1 april, 2012 sergey vasiliev deputy chairman x brics’ role in global development up to 2020

TRANSCRIPT

1

April, 2012

Sergey VasilievDeputy Chairman

x

BRICS’ Role in Global Development up to 2020

2

BRICS ROLE IN WORLD ECONOMIC OUTLOOK

2000-2010: BRIC – demonstrated high growth rates, became drivers of the world economy

Source: Goldman Sachs

2010-2020: BRIC keep their role in world economy, but with lower growth rates

2020-2050: Emerging markets will produce 60-70% of world GDP

0%

20%

40%

60%

80%

100%

1980 1990 2000 2010 2020 2030 2040 2050

Emerging markets Developed countries

World GDP, %

3

EMERGING MARKETS: MULTIPLE CENTERS OF ECONOMIC GROWTH

Emerging markets will become new drivers of the world economy growth, demonstrate the highest growth rate

N-11: Bangladesh, Egypt, Indonesia, Iran, Korea, Mexico, Nigeria, Pakistan, Philippines, Turkey, Vietnam

0

1

2

3

4

5

6

7

8

9

2000-2009 2010-2019 2020-2029 2030-2039 2040-2050

Developed

N-11

BRIC

World

Annual GDP Growth Rate, %

Faster growth in emerging economies outside BRIC

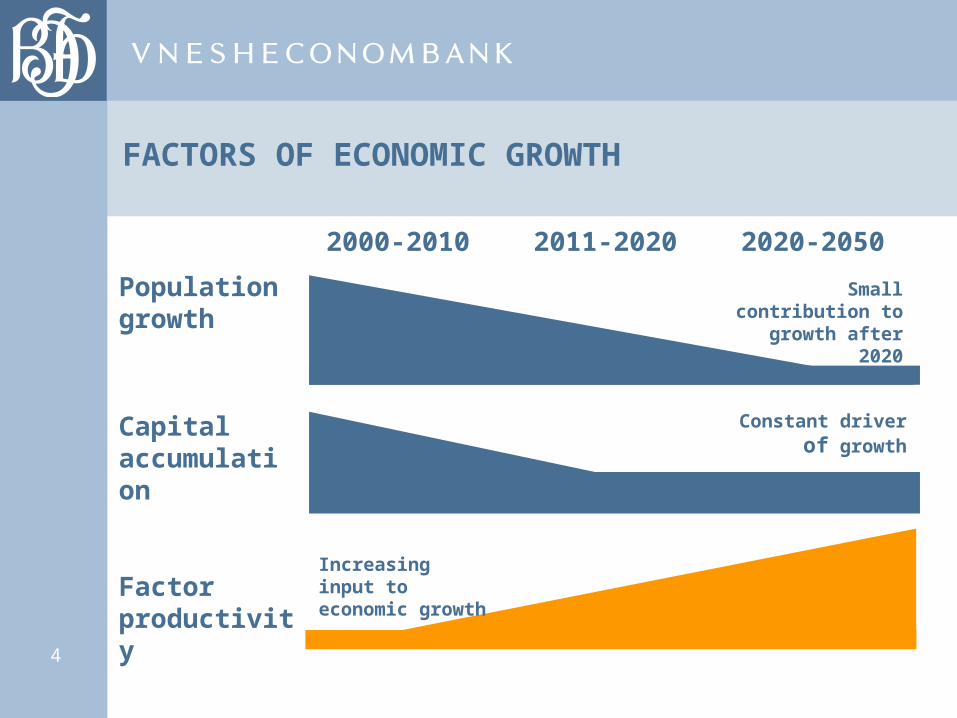

4

2000-2010 2011-2020 2020-2050

Factor productivity

FACTORS OF ECONOMIC GROWTH

Population growth

Capital accumulation

Small contribution to growth after

2020

Constant driver of growth

Increasing input to economic growth

5

Over the last 20 years share of BRICS countries increased sharply

This growth mainly determined by increasing exports to developed countries

Share of BRICS in world trade (%)

BRICS GROWING CONTRIBUTION TO INTERNATIONAL TRADE

4,0%

7,5%

17,1%

9,0%

0,8%

3,7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1990 2000 2011

Exports Imports

6

In recent years mutual trade between BRICS countries enlarged fivefold, but still remains quite low

World Trade Flows in 2011 (All Exports = 100%)

1,5%

4,4%

7,4%

7,4% 8,1%

27,5%

15,5% 14,0%

14,1%

BRICS

G3

Other countries

From: To:

BRICS G3 Other countries

MUTUAL TRADE AMONG BRICS COUNTRIES

7

CASE FOR NATIONAL SETTLEMENT CURRENCIES IN FOREIGN TRADE

-More transparent pricing in bilateral trade

-Reduce dependence on other currencies fluctuations

-Lower trade transaction costs (estimated up to 4% volume)

Benefits

What do BRICS development institutions do to extend international use of national currencies:

Agreement on Financial Cooperation within the BRICS Interbank Cooperation Mechanism

Master Agreement on Extending Facilities in Local Currency under BRICS Interbank Cooperation Mechanism.

Opening new credit lines and implementing joint investment projects on bilateral and multilateral basis

8

CO-FINANCING INVESTMENT IN BRICS ECONOMIES:RDIF EXAMPLE

Bilateral investment among BRICS countries remains very low: • 1.8 % of total foreign direct investment (FDI) inflows • 1.2 % of total FDI outflowsSimilar may be true for bilateral investment between other emerging countries

Russian Direct Investment Fund • $10 billion fund established in 2011 by Russian government • Targets equity investments in the Russian economy• Mandated to co-invest with large investors globally

Management Company of the Fund is a 100% subsidiary of Vnesheconombank and will operate according to international best practices of investment governance.

Facility to promote investment:

9

LONG TERM INVESTMENT CHALLENGE

Solutions to various structural problems (such technology transfer, innovation catch-up and infrastructure demands) in emerging economies require long-term investment.

Perceived economy growth risks and government budget deficits preserve «short-termism» in financing – a key challenge faced by long-term investors.

Needed steps:

• Bring private financing to projects

• Implement frameworks to manage environmental and social risks

• Seek favorable financial regulation for long-term investment

Best practices exchange and joint pilot projects will help advance in these steps.

Major development finance institutions joined to Long Term Investors Club to address these challenges.

Investment needs

Constraints: «short-termism»

Areas for action…

… and cooperation

10

VNESHECONOMBANK GROUP

Russian bank for Small and Medium Enterprise Support

(Russia)

3.6% of Total Assets

Roseximbank

(Russia)

0.4% of Total Assets

VEB Capital

(Russia)

0.3% of Total Assets

VEB Leasing

(Russia)

5.6% of Total Assets

Sviaz-Bank

(Russia)

6.8% of Total Assets

Prominvestbank

(Ukraine)

5.0% of Total Assets

Globexbank

(Russia)

7.3% of Total Assets

Belvnesheconombank

(Belarus)

1.6% of Total Assets

VEB CAPITAL

Core Russian subsidiaries

Banks bailed out by the Government during crisis Representation in CIS countries

1. Assets split provided based on 1H 2011 management accounts

11

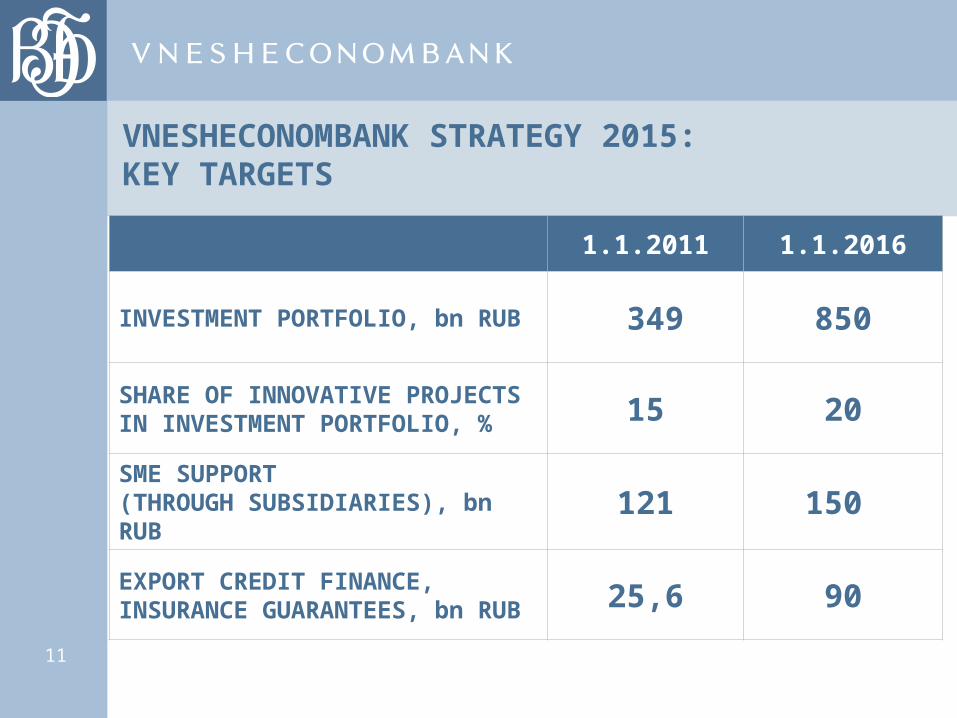

VNESHECONOMBANK STRATEGY 2015:KEY TARGETS

1.1.2011 1.1.2016

INVESTMENT PORTFOLIO, bn RUB 349 850

SHARE OF INNOVATIVE PROJECTS IN INVESTMENT PORTFOLIO, % 15 20

SME SUPPORT (THROUGH SUBSIDIARIES), bn RUB 121 150

EXPORT CREDIT FINANCE, INSURANCE GUARANTEES, bn RUB 25,6 90

12

Thank you !

9 Ak. Sakharov ave. Moscow, Russia

tel.: +7 (495) 721-18-63 fax: +7 (499) 975-21-43

www.veb.ru