2012 · fountainhead property trust | integrated annual report 2012 3 1 june 2007 after the...

TRANSCRIPT

INTE

GRATE

D ANNUAL R

EPO

RT 2

012

IFC Scope

1 Highlights

2 Structure

3 Overview

8 Sustainability

14 Board of Directors and Chief Executive Officer

16 Chairman’s report

18 Corporate governance report

22 Manager’s report

30 Property portfolio overview

39 Property portfolio

42 Salient features

44 Fountainhead Property Trust Financial statements

64 Fountainhead Property Trust Management Limited Financial statements

74 Directors’ report

75 Manager’s responsibility statement and approval of the financial statements

76 Directors’ responsibility statement and approval of the financial statements

77 Report of the Audit and Risk Committee

78 Independent auditor’s report

79 Independent auditor’s report

80 Report of the Trustee

80 Certificate by Company Secretary

80 Unitholders’ diary

81 Definitions and Company details

Contents Scope of the integrated report

The Board has identified our stakeholders

and their particular concerns in a detailed

risk analysis exercise, supplemented

by the Trust’s everyday activities and

experience. To assist in formulating the

best approach, we sought the advice of

specialist professionals who are thoroughly

acquainted with the requirements of King III,

the Global Reporting Initiative (GRI), IFRS

and the Companies Act.

As neither the Trust nor the Manager has any

employees, reporting on certain aspects of

sustainability is necessarily limited.

Utility consumption figures disclosed in

this report include consumption relating to

the Trust’s numerous tenants throughout the

portfolio. While the Trust has undertaken a

number of energy-saving initiatives, the buy-

in of tenants is ultimately required in order to

achieve meaningful savings.

The sustainability report has been published

without independent assurance.

This report, covering the

12 months ended 30 September

2012, is Fountainhead Property

Trust’s second integrated annual

report. We are committed to

continuously improving the scope

of our report.

Tsogo Sun OR Tambo International Airport

Fountainhead Property Trust | Integrated annual report 20121

Highlights

The Trust at a glance

2012 2011

Total distribution (cents) 55.83 55.27

Total return (cents) 195 33

Total annual return (%) 28.7 5.1

Market capitalisation (R billion) 9.4 7.8

Property portfolio value (R billion) 10.8 8.5

Borrowings (R billion) 2.7 1.0

Borrowings as a percentage of the value of properties (%) 24 11

Weighted average cost of borrowings (%) 8.0 9.1

Net asset value (cents) 694 669

Premium to net asset value (%) 16.5 0.1

Listed market price at year-end (cents) 809 670

Completion of Blue Route Mall

Acquisition of the remaining 25% of Centurion Mall for R752 million

Vacancies reduced by 10% to 6.7%

NAV up by 3.7% to 694 cents

Reduction of 10% in operating costs to income ratio to 19.8%

Reduction in average cost of debt from 9.08% to 7.97%

Total annual return up from 5.1% to 28.7%

Blue Route Mall

Centurion Mall

Centurion Mall

Fountainhead Property Trust | Integrated annual report 20122

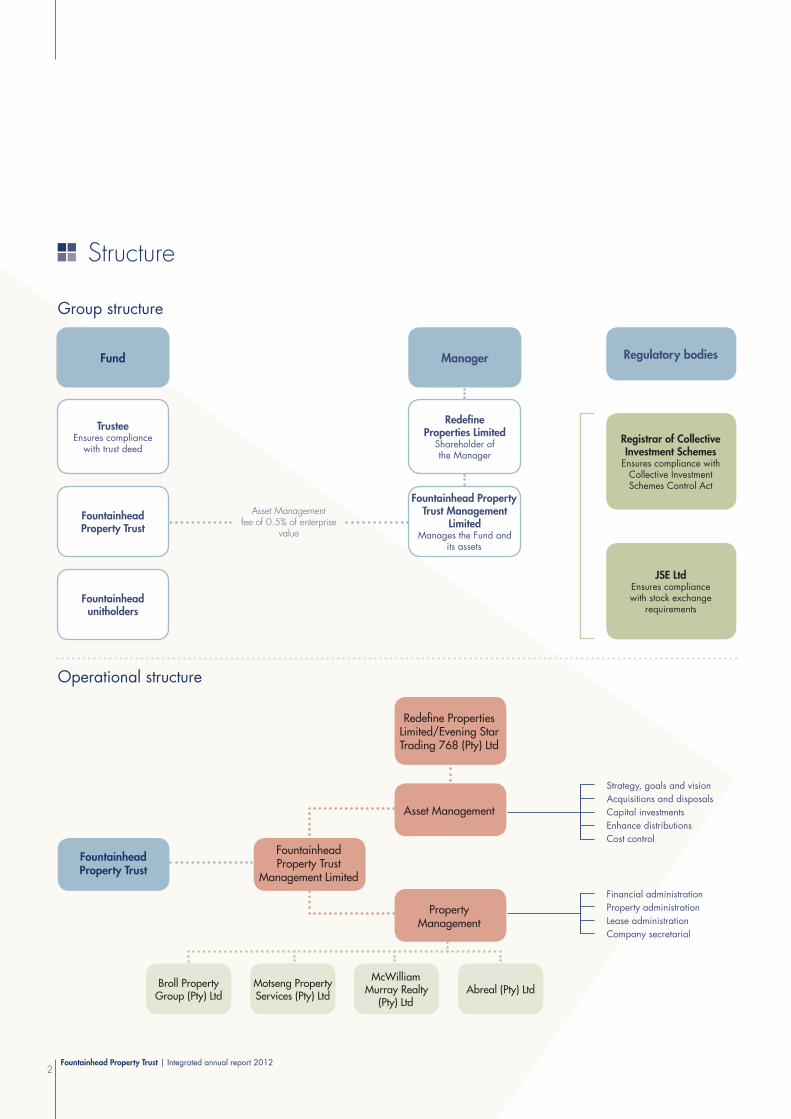

Group structure

Operational structure

Redefi ne Properties Limited/Evening Star Trading 768 (Pty) Ltd

Asset Management

Fountainhead Property Trust

Fountainhead Property Trust

Management Limited

Property Management

Strategy, goals and vision

Acquisitions and disposals

Capital investments

Enhance distributions

Cost control

Financial administration

Property administration

Lease administration

Company secretarial

Broll Property Group (Pty) Ltd

Motseng Property Services (Pty) Ltd

McWilliam Murray Realty

(Pty) LtdAbreal (Pty) Ltd

Structure

Regulatory bodies

Registrar of Collective Investment Schemes

Ensures compliance with Collective Investment Schemes Control Act

JSE LtdEnsures compliance with stock exchange

requirements

Fund

TrusteeEnsures compliance

with trust deed

FountainheadProperty Trust

Fountainheadunitholders

Asset Management fee of 0.5% of enterprise

value

Manager

Redefi neProperties Limited

Shareholder of the Manager

Fountainhead Property Trust Management

LimitedManages the Fund and

its assets

Fountainhead Property Trust | Integrated annual report 20123

1 June 2007 after The Standard Bank of

South Africa Limited purchased the controlling

share in the Manager. The Manager was

later renamed as the Fountainhead Property

Trust Management Limited. On 31 March

2008 Standard Bank sold 50% of its shares

in the Manager to Liberty Group Limited. On

1 August 2012 Redefine Properties Limited

purchased all the shares in the Manager from

Standard Bank and Liberty.

Strategy and valueFountainhead Property Trust aims to grow

and improve its property portfolio in order to

provide sustainable and growing returns for

its unitholders in the long term. This strategy is

implemented by acquiring quality properties

with good growth prospects, while also

disposing of properties with poor growth

prospects. In addition, the refurbishment of

existing assets will be undertaken where

a reasonable return can be generated

for unitholders.

In implementing this strategy, Fountainhead,

as a good corporate citizen, always

seeks to act in the best interests of its

various stakeholders.

Profi leFountainhead Property Trust is a collective

investment scheme in property established in

terms of CISCA.

It is a closed-end fund and distributes to

unitholders all net income earned on its

portfolio of real estate assets.

It is managed by Fountainhead Property Trust

Management Limited (the Manager) whose

investment policy objective is to create wealth

for Fountainhead unitholders by consistently

generating a total rate of return in excess

of inflation. The objective is to optimise

net rental growth and thereby maximising

the appreciation in the value of the underlying

properties in the portfolio.

Formation of FountainheadFountainhead Property Trust is a property

unit trust established in 1983 in terms of the

Unit Trust Control Act, 1981, subsequently, in

March 2003, replaced by CISCA, 2002.

The Trust is a closed-end Fund and is listed

on the Johannesburg Securities Exchange.

Units in the Trust can therefore only be

acquired on the stock exchange and are

not issued by the Manager directly to the

public. Originally known as The Standard

Bank Property Fund and, subsequently,

Allan Gray Property Trust, the Trust was

renamed Fountainhead Property Trust on

Overview

Fountainhead Property Trust aims at

growing and improving its property

portfolio in order to provide

sustainable and growing returns for

its unitholders in the long term.

Overview (continued)

56%

17%

27%

Tenant profi le analysis

Large national tenants, large listed tenants, Government and major franchisees. These include, inter alia, Absa Bank, Edgars Consolidated Stores, FirstRand Bank, Foschini, Pick n Pay Stores, Standard Bank, Telkom, Department of Public Works, Shoprite-Checkers, Massmart, South African Post Offi ce

National tenants, listed tenants, franchisees. These include, inter alia, Cell C, Cape Union Mart, Coricraft, Exclusive Books, Flight Centre, Incredible Connection, Nandos, Nu Metro Cinemas, Pie City Holdings, Ocean Basket, Spec Savers

Other tenants comprise all other tenants that do not fall in the above two categories

A

B

C

Category

Lease expiry profi le by rentable area per sector

Expiry period

Properties by sector by GLA

Retail

Offi ces

Industrial

Specialised

Perc

enta

ge

21%

3%58%

18%

Retail Office Industrial Specialised Total

Number of properties 13 23 26 2 64

Value (R billion) 8.2 1.7 0.5 0.3 10.7

GLA (m2) 471 757 141 702 167 770 26 969 808 198

Occupancy 93.5%* 92.9% 92% 100% 93.3%

0

20

40

60

80

100

Vacant 2013 2014 2015 2016 2017 >2017

8 7 7

17 16

53

14

9

22 22

1411

96

2

8

17

6

22

31

100

Fountainhead Property Trust | Integrated annual report 2012Fountainhead Property Trust | Integrated annual report 20124

*Includes office vacancies at Centurion, Boulders, Benmore and Rosebank Mews.

Fountainhead Property Trust | Integrated annual report 20125

Trust’s performance

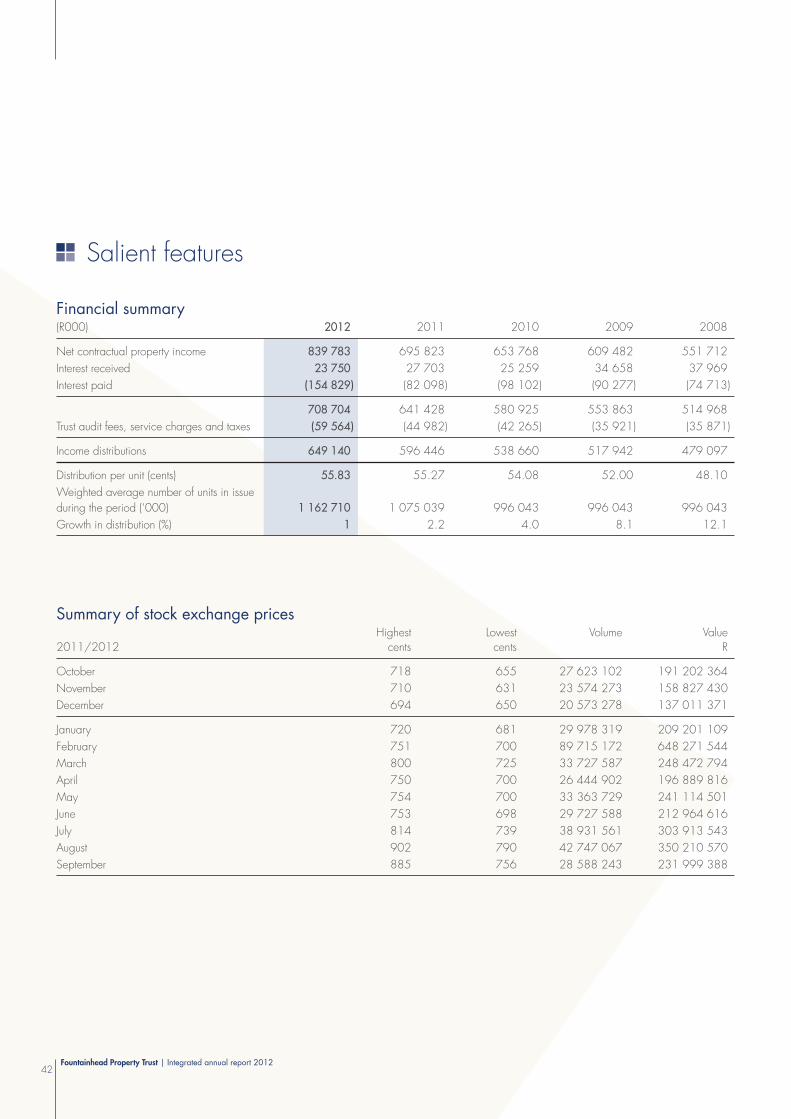

Financial summary

(R000) 2012 2011 2010 2009

Net contractual property income 839 783 695 823 653 768 609 482

Interest received 23 750 27 703 25 259 34 658

Interest paid (154 829) (82 098) (98 102) (90 277)

708 704 641 428 580 925 553 863

Trust audit fees, service charges and taxes (59 564) (44 982) (42 265) (35 921)

Income distributions 649 140 596 446 538 660 517 942

Distribution per unit (cents) 55,83 55,27 54,08 52,00

Weighted average number of units in issue during the

period (‘000) 1 162 710 1 075 039 996 043 996 043

Growth in distribution (%) 1% 2,2 4,0 8,1

2011 vs 2012 movement

575 000

595 000

615 000

635 000

655 000

675 000

695 000

715 000

735 000

755 000

19

12 74

41 13

649643

Distributable income 2011

Rights offer prepaid

distribution

Net operating income - Core

Acquisitions Disposals Developments Non-recurring income

Interest paid bond

Interest received

Other Service charge Distributable income 2012

46

25

92 4

Increase on 2011

Decrease on 2011

Overview (continued)

Fountainhead Property Trust | Integrated annual report 2012Fountainhead Property Trust | Integrated annual report 20126

Unit performanceTotal rate of returnThe annual total rates of return for the years ended 30 September are as follows:

2008 2009 2010 2011 2012

5-year average

2008 – 2012

Fountainhead (10.6) 21.3 20.5 5.1 28.7 22.3

PUT sector (15.8) 21.5 29.6 8.5 27.5 20.9

Out/(under) performance 5.2 (0.2) (9.1) (3.4) 1.3 1.4

PLS sector (11.8) 17.2 30.7 78.2 39.8 29.5

Fountainhead closing yield 8.1 8.1 7.7 8.1 7.0 n/a

PUT sector closing yield 9.4 9.1 7.9 8.1 7.1 n/a

FTSE/JSE Africa listed (13.1) 18.3 30.5 8.3 36.5 26.8

(Under)/out performance 2.5 3.0 (10.0) (3.2) (7.8) (4.5)

All share index (18.3) 9.0 20.9 3.2 23.6 20.2

Financial and industrial index (13.5) 13.1 26.5 4.4 35.8 22.4

All bond index 6.0 9.1 15.3 5.9 17.5 9.5

Cash STFIND 11.2 10.3 7.2 5.9 5.6 8.4

Trust’s performance (continued)

(R000) Total

Percentage change

2011Distribution

per unit

Core portfolio 508 371 5.2 43.72

Gross rental 633 964 5.1 54.52

Operating costs (110 540) 3.2 (9.51)

Net utility expense (15 053) 16.7 (1.29)

Acquisitions 250 385 57.6 21.53

Disposals 1 310 (73.8) 0.11

Developments 69 268 37.8 5.96

Non-recurring income 11 687 0.0 1.01

Trust expenses (191 881) 90.4 (16.50)

Interest paid bond (129 638) 57.9 (11.15)

Interest paid – Blue Route (25 192) 0.0 (2.17)

Interest received 22 188 (15.2) 1.91

Other (5 726) 29.8 (0.49)

Service charge (53 513) 32.3 (4.60)

Distributable income 2012 649 140 – 55.83

Growth 1.0% – 1.0%

Fountainhead Property Trust | Integrated annual report 20127

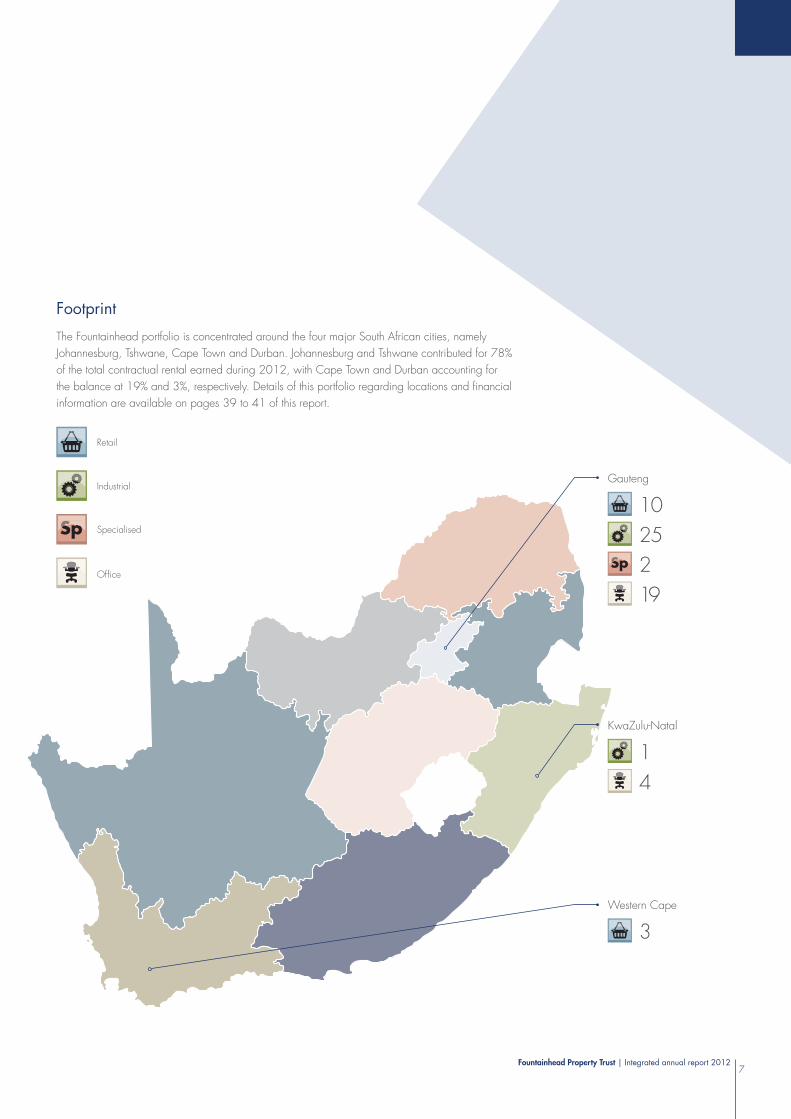

SpSp

10

2

25

19

Gauteng

SpSp

Retail

Specialised

Industrial

Office

1

4

KwaZulu-Natal

3

Western Cape

Footprint

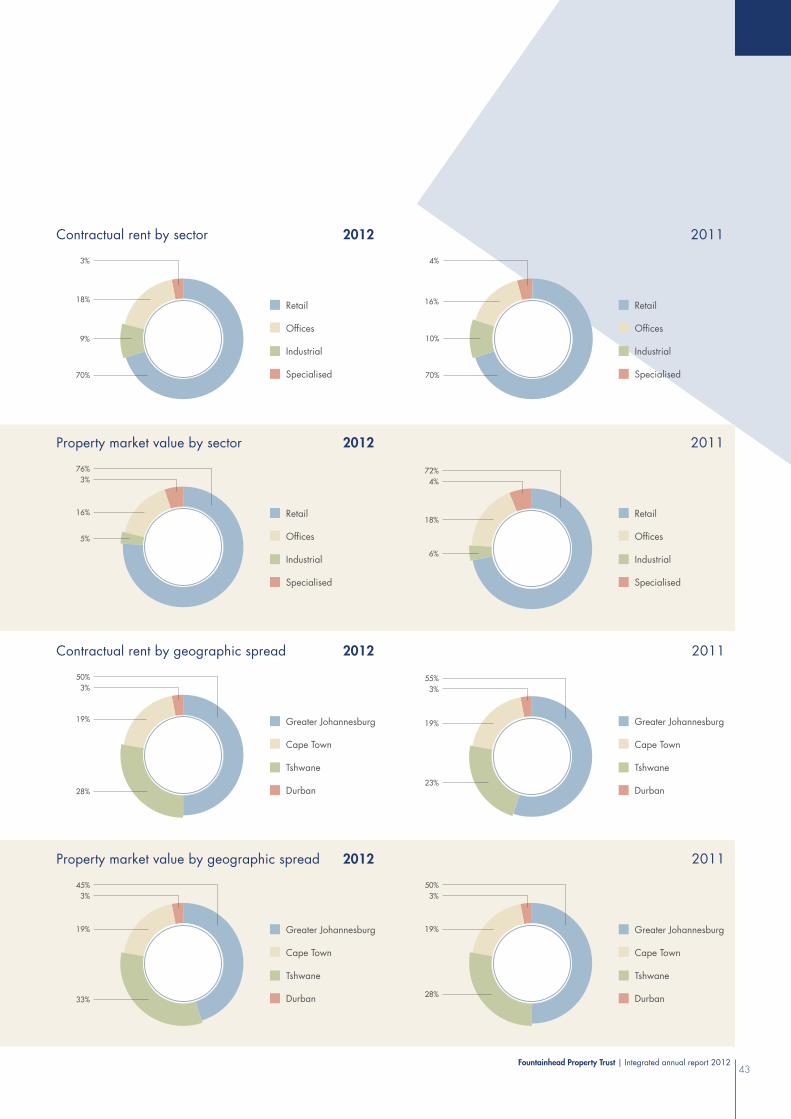

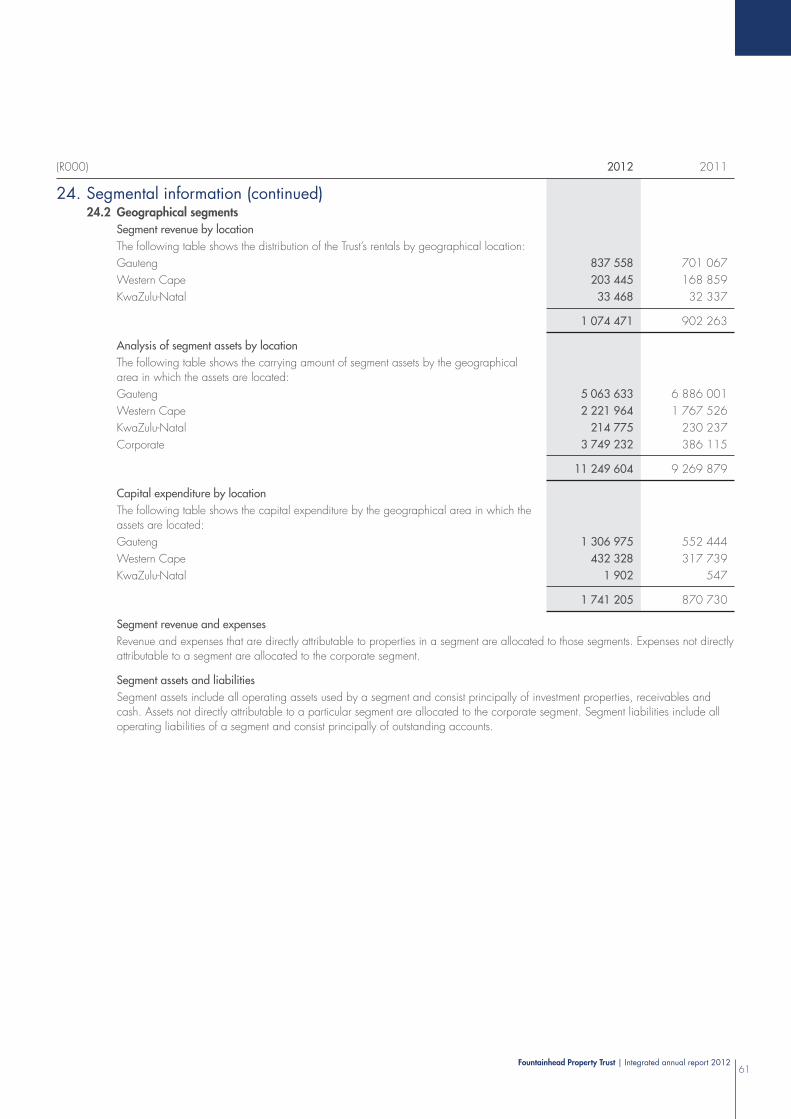

The Fountainhead portfolio is concentrated around the four major South African cities, namely

Johannesburg, Tshwane, Cape Town and Durban. Johannesburg and Tshwane contributed for 78%

of the total contractual rental earned during 2012, with Cape Town and Durban accounting for

the balance at 19% and 3%, respectively. Details of this portfolio regarding locations and financial

information are available on pages 39 to 41 of this report.

Sustainability

Sustainability Key Performance Indicators 2012 2011

Unitholder returns

Distribution growth 1.00% 2.20%

Total return 28.70% 5.10%

Consumer price index 5.76% 5.03%

Property

Vacancies 6.70% 7.40%

Tenant retention ratio 80.00% 58.00%

Comprehensive insurance Yes Yes

OHS Act non-compliance incidents 0 0

Corporate and financial

Board evaluation Yes No

Corporate governance compliance Yes Yes

Fixed interest rate debt 40.00% 76.00%

Environment

Electricity usage (KWh per m2) 270 259

Water usage (Kl per m2) 1.20 1.17

Reported regulatory non-compliance 0 0

Fountainhead Property Trust | Integrated annual report 20128

The Trust evaluates its operation holistically; paying attention to the

communities in which it operates, the environment, other businesses in

its value chain, and tenants and suppliers. With the extensive overview

that this achieves, the Trust is able to ensure a balance between

environmental, social and economic factors and is thus better placed

to create a sustainable business.

Blue Route Mall

Fountainhead Property Trust | Integrated annual report 20129

Risk Management

Risk management has been identifi ed as a key element in the practice of good corporate governance. The risk management principles adopted

are based on the principles of King III. The major strategic risks together with any mitigating controls/action points are listed below:

Key risk Mitigation strategy Affected stakeholder

Investment property deterioration affecting long-term sustainability of the business, impacting profi tability and the ability to pay expenses

Property management outsourced to specialistsAsset managers ensure that properties are properly managedRegular site visits by managementAnnual building inspection by trustees

UnitholdersProperty managersTrustees of the SchemeBankersLocal GovernmentGeneral suppliers and service providers

Tenants

Risk of tenant default

Detailed leasing strategy in place by property managers approved by asset managerBackground checks on tenants before leases signedRegular interaction via property managersMonitor tenant turnoversOperating cost management initiatives

Unitholders

Investment property not being adequately insured for damages, loss of income and third party claims

Regular monitoring of the adequacy of the insurance cover by Audit and Risk Committee and the Executive Committee

Unitholders

Banker

Trustee

Non-compliance with the various laws and regulations that govern the business

Regular monitoring of compliance by those charged with governance thereof

Regulators

Trustee

Offers to acquire property portfolio of the Trust

Unitholder approval required for disposal of a major part of property portfolioBoard to constitute a committee to review any offersTrust Deed defi nes steps to be takenReputable independent advisors to provide legal and technical support

Unitholders

Take-over of the Manager Regulated by The Trust Deed and CISCAUnitholders

Trustee

Confl ict of interest between the Manager and the Trust

A properly constituted Board with independent non-executive membersAcquisitions undertaken have to meet minimum investment criteriaUnitholders approval for disposal of signifi cant assets

Unitholders

Breakdown of internal controls at outsourced property managers

Service level agreements to be in placeInternal controls of the property managers assessed independently by outsourced internal audit function that reports to the Audit and Risk Committee

Property managers

Fountainhead Property Trust | Integrated annual report 201210

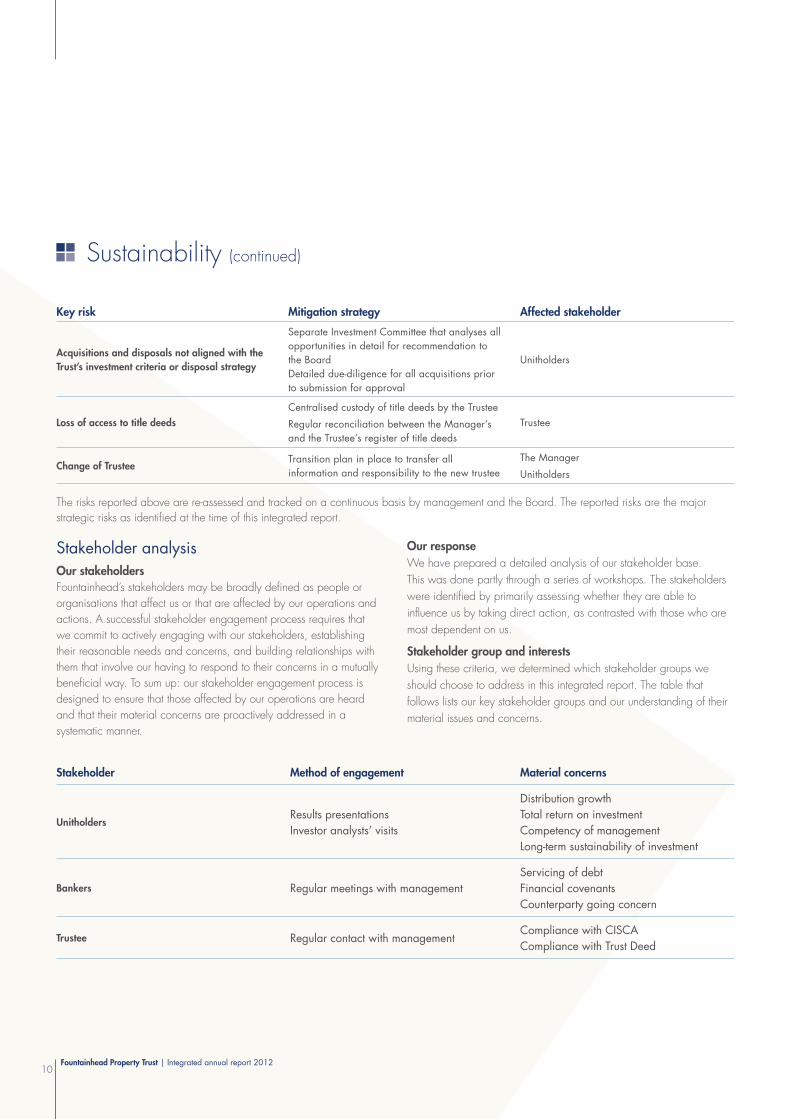

Sustainability (continued)

Key risk Mitigation strategy Affected stakeholder

Acquisitions and disposals not aligned with the Trust’s investment criteria or disposal strategy

Separate Investment Committee that analyses all

opportunities in detail for recommendation to

the Board

Detailed due-diligence for all acquisitions prior

to submission for approval

Unitholders

Loss of access to title deedsCentralised custody of title deeds by the Trustee

Regular reconciliation between the Manager’s

and the Trustee’s register of title deeds

Trustee

Change of TrusteeTransition plan in place to transfer all

information and responsibility to the new trustee

The Manager

Unitholders

The risks reported above are re-assessed and tracked on a continuous basis by management and the Board. The reported risks are the major

strategic risks as identified at the time of this integrated report.

Stakeholder analysis

Our stakeholdersFountainhead’s stakeholders may be broadly defined as people or

organisations that affect us or that are affected by our operations and

actions. A successful stakeholder engagement process requires that

we commit to actively engaging with our stakeholders, establishing

their reasonable needs and concerns, and building relationships with

them that involve our having to respond to their concerns in a mutually

beneficial way. To sum up: our stakeholder engagement process is

designed to ensure that those affected by our operations are heard

and that their material concerns are proactively addressed in a

systematic manner.

Our responseWe have prepared a detailed analysis of our stakeholder base.

This was done partly through a series of workshops. The stakeholders

were identified by primarily assessing whether they are able to

influence us by taking direct action, as contrasted with those who are

most dependent on us.

Stakeholder group and interestsUsing these criteria, we determined which stakeholder groups we

should choose to address in this integrated report. The table that

follows lists our key stakeholder groups and our understanding of their

material issues and concerns.

Stakeholder Method of engagement Material concerns

UnitholdersResults presentations

Investor analysts’ visits

Distribution growth

Total return on investment

Competency of management

Long-term sustainability of investment

Bankers Regular meetings with management

Servicing of debt

Financial covenants

Counterparty going concern

Trustee Regular contact with managementCompliance with CISCA

Compliance with Trust Deed

Fountainhead Property Trust | Integrated annual report 201211

Stakeholder Method of engagement Material concerns

TenantsRegular interaction mainly via outsourced property

managers

Performance in terms of lease agreement

Proper Management and Regulatory compliance

Operating cost management

Safe and Secure Shopping Experience

for customers

Property ManagersMonthly executive meetings

Daily interaction via asset managers

Compliance with management agreements

Key Performance Indicator assessments

Reliance on income from client

Local GovernmentRegular interaction mainly via outsourced property

managers

Timely payment of utility and rates charges

Infrastructure impact of properties

Energy-saving initiatives

General suppliers and service providersRegular interaction mainly via outsourced property

managers

Timely payment of goods and services

Fair tender processes and procurement criteria

Tenant customer and surrounding communitiesRegular interaction mainly via outsourced property

managers

Safe and secure shopping environment

Corporate social investment

Communication with surrounding community

RegulatorsSubmission of periodic returns

Periodic meetings and annual auditsCompliance with laws and regulations

Environmental responsibility

The Trust acknowledges environmental responsibility as an important

principle which affects its future success. The Trust has therefore

undertaken an initiative to further understand the impact of its

properties on the environment in order to monitor and take control of

its environmental impact. The Trust and managers have undertaken

to educate and involve their staff, shareholders, tenants, stakeholders

and suppliers in an effort to create awareness and instigate change at

all levels of its operation.

The Trust strives to employ techniques and technologies to reduce

consumption, ensuring that utilities are kept down, thereby benefitting

not only its tenants but also the environment. Henceforth the Trust

intends to increase the level of environmentally friendly technology in

its commitment to develop and manage properties that are efficient

in minimising negative impacts on the environment.

Not only does the Trust endeavour to mitigate its negative effect on the

environment, but it endeavours to contribute positively by improving the

surroundings of its properties, contributing to community needs

and initiatives, and monitoring security and crime levels in the

communities in which it has a presence. It is also currently in

negotiations with the local authority to assist in the restoration of

the Centurion Lake adjacent to Centurion Mall.

The Trust’s initiatives have already achieved much success and

its properties have been recognised as raising the bar in energy-

efficiency for shopping centres in South Africa.

Recently, in the National Energy Barometer Survey, which is

conducted by Energy Cybernetics, the N1 City Shopping

Centre was awarded first place in energy efficiency. The centre’s

management team took the decision to enter the building into the

survey in order to establish how the building benchmarked within

its relevant retail sector.

In an effort to increase the building’s energy efficiency, the

management team overhauled its lighting, load-shifting, and air-

conditioning by replacing old corroded pipes, installing new chillers

and repainting the building’s entire roof with an energy-saving coating

designed to reflect more light.

Fountainhead Property Trust | Integrated annual report 201212

Sustainability (continued)

The management team also ensured that all operation managers

and employees were informed of the energy-saving initiatives and

are actively involved in implementing them in the Mall’s day-to-day

operations. The team identified this policy of involvement as the

key to its success in reducing utility costs which, in turn, decreased

expenditure and improved the Trust’s bottom-line figures.

The runner-up in the shopping centre category of the Survey was

Centurion Mall, another of the Trust’s properties.

Prior to its participation in the Survey the management team of

Centurion Mall undertook a green initiative which included the

installation of timers in various areas to manage the hours that the lights

operate, the installation of power-correction units and the replacement

of the majority of lights with energy-saving lights. The geysers in all the

bathrooms were also switched off.

This national recognition is a positive indication that the Trust’s

properties and management teams are aware of the need to address

energy efficiency and are engaged in implementing systems to

improve the energy output of its centres.

Electricity and water consumptionThe table below shows the average annual electricity and water consumption by sector for the 12 months ended 30 September 2012:

Reportable area (m2)

Electricity consumptionKWh per m2

Water consumption Kl per m2

Sector 2012 2011 2012 2011 2012 2011

Retail 407 291 394 611 327 325 1.25 1.34

Office 31 713 46 027 113 139 1.06 0.80

Industrial 90 462 113 569 65 77 0.99 0.71

529 466 554 207 270 259 1.20 1.17

Electricity and water consumption are monitored on a continuous

basis. Management has appointed Utility Administration Service CC

(UAS) to administer the utility function. UAS has assisted in identifying

inefficiencies and advising on energy-saving initiatives that we have

undertaken or planned, including:

Fitting energy-efficient light-bulbs.

Upgrading air-conditioners to be more energy efficient at

N1 City Mall, for example, where a total of R5.8 million

(Fountainhead Share) was spent on an air-conditioner chiller

upgrade and, at Westgate Mall, where a similar project is

underway, costing R10.5 million (Fountainhead Share).

At Brightwater Commons Mall, a water reticulation and water

storage system has been installed to collect water and rain water

run-off to irrigate the surrounding gardens.

Social and economic responsibility

The Trust considers the safety and security of shoppers and tenants

a priority. As a matter of strict policy, therefore, all security service

providers and individual security personnel must be registered and

accredited by the Private Security Regulatory Authority (PSIRA).

Security personnel must also be trained in first-aid and undergo regular

emergency evacuation drills.

To ensure that properties are safe for use, each building is assessed

for compliance with Occupational Health and Safety Act (OHS)

regulations by an outsourced service provider, which will continue to

assess them from time to time. In addition, property managers regularly

perform compliance checks as part of their routine responsibilities.

The Trust, through its various shopping centres, has always played

an active role in corporate social responsibility initiatives. These

initiatives include providing complementary promotional court space

to charitable organisations, arranging fund-raising events and

making donations.

During the 2012 financial year, the Trust was instrumental in raising

over R1.5 million through such initiatives.

Specific activities during the year included:

A charity day at N1 City Mall where money was raised for

Robertson House in Milnerton – a home for the physically disabled.

The Mall also hosted a CANSA Shavathon and an Adopt a

Charity Week-end where tenants of the Mall were encouraged to

Fountainhead Property Trust | Integrated annual report 201213

adopt a charity for the day. Those tenants that adopted a charity

were given a free table in the centre and a percentage of the

sales that resulted from the table were donated to the tenant’s

chosen charities.

The Boulders participated in the 67 Minutes for Madiba initiative

by collecting food and toiletry parcels for a welfare organisation in

President Park and revamping the kitchen of the Miriam Makeba

Children’s Home. They also sponsored a full soccer kit for a

community school’s soccer team.

Centurion Mall’s very successful corporate responsibility initiatives,

which included a festive season gift wrapping station, a CANSA

Shavathon, a road race and a spin-a-thon, raised the significant

sum of R0.6 million.

Blue Route Mall made generous donations to the Zwaanswyk

Academy and to Butterfly Way Educare as well as hosting

an exhibition.

Kenilworth Centre raised money for the CANSA Shavathon and

Stop Hunger Now. They also hosted a charity awareness day,

arranged a visit to Erica’s Old Age Home and hosted a party for

an orphanage.

Benmore Shopping Centre donated promotional court space

to CANSA Shavathon, Hospice, Reach for a Dream, the South

African Blood Bank, and book sales in aid of St Johns Church,

United Sisterhood, Jewish Woman’s Benevolent Society and

Our Parents Home.

During the 2012 financial year no fines or penalties have been

incurred for the contravention of any laws and regulations applicable

to the business.

2 Pybus Street, Sandton

Boulders

Fountainhead Property Trust | Integrated annual report 201214

Board of Directors and Chief Executive Officer

David Savage (48)

Independent Non-executive Director

Appointed: 2 August 2011

Nationality: South African

Qualifi cation: BSc (Building) and MSc (Building Project Management)

Experience: Managing Director of Abland since 1998

Current directorships: Abland Proprietary Limited and related subsidiaries; The Pivotal Fund Limited

Haroon Laher (49)

Independent Non-executive Director

Appointed: 4 December 2008

Nationality: South African

Qualifi cation: B Proc, LLB

Experience: Director at Bowman Gilfi llan Inc. practising in the areas of commercial and banking litigation, insolvency and liquidation, BEE mergers and acquisitions, and tax

Current directorships: Bowman Gilfi llan Inc.

Michael Kirchmann (75)

Chairman and Independent

Non-executive Director

Appointed: 1 June 1988

Nationality: South African

Qualifi cation: RQS.M.A.Q.S

Experience: Managing Director of Northprop Proprietary Limited. Involved in the property sector since 1960

Current directorships: Northprop Proprietary Limited; African Realty Proprietary Limited; Hydenorth Proprietary Limited; Craig Park West Proprietary Limited; Linkway Proprietary Limited; Dainfern Shopping Centre Proprietary Limited; Alexandra Village Proprietary Limited; Tucana Property Holdings Proprietary Limited; Zamia Property Holdings Proprietary Limited; Craig Park Four Proprietary Limited

Victor Christian (71)

Chairman of Audit and Risk

Committee and Independent

Non-executive Director

Appointed: 19 July 2006

Nationality: South African

Qualifi cation: CA (SA)

Experience: Former partner at Ernst & Young and Non-executive Director of other companies

Current directorships: Allan Gray Employee Holdings Proprietary Limited; Allan Gray Life Limited; Allan Gray Unit Trust Management Limited; Phetogo Investments Proprietary Limited; Withmore Investments Proprietary Limited; Garden Cities Association Not For Gain

Fountainhead Property Trust | Integrated annual report 201215

Alex Phakathi (46)

Chief Executive Offi cer

Appointed: 7 September 2012

Nationality: South African

Qualifi cation: MCom (Wits)

Experience: Prior to being appointed, Alex was on the executive committee of Redefi ne Properties Limited responsible for acquisitions and disposals. Former Managing Director at Pareto Limited. Over 15 years of commercial property experience

Current directorships: Benguni Investments Proprietary Limited, Gwalagwala Investments Proprietary Limited and South African Council of Shopping Centres

Bernard Nackan (68)

Non-executive Director

Appointed: 20 September 2012

Nationality: South African

Qualifi cation: BA Econ Sep (Stanford)

Experience: Former fi nancial editor of the Rand Daily Mail and Executive Director of Sage Group

Current directorships: Redefi ne Properties Limited, Redefi ne International Limited and Rezco Asset Management

Andrew Konig (45)

Non-executive Director

Appointed: 20 September 2012

Nationality: South African

Qualifi cation: CA (SA)

Experience: Financial Director of Redefi ne Properties Limited. Over 19 years of commercial and fi nancial experience

Current directorships: Redefi ne Properties Limited, Alternate Director for Redefi ne International PLC

John Rainier (56)

Independent Non-executive Director

Appointed: 30 June 1997

Nationality: South African

Qualifi cation: BCom, LLB

Experience: Former Managing Director of Fountainhead Property Trust. Involved in property management since 1980

Current directorships: None

Fountainhead Property Trust | Integrated annual report 201216

It is a great pleasure for me, as Chairman

of Fountainhead Property Trust Management

Limited, to review the general state of

Fountainhead Property Trust for the financial

year ended 30 September 2012.

Whilst the global economic data has

continued to disappoint, the South African

social-economic environment has also been

challenging. GDP growth expectations for

2012 have been lowered from a previous

3.4% to 2.5%. Both consumer and producer

confidence levels are trending down, and

unemployment remains intractable. Two of

the major rating agencies downgraded the

sovereign debt of South Africa (Moody’s

Investor Services and Standard & Poor’s).

The listed property sector performed

well, helping to push the sector’s market

capitalisation to new levels. Once again, for

the 12 months ended 30 September 2012,

the sector produced the highest total return

of 37.71%, followed by equities (24.43%),

bonds (16.99%) and cash (5.61%). Analysts,

however, caution that it would be unrealistic

to expect a repeat of last year’s total return.

There continues to be downward pressure

on office rentals and rising operating

expenses across all sectors. These factors are

expected to have a negative impact on the

performance of the property sector in the short

to medium term.

The Fountainhead portfolio showed resilience

over this financial year. The weighting of

the portfolio in favour of retail has been a

distinct benefit in the performance of the

We are proud to present

Fountainhead’s second Integrated

Annual Report. Fountainhead’s aim

is to improve engagement with its

various stakeholders, ensuring that

their main concerns and interests

are adequately addressed.

Chairman’s report

Trust. Our well-located regional shopping

centres have demonstrated their defensive

attributes by maintaining low vacancies and

positive rental growth. The two key projects,

the acquisition of the remaining 25% of

Centurion and redevelopment of Blue Route

Mall, were successfully completed during

the financial year. Retailers and shoppers

responded positively to both investments.

The refurbishment and upgrade of Bryanston

Shopping Centre is progressing well.

We are pleased to report that, despite the

challenges mentioned above, Fountainhead

met its distribution forecasts for 2012, and

achieved a total annual return of 28.7%.

Operating costs were contained at 19.8%

of revenue and average cost of borrowings

reduced from 9.08% to 7.97%. Also, market

capitalisation grew by 20% to R9.4 billion.

On 1 August, Redefine Properties Limited

acquired the entire shareholding in

Fountainhead Property Trust Management

Limited (The Manager). As a result of this

acquisition, Redefine seconded asset managers

to manage the Fountainhead property portfolio,

and Alex Phakathi was appointed the Chief

Executive Officer. In September and October,

Redefine Properties Limited and Growthpoint

Limited, respectively, submitted indicative offers

to acquire the property assets of Fountainhead.

The Board of directors has appointed an

independent committee to deal with these

unsolicited offers.

Consequent to the change in shareholding

in the Manager, the following changes to

WM Kirchmann – Chairman

Fountainhead Property Trust | Integrated annual report 2012

the Board of directors occurred: Messrs Shaw-Taylor, Ogbu and

Reubenheimer resigned from the Board and Messrs Nackan and

Konig were appointed. We would like to thank the retired directors

for their contribution to the success of Fountainhead over the years.

We look forward to benefiting from the contribution of Messrs Konig,

Nackan and Phakathi.

In concluding my remarks on this unexpected new phase in

Fountainhead’s life, I wish to stress that we on the Fountainhead Board

and in the management team have endeavoured to be absolutely

scrupulous in advising unitholders about every development to enable

them to make fully informed decisions.

Finally I wish to thank my colleagues on the Board of Fountainhead

Property Trust Management Limited for their wise counsels and clear

strategy in driving the Trust’s performance, the excellence of which

has been signally recognised by our peers in the market place. Their

experience and expertise in the property sector will ensure optimum

performance by the Trust in the future, however discouraging the

macro-economy may be.

WM Kirchmann

Chairman

Blue Route Mall

Blue Route Mall

17Fountainhead Property Trust | Integrated annual report 2012

Fountainhead Property Trust | Integrated annual report 201218

King III Chapter Principle not fully applied

Board and directors The Board currently does not appoint the Chief Executive Officer. This is done by the

shareholders of the Manager. Each Board member assesses the performance of the

Chief Executive Officer annually.

No separate Nomination Committee is in place. All appointments are agreed by the Board and

the shareholder of the Manager.

No Remuneration Committee is in place as the Trust and the Manager do not have any

employees. The remuneration of each individual director is reflected in the table on page 20.

Director fees are approved by the Shareholder of the Manager.

Audit and Risk Committee The Audit and Risk Committee recommends the appointment of the external auditor and overseeing

the external audit process. Auditors are not approved by the Shareholder as no AGM is held but

reviewed and recommended by Audit and Risk Committee to the Board as required by CISCA.

Integrated reporting and disclosure The sustainability reporting and disclosure has not been independently assessed. It is envisaged

that this will be done in the future as this process matures.

Corporate governance report

The Board of Fountainhead Property

Trust Management Limited is committed

to complying with the principles of good

corporate governance as outlined in the King

Code on Corporate Governance (King III).

The board acknowledges that maintaining

good corporate governance is a continuous

process that must be consistently applied.

Having implemented various practices and

procedures recommended by King III, the

Board is satisfied that Fountainhead complies

with the requirements of King III, except in the

specific instances outlined below.

After comparing current practices with those

recommended by King III, key areas of

improvement have been identified and goals

set to achieve the desired compliance.

9. Integrated Reporting and disclosure

7. Internal Audit

8. Governing stakeholder relationships

Current State Desired State

1. Ethical leadership and corporate citizenship

2. Board and Directors

4. The governance of risk

5. The governance of Information Technology

6. Compliance with laws, codes, rules and standards

3. Audit and Risk Committee

Fountainhead Property Trust | Integrated annual report 201219

with Mr Raubenheimer stepping down as Managing and Financial

Director. Messers Konig and Nackan are directors of the Shareholder

of the Manager and are therefore not considered independent. Messrs

Laher, Savage, Christian and Rainer are classified as independent non-

executive directors.

Responsibilities:The Board meets regularly and retains full and effective control

of the Trust. The Board monitors the activities and performance of

management and is responsible for the following:

The Trust’s overall strategy

The Acquisitions and Disposal policy

Approving and monitoring the annual budget

Approving development projects

Communicating with unitholders openly and timeously throughout

the year

Significant matters relating to finance

Corporate governance

Directors are encouraged to take independent advice, at the

cost of the Manager, for the proper execution of their duties and

responsibilities. The Board has unrestricted access to the external

auditors, professional advisors, the services of the Company

Secretary, the executives and the staff of the property and asset

managers at any given time.

Board of directors:

In terms of CISCA, the Registrar of Collective Investments Schemes

strictly controls the shareholding of the Manager. The change

in shareholding of the Manager to Redefine Properties Limited,

previously Standard Bank Properties Proprietary Limited and Liberty

Group Limited, has resulted in the change in the composition of the

Board. Three directors resigned during the period and Redefine

appointed two directors to the Board of the Manager. Each director

has one vote.

The Board comprises seven non-executive directors. Five of these

directors are considered independent. The independence of directors

is assessed in accordance with King III, the JSE Listings Requirements,

and the determination of Fit and Proper assessments as required by

the Registrar. There exists a balance of power and authority at Board

level such that no one individual director has undue powers of

decision-making.

The roles of Chairman and CEO are separated. Mr Kirchmann, an

independent non-executive director, is the Chairman of the Board. The

Board has examined Mr Kirchmann’s independent status in light of his

length of service (director since 1988). The board is of the opinion

that Mr Kirchmann still acts in an independent manner in fulfilling his

duties as a Board Member. Mr Alex Phakathi was appointed CEO

The attendance at Board and Audit and Risk Committee meetings held during the year was as follows:

Director BoardAudit and Risk

CommitteeMeetingsattended

Meetings eligible

Percentageattendance

Non-executive

WM Kirchmann (Chairman) 6 – 6 7 86

VC Christian 6 5 11 12 91

HY Laher 7 5 12 12 100

DS Ogbu (resigned 24 August 2012) 4 – 4 6 67

S Shaw Taylor (resigned 24 August 2012) 5 – 5 6 83

DS Savage 7 – 7 7 100

JD Rainier 6 5 11 12 91

AJ Konig (appointed 20 September 2012) – – – – –

B Nackan (appointed 20 September 2012) – – – – –

Executive

AE Raubeheimer (resigned 30 September 2012) 7 7 7 100

Overall attendance 48 15

Maximum attendance 54 15

Percentage attendance 89 100

Fountainhead Property Trust | Integrated annual report 201220

The Board’s role and responsibilities as well as the requirements for its composition and meeting procedures are detailed in the Board Charter. The main functions of the Board as listed in the charter are to: ensure that all stakeholder relationships are managed along sound

corporate governance principles; consider strategy, risk, performance and sustainability; provide effective leadership on an ethical foundation; ensure that the business is and is seen to be a responsible

corporate citizen; ensure that ethics are managed effectively; ensure that an effective and independent Audit and Risk Committee

is in place; be responsible for the governance of risk; be responsible for Information Technology (IT) governance; ensure compliance with applicable laws and regulations; ensure that an effective risk-based internal audit is in place; ensure the integrity of the integrated annual report; ensure that directors act in the best interest of the business by

adhering to legal standards of conduct, disclosing any real or perceived conflicts to the Board, dealing in shares only in accordance with the policy adopted by the Board, and encouraging directors to take independent advice when needed fulfilling their duties; and

elect a chairman who is an independent non-executive director.

The Board has overall responsibility for managing risks. Broadly, the Board has a low risk appetite and during the year ended 30 September 2012 did not take on any undue, unexpected or unusual risks. Furthermore, no material losses were incurred by the business during the year.

The Board is not aware of any current, imminent or envisaged risk that may threaten the long-term sustainability of the business.

The Board maintains overall responsibility for managing the risk management process. In fulfilling these duties, it has delegated to the Audit and Risk Committee responsibility for ensuring that the business has an effective compliance framework and processes in place. During the year, under the guidance of the Audit and Risk Committee, various risk management processes have been put in place that the Board considers to be effective in identifying and mitigating the major risks of the business. A detailed risk register has been established which is continually reviewed by the Board. The risk register details the strategic and operational risks facing the business, the controls in place to mitigate those risks, and an action plan to reduce risk when needed.

The Board considers the internal audit function to be critical to the business. The Board has delegated to the Audit and Risk Committee responsibility for overseeing this function. Based upon the internal audit findings, the Board is satisfied with the effectiveness of the internal control system.

The following directors’ fees were paid during the year:

(R000) 2012 2011

AE Raubenheimer*†#

(resigned 30 September 2012) 86 80

WM Kirchmann 130 120

VA Christian 136 138

AJ Konig (appointed 20 September 2012) – –

HY Laher 136 138

B Nackan (appointed 20 September 2012) – –

DS Ogbu‡ (resigned 24 August 2012) 72 80

JD Rainier˜ 136 138

DS Savage (appointed 2 August 2011) 86 13

S Shaw-Taylor† (resigned 24 August 2012 72 80

Total directors’ remuneration 854 854

* Executive.† Paid directly to The Standard Bank of South Africa Limited.‡ Paid directly to Liberty Group Limited.˜ In 2012 Rnil paid directly to Standard Bank. 2011 R40 000 was paid directly to

Standard Bank.# In 2012 R72 000 paid directly to Standard Bank and R14 400 was paid directly

to Redefine.

The directors’ fees are approved by the Shareholder and are

benchmarked against market trends.

The Board has established a formal policy to regulate private account

dealings in the Trust’s units. This is applicable to all directors as well

as employees of the Trust’s asset manager who are involved in the

management of the Trust as well as those employees of the contracted

third party managers. The Board enforces a closed period when no

private account dealings are permitted from one month prior to year-

end or half-year, as the case may be, until such time as the results are

published.

Directors’ interests in Fountainhead Property Trust at 30 September

2012 are as follows:

Director

Number

of shares

Movement

for the year

WM Kirchmann 118 006 –

AE Raubenheimer 10 000 –

HY Laher 768 –

J Rainier 160 000 –

There has been no change in directors’ interests from the end of

the financial year to the date of approval of the annual financial

statements.

Corporate governance report (continued)

Fountainhead Property Trust | Integrated annual report 201221

The committee has adopted formal terms of reference which have been approved by the Board. The committee has fulfilled its responsibilities for the year in compliance with its terms of reference. The main responsibilities of the committee as listed in the terms of reference are to: oversee the integrated reporting process; ensure that the combined assurance model is applied to provide a

co-ordinated approach to all assurance activities; review the expertise, resources and experience of the Trust’s

finance function; oversee the internal audit function; oversee the risk management process; and recommend the appointment of the external auditor and oversee

the external audit process.

The internal audit function has been outsourced to BDO Risk Advisory Services Proprietary Limited (BDO). BDO has a direct reporting line to the committee, and works closely with management in order to help fulfil their duties.

The committee reviewed and approved the internal audit plan for 2012 and is satisfied that the plan was executed accordingly. The committee has also reviewed the internal audit findings from BDO for the 2012 financial year. Based on the internal audit report, the committee is satisfied that adequate controls exist and that they operate effectively within the internal control environment. In conjunction with BDO, the committee formulated an internal audit charter which has been approved by the Board.

The committee has complied with all applicable legal and regulatory responsibilities.

Based on the committee’s aggregated experience and assurances received, nothing has come to the attention of the committee that could possibly impair the independence of the external auditor. The committee has recommended the re-appointment of KPMG Inc. as external auditors for 2013. The committee has assessed the expertise, adequacy and experience of the finance function and its senior staff members. After discussion with external and internal audit, and following the committee’s interaction with the finance function, the committee is satisfied with the expertise and adequacy of the finance function as well as the experience of senior staff members within the finance function. Furthermore, the committee believes that Mr Aaron Suckerman, the Financial Manager, possesses the appropriate expertise and experience to meet his responsibilities in this position as required by the JSE Listings Requirements.

The committee has recommended the integrated annual report to the Board for approval.

On behalf of the committee

Victor Christian

Chairman of the Audit and Risk Committee

The Board considers sound relationships with the various stakeholders to be a priority and management has responsibility for ensuring that effective and transparent communication channels with the various stakeholders are in place. In line with the requirements of the Registrar, the Trust has established a Complaint Resolution Policy which is available for viewing on the Trust’s website and at the registered office. During the year, dealings with stakeholders have been in the normal course of business and have been administered in a professional manner.

Board assessmentThe Board has adopted a Board and committee assessment framework. The first assessment was performed during the 2012 financial year, the evaluation including an evaluation of the true independence of directors classified as independent non-executive directors.

The Board was asked to rate relevant issues on a 1 to 5 scale; from ‘strongly disagree’ to ‘strongly agree’. The responses are indicative of a general perception by Board Members that they contribute to corporate leadership and stewardship and the achievement of the Trust’s objectives. The directors believe they have a good understanding of Fountainhead’s strategic plan and key issues. Board members generally believe that they contribute constructively to the resolution of issues at meetings, and that communication of expectations is clear. In general, the view is that information is obtained in an adequate, relevant and timely manner and that meeting attendance and preparation for such meetings are good.

Audit and Risk CommitteeThe Audit and Risk Committee (the committee) is a statutory committee of the Board of directors of Fountainhead Property Trust Management Limited in respect of its statutory duties in terms of the Companies Act. In addition, the committee has similar duties in terms of CISCA in relation to Fountainhead Property Trust. The committee also has other duties as assigned to it by the Board of directors. It reports to the Board regularly. In addition, it reports to unitholders on the extent to which it has carried out its statutory oversight duties – in respect of the external auditors, the appropriateness of the financial statements and the accounting practices, as well as the effectiveness of the internal financial controls.

The committee comprises three independent directors:

Director Period served on committee

VA Christian 19 May 2006 – present

HY Laher 4 February 2009 – present

JD Rainier 4 February 2009 – present

Fountainhead Property Trust | Integrated annual report 201222

1. Nature of business and strategy As indicated earlier in this integrated report, the Fountainhead

Property Trust, as a collective investment scheme in property, distributes to its unitholders all the net income derived from its real estate assets.

Our strategy is to grow the value of our property portfolio and our distributions to provide sustainable and increasing returns for unitholders over the long term. We seek to acquire quality properties with good growth prospects and where appropriate, dispose of underperforming assets. Properties are refurbished where the expenditure is justified by the return on capital or to preserve the asset values.

Manager’s report

2. Global economic overview Domestic economic confidence and performance have

shadowed the turmoil in global economic markets. Global economic data continues to disappoint expectations of imminent recovery, especially in the Eurozone, and GDP growth forecasts have sagged across the board. Expected World GDP growth for 2012 has fallen to 3.1%, 0.6% lower than was forecast in October 2011. South Africa’s GDP growth for 2012 has also been revised down to 2.5%, 0.9% lower than the previous forecast.

Expectations of GDP growth for 2012 in various major global economies are shown in the table below:

Oct 2011 Nov 2012 Change

US 2.5 2.2 (0.3)Euro Area 0.9 (0.4) (1.3)UK 1.4 0.0 (1.4)Japan 2.4 2.1 (0.3)Brazil 3.9 1.6 (2.3)Russia 4.4 3.9 (0.5)India 7.6 5.4 (2.2)China 8.4 7.6 (0.8)South Africa 3.4 2.5 (0.9)World 3.7 3.1 (0.6)

Source: Barclays Capital

In this scenario, most central banks, including the South African Reserve Bank (SARB), have kept interest rates at lower levels for far longer than ever before in an effort to stimulate their economies. The SARB has kept the repo rate below 10% since 2009. The current repo rate is 5%.

South African economic overview As illustrated in the graph below, business and consumer confidence have fallen steadily over the short to medium term, further confirming that

the economy is in a period of much subdued growth. Real retail sales registered growth of 4.3% in the year to 30 September 2012.

-20

0

20

40

60

80

100

05

05

06

06

06

06

07

07

08

08

08

08

09

09

09

09

10

10

10

10

11

11

11

11

12

12

12

12

07

07

Source: Bureau for Economic Research

Fountainhead Property Trust | Integrated annual report 201223

Certain salient issues emerging from an analysis of the 2011 census figures are influencing and will continue to influence the general direction of the economy and the property sector. These issues are:

Relatively slower population growth. A younger population. Migration to the metropolitan areas, where work opportunities

are greater. Increases in the numbers of learners completing school and in

the numbers of those proceeding to tertiary education. Increasing average household income.

These findings have a particular relevance in planning property development and investment, especially in retail properties.

The property market trends For the 12 months ended 30 September 2012, SA Listed

Property, as an asset class, recorded the highest total return (37.71%), followed by SA Equities (24.43%), SA Bonds (16.99%) and Cash (5.61%). Direct property investment, according to the recent IPD Index, achieved a respectable total return of 10.4%, which is above the inflation rate for the same period. Income return and capital growth registered 8.9% and 1.4%, respectively.

The chart below shows the relative performance of the three property sectors in South Africa. There were no significant differences in the capital growth performance of the individual sectors. Retail property was marginally ahead of office and industrial, but it is expected that all values will remain subdued until there is improvement in the overall economy.

Source: Investment Property Databank

REIT tax legislation Real Estate Investment Trust (REIT) tax legislation was announced

and published in the Taxation Laws Amendment Bill of 25 October

2012, to come into effect from 1 April 2013. A “REIT” is defined

as a company that is a South African resident and the shares of

which are listed on an exchange. The definition of “company”

has been expanded to include a portfolio of a collective

investment scheme in property (PUT). This allows PUTs to qualify

for company restructuring provisions and rollover relief at unitholder

level. The salient features of the REIT tax legislation are:

REITs are permitted to have external asset management

companies.

No conversion or transfer tax will be payable.

Deferred tax arising from property revaluations will be

eliminated from statements of financial position and no CGT

will be payable on property disposals.

Gearing is capped at 60% loan to value.

Minimum 75% of income to be property rental.

Minimum 75% payout ratio (retained income will be taxed).

Foreign withholding tax of 15% to be levied from 2014.

The introduction of REIT legislation is a significant development for

the listed property industry and should benefit all stakeholders.

3. Management of the Fountainhead Portfolio

On 1 August 2012 Redefine Properties Limited acquired

the entire shareholding in Fountainhead Property Trust

Management Limited (the Manager), replacing Standard

Bank and Liberty. All formalities have been completed

and the shares have been duly transferred to Redefine. In

September, Redefine seconded four asset managers and a

finance manager to provide asset management services to

the Fountainhead Portfolio.

The Broll Property Group continues to provide property

management to the bulk of the property portfolio, whilst

Redefine and Motseng Property Services have been appointed

to manage the remainder of the properties.

In November 2011, Absa Bank Limited gave notice of its

intention to retire as trustee of Fountainhead Property Trust, in

accordance with the requirements of the Collective Investments

Schemes Control Act of 2002. The board of directors of

the Manager approved the appointment of FirstRand Bank

Limited as trustee in the place of Absa, subject to approval

by the FSB, which was duly granted with effect from

16 November 2012.

Ret

urn

(%pa)

0

2

4

6

8

10

12

14

Retail

1.6

8.3

10.1

Office

1.3

9.7

11.2

Industrial

1.4

10.4

11.9

Capital Growth (% pa)

Income Return (% pa)

Total Return (% pa)

All Property

1.4

8.9

10.4

Fountainhead Property Trust | Integrated annual report 201224

4. Review of results and operations

Fountainhead Property Trust has declared a distribution of

27.83 cents per unit for the six months ended 30 September

2012 which, combined with the distribution of 28 cents for the

half-year ended 30 March 2012, resulted in a total distribution

of 55.83 cents per unit for the year ended 30 September

2012, 1% more than in the previous year. Included in the

current year’s distribution is the reversal of prior year municipal

accruals of R11.6 million and the dilutive effect of expensing the

borrowing costs of the redevelopment of Blue Route Mall. The

core portfolio, excluding properties acquired, properties disposed

of, or properties under development showed growth of 5.2%,

with contractual rental showing muted growth of 6.0%, primarily

due to tougher market conditions and negative reversions on

lease renewals.

Retail Market The Trust’s retail portfolio, which measures 471 757 m2,

generated net income growth of 20.9% for the year to

30 September 2012. On a like-for-like basis, excluding the

effect of purchasing 25% of Centurion Mall, net income growth

was 11.7%. The Blue Route Mall opened on 29 March 2012

and contributed R52 million to distributable income for the year.

The retail market continues to perform well, with retail vacancies

declining from 7.0% to 6.5%. Included in the vacancy figure is

the office space at Centurion Mall, which remains vacant and

contributes 3.2% of the total vacancy. Leases were concluded

on 65 501m2 of GLA at an average rental of R165/m2,

representing average rental growth of 1.1%. Of the leases that

expired during the period, 85% were renewed. The weighted

average rental increased from R133/m2 at 30 September 2011

to R141/m2 at 30 September 2012, with an average lease

escalation of 8.32%.

Key Retail Portfolio indicators Total reported sales turnover grew by 8.78%.

Foot-counts increased by 2%.

Average basket size increased by 6% to R111.

The operating expenses as a percentage of income reduced

by 10.0% to 21.1%.

The rent-to-turnover ratio is 6.03% and remains comfortably within

accepted norms for the retail sector. The tenant’s sales revenues

are growing comfortably in line with rentals.

Office Portfolio The Trust’s office portfolio, which measures 141 702m2,

generated net income growth of 33.6%. On a like-for-like basis,

excluding the effect of properties not held for 12 months in a

comparable period, the growth for the year is 3.72%. The office

market continues to improve in the year under review, the vacancy

rate declining sharply from 10.2% at September 2011 to 7.1%

at the end of the current financial year. Leases were concluded

on 23 393m2 of GLA at an average rental of R88/m2 and an

average negative rental reversion of -12.14%.The weighted

average rental increased from R109/m2 at 30 September 2011

to R115/m2, representing an average lease escalation of 8.24%.

Key Performance Indicators Negative rental reversions of -12.14% on new lets

and renewals.

71% of leases expiring during the period were renewed.

The operating expenses as a percentage of income reduced

by 18.00% to 17.42%.

Industrial Portfolio The Trust’s Industrial portfolio, which measures 167 770m2,

generated net income growth of 2.4%. The industrial market

continued to take strain, with rental continuing to be under

negative pressure and the vacancy rate increasing from 7.3%

at 30 September 2011 to 8% at the end of the current financial

Manager’s report (continued)

Segmental contribution to retail turnover for the year

6%

2%26%

5%

2%

8%

7%

4%

40%

Food Retailers

Apparel

Home & Furniture

Electronic & Media

Health & beauty

Food & Entertainment

Jewellery & Eyewear

Mass Discounters

Other

Fountainhead Property Trust | Integrated annual report 201225

year. Leases were concluded on 42 624m2 of GLA at an

average rental of R38/m2 and an average negative rental

reversion of -10.89%. The weighted average rental increased

slightly from R45/m2 at 30 September 2011 to R47/m2, with

an average lease escalation of 8.05%.

Key Performance Indicators Negative rental reversions of –10.89% on new lets and renewals.

74% of leases expiring during the period were renewed.

The operating expenses as a percentage of income increased

by 2.00% to 21.64%.

5. Property expenses and cost ratios

Net operating income from properties:

Property revenue (R) 1 042 million

Operating costs (R) 202 million

Net operating income (R) 840 million

Operating cost (%)* 19.8

*Excludes tenant installation and letting commission amortisation

Percentage of total operating cost summarised as follows:

Portfolio ratios: Property management costs as a % of collections 2.7%

Municipal recoveries as a % of municipal charges 74.0%

Electricity recoveries as a % of electricity charges 115.0%

6. Exposure to major tenants Exposure to major tenants is as follows (proportionate share where appropriate):

0%

5%

10%

15%

20%

25% 23.3%20.6%

18.7%

12.8%

4.9% 4.7% 3.8% 3.6% 2.8% 2.6% 2.2%

Man

agem

ent f

ees

Staf

f

Clean

ing

Letting

com

miss

ion

Repa

irs &

mai

nten

ance

Insu

ranc

e

Sund

ry e

xpen

ses

Tena

nt in

stalla

tions

Secu

rity

Bad

debt

s

Mar

ketin

g

Edco

n

Stan

dard

Ban

k

Shop

rite

Ster

Kinek

or

Truw

orths

Mr P

rice

Southe

rn S

un

PEPK

OR

Mas

smar

t

Ned

bank

Fosc

hini

ABSA

Life

Hea

lthca

re G

roup

Clic

ks

Mur

ray

and

Robe

rts

Pick

n P

ay

Gov

ernm

ent o

f RSA

Woo

lwor

ths

First N

atio

nal B

ank

Virg

in A

ctive

0

1%

2%

3%

4%

5%

6%

% Total Fountainhead Area % Total Fountainhead Rental

Fountainhead Property Trust | Integrated annual report 201226

7. Lease expiries for the next 12 months The lease expiry profile as a % of rentable area at 30 September 2012 is:

Building Vacant Year 1 Year 2 Year 3 Year 4 Year 5 5 year +

Retail 8 17 14 22 9 8 22

Office 7 16 9 14 6 17 31

Industrial 7 53 22 11 2 6 0

Specialised 0 0 0 0 0 0 100

Total 6 25 14 18 7 9 21

Due to the large number of industrial tenants on monthly leases, the lease expiry figure for the following year is inflated. The majority of these

tenants have been in occupation for over three years and are not expected to vacate during the next 12 months.

8. Valuations The composition of Fountainhead Property Trust’s Portfolio, as valued by the independent valuer, Rode and Associates CC,

as at 30 September 2012, is as follows:

Value Cents/UnitForward

earnings yield Percentage of portfolio

Sector (Rm) (%) 2012 2011

Retail 8 226 707 8.0 76 72

Office blocks 1 680 145 9.7 16 18

Industrial 541 47 12.1 5 7

Specialised 348 30 10.4 3 3

Total property 10 795 929 8.5 100 100

Interest-bearing liability (2 733) (235)

Net current assets 1 0

8 063 694

The portfolio is concentrated significantly around 15 properties making up 85% of the portfolio value. There have been no material changes

to the information used and the assumptions applied by the registered valuer compared to prior years.

Manager’s report (continued)

Fountainhead Property Trust | Integrated annual report 201227

9. Acquisitions and disposals The Trust purchased the following properties during the year:

Sector Building name Location Price Initial yield Transfer date

Retail Centurion Mall – 25% undivided share Centurion, PTA R751 519 364 7,10% 15 December 2011

Retail Centurion Boulevard Centurion, PTA R366 000 000 8,20% 27 March 2012

Office Cedarwood Bryanston, JHB R77 843 799 9,00% 4 January 2012

The Trust sold the following properties during the year:

Sector Building name Location Transfer date Selling price Valuation Profit on sale

Industrial Medsave House Strijdom Park, Johannesburg 3 October 2011 R2 446 000 R2 446 000 –

Industrial 4 Walter Place Watervalpark, Mayville 18 April 2012 R27 352 730 R22 536 643 R4 816 087

Office Wierda Mews 41 Wierda Road, Wierda Valley 3 April 2012 R17 949 963 R10 979 681 R6 970 282

Essex Park realised net proceeds of R30.2 million (valuation R30.2 million), with registration of transfer occurring after year-end.

10. Major capital projects

Blue Route Mall The Mall was opened on 29 March 2012 and was 99% let at the time. The Mall is trading in line with expectations and has been

well-received by tenants and shoppers. On-grade parking for an additional 2 000 parking bays is currently under construction and is due

for completion in early 2013, bringing this phase of the project to final completion. During the year an application for additional bulk

was submitted to allow for future expansion of the Mall. The additional parking bays under construction will allow for future expansion of

the Mall.

Bryanston Shopping Centre A R32 million refurbishment is underway at Bryanston Shopping Centre. The centre will receive a major facelift, with all ceilings and floors

being replaced and entrances enhanced. The refurbishment, due for completion in November 2012, will marginally enhance earnings.

Centurion Mall A R19 million refurbishment is underway which includes an upgrade of the spine area and capital replacement of the skylights.

The refurbishment is due for completion in November 2012. This capital expenditure will enhance the overall appeal of the Mall.

11. Letting activity

Retail Office Industrial

Area (m2)% of year end area Area (m2)

% of year end area Area (m2)

% of year end area

Vacant at 30 September 2011 29 221 6.2 14 217 10.0 13 355 8.0

Sold – – 1 166 0.8 – –

Acquired 3 994 0.8 – – – –

Vacated 22 834 4.8 5 890 4.2 13 493 8.0

New leases (25 237) (5.3) (11 272) (7.9) (13 359) (8.0)

Vacant at 30 September 2012 30 812 6.5 10 001 7.1 13 489 8.0

Fountainhead Property Trust | Integrated annual report 201228

12. Borrowings The Trust has a total facility of R3 035 million. The Trust’s gearing level is presently at 24.3%. The recent acquisitions and the redevelopment

of Blue Route Mall have increased the gearing ratio from 11.32% at 30 September 2011. The Board is satisfied with the increase in

gearing and the trust deed allows for a maximum gearing of up to 40%. The Interest cover is currently 5.2 times, which is well within the

debt covenants, set at 2 times.

Current facilities

Facility

(R000)Balance at

September 2012 Available Rate Maturity

Term loan 1 685 544 64 456 7.06% 30 June 2015

Term loan 2 250 000 – 11.39% 30 June 2013

Term loan 3 200 000 – 6.76% 30 June 2013

Term loan 4a 350 000 – 8.42% 31 May 2015

Term loan 4b 427 661 157 339 7.54% 31 May 2015

Term loan 5 520 000 80 000 8.72% 28 February 2016

Term loan 6 220 000 – 6.79% 30 June 2013

Term loan 7 80 000 – 6.74% 30 June 2013

2 733 205 301 795 7.97%

13. Vacancies The table below provides details of the Trust’s vacancies at 30 September 2011 and 30 September 2012:

SectorSeptember 2012

%September 2011

%

Retail 6.5 7.0

Office blocks 7.1 10.2

Industrial 8.0 7.3

Specialised – –

Total 6.7 7.4

Vacancy levels in terms of rentable area were as follows:

By value, the vacancies equated to 3.5% of the rent roll for September 2012, compared with 4.9% at 30 September 2011.

The retail component has a vacancy of 6.5%, primarily at Brightwater Commons and the offices at Centurion Mall, also known as

Die Anker.

The office component has a vacancy of 7.1%, primarily in Grayston Ridge and AMR Office Park.

The industrial component has a vacancy of 8%, primarily at Supreme Industrial Park and the Jet Park mini-units.

Manager’s report (continued)

Fountainhead Property Trust | Integrated annual report 201229

14. Unitholder summary The Trust’s major shareholders at 30 September 2012 are shown below:

Unitholders’ groupings holding 3% or more Number of units Percentage

Old Mutual 96 049 720 8.26STANLIB 87 389 923 7.52Government Employees Pension Fund 70 551 641 6.07Investec 59 073 608 5.08Standard Bank 51 523 517 4.43Eskom Pension & Provident Fund 45 899 050 3.95Investment Solutions 44 443 083 3.82Sanlam 34 919 055 3.00

Total 489 849 597 42.13

Public and non-public unitholders According to Fountainhead’s transfer secretaries, the unitholders spread of Fountainhead is as follows:

Number of unitholders Number of units Percentage

Non-public unitholders 5 580 494 0.05Public unitholders 8 267 1 162 129 254 99.95

Total 8 272 1 162 709 748 100.00

The non-public unitholders are the directors, whose interests are disclosed in the Corporate governance report, and the Manager whose holding is disclosed in note 2 to the annual financial statements of FPTML.

15. Asset and property management fees The service fee payable by the Trust to the Manager for the year was 0.5% per annum of the enterprise value of the Fund, which is total

market capitalisation plus the aggregate amount of borrowings, calculated monthly on the average daily closing prices. The amount paid was R53.5 million (2011: R40.4 million).

Asset management fees of R40.1 million (2011: R30.3 million) were paid by the Manager to the Evening Star Trading 768 Proprietary Limited. Administration fees of R1.3 million (2011: R1.2 million) were paid by the Manager to Broll Property Group.

Property management fees paid for the 12 months ended 30 September 20122012(R000)

2011(R000)

Broll Property Group Proprietary Limited 31 084 32 426Motseng Property Services Proprietary Limited 3 070 2 801McWilliam Murray Realty Proprietary Limited 1 362 1 219Abreal Proprietary Limited 6 446 –

41 962 36 446

16. Prospects Based on difficult trading conditions currently being experienced, the temporary dilution of Blue Route Mall, the effect of hedging the debt

and further committed capital expenditure of approximately R98 million, it is anticipated that distributions for 2013 will be unchanged compared with the year ended 30 September 2012. Distributions for the year ending 30 September 2014 are expected to show an increase of 7.2%.

This forecast has not been reviewed or reported on by Fountainhead Property Trust’s auditor.

Fountainhead Property Trust | Integrated annual report 201230

Blue Route MallA thorough redevelopment of the Blue Route

Mall in Cape Town had been contemplated

for some years and several considerations

contributed to the ultimate decision to proceed

with a radical makeover including the erection

of a new shopping centre.

The thirty-year old premises had grown

somewhat haphazardly over time, with

little regard to the architectural aptness of

occasional add-ons. The fabric of the building

and the services (power and water) had also

considerably decayed or deteriorated.

In addition, the centre did not function well

from a retail perspective – parking was

neither adequate nor readily accessible and

customer traffic flow through and around the

Mall was poor. Importantly, retail tenants did

not have ideally sized and suited spaces and

were therefore not trading as successfully as

they otherwise might have.

After consideration of the above, the

Fountainhead Board decided to rebuild

Blue Route in order to create a new mall

with a lettable area of 55 504m² and attract

retail tenants appropriate to the upmarket

demographics of the neighbourhood. The

budgeted estimated project capital cost

was approximately R935 million at a 5%

incremental yield.

A double-volume design with spacious, airy

malls was decided on, with attractive views of

the Constantiaberg to be had from the food-

court and elsewhere.

While construction was proceeding,

the Manager applied for 20 000m² of

additional bulk which is still being considered

by the local authority. Fountainhead has

decided to proceed with construction of a

further 400 parking bays needed for future