analyst/investor day - nex.com · analyst/investor day june 2006. 2 ... capital markets...

TRANSCRIPT

1

Analyst/Investor Day

June 2006

2

These materials do not constitute an offer to sell or the solicitation of an offer to purchase any security. These materials contain "forward-looking statements" as defined in the U.S. Private Securities Litigation Reform Act of 1995. These statements are based on current Company expectations and are subject to risks and uncertainties, which could cause actual results to differ materially. Such risks and uncertainties include, but are not limited to: fluctuations in interest rates and foreign currency exchange rates; market acceptance of new trading technologies; global and regional economic conditions and legislative, regulatory and political developments; and domestic and international competition in the Company's global markets. Additional information regarding these and other factors is available in the Company's reports available on request from the Company.

This document may not be distributed where to do so would be unlawful. This document may not be distributed in the UK except to persons falling within article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001.

3

ICAP Americas

Ron Purpora - COODoug Rhoten - CEO

4

Securities Division – Voice and Hybrid

• Core Divisions– Treasury Products– Mortgage Securities– Federal Agency Issues– Repurchase Agreements– Corporate Products including

• Corporate Bonds• CDS• Emerging Markets• Equity and Related

5

Treasuries – Off-the-Run Products

12%

59%20%

6%

ICAPTullett-PrebonHill FarberBGC/Cantor

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 59%– Rank #1

• Hybrid Brokerage Service– 50% conducted electronically

with Brokertec– Enhanced group margins

• ICAP accounts for all electronic trading in this product group

• Dominant market shares in Bills, Short Coupons, TIP’s

6

Mortgage Securities

32%

31%

5%

3% 5%

24% ICAPTullett-PrebonHill FarberTraditionChapdelaineBGC

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 32%– Rank: Co-Leader

• Technology Deployed– Voice Service with proprietary

screens– Separate liquidity pools for e-

trading• ICAP accounts for all

electronic trading in this product group

• 36 brokers, 29% margin on Net Brokerage

• Developing products– Derivatives – CMBS, ABS

7

Agency Issues

75%

4%

20%

1%

ICAPTullett-PrebonBGCTradition

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 75%– Rank #1

• Technology Deployed– Voice service with proprietary

market screens– Separate liquidity pools for e-

trading• ICAP accounts for all

electronic trading in this product group

8

Repurchase Agreements

59%

6%3%3%

29%

ICAPTullett-PrebonBGCTraditionHill Farber

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 59%– Rank #1

• Franchise approach– Scale

• Technology Deployed– Separate liquidity pools for

exclusive e-trading– Hybrid capabilities among

franchises

9

Corporate Products – Corporate Bonds

34%

25%

14%

10%5%

12%

ICAPTullett-PrebonChapdelaineFIMATBGCOthers

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 34%– Rank #1

• Technology– Developing STP capabilities– Voice brokered markets– Lower liquidity

• Drivers– Transparency initiatives– CDS migration

10

Corporate Products – CDS

17%

8%10%

16%

12%

26%

11%

ICAPGFITullett-PrebonCreditExCreditTradeChapdelaineOthers

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 17%– Rank #2

• Established Single Name, EMK, Hi-Yield Index

• Growth in Structured, CMBS• Technology

– AffirmXpress• Automated confirmation

process offering significant efficiencies

• One of 3 participating brokers

– Hybrid Market development • Drivers

• Market take-up at expense of cash credit

• Consolidation

11

Capital Markets Introduction

• Divisions covered – Emerging Products– Structured Products– Equity Derivatives– Emerging Markets– Energy– Interest Rate Derivatives– Money Market– Foreign Exchange

12

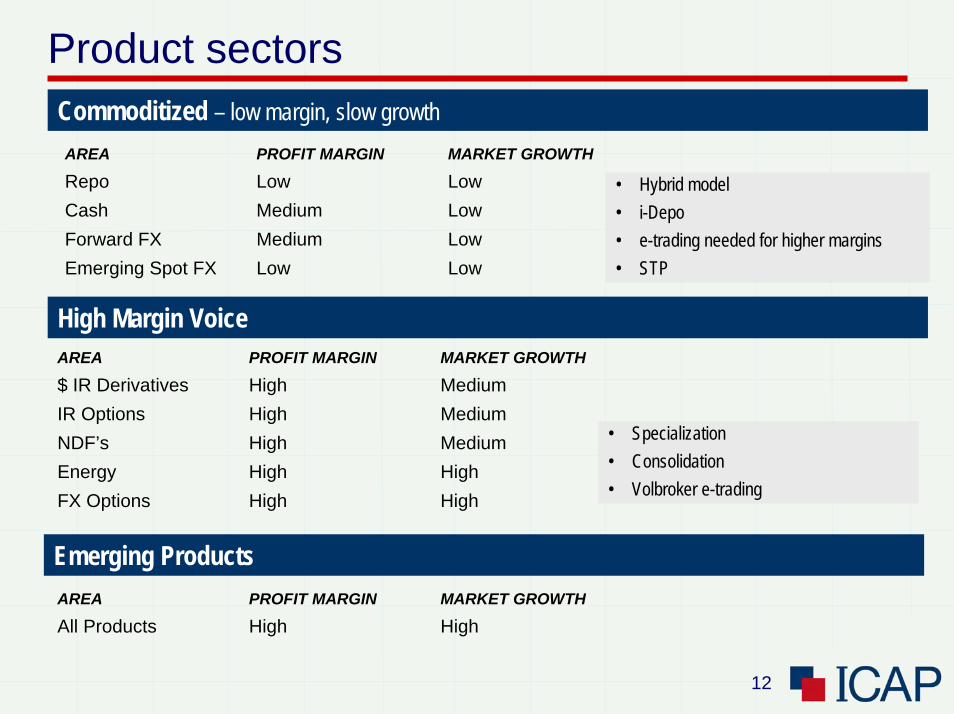

Product sectorsCommoditized – low margin, slow growthAREA PROFIT MARGIN MARKET GROWTH

Repo Low LowCash Medium LowForward FX Medium LowEmerging Spot FX Low Low

• Hybrid model• i-Depo• e-trading needed for higher margins• STP

High Margin VoiceAREA PROFIT MARGIN MARKET GROWTH

$ IR Derivatives High MediumIR Options High MediumNDF’s High MediumEnergy High HighFX Options High High

• Specialization• Consolidation• Volbroker e-trading

Emerging ProductsAREA PROFIT MARGIN MARKET GROWTH

All Products High High

13

Build Verbal Liquidity

• Market Share Goal: 35%• Production Specialization• Displace Customer Sales force• Invest in Emerging Products• Customers Help Drive Process

14

Creating Indices

• 19900 Telerate• CMM on Telerate 19944• ISDA Swapfix• Fed Funds (Telerate page 5)• SwapPX• GovPX• LatAm markets through Bloomberg• Mexico markets through Bloomberg• ICAP Markets Blog

15

Foreign Exchange – Voice market

65%

35%

ICAPTullett-Prebon

SpotSpot

ForwardsForwards

45%

15%

10%

30%

ICAPTullett-PrebonGFIOther

NDF’sNDF’s

40%15%

10%

35%

ICAPTullett-PrebonTraditionOther

16

Money Market

38%

17%

17%

28%

ICAPTullett-PrebonEurobrokersTradition

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 38%– Rank #1

• Technology– iFeds– Financial Oxygen STP

• Benchmark Index– Telerate Page 5

• Partnership– Financial Oxygen– (JP Morgan & BOA)

• Future Drivers– iFeds– Whole Loans– GSE’s

17

ICAP Voted Top Broker in…

• …22 Interest Rate and 11 Currency Derivatives groupings.

• Summary of 2005 Risk Survey Rankings:ICAP #1 in:– Interest Rate Swaps – Interest Rate Options – OIS – Cross Currency Swaps – FX Forwards– Credit Derivatives

18

$ Interest Rate Derivatives

40%13%

12%5%

30%

ICAPTullett-PrebonOtherGFITradition

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 40%– Rank #1

• Technology– FRACross– Swapswire STP– iSwap & Datatec

• Benchmark Index– Telerate 19900 & SwapPX– ISDA Swapfix

• Partnership– Swapswire– ISDA

• Drivers– FRACross– Short Swap push– Hybrid trading– Structured Products

19

Emerging Market Derivatives

50%12%

18%

20%

ICAPTullett-PrebonLocal BrokersGFI

Estimated Market Share – North AmericaEstimated Market Share – North AmericaHighlightsHighlights

• Market Share – 50%– Rank #1

• Technology– Datatec– Sipo

• Benchmark Index– 12 Bloomberg pages– LatAm PX

• Partnership– LatAm Stock Exchanges

• Drivers– FRACross– Chilean IRS– Colombian IRS– Asian IRS– Mexican CPI

20

Non-Securities GrowthHighlightsHighlights

01/02 02/03 03/04 04/05 05/06

Operating Profit

– Operating Profit Increased by 265%– Net Revenue Increases by 130% – Profit Margin Increased from 15% to 24%

01/02 02/03 03/04 04/05 05/06

Net Revenue

21

Macro Market TrendsKey Environmental Factors Impact on ICAP

Macroeconomic imbalances in commodities and credit

Price volatility. Growth in CDS, FX, Energy, Derivatives, Futures.

Search for Yield …………………….

Growth in structured credit, equity, commodity and interest rate products.

Commoditisation of “flow” markets…..

Higher volumes, polarized risk, e-trading opportunities and expanded customer base.

Agency to principle model equity markets …..

Supplement reduction in dealer sales forces.

Liberalization of emerging markets

Growth in local currency derivatives, fixed income and credit markets.

22

ICAP’s biggest opportunity

• Structured products • Equity derivatives• Emerging markets

Growth Products

Consolidation Opportunities

• Energy• Equity Derivatives• Equities

23

ICAP Voted ‘Best of the Best’…

• …within energy commodity markets

• The highest honor within the brokerage category … 2nd year running

24

Energy PositioningOpportunity - ConsolidationOpportunity - Consolidation

– Operating Profit Increased by 290%– Net Revenue Increases by 270%

01/02 02/03 03/04 04/05 05/06

Operating ProfitNet Revenue

25

LatAm StrategyOpportunity – Grow footprintOpportunity – Grow footprint

Drivers for Growth in the Market

• Continued liberalization of local LatAmmarkets

• NDF sectorization• Derivative sectorization• International distribution of local products

• SIF/Garban Mexico• Technology

– Datatec & Sipo• LatAm Expansion

– 5 Stock Exchange Joint Ventures– Purchase and merge 2 largest Colombian voice

brokers– Open Brazil branch

Our Positioning

26

Structured Products DivisionProducts Status

• Hired 10 broker Structured CDS team in 2005

• Hired 5 broker Index team

• #1 broker in FX Options

• Restructuring to combine with derivatives

• Structured CDS

• Structured Interest Rate

• FX Options

• Structured Notes

• Commodities

• Equity Derivatives/Exotics

27

Equity Derivatives

• Hyper growth in index products• Dealer move from agency to principle

model• Reduction of dealer sales forces• Expansion of customer base• Need for bilateral block trade negotiation• Sectorization of single names• Structured and exotic desk• Expand variance and correlation desk

28

Structured Interest Rate ProductsOpportunity – Pursue emerging sectorsOpportunity – Pursue emerging sectors

• Libor digital caps/floors• CMS spread caps/floors• Callable range accrual swaps• Capped callable floaters• Constant Maturity Mortgage• US CPI swaps/options• Other structured swaps

29

OpportunitiesEmerging Products Growth

• Energy Consolidation (Oil)

• Equity Derivatives

• Whole Loan Brokering

• Logistic Derivatives

• Electronic Trading

• Exotic Derivatives

• Structured CDS

• Structured Equities

• Real Estate Derivatives

30

Product evolution

Build Market Share

Commoditization

FosterBank

Interest

DevelopingProducts

Migration toelectronic

31

A Global E-broking Business

Jack JefferyCEO of ICAP Electronic Broking

32

A strategy for growth“ICAP’s e-strategy will create the largest global electronic

broker in liquid, commoditised OTC markets”

33

Foreign Exchange

34

Spot FX volumesGlobal FX Average Daily Volume - Single Count

0

20

40

60

80

100

120

140

160

180

200

Jan-9

6Ju

l-96

Jan-9

7Ju

l-97

Jan-9

8Ju

l-98

Jan-9

9Ju

l-99

Jan-0

0Ju

l-00

Jan-0

1Ju

l-01

Jan-0

2Ju

l-02

Jan-0

3Ju

l-03

Jan-0

4Ju

l-04

Jan-0

5Ju

l-05

Jan-0

6

US$

Bill

ions

Jun-0

6

35

Foreign Exchange• EBS Spot

– Average daily volumes - USD 145 billion– Record trading of USD 259 billion on 17 May 06– Top five trading days all recorded in 2006– >2,000 traders on >820 dealing floors across the globe

36

EBS Prime volumesEBS Prime Average Daily Volume (US$bn)

0

5

10

15

20

25

30

35

40

45

50

Jan-2

004

Mar-20

04May

-2004

Jul-2

004

Sep-20

04Nov

-2004

Jan-2

005

Mar-20

05May

-2005

Jul-2

005

Sep-20

05Nov

-2005

Jan-2

006

Mar-20

06May

-2006

US$

Bill

ions

37

Foreign Exchange• EBS Spot

– Average daily volumes - USD 145 billion– Record trading of USD 259 billion on 17 May 06– Top five trading days all recorded in 2006– >2,000 traders on >820 dealing floors across the globe

• EBS Prime– 149 users now live

• 37 non-bank customers including hedge funds• 112 bank customers

38

EBS Spot Ai - algorithmic trading volumes

EBS Ai Volume Trend Analysis

0

5

10

15

20

25

30

35

40

45

May-20

03Sep

-2003

Jan-2

004

May-20

04Sep

-2004

Jan-2

005

May-20

05Sep

-2005

Jan-2

006

May-20

06

0 %

5 %

10 %

15 %

20 %

25 %Ai Average Daily Volume ($ bil) Ai Market Share %

June

-2006

39

Foreign Exchange• EBS Spot

– Average daily volumes - USD 145 billion– Record trading of USD 259 billion on 17 May 06– Top five trading days all recorded in 2006– >2,000 traders on >820 dealing floors across the globe

• EBS Prime– 149 users now live

• 37 non-bank customers including hedge funds• 112 bank customers

• EBS Spot Ai– API or ‘black-box’ FX trading– Average daily volumes - USD 30 billion– Record day – 24 May 06 – USD 59.3 billion– 20% of EBS volumes from API-based trading

• EBS Market Data– The source of global spot FX pricing– Premium live feed and historical data commercialised

40

Fixed Income

41

Fixed income volumesAverage Daily Volume - Single Count

0

1

2

3

4

5

Apr-03

Jul-0

3Oct-

03Ja

n-04

Apr-04

Jul-0

4Oct-

04Ja

n-05

Apr-05

Jul-0

5Oct-

05Ja

n-06

Apr-06

US$

Bill

ions

Agency Mortgages Canadian Govt Euro GB Eurobonds

42

Fixed incomeAverage Daily Volume - Single Count

0

50

100

150

200

250

Apr-03

Jul-0

3Oct-

03Ja

n-04

Apr-04

Jul-0

4Oct-

04Ja

n-05

Apr-05

Jul-0

5Oct-

05Ja

n-06

Apr-06

US$

Bill

ions

UST US Repo EU Repo

43

Fixed income:US treasuries• Asia – US treasuries

– 65% market share for the past year

• London EU US Treasury Actives – Volume totalled a record $365 billion in May ‘06– Volumes continue to break records month over month– Volumes increasing each month in 06– 65% increase in volume from May 05– London market share ~ 60%

• US treasury volumes– volumes consistently above forecast in 06

44

Fixed Income US - Repo and Mortgages• US Repo

– Volumes remain healthy in face of new competition– Customer benefits

• Total Anonymity• STP• Significant cost saving benefits

• Mortgages– ICAP offers the only e-broking platform for Mortgage-Backed

Securities (MBS)• Continued growth in e-traded volumes• Customers seeing cost and STP benefits of e-broking • New functionality added

45

Fixed income: Eurobonds

• Launched in Feb 2006 across:– Bank capital– Industrials– Autos and Telecoms

• First electronic trading in CDS and Euro Credit bonds on the same front end

• Eurobonds– Volume of €959m in May 06 - up from €373m in April 06– June 06 volume so far €737m– 8% of business electronically traded (4.5% in April)– 11% so far in June

• Averaging 25 trades per day• 18 firms have so far traded Eurobonds with two further firms

enabled.• 38 traders have so far executed e-trades

46

EU Repo

• Repo daily volumes - €159 billion nominal single count daily

• 24% increase on June 05 (ICMA Repo survey saw 15-18% increase in outstanding Repo)

• Record volume day of €200 billion on 7 March 06

• Daily average Repo transactions is now at 5,000

47

Global trends in spot FX• Increasing cross-border trading activity

• Increasing proprietary risk taking at banks

• Growth of single and multi-dealer bank portals

• Growth of leveraged investors/hedge funds

• Growth of prime broking

• Continued development of algorithmic trading engines

• Liberalisation of emerging markets

48

Global trends in Fixed Income• Emerging markets offer opportunities for growth

• Algorithmic trading will force differentiation in trading models

• Integration of third party front, middle, and back office systems into trading platforms

• Increased competition among prime broking firms

• Migration towards e-execution for less liquid products

49

Foreign Exchange: New products

• Non–Deliverable Forwards– Estimated USD 1 trillion market (BIS 2003)– Provisional launch in Q4 2006

• Enhanced EBS Spot dealing screens– Offering up to 22 currency panels on one screen– Designed to facilitate:

• trading in multiple currencies• high frequency trading• placing more orders into the EBS market

50

Fixed income: New products

• North America– Canadian Government bonds – launched Q4 05– Credit Default Swaps – Q1 06– Yield Curve Swaps – In pilot– RP Cross

• Europe– Euro Eurobond sector– Euro-Sterling - roll-out Q4 06– Euro-Financials – in pilot phase

• Eurobonds issued by a financial corporate

51

Key drivers for success

Superior customer relationships1 Customer satisfaction2

A trusted global brand3 Focus on customer needs and market competition4

Maintaining and building the liquidity pool5 Unique product

selling points6

Solid and scaleable business model8Leading technology7

Talented and dedicated people9 Robust analysis10

52

ICAP Technology BriefingBusiness value creation through technology

Jay SpencerGlobal Chief Information Officer

53

ICAP IT Profile

TOTAL STAFF = 341

PRODUCT MANAGEMENT & DESIGN

PRODUCT DEVELOPMENT

CORE IT

DER

IVA

TIVE

S

FIN

AN

CIN

G

Application Development & Architecture

Infrastructure & Architecture

Market Data & Analytics Development

Production Support & Quality Assurance

Networks

OperationsSupport

Internal Systems

REP

OG

OVE

RN

MEN

TS

AG

ENC

IES

JGB

sM

OR

TGA

GES

CO

RPO

RA

TES

Equities Commodities Market Information /

Analytics

Fixed Income

SPO

T

FOR

WA

RD

S

CR

EDIT

DER

IVA

TIVE

SIR

S / I

-SW

AP

EXC

HA

NG

E TR

AD

ED

CLE

AR

ING

STR

UC

TUR

ED P

RO

DU

CTS

Emerging Markets

Derivatives FXFutures

54

EBS IT Profile

DER

IVA

TIVE

S

FIN

AN

CIN

G

REP

OG

OVE

RN

MEN

TS

AG

ENC

IES

JGB

sM

OR

TGA

GES

CO

RPO

RA

TES

SPO

T

FOR

WA

RD

S

CR

EDIT

DER

IVA

TIVE

SIR

S / I

-SW

AP

EXC

HA

NG

E TR

AD

ED

CLE

AR

ING

STR

UC

TUR

ED P

RO

DU

CTS

55

Key Management Drivers

• Ensure delivery commitments are met to support:– organic growth– balanced voice and electronic needs– product opportunities defined in corporate strategy

• Operation efficiency– execution on defined plans– cost savings and cost leverage

• IT business control

• “Legacy” synergies

• EBS integration

56

Keys to successful EBS Integration

• Minimize distraction to existing ICAP and EBS delivery schedules

• Retain critical players

• Get to steady state organization over next 12 months

• Apply “insourcing” options and flexibility built into EDS agreement

57

We know how to manage it; we’ve been here before

• Project funding

• Product plans; business-as-usual

• Most experienced players assigned to EBS Integration steering and delivery teams

• Protection key players with agreements

• Timely organisational changes

58

Leverage from the EBS acquisition

• Product knowledge

• Development resources and capacity with similar skills

• IT Infrastructure expertise

• Globally based solutions team and operations support

• Major conversion to new infrastructure completed by EBS

59

Primary Synergy Opportunities

• Redundant capex spend• Overlapping networks and costs to support • Consolidated System Command Center and operations

staff• Consolidated IT facilities and centers• Duplicated Telecoms• EDS contract savings• Overlapping organisation functions

60

Future Opportunities

• New revenue opportunity – leverage trading architectures

• Front end consolidation – “application container” architecture

• Diverse matching technology

61

Summary Slide

• We have the resources

• We have the capability

• We make efficient use of capital

• Above all, we have a unique blend, range and distinct

combination of product and technical skill

62

Steve McDermott Executive Director, ICAP

Integration of EBS and ICAP

63

Introduction

• Maintaining momentum in the business

• Clarity of overall business objectives

• A dedicated project management office to oversee the process of integration

• Impressive people and the technology

• Prioritising the immediate decisions

64

Transaction synergies (21 April 2006)

IT Network: $9m

IT Infrastructure: $10m

Other IT: $2m

Property and other: $11m

0

5

10

15

20

25

30

35

2006/7 2007/8 2008/9 Full Impact

Projected Transaction SynergiesUS$ millionsProjected Transaction SynergiesUS$ millions

Sources of SynergiesUS$ millionsSources of SynergiesUS$ millions

TechnologyNon-Technology$m

$24m

Cost toAchieve

Note: The costs to achieve the synergies of $24 million will be treated as an “exceptional” item in the income statement in 2006/7 and 2007/8

$32m

65

Integration

• IT- People, Network and Hardware

• ICAP Electronic Broking - Sales, Product, Marketing

• Support - Property, HR, Finance, Legal and Compliance

• Combining the cultures

66

Challenges

• e-broking now substantial business

• Recognition of the power of e-broking and greater understanding in voice business of benefits

• Committed to investing to building the e-business further

• Potential revenue synergies

• Staying ahead of the curve

67

Investor Relations queries to :

Mike SheardDirector of Corporate AffairsICAP plc2 BroadgateLondon EC2M 7UR(44) 207 050 [email protected]