© the mcgraw-hill companies, inc., 2007 appendix d accounting for partnerships

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2007

Appendix D

Accounting for Partnerships

© The McGraw-Hill Companies, Inc., 2007

Conceptual Chapter Objectives

C1: Identify characteristics of partnerships and similar organizations

© The McGraw-Hill Companies, Inc., 2007

Analytical Chapter Objectives

A1: Compute partner return on equity and use it to evaluate partnership performance

© The McGraw-Hill Companies, Inc., 2007

Procedural Chapter Objectives

P1: Prepare entries for partnership formation

P2: Allocate and record income and loss among partners

P3: Account for the admission and withdrawal of partners

P4: Prepare entries for partnership liquidation

© The McGraw-Hill Companies, Inc., 2007

Partnership Form of Organization

Partnership Agreement

Partnership Agreement

Voluntary Association

Voluntary Association

Limited Life

Limited Life

TaxationTaxation

Unlimited Liability

Unlimited Liability

Mutual Agency

Mutual Agency Co-

Ownership of Property

Co-Ownership of Property

C1

© The McGraw-Hill Companies, Inc., 2007

Organizations with Partnership Characteristics

Limited Partnerships

(LP)

Limited Partnerships

(LP)

•General partners assume management duties and unlimited liability for partnership debts.•Limited partners have no personal liability beyond invested amounts.

•General partners assume management duties and unlimited liability for partnership debts.•Limited partners have no personal liability beyond invested amounts.

Limited Liability

Partnerships(LLP)

Limited Liability

Partnerships(LLP)

•Protects innocent partners from malpractice or negligence claims.

•Most states hold all partners personally liable for partnership debts.

•Protects innocent partners from malpractice or negligence claims.

•Most states hold all partners personally liable for partnership debts.

Limited Liability

Corporations

(LLC)

Limited Liability

Corporations

(LLC)

•Owners have same limited liability feature as owners of a corporation.

•A limited liability corporation typically has a limited life.

•Owners have same limited liability feature as owners of a corporation.

•A limited liability corporation typically has a limited life.

C1

© The McGraw-Hill Companies, Inc., 2007

Choosing a Business FormProprietorship Partnership LLP LLC S Corp. Corporation

Business entity yes yes yes yes yes yesLegal entity no no no yes yes yesLimited liability no no limited* yes yes yesBusiness taxed no no no no no yesOne owner allowed yes no no yes yes yes

*A partner's personal liability for LLP debts is limited. Most LLPs carry insurance to protect against malpractice.

Many factors should be considered when choosing the proper business form.

Many factors should be considered when choosing the proper business form.

C1

© The McGraw-Hill Companies, Inc., 2007

Organizing a PartnershipPartners can invest both assets and liabilities in the

partnership.Partners can invest both assets and liabilities in the

partnership.

Assets and liabilities are recorded at an agreed-upon value, normally fair market value.

Assets and liabilities are recorded at an agreed-upon value, normally fair market value.

Asset contributions increase the partner’s capital account.

Asset contributions increase the partner’s capital account.

Withdrawals from the partnership decrease the partner’s capital account.

Withdrawals from the partnership decrease the partner’s capital account.

P1

© The McGraw-Hill Companies, Inc., 2007

Organizing a PartnershipOn 2/15/08, Smith and Jones form a partnership. Smith contributes $80,000 cash. Jones contributes land valued at

$40,000.

On 2/15/08, Smith and Jones form a partnership. Smith contributes $80,000 cash. Jones contributes land valued at

$40,000.Feb. 15 Cash 80,000

Land 40,000 Smith, Capital 80,000 Jones, Capital 40,000

To record initial investment in partnership

P1

© The McGraw-Hill Companies, Inc., 2007

Dividing Income or Loss

Three frequently used methods to divide income or loss are allocation on:

1. Stated ratios.2. Capital balances.3. Services, capital and stated ratios.

Three frequently used methods to divide income or loss are allocation on:

1. Stated ratios.2. Capital balances.3. Services, capital and stated ratios.

Partners are not employees of the partnership but are its owners. This means there are no salaries reported as expense on the income statement. Profits or losses of the partnership are divided on some agreed upon ratio.

P2

© The McGraw-Hill Companies, Inc., 2007

Allocation Based on Stated Ratios

Smith and Jones agree to divide profits or losses ¾ for Smith and ¼ for Jones. For 2008, the partnership reported net income of $60,000.

Dec. 31 Income Summary 60,000 Smith, Capital 45,000 Jones, Capital 15,000

To record division of 2008 net income.

$60,000 × ¾ = $45,000

P2

© The McGraw-Hill Companies, Inc., 2007

Allocation Based on Capital Balances

Smith’s capital balance, before division of profits or losses is $80,000 and Jones’s capital balance is $40,000. The partnership agreement calls for income or loss to be allocated based on the relative capital balances. Net income for 2008 is $60,000.

Smith’s capital balance, before division of profits or losses is $80,000 and Jones’s capital balance is $40,000. The partnership agreement calls for income or loss to be allocated based on the relative capital balances. Net income for 2008 is $60,000.

Balance Ratio Income AllocationSmith, Capital 80,000$ 66.67% 60,000$ 40,000$ Jones, Capital 40,000 33.33% 60,000 20,000 Totals 120,000$ 100.00% 60,000$

P2

© The McGraw-Hill Companies, Inc., 2007

Allocation Based on Capital Balances

Smith’s capital balance, before division of profits or losses is $80,000 and Jones’s capital balance is $40,000. The partnership agreement calls for income or loss to be allocated based on the relative capital balances. Net income for 2008 is $60,000.

Smith’s capital balance, before division of profits or losses is $80,000 and Jones’s capital balance is $40,000. The partnership agreement calls for income or loss to be allocated based on the relative capital balances. Net income for 2008 is $60,000.

Dr. Cr. Dec. 31 Income Summary 60,000

Smith, Capital 40,000 Jones, Capital 20,000

To record division of 2008 net income.

P2

© The McGraw-Hill Companies, Inc., 2007

Allocation Based on Services, Capital, and Stated Ratios

Smith and Jones have a partnership agreement with the following conditions:

Smith receives $15,000 and Jones receives $10,000 as annual salaries.

Each partner is allowed an annual interest allowance of 5% on the beginning-of-year capital balance.

Any remaining balance of income or loss is allocated equally.

Net income for 2008 is $60,000.

Smith and Jones have a partnership agreement with the following conditions:

Smith receives $15,000 and Jones receives $10,000 as annual salaries.

Each partner is allowed an annual interest allowance of 5% on the beginning-of-year capital balance.

Any remaining balance of income or loss is allocated equally.

Net income for 2008 is $60,000.

P2

© The McGraw-Hill Companies, Inc., 2007

Smith Jones Remainder60,000$

15,000$ 10,000$ 35,000 4,000 2,000 29,000

14,500 14,500 - 33,500 26,500

SalariesNet income

Income Distribution

InterestEqual allocationIncome to each partner

Allocation Based on Services, Capital, and Stated Ratios

Smith Jones Remainder60,000$

15,000$ 10,000$ 35,000 4,000 2,000 29,000

14,500 14,500 - 33,500 26,500

SalariesNet income

Income Distribution

InterestEqual allocationIncome to each partner

Smith Jones Remainder60,000$

15,000$ 10,000$ 35,000 4,000 2,000 29,000

14,500 14,500 - 33,500 26,500

SalariesNet income

Income Distribution

InterestEqual allocationIncome to each partner

Smith Jones Remainder60,000$

15,000$ 10,000$ 35,000 4,000 2,000 29,000

14,500 14,500 - 33,500 26,500

InterestEqual allocationIncome to each partner

Net income

Income Distribution

Salaries

$80,000 × 5% = $4,000$80,000 × 5% = $4,000

$29,000 × ½ = $14,500$29,000 × ½ = $14,500

P2

© The McGraw-Hill Companies, Inc., 2007

Partnership Financial Statements

TotalBeginning capital balances -$ -$ -$ Investments by owners 80,000 40,000 120,000 Net income Salary allowances 15,000$ 10,000$ Interest allowances 4,000 2,000 Balance allocated 14,500 14,500 Total net income 33,500 26,500 60,000 Less partners' withdrawals (5,000) (1,000) (6,000) Ending capital balances 108,500$ 65,500$ 174,000

Smith Jones

Smith and Jones PartnershipStatement of Partners' Equity

For the Year Ended December 31, 2008

Assume that during 2008, Smith withdrew $5,000 cash from the partnership and Jones withdrew $1,000.

P2

© The McGraw-Hill Companies, Inc., 2007

Allocation Based on Services, Capital, and Stated Ratios

Smith and Jones have a partnership agreement with the following conditions:

Smith receives $15,000 and Jones receives $10,000 as annual salaries.

Each partner is allowed an annual interest allowance of 5% on the beginning-of-year capital balance.

Any remaining balance of income or loss is allocated equally.

Net income for 2008 is $30,000.

Smith and Jones have a partnership agreement with the following conditions:

Smith receives $15,000 and Jones receives $10,000 as annual salaries.

Each partner is allowed an annual interest allowance of 5% on the beginning-of-year capital balance.

Any remaining balance of income or loss is allocated equally.

Net income for 2008 is $30,000.

P2

© The McGraw-Hill Companies, Inc., 2007

Allocation on Services, Capital, and Stated Ratios

Smith Jones Remainder30,000$

15,000$ 10,000$ 5,000 4,000 2,000 (1,000) (500) (500) -

18,500 11,500

SalariesNet income

Income Distribution

InterestEqual allocationIncome to each partner

($1,000) × ½ = $500($1,000) × ½ = $500

P2

© The McGraw-Hill Companies, Inc., 2007

Admission and Withdrawal of Partners

When the makeup of the partnership changes, the partnership is dissolved.

A new partnership may be immediately formed.

New partner acquires partnership interest by:

1. Purchasing it from the other partners, or

2. Investing assets in the partnership.

When the makeup of the partnership changes, the partnership is dissolved.

A new partnership may be immediately formed.

New partner acquires partnership interest by:

1. Purchasing it from the other partners, or

2. Investing assets in the partnership.

P3

© The McGraw-Hill Companies, Inc., 2007

Admission of a Partner

A new partner can purchase partnership interest directly from the existing partners. The cash goes to the partners,

not to the partnership. To become a partner, the new

partner must be accepted by the current partners.

A new partner can purchase partnership interest directly from the existing partners. The cash goes to the partners,

not to the partnership. To become a partner, the new

partner must be accepted by the current partners.

Purchase of Partnership Interest

P3

© The McGraw-Hill Companies, Inc., 2007

On January 2, 2009, Jones agrees to sell Johnson $10,000 of her partnership interest for $25,000 cash. Smith agrees with this. arrangement.

Purchase of Partnership Interest

Smith Jones Johnson TotalCapital balances before new partner 108,500$ 65,500$ -$ 174,000$ Allocation to new partner (10,000) 10,000 - Capital balances after new partner 108,500$ 55,500$ 10,000$ 174,000$

Jan 2 Jones, Capital 10,000 Johnson, Capital 10,000

To record admission of new partner

P3

© The McGraw-Hill Companies, Inc., 2007

Investing Assets in a Partnership

The new partner can gain partnership interest by contributing assets to the partnership.

The new assets will increase the partnership’s net assets.

After admission, both assets and equity will increase.

The new partner can gain partnership interest by contributing assets to the partnership.

The new assets will increase the partnership’s net assets.

After admission, both assets and equity will increase.

P3

© The McGraw-Hill Companies, Inc., 2007

On January 2, 2009, Smith and Jones agree to accept Johnson as a partner upon his investment of $30,000 cash in the partnership.

Investing Assets in a Partnership

Smith Jones Johnson TotalCapital balances before new partner 108,500$ 65,500$ -$ 174,000$ Allocation to new partner 30,000 30,000 Capital balances after new partner 108,500$ 65,500$ 30,000$ 204,000$

Jan 2 Cash 30,000 Johnson, Capital 30,000

To record admission of new partner

P3

© The McGraw-Hill Companies, Inc., 2007

Bonus to Old or New Partners

Bonus to Old Partners

Bonus to Old Partners

When the current value of a partnership is greater than the recorded amounts of equity, the old partners usually require a new partner to pay a bonus when joining.

When the current value of a partnership is greater than the recorded amounts of equity, the old partners usually require a new partner to pay a bonus when joining.

Bonus to New Partners

Bonus to New Partners

The partnership may grant a bonus to a new partner if the business is in need of cash or if the new partner has exceptional talents.

The partnership may grant a bonus to a new partner if the business is in need of cash or if the new partner has exceptional talents.

P3

© The McGraw-Hill Companies, Inc., 2007

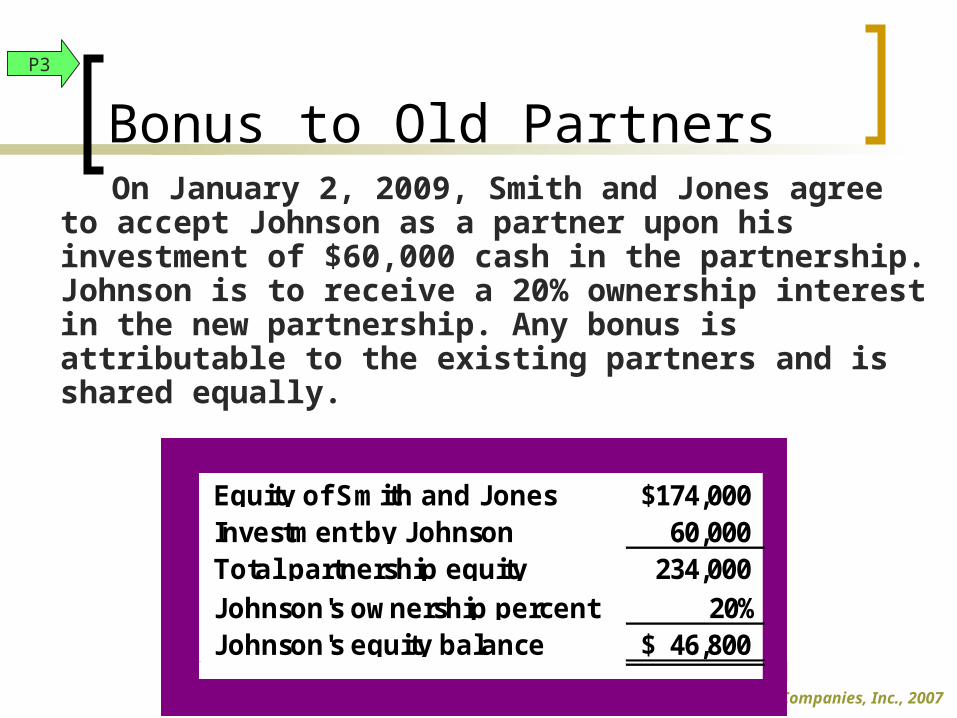

Bonus to Old Partners On January 2, 2009, Smith and Jones agree to

accept Johnson as a partner upon his investment of $60,000 cash in the partnership. Johnson is to receive a 20% ownership interest in the new partnership. Any bonus is attributable to the existing partners and is shared equally.

174,000$ 60,000

234,000 20%

46,800$

Investment by JohnsonEquity of Smith and Jones

Total partnership equityJohnson's ownership percentJohnson's equity balance

P3

© The McGraw-Hill Companies, Inc., 2007

Bonus to Old Partners On January 2, 2009, Smith and Jones agree to

accept Johnson as a partner upon his investment of $60,000 cash in the partnership. Johnson is to receive a 20% ownership interest in the new partnership. Any bonus is attributable to the existing partners and is shared equally.

Dr. Cr. Jan 2 Cash 60,000

Johnson, Capital 46,800 Smith, Capital 6,600 Jones, Capital 6,600

To record admission of new partner

$60,000 - $46,800 = $13,200 × ½ = $6,600$60,000 - $46,800 = $13,200 × ½ = $6,600

P3

© The McGraw-Hill Companies, Inc., 2007

Bonus to New Partner On January 2, 2009, Smith and Jones agree to accept

Johnson as a partner upon his investment of $60,000 cash in the partnership. Johnson is to receive a 30% ownership interest in the new partnership. Any bonus is attributable to the new partner and is shared equally by the existing partners.

174,000$ 60,000

234,000 30%

70,200$

Investment by JohnsonEquity of Smith and Jones

Total partnership equityJohnson's ownership percentJohnson's equity balance

P3

© The McGraw-Hill Companies, Inc., 2007

Bonus to New Partner On January 2, 2009, Smith and Jones agree to accept

Johnson as a partner upon his investment of $60,000 cash in the partnership. Johnson is to receive a 30% ownership interest in the new partnership. Any bonus is attributable to the new partner and is shared equally by the existing partners.

Dr. Cr. Jan 2 Cash 60,000

Smith, Capital 5,100 Johnson, Capital 5,100

Johnson, Capital 70,200 To record admission of new partner

$70,200 - $60,000 = $10,200 × ½ = $5,100$70,200 - $60,000 = $10,200 × ½ = $5,100

P3

© The McGraw-Hill Companies, Inc., 2007

Withdrawal of a Partner

A partner can withdraw in two ways:

The partner can sell his/her partnership interest to another person.

The partnership can distribute cash and/or other assets to the withdrawing partner.

A partner can withdraw in two ways:

The partner can sell his/her partnership interest to another person.

The partnership can distribute cash and/or other assets to the withdrawing partner.

P3

© The McGraw-Hill Companies, Inc., 2007

Withdrawal of a Partner Jones has a capital balance of $65,500. She decides to withdraw from the partnership of Smith, Jones, and Johnson for $50,000 cash. Any bonus is attributable to the remaining partners and is divided equally.

Jones has a capital balance of $65,500. She decides to withdraw from the partnership of Smith, Jones, and Johnson for $50,000 cash. Any bonus is attributable to the remaining partners and is divided equally.

Dr. Cr. Jan 2 Jones, Capital 65,500

Cash 50,000 Smith, Capital 7,750 Johnson, Capital 7,750

To record withdrawal of partner

$65,500 - $50,000 = $15,500 × ½ = $7,750$65,500 - $50,000 = $15,500 × ½ = $7,750

P3

© The McGraw-Hill Companies, Inc., 2007

Liquidation of a Partnership

When a partnership is dissolved, four steps are required:

Noncash assets are sold for cash and a gain or loss on liquidations is recorded.

Gain or loss on liquidation is allocated to partners using their income-and-loss ratio.

Liabilities are paid or settled.

Any remaining cash is distributed to partners based on their capital balances.

When a partnership is dissolved, four steps are required:

Noncash assets are sold for cash and a gain or loss on liquidations is recorded.

Gain or loss on liquidation is allocated to partners using their income-and-loss ratio.

Liabilities are paid or settled.

Any remaining cash is distributed to partners based on their capital balances.

P4

© The McGraw-Hill Companies, Inc., 2007

No Capital Deficiency No capital deficiency means that all partners have a zero or credit balance in their capital accounts.No capital deficiency means that all partners have a zero or credit balance in their capital accounts.

Smith, Jones, and Johnson agree to dissolve their partnership. They sell all of their assets for a net gain of $10,000. Profits and losses are shared as follows: Smith, ½; Jones, ¼; and Johnson, ¼.

Smith, Jones, and Johnson agree to dissolve their partnership. They sell all of their assets for a net gain of $10,000. Profits and losses are shared as follows: Smith, ½; Jones, ¼; and Johnson, ¼.

Smith Jones Johnson TotalBeginning capital balances 108,500$ 65,500$ 30,000$ 204,000$ Allocation of $10,000 net gain 5,000 2,500 2,500 10,000 Capital balances for dissolution 113,500$ 68,000$ 32,500$ 214,000$

Dr. Cr. Dec 2 Smith, Capital 113,500

Jones, Capital 68,000 Johnson, Captial 32,500

Cash 214,000 To liquidate partnership

P4

© The McGraw-Hill Companies, Inc., 2007

Capital Deficiency

Smith Jones Johnson TotalBeginning capital balances 25,000$ 10,000$ 2,000$ 37,000$ Allocation of $10,000 net loss (5,000) (2,500) (2,500) (10,000) Subtotal 20,000 7,500 (500) 27,000 Contribution by Johnson 500 500 Capital balances for dissolution 20,000$ 7,500$ -$ 27,500$

Capital deficiency means that at least one partner has a debit balance in his/her capital account. A partner with a deficit must, if possible, cover the deficit by paying cash into the partnership.

Capital deficiency means that at least one partner has a debit balance in his/her capital account. A partner with a deficit must, if possible, cover the deficit by paying cash into the partnership.

Smith, Jones, and Johnson agree to dissolve their partnership. They sell all of their assets for a net loss of $10,000. Profits and losses are shared as follows: Smith, ½; Jones, ¼; and Johnson, ¼.

Smith, Jones, and Johnson agree to dissolve their partnership. They sell all of their assets for a net loss of $10,000. Profits and losses are shared as follows: Smith, ½; Jones, ¼; and Johnson, ¼.

P4

© The McGraw-Hill Companies, Inc., 2007

Capital Deficiency

Dec 2 Cash 500 Johnson, Capital 500

To make-up deficiency

Dec 2 Smith, Capital 20,000 Jones, Capital 7,500

Cash 27,500 To liquidate partnership

Smith Jones Johnson TotalBeginning capital balances 25,000$ 10,000$ 2,000$ 37,000$ Allocation of $10,000 net loss (5,000) (2,500) (2,500) (10,000) Subtotal 20,000 7,500 (500) 27,000 Contribution by Johnson 500 500 Capital balances for dissolution 20,000$ 7,500$ -$ 27,500$

Any partner’s unpaid deficiency is

absorbed by the remaining partners

with credit balances in accordance

with the partnership agreement.

P4

© The McGraw-Hill Companies, Inc., 2007

Death of a Partner

A partner’s death dissolves a partnership.

A deceased partner’s estate is entitled to receive the equity.

This usually requires closing the books to determine the net income or loss at the date of death and also recording market values for assets and liabilities.

P4

© The McGraw-Hill Companies, Inc., 2007

Partner Return on Equity

Partner returnon equity

Partner net incomeAverage partner equity

=

Total LP I LP II Celtics LPBalance, Beginning of year 84$ 122$ (307)$ 270$ Net income (loss) for year 216 44 61 111 Cash distribution (48) - - (48) Balance, End of year 252$ 166$ (246)$ 333$

Partner return on equity 128.6% 30.6% NA 36.8%

Boston Celtics

A4

© The McGraw-Hill Companies, Inc., 2007

End of Appendix D