19.04.2013 investment in stocks and equities in mongolia risks, challenges and trends, d. gan-ochir

TRANSCRIPT

INVESTMENTS IN EQUITIES AND STOCKS

MARKET: RISKS, CHALLENGES, SUBSEQUENT TRENDS

D.Gan-‐Ochir

Any conclusions, opinions mentioned in this report express only the position of researcher and will not banded as Mongol Bank position.

“Foreign investments – Risks and challenges: Methods of solution” meeting

Scope • D.Gan-‐Ochir 2006, ‘Influence of monetary policy to capital market’ research work, ECONOMY: Theory and practice journal, 2006-12.

• D.Gan-‐Ochir, B.Lkhagvajav and D.Batnyam 2008, ‘Monetary Policy and Bond Market: A Case of Mongolia ’research work <http://www.unescap.org/pdd/projects/bondmkt/12_Mongolia_monetary_policy_bond.pdf>.

D.Gan-‐Ochir 2008, ‘Mongolian capital market model (MSMM): Influence of World financial crisis to economy, capital market’ research work <http://www.eri.mn/index.php/en/l?task=view&catid=49&id=21>

• D.Gan-Ochir 2009, ‘Capital flows and their implications for central bank policies in Mongolia’ research work <http://seacen.org/gui/pdf/publications/research_proj/2009/rp76/6-chap5.pdf>.

• D.Gan-Ochir, G.Borkhuu & D.Tsenddorj2012, ‘Financial Contagion and Volatile Capital Flows’ research work <http://www.eri.mn/index.php/en/l?task=view&catid=49&id=732>.

Plan

⋅ Capital flow in financial system

⋅ Theory trends: Proven documents

⋅ Equities and stock market

⋅ Current situation ⋅ Risks, challenges ⋅ Subsequent trends

⋅ Issues to be considered at equities and stock market development

Financial system: Capital flow

Source: Mishkin, FS & Eakins, SG, Financial Markets and Institutions, 7th edition, Pearson Education, Inc., Boston.

NON-‐DIRECT FINANCING: 60-‐80%

CAPITAL CAPITAL

CAPITAL

CAPITAL CAPITAL

Financial market:

⋅ Bond market ⋅ Capital market

DIRECT FINANCING: 20-‐40%

Creditor – Savers

1. Families 2. Business

companies 3. Government 4. Foreign citizens,

organizations

Borrower – Users

1. Business companies 2. Government 3. Families 4. Foreign citizens,

organizations

Financial intermediaries: ⋅ Bank ⋅ Insurance ⋅ Pension fund

Factors impeding proper development and work of market:

⋅ Information costs ⋅ Transaction costs

Obligations of financial system:

⋅ Savings transfer ⋅ Effective placement of recourses

⋅ Establishing of company control

⋅ Improvement of risk management

⋅ Easing product, service trade Channel for economic

growth:

⋅ Capital accumulation ⋅ Technology modernization

Financial systems proven documents

Source: Mishkin, FS, The Economics of Money, Banking and Financial Markets, 10th edition, Pearson Education, Inc., New Jersey.

Bank loan Nonbanking financial institutions loans

Bond Equities

USA

Germany

Japan

Canada

Equities and stocks are not main source of business financing

⋅ Transaction costs:(1) Expansion effectiveness (2) Professionalism (computer technology)

⋅ Asymmetrical information:(1) Bad choice (Lemon’s issue) (2) Ethics deformation (another’s money)

Financial intermediaries, especially banks are essential source of financing business activities

Only major companies are able to raise financing from equities market

Financial system is most regulated sector of economy

⋅ Increase of information ⋅ Improvement of correct and transparent conditions

⋅ Improvement of monitoring

CURRENT SITUATION IN EQUITIES AND STOCK MARKET

Equities and stocks market development (1)

Source: Mongol bank’s monthly statistical bulletin

3,3% 3,0% 2,3% 2,7% 1,3% 1,8% 3,3%

14,5%

7,9% 9,4%

16,3%19,6%

12,9%

5,5%9,7%

14,9%

24,2% 25,7%28,3%

30,4%

41,5% 40,2% 40,3% 38,8%

49,1% 50,1%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Хөрөнгийн зах зээлийн үнэлгээ, нэрлэсэн ДНБ-ий харьцаа

Банкны салбарын нийт зээл, нэрлэсэн ДНБ-ий харьцаа

0,0

500,0

1000,0

1500,0

2000,0

2500,0

3000,0

2005

01 05 09

2006

01 05 09

2007

01 05 09

2008

01 05 09

2009

01 05 09

2010

01 05 09

2011

01 05 09

2012

01 05 09

Хөрөнгийн зах зээлийн нийт үнэлгээ, сая ам.доллараар

0

2 000

4 000

6 000

8 000

10 000

12 000

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

2005

01 05 09

2006

01 05 09

2007

01 05 09

2008

01 05 09

2009

01 05 09

2010

01 05 09

2011

01 05 09

2012

01 05 09Топ-20 (max)-Топ-20 (Min), баруун тэнхлэг

Топ-20 индекс (Хамгийн их утга)

Топ-20 индекс (хамгийн бага утга)

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

0

20 000

40 000

60 000

80 000

100 000

120 000

2007

01 04 07 10

2008

01 04 07 10

2009

01 04 07 10

2010

01 04 07 10

2011

01 04 07 10

2012

01 04 07 10

Нийт гүйлгээний дүн, сая төгрөг

Засгий газрын бонд, сая төгрөг

Компанийн бонд, сая төгрөг

Хувьцаа, сая төгрөг

Sri Lanka: 40% Indonesia: 50% Mongolia: 12.9%

Cycle related capital market

Capital market value, declared GNP ratio

Total loans of banking sector, declared GNP ratio

Capital market value, million US$ Top-‐20 (max) – Top-‐20 (min), right axis Top-‐20 index (Maximal value) Top-‐20 index (Minimal value)

Total transactions sum, million tugrik’s Government bonds, million tugrik’s Company bonds, million tugrik’s Stocks, million tugrik’s

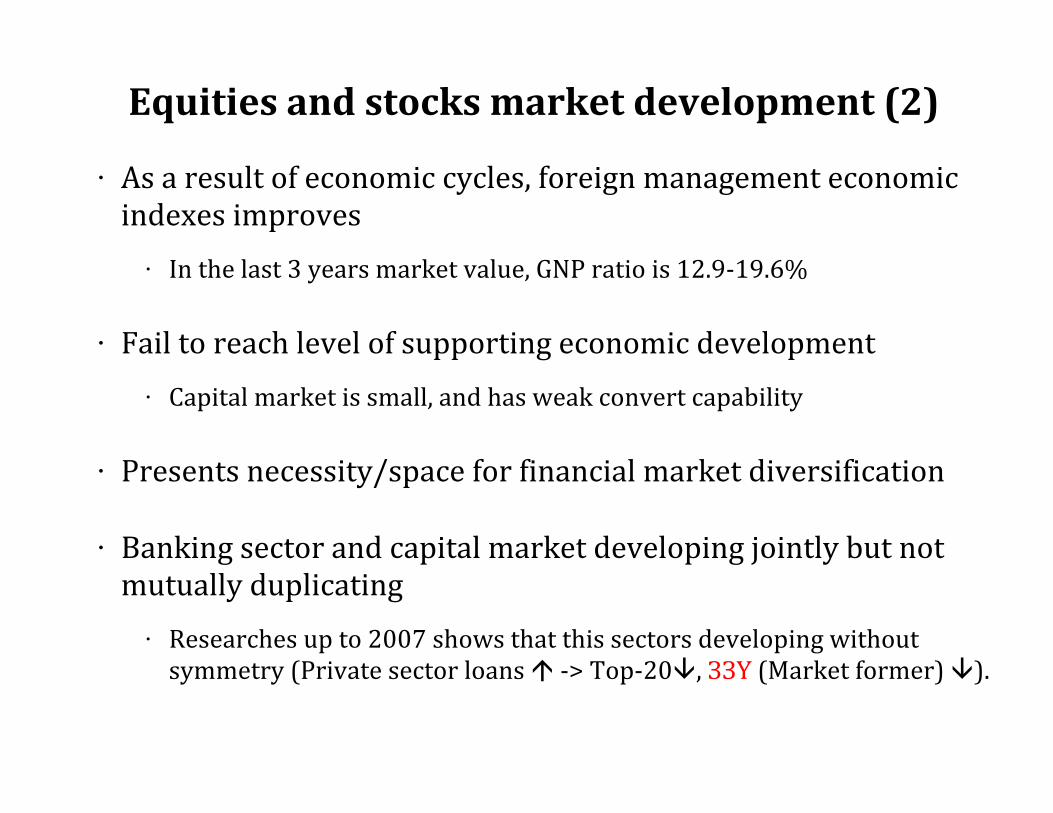

Equities and stocks market development (2)

⋅ As a result of economic cycles, foreign management economic indexes improves

⋅ In the last 3 years market value, GNP ratio is 12.9-‐19.6%

⋅ Fail to reach level of supporting economic development

⋅ Capital market is small, and has weak convert capability

⋅ Presents necessity/space for financial market diversification

⋅ Banking sector and capital market developing jointly but not mutually duplicating

⋅ Researches up to 2007 shows that this sectors developing without symmetry (Private sector loans á -‐> Top-‐20â, ЗЗҮ (Market former) â).

EQUITIES AND STOCK MARKETS RISKS AND CHALLENGES

Foreign sector conditions is weak

-0.1

0.1

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Худалдааны нөхцөл (баруун тэнхлэг)

Экспортын үнийн индекс

Импортын үнийн индекс

1123

-225-377

-1500

-1000

-500

0

500

1000

1500

2000

2500

I '09

II '0

9

III '

09

IV '0

9

I '10

II '1

0

III '

10

IV '1

0

I '11

II '1

1

III '

11

IV '1

1

I '12

II '1

2

III '

12

IV '1

2

Хөрөнгө ба санхүүгийн тэнцэл

Урсгал тэнцэл

Нийт тэнцэл

838 570

1 630

4 6203 835

0

1 000

2 000

3 000

4 000

5 000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Foreign direct investments decreased by 17% (785 million US$)

2009:01 1.315

2013:02 1.432

Foreign trade conditions worsened by

12.5%

Current account deficit was defrayed

by capital and financial balance

profits

Trade conditions (right axis)

Export price index

Import price index

Capital and finance equality

Flow equality

Total equality

Current conditions of macroeconomics (As of February 2013)

• Export lowering -‐ 4.5%

• Import lowering -‐ 13.6%

• Frogeign trade conditions lowering -‐ 12.5%

• Foreign-‐trade deoicit -‐305.2 million $

• М2 money growth-‐ 16.1%

• Increasment of remainder of the debts -‐ 21.6%

• Inolation rate in Ulaanbaatar -‐ 11.1%

• Inolation rate in state -‐ 11.3%

• Currency rate weakening -‐ 4.6%

• Actual GNP growth -‐ 12.3%

• Agricultural sector growth -‐ 21.3%

• Mining sector growth -‐ 8.9%

• Others -‐ 11.3% Economic growth

Inolation, currency

exchange rate

Foreign trade Money, loan increasement

Economy sensitivity assessment: end of the 2012

Foreign sector

Budget Money&curre

ncy rate

Finance Society

⋅ Raw material export/Total export: 90.8%

⋅ Export/GNP: 43.9% ⋅ ГВЦАН/Import: 20 долоо хоног

⋅ Trade balance/GNP: 23.6%

⋅ Budget balance/GNP:6.7% ⋅ Government dept’s/GNP:

49.6% ⋅ Financial source

necessity/GNP: 7.6% ⋅ Essential expenses/Total

costs:75% ⋅ Raw materials income/Total

income: 32.9%

⋅ Inflation: 14.0% ⋅ Actual interests: -0.75% ⋅ Forex resources/GNP:

40.9% ⋅ Currency rate

flexibility: Relatively weak

⋅ Percentage of foreign currency dept’s in total dept’s: 19.2%

⋅ Equity capital, total assets ratio: 8.2%

⋅ Low grade loan, total loan ratio: 4.2%

⋅ Loan, deposit ratio: 99.7% ⋅ Loan, GNP ratio increase:

2.2%

⋅ Poverty sensitivity: 2.7

⋅ Unemployment rate: 7.7%

⋅ Number of indigents with daily income less than $1.25/total population: 29.8%

⋅ Jeni index: 0.44

Economy sensitivity

Economy sensitivity to foreign shocks is high.

Financial sector sensitivity is average.

Social sector sensitivity is average.

Money, currency rate sensitivity is average-> high.

Budget sensitivity is high.

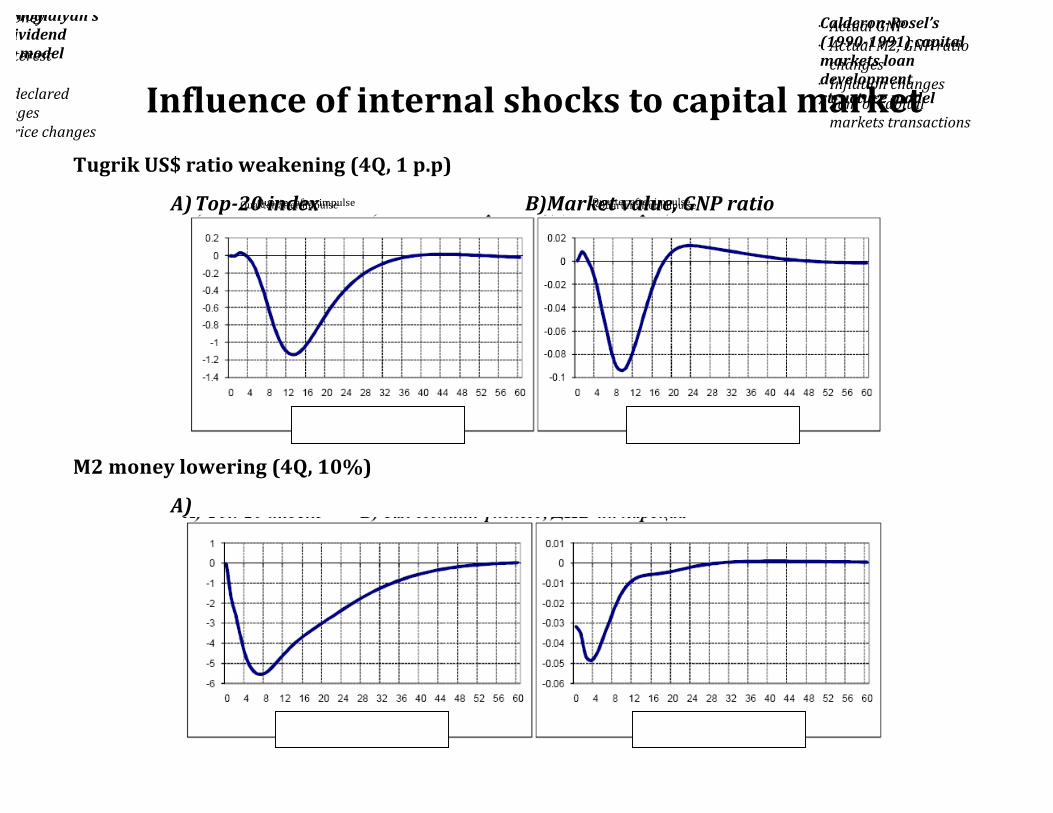

Influence of internal shocks to capital market Tugrik US$ ratio weakening (4Q, 1 p.p)

A) Top-‐20 index B)Market value, GNP ratio

М2 money lowering (4Q, 10%)

A)

Calderon-‐Rosel’s (1990-‐1991) capital markets loan development structure model

Miller & Mogidlyan’s (1961) dividend deflation model

⋅ Actual money changes

⋅ Actual interest changes

⋅ Tugrik’s declared rate changes

⋅ Copper price changes

⋅ Actual GNP ⋅ Actual М2, GNP ratio changes

⋅ Inflation changes ⋅ Sum of capital markets transactions

Quarter after impulse Quarter after impulse Quarter after impulse Quarter after impulse

Influence of foreign shocks to capital market

Deceleration of Chinese growth (4Q, 1 p.p)

Copper price lowering (4Q, 10%)

⋅ Actual money changes

⋅ Actual interest changes

⋅ Tugrik’s declared rate changes

⋅ Copper price changes

⋅ Actual GNP ⋅ Actual М2, GNP ratio changes

⋅ Inflation changes ⋅ Sum of capital markets transactions

Quarter after impulse Quarter after impulse Quarter after impulse Quarter after impulse

A)Top-‐20 index B) Market value, GNP ratio A)Top-‐20 index B) Market value, GNP ratio

Economic growth, inflation guiding indexes

2008-‐09 оны хямралын үе

Э/З-‐ийн өрнөлийн үе

???

2008-‐09 оны хямралын үе

Э/З-‐ийн өрнөлийн үе

??? 2008-‐09 оны хямралын үе

Э/З-‐ийн өрнөлийн үе

??? ⋅ In economic growth with 5-‐6 quarters delay

⋅ In annual inflation with 2 quarters delay

⋅ In annual inflation with 2 quarter delay

⋅ In economic growth with 1-‐5 quarter delay

⋅ In annual inflation with 2-‐3 quarter delay

Foreign sector sensitivity index Finance sensitivity index

General sensitivity index 1 General sensitivity index 5

2008-‐2009 crisis period

2008-‐2009 crisis period

2008-‐2009 crisis period

Economy growth period

Economy growth period

Economy growth period

SUBSEQUENT TRENDS AND CHALLENGES OF EQUITIES AND STOCK MARKET

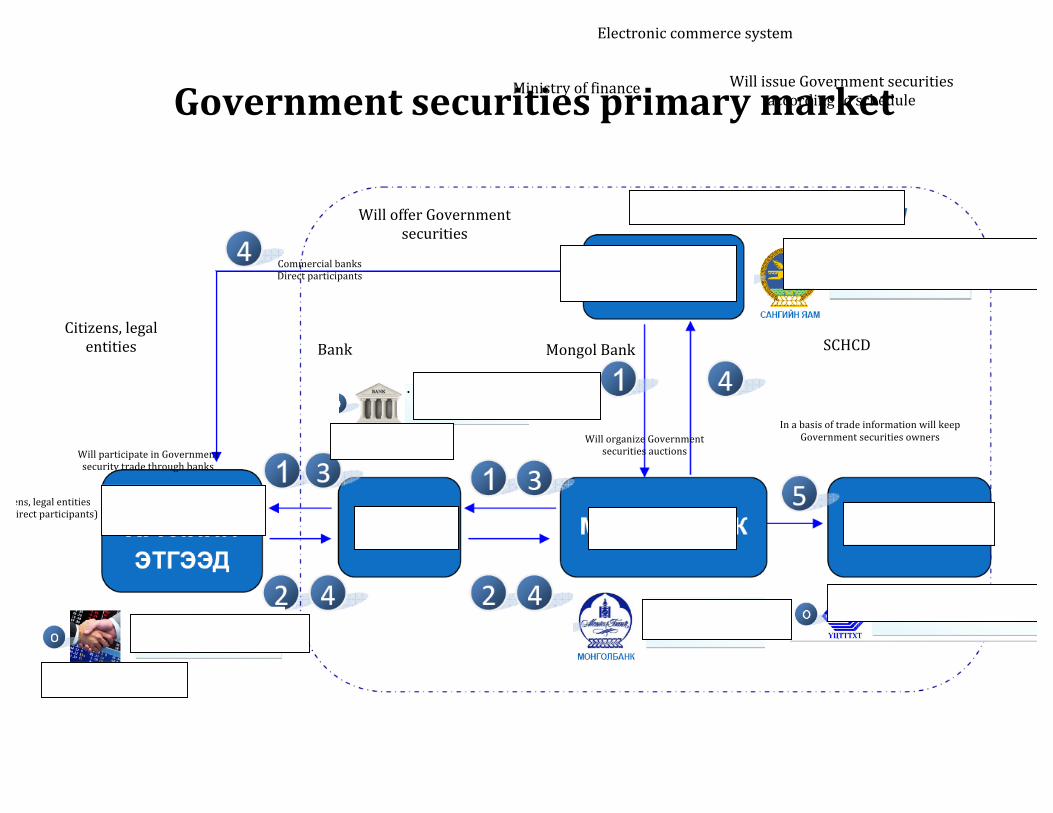

Government securities primary market

Electronic commerce system

Ministry of finance Will issue Government securities according to schedule

Will offer Government securities

Commercial banks Direct participants

Citizens, legal entities Bank Mongol Bank

Citizens, legal entities (non-‐direct participants)

SCHCD

Will participate in Government security trade through banks

Will organize Government securities auctions

In a basis of trade information will keep Government securities owners

Foreign investment procedure in domestic bond, equities market

International financial market

Foreign investors

Domestic banks

Foreign currency swap market Domestic

banks Domestic broker, dealer companies

Government bond market

Mongolian capital market

USD

LIBOR USD

USD ₮ ₮

LIBOR

PR<i<RP

₮ ₮

Government securities interest хүү (12.0%, 1 year)

₮

Government securities, Government

bonds

Companies securities, bonds ₮

Equities, bonds interest

Will conclude executive agent contract

Will give sale, purchase order Mongolian rating

Moody’s: B1

S&P:BB-‐

Fitch:B+

Are foreign investors will be interested in domestic Government bonds?

5 years: 4.125%+3.2%(45₮)=>7.5%

10 years: 5.125%+3.2%(45₮)=> 8.5%

Long-‐term, stabile structure of housing financing Mongol Bank (Finance

intermediator)

Commercial bank

Owners of old housing

New housing payment

Co-‐owner of new housing

State owned organizations in

mortgage secondary market

(SOOMSM)

Capital market Government Investors (SIF etc.)

Source Advance payment

Remainder

Old housing: Credit security

New housing: Credit security

Mortgage loan

Mortgage credit line

Government m

edium-‐

term bonds

At the first stage of development – Government guarantees for

SOOMSM equities

(7) M

ortgage loan

Source

Source

Equities secured by mortgage loan

Equities secured by mortgage loan

Source

(1) (2)

(2)

(2)

(3)

(3)

(3)

(1)

(4)

(5) (6) (6)

(6) (6)

(7) (7)

Mortgage secondary market

Financial structure of purchasing new housing in a basis of old housing

(4) New mortgage loan

Mongol Bank, Government and banks will conclude trilateral contract: Bank will transfer new loan pack, received from Mongol Bank and issued in a basis of Government bond source to the SOOMSM.

Some necessary works

⋅ Government has to activate secondary securities market

⋅ Give possibility to organize human benchmark or effectiveness curve ⋅ Will be formed possibilities to use in implementation of monetary policy

⋅ Organize institutional investors based on pension fund

⋅ Main investor in financial system ⋅ Will be organized long-‐term sources

⋅ Support financial organizations in mortgage secondary market

⋅ Issue MBS of become one of the main supplier of equities ⋅ Will be created long-‐term sources

ISSUES TO BE CONSIDERED AT EQUITIES AND STOCK MARKET DEVELOPMENT

Basic conditions of market development

⋅ Constant sale of Government equities, bonds according to determined schedule, make information transparent

⋅ Will be formed market benchmarks ⋅ Will be developed company bond & derivative market ⋅ Search for bank or foreign sources by companies will be lowered

⋅ Development of market of shares

⋅ Number of registered major companies are low (6 major companies: 5 million $)

⋅ Improvement of assessment process ⋅ Create true, open state of company profit, income ⋅ Improve activity and capability of capital market intermediator’s ⋅ Increase investors knowledge and trust

⋅ Extend base of institutional investors: Joined investment fund, pension fund, insurance companies

⋅ Stabile demand for long-‐term equities and stocks

Questions to be considered during market development

⋅ Improvement of legal environment ⋅ Updated revision of Equity market law ⋅ Adjust in accordance with International capital market principles

⋅ Create legal system oriented to power of the companies and improvement of openness ⋅ Recording, audit standards: Increase trust to companies

⋅ Give consideration to improve capabilities and potentials of capital market participants ⋅ Discuss market difficulties, take information about and implement new products and cervices

⋅ Correct definition of subsequent reforms ⋅ Prepare documents including challenges, solutions and cooperation in the way of capital market development

Thank you for your attention