1 economy - boardsandcommissions.sd.govboardsandcommissions.sd.gov/bcuploads/gcea.102815.pdfthe...

TRANSCRIPT

The State of the SD Economy

Presentation to the Governor’s

Council of Economic Advisors

October 28, 2015

Ralph J. Brown, Professor Emeritus of Economics

University of South Dakota

1

Outline of Presentation

Overview of US economy

US economy forecast

SD economy

Summary & Conclusions

2

US Forecast

Global Insight Forecast – October 9, 2015

Real GDP

Consumption

Housing Starts

Federal Budget

Interest Rates and Inflation

3

GDPGDP growth in the 2nd half of 2015 will be constrained due to large inventory accumulation in the 1st half. GDP growth in 2016 and 2017 will be strong at 2.9% and 3.0%, respectively.Consumption spending will be strong.Business investment and housing will also be strong over the next two years.The strong $ will hold back growth in the foreign sector.

4

Faster Growth 2016 & 20175

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2006 2008 2010 2012 2014 2016

1997-2007 3.0%

GROSS DOMESTIC PRODUCT

Actual Forecast

Source: BEA and IHS

2014 2.4%Forecast2015 2.5%2016 2.9%2017 3.0%

GDP2011Q3=2007Q4

Components of GDP are:

GDP = Consumption (69%)

Investment (17%)

Government (18%)

Net Export (-4%)

6

Consumption

Consumption spending is expected to remain strong through 2017.

Solid job growth, low inflation, strong HH finances, and lower energy prices all support consumer growth.

Auto sales are expected to be strong.

Low import prices will support consumption as well.

7

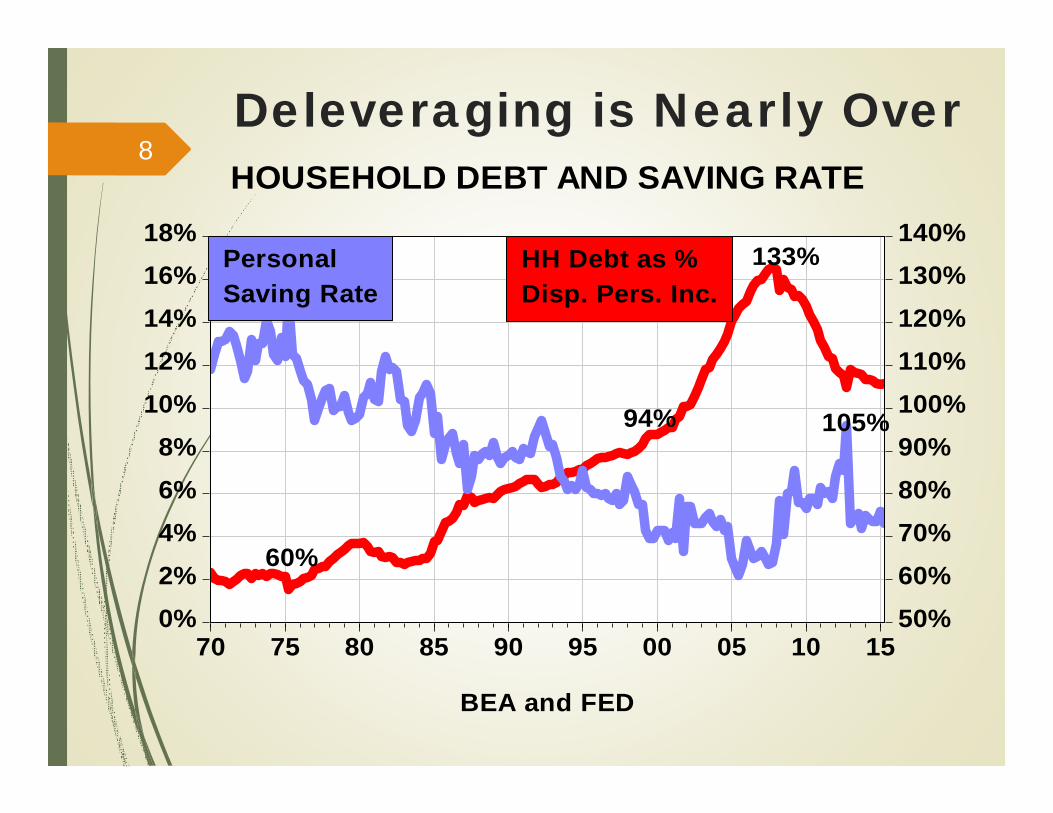

Deleveraging is Nearly Over8

0%2%4%6%8%

10%12%14%16%18%

50%60%70%80%90%100%110%120%130%140%

70 75 80 85 90 95 00 05 10 15

BEA and FED

PersonalSaving Rate

HH Debt as %Disp. Pers. Inc.

133%

105%

60%

94%

HOUSEHOLD DEBT AND SAVING RATE

Good Growth9

-6%

-4%

-2%

0%

2%

4%

6%

-6%

-4%

-2%

0%

2%

4%

6%

2006 2008 2010 2012 2014 2016

Actual Forecast

REAL CONSUMPTION

Source: BEA and IHS

1997-2007 3.6%

2014 2.7%Forecast2015 3.0%2016 3.1%2017 2.9%

Investment Sector

In the energy sector, it looks like the drilling rig count will continue to be negative and bottom out next year.

Housing starts will be strong over the next two years.

Investment in commercial structures is projected for positive growth in 2016 and 2017 after a decline in 2015.

Spending on equipment is projected for good growth in 2016 and 2017.

10

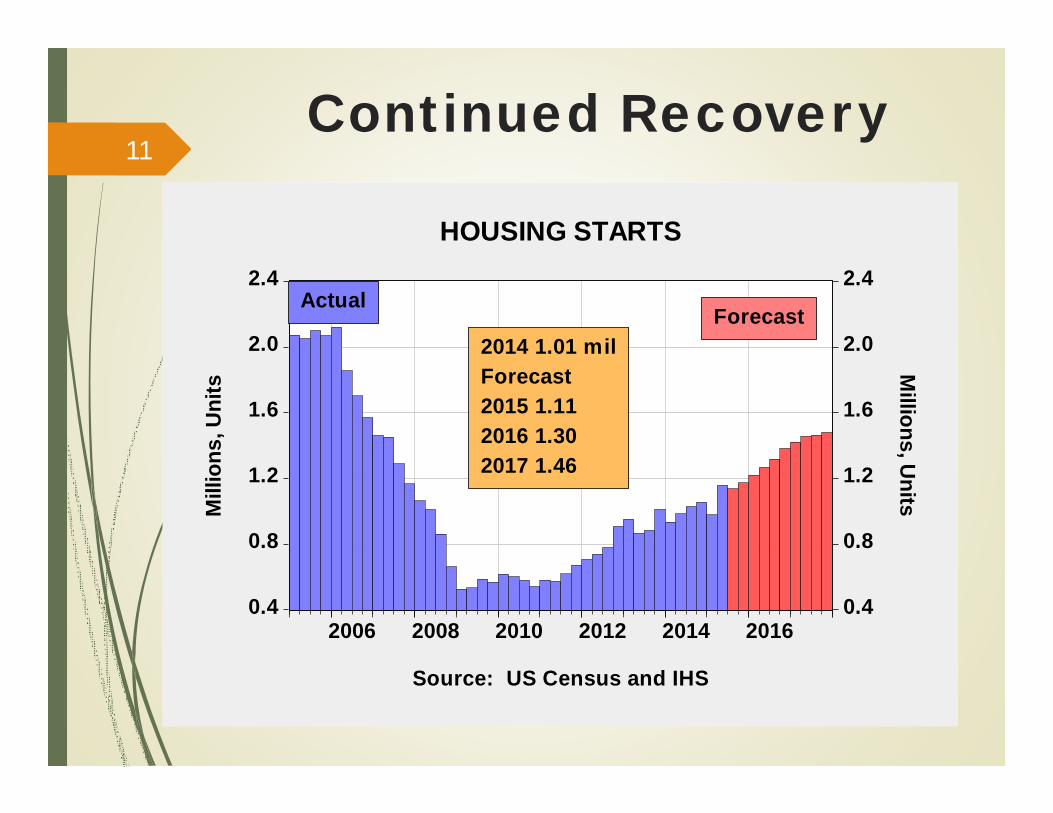

Continued Recovery 11

0.4

0.8

1.2

1.6

2.0

2.4

0.4

0.8

1.2

1.6

2.0

2.4

2006 2008 2010 2012 2014 2016

ActualForecast

2014 1.01 milForecast2015 1.112016 1.302017 1.46

HOUSING STARTS

Source: US Census and IHS

Mill

ions

, Uni

ts

Millions, U

nits

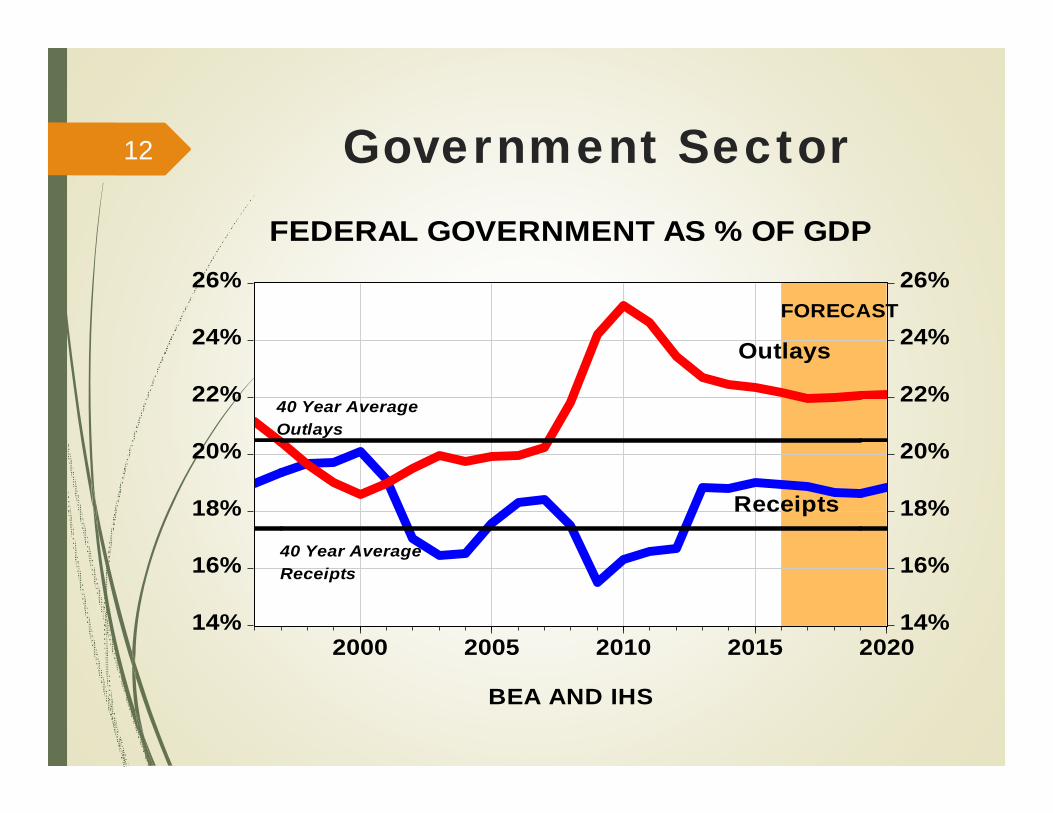

Government Sector12

14%

16%

18%

20%

22%

24%

26%

14%

16%

18%

20%

22%

24%

26%

2000 2005 2010 2015 2020

Receipts

Outlays

40 Year AverageReceipts

40 Year AverageOutlays

FEDERAL GOVERNMENT AS % OF GDP

BEA AND IHS

FORECAST

Debt Held by Public13

30%

40%

50%

60%

70%

80%

30%

40%

50%

60%

70%

80%

00 02 04 06 08 10 12 14 16 18 20

FEDERAL DEBT HELD BY PUBLIC AS % OF GDP

FORECAST

Source: IHS

Debt held by ind, corp, s&l govtforeigners, and Fed Res Syst

The balance ownedby intergovt holdingssuch as Soc Sec

Foreigners holdabout 47% ofpublicly helddebt

Foreign Sector

$ at highest level since 2003 and will continue to be strong through the first half of 2016.

China is no longer the locomotive leading the growth in Asian countries and commodity-exporting countries.

China is undergoing a series of transitions (external to internal demand, rural to urban, industry to services, and fixed investment to consumption).

The US is one of the bright spots in the world economy.

14

Last Month Only 142K15

-1,000

-800

-600

-400

-200

0

200

400

600

-1,000

-800

-600

-400

-200

0

200

400

600

05 06 07 08 09 10 11 12 13 14 15

NONFARM EMPLOYMENT

P to T-8.7 mil-6.3%

Back to PMay 2014

+229,000 mth avglast 12 monthsch

ange

in th

ousa

nds change in thousands

Source: BLS

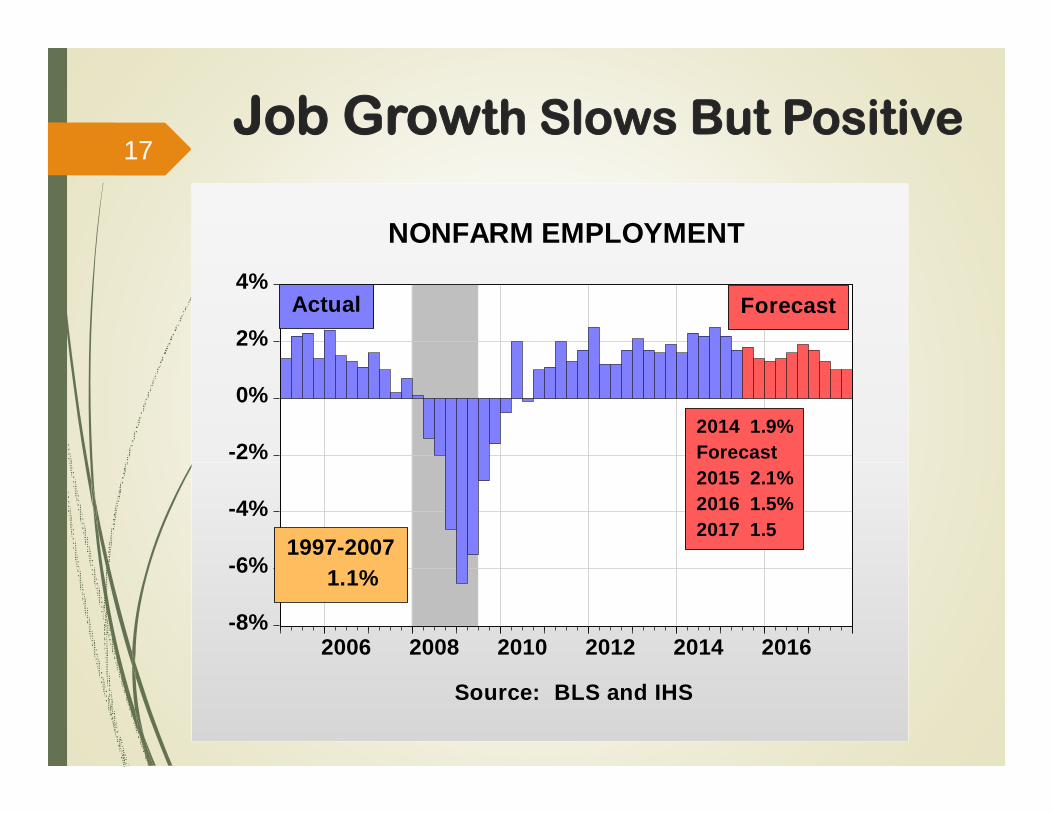

Employment & Unemployment

After a year of job growth of more than 200,000 per month, there is some evidence that the job market is losing momentum.

Unemployment rate will average 5.3% in 2015 and 5.0% in 2016 and 4.9% in 2017.

Yet, the labor force participation rate is at a 38 year low and wage growth is sluggish.

16

Job Growth Slows But Positive17

-8%

-6%

-4%

-2%

0%

2%

4%

2006 2008 2010 2012 2014 2016

NONFARM EMPLOYMENT

Source: BLS and IHS

Actual Forecast

1997-2007 1.1%

2014 1.9%Forecast2015 2.1%2016 1.5%2017 1.5

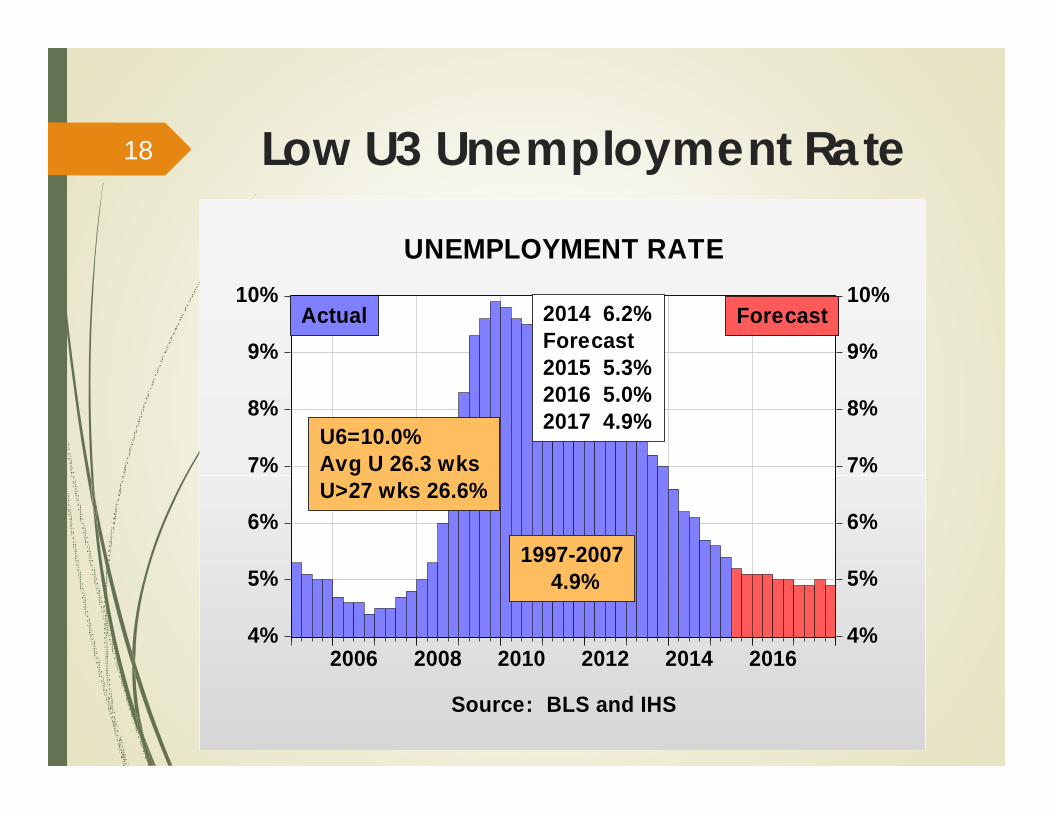

Low U3 Unemployment Rate

4%

5%

6%

7%

8%

9%

10%

4%

5%

6%

7%

8%

9%

10%

2006 2008 2010 2012 2014 2016

Actual Forecast

UNEMPLOYMENT RATE

Source: BLS and IHS

1997-2007 4.9%

U6=10.0%Avg U 26.3 wksU>27 wks 26.6%

2014 6.2%Forecast2015 5.3%2016 5.0%2017 4.9%

18

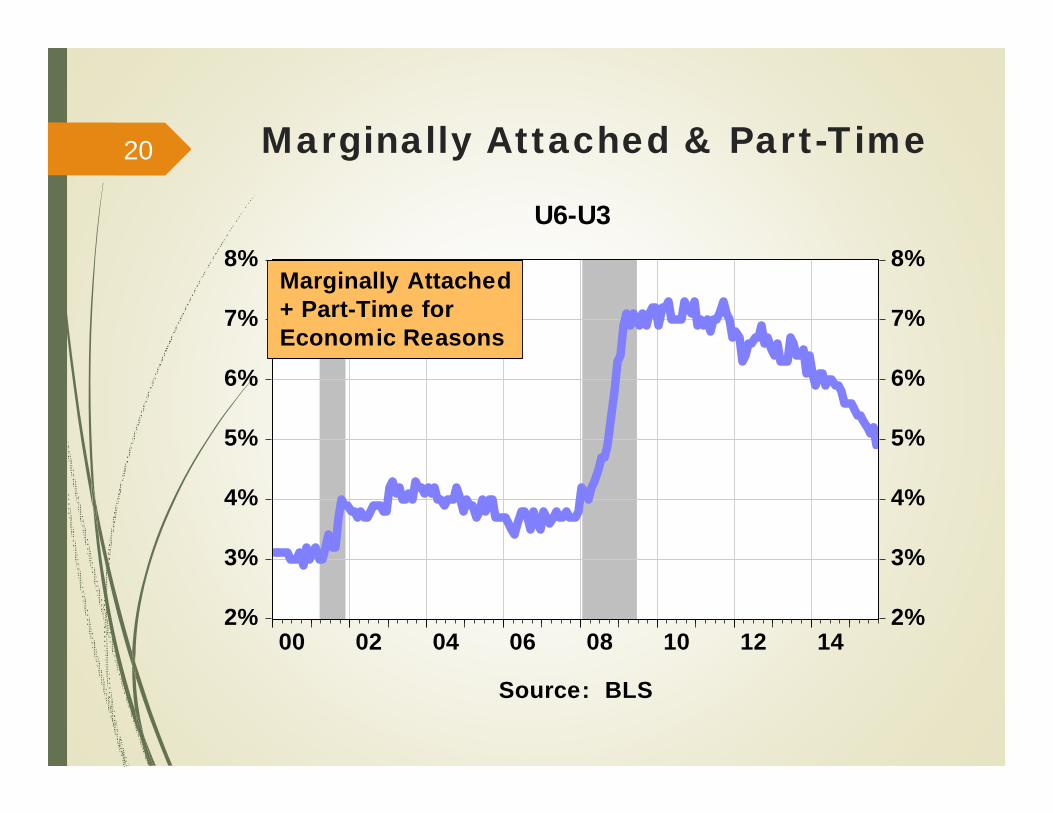

U3 & U6 Unemployment Rates19

2%

4%

6%

8%

10%

12%

14%

16%

18%

2%

4%

6%

8%

10%

12%

14%

16%

18%

00 02 04 06 08 10 12 14

Unemployment Rates

Source: BLS

U6

U3

U3=Unemployment RateU6=U3+Marginally Attached& Part-Time for Econ. Reasons

Marginally Attached & Part-Time20

2%

3%

4%

5%

6%

7%

8%

2%

3%

4%

5%

6%

7%

8%

00 02 04 06 08 10 12 14

U6-U3

Source: BLS

Marginally Attached+ Part-Time forEconomic Reasons

US & SD U6 21

6%

8%

10%

12%

14%

16%

18%

6%

8%

10%

12%

14%

16%

18%

2009 2010 2011 2012 2013 2014

US AND SD U6UNEMPLOYMENT RATE

Source: BLS

US

SD

Inflation & Interest Rates

Low energy prices and the strong $ keep inflation under control and well below FED’s 2% target.

Weak international sector and financial market volatility is the reason FED did not raise rates in September.

IHS expects FED to begin raising rates in December 2015. Greater than 50/50.

If the job market loses more momentum and/or a govt shutdown, December rate rise could be delayed again.

22

Still Very Low23

-12%

-8%

-4%

0%

4%

8%

2006 2008 2010 2012 2014 2016

INFLATION: CPI

Source: BLS and IHS

ForecastActual

1997-2007 2.6%

2014 1.6%Forecast2015 0.0%2016 1.8%2017 2.4%

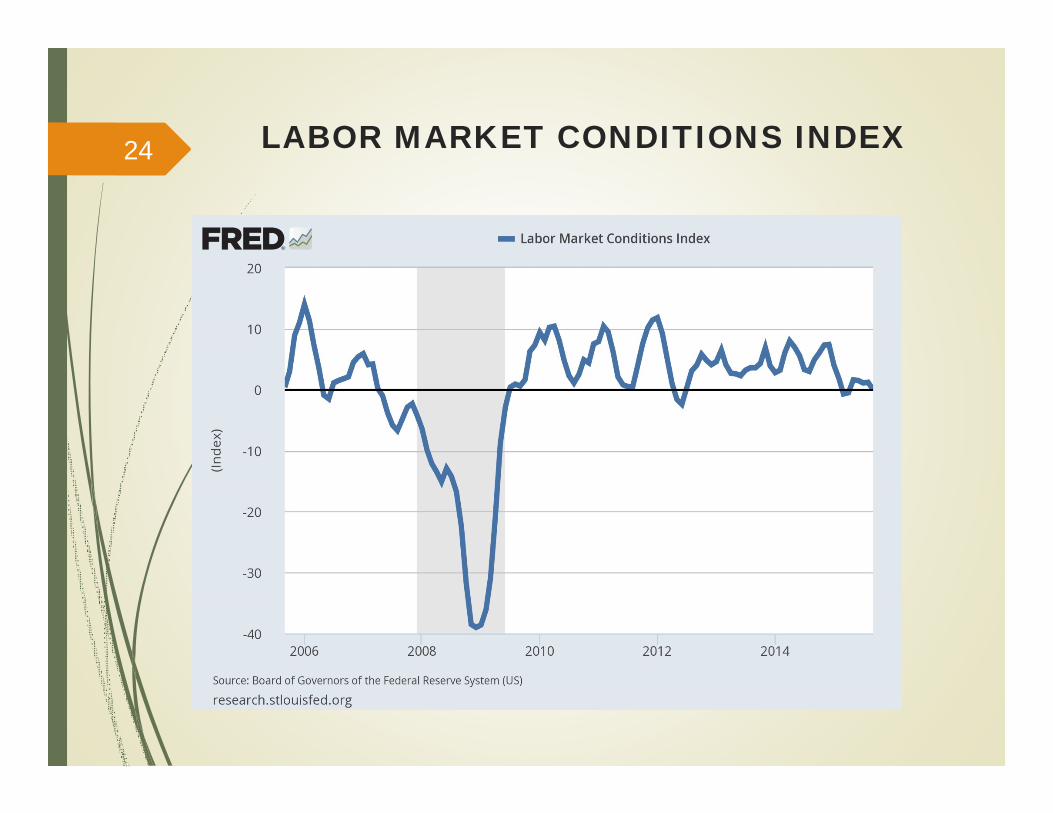

LABOR MARKET CONDITIONS INDEX24

PERSONAL CONSUMPTION EXPENDITURESDEFLATOR LESS FOOD AND ENERGY25

IHS GLOBAL INSIGHT FORECAST 2/6/14

Variable 2014 2015 2016 2017 GDP 2.4% 2.5 % 2.9% 3.0%

NA Emp 1.9% 2.1% 1.5% 1.5%

Oil(Brent) $100 $54 $55 $63

Housing 1.01 1.11 1.30 1.46

CPI 1.6% 0.0% 1.8% 2.4%

Un Rate 6.2% 5.3% 5.0% 4.9%

IHS GLOBAL INSIGHT FORECAST October 201526

Risks to Forecast

20% chance of recession.Risks are:Slowing growth of developing economies

because of low commodity prices.The international weakness causes risk-

averse investors to seek security in US assets driving up the value of the $.

Then US economy slows causing a sharp drop in the stock market. By 2nd qtr of 2016 the S&P 500 down 24% year-over-year.

Consumer confidence drops, etc. etc.

27

Key Variables Tracking SD Economy

Nonfarm employment

Housing starts

Real nonfarm personal income

Taxable sales

Leading indicator

28

Steady Growth29

144,000

140,000

136,000

132,000

128,000

440

430

420

410

400

390

380

05 06 07 08 09 10 11 12 13 14 15

Thou

sand

s Thousands

Source: BLS

NONFARM EMPLOYMENT

SD

US

RatioScale

Job Loss P to TUS -8.7 mil -6.3%SD -12.7 thous -3.1%

SD RecessionBegins =>

2014 M04

2012 MO2

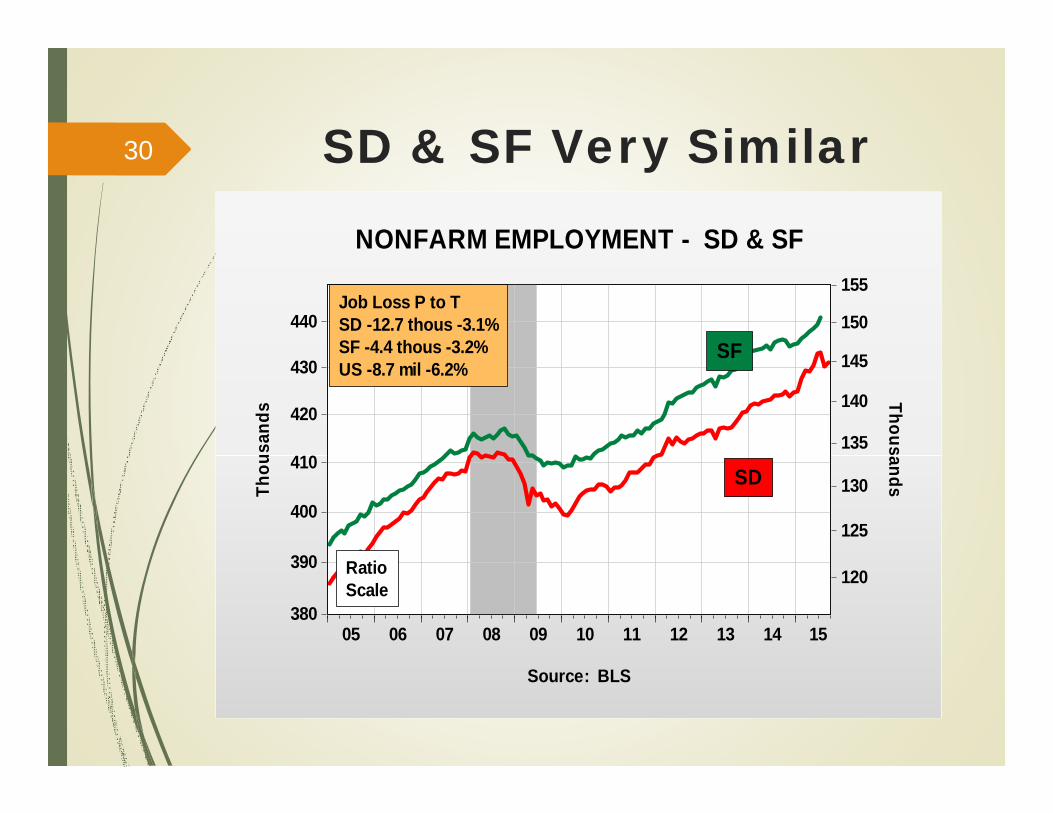

SD & SF Very Similar30

440

430

420

410

400

390

380

155

150

145

140

135

130

125

120

05 06 07 08 09 10 11 12 13 14 15

RatioScale

Thou

sand

s Thousands

Source: BLS

NONFARM EMPLOYMENT - SD & SF

SD

SF

Job Loss P to TSD -12.7 thous -3.1%SF -4.4 thous -3.2%US -8.7 mil -6.2%

Recovery – Almost Back31

8,0007,5007,0006,5006,000

5,500

5,000

25

24

23

22

21

20

05 06 07 08 09 10 11 12 13 14 15

Thou

sand

s Thousands

RatioScale

SD

US

Source: BLS

CONSTRUCTION EMPLOYMENT

P to TUS -29%SD -16%

Which is More Cyclical?32

72

68

64

60

56

370

360

350

340

330

320

05 06 07 08 09 10 11 12 13 14 15

Service EmploymentRight Scale==>

RatioScale

Goods Employment<==Left Scale

Thou

sand

s Thousands

SOUTH DAKOTA SERVICE AND GOODSPRODUCING EMPLOYMENT

Source: BLS

Goods-Producing = Manufacturing+Construction

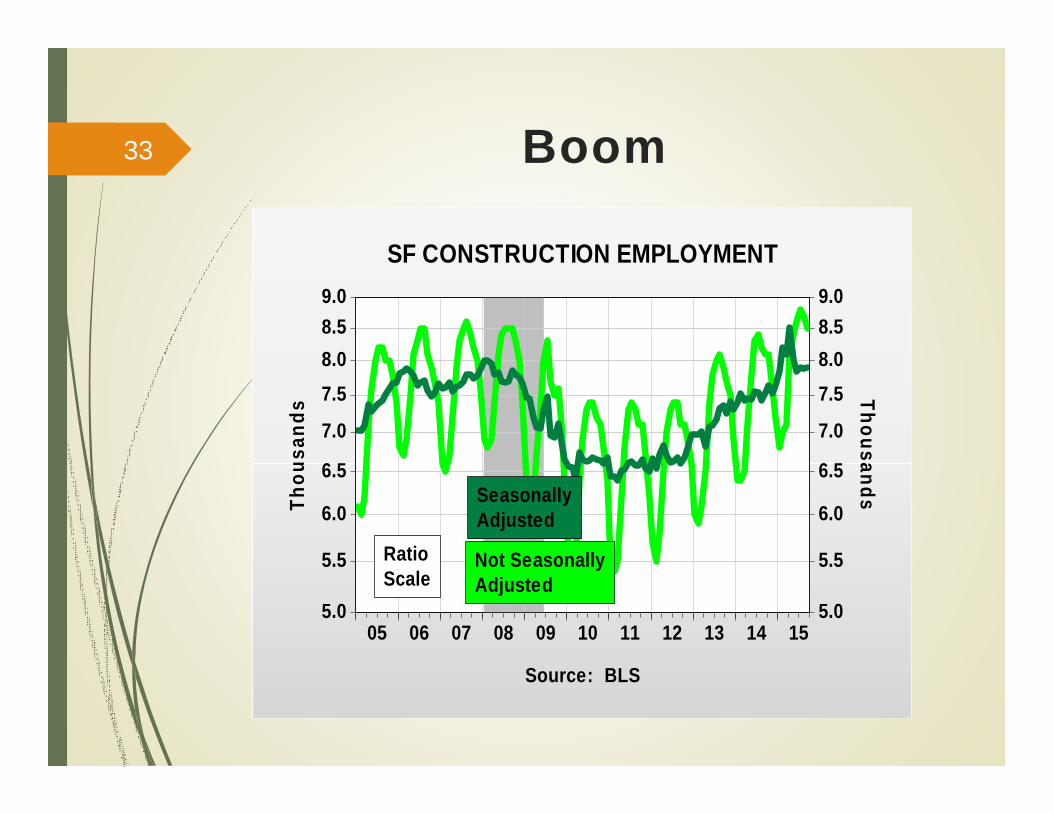

Boom33

9.08.58.07.5

7.0

6.5

6.0

5.5

5.0

9.08.58.07.5

7.0

6.5

6.0

5.5

5.005 06 07 08 09 10 11 12 13 14 15

Thou

sand

s

Source: BLS

Thousands

SF CONSTRUCTION EMPLOYMENT

RatioScale

SeasonallyAdjusted

Not SeasonallyAdjusted

Not Quite Back to Peak34

0100200300400500600700800900

0100200300400500600700800900

05 06 07 08 09 10 11 12 13 14 15

Total, SD

Single, SD

Uni

tsSD Building Permits, Total & Single

12 Month Moving Average

Source: Census Bureau

Booming35

0

100

200

300

400

500

05 06 07 08 09 10 11 12 13 14 15

SF Total

SF Single

12 MonthMoving Avg

12 MonthMoving Avg

Sioux Falls Building Permits

Source: US Census Bureau

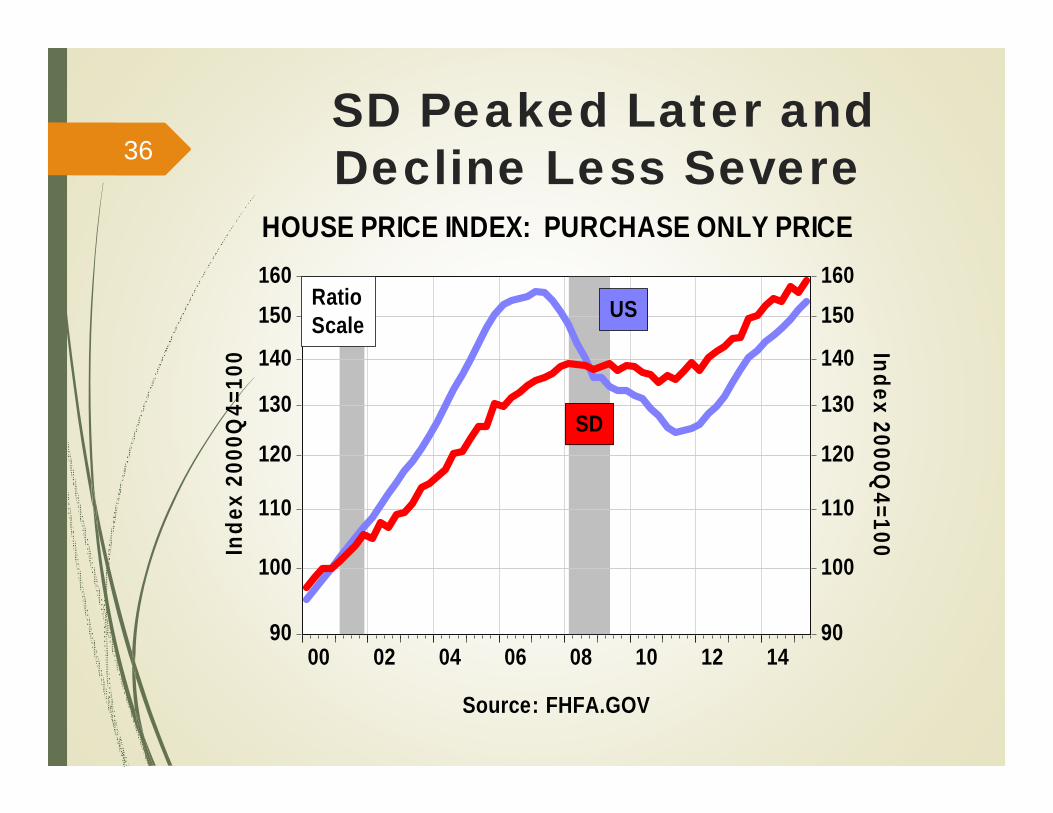

SD Peaked Later and Decline Less Severe36

160150

140

130

120

110

100

90

160150

140

130

120

110

100

9000 02 04 06 08 10 12 14

RatioScale

US

SD

Inde

x 20

00Q

4=10

0 Index2000Q

4=100

HOUSE PRICE INDEX: PURCHASE ONLY PRICE

Source: FHFA.GOV

Mfg Above Peak Fin Not

14,50014,00013,50013,00012,50012,00011,50011,000

4644

42

40

38

36

05 06 07 08 09 10 11 12 13 14 15

MANUFACTURING EMPLOYMENTTh

ousa

nds Thousands

Source: BLS

RatioScale

SD

USSince 12/2007US -13.1%SD -4.8%

MFG %US 8.9%SD 9.4%SF 9.3%

37

SD Not Back to Peak

8,400

8,200

8,000

7,800

7,600

17.216.816.416.015.615.214.8

05 06 07 08 09 10 11 12 13 14 15

SD

USRatioScale

Source: BLS

Thou

sand

s Thousands

FINANCIAL ACTIVITY EMPLOYMENT

P to TUS -8.5%SD -13.0%

Fin %US 5.8%SD 6.7%SF 10.6%

38

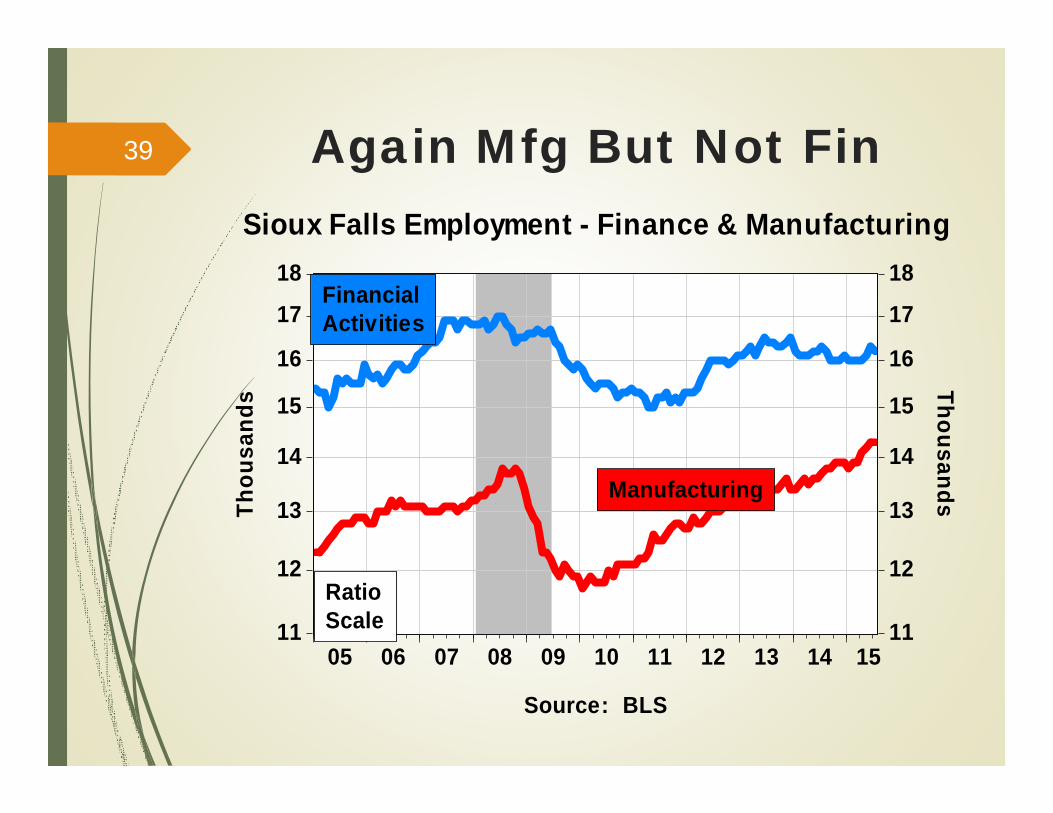

Again Mfg But Not Fin39

18

17

16

15

14

13

12

11

18

17

16

15

14

13

12

1105 06 07 08 09 10 11 12 13 14 15

Thou

sand

s Thousands

RatioScale

FinancialActivities

Manufacturing

Sioux Falls Employment - Finance & Manufacturing

Source: BLS

SD 3.5% SF(SA) 2.7%40

2%3%4%5%6%7%8%9%

10%11%

2%3%4%5%6%7%8%9%10%11%

05 06 07 08 09 10 11 12 13 14 15

UNEMPLOYMENT RATE

U6 (US)=10.0%U6 (SD)= 6.7%

Source: BLS

US

SD

SF

1997-2007US 4.9%SD 3.2%SF 2.5%

SD Smaller Decline – Way Above Previous Peak41

$14,000

$13,500

$13,000

$12,500

$12,000

$11,500

$11,000

$36

$34

$32

$30

$28

$26

05 06 07 08 09 10 11 12 13 14 15

RatioScale

Bill

ions

Billions

Source: BLS

NONFARM PERSONAL INCOME (2009 $S)

SD

US

P to TUS -2.8%SD -1.1%

US and SD Track42

-6%

-4%

-2%

0%

2%

4%

6%

8%

00 02 04 06 08 10 12 14

SD

US

REAL NONFARM PERSONAL INCOME(Year-Over-Year Percent Change)

Souce: BEA

High Prodn Low Prices Low Prices

43

$40

$60

$80

$100

$120

$140

$0

$1

$2

$3

$4

$5

05 06 07 08 09 10 11 12 13 14 15

Bill

ions

Billions

SD

US

Source: BEA

FARM INCOME

5 Year Avg% of PIUS = 0.7%SD = 8.6%

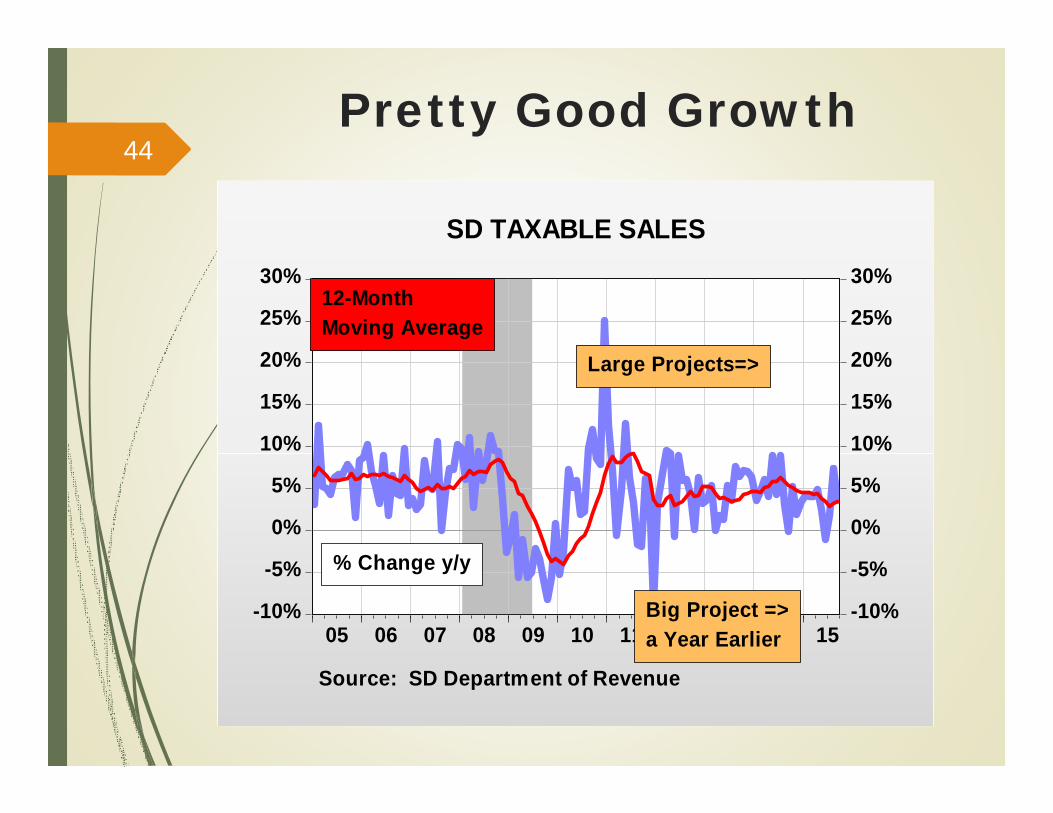

Pretty Good Growth44

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

05 06 07 08 09 10 11 12 13 14 15

Large Projects=>

% Change y/y

12-MonthMoving Average

SD TAXABLE SALES

Source: SD Department of Revenue

Big Project =>a Year Earlier

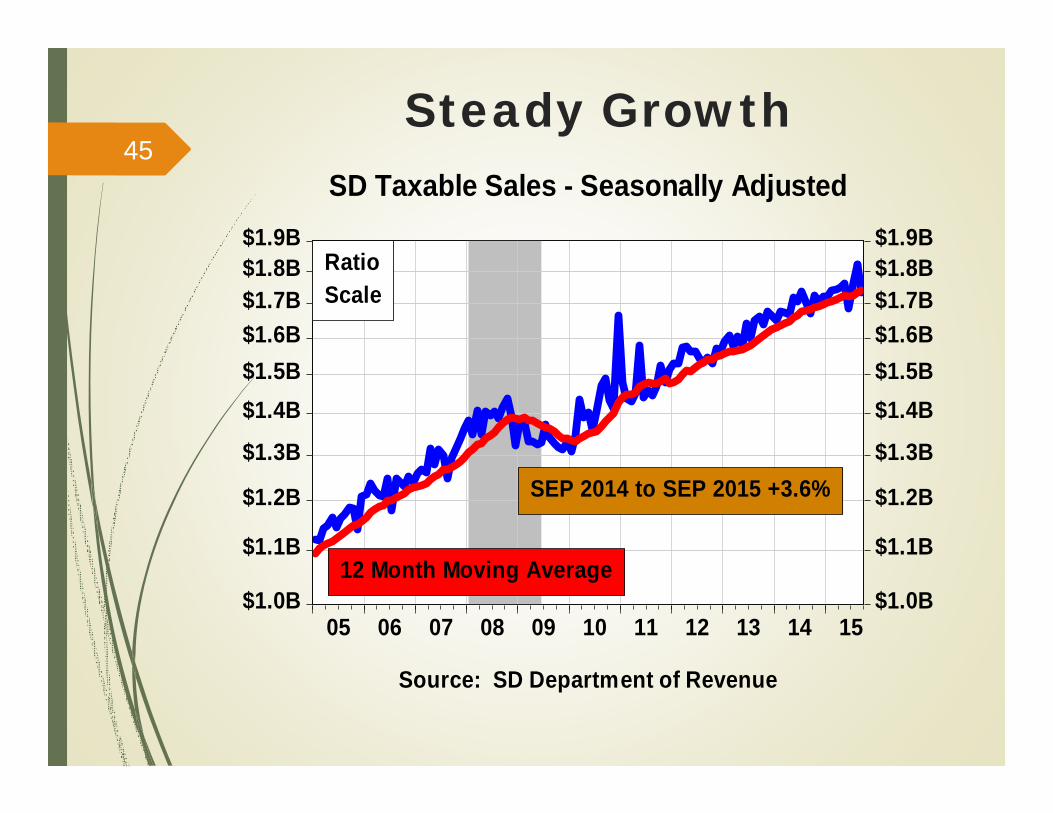

Steady Growth45

$1.9B$1.8B$1.7B$1.6B$1.5B$1.4B

$1.3B

$1.2B

$1.1B

$1.0B

$1.9B$1.8B$1.7B$1.6B$1.5B$1.4B

$1.3B

$1.2B

$1.1B

$1.0B05 06 07 08 09 10 11 12 13 14 15

RatioScale

SD Taxable Sales - Seasonally Adjusted

Source: SD Department of Revenue

12 Month Moving Average

SEP 2014 to SEP 2015 +3.6%

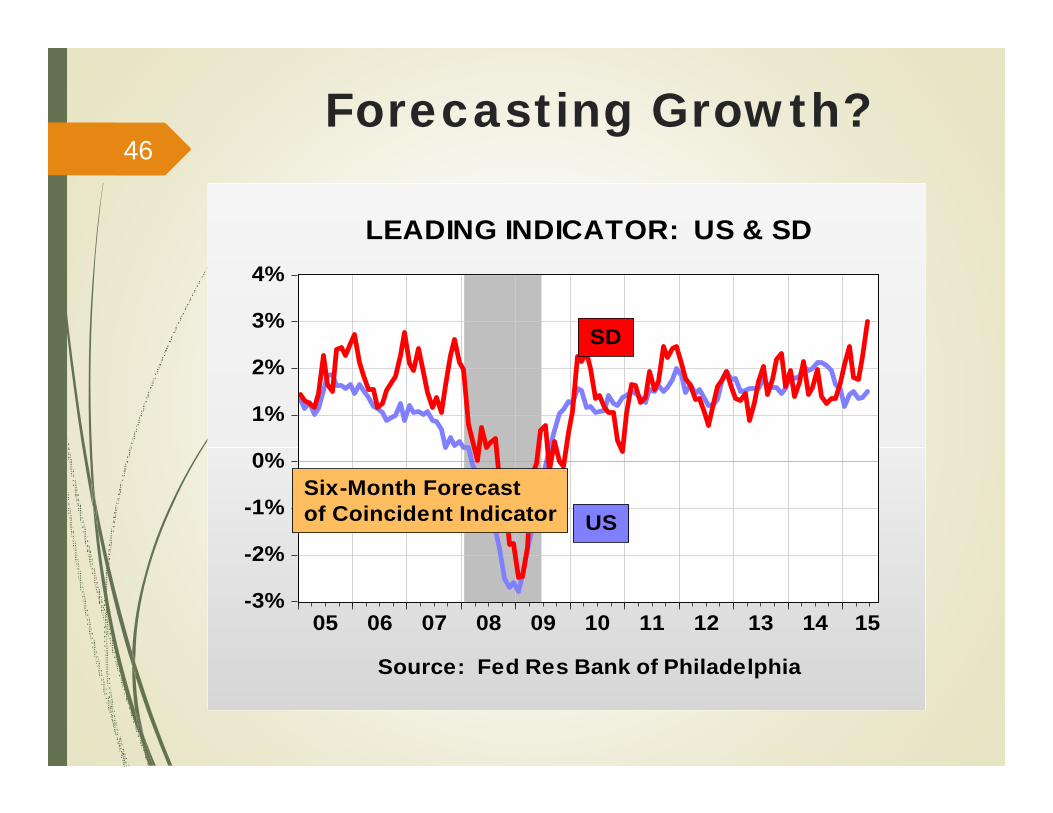

Forecasting Growth?46

-3%

-2%

-1%

0%

1%

2%

3%

4%

05 06 07 08 09 10 11 12 13 14 15

SD

US

LEADING INDICATOR: US & SD

Source: Fed Res Bank of Philadelphia

Six-Month Forecastof Coincident Indicator

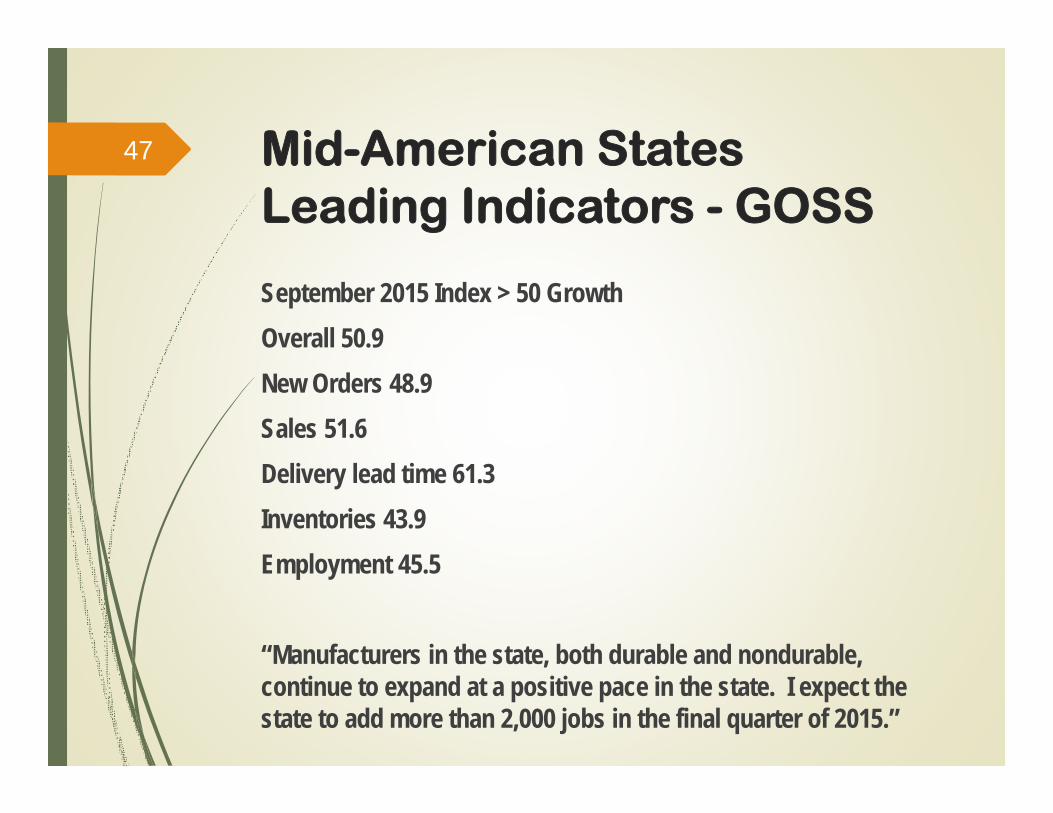

Mid-American States Leading Indicators - GOSS

September 2015 Index > 50 GrowthOverall 50.9New Orders 48.9Sales 51.6Delivery lead time 61.3Inventories 43.9Employment 45.5

“Manufacturers in the state, both durable and nondurable, continue to expand at a positive pace in the state. I expect the state to add more than 2,000 jobs in the final quarter of 2015.”

47

PER CAPITA PERSONAL INCOME

48

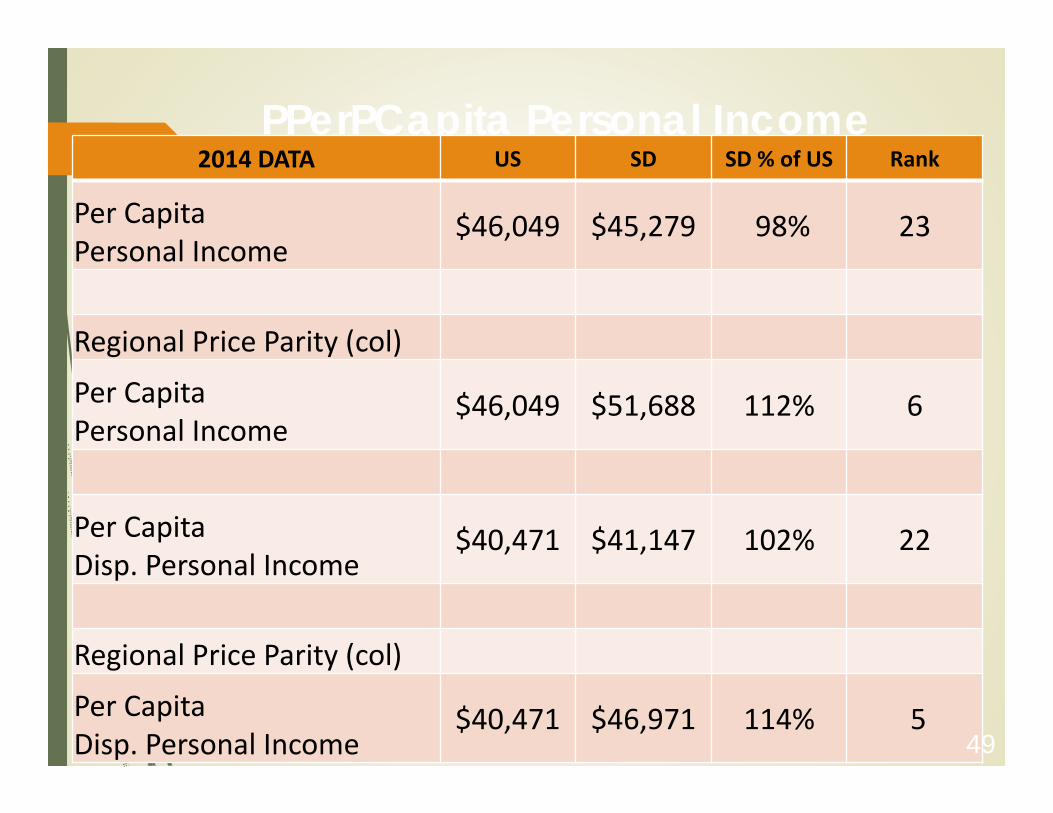

PPerPCapita Personal Income2014 DATA US SD SD % of US Rank

Per Capita Personal Income

$46,049 $45,279 98% 23

Regional Price Parity (col)

Per CapitaPersonal Income

$46,049 $51,688 112% 6

Per Capita Disp. Personal Income

$40,471 $41,147 102% 22

Regional Price Parity (col)

Per Capita Disp. Personal Income

$40,471 $46,971 114% 549

Conclusions

SD economy growing at moderate rate

SF economy growing at faster rate

US economy will speed up

Only 15% chance of recession

50

The End51