20091218_rei_report

DESCRIPTION

20091218_REI_ReportTRANSCRIPT

Real Estate Asset Class Review

December 18, 2009

Gary R. Dokes, ASRS Chief Investment Officer

Eric Rovelli, ASRS Real Estate Portfolio Manager

Micolyn Yalonis, The Townsend Group Principal

Jennifer Young, The Townsend Group Consultant

Bruce Rosenberg, Director, Credit Suisse, CFIG

Page(s)

■ Real Estate Program Overview 3

■ Real Estate Program Constraints 4

■ Real Estate Program Activity 5

■ Portfolio Performance 6 - 7

■ Portfolio Composition 8 - 9

■ Portfolio Vintage Exposure 10 - 13

■ Risk Assessment 14 - 16

■ View of the World & ASRS Capital Plan (Exhibit A)

2

ASRS Real Estate Program – Discussion Items

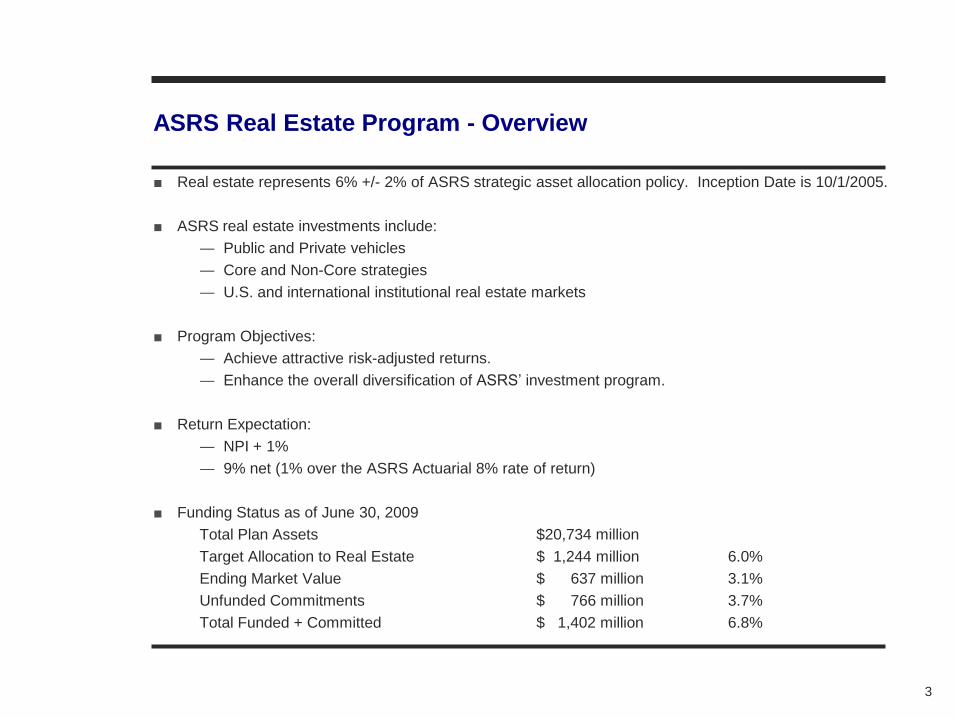

■ Real estate represents 6% +/- 2% of ASRS strategic asset allocation policy. Inception Date is 10/1/2005.

■ ASRS real estate investments include:

― Public and Private vehicles

― Core and Non-Core strategies

― U.S. and international institutional real estate markets

■ Program Objectives:

― Achieve attractive risk-adjusted returns.

― Enhance the overall diversification of ASRS‟ investment program.

■ Return Expectation:

― NPI + 1%

― 9% net (1% over the ASRS Actuarial 8% rate of return)

■ Funding Status as of June 30, 2009

Total Plan Assets $20,734 million

Target Allocation to Real Estate $ 1,244 million 6.0%

Ending Market Value $ 637 million 3.1%

Unfunded Commitments $ 766 million 3.7%

Total Funded + Committed $ 1,402 million 6.8%

3

ASRS Real Estate Program - Overview

* ASRS‟ 31% exposure to Non-U.S. investments represents the Plan‟s current Funded Portfolio.

Significant capital has been committed, but not yet called for domestic strategies which will decrease

ASRS‟ exposure to Non-U.S. investments over time (AEW, CBRE, CIM, Dune and Westbrook).

― The ASRS Strategic Plan allows for temporary variances in diversification during initial

allocations and Portfolio formation.

** The Core Private Portfolio has exceeded its loan-to-value constraint due to unrealized equity losses,

not deliberate use of excess debt. However, all debt was in compliance of Strategic Plan guidelines at

the time of origination.

4

ASRS Real Estate Program – Constraints

1Percentages representative of private assets only. 2F&C is defined as Funded & Committed which equals the 6/30/2009 market value + unfunded commitments. 3Percentages represent ASRS‟ Funded status as of 6/30/2009.

Constraint1 Strategic

Allowance

% of Portfolio F&C as

of 6/30/20092

Total Core Portfolio Minimum 20% 23%

Public Securities Maximum 30% 6%

Total Non-Core Portfolio Maximum 80% 77%

International Exposure3 Maximum 30% 31%*

Total Portfolio Leverage3 Maximum 65% 58%

Total Core Private Portfolio Leverage3 Maximum 30% 42%**

ASRS % Interest in Commingled Fund Maximum 20% N/A

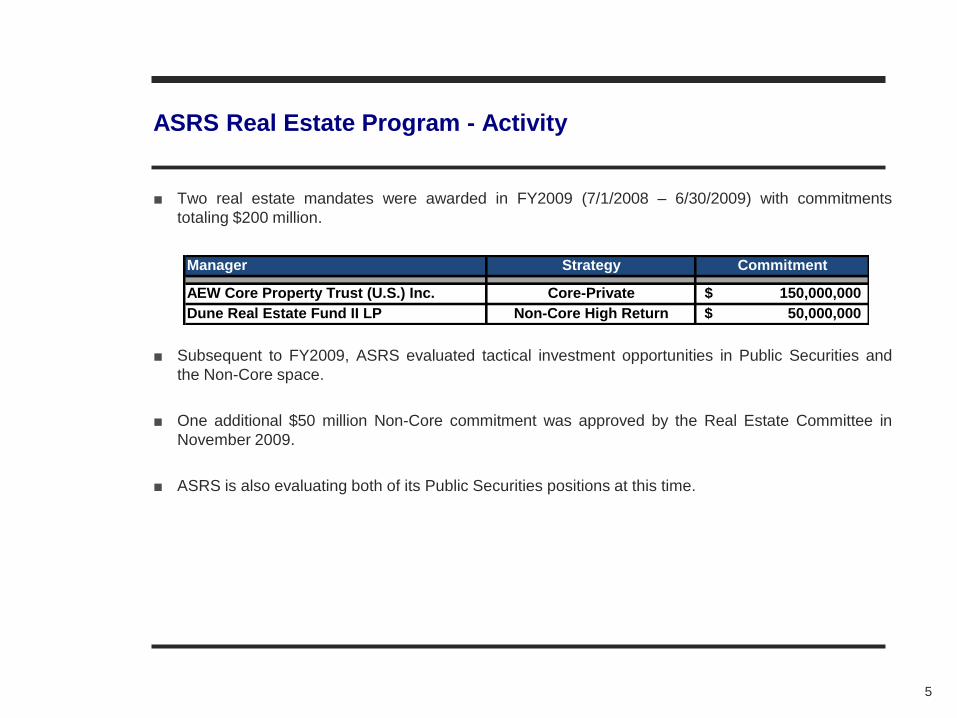

■ Two real estate mandates were awarded in FY2009 (7/1/2008 – 6/30/2009) with commitments

totaling $200 million.

■ Subsequent to FY2009, ASRS evaluated tactical investment opportunities in Public Securities and

the Non-Core space.

■ One additional $50 million Non-Core commitment was approved by the Real Estate Committee in

November 2009.

■ ASRS is also evaluating both of its Public Securities positions at this time.

5

ASRS Real Estate Program - Activity

Manager Strategy Commitment

AEW Core Property Trust (U.S.) Inc. Core-Private 150,000,000$

Dune Real Estate Fund II LP Non-Core High Return 50,000,000$

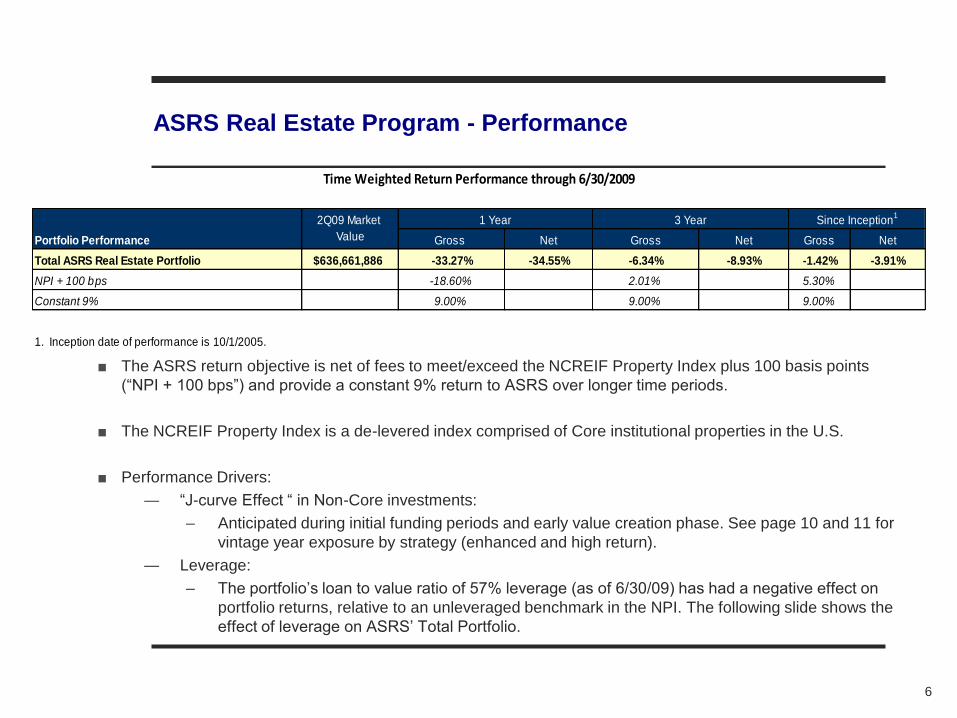

■ The ASRS return objective is net of fees to meet/exceed the NCREIF Property Index plus 100 basis points

(“NPI + 100 bps”) and provide a constant 9% return to ASRS over longer time periods.

■ The NCREIF Property Index is a de-levered index comprised of Core institutional properties in the U.S.

■ Performance Drivers:

― “J-curve Effect “ in Non-Core investments:

– Anticipated during initial funding periods and early value creation phase. See page 10 and 11 for

vintage year exposure by strategy (enhanced and high return).

― Leverage:

– The portfolio‟s loan to value ratio of 57% leverage (as of 6/30/09) has had a negative effect on

portfolio returns, relative to an unleveraged benchmark in the NPI. The following slide shows the

effect of leverage on ASRS‟ Total Portfolio.

6

ASRS Real Estate Program - Performance

Gross Net Gross Net Gross Net

Total ASRS Real Estate Portfolio $636,661,886 -33.27% -34.55% -6.34% -8.93% -1.42% -3.91%

NPI + 100 bps -18.60% 2.01% 5.30%

Constant 9% 9.00% 9.00% 9.00%

1. Inception date of performance is 10/1/2005.

1 Year 3 Year Since Inception1

Portfolio Performance

2Q09 Market

Value

Time Weighted Return Performance through 6/30/2009

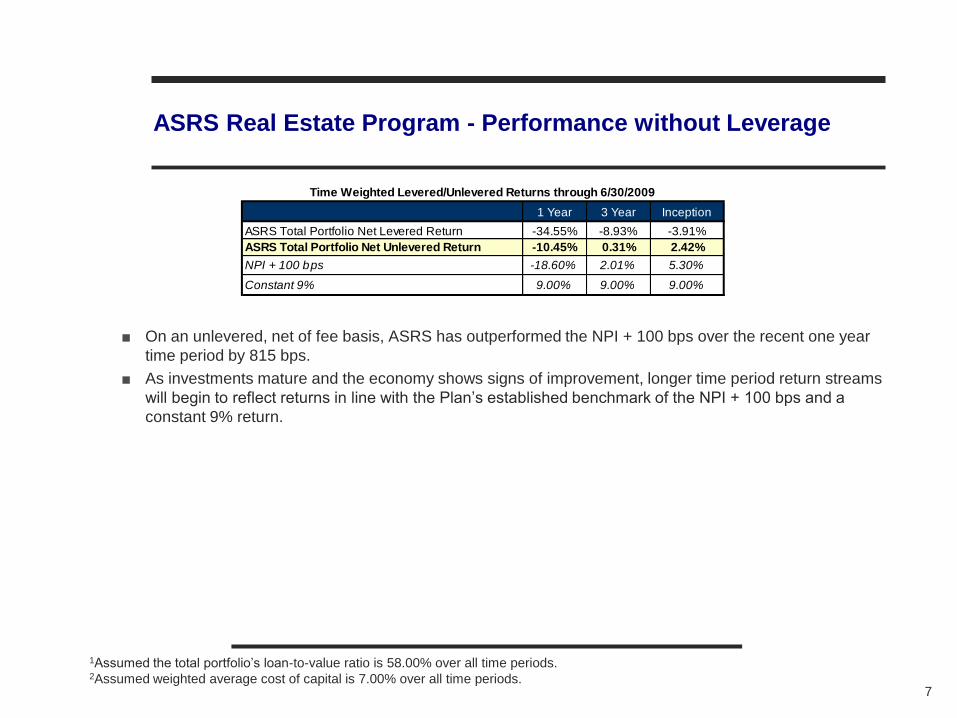

■ On an unlevered, net of fee basis, ASRS has outperformed the NPI + 100 bps over the recent one year

time period by 815 bps.

■ As investments mature and the economy shows signs of improvement, longer time period return streams

will begin to reflect returns in line with the Plan‟s established benchmark of the NPI + 100 bps and a

constant 9% return.

7

ASRS Real Estate Program - Performance without Leverage

1 Year 3 Year Inception

ASRS Total Portfolio Net Levered Return -34.55% -8.93% -3.91%

ASRS Total Portfolio Net Unlevered Return -10.45% 0.31% 2.42%

NPI + 100 bps -18.60% 2.01% 5.30%

Constant 9% 9.00% 9.00% 9.00%

Time Weighted Levered/Unlevered Returns through 6/30/2009

1Assumed the total portfolio‟s loan-to-value ratio is 58.00% over all time periods. 2Assumed weighted average cost of capital is 7.00% over all time periods.

8

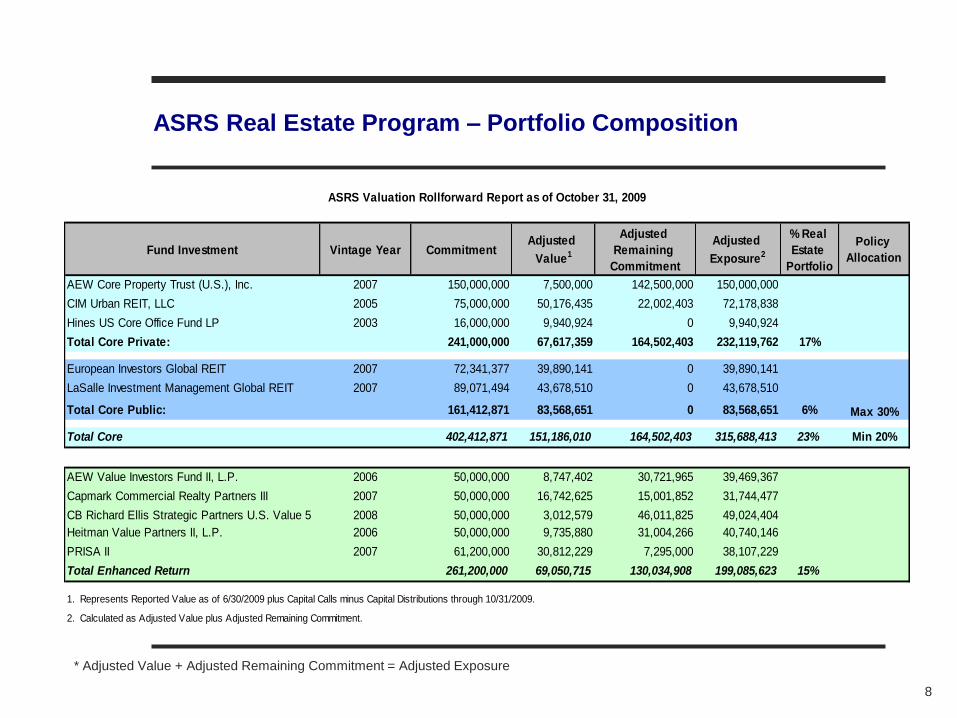

ASRS Real Estate Program – Portfolio Composition

* Adjusted Value + Adjusted Remaining Commitment = Adjusted Exposure

Fund Investment Vintage Year CommitmentAdjusted

Value1

Adjusted

Remaining

Commitment

Adjusted

Exposure2

% Real

Estate

Portfolio

Policy

Allocation

AEW Core Property Trust (U.S.), Inc. 2007 150,000,000 7,500,000 142,500,000 150,000,000

CIM Urban REIT, LLC 2005 75,000,000 50,176,435 22,002,403 72,178,838

Hines US Core Office Fund LP 2003 16,000,000 9,940,924 0 9,940,924

Total Core Private: 241,000,000 67,617,359 164,502,403 232,119,762 17%

European Investors Global REIT 2007 72,341,377 39,890,141 0 39,890,141

LaSalle Investment Management Global REIT 2007 89,071,494 43,678,510 0 43,678,510

Total Core Public: 161,412,871 83,568,651 0 83,568,651 6%

Total Core 402,412,871 151,186,010 164,502,403 315,688,413 23% Min 20%

AEW Value Investors Fund II, L.P. 2006 50,000,000 8,747,402 30,721,965 39,469,367

Capmark Commercial Realty Partners III 2007 50,000,000 16,742,625 15,001,852 31,744,477

CB Richard Ellis Strategic Partners U.S. Value 5 2008 50,000,000 3,012,579 46,011,825 49,024,404

Heitman Value Partners II, L.P. 2006 50,000,000 9,735,880 31,004,266 40,740,146

PRISA II 2007 61,200,000 30,812,229 7,295,000 38,107,229

Total Enhanced Return 261,200,000 69,050,715 130,034,908 199,085,623 15%

ASRS Valuation Rollforward Report as of October 31, 2009

Max 30%

1. Represents Reported Value as of 6/30/2009 plus Capital Calls minus Capital Distributions through 10/31/2009.

2. Calculated as Adjusted Value plus Adjusted Remaining Commitment.

9

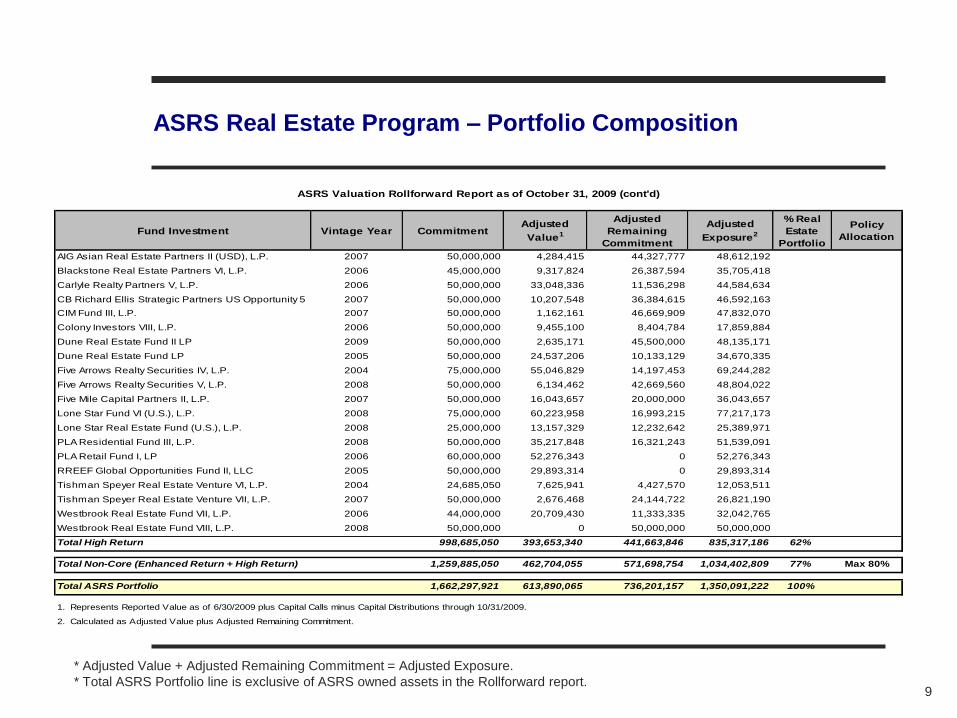

ASRS Real Estate Program – Portfolio Composition

* Adjusted Value + Adjusted Remaining Commitment = Adjusted Exposure.

* Total ASRS Portfolio line is exclusive of ASRS owned assets in the Rollforward report.

Fund Investment Vintage Year CommitmentAdjusted

Value1

Adjusted

Remaining

Commitment

Adjusted

Exposure2

% Real

Estate

Portfolio

Policy

Allocation

AIG Asian Real Estate Partners II (USD), L.P. 2007 50,000,000 4,284,415 44,327,777 48,612,192

Blackstone Real Estate Partners VI, L.P. 2006 45,000,000 9,317,824 26,387,594 35,705,418

Carlyle Realty Partners V, L.P. 2006 50,000,000 33,048,336 11,536,298 44,584,634

CB Richard Ellis Strategic Partners US Opportunity 5 2007 50,000,000 10,207,548 36,384,615 46,592,163

CIM Fund III, L.P. 2007 50,000,000 1,162,161 46,669,909 47,832,070

Colony Investors VIII, L.P. 2006 50,000,000 9,455,100 8,404,784 17,859,884

Dune Real Estate Fund II LP 2009 50,000,000 2,635,171 45,500,000 48,135,171

Dune Real Estate Fund LP 2005 50,000,000 24,537,206 10,133,129 34,670,335

Five Arrows Realty Securities IV, L.P. 2004 75,000,000 55,046,829 14,197,453 69,244,282

Five Arrows Realty Securities V, L.P. 2008 50,000,000 6,134,462 42,669,560 48,804,022

Five Mile Capital Partners II, L.P. 2007 50,000,000 16,043,657 20,000,000 36,043,657

Lone Star Fund VI (U.S.), L.P. 2008 75,000,000 60,223,958 16,993,215 77,217,173

Lone Star Real Estate Fund (U.S.), L.P. 2008 25,000,000 13,157,329 12,232,642 25,389,971

PLA Residential Fund III, L.P. 2008 50,000,000 35,217,848 16,321,243 51,539,091

PLA Retail Fund I, LP 2006 60,000,000 52,276,343 0 52,276,343

RREEF Global Opportunities Fund II, LLC 2005 50,000,000 29,893,314 0 29,893,314

Tishman Speyer Real Estate Venture VI, L.P. 2004 24,685,050 7,625,941 4,427,570 12,053,511

Tishman Speyer Real Estate Venture VII, L.P. 2007 50,000,000 2,676,468 24,144,722 26,821,190

Westbrook Real Estate Fund VII, L.P. 2006 44,000,000 20,709,430 11,333,335 32,042,765

Westbrook Real Estate Fund VIII, L.P. 2008 50,000,000 0 50,000,000 50,000,000

Total High Return 998,685,050 393,653,340 441,663,846 835,317,186 62%

Total Non-Core (Enhanced Return + High Return) 1,259,885,050 462,704,055 571,698,754 1,034,402,809 77% Max 80%

Total ASRS Portfolio 1,662,297,921 613,890,065 736,201,157 1,350,091,222 100%

1. Represents Reported Value as of 6/30/2009 plus Capital Calls minus Capital Distributions through 10/31/2009.

2. Calculated as Adjusted Value plus Adjusted Remaining Commitment.

ASRS Valuation Rollforward Report as of October 31, 2009 (cont'd)

10

ASRS Real Estate Program – Vintage Exposure (IRR1)

The Average Projected IRR represents the average targeted return promised by investment managers in

their respective vintage year. The Average Actual Gross ASRS IRR represents the average gross IRR of

investments to date relative to the displayed vintage year based on actual cash flows. Total commitments to

the enhanced space represent $261 million since inception.

As of June 30th, 2009 the market value of all enhanced investments represents 26.4% of total commitments

made to enhanced strategies and 49.7% of total capital committed remains for future investments.

Vintage

ASRS

Exposure (#

of Funds)

2006 2

2007 2

2008 1

13.5% 13.5% 14.0%

-41.1%-44.2%

-30.5%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

2006 2007 2008

IRR

Enhanced Investment Performance by Vintage Year

Average Targeted Gross IRR Average Actual Gross ASRS IRR

1Internal Rate of Return.

*Measures the promised average IRR relative to current average IRR with in place cash flow. Current performance is not indicative of fund

level performance at maturity.

11

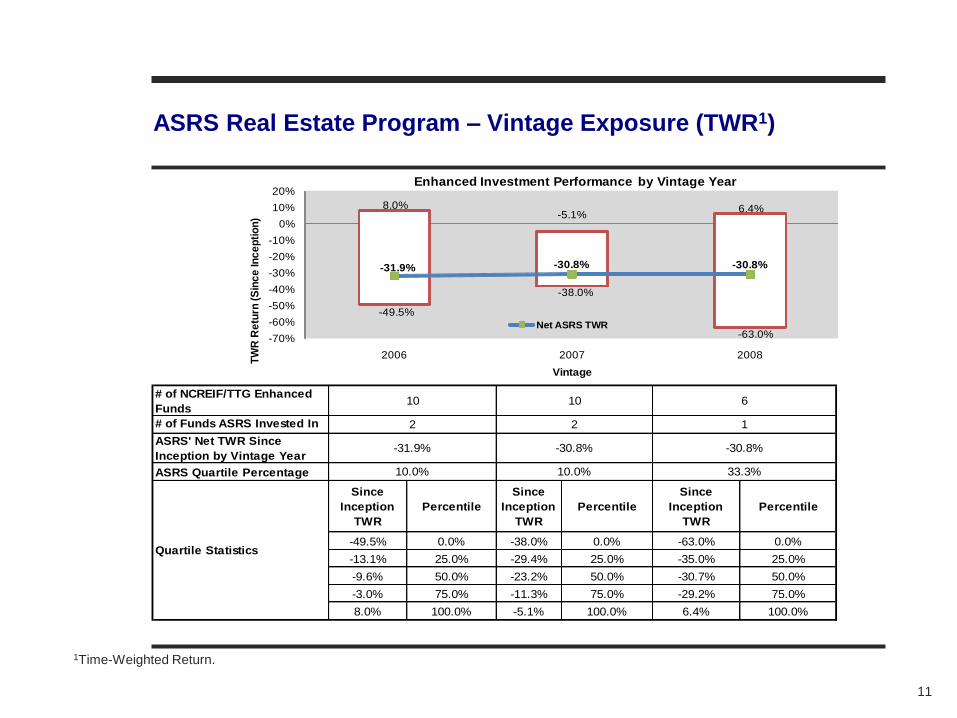

ASRS Real Estate Program – Vintage Exposure (TWR1)

1Time-Weighted Return.

# of NCREIF/TTG Enhanced

Funds

# of Funds ASRS Invested In

ASRS' Net TWR Since

Inception by Vintage Year

ASRS Quartile Percentage

Since

Inception

TWR

Percentile

Since

Inception

TWR

Percentile

Since

Inception

TWR

Percentile

-49.5% 0.0% -38.0% 0.0% -63.0% 0.0%

-13.1% 25.0% -29.4% 25.0% -35.0% 25.0%

-9.6% 50.0% -23.2% 50.0% -30.7% 50.0%

-3.0% 75.0% -11.3% 75.0% -29.2% 75.0%

8.0% 100.0% -5.1% 100.0% 6.4% 100.0%

Quartile Statistics

-30.8%

10.0%

6

1

-30.8%

33.3%

10

2

-31.9%

10

2

10.0%

8.0%-5.1%

6.4%

-49.5%

-38.0%

-63.0%

-31.9% -30.8% -30.8%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

2006 2007 2008

TW

R R

etu

rn (

Sin

ce

In

ce

pti

on

)

Vintage

Enhanced Investment Performance by Vintage Year

Net ASRS TWR

12

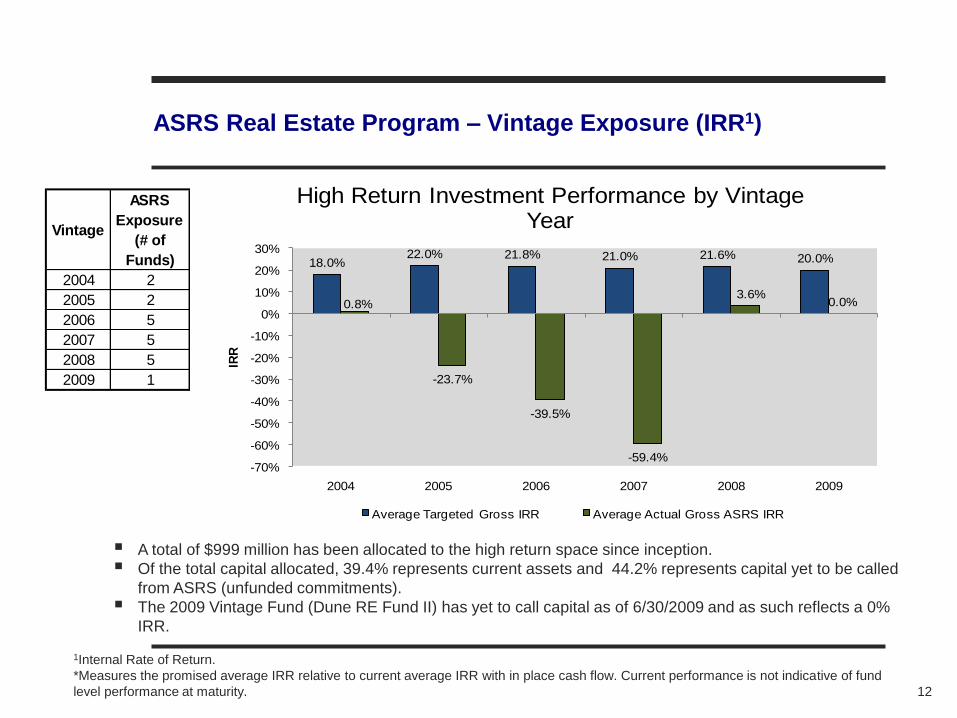

ASRS Real Estate Program – Vintage Exposure (IRR1)

A total of $999 million has been allocated to the high return space since inception.

Of the total capital allocated, 39.4% represents current assets and 44.2% represents capital yet to be called

from ASRS (unfunded commitments).

The 2009 Vintage Fund (Dune RE Fund II) has yet to call capital as of 6/30/2009 and as such reflects a 0%

IRR.

Vintage

ASRS

Exposure

(# of

Funds)

2004 2

2005 2

2006 5

2007 5

2008 5

2009 1

18.0%22.0% 21.8% 21.0% 21.6% 20.0%

0.8%

-23.7%

-39.5%

-59.4%

3.6%0.0%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2004 2005 2006 2007 2008 2009

IRR

High Return Investment Performance by Vintage Year

Average Targeted Gross IRR Average Actual Gross ASRS IRR

1Internal Rate of Return.

*Measures the promised average IRR relative to current average IRR with in place cash flow. Current performance is not indicative of fund

level performance at maturity.

13

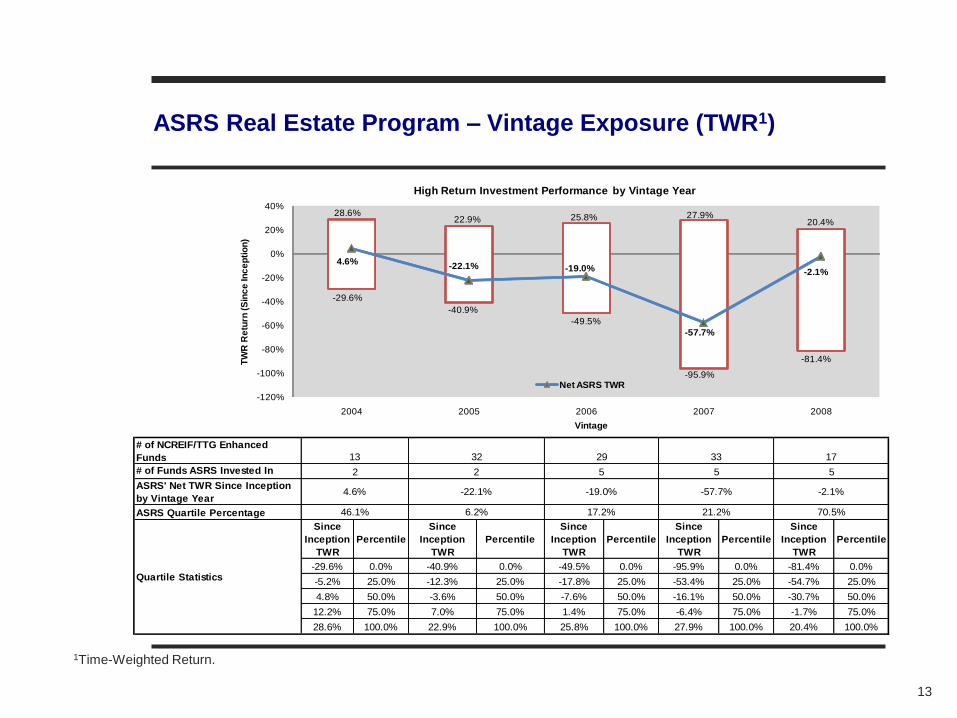

ASRS Real Estate Program – Vintage Exposure (TWR1)

1Time-Weighted Return.

# of NCREIF/TTG Enhanced

Funds

# of Funds ASRS Invested In

ASRS' Net TWR Since Inception

by Vintage Year

ASRS Quartile Percentage

Since

Inception

TWR

Percentile

Since

Inception

TWR

Percentile

Since

Inception

TWR

Percentile

Since

Inception

TWR

Percentile

Since

Inception

TWR

Percentile

-29.6% 0.0% -40.9% 0.0% -49.5% 0.0% -95.9% 0.0% -81.4% 0.0%

-5.2% 25.0% -12.3% 25.0% -17.8% 25.0% -53.4% 25.0% -54.7% 25.0%

4.8% 50.0% -3.6% 50.0% -7.6% 50.0% -16.1% 50.0% -30.7% 50.0%

12.2% 75.0% 7.0% 75.0% 1.4% 75.0% -6.4% 75.0% -1.7% 75.0%

28.6% 100.0% 22.9% 100.0% 25.8% 100.0% 27.9% 100.0% 20.4% 100.0%

5

-22.1%

21.2% 70.5%

29

5

-19.0%

17.2%

33 17

5

6.2%

-57.7% -2.1%

Quartile Statistics

13

2

46.1%

4.6%

32

2

-29.6%

-40.9%

-49.5%

-95.9%

-81.4%

28.6%22.9% 25.8% 27.9%

20.4%

4.6%-22.1% -19.0%

-57.7%

-2.1%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

2004 2005 2006 2007 2008

TW

R R

etu

rn (

Sin

ce

In

ce

pti

on

)

Vintage

High Return Investment Performance by Vintage Year

Net ASRS TWR

■ Evaluate Current Market Environment

― Broad based diversification (sectors, styles, location, life cycle) did not protect against the market collapse.

― All portfolio‟s with existing exposure to real estate were impacted.

― Expect “workout” to consume efforts in 2009, 2010 and into 2011.

■ Assess Risk and Exposure

― Identify debt maturities, mark-to-market progress and covenants.

― Expose and monitor assets at risk or those with permanent impairment.

― Identify available equity; whether through unfunded commitments, reserves, future cash flow or other sources.

― Minimize capital loss and stop „good money-after-bad‟ capital requests.

― Consider organizational stability and retention within the General Partnership.

■ Manage Future Portfolio

― Position portfolio to take advantage of inevitable recovery.

― Diversify away from “bad vintages.”

■ Five quarters of „reset‟ has exceeded 30% expected core equity declines

― Not all of NPI index has been revalued

― Write-downs in 2010 will reflect fundamental declines

■ ASRS - One Year Performance Ending June 30, 2009

― Levered Time Weighted Return of -33.3%

― Unlevered Time Weighted Return of -9.9%, assuming current Portfolio leverage of 58% and a 7% WACC.

14

ASRS Portfolio Risk Assessment

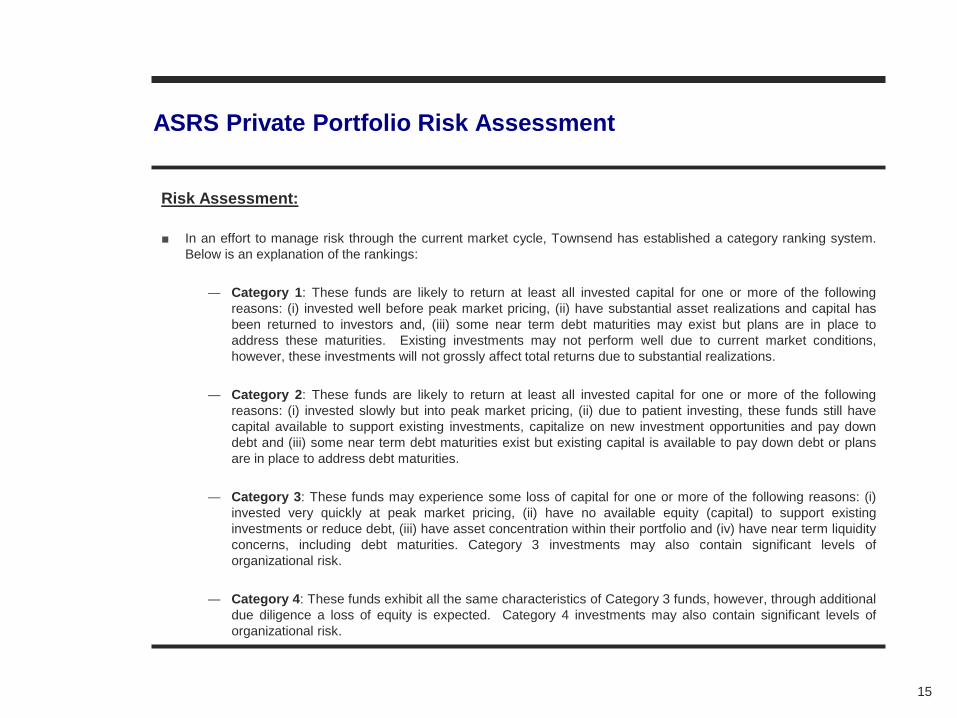

Risk Assessment:

■ In an effort to manage risk through the current market cycle, Townsend has established a category ranking system.

Below is an explanation of the rankings:

― Category 1: These funds are likely to return at least all invested capital for one or more of the following

reasons: (i) invested well before peak market pricing, (ii) have substantial asset realizations and capital has

been returned to investors and, (iii) some near term debt maturities may exist but plans are in place to

address these maturities. Existing investments may not perform well due to current market conditions,

however, these investments will not grossly affect total returns due to substantial realizations.

― Category 2: These funds are likely to return at least all invested capital for one or more of the following

reasons: (i) invested slowly but into peak market pricing, (ii) due to patient investing, these funds still have

capital available to support existing investments, capitalize on new investment opportunities and pay down

debt and (iii) some near term debt maturities exist but existing capital is available to pay down debt or plans

are in place to address debt maturities.

― Category 3: These funds may experience some loss of capital for one or more of the following reasons: (i)

invested very quickly at peak market pricing, (ii) have no available equity (capital) to support existing

investments or reduce debt, (iii) have asset concentration within their portfolio and (iv) have near term liquidity

concerns, including debt maturities. Category 3 investments may also contain significant levels of

organizational risk.

― Category 4: These funds exhibit all the same characteristics of Category 3 funds, however, through additional

due diligence a loss of equity is expected. Category 4 investments may also contain significant levels of

organizational risk.

15

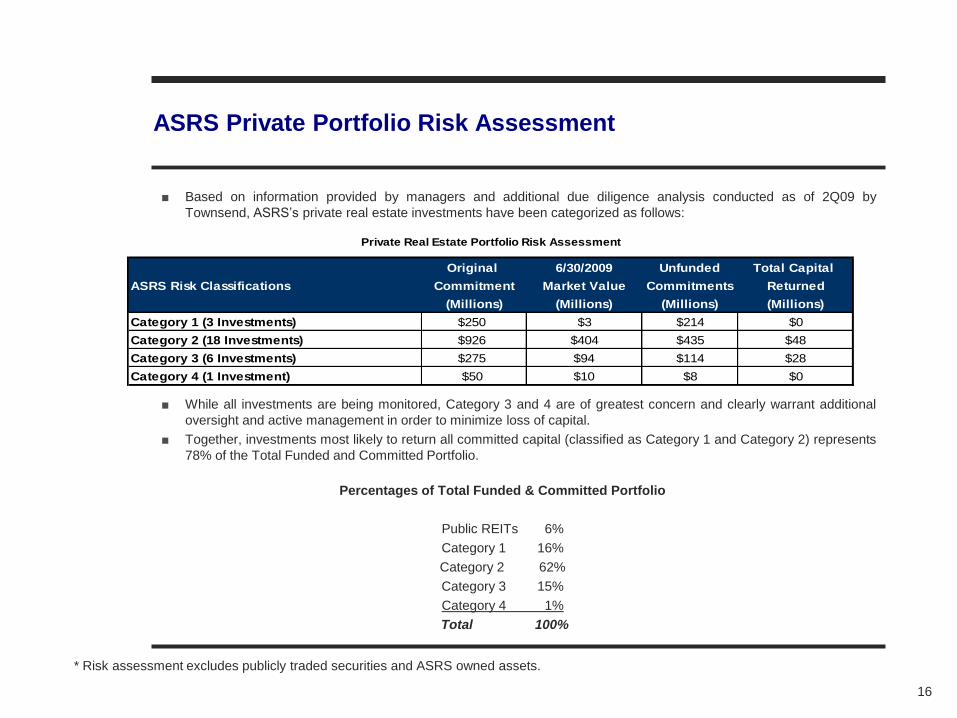

ASRS Private Portfolio Risk Assessment

■ Based on information provided by managers and additional due diligence analysis conducted as of 2Q09 by

Townsend, ASRS‟s private real estate investments have been categorized as follows:

■ While all investments are being monitored, Category 3 and 4 are of greatest concern and clearly warrant additional

oversight and active management in order to minimize loss of capital.

■ Together, investments most likely to return all committed capital (classified as Category 1 and Category 2) represents

78% of the Total Funded and Committed Portfolio.

16

ASRS Private Portfolio Risk Assessment

Percentages of Total Funded & Committed Portfolio

Public REITs 6%

Category 1 16%

Category 2 62%

Category 3 15%

Category 4 1%

Total 100%

* Risk assessment excludes publicly traded securities and ASRS owned assets.

Original 6/30/2009 Unfunded Total Capital

ASRS Risk Classifications Commitment Market Value Commitments Returned

(Millions) (Millions) (Millions) (Millions)

Category 1 (3 Investments) $250 $3 $214 $0

Category 2 (18 Investments) $926 $404 $435 $48

Category 3 (6 Investments) $275 $94 $114 $28

Category 4 (1 Investment) $50 $10 $8 $0

Private Real Estate Portfolio Risk Assessment

View of the World

Global Real Estate Investment Opportunities

The Townsend Group

Overview of Global Real Estate Markets

■ Two primary forces shape the world‟s real estate markets:

― The credit crisis

― Questionable economic growth

■ Other forces, such as undersupply in emerging markets, continue to influence

long-term strategic planning but are not central to constructing a global real

estate portfolio today.

18

(8.0)

(6.0)

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gross Domestic Product, Real Annual Growth Rate

World

G7

Transition Economies

Source: Thomson Reuters, Economist Intelligence Unit

The Townsend Group

75% D

ebt

55% D

ebt

Funding Gap

Equity

0

20

40

60

80

100

Initial '07 Capital Stack '09 Capital Stack

Depleted Equity Margins

20% GAV

Reduction

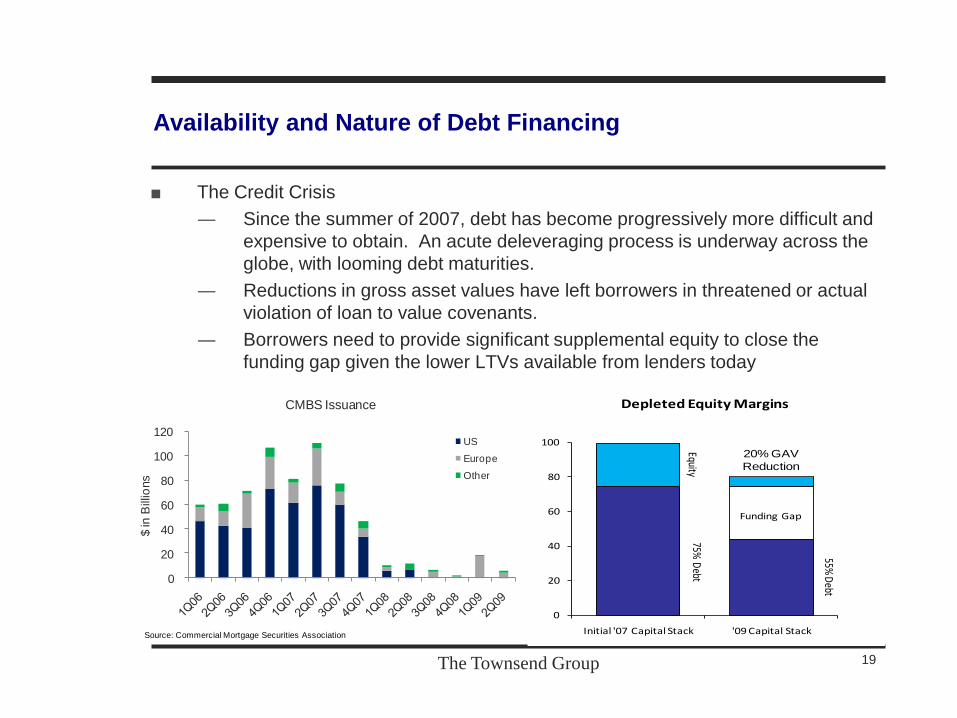

Availability and Nature of Debt Financing

■ The Credit Crisis

― Since the summer of 2007, debt has become progressively more difficult and

expensive to obtain. An acute deleveraging process is underway across the

globe, with looming debt maturities.

― Reductions in gross asset values have left borrowers in threatened or actual

violation of loan to value covenants.

― Borrowers need to provide significant supplemental equity to close the

funding gap given the lower LTVs available from lenders today

19

0

20

40

60

80

100

120

$ in

Bill

ions

CMBS Issuance

US

Europe

Other

Source: Commercial Mortgage Securities Association

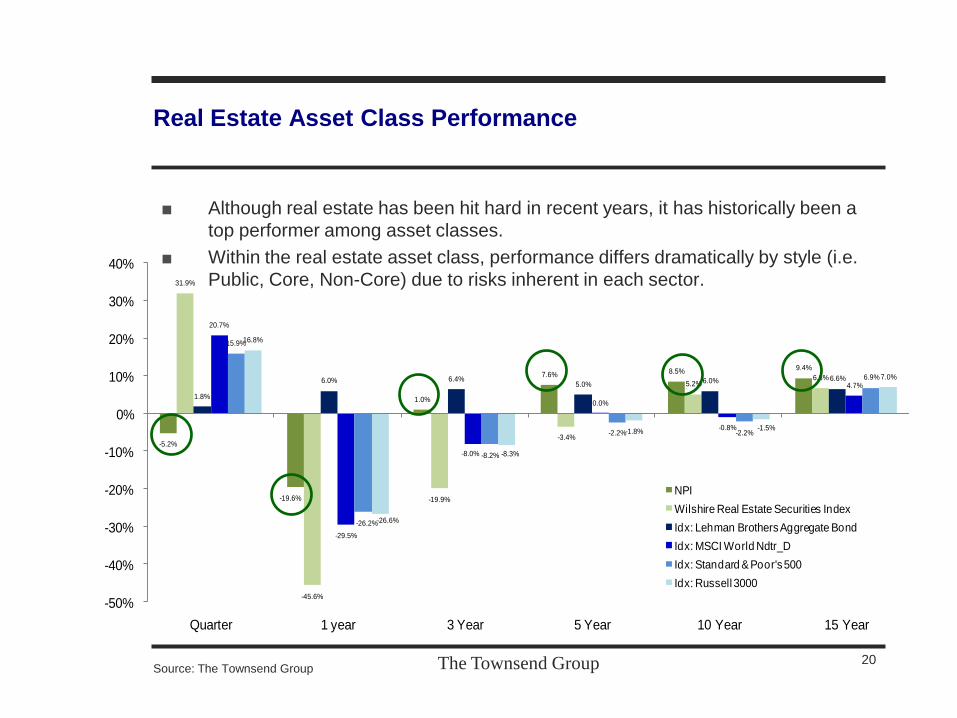

The Townsend Group

-5.2%

-19.6%

1.0%

7.6% 8.5% 9.4%

31.9%

-45.6%

-19.9%

-3.4%

5.2%6.8%

1.8%

6.0% 6.4%5.0%

6.0% 6.6%

20.7%

-29.5%

-8.0%

0.0%

-0.8%

4.7%

15.9%

-26.2%

-8.2%

-2.2% -2.2%

6.9%

16.8%

-26.6%

-8.3%

-1.8%-1.5%

7.0%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Quarter 1 year 3 Year 5 Year 10 Year 15 Year

NPI

Wilshire Real Estate Securities Index

Idx: Lehman Brothers Aggregate Bond

Idx: MSCI World Ndtr_D

Idx: Standard & Poor's 500

Idx: Russell 3000

Real Estate Asset Class Performance

■ Although real estate has been hit hard in recent years, it has historically been a

top performer among asset classes.

■ Within the real estate asset class, performance differs dramatically by style (i.e.

Public, Core, Non-Core) due to risks inherent in each sector.

20Source: The Townsend Group

The Townsend Group

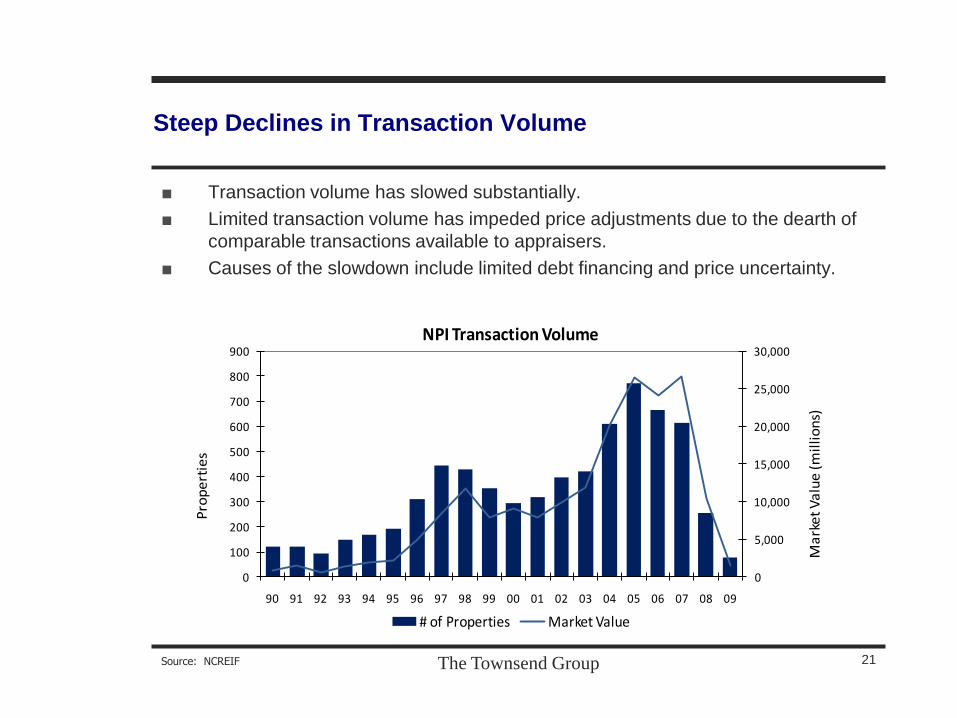

Steep Declines in Transaction Volume

■ Transaction volume has slowed substantially.

■ Limited transaction volume has impeded price adjustments due to the dearth of

comparable transactions available to appraisers.

■ Causes of the slowdown include limited debt financing and price uncertainty.

21Source: NCREIF

0

5,000

10,000

15,000

20,000

25,000

30,000

0

100

200

300

400

500

600

700

800

900

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Ma

rke

t V

alu

e (

mil

lio

ns)

Pro

pe

rtie

s

NPI Transaction Volume

# of Properties Market Value

The Townsend Group

Real Estate Performance

Current Downturn vs. Previous Downturn

■ Although relatively few transactions have occurred, values have adjusted at a

historic rate.

■ Use of high levels of leverage greatly accelerated the pace of write downs.

22

55

60

65

70

75

80

85

90

95

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

Cap

ital V

alu

e f

rom

Peak

Quarters f rom Peak

Peak to Trough Capital Return for US ODCE IndexPrevious Major Correction vs. Current through 3rd Qtr Prelim

1990-1994 Correction

Current Correction

Source: The Townsend Group

The Townsend Group

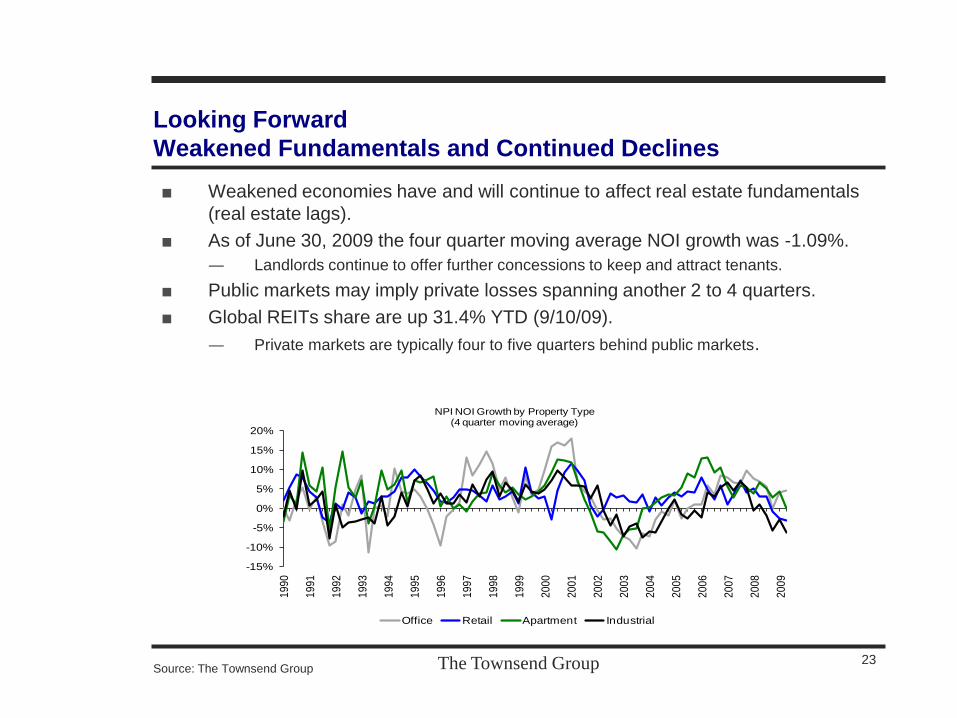

Looking Forward

Weakened Fundamentals and Continued Declines

■ Weakened economies have and will continue to affect real estate fundamentals

(real estate lags).

■ As of June 30, 2009 the four quarter moving average NOI growth was -1.09%.

― Landlords continue to offer further concessions to keep and attract tenants.

■ Public markets may imply private losses spanning another 2 to 4 quarters.

■ Global REITs share are up 31.4% YTD (9/10/09).

― Private markets are typically four to five quarters behind public markets.

23

-15%

-10%

-5%

0%

5%

10%

15%

20%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

NPI NOI Growth by Property Type(4 quarter moving average)

Office Retail Apartment Industrial

Source: The Townsend Group

The Townsend Group

Looking Forward

Overall Global Themes and Future Opportunities

■ US and Japan offer sharply discounted pricing, with looming debt maturities, as rents continue to roll down. Need to watch for deflation in Japan; a jobless recovery in the US. Little transaction volume to date.

■ Be prepared to capitalize on distress in the market. ASRS‟ capital projections indicate that future capital is available for new commitments to real estate in 2010.

■ Expect U.K to be first economy in Eurozone to return to growth; rents will continue to fall; sharp correction in property values coupled with weak currency is attracting foreign investors.

■ Fewer opportunities in France and Germany until 2011-2014 when assets need restructuring, debt maturities require recapitalization.

■ China and Singapore offer comparatively outsized growth; need to avoid inflation and bubble pricing; Residential leads recovery; Logistics lags.

■ Latin American offers growth, stability and relatively low unemployment. Development is key, with consequent risk of oversupply.

24

The Townsend Group

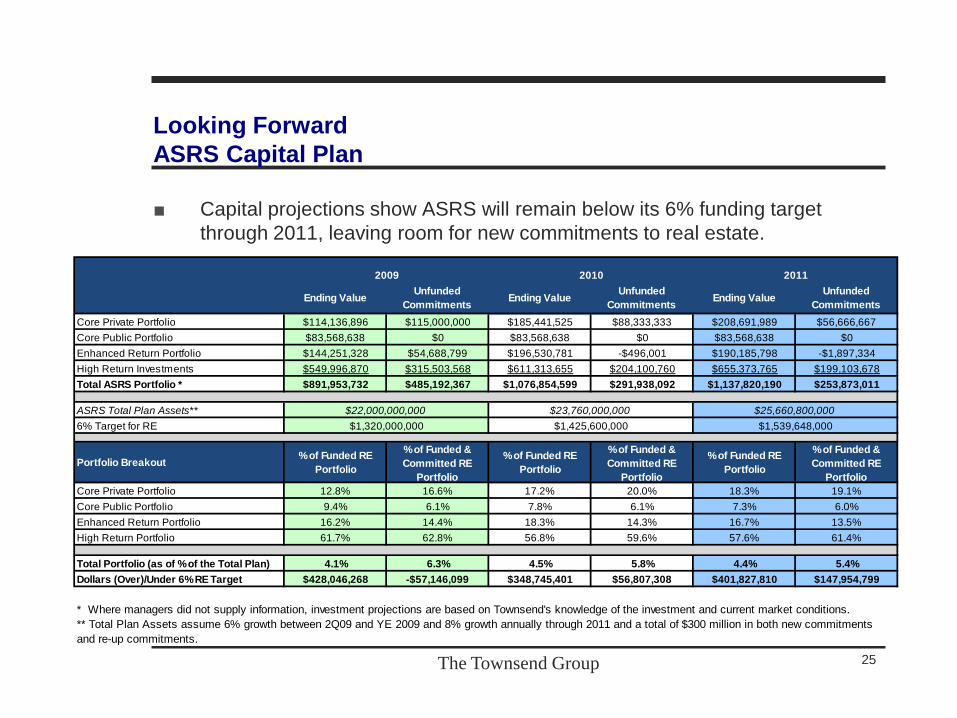

Looking Forward

ASRS Capital Plan

■ Capital projections show ASRS will remain below its 6% funding target

through 2011, leaving room for new commitments to real estate.

25

Ending ValueUnfunded

CommitmentsEnding Value

Unfunded

CommitmentsEnding Value

Unfunded

Commitments

Core Private Portfolio $114,136,896 $115,000,000 $185,441,525 $88,333,333 $208,691,989 $56,666,667

Core Public Portfolio $83,568,638 $0 $83,568,638 $0 $83,568,638 $0

Enhanced Return Portfolio $144,251,328 $54,688,799 $196,530,781 -$496,001 $190,185,798 -$1,897,334

High Return Investments $549,996,870 $315,503,568 $611,313,655 $204,100,760 $655,373,765 $199,103,678

Total ASRS Portfolio * $891,953,732 $485,192,367 $1,076,854,599 $291,938,092 $1,137,820,190 $253,873,011

ASRS Total Plan Assets**

6% Target for RE

Portfolio Breakout% of Funded RE

Portfolio

% of Funded &

Committed RE

Portfolio

% of Funded RE

Portfolio

% of Funded &

Committed RE

Portfolio

% of Funded RE

Portfolio

% of Funded &

Committed RE

Portfolio

Core Private Portfolio 12.8% 16.6% 17.2% 20.0% 18.3% 19.1%

Core Public Portfolio 9.4% 6.1% 7.8% 6.1% 7.3% 6.0%

Enhanced Return Portfolio 16.2% 14.4% 18.3% 14.3% 16.7% 13.5%

High Return Portfolio 61.7% 62.8% 56.8% 59.6% 57.6% 61.4%

Total Portfolio (as of % of the Total Plan) 4.1% 6.3% 4.5% 5.8% 4.4% 5.4%

Dollars (Over)/Under 6% RE Target $428,046,268 -$57,146,099 $348,745,401 $56,807,308 $401,827,810 $147,954,799

* Where managers did not supply information, investment projections are based on Townsend's knowledge of the investment and current market conditions.

** Total Plan Assets assume 6% growth between 2Q09 and YE 2009 and 8% growth annually through 2011 and a total of $300 million in both new commitments

and re-up commitments.

$22,000,000,000

$1,320,000,000

$23,760,000,000

$1,425,600,000

$25,660,800,000

$1,539,648,000

2010 20112009