160525 kempen real estate seminar - home - nsi · kempen real estate seminar ... - junctions...

TRANSCRIPT

Kempen Real Estate Seminar-25 May 2016-

Company profile

• Dutch REIT, founded in 1993 and listed in Amsterdam in 1998

• NSI acquired VastNed Offices (VNOI) in 2011

• NSI launched its full service and flexible office concept HNK in 2012

• Successful recapitalisation in November 2013

• Refinancing of €550 mln with group of banks and institutionals completed in 2015

• NSI divested its interest in IOW in 2015/2016*

• Industrials portfolio divested in 2016

1

Company description

Segment breakdown on asset value Breakdown on gross rental income

Key financials

FY 2015* FY 2014

Portfolio value (€m) * 1,203.5 1.668.1 Gross rental income (€m) 113.8 133.6 Net rental income (€m) 91.3 109.2 Direct investment result (€m) 50.6 48.2 Loan-to-Value (%) 43.2 48.9 Occupancy (%) 77.3 77.1 Interest cover ratio (x) 3.2 2.6

* IOW i s no longer consolidated in the income statement from Q3 2015 onwards and in the balance sheet as per 30 June 2015.

Offices (121 properties)

HNK (11 properties)

Retail (35 properties)

LSR (6 properties)

51%

11%

31%

6%

Offices

HNK

Retail

LSR

52%

6%

52%

10%

32%

Dutch economy in a nutshell

2

Macro economic parameters are turning positive

economic growth

decreasing unemployment rate

increasing consumer confidence & spending

strong recovery residentual market

Economic growth

Unemployment rate Consumer confidence

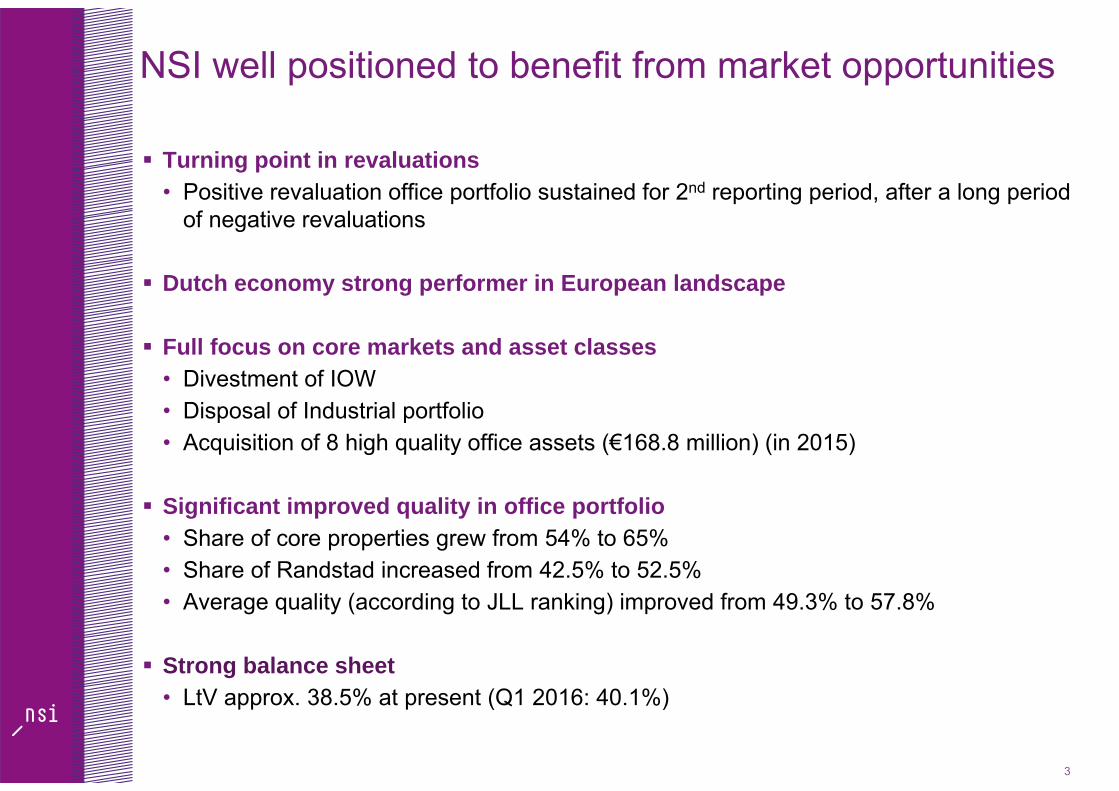

Turning point in revaluations• Positive revaluation office portfolio sustained for 2nd reporting period, after a long period

of negative revaluations

Dutch economy strong performer in European landscape

Full focus on core markets and asset classes• Divestment of IOW• Disposal of Industrial portfolio• Acquisition of 8 high quality office assets (€168.8 million) (in 2015)

Significant improved quality in office portfolio • Share of core properties grew from 54% to 65%• Share of Randstad increased from 42.5% to 52.5%• Average quality (according to JLL ranking) improved from 49.3% to 57.8%

Strong balance sheet • LtV approx. 38.5% at present (Q1 2016: 40.1%)

3

NSI well positioned to benefit from market opportunities

Strategy: portfolio focus further increased Sale of almost entire industrial portfolio (€48.1 million) Sale of the remaining interest (15.2%) in IOW Agreement to release securities related to bank funding (€450 million) as per

1 September 2016 LtV, after asset sales and dividend distribution, to approx. 38.5% at present

Operational Occupancy rate of total portfolio increases to 78.1% (31 December: 77.3%)

Occupancy rate total office portfolio increased to 74.3% (Q1 2015: 71.4%, Q4 2015: 73.6%) Rental income Dutch office portfolio grew slightly compared with Q4 2015−Quality improvement and focus on HNK start to pay off−HNK continues to perform strongly

Retail remains challenging; occupancy level increased over stable development of rent levels 4

Highlights Q1 2016

ASSET ROTATION UPDATE2

6

Conglomerates in European perspective

Combined strenght of the Netherlands, Belgian Flemish Diamond and German Rhein/Ruhr area

GATEWAY TO EUROPE

EUROPEAN CAPITAL

BRUSSELS TECH ZONE

MANUFACT

URIN

G

RHEIN

/RUH

R

RAND

STAD

GATEWAYTO EUROPE

EU-CAPITALBRUSSELS

RHEIN/RUHRBRABANT

EINDHOVENBRAINPORT

The Netherlands is fundamentally strong positioned

30 million inhabitants € 150 billion internal Trade

European manufacturing industry Gateway to Europe Largest port of Europe Best airport of Western-Europe European political and governing centre Strong universities

NSI is focusing on 18 cities- Junctions determine the economic dynamics -

52% 28 %

20 %

Geographical distrbution office portfolio (in value)

Asset rotation in € millions 2008 - 2016

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014 2015 2016

AcquiredDivested

Portfolio Philips Pensioenfonds and

Swiss assets

Excluding acquisition VNOI

(€971m)

8 high quality office assets (€169 m)

Disposal industrial portfolio

10

Divesting non-core assets and assets of which the value potential under NSI’s management has been optimised is part of NSI’s strategy to create value in its portfolio

Investment focus on Dutch office market, migrating to a higher quality

Cumulative divestment volume 2008-2016: €465 million, excluding divestment IOW shares (€165 million) Cumulative acquisition volume (2008-2016): € 1,618 million (including Vastned)

Excluding divestmentIOW shares (€165 m)

Vivaldi 1Location: Amsterdam South-Axis

Total size: 9,592 sq m

Passing rent: € 2.4 mio

WAULT (yrs) 14.4

Occupancy: 100%

Tenure Multi tenant (leased to operator)

1 Vivaldi 2Location: Amsterdam South-Axis

Total size: 8,687 sq m

Passing rent: € 2.3 mio

WAULT (yrs) 7.1

Occupancy: 100%

Tenure Multi tenant, leased to operator

2

Centerpoint 1Location: Amsterdam South-East

Total size: 9,011 sq m

Passing rent: € 1.9 mio

WAULT (yrs) 4.8

Occupancy: 98.9%

Tenure Multi tenant

3 Centerpoint 2Location: Amsterdam South-East

Total size: 6,249 sq m

Passing rent: € 1.3 mio

WAULT (yrs) 6.0

Occupancy: 100%

Tenure Single tenant

4

AlexanderpoortLocation: Rotterdam Alexander

Total size: 9,408 sq m

Passing rent: € 1.5 mio

WAULT (yrs) 3.1

Occupancy: 88.5%

Tenure Multi tenant

5 AlexanderhofLocation: Rotterdam Alexander

Total size: 3,120 sq m

Passing rent: € 0.5 mio

WAULT (yrs) 3.0

Occupancy: 94%

Tenure Multi tenant

6

het BinnenhofLocation: Den Bosch, Paleiskwartier

Total size: 10,442 sq m

Passing rent: € 1.5 mio

WAULT (yrs) 5.9

Occupancy: 90.6%

Tenure Multi tenant

7 YpsilonLocation: Leiden, Bio Science Park

Total size: 9,418 sq m

Passing rent: € 1.6 mio

WAULT (yrs) 4.5 (break-date)

Occupancy: 100%

Tenure Single tenant

8

Transformations Office Portfolio

5. 7. 9.6.

Total realized ca. 50,000 m² Total in pipeline ca. 48,000 m²

City m² (ca.) Potential type of useEindhoven 22,650 Residential/ Hotel Amsterdam 1,250 ResidentialDen Haag 3,000 ResidentialUtrecht 3,300 Residential/ SocialBreda 5,000 ResidentialGouda 10,000 IndustrialZoetermeer 3,000 Residential

City Address m² Type of use1. Amsterdam Koningen Wilhelminaplein 5,019 Residential2. Amsterdam Arlandaweg 4,257 School3. Utrecht Reactorweg/Kobaltweg* 10,009 Industrial4. Zeist Montaubanstraat* 1,539 Residential5. Amsterdam Karel du Jardinstraat* 6,107 Residential6. Amersfoort Hardwareweg* 5,858 School7. Nieuwegein Villawal* 5,783 Residential8. Amsterdam Delflandlaan* 7,440 Hotel9. Den Haag Ln Copes v Cattenburgh* 1,705 Residential10. Velp Arnhemsestraatweg* 2,155 Residential

REALIZED (2014-2016) IN PROGRESS (2016)

* = sold assets

After big step up in 2014-2015; asset rotation is continuous part of strategy− Focus on improving performance− Full focus on Dutch high quality multi tenant offices in selected regions and

neighbourhood shopping centers− Non strategic: Large Scale Retail, 2 remaining Industrial assets

NSI leasing platform allows for further growth in offices− More focused portfolio and organisation− Leveraging gross to net

Roll out HNK from 11 at present to 20 HNKs by year end 2016− Currently under construction:

• HNK Rotterdam Blaak (2nd HNK in Rotterdam)• HNK Amsterdam Arena (2nd HNK in Amsterdam)

− Selective acquisitions to optimise nation-wide network

13

Next phase in offices – focus on performance

OPERATIONAL PERFORMANCE - OFFICES3

14

‘

15

Co working & members space Cafe

Tailored offices

Meeting rooms

Higher take up Higher effective rent Quicker re-lettings Higher retention Additional income

stream Customer satisfaction

Managed Offices

‘social heart’+ =

HNK - a place to be: inspiring meeting place to work, connect and meet

Connected

Operational highlights offices

16

Offices (Excluding HNK) Q1 2016 Q4 2015 Q1 2015 2015 2014

Gross Rental income (€ million) 11.5 12.1 10.6 43.1 54.7

Occupancy rate in % 79.7 76.7 74.4 76.7 77.4

Take up 2,925 4,615 4,840 28.006 18.910

Take up / supply ratio (12 months rolling in %) 17.4 18.5 18.5% 10.5%

Effective rent level new leases (12 months rolling) per sqm €106 €107 €107 €107 €113

Effective rent level per sqm total portfolio €153 €157 €146 €157 €143

Like-for-like growth gross rental income in % -9,1 -11.5 -8.7 - 11.5 - 4.0

WAULT 5.1 5.1 3.8 5.1 3.5

Occupancy rate positively impacted by reclassifications; underlying stable development Q4 vs Q1

Negative l-f-l growth largely due to expired contracts in last 12 months; Q1/16 vs Q4/15 shows improving trend

Stable development effective rent level new leases

7% of office contracts expire in 2016

OPERATIONAL PERFORMANCE HNK 4

17

Operational highlights HNK

19

Q1 2016 Q4 2015 Q1 2015 2015 2014

Gross rental income( € million) 2.6 2.1 1.7 8.0 5.4

Occupancy rate in % 57.0 59.6 57.5 59.6 56.6

Take up 3,414 6,167 4,250 21,139 4,855

Take up supply ratio in % 39 45 36 45 26

Effective rent level new leases (12 months rolling) per sqm €166 €165 €167 €165 €169

Effective rent level per sqm total portfolio €180 €188 €167 €188 €160

Like-for-like growth gross rental income in % 12.8 18.6 29.7 18.6 25.5

WAULT 3.2 3.1 2.8 3.1 2.4

All product categories show positive trend

GRI HNK as % of GRI total offices rose to18.6% in Q1 2016 from 14.7% in Q4 2016

Gross Net should evolve to 75-80% when fully leased up (occupancy 85-90%)

Occupancy rate continously impacted by inflow of new HNK’s All other individual HNKs showed increasing occupancy rates, except for HNK Rotterdam due to

legacy tenant that left in Q4 2015

L-f-l growth in HNK expected to largely compensate negative l-f-l growth in traditional offices

HNK won award “Best office landlord 2016”

Operational highlights total offices

20

Offices ((Including HNK) Q1 2016 Q4 2015 Q1 2015 2015 2014

Gross Rental income (€ million) 14.2 14.1 12.4 51.1 60.1

Occupancy rate in % 74.3 73.6 71.4 73.6 71.5

Effective rent level new leases (12 months rolling) per sqm €138 €138 €133 €135 €129

Effective rent level per sqm total portfolio €157 €161 €146 €161 €149

Like-for-like growth gross rental income in % -5.0 -6.9 -8.7 -6.9 -4.0

Occupancy rate total offices increased, in combination with stable rental levels of new leases

GRI total office portfolio shows slightly improving trend

OPERATIONAL PERFORMANCE - RETAIL5

21

The changing retail market- enforces to make choices -

“Fun shopping”: Shopping for leisure

“Daily needs”: efficient shopping + meet (locally)

Experience

Services

23

Easyshopping adds extra dimension to dailyshopping centre:

Connect: • Creating communities• Offering (online) services• Intensify relationship retailer - consumer

Enlarge reach through active (online) marketing

Increase dynamics: through activities in shopping centre

Launched in shopping centre Zevenkamp (Rotterdam) Roll out to shopping centres in region Rotterdam

AddedValue

24

Retail Local Convenience

Q1 2016 Q4 2015 Q1 2015 2015 2014 2015

Gross Rental Income € million) 6.4 6.9 7.1 27.9 32.1

Occupancy rate in % 85.3 84.4 88.2 84.4 88.4 89

Effective rent level per sqm total portfolio per sqm €199 €215 €159 €215 €135

Effective rent level per sqm total portfolio per sqm €179 €178 €178 €178 € 183 € 173

Valuation development in % -2.5 1.0

Like-for-like growth gross rental income in % -8.0 4.3 3.1 4.3 - 11.0 1.0

WAULT 4.4 4.6 4.6 4.6 4.5

Retail market remains challenging despite improving consumer confidence & spending

Negative l-f-l growth largely explained by one-off gains in 2015

5% of retail contracts expire in 2016

Operational highlights retail

FINANCIAL6

25

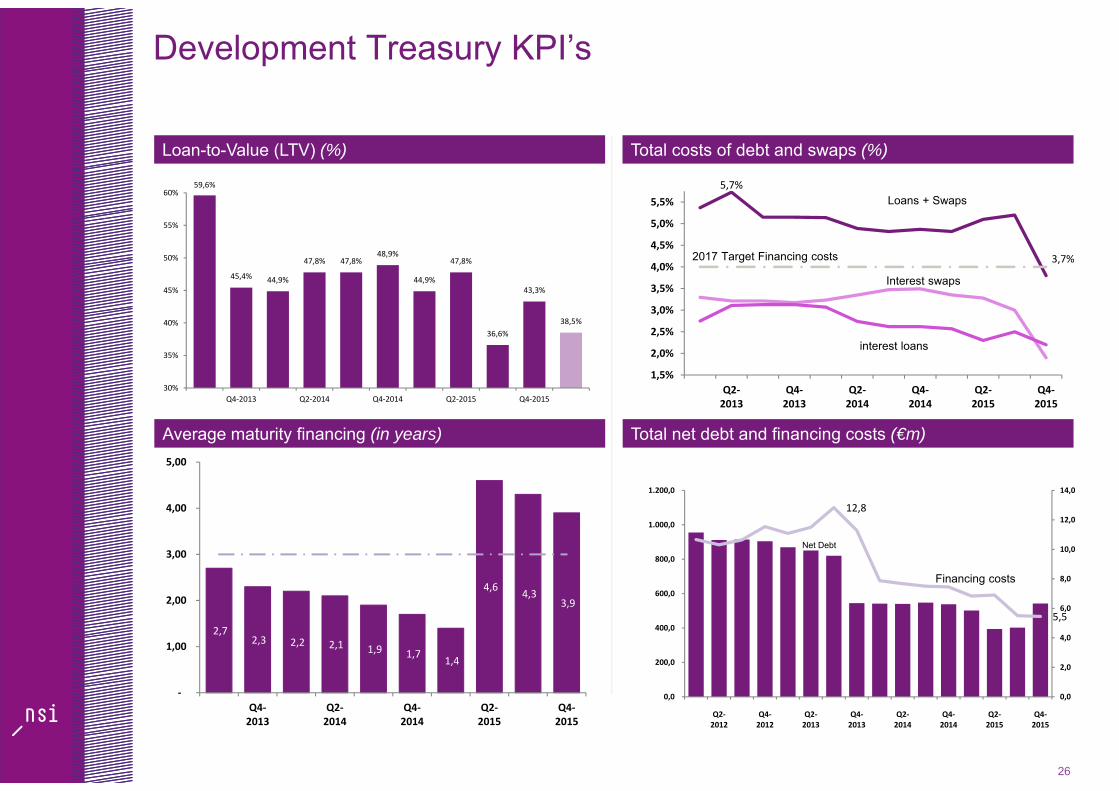

Development Treasury KPI’s

26

Loan-to-Value (LTV) (%) Total costs of debt and swaps (%)

Average maturity financing (in years) Total net debt and financing costs (€m)

5,7%

3,7%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

5,5%

Q2‐2013

Q4‐2013

Q2‐2014

Q4‐2014

Q2‐2015

Q4‐2015

Interest swaps

interest loans

2017 Target Financing costs

Loans + Swaps

2,7 2,3 2,2 2,1 1,9 1,7 1,4

4,6 4,3 3,9

‐

1,00

2,00

3,00

4,00

5,00

Q4‐2013

Q2‐2014

Q4‐2014

Q2‐2015

Q4‐2015

12,8

5,5

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

0,0

200,0

400,0

600,0

800,0

1.000,0

1.200,0

Q2‐2012

Q4‐2012

Q2‐2013

Q4‐2013

Q2‐2014

Q4‐2014

Q2‐2015

Q4‐2015

Net Debt

Financing costs

59,6%

45,4% 44,9%

47,8% 47,8%48,9%

44,9%

47,8%

36,6%

43,3%

38,5%

30%

35%

40%

45%

50%

55%

60%

Q4‐2013 Q2‐2014 Q4‐2014 Q2‐2015 Q4‐2015

Financing strategy

27

Conversion to financing without collateral

Optimise secured financing (Pandbrieffinanciering)

Increase current facilities and use of accordeon

Enter bilateral financing with institutional parties

I

II

III

IV

Issue convertible bondV

KPI 13Q3 Q1 2016 Target 2017

Loan to Value

Average duration

43.2%

2.6yrs

40.1%

3.7yrs

40 – <50%

> 3yrs

Available funding 25% 28% 10 – 20%

Costs of debt 4.8% 3.8% < 4.0%

Improved financing structure provides multiple strategic financing opportunities

Div Cost Refi Mat Unsec

Div = diversify funding sources, Cost = Lower financing costs, Refi = Refinancing risk, Cov = Covenants, Mat = maturies, Unsec = unsecured

Strategic financing opportuities

Diversification 8% 18.4% 40 – <50%

Secured/ non secured 100% <100% <35 \>65%

Financial highlights

28

x€1,000 FY 2015 FY 2014 HY2 2015 HY1 2015

Gross rental income 113,835 133,599 45,703 68,132

Service costs not recharged to tenants -5,796 -5,828 -2,453 -3,343

Operating costs -16,715 -18,611 -8,660 -8,055

Net rental income 91,324 109,160 34,590 56,734

Administrative costs -6,914 -7,711 -3,075 -3,839

Financing income 2,541 176 2,494 47

Financing costs -30,777 -42,391 -10,913 -19,864

Result minority interests 2,377 - 2,377 -

Direct investment result before tax 58,511 59,234 25,433 33,078

Corporate income tax -125 -111 -7 -118

Direct result att. to minorities -7,811 -10,672 - -7,811

Direct investment result 50,575 48,451 25,426 25,149

Indirect investment result 13,219 -185,348 -4,032 17,251

Total result 63,794 -136,897 21,394 42,400

€ 200 mln improvement year on year

Deconsolidation IOW, asset rotation and negative L-f-l of -€ 2,6mln,

Divestment non-core and cost control

Enlargement portfolio, + € 2.5 mln one-off in BE Letting costs (Deloitte) in HY1

€ 2.5 mln one-off from settlement withholding tax Belgian Authority

IOW, Lower debt, improved conditions in refinancing agreement, changes in swap portfolioIOW result after deconsolidation

Minority share before sale to minority

Significant improvement on all elements: valuations, asset sales, IOW sale, value of derivatives

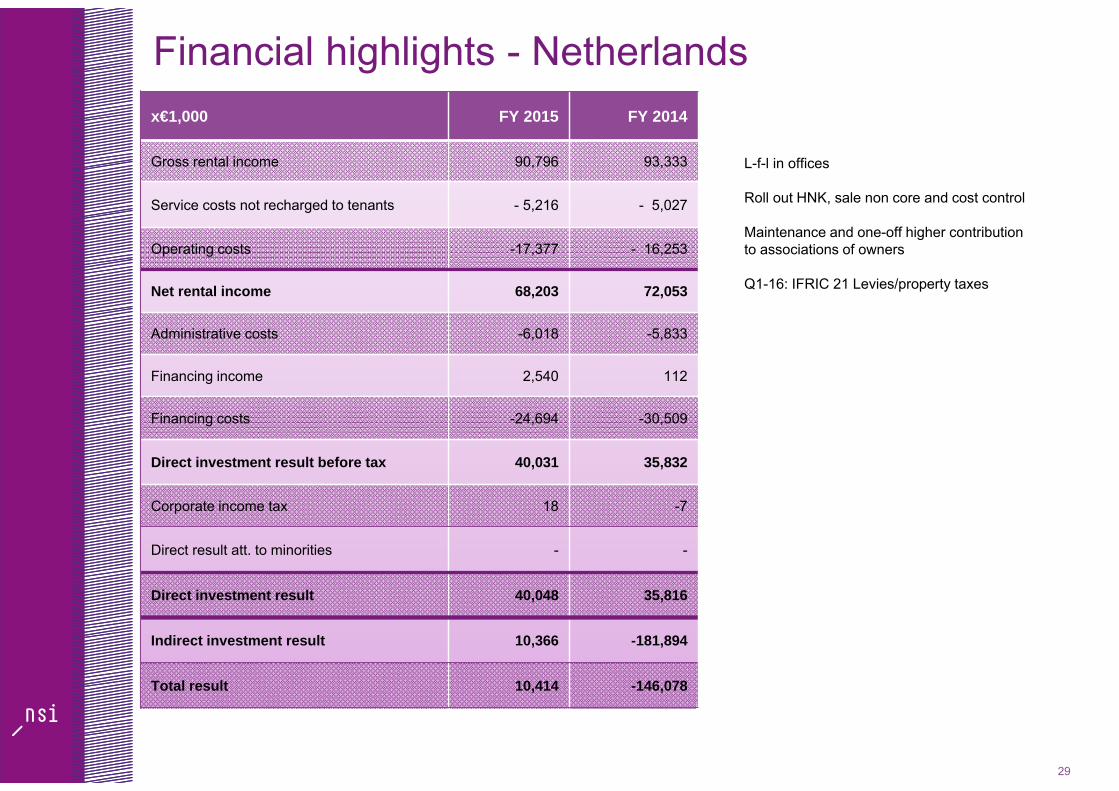

Financial highlights - Netherlands

29

x€1,000 FY 2015 FY 2014

Gross rental income 90,796 93,333

Service costs not recharged to tenants - 5,216 - 5,027

Operating costs -17,377 - 16,253

Net rental income 68,203 72,053

Administrative costs -6,018 -5,833

Financing income 2,540 112

Financing costs -24,694 -30,509

Direct investment result before tax 40,031 35,832

Corporate income tax 18 -7

Direct result att. to minorities - -

Direct investment result 40,048 35,816

Indirect investment result 10,366 -181,894

Total result 10,414 -146,078

L-f-l in offices

Roll out HNK, sale non core and cost control

Maintenance and one-off higher contribution to associations of owners

Q1-16: IFRIC 21 Levies/property taxes

Balance sheet highlights

30

x€1,000 31/12/15 30/6/15 31/12/14

Real estate investments 1,203,465 1,048,940 1,668,176

Total shareholders equity 660,748 657,951 788,302

Shareholders equity of NSI 660,720 657,979 632.112

Debt to credit institutions (excl. derivatives) 542,332 385,479 815,483

Average cost of debt (%) 3.7 5.1 4.6

Net loan to value (%) 43.2 35.1 48.9

Average debt maturity (years) 3.9 4.6 2.0

Fixed interest debt (%) 80.4 94.2 89,7

Interest coverage ratio 3.2 2.9 2.6

NAV (€/share) 4.61 4.59 4.41

EPRA NAV (€/share) 4.79 4.78 4.69

Deconsolidation of IOW (€ 636 mln), asset sales (€ 43,3mln), acquisitions (€ 169 mln),investments (€ 16,8 mln) and revaluations (€1,4 mln). Industrial portfolio (€ 61,2 mln) classified as held for sale

Minority stake - € 156 mln

Positive result (€ 63,8 mln) - dividend payments (€ 35.8 mln), value 15.2% stake IOW (€ 51.4 million)

Deconsolidation of net Belgian debt and net investment

As result of improved conditions in refinancing agreement, changes in derivative portfolio

LtV, after asset sales and dividend distribution, 38.5% at present

Minimum coverage policy = 70%

Minimum ICR is 2

First increase in NAV since 2011

CONCLUSION7

31

Outlook

NSI expects to improve the overall occupancy rate of the total portfolio; Improvement of the occupancy rate of office portfolio Relatively stable development of the occupancy rate in retail portfolio.

GRI of Dutch portfolio (excluding sold industrial portfolio) will show a slightly improving trend HNK expected to largely compensate for negative l-f-l growth in traditional office

portfolio

Impact divestment IOW in 2016 vs 2015 amounts to approx. €23.0 mln in GRI and approx. €8.5 mln in direct result

Impact divestment industrial portfolio in 2016 vs 2015 amounts to approx. €3.7 mln in GRI and approx. €2.5 mln in direct result

Impact IFRIC 21 directive on operating costs in HY1

32

APPENDIX

34

− Recognition of NSI’s remaining 15,2% share in IOW• Significant influence in IOW

• Equity method to be used going forward

• Pro-rate share in net income to be recognized in NSI results on a quarterly basis

• Financial Fixed Asset, value based upon NAV + Future results to be added - future dividends to be deducted results in future NAV in NSI books

− Impact on Balance sheet as per 31 December 2015:• Decrease in value of real estate investments of € 635.7 million

• Balance sheet total decreased by € 656.1 million

• Debt to credit institutions decreased by € 320.4 million

• 15.2% share classified as “minority interest” at € 51.4 million: € 20,75/share

− Impact on P&L• Total DR HY1-15: 7,8 Million (incl one-off)

• Total DR HY2-15: 2,3 Million + reduction Interest costs @1,5-2%

• DR 2015:10,2 million (2014: 12,6 million)

• Reinvestment after 1 quarter

Recognition of IOW stake in 2015

2015: Turning point in Dutch revaluations

2008 2009 2010 2011 2012 2013 2014 HY1 15 HY2 15 2015

Industrial

LSR

Retail

Offices

35

Positive revaluation of the office portfolio sustained for second reporting period, after a long period of negative revaluations (€630 million since 2008, of which 75% in offices)

- to €9.1 million in total in 2015- driven by slight decrease in market yields and market rents- Includes transaction costs of acquisitions (cobra portfolio) of approx. €9 million

Offset by negative revaluations in the retail portfolio- to €9.4 million in total in 2015- driven by increasing market yields

The value of the large scale retail portfolio saw an increase of €4.3 million in total in 2015, the industrial portfolio decreased by €2.6 million in total in 2015

In millions € 2015 Bookvalue31/121/15

Offices €9.1 717.1

Retail - €9.4 356.9

LSR €4.3 68.2

Industrial - €2.6 61.2

Total €1.4 1,203.5