1 #cbizmhmwebinar ima midatlantic council september 24, 2015 current standard setting activities...

TRANSCRIPT

1#CBIZMHMwebinar

IMA MIDATLANTIC COUNCIL

SEPTEMBER 24, 2015CURRENT STANDARD SETTING ACTIVITIES

KARL G. FASSNACHT, CPA

2#CBIZMHMwebinar

Today’s Agenda

1

2

Recent Accounting Standards

Proposed Accounting Standards

3#CBIZMHMwebinar

Recent Accounting Standards

ASU 2014-07 - Pushdown Accounting

ASU 2015-01 - Extraordinary Items

ASU 2014- 18 - Business Combinations - Accounting for Identifiable Intangible Assets in a Business Combination

ASU 2015-03 - Interest - Imputation of Interest

4#CBIZMHMwebinar

Permits an entity that has been acquired to elect to “push down” into its separate financial statements the step-up in basis of the acquirer that results from (would have resulted from) the acquisition method of accounting

The election applies to each individual change-in-control event Control can be obtained in many ways, including:

Cash transfers or issuance of equity By contract Change in primary beneficiary of a variable interest entity

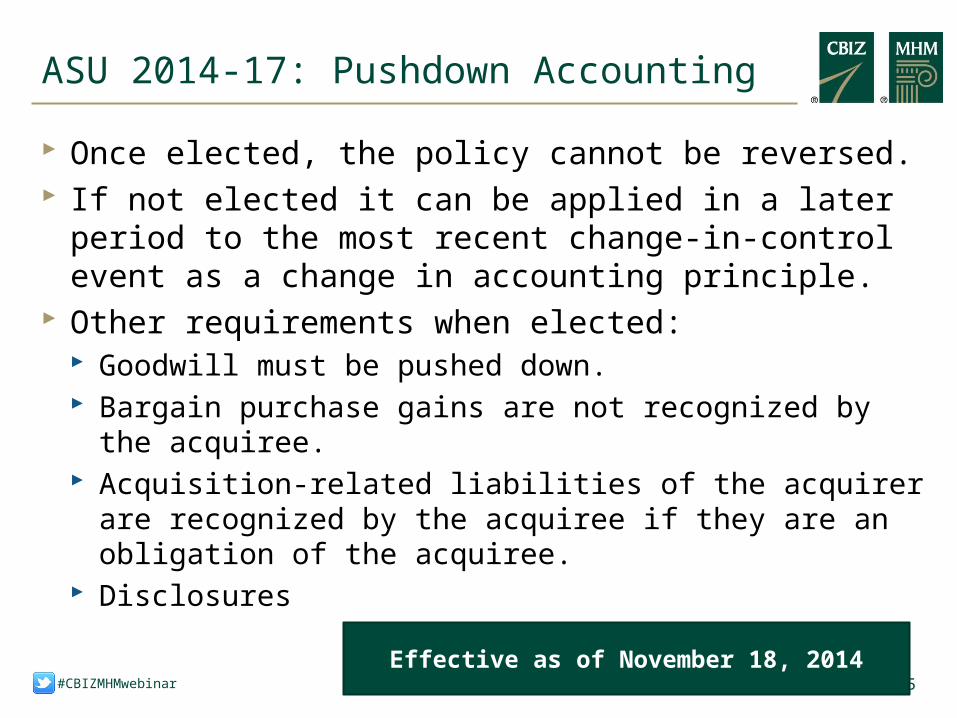

ASU 2014-17: Pushdown Accounting

5#CBIZMHMwebinar

Once elected, the policy cannot be reversed. If not elected it can be applied in a later period to the most

recent change-in-control event as a change in accounting principle.

Other requirements when elected: Goodwill must be pushed down. Bargain purchase gains are not recognized by the acquiree. Acquisition-related liabilities of the acquirer are recognized by

the acquiree if they are an obligation of the acquiree. Disclosures

ASU 2014-17: Pushdown Accounting

Effective as of November 18, 2014

6#CBIZMHMwebinar

Staff Accounting Bulletin 115 Removes the prior guidance from the SEC Staff on the

application of pushdown accounting: Pushdown accounting should be reflected when the transaction

resulted in a “substantially wholly owned subsidiary.” Encouraged, but did not require, push down accounting when a

significant noncontrolling interest in the subsidiary existed Specific guidance on the treatment of debt, debt issue costs and

related interest expense As a result, SEC registrants should follow the requirements

of ASU 2014-17.

ASU 2014-17: Pushdown Accounting

7#CBIZMHMwebinar

Extraordinary Items (ASU 2015-01)

Accounting Standards Update 2015-01: Simplifying Income Statement Presentation by

Eliminating the Concept of Extraordinary Items Extraordinary items were both:

Unusual in nature, and Infrequent in occurrence

Extraordinary item concept and all related presentation and disclosure guidance are removed from U.S. GAAP.

8#CBIZMHMwebinar

Extraordinary Items (ASU 2015-01)

Items that are unusual in nature, infrequent in occurrence — or both — shall be reported as a separate component of income

from continuing operations.

The guidance on unusual or infrequently occurring items is retained.

Unusual means the underlying event or transaction possesses a high degree of abnormality or must be clearly unrelated to ordinary/typical activities of the entity.

Infrequent means the underlying event or transaction should not be reasonably expected to recur in the foreseeable future.

9#CBIZMHMwebinar

Extraordinary Items (ASU 2015-01)

Effective date: Annual period (including interim periods within) beginning after

December 15, 2015 Early adoption is permitted.

Transition: Prospective, or

Disclose the nature and amount of any income statement effect on continuing operations of items previously classified as extraordinary items.

Retrospective Disclosures applicable for a change in accounting principle

10#CBIZMHMwebinar

New Private Company Alternative (ASU 2014-18)

Accounting Standards Update 2014-18: Business Combinations (Topic 805): Accounting for

Identifiable Intangible Assets in a Business Combination May be elected if the entity is not a:

Public business entity Not-for-profit entity Employee benefit plan

11#CBIZMHMwebinar

New Private Company Alternative (ASU 2014-18)

Accounting alternative permits an entity to not recognize, for certain transactions: Customer-related intangible assets unless they are capable

of being sold or licensed independently from other assets of a business, and

Noncompetition agreements.

The impact is such that customer related intangible assets and non-complete agreements are subsumed into the goodwill balance recognized in connection

with the transaction. Therefore, goodwill must also be amortized.

12#CBIZMHMwebinar

New Private Company Alternative (ASU 2014-18)

Applicable to these types of transactions: Business combinations Investments accounting for under the equity method Reorganizations applying fresh-start accounting

Once elected, the accounting alternative must be applied to all qualifying transactions.

13#CBIZMHMwebinar

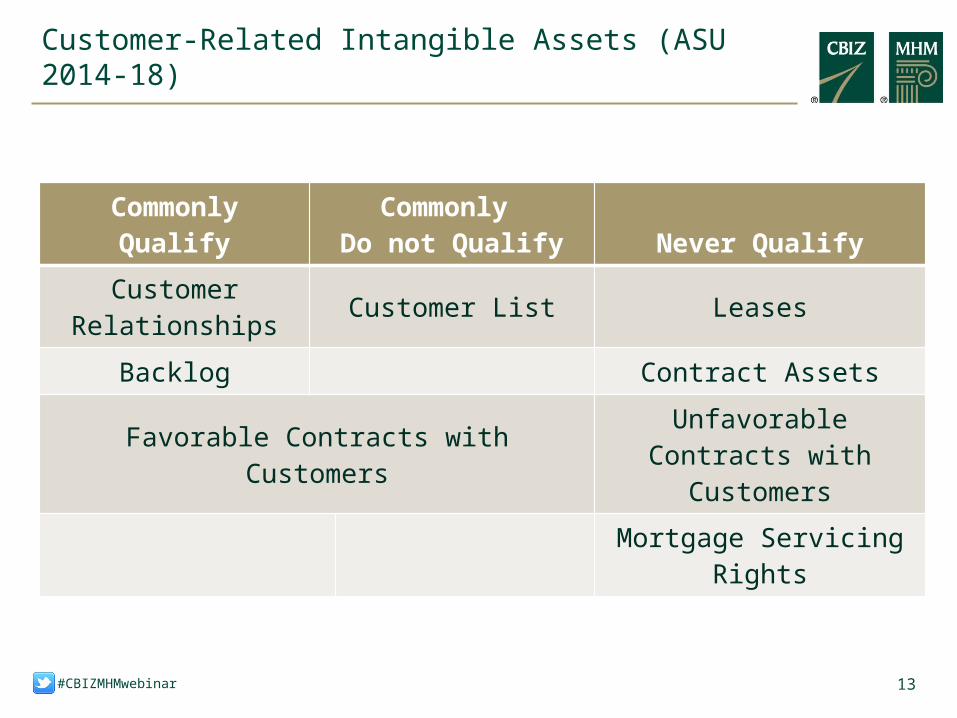

Customer-Related Intangible Assets (ASU 2014-18)

Commonly QualifyCommonly

Do not Qualify Never Qualify

Customer Relationships Customer List Leases

Backlog Contract Assets

Favorable Contracts with Customers Unfavorable Contracts with Customers

Mortgage Servicing Rights

14#CBIZMHMwebinar

Customer-Related Intangible Assets (ASU 2014-18)

Disclosures and Other Requirements Existing required disclosures remain unchanged:

Business combinations qualitatively disclose the components of goodwill.

Equity method investments have no additional disclosures.

An entity electing this alternative must also apply the alternative on amortizing goodwill under ASU 2014-02.

15#CBIZMHMwebinar

Customer-Related Intangible Assets (ASU 2014-18)

Transition and Effective Date Prospectively applied upon election to adopt, upon the first

qualifying transaction that occurs subsequent to the annual period beginning after December 15, 2015 If the first qualifying transaction is in the first annual period after

December 15, 2015 the guidance is effective at the beginning of the annual period.

If the first qualifying transaction is in a subsequent annual period the guidance is effective at the beginning of the interim period in that annual period.

Early adoption for any financial statements not yet made available for issuance is permitted.

16#CBIZMHMwebinar

Customer-Related Intangible Assets (ASU 2014-18)

Considerations Upon Adoption Is the value of entities acquired heavily reliant on customer-

related intangibles that would cause the financial statements to be less useful?

Do users of the financial statements expect to see customer-related intangibles?

Are financial covenants impacted? Do plans exist that may result in the entity no longer

qualifying within the scope as a private company?

The FASB is researching changes to the goodwill impairment model and the recognition guidance of intangible assets for all entities.

17#CBIZMHMwebinar

Debt Issuance Costs

FINAL STANDARD ISSUED: ASU 2015-03 Interest ― Imputation of Interest (Subtopic

835-30): Simplifying the Presentation of Debt Issuance Costs Debt issuance costs related to a recognized debt liability are

required to be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts.

Only addresses presentation, not recognition or measurement Effective for years beginning after December 31, 2015 (January 1,

2016). Retrospective application required.

18#CBIZMHMwebinar

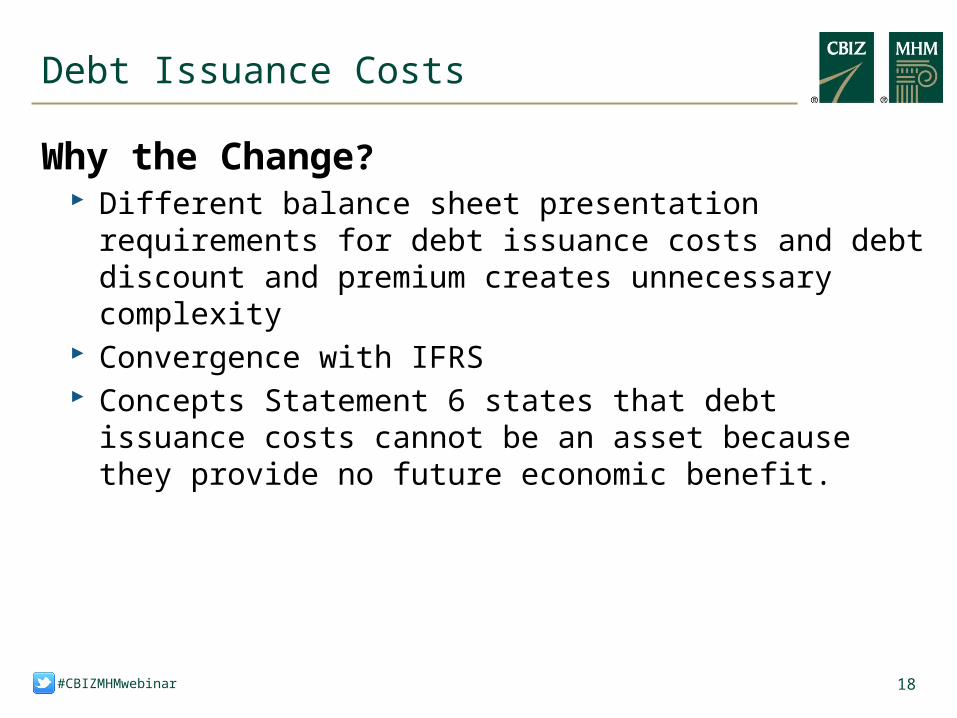

Debt Issuance Costs

Why the Change? Different balance sheet presentation requirements for debt

issuance costs and debt discount and premium creates unnecessary complexity

Convergence with IFRS Concepts Statement 6 states that debt issuance costs cannot

be an asset because they provide no future economic benefit.

19#CBIZMHMwebinar

Equity Method and Joint Ventures – Simplifying the Equity Method of Accounting

Compensation – Stock Compensation to Employee Share-based Payment Accounting

Not-for-Profit Entities and Health Care Entities Income Taxes – Balance Sheet Classification of

Deferred Taxes Business Combinations – Simplifying the Accounting for

Measurement – Period Adjustments Leases

20#CBIZMHMwebinar

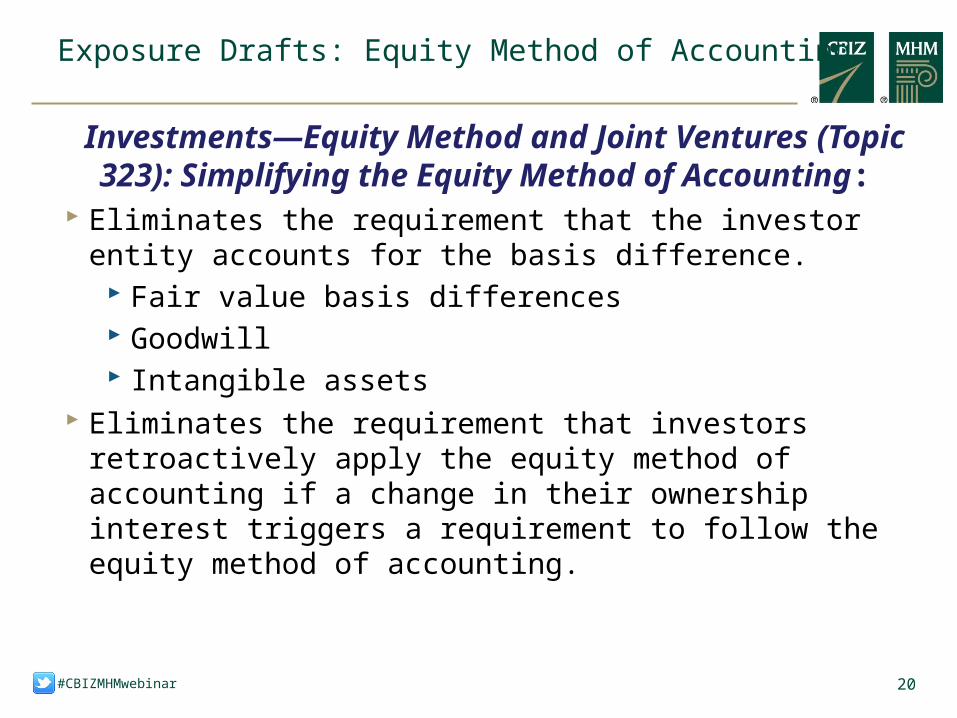

Exposure Drafts: Equity Method of Accounting

Investments—Equity Method and Joint Ventures (Topic 323): Simplifying the Equity Method of Accounting:

Eliminates the requirement that the investor entity accounts for the basis difference.

Fair value basis differences Goodwill Intangible assets

Eliminates the requirement that investors retroactively apply the equity method of accounting if a change in their ownership interest triggers a requirement to follow the equity method of accounting.

21#CBIZMHMwebinar

Exposure Drafts: Stock Compensation

Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting

Statutory withholding Forfeitures Accounting for income taxes when awards vest or are settled Classification of awards with repurchase features Private company practical expedients:

Estimate of expected term Elect a one-time change in accounting principle to measure

liability-classified awards at intrinsic value, if currently measured at fair value

22#CBIZMHMwebinar

Exposure Drafts: Stock Compensation

Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment AccountingStatutory Withholding Under current guidance, if the fair value of the shares withheld to pay

income taxes exceeds the employer’s minimum statutory withholding obligation, the entire award must be classified as a liability.

The proposal allows for an employer to avoid triggering liability accounting if the value of the shares repurchased does not exceed the amount of the employee’s maximum individual statutory rate in the applicable jurisdiction.

Will allow companies to repurchase shares from employees in high-income tax brackets for withholding purposes without triggering liability accounting.

23#CBIZMHMwebinar

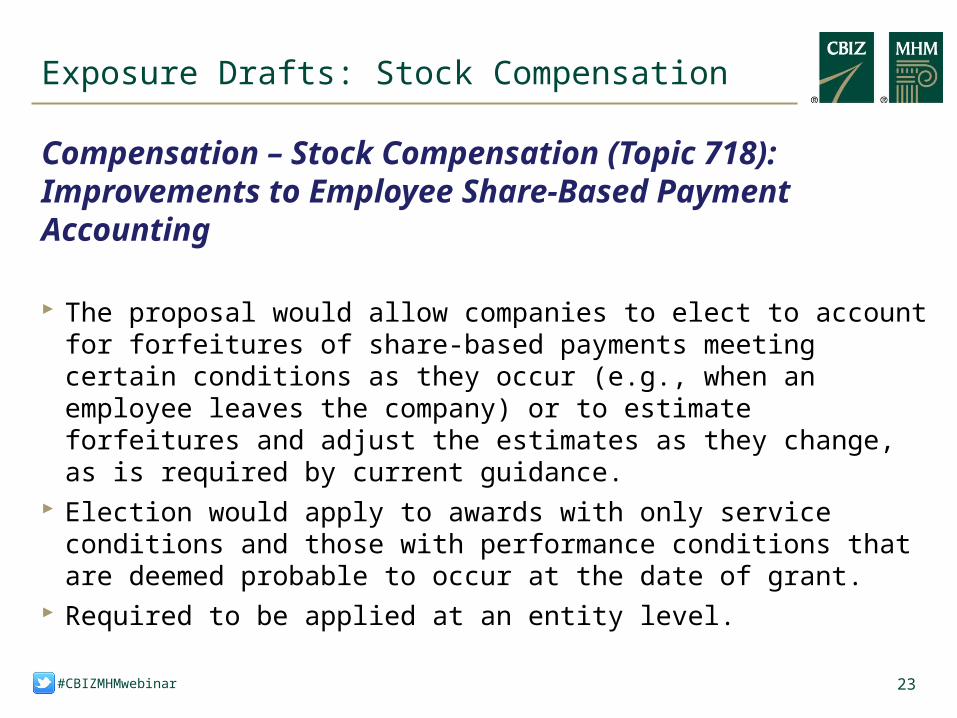

Exposure Drafts: Stock Compensation

Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment AccountingForfeitures The proposal would allow companies to elect to account for forfeitures of

share-based payments meeting certain conditions as they occur (e.g., when an employee leaves the company) or to estimate forfeitures and adjust the estimates as they change, as is required by current guidance.

Election would apply to awards with only service conditions and those with performance conditions that are deemed probable to occur at the date of grant.

Required to be applied at an entity level.

24#CBIZMHMwebinar

Exposure Drafts: Stock Compensation

Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment AccountingAccounting for income taxes when awards vest or are settled APIC pools would be eliminated. Would require companies to include all excess tax benefits and tax

deficiencies as income tax expense or benefit in the income statement. Would eliminate the requirement that excess tax benefits be realized (i.e.,

reduce income taxes payable) before being recognized. Would require companies to present excess tax benefits as an operating

activity in the statement of cash flows rather than as a financing activity.

25#CBIZMHMwebinar

Exposure Drafts: Stock Compensation

Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment AccountingClassification of awards with repurchase features A company would focus solely on the probability that the contingent event

would occur to determine whether to classify these awards as liabilities or equity (i.e., which party controls the contingent event would no longer be relevant).

Intended to eliminate diversity in practice.

26#CBIZMHMwebinar

Exposure Drafts: Stock Compensation

Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment AccountingPrivate company practical expedients Estimate of expected term Elect a one-time change in accounting principle to measure liability-

classified awards at intrinsic value, if currently measured at fair value

27#CBIZMHMwebinar

Exposure Drafts: Not-for-Profit

Not-for-Profit Entities (Topic 958) and Health Care Entities (Topic 954): Presentation of Financial Statements of Not-for-Profit EntitiesThe main provisions would require a not-for-profit entity to: Present on the face of the statement of financial position amounts for two

classes of net assets (net assets with donor restrictions and net assets without donor restrictions) at the end of the period, rather than for the currently required three classes.

Present on the face of the statement of activities the amount of the change in each of the two classes of net assets rather than that of the currently required three classes.

Present on the face of the statement of activities two additional amounts (subtotals) of the operating activities that are associated with changes in net assets without donor restrictions.

28#CBIZMHMwebinar

Exposure Drafts: Not-for-Profit

Not-for-Profit Entities (Topic 958) and Health Care Entities

(Topic 954): Presentation of Financial Statements of

Not-for-Profit Entities

The main provisions would require a not-for-profit entity to (cont.):

Present on the face of the statement of cash flows the net amount for

operating cash flows using the direct method of reporting.

Classify certain cash flows differently than how they are classified under

current guidance,

Provide enhanced disclosures.

Use the placed-in-service approach for reporting expirations of restrictions

on gifts of cash or other assets to be used to acquire or construct a long-

lived asset.

Report investment income net of external and direct internal investment

expenses.

29#CBIZMHMwebinar

Accounting for Income Taxes

EXPOSURE DRAFTS: Intra-Entity Asset Transfers

Eliminates the exception that prohibits recognizing current and deferred income tax consequences for an intra-entity asset transfer until the asset or assets have been sold to an outside party.

Requires that an entity recognize the current and deferred income tax consequences of an intra-entity asset transfer when the transfer occurs.

Aligns with IAS 12 Income Taxes

Balance Sheet Classification of Deferred Taxes Deferred tax liabilities and assets should be classified as noncurrent in

a classified statement of financial position. Aligns with IAS 1 Presentation of Financial Statements

30#CBIZMHMwebinar

Exposure Drafts: Business Combinations

Business Combinations (Topic 805): Simplifying the Accounting for Measurement-Period Adjustments US GAAP requires the acquirer to retrospectively adjust the

provisional amounts recognized at the acquisition date to reflect that information with a corresponding adjustment to

goodwill, and revise comparative information for prior periods presented.

The proposed amendments would require that the acquirer recognize adjustments to provisional amounts that are identified during the measurement period in the reporting period in

which the adjustment amount is determined, as well as the effect on earnings, if any, as a result of the change to

the provisional amounts, calculated as if the accounting had been completed at the acquisition date.

31#CBIZMHMwebinar

Project: Leases

The FASB has directed the staff to prepare a final standard!!

The FASB will discuss the benefits and costs of the new leases standard, effective date, and any issues that arise during drafting of the final leases standard.

The Board will discuss private company considerations at a future Board meeting.

32#CBIZMHMwebinar

Project: Leases

Affirmed the exemption for short-term leases with terms less than 12 months

“Type A” and “Type B” leases are presented separately on the balance sheet. Principal payments on Type A leases are presented as

financing activities. Sale-leaseback transaction where the lease is a Type A

lease is not treated as a sale

Type A leases are similar to today’s capital leases, while Type B leases are recorded on the balance sheet, but have income statement presentation

similar to today’s operating leases.

33#CBIZMHMwebinar

Transition will be a modified retrospective approach as of the earliest comparative period presented – full retrospective will not be permitted. Permit the election of a package of relief measures Permit the use of hindsight for renewals and purchase options Entities need not re-evaluate sale-lease backs using Topic 606

The IASB and FASB will not be fully converged, differences include: Different income statement presentation for Type A and Type B leases Accounting for reassessment of the discount rate and variable lease

payments Certain disclosures

Project: Leases