©2012 pearson education, auditing 14/e, arens/elder/beasley 5 - 5 audit of cash balances chapter 23

TRANSCRIPT

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 5 - 5

Audit of Cash BalancesAudit of Cash Balances

Chapter 23Chapter 23

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 22

Learning Objective 1Learning Objective 1

Show the relationship of cash in the Show the relationship of cash in the bank to the various transaction bank to the various transaction cycles.cycles.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 33

Relationships of Cash in the Relationships of Cash in the Bank and Transaction Bank and Transaction

CyclesCycles

Cash in Bank

Capital Stock – Common

Paid-in Capital in Excessof Par – Common

Redemptionof stock

Redemptionof stock

Issue ofstock

Issue ofstock

Dividends PayablePayment ofdividends

Capital Acquisition and Repayment Cycle:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 44

Cash in the Bank and Cash in the Bank and Transaction CyclesTransaction Cycles

Failure to bill a customer

An embezzlement of cash

receipts from customers

Misstatements which may not be discoveredas a part of the audit of the bank reconciliation:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 55

Cash in the Bank and Cash in the Bank and Transaction CyclesTransaction Cycles

Duplicate payments Improper payments of personal expenses Payment for raw materials not received Payment to employee for hours not worked Payment of excessive interest to related

party

Misstatements (continued):

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 66

Cash in the Bank and Cash in the Bank and Transaction CyclesTransaction Cycles

Misstatements which are normally discoveredas a part of the tests of a bank reconciliation:

Failure to include a check on the outstanding check list

Cash received by the client recorded in the wrong period

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 77

Cash in the Bank and Cash in the Bank and Transaction CyclesTransaction Cycles

Deposits recorded near year end,deposited in the bank in the same month, and included in the bank reconciliation as a deposit in transit

Payments on notes payable debited directlyto the bank balance but not entered in the client’s records

Misstatements which are normally discoveredas a part of the tests of a bank reconciliation:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 88

Learning Objective 2Learning Objective 2

Identify the major types of cash Identify the major types of cash accounts maintained by business accounts maintained by business entities.entities.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 99

General cash account

Imprest accounts

Branch bank account

Imprest petty cash fund

Cash equivalents

Types of Cash AccountsTypes of Cash Accounts

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1010

Relationship of General Relationship of General Cash to Other Cash Cash to Other Cash

AccountsAccountsBranch Bank

Account

CashEquivalents

Imprest PayrollAccount

Imprest PettyCash Fund

GeneralCash

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1111

Learning Objective 3Learning Objective 3

Design and perform audit tests of the Design and perform audit tests of the general cash account.general cash account.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1212

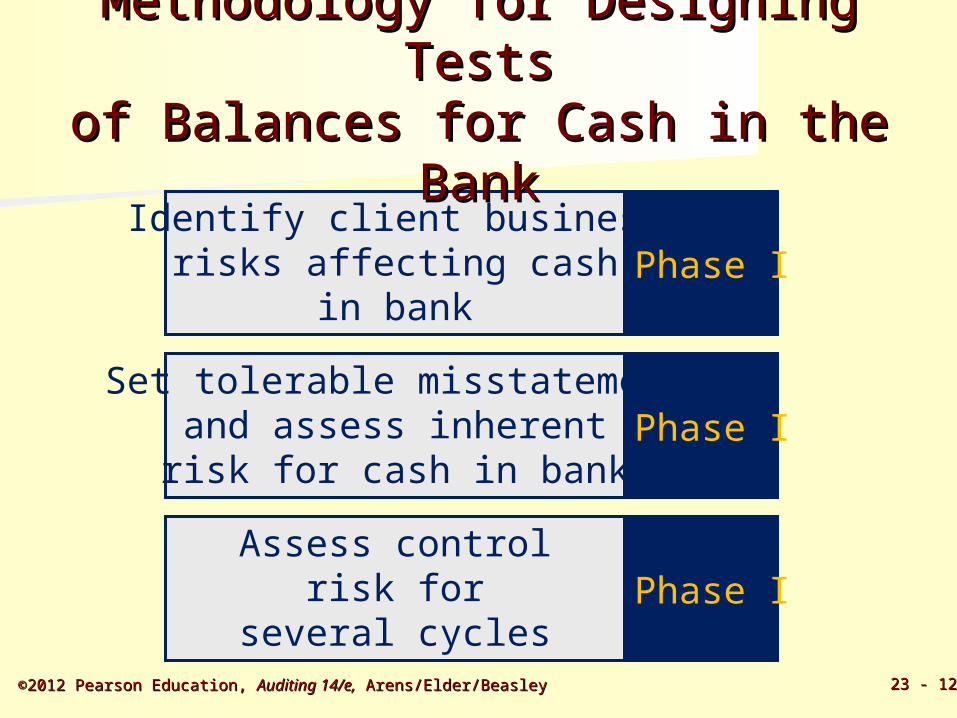

Identify client businessrisks affecting cash

in bank

Methodology for Designing TestsMethodology for Designing Testsof Balances for Cash in the Bankof Balances for Cash in the Bank

Set tolerable misstatementand assess inherentrisk for cash in bank

Assess controlrisk for

several cycles

Phase I

Phase I

Phase I

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1313

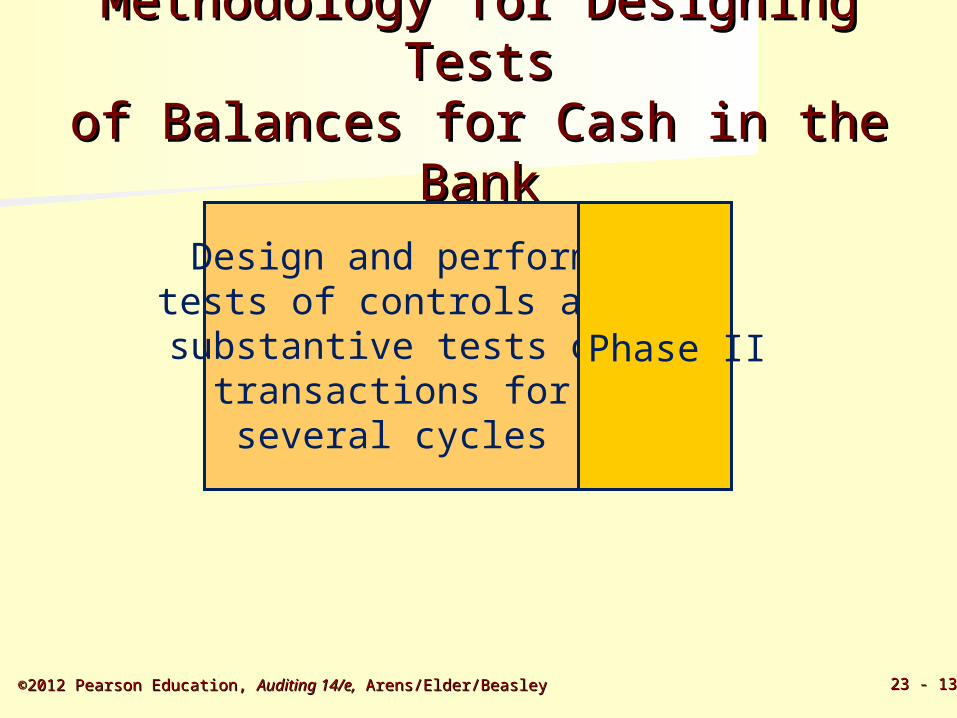

Methodology for Designing TestsMethodology for Designing Testsof Balances for Cash in the Bankof Balances for Cash in the Bank

Design and performtests of controls andsubstantive tests of

transactions forseveral cycles

Phase II

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1414

Timing

Items to select

Sample size

Audit procedures

Methodology for Designing TestsMethodology for Designing Testsof Balances for Cash in the Bankof Balances for Cash in the Bank

Design and performanalytical procedures

for cash in bank

Design tests ofdetails of cash inbank to satisfybalance-relatedaudit objectives

Phase III

Phase III

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1515

Audit Schedule for a Bank Audit Schedule for a Bank ReconciliationReconciliation

Clawson IndustriesBank Reconciliation

12/31/09

Schedule A-2 DatePrepared by Client DED 1/10/10Approved by SW 1/18/10Account 101 – General account, First National Bank

Balance per bank $109,713Add: Deposits in transit 21,117Deduct: Outstanding checks – 87,462Other reconciling items: Bank error – 15,200Balance per bank, adjusted $ 28,168

Balance per books before adjustments $ 32,584Adjustments: Unrecorded bank service charge 216

NSF 4,200 – 4,416Balance per books, adjusted 8,168

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1616

Balance-related Audit Balance-related Audit ObjectivesObjectives

Cutoff

Detail tie-in

Existence

Completeness Accuracy

Cash Balance-related

Audit Objectives

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1717

ProceduresProcedures

Bank Confirmation

Bank Reconciliation

Cutoff Bank

Statement

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1818

Types of Audit Tests Used Types of Audit Tests Used for General Cash in Bankfor General Cash in Bank

Cash in Bank

Ending balance

TOC-T + TOC-B + STOT + AP + TDB= Sufficient appropriate evidence

Audited byTOC-T, STOT, and AP

Beginning balance

Cash receipts Cash disbursements

Audited byTOC-T, STOT, and AP

Audited byTOC-B, AP, and TDB

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 1919

Learning Objective 4Learning Objective 4

Recognize when to extend audit tests Recognize when to extend audit tests of the general cash account to test of the general cash account to test further for material fraud.further for material fraud.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2020

Fraud-oriented ProceduresFraud-oriented Procedures

The auditor must extend the proceduresin the audit of year-end cash to determinethe possibility of a material fraud.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2121

Extended Tests of the Bank Extended Tests of the Bank ReconciliationReconciliation

When the auditor believes that the year-end bank reconciliation may beintentionally misstated, it is appropriate to perform extended tests of the year-end bank reconciliation.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2222

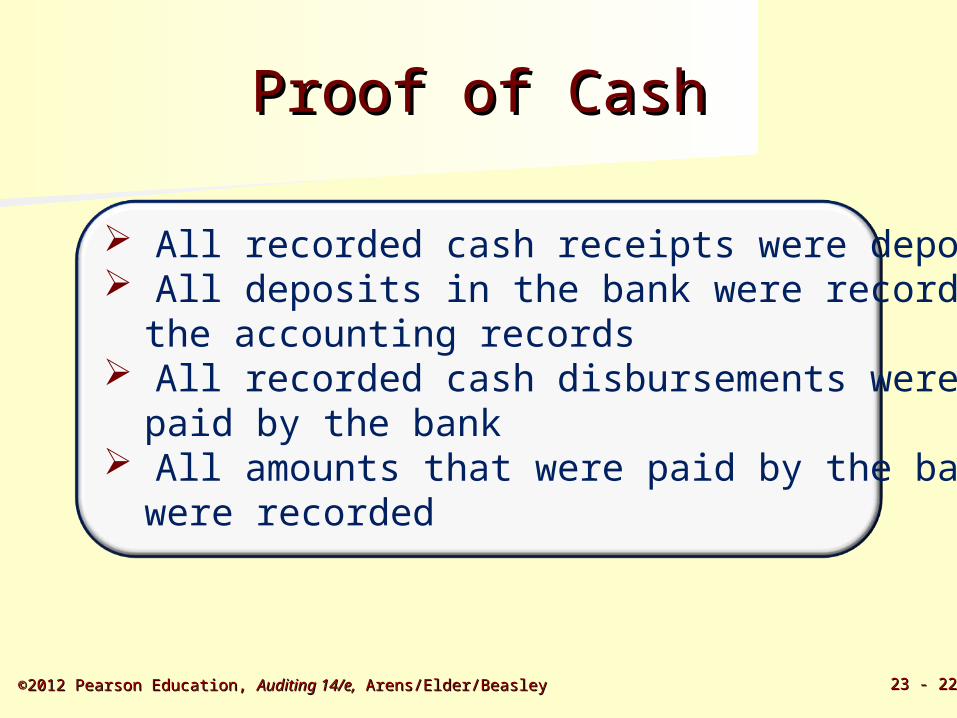

Proof of CashProof of Cash

All recorded cash receipts were deposited All deposits in the bank were recorded in

the accounting records All recorded cash disbursements were

paid by the bank All amounts that were paid by the bank

were recorded

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2323

Proof of Cash ScheduleProof of Cash Schedule

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2424

1.The balance on the bank statement withthe general ledger balance at thebeginning of the proof-of-cash period

2.Cash receipts deposited per the bank withthe cash receipts journal for a given period

Proof of CashProof of Cash

Includes the following reconciliation tasks:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2525

3.Cancelled checks clearing the bank withthose recorded in the cash disbursementsjournal for a given period

4.The balance on the bank statement with thegeneral ledger balance at the end of theproof-of-cash period

Proof of CashProof of Cash

Includes the following reconciliation tasks:

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2626

Interbank Transfer ScheduleInterbank Transfer Schedule

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2727

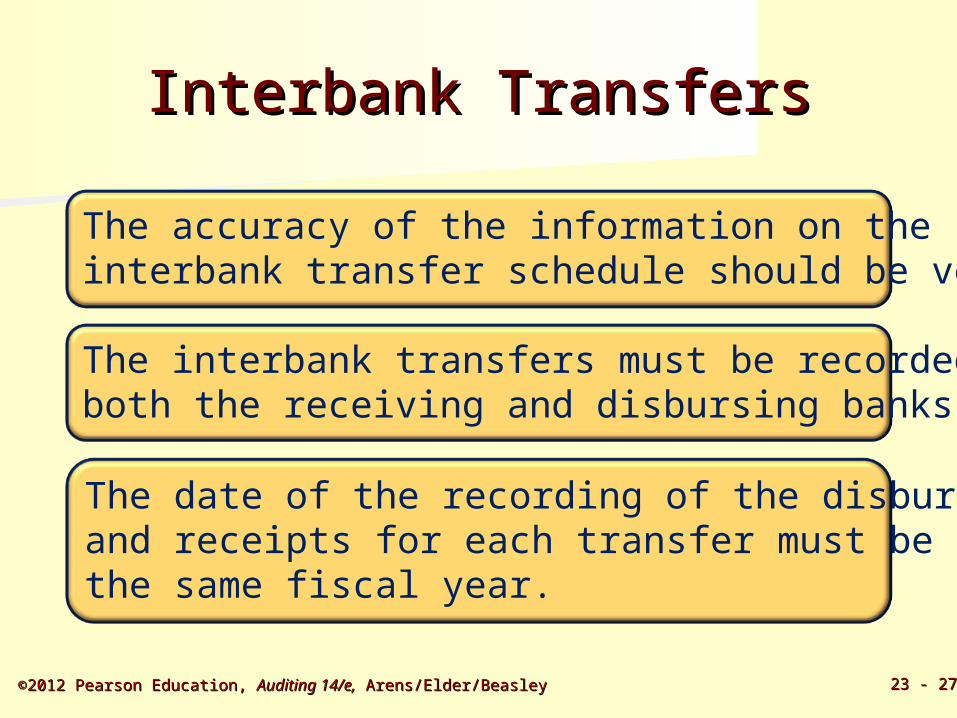

The accuracy of the information on theinterbank transfer schedule should be verified.

The interbank transfers must be recorded inboth the receiving and disbursing banks.

The date of the recording of the disbursementsand receipts for each transfer must be inthe same fiscal year.

Interbank TransfersInterbank Transfers

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2828

Disbursements on the interbank transferschedule should be correctly included in orexcluded from year-end bank reconciliationas outstanding checks.

Interbank TransfersInterbank Transfers

Receipts on the interbank transfer scheduleshould be correctly included in or excludedfrom year-end bank reconciliations asdeposits in transit.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 2929

Learning Objective 5Learning Objective 5

Design and perform audit tests of the Design and perform audit tests of the imprest payroll bank account.imprest payroll bank account.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 3030

Typically, the only reconcilingitems are outstanding checks.

Audit of the Imprest Payroll Audit of the Imprest Payroll Bank AccountBank Account

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 3131

Learning Objective 6Learning Objective 6

Design and perform audit tests of Design and perform audit tests of imprest petty cash.imprest petty cash.

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 23 - 23 - 3232

Petty cash is a unique account becauseit is often immaterial in amount, yet it isverified on many audits.

The account is verified primarily becauseof the potential for embezzlement and theclient’s expectation of an audit revieweven when the amount is immaterial.

Petty CashPetty Cash

©2012 Pearson Education, ©2012 Pearson Education, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 5 - 5

End of Chapter 23End of Chapter 23