAIR

36

Top 10 brands Beauty market - France

26/09/2013

2010 2011 2012 %value change

2012/2011

L’Oréal Paris 6.2 6.2 6.4 +2.8%

Yves Rocher 5.4 5.9 5.6 -5.3%

Garnier 3.5 3.3 3.5 +5.0%

Christian Dior 3.1 3.2 3.2 +1.5%

Nivea 3.6 3.3 2.9 -11.2%

Chanel 2.8 2.9 2.8 -3.2%

Avene 2.2 2.2 2.4 +7.5%

Gemey Maybelline 2.4 2.4 2.3 -4.4%

Lancôme 1.9 2.0 2.1 +5.9%

Guerlain 1.8 1.8 2.0 +9.9%

Source: Intern Custagg Panel IRI + Panel NPD + Panel IMS + Panel KANTAR

Hairsalons: excluding services / Perfume stores excluding own brand products

VALUE MARKET SHARES (%) – SELL OUT

FOCUS ON OUR DIVISIONS

38 26/09/2013

2012 %value change vs

2011

MASS MARKET +0.6%

L’ORÉAL CPD 45.4 +3.4%

PRIVATE LABELS 8.4 -1.8%

UNILEVER 8.1 +1.4%

BEIERSDORF 7.4 -10.4%

HENKEL 6.9 +1.0%

VALUE MARKET SHARE (%)

Source: IRI

L’ORÉAL Consumer Products Division

39

L’ORÉAL Consumer Products Division OUR AMBITION

26/09/2013

The strength of our brands

The quality of our innovations

The conquest of new consumer targets

“Fair share” on each major category

The expansion of our distribution

Being best in class in terms of A&P optimization: reaching consumers through all touch points and maximising return on investment

GROW OUR LEADERSHIP through:

40 26/09/2013

2012 %value change vs

2011

PHARMACY / PARA +3.6%

PIERRE FABRE 24.6 +4.9%

L’ORÉAL ACD 15.5 +8.1%

NUXE 5.8 +13.2%

BIODERMA 5.0 +12.4%

CAUDALIE 4.2 +3.3%

VALUE MARKET SHARE (%)

L’ORÉAL Active Cosmetics Division

Source: IMS

41

L’ORÉAL Active Cosmetics Division OUR AMBITION

26/09/2013

Brand priorities

1. Conquer leadership with La Roche-Posay

2. Vichy in the top 3

3. Add new targets thanks to Roger&Gallet and Sanoflore

Categories

Focus on Skincare & Haircare

Business model: conquer the distribution

Visibility, Consumer Experience & Advice, 1.500 new clients

Preempt the digital sphere

REACH 20% MARKET SHARE by 2017

42 26/09/2013

2012 %value change vs

2011

LUXURY -0.6%

LVMH 23.5 +1.3%

L’ORÉAL LUXE 20.9 +2.6%

CHANEL 9.9 -2.2%

CLARINS 9.6 -1.0%

PUIG 5.7 -3.0%

VALUE MARKET SHARE (%)

L’ORÉAL Luxury Division

Source: NPD

43

L’ORÉAL Luxury Division OUR AMBITION

26/09/2013

Grow our strategic brands: Lancôme - Yves Saint Laurent - Giorgio Armani (3 brands in the top 10)

• Winning Business model by categories 3 brands Skincare specialist / 3 brands Fragrace specialist / 1 brand Makeup specialist

• Build pillars while maximizing launches

• Deliver Retail excellence build on Oultet segmentation

Consistently ensure innovative & outstanding execution

N°1 LUXURY BEAUTY PLAYER by 2017

44 26/09/2013

2012

PROFESSIONAL PRODUCTS

L’ORÉAL PPD 50.8

SCHWARZKOPF 11.6

WELLA 7.4

EUGENE PERMA 6.9

COLOMER 5.2

VALUE MARKET SHARE (%)

L’ORÉAL Professional Products Division

Source:Intern

45

L’ORÉAL Professional Products Division OUR AMBITION

26/09/2013

Accelerate trafic to salons

Products innovation

Develop new territories and new channels

Increase our Distribution base

Boost the image of the industry

GROW OUR LEADERSHIP through:

46

L’ORÉAL France OUR AMBITION

26/09/2013

Be N°1 in each distribution channel and each category

Outperform the market

and boost our market share on total Beauty (> 30%)

Bring strong contribution to worldwide growth in value

Entrepreneurship and Excellence

FRANCE A REGION FOR GROWTH: