1 health savings account open enrollment 2010. 2 enable informed decision-making by providing...

TRANSCRIPT

1

Health Savings Account

Open Enrollment 2010

2

• Enable informed decision-making by providing members with meaningful & easy to use information

• Engage consumers with health & wellness programs that emphasize routine preventive care which can lead to healthier behaviors now and in the long term

• Encourage members to make informed health care decisions by creating financial incentives, such as portable health care cash accounts with balance rollover

The concept of consumer directed health plans (CDHP) focuses on encouraging members to become more involved in and taking more responsibility for their health care decisions, purchases and use of health care services.

Definition of Consumer Directed Health

3

Capital BlueCross markets CDH products under the name of SimplySelect. SimplySelect incorporates products, web tools and clinical programs into a cohesive, packaged consumer directed product.

Consumer Directed Product Suite

4

Health Savings Account

HSA Overview

5

Savings account with money in it

Allows you to put money aside to pay for qualified expenses tax-free*

Unused dollars roll over into the next year

The account can be invested and you keep any earnings

Employer and/or employee contributions permitted up to the established IRS maximum contribution limit each year

It’s portable - you own the account funds even after termination, retirement, etc.

You retain control and make choices about how to spend your health care dollars

Allows you to pay for medical expenses that may not be covered under your health plan

Health Savings Accounts are like a medical 401(k)...a way for you to save for retirement.Health Savings Accounts are like a medical 401(k)...a way for you to save for retirement.

What is an HSA?

*Tax references are for federal taxes only. State taxes vary. Consult your tax advisor.

6

You must have a You must have a IRS-qualifiedIRS-qualified High Deductible Health Plan (HDHP) in order to open an HSA. High Deductible Health Plan (HDHP) in order to open an HSA. The two pieces work together to create the SimplySelect HSA product.The two pieces work together to create the SimplySelect HSA product.

Preventive Care

Deductible

PPO Medical Plan

Prescription Drug Plan

Heal

th S

avin

gs A

ccou

nt

HDHP HSA

HDHP + Account = SimplySelect HSA

**

***

In-network preventive services (medical & Rx) not subject to the deductible

Medical and prescription drug expenses accumulate to the same combined deductible

The PPO medical plan covers medical expenses after the deductible has been met

The prescription drug plan covers drug costs after your deductible has been met

Funds in the HSA can be used to pay for any eligible expenses as defined by Section 213(d)

7

The IRS requires important design differences in these qualified high deductible health plans The IRS requires important design differences in these qualified high deductible health plans compared to our standard PPO plans.compared to our standard PPO plans.

The deductible applies to ALL services, except preventive (medical & Rx). This includes ER visits, ambulance services, prescription drugs and office visits. The

deductible must be met before the medical and/or prescription plans will pay.

The deductible applies to ALL services, except preventive (medical & Rx). This includes ER visits, ambulance services, prescription drugs and office visits. The

deductible must be met before the medical and/or prescription plans will pay.

Qualified plans only have two tiers of deductible coverage – single or family.

The entire family deductible (contracts of 2 or more) must be met before any family member is eligible for covered benefits.

Qualified plans only have two tiers of deductible coverage – single or family.

The entire family deductible (contracts of 2 or more) must be met before any family member is eligible for covered benefits.

The OOP max includes the deductible, coinsurance and copayments.

The OOP max includes the deductible, coinsurance and copayments.

Once the in-network OOP max is met, everything is covered in full. Coinsurance is 100% and all copayments are waived

(in-network) through the end of that calendar year.

Once the in-network OOP max is met, everything is covered in full. Coinsurance is 100% and all copayments are waived

(in-network) through the end of that calendar year.

Deductible Out-of-Pocket

Design Differences PPO Q vs. PPO

8

HSA “Q”ualified HDHP Plan DesignHere’s a high level outline of your qualified HDHP plan...

PPO HSA 1500QDeductible $1,500 member;

$3,000 family

OOP Max $2,000 member; $4,000 family

Coinsurance 100% In-network80% out-of-network

PCP $25 (subject to deductible)

Specialist $35 (subject to deductible)

ER $100 (subject to deductible)

IP Copay None

OP Facility Copay None

Rx(subject to deductble)

Retail: $8/$30/$60Mail: $16/$60/$120

Specialty: $15/$50/$100

2010 EMPLOYER HSAFunding (50%)

Single $750

Family $1,500

9

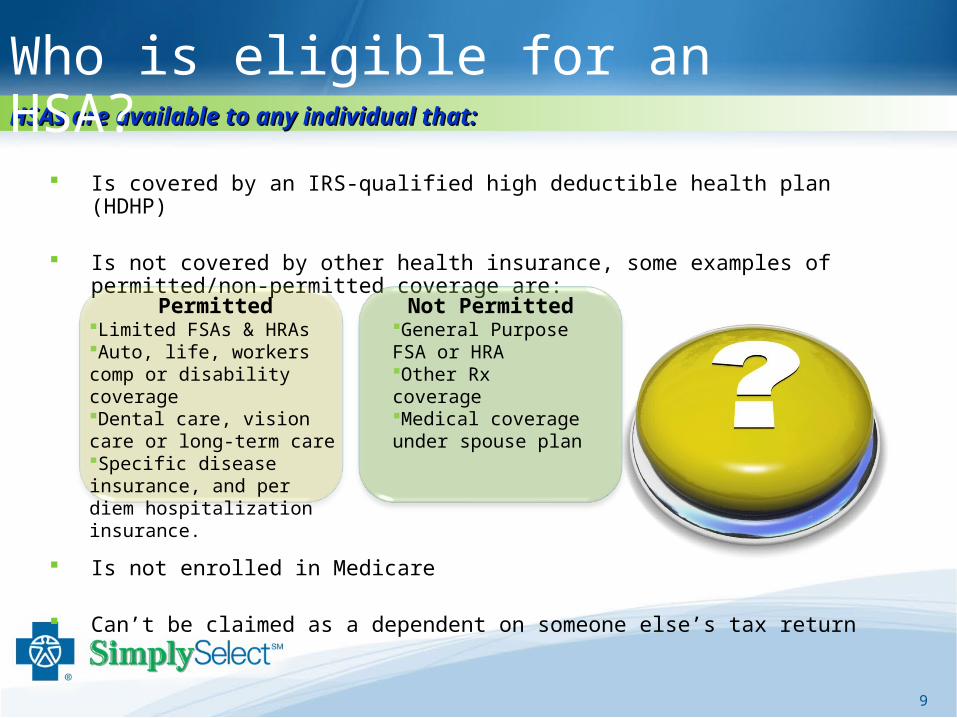

HSAs are available to any individual that:HSAs are available to any individual that:

Who is eligible for an HSA?

Is covered by an IRS-qualified high deductible health plan (HDHP)

Is not covered by other health insurance, some examples of permitted/non-permitted coverage are:

Is not enrolled in Medicare

Can’t be claimed as a dependent on someone else’s tax return

PermittedLimited FSAs & HRAsAuto, life, workers comp or disability coverageDental care, vision care or long-term careSpecific disease insurance, and per diem hospitalization insurance.

Not PermittedGeneral Purpose FSA or HRAOther Rx coverageMedical coverage under spouse plan

10

The IRS annually adjusts minimum deductible amounts and maximum contribution amounts The IRS annually adjusts minimum deductible amounts and maximum contribution amounts based on Cost of Living (COLA). HSA guidelines for 2010 are listed below. based on Cost of Living (COLA). HSA guidelines for 2010 are listed below.

HSA Contributions

2010

Minimum Deductible $1,200 single $2,400 family

Maximum Contribution* $3,050 single $6,150 family

Maximum Out-of-Pocket $5,950 single $11,900 family

55+ Catch up Contributions $1,000

11

In addition to using your HSA funds to pay for eligible deductible, coinsurance and copays In addition to using your HSA funds to pay for eligible deductible, coinsurance and copays under your health plan, funds can also be used for any IRS-qualified medical expenses. Below under your health plan, funds can also be used for any IRS-qualified medical expenses. Below are just a few examples of covered and non-covered servicesare just a few examples of covered and non-covered services

• Certain OTC Drugs

• Hearing Aids

• LASIK Surgery

• In Vitro Fertilization

• Long-Term Care Premiums

• Eyeglasses/Contacts

• Copays

• Coinsurance & Deductibles

• COBRA premiums

• Wheelchairs

For a complete listing of IRS qualified expenses, go to www.irs.gov/pub/irs-pdf/p502.pdf

• Life Insurance Premiums

• Health Club Fees

• Special Food & Beverages

• Cosmetic Surgery

• Bottled Water

• Burial Expenses

• Maternity Clothes

• Cosmetics

• Medigap Premiums

• Spa Treatments

COVERED EXPENSESCOVERED EXPENSES NON-COVERED EXPENSESNON-COVERED EXPENSES

HSA Eligible Expenses

12

Ability to save for future health care expenses and retiree health care coverage

Funds belong to you and the balance rolls over from year to year regardless of job changes or retirement

Ability to pay for services not covered under your medical plan - LASIK, OTC drugs, dental and vision care.

Triple tax advantage - Contributions are made pre-tax, plus any interest earned is earned tax-free and payment (distributions) for eligible expenses are tax free

After age 65, funds can be used for anything without penalty (only taxes apply)

You can continue to use your HSA funds even if you are no longer covered by an IRS qualified HDHP (cannot make any more contributions though)

Some advantages of HSAs are:Some advantages of HSAs are:

HSA Advantages

13

The chart below shows possible savings for individuals with an HSA.The chart below shows possible savings for individuals with an HSA.

Health Savings Account Balances (Assumes a $2,000 deductible and deposit each year)

Account Balance after X Years

Age of Head of Household

starting at 25

After Family Medical

Expenses of $1,000 each year

After Family Medical

Expenses of $500 each year

$0 Family Medical

Expenses

5 Years

10 Years

15 Years

20 Years

25 Years

35 Years

30 Years

30

35

40

45

50

60

55

$5,802

$13,207

$22,657

$34,719

$50,113

$94,836

$69,761

$8,703

$19,810

$33,986

$52,079

$75,170

$142,254

$104,641

$11,604

$26,414

$45,315

$69,439

$100,227

$189,673

$139,522

40 Years 65 $126,840 $190,260 $253,680

Source: The HSA Coalition; HSAInsider.com

Assumes 5% interest per year, and 100% of a $2,000 deductible is deposited each year.

Potential HSA Savings

14

HSAs are an IRS program, and as such, require tax filing every year.HSAs are an IRS program, and as such, require tax filing every year.

Employee Responsibilities for HSA

If your funds are used for a non-qualified expense before age 65, taxes and a 10% penalty will apply

Save your receipts in the event of an audit

You should contact your tax professional for more information on tax implications and filings

15

How does it work?

HSA Mechanics

16EOB = Explanation of Benefits HDHP = High Deductible Health Plan SOR = Statement of Remittance OOP = Out of Pocket

HSA Process Flow

Member writes check from ACS|BNY Mellon

account and reimburses themselves

Member writes check from ACS|BNY Mellon

account and reimburses themselves

Member chooses to pay OOP and saves HSA funds for

future use

Member chooses to pay OOP and saves HSA funds for

future use

Member pays provider with debit card or

check

Member pays provider with debit card or

check

Provider bills member for outstanding

liability amount

Provider bills member for outstanding

liability amount

Capital mails EOB to

member, SOR to provider

Capital mails EOB to

member, SOR to provider

Capital mails check to

provider and EOB to member

Capital mails check to

provider and EOB to member

Capital processes claim

Capital processes claim

Yes

Claim is processed and

applied to deductible

Claim is processed and

applied to deductibleNo

Option 1

Member pays provider with

own OOP funds

Member pays provider with

own OOP funds

Option 2 Option 3

Provider submits claim

to Capital

Provider submits claim

to Capital

Member goes to the doctor‘s office

for service and pays copay at time

of service

Member goes to the doctor‘s office

for service and pays copay at time

of service

Capital determines if

deductible met

Capital determines if

deductible met

17

Single contract with PPO 1500Q…

SimplySelect Scenario 1

Single with minimal needs...

HSA -YEAR ONE HSA -YEAR TWO

Your employer contribution

$750HSA

Account Balance $1,750

Roll over from year 1 $787

HSA Account Balance$2,037

Your contribution $1000

Your employer contribution

+$750

Your contributionStarting balance

+$500You see your doctor for your annual physical

-$25 copay

$1,725

A minor hiking accident sends you to the emergency room

-$638 $1,087 See your doctor for a cold

-$85 $1,952

Monthly prescription filled @ $25/mo

-$300 $787 You fill a prescription for antibiotics and purchase some OTC cold medicine

-$76 $1,876

HSA balance at the end of year one

$787 Monthly prescription filled @ $25/mo

-$300 $1,576

HSA balance at the end of year two

$1,576

Costs and expenses are for example purposes only.

18

Family contract with PPO 1500Q (a $3,000 family deductible)…

SimplySelect Scenario 2

Family of seven with many needs...

HSA -YEAR ONE HSA -YEAR TWOYour employer contribution $1,500

HSA Account Balance $2,500

Roll-over $1,583

HSA Account Balance $4,083

Your contribution $1,000 Your employer contribution $1,500

Family receives annual physicals - $25 copay for each person- you decide to pay OOP (do not use HSA)

$175 $2,500 Your contribution $1,000

Three kids visit doctor for a case of pink eye ($75)

-$225 $2,275 Family receives annual physicals - $25 copay for each person

-$175 $3,908

Antibiotics for pink eye -$53 $2,222 4th child goes to emergency room after bike accident

-$850 $3,058

Youngest sees a speech therapist

-$125 $2,097 Your husband/wife has their gall bladder removed (Total bill is $4100)

You visit the doctor for the flu -$75 $2,022 You pay out of your HSA to meet your remaining family deductible

-$1,975 $1,083

OTC cold medicine -$18 $2,004 You pay out of your own pocket for coinsurance (0%)

$0 $1,083

Youngest sprains a wrist & visit the ER

-$421 $1,583 Remaining cost of surgery - plan pays 100%

$2,125 $1,083

HSA balance end of year 1 $1,583 Balance end of year 2 $1,083Costs and expenses are for example purposes only.

19

HSA FSA

Who owns it? Employee Employee

Who funds it? Employer and/or Employee Employee

Are there insurance

requirements?

Yes. IRS qualified HDHP None. Employee does not need to participate in the employer's health plan

What is the maximum contribution?

IRS dictates annual limits No legal limit. Employers typically impose a limit from $2500 to $5000

Does the unused money

carry over?

Yes No - 'use it or lose it'

Is it portable? Yes, it belongs in a personal account and the money belongs to the employee

Unused funds must be spent by year-end (or by March 15 of following year if grace period provision is adopted by employer) otherwise individual forfeits

the money

What are the tax benefits?

The employee does not have to claim reimbursement as income. Employee

contributions are pre-tax, and interest earned is tax-free

Contributions to FSA are tax free and reduces annual taxable income

Can funds be used for non-medical expenses?

No, only expenses defined under 213(d) of IRC. If used for other expenses, the funds

are taxed and a 10% penalty is applied. After age 65, no penalty applies

No, health portion of FSA is only used for expenses defined under 213(d) of IRC

Dependent Care expenses eligible?

No Yes, employee can select a separate amount of money to pay for dependent care

HSA vs. FSA Account Comparison

20

ACS|BNY MellonWhere do they fit in?

21

Capital BlueCross partners with ACS|BNY Mellon to provide the savings accounts portion of Capital BlueCross partners with ACS|BNY Mellon to provide the savings accounts portion of your program.your program.

ACS|BNY Mellon Background

ACS|BNY Mellon HSA Solution (“The HSA Solution℠”) is an independent company whose products and services are not BlueCross® products and services. The HSA Solution is solely responsible for these financial services.

Both ACS (Affiliated Computer Services) and BNY (Bank of New York) Mellon are Fortune 500 companies

Largest HSA administrator in the country with 800,000+ total accounts

Dedicated customer service that specializes in HSAs

Simple, easy-to-use online tools for groups & members

Access to account information 24/7

22

Access to online enrollment, estimator tools, educational materials and account information 24/7.

Web site & Tools

23

TransactionAccount

InvestmentAccount

Make the most of your money and manage it online - day or night.

Investments

FDIC Insured

Ready access to funds via checkbook or debit card

Balances & transaction info available via IVR

$1,500 minimum to invest

20+ highly-rated funds from multiple fund families Automatic investing No minimum for investments No transaction fees All options are no-load or load-waived mutual funds

24

NOTE: You can use your debit card to pay copays during an office visit, but let the provider submit your medical claim so Capital discounts can be applied - There is no need to inform your provider that you have an HSA.

How do I get money out?

Write a check! -- No manual claim forms or receipts need to be submitted

Signature card in your welcome kit must be signed and returned for checkbooks to be issued

Your first 40 checks are free, additional checkbooks are $5

A signature based card or pin based

You cannot use card at ATM’s to withdraw funds

Your card is automatically issued when the account is opened

Your first card is free, additional cards are $5 each

DEBIT CARD CHECKBOOK

Distributions & Reimbursement

25

If you have medical or Rx questions on the QHDHP call the Capital BlueCross customer service number on the back of your ID card

If you have specific HSA questions, Capital BlueCross customer service will transfer you to ACS|BNY Mellon or call the dedicated line directly at 866-274-2194

One phone call does it all...One phone call does it all...

What if I have a question…

26

• $15 one time set-up fee

• 1st debit card is free, additional cards are $5

• 1st checkbook (40 checks) is free, additional checkbooks are $5

• $3.50 fee per HSA account per month, waived if average balance is over $1,000

• All dollars in the account over $1,500 can be invested

• Flat monthly fee of $2.90 on invested dollars

Competitive fees in today’s market...Competitive fees in today’s market...

HSA Fees

27

Questions?

28

SimplySelect is offered by Capital Advantage Insurance Company®, a Capital BlueCross subsidiary. Independent licensees of the Blue Cross and Blue Shield

Association.

Communications issued by Capital BlueCross in its capacity as administrator of programs

and Provider relations for all companies.