02 banker customer realtion ship and special types of accounts

TRANSCRIPT

Retail Banking and

Financial Inclusion

DEFINITION of 'Retail Banking'

• Typical mass-market banking in which individual customers use local branches of larger commercial banks.

• Services offered include savings and checking accounts, mortgages, personal loans, debit/credit cards and certificates of deposit (CDs).

• Retail banking aims to be the one-stop shop for as many financial services as possible on behalf of retail clients.

• Some retail banks have even made a push into investment services such as wealth management, brokerage accounts, private banking and retirement planning and include them in retail banking

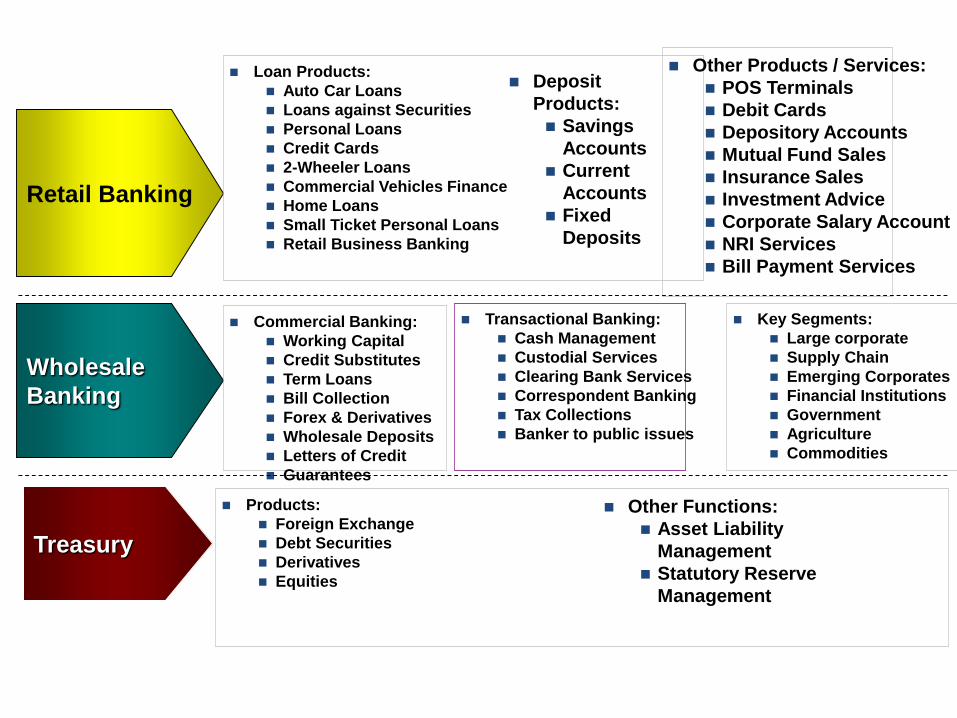

Retail Banking

Loan Products:

Auto Car Loans

Loans against Securities

Personal Loans

Credit Cards

2-Wheeler Loans

Commercial Vehicles Finance

Home Loans

Small Ticket Personal Loans

Retail Business Banking

Other Products / Services:

POS Terminals

Debit Cards

Depository Accounts

Mutual Fund Sales

Insurance Sales

Investment Advice

Corporate Salary Account

NRI Services

Bill Payment Services

Wholesale

Banking

Commercial Banking:

Working Capital

Credit Substitutes

Term Loans

Bill Collection

Forex & Derivatives

Wholesale Deposits

Letters of Credit

Guarantees

Key Segments:

Large corporate

Supply Chain

Emerging Corporates

Financial Institutions

Government

Agriculture

Commodities

Treasury

Products:

Foreign Exchange

Debt Securities

Derivatives

Equities

Deposit

Products:

Savings

Accounts

Current

Accounts

Fixed

Deposits

Other Functions:

Asset Liability

Management

Statutory Reserve

Management

Transactional Banking:

Cash Management

Custodial Services

Clearing Bank Services

Correspondent Banking

Tax Collections

Banker to public issues

Banker Customer Relationship

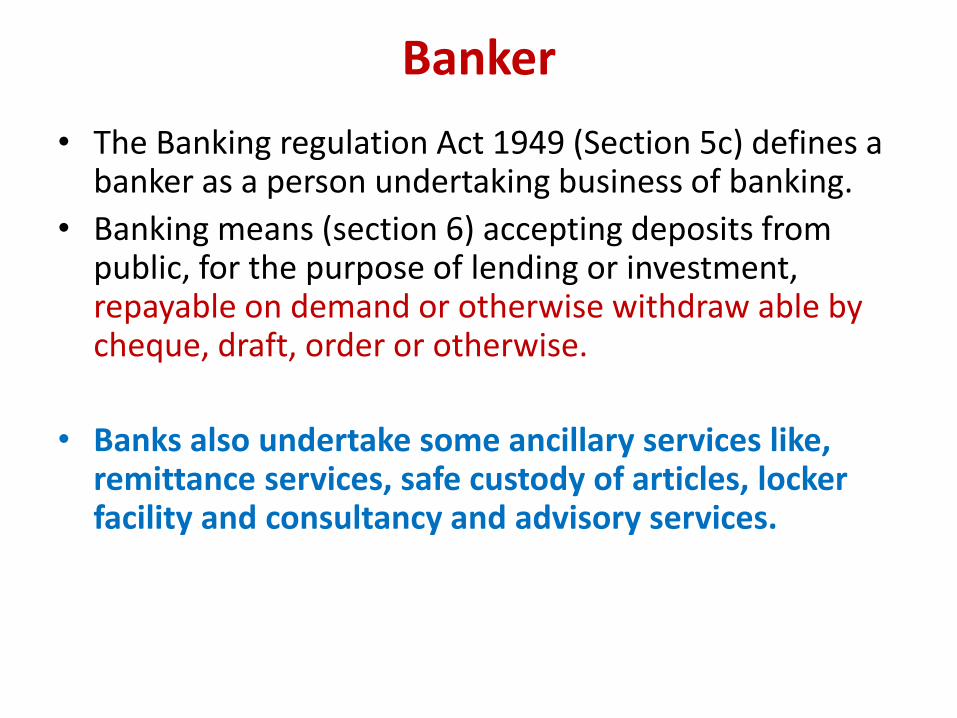

Banker

• The Banking regulation Act 1949 (Section 5c) defines a banker as a person undertaking business of banking.

• Banking means (section 6) accepting deposits from public, for the purpose of lending or investment, repayable on demand or otherwise withdraw able by cheque, draft, order or otherwise.

• Banks also undertake some ancillary services like, remittance services, safe custody of articles, locker facility and consultancy and advisory services.

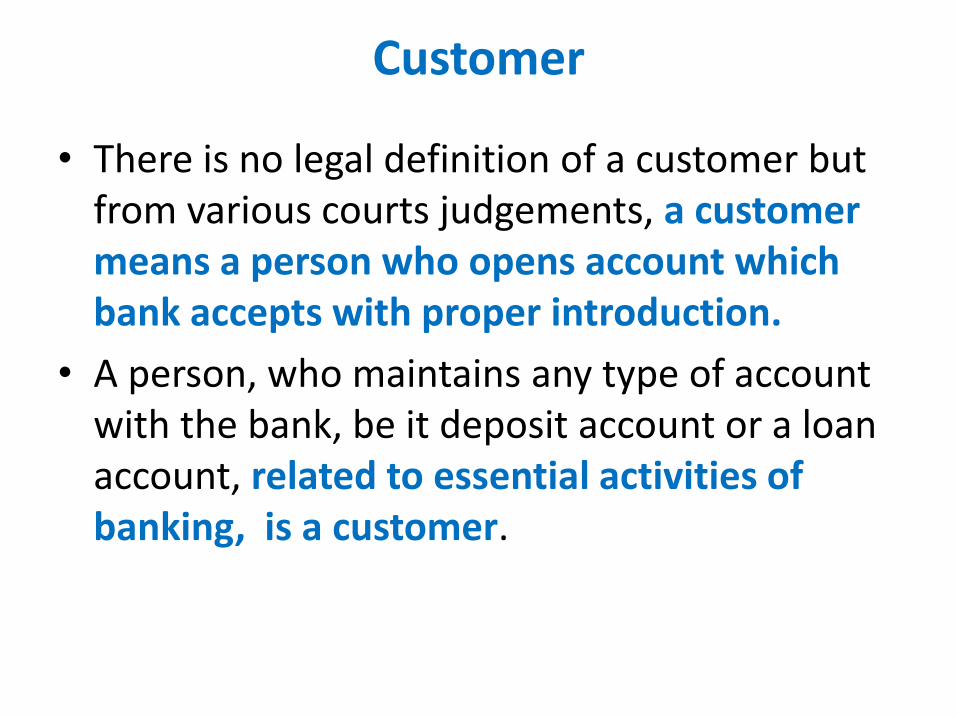

Customer

• There is no legal definition of a customer but from various courts judgements, a customer means a person who opens account which bank accepts with proper introduction.

• A person, who maintains any type of account with the bank, be it deposit account or a loan account, related to essential activities of banking, is a customer.

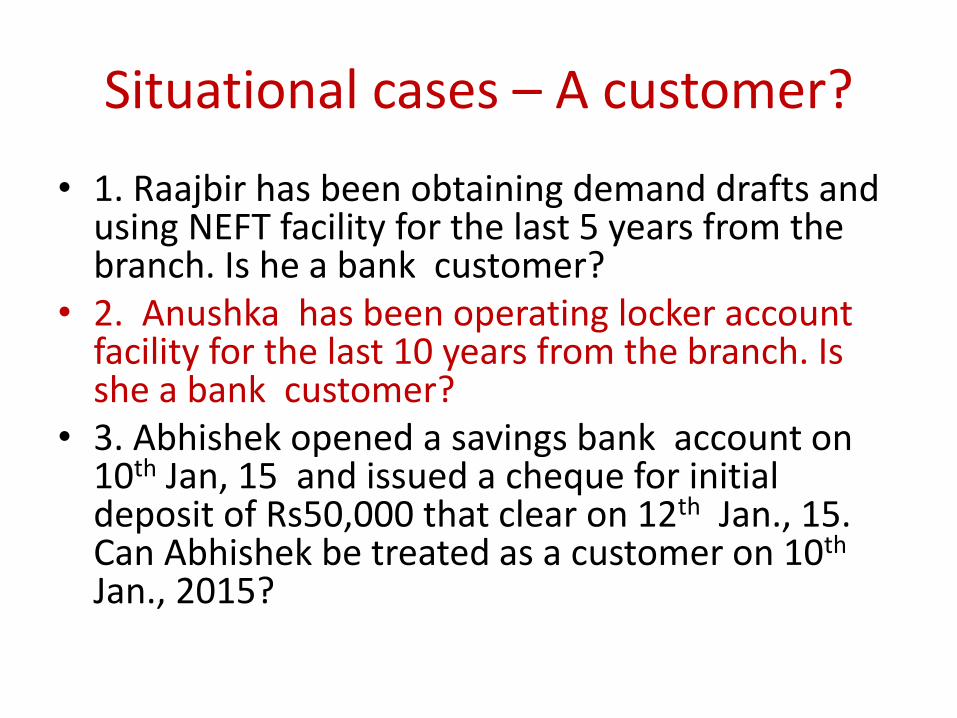

Situational cases – A customer?

• 1. Raajbir has been obtaining demand drafts and using NEFT facility for the last 5 years from the branch. Is he a bank customer?

• 2. Anushka has been operating locker account facility for the last 10 years from the branch. Is she a bank customer?

• 3. Abhishek opened a savings bank account on 10th Jan, 15 and issued a cheque for initial deposit of Rs50,000 that clear on 12th Jan., 15. Can Abhishek be treated as a customer on 10th

Jan., 2015?

KYC (Know Your Customer) Norms for new customer accounts:

• KYC procedure is the key principle intended for identification of an individual or a corporate opening an account.

• The customer identification should entail verification through

1) An introductory reference from an existing account holder

2) A person known to the bank or 3) On the basis of documents provided by the

customer.

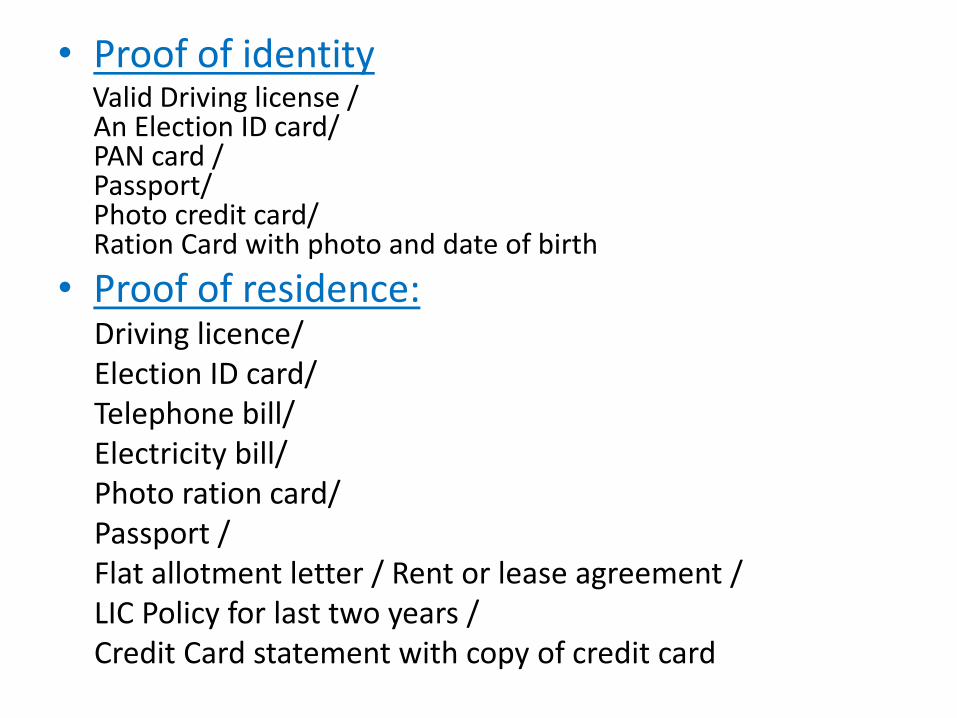

• Proof of identityValid Driving license /An Election ID card/ PAN card / Passport/ Photo credit card/ Ration Card with photo and date of birth

• Proof of residence: Driving licence/ Election ID card/ Telephone bill/ Electricity bill/ Photo ration card/ Passport / Flat allotment letter / Rent or lease agreement / LIC Policy for last two years / Credit Card statement with copy of credit card

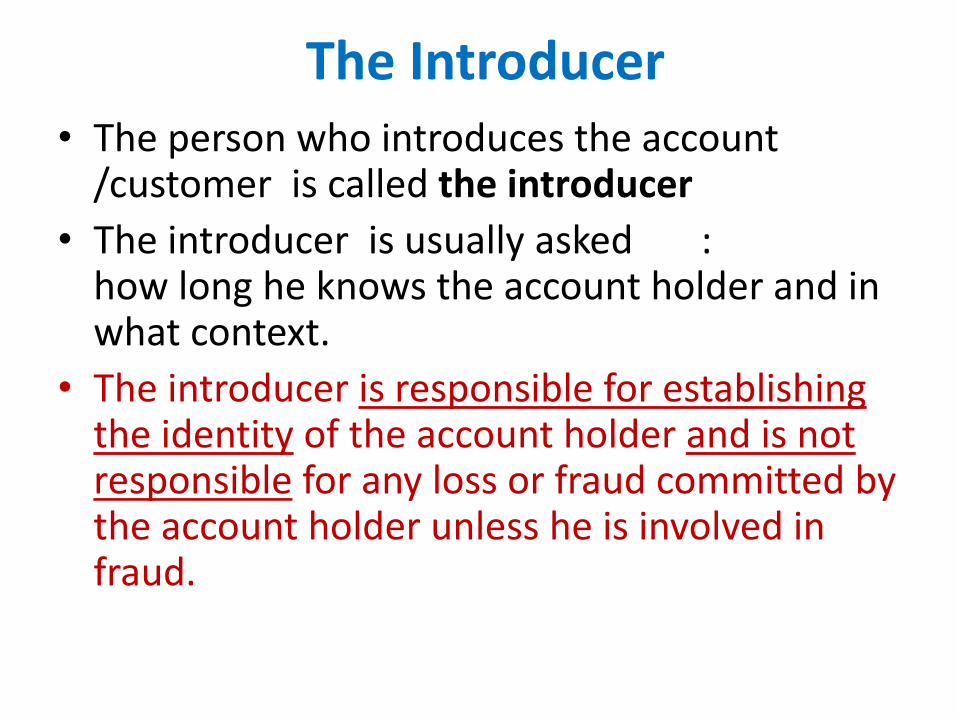

The Introducer• The person who introduces the account

/customer is called the introducer

• The introducer is usually asked : how long he knows the account holder and in what context.

• The introducer is responsible for establishing the identity of the account holder and is not responsible for any loss or fraud committed by the account holder unless he is involved in fraud.

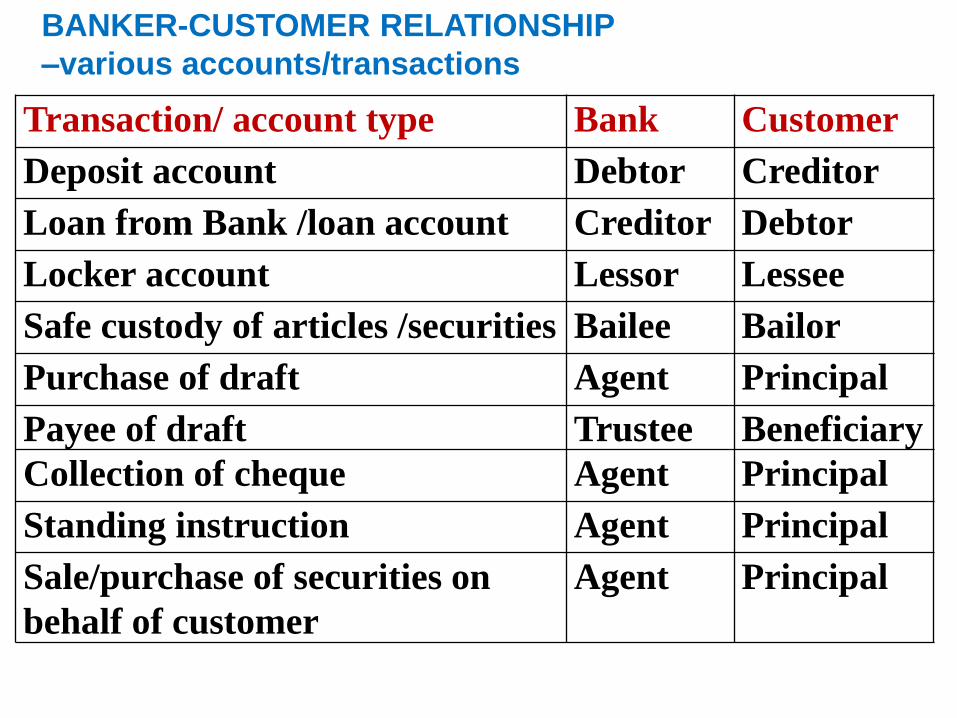

Transaction/ account type Bank Customer

Deposit account Debtor Creditor

Loan from Bank /loan account Creditor Debtor

Locker account Lessor Lessee

Safe custody of articles /securities Bailee Bailor

Purchase of draft Agent Principal

Payee of draft Trustee Beneficiary

Collection of cheque Agent Principal

Standing instruction Agent Principal

Sale/purchase of securities on

behalf of customer

Agent Principal

BANKER-CUSTOMER RELATIONSHIP

–various accounts/transactions

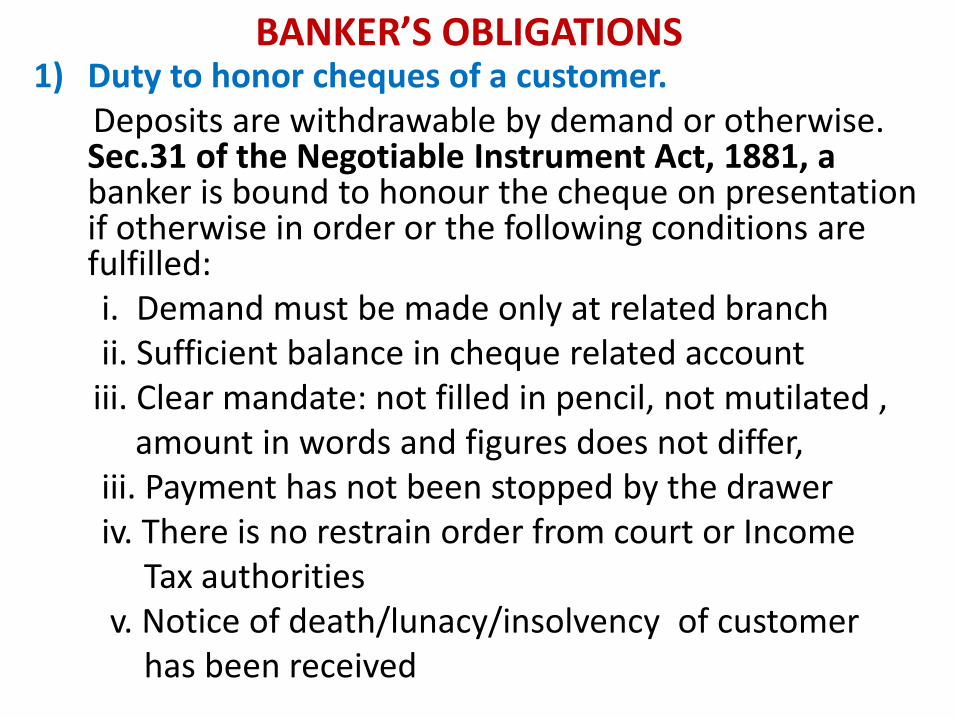

BANKER’S OBLIGATIONS1) Duty to honor cheques of a customer.

Deposits are withdrawable by demand or otherwise. Sec.31 of the Negotiable Instrument Act, 1881, a banker is bound to honour the cheque on presentation if otherwise in order or the following conditions are fulfilled: i. Demand must be made only at related branchii. Sufficient balance in cheque related account

iii. Clear mandate: not filled in pencil, not mutilated , amount in words and figures does not differ,

iii. Payment has not been stopped by the draweriv. There is no restrain order from court or Income

Tax authorities v. Notice of death/lunacy/insolvency of customer

has been received

Duty to maintain secrecy of affairs or transactions of accounts

• Implied contract for secrecy +

• Section 13 of Banking Companies (Acquisition and Transfer of Undertakings ) Act 1970

• Justified Disclosures:

• Banking practices

• In interets of Bank/Public/ Nation

• With consent of customer

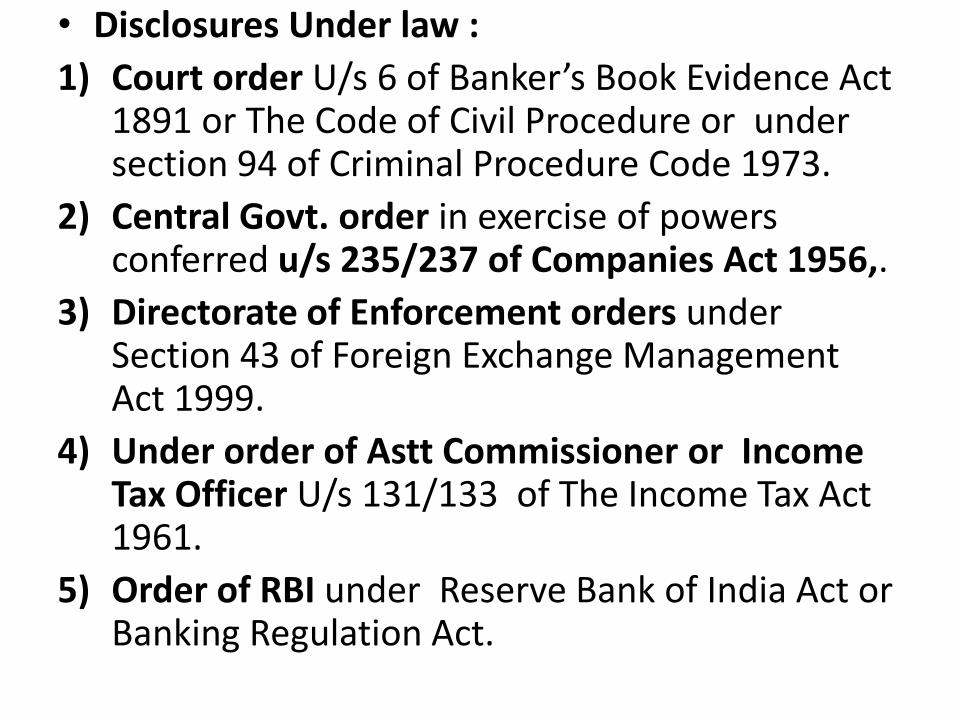

• Disclosures Under law :

• Disclosures Under law :

1) Court order U/s 6 of Banker’s Book Evidence Act 1891 or The Code of Civil Procedure or under section 94 of Criminal Procedure Code 1973.

2) Central Govt. order in exercise of powers conferred u/s 235/237 of Companies Act 1956,.

3) Directorate of Enforcement orders under Section 43 of Foreign Exchange Management Act 1999.

4) Under order of Astt Commissioner or Income Tax Officer U/s 131/133 of The Income Tax Act 1961.

5) Order of RBI under Reserve Bank of India Act or Banking Regulation Act.

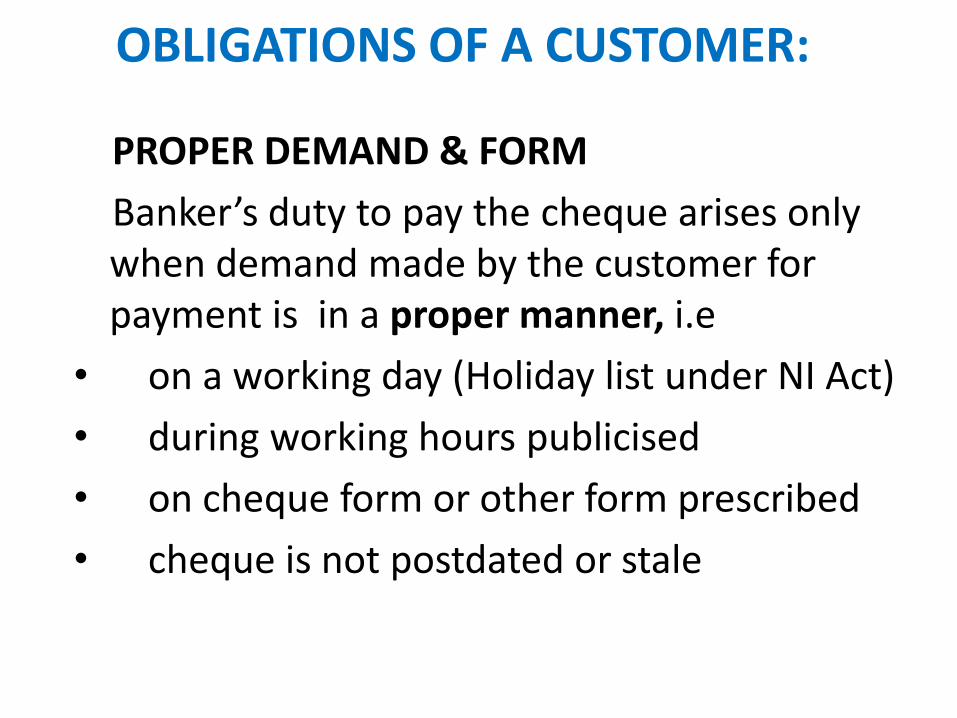

OBLIGATIONS OF A CUSTOMER:

PROPER DEMAND & FORM

Banker’s duty to pay the cheque arises only when demand made by the customer for payment is in a proper manner, i.e

• on a working day (Holiday list under NI Act)

• during working hours publicised

• on cheque form or other form prescribed

• cheque is not postdated or stale

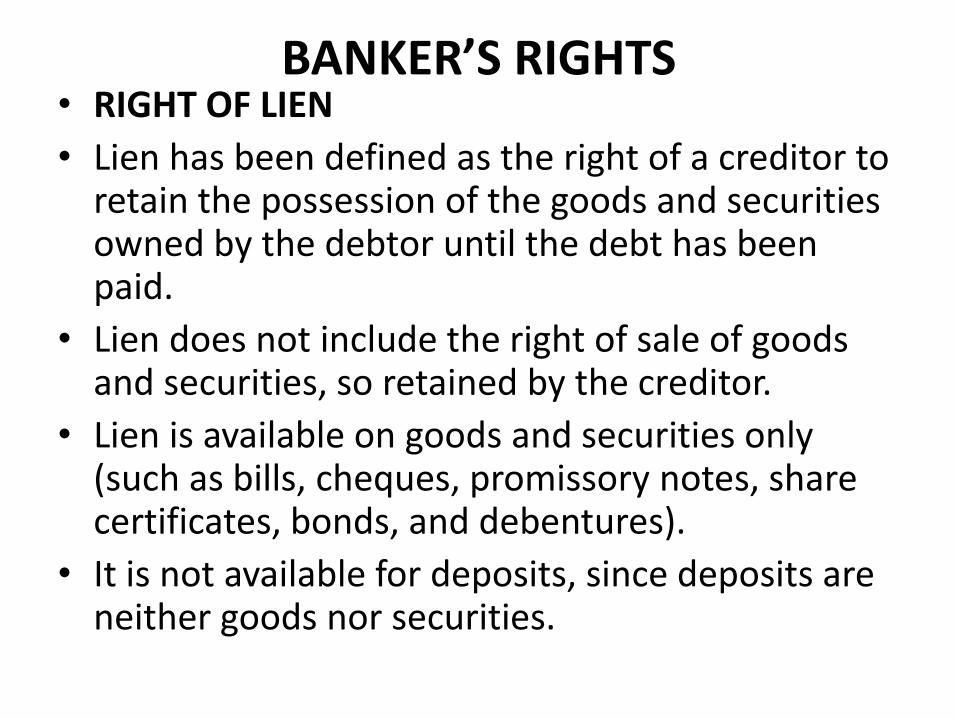

BANKER’S RIGHTS • RIGHT OF LIEN

• Lien has been defined as the right of a creditor to retain the possession of the goods and securities owned by the debtor until the debt has been paid.

• Lien does not include the right of sale of goods and securities, so retained by the creditor.

• Lien is available on goods and securities only (such as bills, cheques, promissory notes, share certificates, bonds, and debentures).

• It is not available for deposits, since deposits are neither goods nor securities.

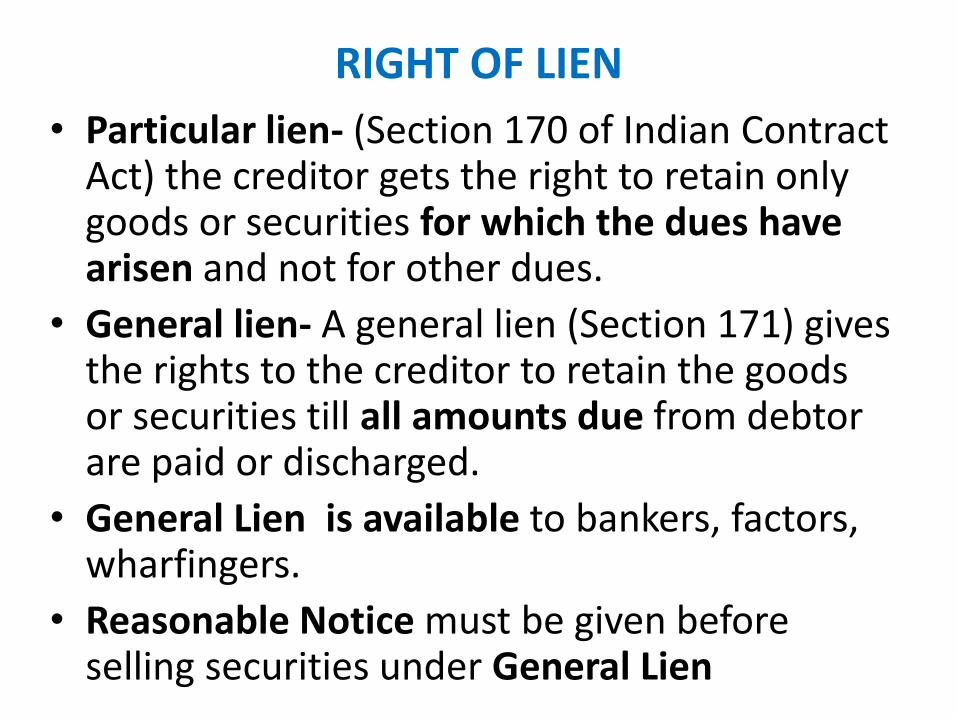

RIGHT OF LIEN

• Particular lien- (Section 170 of Indian Contract Act) the creditor gets the right to retain only goods or securities for which the dues have arisen and not for other dues.

• General lien- A general lien (Section 171) gives the rights to the creditor to retain the goods or securities till all amounts due from debtor are paid or discharged.

• General Lien is available to bankers, factors, wharfingers.

• Reasonable Notice must be given before selling securities under General Lien

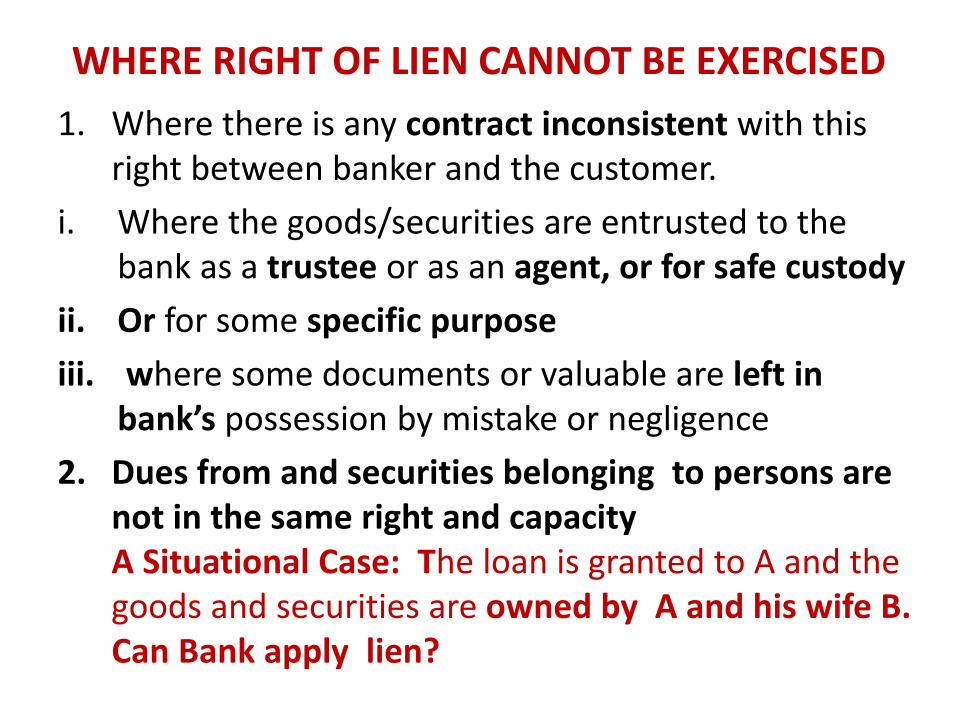

WHERE RIGHT OF LIEN CANNOT BE EXERCISED

1. Where there is any contract inconsistent with this right between banker and the customer.

i. Where the goods/securities are entrusted to the bank as a trustee or as an agent, or for safe custody

ii. Or for some specific purpose

iii. where some documents or valuable are left in bank’s possession by mistake or negligence

2. Dues from and securities belonging to persons are not in the same right and capacity A Situational Case: The loan is granted to A and the goods and securities are owned by A and his wife B. Can Bank apply lien?

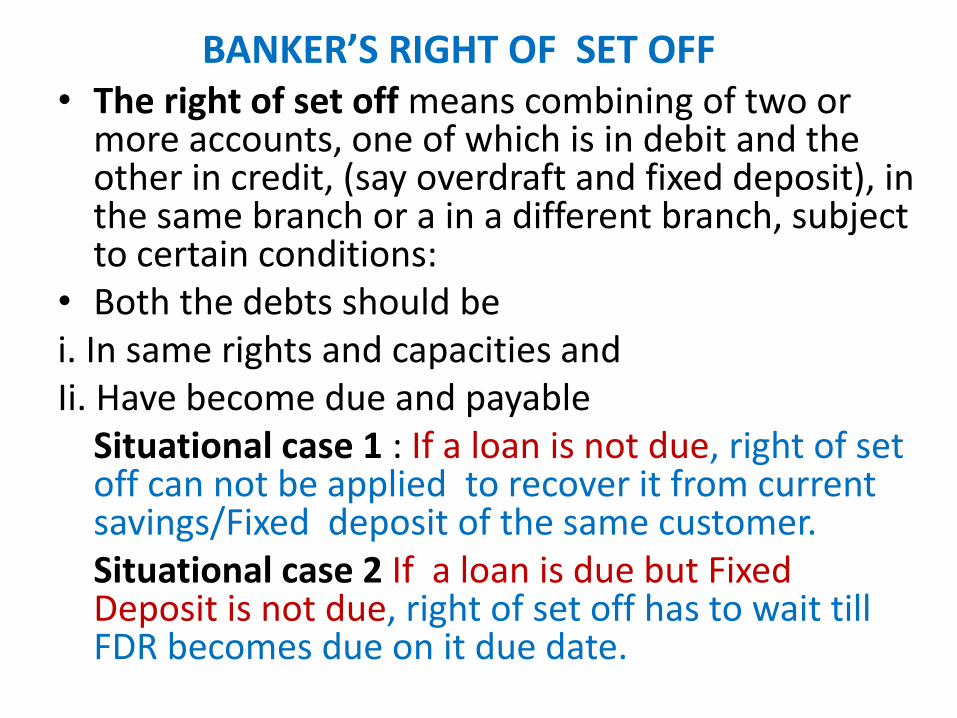

BANKER’S RIGHT OF SET OFF• The right of set off means combining of two or

more accounts, one of which is in debit and the other in credit, (say overdraft and fixed deposit), in the same branch or a in a different branch, subject to certain conditions:

• Both the debts should be i. In same rights and capacities and Ii. Have become due and payable

Situational case 1 : If a loan is not due, right of set off can not be applied to recover it from current savings/Fixed deposit of the same customer. Situational case 2 If a loan is due but Fixed Deposit is not due, right of set off has to wait till FDR becomes due on it due date.

Special types

of

customers

in

Retail Banking

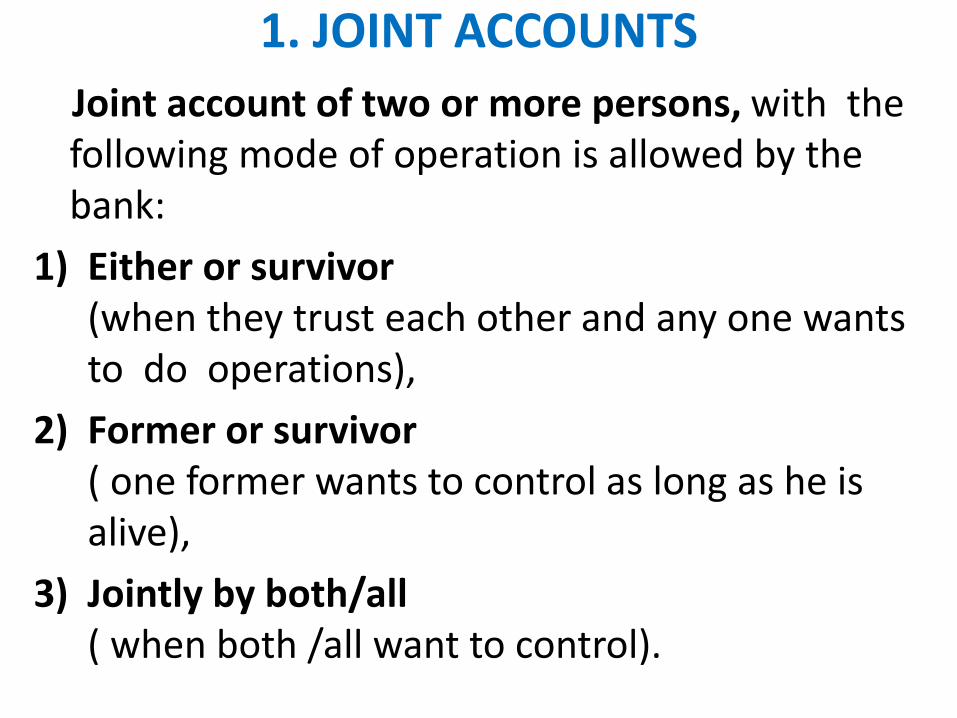

1. JOINT ACCOUNTS

Joint account of two or more persons, with the following mode of operation is allowed by the bank:

1) Either or survivor (when they trust each other and any one wants to do operations),

2) Former or survivor ( one former wants to control as long as he is alive),

3) Jointly by both/all ( when both /all want to control).

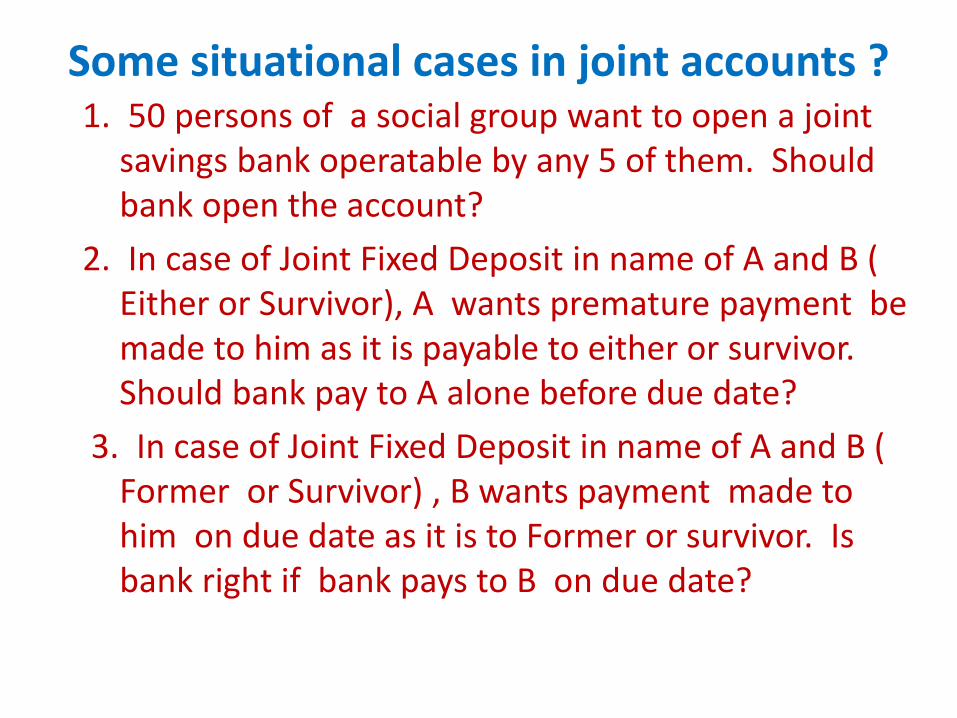

Some situational cases in joint accounts ? 1. 50 persons of a social group want to open a joint

savings bank operatable by any 5 of them. Should bank open the account?

2. In case of Joint Fixed Deposit in name of A and B ( Either or Survivor), A wants premature payment be made to him as it is payable to either or survivor. Should bank pay to A alone before due date?

3. In case of Joint Fixed Deposit in name of A and B ( Former or Survivor) , B wants payment made to him on due date as it is to Former or survivor. Is bank right if bank pays to B on due date?

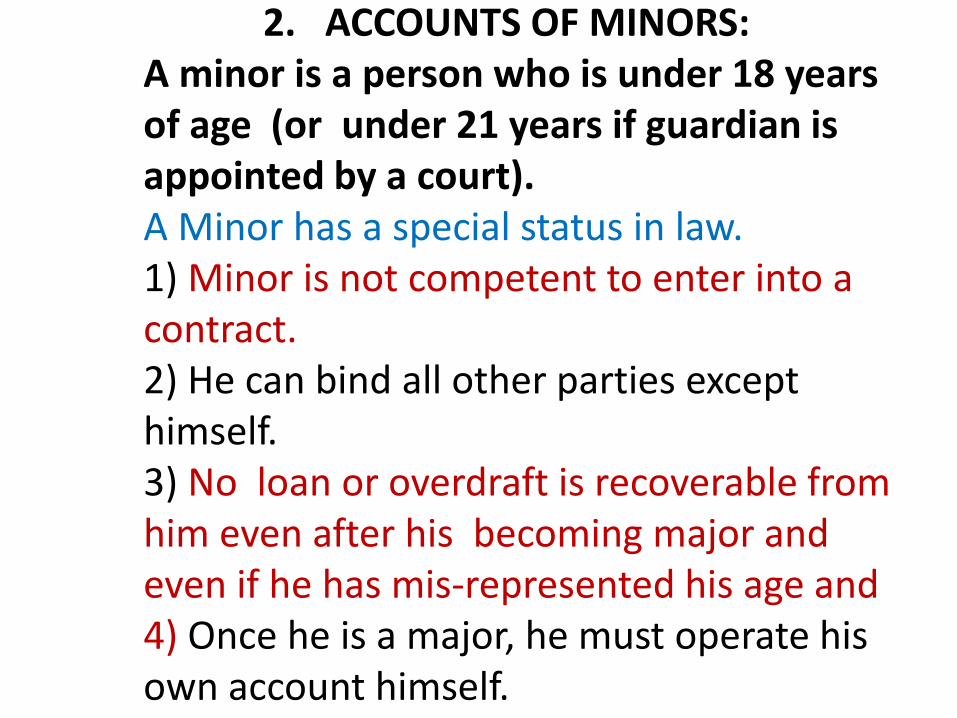

2. ACCOUNTS OF MINORS:A minor is a person who is under 18 years of age (or under 21 years if guardian is appointed by a court). A Minor has a special status in law. 1) Minor is not competent to enter into a contract. 2) He can bind all other parties except himself. 3) No loan or overdraft is recoverable from him even after his becoming major and even if he has mis-represented his age and 4) Once he is a major, he must operate his own account himself.

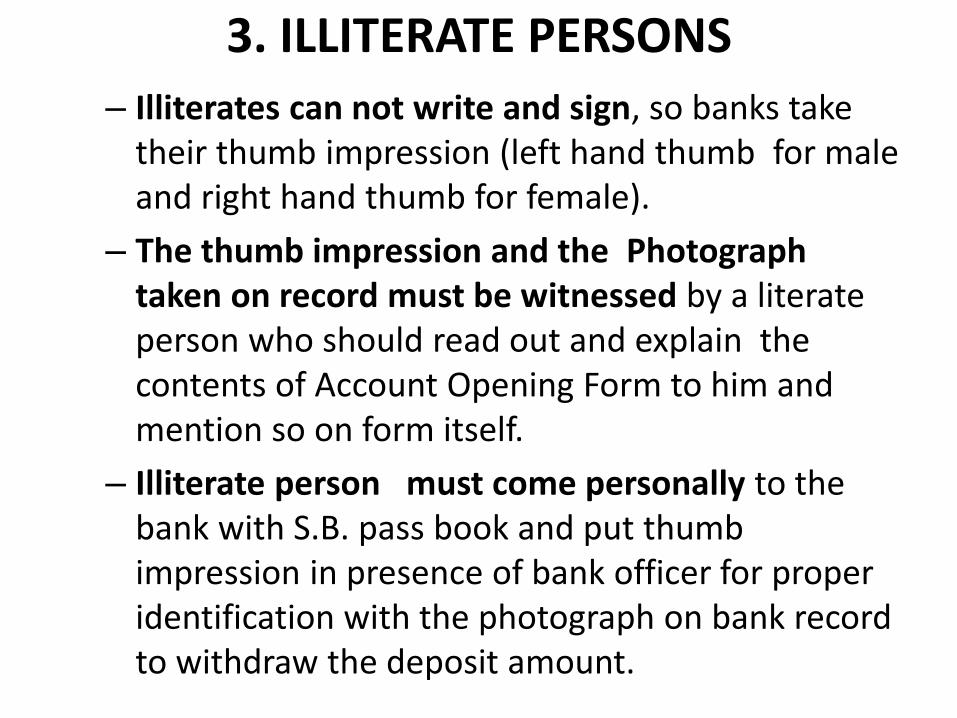

3. ILLITERATE PERSONS

– Illiterates can not write and sign, so banks take their thumb impression (left hand thumb for male and right hand thumb for female).

– The thumb impression and the Photograph taken on record must be witnessed by a literate person who should read out and explain the contents of Account Opening Form to him and mention so on form itself.

– Illiterate person must come personally to the bank with S.B. pass book and put thumb impression in presence of bank officer for proper identification with the photograph on bank record to withdraw the deposit amount.

4. FACILITY OF NOMINATION • Banking Companies (Nomination) Rules 1985 permit

banks to pay dues to nominees in the event of death of depositor(s) without asking for succession certificate or verifying claims of legal heirs.

• This simplifies settlement for bank and nominee• But the nominee is accountable to legal heirs as a Trustee

of money so received as a nominne from a bank .• Nomination facility is available for bank deposits, safe

deposit lockers, safe custody articles.• There can be only one Nominee for a deposit account

whether held singly or jointly.• There can be two nominees for a jointly held locker.• Minor can be a nominee but name of a major must be

given to receive money during minority of the minor. • A person legally empowered to operate a minor's account

(natural or court appointed guardian) can file a nomination on behalf of the minor