1 chapter 8 nonfinancial investments. 2 chapter goals make better choices by recognizing that...

TRANSCRIPT

1

Chapter 8

Nonfinancial Investments

2

Chapter Goals

Make better choices by recognizing that household assets and investment planning is broader than believed.

Differentiate a typical household cost from a capital expenditure.

Become more effective in decision making by employing TPM, the household’s all-asset approach.

Benefit from linking household outlays on durable goods with business capital expenditures.

3

Chapter Goals, cont.

Apply the methods of calculating returns on capital expenditures.

Establish the advantages of owning a home. Determine whether to buy or lease a home or car. Utilize the knowledge that your salary is often your

largest household asset.

4

Defining and Detailing Nonfinancial Assets

Financial assets: Assets in which ownership is represented and traded solely through pieces of paper.

Fully marketable assets: Assets that can be sold currently in a public forum for fair value at low transaction costs.

Nonfinancial assets: All the other assets that the household possesses.

Nonfinancial assets include real assets, human-related assets, and other assets.

5

Defining and Detailing Nonfinancial Assets, cont.

Real assets: Nonfinancial assets that you can see or touch that have market value.

Sometimes real assets are called tangible assets, physical assets, or hard assets.

Real assets can be separated into real estate and durable goods.

Aside from their physical features, real assets differ from financial ones in that real assets generally decline in value over time, with the exception being the home, which, if maintained properly, can appreciate, at least for a relatively long time.

Real assets are generally used in the household currently while financial assets may be reserved for future use.

6

Defining and Detailing Nonfinancial Assets, cont.

Human-related assets: Assets that derive their value from particular people.

In personal finance we are principally concerned with assets in this category that generate income.

People generate income directly through their work efforts, through corporate and government pensions, or through anticipated gifts and bequests.

Human related assets are sometimes called intangible assets.

Other assets is a catch-all category that includes any other assets of worth.

7

Defining and Detailing Nonfinancial Assets, cont.

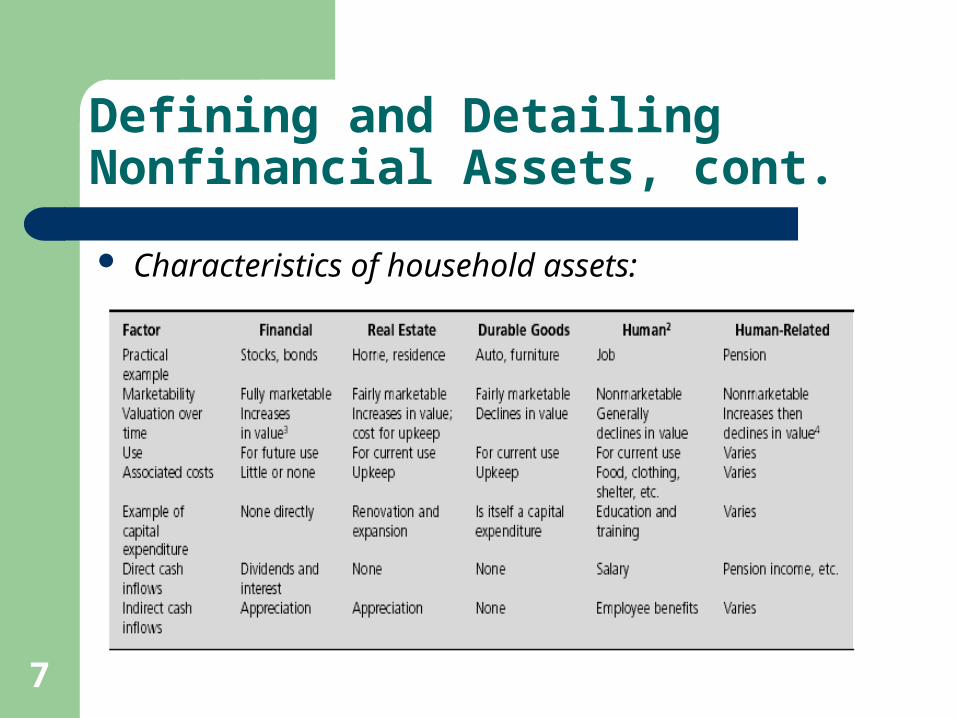

Characteristics of household assets:

8

Defining and Detailing Nonfinancial Assets, cont.

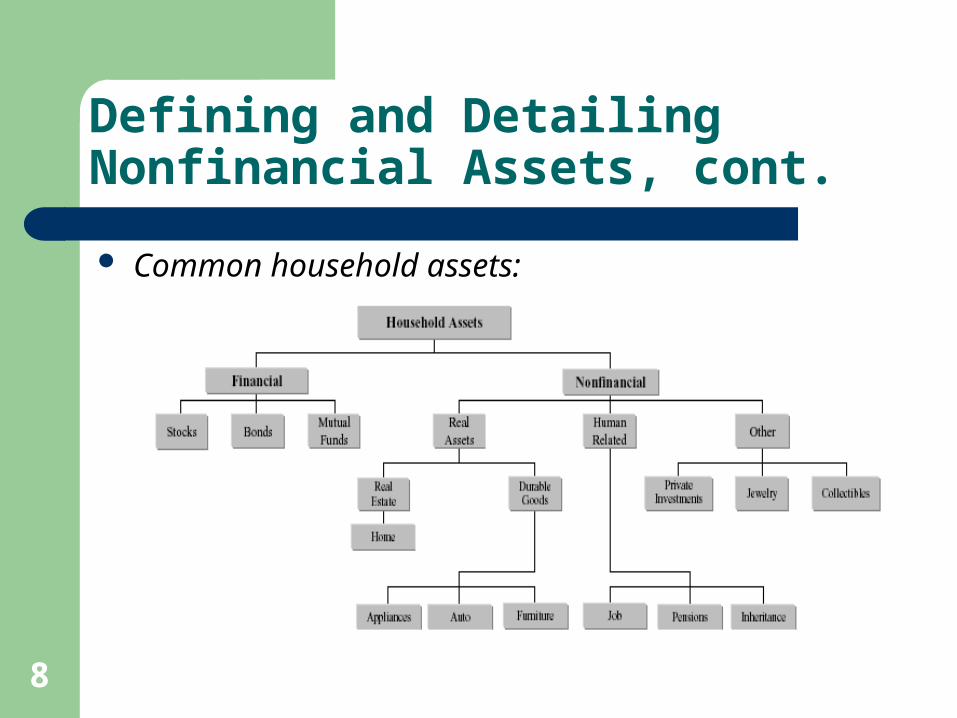

Common household assets:

9

Household Finance and Total Portfolio Management

Household finance looks at the household as one enterprise that resembles a business.

Each of its operations can require investments that can be evaluated from three perspectives.

1. Individual Asset Basis: When looked at by itself, is this asset attractive?

2. Within Activity Basis: How does this proposed expenditure compare with current or future alternatives within the same activity?

3. Fully Integrated Basis: Decisions are not made on a per asset or per activity basis but on an overall household basis.

10

Household Finance and Total Portfolio Management, cont.

Under the fully integrated basis, we perceive that each activity has assets that benefit the household.

These assets can be grouped into financial and nonfinancial categories that form a portfolio of assets, the household portfolio.

The process of developing and maintaining an efficient combination of assets is designated Total Portfolio Management (TPM).

TPM allows us to identify which assets to place in the household portfolio and how to weigh them.

TPM incorporates both risk and return, and sometimes correlations.

11

Making Capital Expenditures Decisions

Capital expenditures: Outlays that provide benefits over an extended period of time.

Capital expenditure is the term used for outlays for real or human-related assets only.

The benefits of capital expenditure may be greater revenues, lower cash cost, less time to produce a desired result, or an immediate increase in satisfaction.

When faced with a variety of capital expenditure alternatives, we decide which to fund using the business capital budgeting techniques, such as Net Present Value (NPV) and Internal Rate of Return (IRR).

12

The Capital Expenditure Process

Review Goals: It is important to place our nonfinancial investments in the context of our overall goals.

Establish Required Rate of Return: Our capital outlays must reach a required rate of return for all projects, based on market figures for savings and investing in financial assets.

Identify Potential Projects. Evaluate Projects: We evaluate the projects using

the costs and returns for each project. We calculate returns using IRR or NPV.

13

The Capital Expenditure Process, cont.

Rank All Projects: We rank within activity, within category, and Total Portfolio. Risk and correlations should be taken into account.

Establish Overall Capital Availability: Taking into account all factors, the amount of capital to be made available is established.

Select and Invest in Final Projects: Some projects are eliminated; others are brought up at a future time as attractiveness and financial resources change.

14

Net Present Value (NPV)

Net Present Value (NPV): The present value of all projected future cash inflows and outflows.

We calculate NPV by discounting all cash flows back to the present at an appropriate discount rate.

This discount rate, designated the required rate of return, is generally equal to the return that can be earned on marketable securities with similar risk characteristics.

If NPV is positive the capital expenditure is preferable to a marketable investment. If NPV is negative, we have not earned the required return and the proposed expenditure is rejected.

15

Net Present Value (NPV), cont.

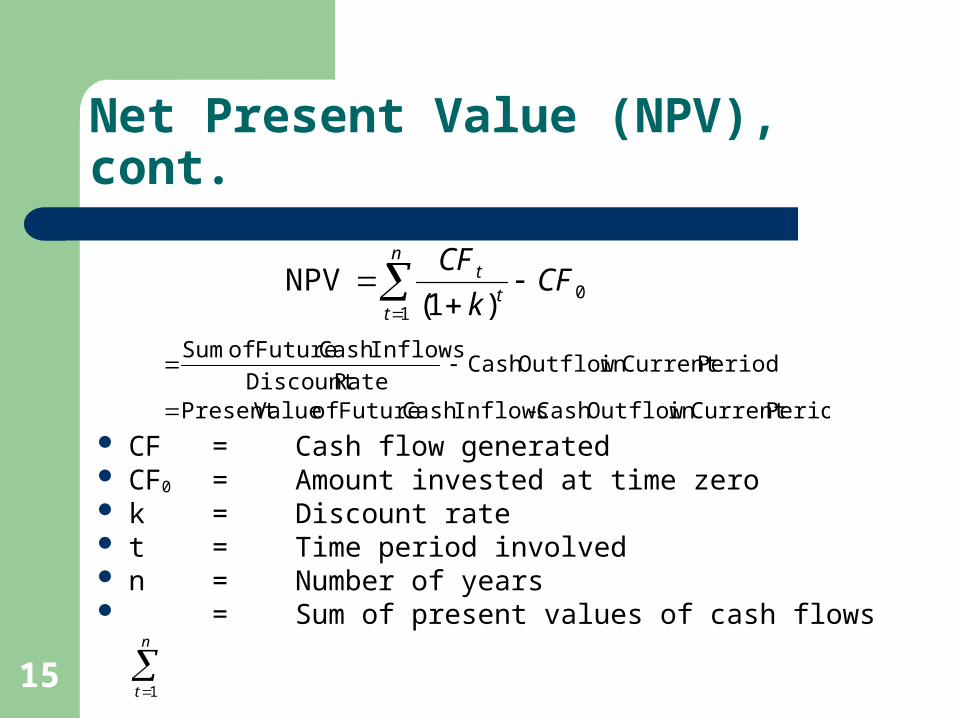

CF = Cash flow generated CF0 = Amount invested at time zero k = Discount rate t = Time period involved n = Number of years = Sum of present values of cash flows

01 )1(

NPV CFk

CFn

tt

t

n

t 1

PeriodCurrent in OutflowCash -InflowsCash Future of ValuePresent

PeriodCurrent in OutflowCash RateDiscount

InflowsCash Future of Sum

16

Net Present Value (NPV), cont.

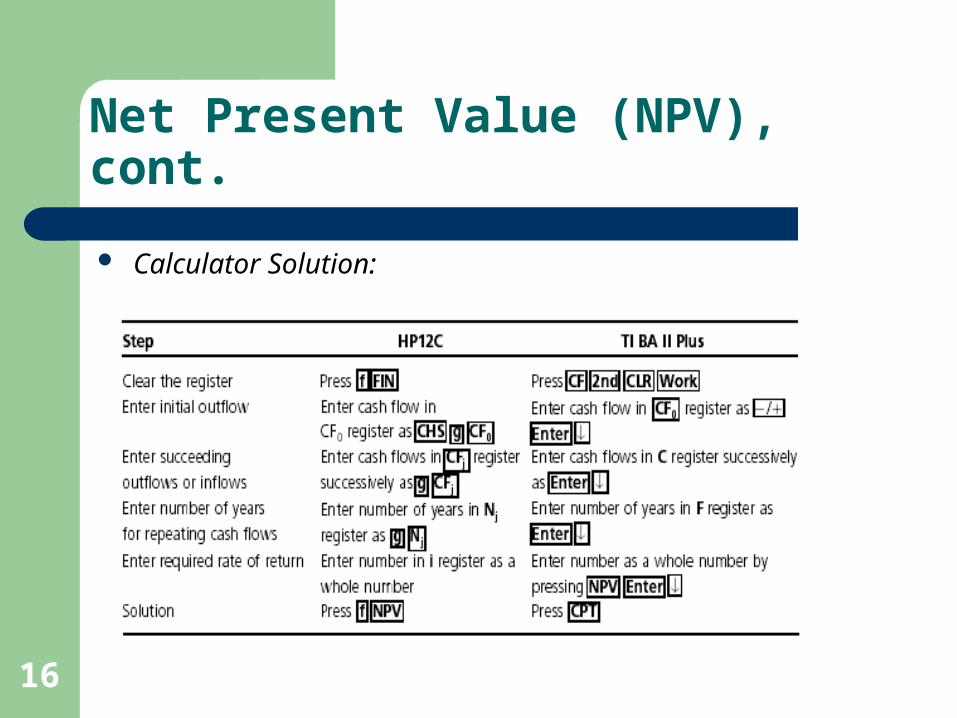

Calculator Solution:

17

Net Present Value (NPV), cont.

To rank investments in terms of attractiveness we can use the profitability index (PI).

Any savings in the opportunity cost of time should be included in calculating the additional cost or benefits for household expenditures as this time used potentially could be employed in developing additional cash flows.

We assign a cash flow figure to the cost of time based on the hourly wage rate that could be received if the time was spent working.

Cost Original

NPV

18

Internal Rate of Return (IRR)

The Internal Rate of Return (IRR): The rate of return that makes the present value of cash inflows equal to that of cash outflows.

The IRR is the discount rate that makes NPV equal to 0.

We compare the IRR with our required rate of return, the return we could get on marketable securities with the same risk.

If the IRR is greater than the required rate of return, we accept it. If it isn’t, we reject the proposed capital outlay.

19

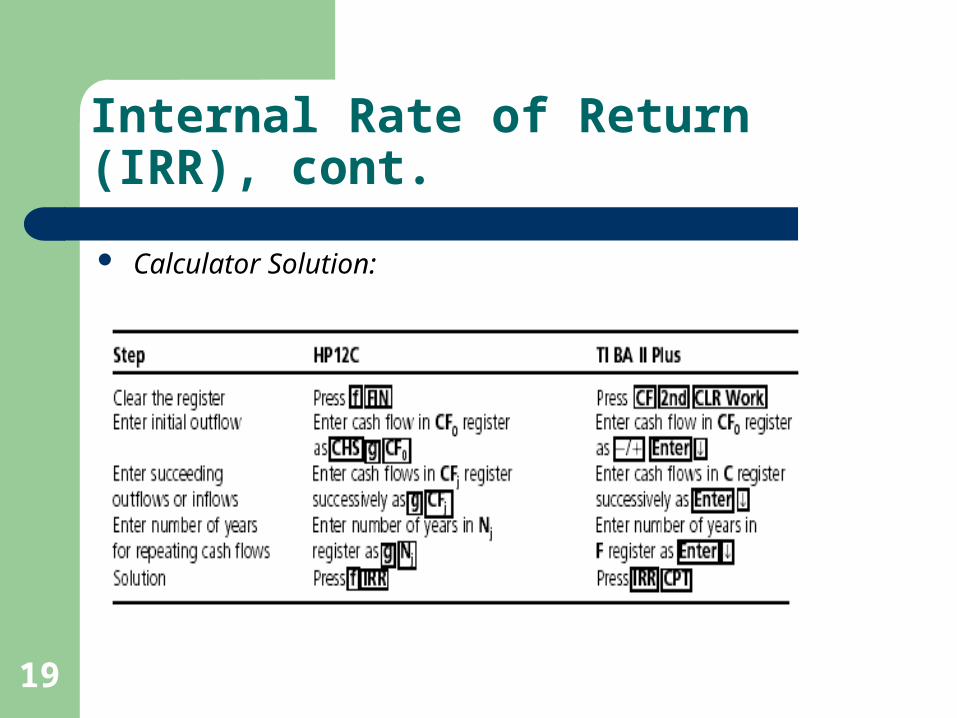

Internal Rate of Return (IRR), cont.

Calculator Solution:

20

Comparison of IRR and NPV Methods

NPV is the purer, more accurate method. However, since IRR is expressed in percentage return

terms, it can be easier to understand and relate to. Moreover, an IRR can compare returns for

expenditures of different amounts and time frames. A major difference in approach is that NPV assumes

that cash flows from projects are invested at the required rate of return while IRR assumes they are reinvested at the rate of return of that particular project.

IRR also gives multiple answers under some circumstances.

21

Durable Goods

Consumer durable goods are capital expenditures that can benefit many types of household operations.

Among the reasons that you would purchase a durable good are:

– To take advantage of a technological improvement.– Physical wear and tear that results in an existing durable

good having reached the end of its useful life. – A change in circumstances.– To provide more pleasure.– To attempt to raise returns on assets.

22

The Automobile

Major factors in deciding to change automobiles:– State of Current Car: The higher the repair bills, the lower the

car’s attractiveness, and the more likely a trade-in will be contemplated.

– Existing Finances: The greater the cash on hand, the more favorable the job and economic outlook, the more likely the trade-in.

– Current Car Promotions: At certain times in the economic cycle the purchase of a new or used car may be particularly attractive.

– Attractiveness of New Car: New cars may have style, safety, or mileage features that purchase.

23

Human Assets

Human assets: the resource that reflects the current value of all our future earnings.

Factors that directly influence a person’s income-earning ability can be simplified as knowledge and skills, with general health used as support for them.

Human assets are a nonmarketable asset that is often rented to an employer for a period of time at an hourly fee or a salary.

Without knowledge and skills human capital can be viewed as a basic commodity with the ability to earn just the minimum wage.

Capital expenditures include formal education and other ways of developing knowledge.

24

Calculating Human Assets

The value of your human assets varies over your life cycle.

If you are a skilled employee, your asset value may actually go up for a time.

As you age, the decline in the number of your earning years generally results in a drop in your human assets over your life cycle.

In effect, human assets depreciate over time. Capital expenditures on human assets are treated

similarly to those for other assets with benefits compared with costs.

25

Housing Features

Unique Physical Characteristics: No two houses are exactly the same.

Long-lasting: Through maintenance and renovation the property’s overall asset value can often be prevented from declining for many years.

Tax Benefits: The government provides tax benefits to owners.

Appreciation Potential: Many properties tend to rise in value over time.

A Fixed Location: A house’s location is significant. Land: Land may fluctuate in value, but over a long

period of time value tends to rise.

26

Housing Uses

Housing Uses: – Provides shelter. – Long-term investment.– Provides pleasure to its occupants.

Because of its benefits and increases in household discretionary income in this country, the rate of home ownership has risen over the past 50 years.

27

Housing Uses, cont.

Home Ownership Rates by Household and Type of Structure:

Source: US Census Bureau, Historical Census of Housing Tables.

Total One-family

detached house Apartments with 5 or more units

Mobile homes One-person households

1950 55.0% 73.0% 4.1% 79.4% 42.1%

1960 61.9% 78.3% 4.6% 88.3% 40.8%

1970 62.9% 81.6% 5.2% 84.5% 42.4%

1980 64.4% 85.6% 10.2% 79.8% 43.5%

1990 64.2% 85.5% 9.6% 79.8% 48.7%

2000 66.2% N/A N/A N/A N/A

2004 69.0% N/A N/A N/A N/A

28

Tax Benefits for a Home

Mortgage interest and property taxes are tax deductible, and appreciation in home value is not taxed until the home is sold.

Upon sale the first $250,000 of gain per person or $500,000 per couple is tax free with amounts over that taxed at capital gains rates.

Capital expenditures on home improvements are added to the purchase price in calculating your basis in the property, which reduces the ultimate gain.

This $250,000 or $500,000 benefit is allowed once every two years for those people who have had their home as their primary residence for any two of the past five years.

29

Traditional Durables vs. House

30

Return on House for Period

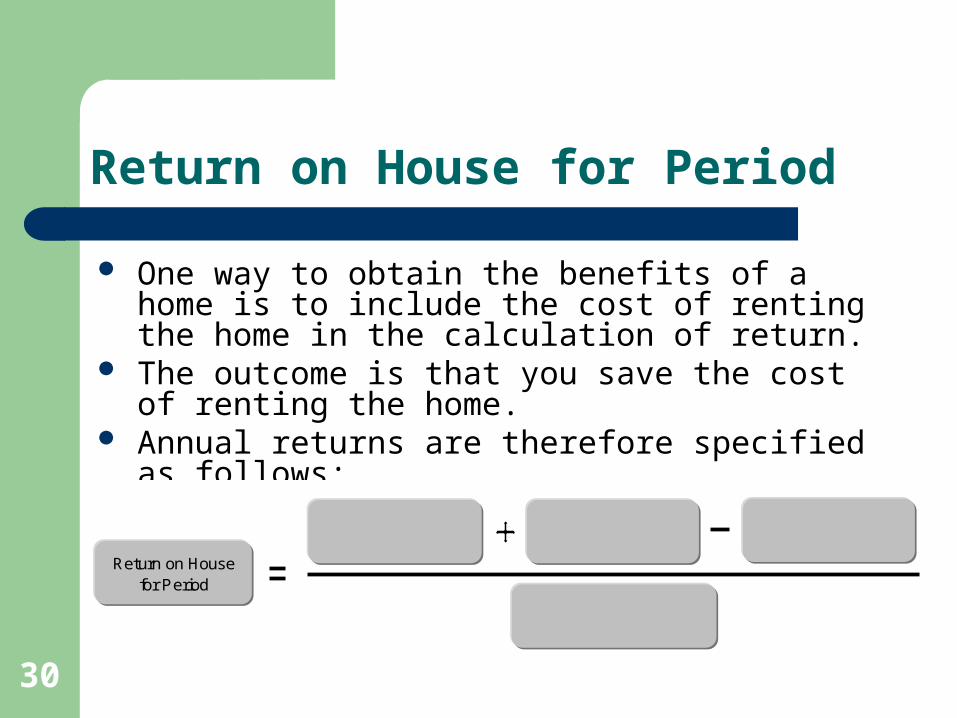

One way to obtain the benefits of a home is to include the cost of renting the home in the calculation of return.

The outcome is that you save the cost of renting the home.

Annual returns are therefore specified as follows:

Return on House for Period

Increase in House Value During Period

Rent Not Paid Cost of Upkeep

Market Value of House Beginning of Period

31

Home Affordability

Factors that influence home affordability include:– Current Income: The more you earn, the larger the home

outlay you should be able to afford.– Tax Bracket: The higher your tax bracket, the greater the

“government subsidy” for tax-deductible real estate taxes and interest expense, the more expensive the home you can buy.

– Liquid Assets and Debt Accumulated: The larger the down payment, the larger the home you can afford since ongoing demands on household cash flow will be lessened. On the other hand, the greater the amount of non-

mortgage debt, outstanding, the lower the overhead costs that can be undertaken through home purchase.

32

Home Affordability, cont.

– Value System: The more important the home, the greater the sacrifice you are willing to make in other areas, and thus the higher priced home you can afford.

– The Local Realities: Homes vary in price in different markets.

– Outlook: The more optimistic you are about your future income situation and about the price appreciation of real estate, the greater the outlay you will be willing to assume.

– Risk Tolerance: The higher your risk tolerance, the greater the mortgage payment you will be willing to assume relative to your available cash flow.

33

An Introduction To Leasing

We tend to purchase durable goods for their benefits for household activities today and for periods in the immediate future.

Owning them does not provide appreciation in those assets as, say, owning stocks would.

Therefore, we often considering leasing assets. A lease is a way to acquire the use of an asset without

purchasing it. The lease allows you to receive the asset's operating

benefits in return for an obligation to make a series of payments over the term of the lease.

The maintenance and overhead costs may be paid by the lessor.

34

Reasons for Leasing

Economic reasons for leasing include:– The lessor may absorb the risk of technological or fashion

obsolescence or large unforeseen expenditures on the asset.

– The lessor is sometimes able to develop efficiencies in specializing in that asset.

– The business owner may receive tax benefits that the lessor will not.

The cost of leasing generally is greater than the cost of purchasing.

The lessor’s administrative cost including the need for profit.

35

Reasons for Leasing, cont.

Leasing may be advisable when the asset is needed for only part of the period.

A common reason for leasing an asset is that households are short of capital. Leases may be offered with no down payment.

Leasing is generally not presented as a liability on the household’s balance sheet, as it often is on the business statement.

Therefore, when the household is short of funds and has limited liability to borrow, leasing may not show up in qualifying for a new loan.

36

Automobile Leasing

Factors to consider when deciding whether to lease or purchase an automobile:– How Long the Car is to Be Held: Depreciation in prices of a car

moderates after the first few years.– The Age of the Car: New cars offer fewer problems and are covered by

warranty. – The Cost of Time: Selling a car that you own involves time and can

expose you to price risk.– Inspection Standards: Lessees must comply with inspection standards

when returning the car– Mileage Charges: Leases contain maximum mileage charges. – Lease Obligation: A lease is made for a fixed period of time– Ability to Fund Monthly Payments: Monthly payments for leasing will be

lower than loan payments. But once your loan payments have been completed, you own the car.

37

Overall Appraisal of the Home as an Investment

Two key factors in making the purchase of a home:– Tax benefit. – Continued growth of the house at around the inflation rate -

and in some cases significantly beyond that rate. Thus, the house provides a hedge against inflation

and returns on the investment when sold. Other factors:

– Pride of ownership.– The forced-savings feature of homes.

38

Overall Appraisal of the Home as an Investment, cont.

The disadvantages of home ownership include: – Its lack of short-term liquidity should immediate sale

become necessary. – The responsibility for maintaining the home and grounds.– The cyclical nature of home prices over shorter periods of

time. On balance, for expected holding periods of, say,

three years or more, owning a home has historically been a highly rewarding investment.

39

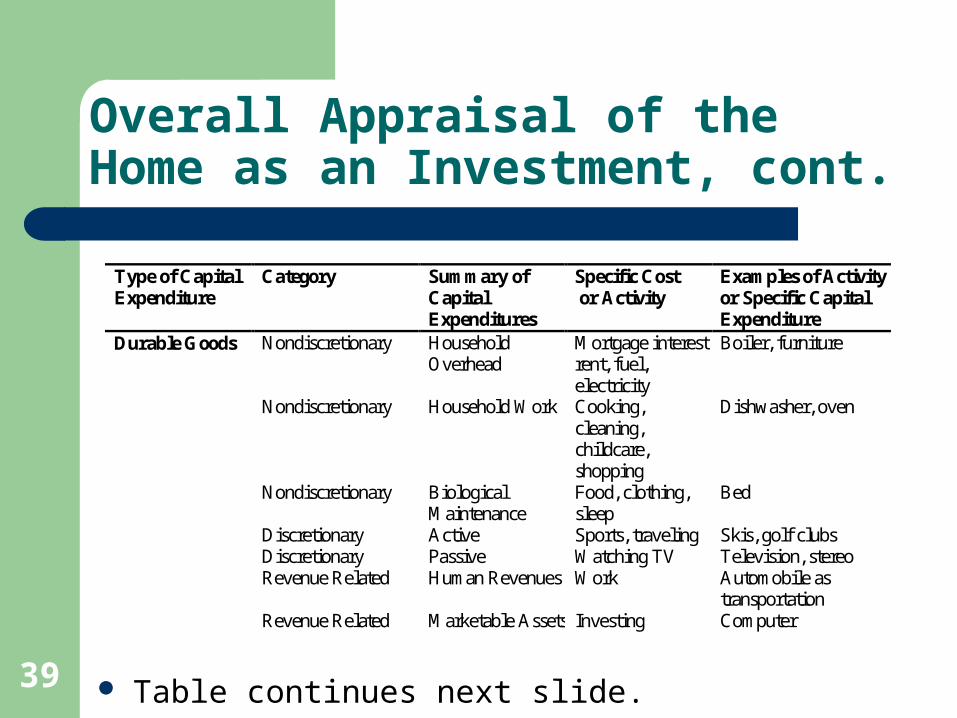

Overall Appraisal of the Home as an Investment, cont.

Table continues next slide.

Type of Capital Expenditure

Category Summary of Capital Expenditures

Specific Cost or Activity

Examples of Activity or Specific Capital Expenditure

Durable Goods Nondiscretionary

Household Overhead

Mortgage interest, rent, fuel, electricity

Boiler, furniture

Nondiscretionary Household Work Cooking, cleaning, childcare, shopping

Dishwasher, oven

Nondiscretionary Biological Maintenance

Food, clothing, sleep

Bed

Discretionary Active Sports, traveling Skis, golf clubs Discretionary Passive Watching TV Television, stereo Revenue Related Human Revenues Work Automobile as

transportation Revenue Related Marketable Assets Investing Computer

40

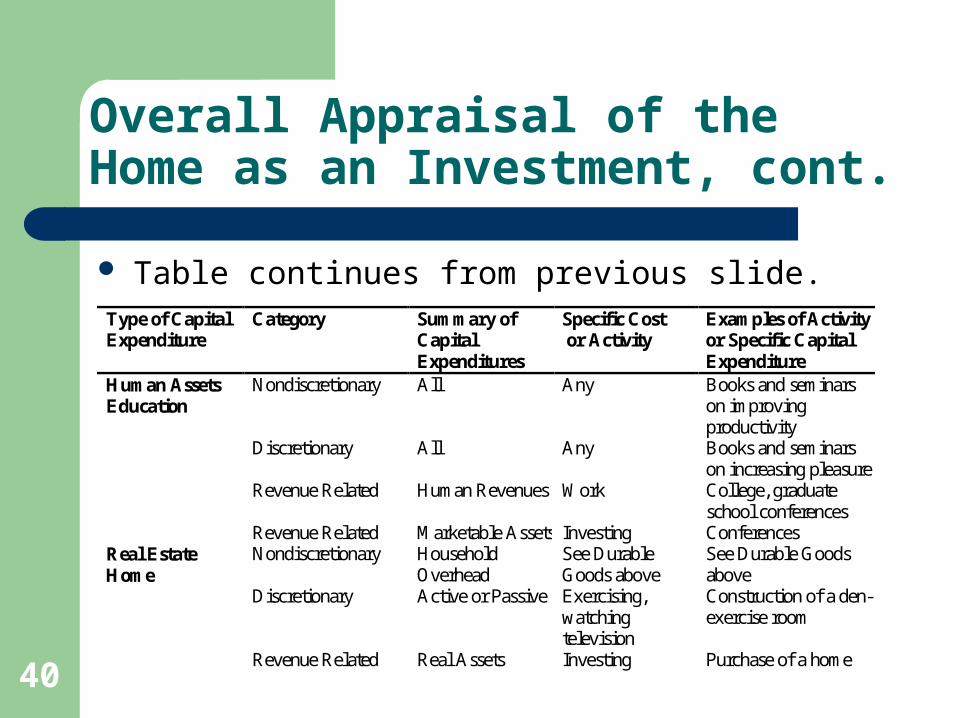

Overall Appraisal of the Home as an Investment, cont.

Table continues from previous slide.Type of Capital Expenditure

Category Summary of Capital Expenditures

Specific Cost or Activity

Examples of Activity or Specific Capital Expenditure

Human Assets Education

Nondiscretionary All Any Books and seminars on improving productivity

Discretionary All Any Books and seminars on increasing pleasure

Revenue Related Human Revenues Work College, graduate school conferences

Revenue Related Marketable Assets Investing Conferences Real Estate Home

Nondiscretionary Household Overhead

See Durable Goods above

See Durable Goods above

Discretionary Active or Passive Exercising, watching television

Construction of a den-exercise room

Revenue Related Real Assets Investing Purchase of a home

41

Chapter Summary

Our objective is to select the best mix of household assets overall. Investment returns can be measured on an individual asset basis, within a household activity, or on a Total Portfolio Management Basis.

Capital expenditures can be evaluated using either an NPV or an IRR approach. In each case, returns on projected outlays are compared with similar market-based investment returns. NPV uses market returns to develop current values and accepts all investments that have a positive present value. IRR provides a return that is compared directly with the market-based return that is used to accept or reject a proposed outlay.

42

Chapter Summary, cont.

Real assets are often durable goods such as a car or an appliance. Human-related assets consist of job-related income discounted to the present plus those related to human work and other rights and relationships and anticipated gifts and bequests. Home ownership is an asset with unique characteristics. It often presents advantages over renting because of its tax benefits.

Leasing is an alternative way to obtain use of an asset. It is generally more costly than purchase, but is attractive for people who are short of capital or who desire more flexibility with their monies.