18.7 lower of cost and net realisable value

TRANSCRIPT

18.7LOWER OF COST AND NET REALISABLE VALUE

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

18.7 LOWER OF COST AND

NET REALISABLE VALUE Example: a retailer purchased 10,000

iPods in 2006 thinking they could be sold easily for the next 10 years. The iPods cost the retailer $250 each.

The retailer didn’t anticipate the iPhone making the iPod obsolete , and today the retailer has 1,000 iPods left that can be sold for only $150 each.

How should these be valued today?2006 Cost of Stock

$250

Current Selling Price $150

Vs.

Relevance?

Reliability?

Historical Cost?

Conservatism?

Consistency?

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Inventory is not always valued at its “cost” price. Sometimes, the amount stock can be sold for is less than it actually costs

Example… hotel rooms

$199Usual cost of 1 room at Hotel Windsor site

$149Today’s rate at lastminute.com.au

18.7 LOWER OF COST AND

NET REALISABLE VALUE

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Example… David Jones swimwear in June, July and August

Why is swimwear on sale this time every year?

18.7 LOWER OF COST AND

NET REALISABLE VALUE

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Why do businesses sell stock for less than its cost? Sometimes a business will sell an item of stock for less than its cost because the item of inventory:

Has been superseded by a newer model, e.g. old model iPhone

Has become obsolete, e.g. typewriters, CDs

Is out of season, e.g. selling umbrellas during summer

Is out of fashion, e.g. wrong colour for this season

Is damaged or spoiled, e.g. bread, fruit, vegetables

Is being deliberately sold below cost, e.g. discounting to attract customers, selling tickets that would otherwise go to waste

18.7 LOWER OF COST AND

NET REALISABLE VALUE

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

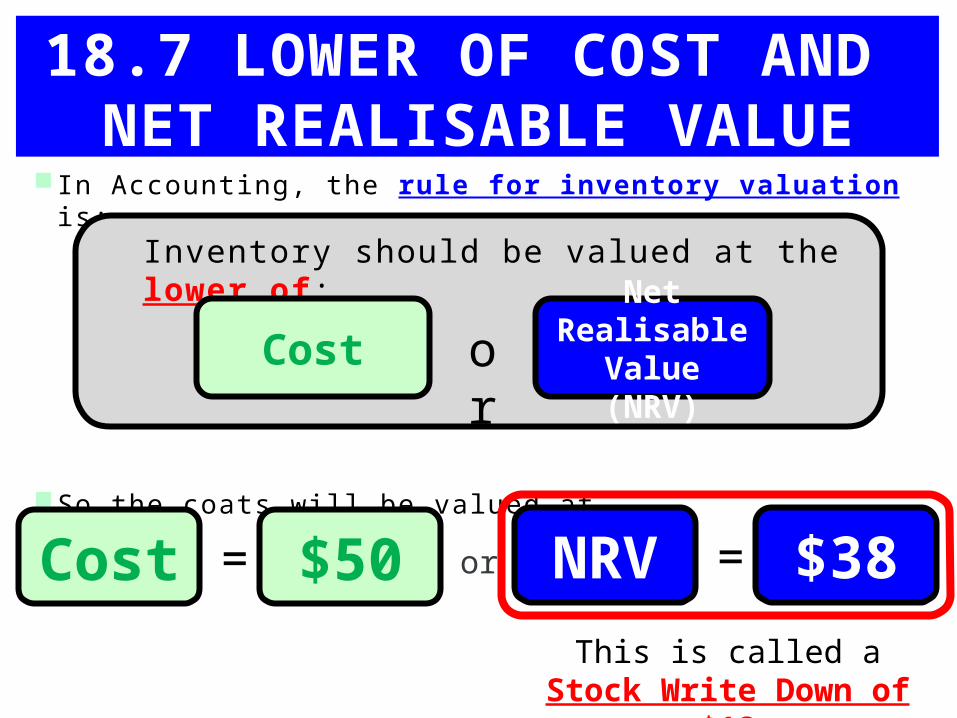

In Accounting, the rule for inventory valuation is:

Inventory should be valued at the lower of:

CostNet

Realisable Value (NRV)

or

18.7 LOWER OF COST AND

NET REALISABLE VALUE

The item’s Product Cost

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Net realisable value (NRV) is:

The estimated selling price of an item of inventory, less any costs incurred in

Selling

Marketing or

Distributing the stock to the customer

NRV = Estimated selling price of stock

Selling, marketing and

distribution costs

18.7 LOWER OF COST AND

NET REALISABLE VALUE

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Net realisable value (NRV) example:

On 1 December a firm has 100 coats in stock.

The Product Cost of each coat is $50

How much should the coats be valued for in the firm’s Balance Sheet?

To sell the coats in summer, the selling price has been lowered to $40

In addition, an advertisement costing $200 has been taken out in the local newspaper advertising the sale (for 100 coats)

$50?

$52?

$40?

$38?

$42?

18.7 LOWER OF COST AND

NET REALISABLE VALUE

Inventory should be valued at the lower of:

CostNet

Realisable Value (NRV)

or

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Cost = $50

NRV =Estimated

selling price of stock

Selling,

marketing and distribution

costs$40 $2 $38=

18.7 LOWER OF COST AND

NET REALISABLE VALUE Net realisable value (NRV) example:

On 1 December a firm has 100 coats in stock.

The Product Cost of each coat is $50

To sell the coats in summer, the selling price has been lowered to $40

In addition, an advertisement costing $200 has been taken out in the local newspaper advertising the sale (for 100 coats)

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

or

In Accounting, the rule for inventory valuation is:

So the coats will be valued at…

18.7 LOWER OF COST AND

NET REALISABLE VALUEInventory should be valued at the lower of:

CostNet

Realisable Value (NRV)

or

Cost = $50 NRV = $38This is called a

Stock Write Down of $12

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

18.7 LOWER OF COST AND

NET REALISABLE VALUEIncome StatementRevenue $ $

Cash sales 100000

Credit sales 20000 120000

less Cost of Goods Sold

Cost of sales 48000

Import duties 2000 50000

Gross Profit 70000

less Stock loss 900

Stock write down XXXX

Adjusted Gross Profit 68700

less Other Expenses

Rent 3000

Insurance 2400 5400

Net Profit 63300

Stock Write Down is an Expense

Hence, it must be reported in the Income Statement

It is listed in between Gross Profi t and Adjusted Gross Profi t along with stock loss/gain

Income StatementRevenue $ $

Cash sales 100000

Credit sales 20000 120000

less Cost of Goods Sold

Cost of sales 48000

Import duties 2000 50000

Gross Profit 70000

less Stock loss 900

Stock write down XXXX

Adjusted Gross Profit 68700

less Other Expenses

Rent 3000

Insurance 2400 5400

Net Profit 63300

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

TASK

In-class Homework

SQ5 XSQ6 X