0 forwards, futures swaps and options workbook by ramon rabinovitch

TRANSCRIPT

1

Forwards, futures swaps and options

WORKBOOKBy

Ramon Rabinovitch

2

Introduction

Chapter 1

3

The Nature of Derivatives

A derivative is a financial instrument whose value depends on the values of other more basic underlying variables

In particular, it depends on the market price of the so called:

underlying asset.

4

Underlying assets:StocksBondsForeign currenciesGold, Silver…Crude oil, Natural gas, Gasoline, heating oil…Wheat, corn, rice, grain feed, soy beans,

porkbellies…Stock indexes

5

DERIVATIVES ARE CONTRAC TS:

FORWARDS

FUTURES

OPTIONS

SWAPS

6

WHY TRADE DERIVATIVES?

THE FUNDAMENTALREASON FOR TRADING

DERIVATIVES IS TO HEDGE: THE PRICE RISK

(VOLATILITY)Exhibited by the spot price of the

underlying commodity

7

PRICE RISK IS THE

VOLATILITYASSOCIATED WITH THE COMMODITY’S

PRICE IN THE CASH MARKET

REMEMBER THAT THE CASH MARKET IS WHERE FIRMS DO THEIR BUSINESS. I.E., BUY

AND SELL THE COMMODITY.

ZERO PRICE VOLATILITYNO DERIVATIVES!!!!

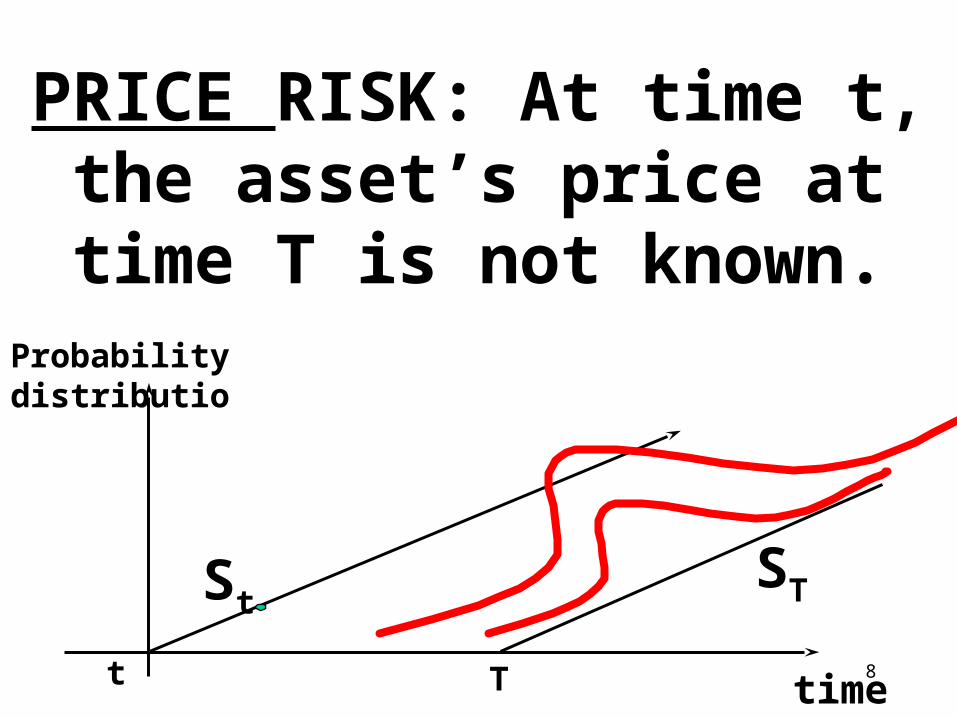

8t

Probability distributio

St

T time

ST

PRICE RISK: At time t, the asset’s price at time T is not

known.

9

Ways Derivatives are Used

• To hedge risks• To speculate (take a view on the

future direction of the market)• To lock in an arbitrage profit• To change the nature of a liability• To change the nature of an

investment without incurring the costs of selling one portfolio and buying another

10

Types of risk:Price riskCredit risk

Operational riskCompletion risk

Human riskRegulatory risk

Tax risk

11

IN THIS CLASS WE WILL ONLY ANALYZE THE

RISK ASSOCIATED WITH THESPOT MARKET PRICE

OFTHE UNDERLYING ASSET

12

DERIVATIVES ARE CONTRACTS:

Two parties

Agreement

Underlying security

Contract termination date

13

DERIVATIVES ARE CONTRACTSThe distinction is made by the different stipulations

of the contract

Forwards and Futures are Fixed obligations

A FORWARDIS A CONTRACT IN WHICH ONE PARTY COMMITS TO BUY AND THE OTHER PARTY COMMITS TO SELL A SPECIFIED

AMOUNT OF AN AGREED UPON COMMODITY FOR A PREDETERMINED PRICE ON A SPECIFIC DATE IN THE

FUTURE.

14

BUY = OPEN A LONG POSITIONSELL = OPEN A SHORT POSITION

t

Buy or sell a forward T Tim

e

Delivery and payment

15

Forward Price• The forward price for a contract

is the delivery price that would be applicable to the contract if were negotiated today (i.e., it is the delivery price that would make the contract worth exactly zero)

• The forward price may be different for contracts of different maturities

16

EXAMPLE: GBP 18.5.99

SPOT USD1,6850/GBP

30 days forward USD1,7245/GBP

60 days forward USD1,7455/GBP

90 days forward USD1,7978/GBP

180 days forward USD1,8455/GBP

The existence of forward exchange rates implies that there is a demand and supply for the GBP for future dates.

In the actual market, however, different rates are quoted for buy (ask) and for sell (bid) orders.

17

Foreign Exchange Quotes for USD/GBP on Aug 16, 2001 ( page 3)

Bid Offer

Spot 1.4452 1.4456

1-month forward 1.4435 1.4440

3-month forward 1.4402 1.4407

6-month forward 1.4353 1.4359

12-month forward 1.4262 1.4268

18

Profit from aLong Forward Position

Profit

Price of Underlying at Maturity, STK

19

Profit from a Short Forward Position

Profit

Price of Underlying at Maturity, STK

20

A FUTURES

A STANDARDIZED FORWARD TRADED ON AN ORGANIZED EXCHANGE.

STANDARDIZATION THE COMMODITY

TYPE AND QUALITY

THE QUANTITY

PRICE QUOTES

DELIVERY DATES

DELIVERY PROCEDURES

21

Futures Contracts

• Agreement to buy or sell an asset for a certain price at a certain time

• Similar to forward contract• Whereas a forward contract is

traded OTC, a futures contract is traded on an exchange

22

AN OPTION IS A CONTRACT IN WHICH ONE PARTY HAS THE RIGHT,

BUT NOT THE OBLIGATION, TO BUY OR SELL A SPECIFIED AMOUNT OF AN AGREED UPON COMMODITY

FOR A PREDETERMINED PRICE BEFORE OR ON A SPECIFIC DATE IN THE FUTURE. THE OTHER PARTY HAS

THE OBLIGATION TO DO WHAT THE FIRST PARTY WISHES TO DO. THE FIRST PARTY, HOWEVER, MAY

CHOOSE NOT TO EXERCISE ITS RIGHT AND LET THE OPTION EXPIRE WORTHLESS.

A CALL = A RIGHT TO BUY THE UNDERLYING ASSET

A PUT = A RIGHT TO SELL THE UNDERLYING ASSET

23

Long Call on Microsoft (Figure 1.2, Page 7)

Profit from buying a European call option on Microsoft: option price = $5, strike price = $60

30

20

10

0-5

30 40 50 60

70 80 90

Profit ($)

Terminalstock price ($)

24

Short Call on Microsoft (Figure 1.4, page 9)

Profit from writing a European call option on Microsoft: option price = $5, strike price = $60

-30

-20

-10

05

30 40 50 60

70 80 90

Profit ($)

Terminalstock price ($)

25

Long Put on IBM (Figure 1.3, page 8)

Profit from buying a European put option on IBM: option price = $7, strike price = $90

30

20

10

0

-790807060 100 110 120

Profit ($)

Terminalstock price ($)

26

Short Put on IBM (Figure 1.5, page 9)

Profit from writing a European put option on IBM: option price = $7, strike price = $90

-30

-20

-10

7

090

807060

100 110 120

Profit ($)Terminal

stock price ($)

27

A SWAPIS A CONTRACT IN WHICH THE TWO

PARTIES COMMIT TO EXCHANGE A SERIES OF CASH FLOWS. THE CASH FLOWS ARE BASED ON AN AGREED UPON PRINCIPAL

AMOUNT. NORMALLY, ONLY THE NET FLOW EXCHANGES HANDS.

Principal amount = EUR100,000,000; semiannual payments.

Party A Party B7%

6-months LIBOR

28

Types of Derivatives Traders• Speculators

• Hedgers

•ArbitrageursSome of the large trading losses in

derivatives occurred because individuals who had a mandate to

hedge risks switched to being speculators

29

THE ECONOMIC PURPOSES OF DERIVATIVE MARKETS

HEDGINGPRICE DISCOVERYSAVING

HEDGING IS THE ACTIVITY OF MANAGING PRICE RISK EXPOSURE

PRICE DISCOVERY IS THE REVEALINGOF INFORMSTION ABOUT THE FUTURECASH MARKET PRICE FOR A PRODUCT.

SAVING IS THE COST SAVING ASSOCIATED WITH SWAPING CASH FLOWS