© boardworks ltd 2007 1 of 22 cash flow forecasts teacher’s notes included in the notes pageflash...

TRANSCRIPT

© Boardworks Ltd 20071 of 22

Cash Flow Forecasts

Teacher’s notes included in the Notes PageFlash activity. These activities are not editable.

Icons key: For more detailed instructions, see the Getting Started presentation

Cash Flow Forecasts Unit 3: Business Finance

Web addressesExtension activities Sound

© Boardworks Ltd 20071 of 22

© Boardworks Ltd 20072 of 22

Learning objectives

What is a cash flow forecast?

How are cash flow forecasts constructed?

How are cash flow forecasts used by businesses?

How is ICT used in cash flow forecasts?

© Boardworks Ltd 20072 of 22

© Boardworks Ltd 20073 of 22

Cash flow forecasts

A cash flow forecast is a prediction of the future flows of money in and out of the business for a specified period of time. A cash flow forecast shows, month by month, the money that it is anticipated will be coming into the business and the money that the business will be paying out. The working capital is the money available after the business has paid out all the money owing.

Cash flow is the money coming into a business (the income or inflows) and the money going out of the business (the expenditure or outflows). For a business to profit, more money needs to be flowing in than out.

© Boardworks Ltd 20074 of 22

Inflows and outflows

© Boardworks Ltd 20075 of 22

Why do businesses forecast cash flow?

decide whether to expand or reduce existing activities

decide whether to produce new goods or services, invest in new resources or carry out new activities

identify any potential deficits and allow the business to plan ahead for them

identify any potential surpluses so that the business can use this money to their benefit.

Cash flow forecasts can be used to:

Producing a cash flow forecast allows a business to plan how much money the business will have at any given time. This information can then be used to make decisions about business activities.

© Boardworks Ltd 20076 of 22

How to construct a basic cash flow forecast

A spreadsheet program is normally used for completing simple cash-flow forecasts.

Here, the headings of the six columns are the first six months of the year. Cash flow forecasts are normally done on a monthly basis for either six or twelve months ahead.

The first column shows the amount of money the business expects to receive during January.

A total is calculated at the bottom of this column.January February March April May June

InflowsSales revenue 143,000 150,000 209,000 180,000 195,000 198,000Loans 20,000 0 0 0 0 0Grants 0 0 0 0 0 0Investors' capital 0 0 0 5,000 0 0

© Boardworks Ltd 20077 of 22

How to construct a basic cash flow forecast

OutflowsStock 30,000 28,000 28,500 31,200 29,000 29,800Wages 110,000 110,000 110,000 110,000 115,000 115,000Rent 4000 4000 4000 4000 4000 4000Utility bills 1000 1000 1000 1000 1000 1000Interest on loans 2000 2000 2000 2000 2000 2000Taxes 500 500 500 500 500 500Advertising 12,000 13,000 12,000 15,000 12,000 14,000Total outflows 159,500 158,500 158,000 163,700 163,500 166,300

The next section shows the amount of money the business expects to spend – its outflows. A total is calculated for each month.

© Boardworks Ltd 20078 of 22

How to construct a basic cash flow forecast

The final section shows the opening balance for the month – this is the same as the closing balance from the month before.

The next row shows the net cash flow. This is the total inflows minus the total outflows, i.e. the amount of money it is predicted the business will make in that month.

The final row is the closing balance. This is worked out by adding the net cash flow to the opening balance.

Monthly summaryOpening bank balance 20,000 23,500 15,000 66,000 87,300 118,800Net cash flow 3,500 -8,500 51,000 21,300 31,500 31,700Closing bank balance 23,500 15,000 66,000 87,300 118,800 150,500

What do you notice about the net cash flow predicted for February?

© Boardworks Ltd 20079 of 22

How to construct a basic cash flow forecast

January February March April May JuneInflowsSales revenue 143,000 150,000 209,000 180,000 195,000 198,000Loans 20,000 0 0 0 0 0Grants 0 0 0 0 0 0Investors' capital 0 0 0 5,000 0 0Total inflows 163,000 150,000 209,000 185,000 195,000 198,000

OutflowsStock 30,000 28,000 28,500 31,200 29,000 29,800Wages 110,000 110,000 110,000 110,000 115,000 115,000Rent 4000 4000 4000 4000 4000 4000Utility bills 1000 1000 1000 1000 1000 1000Interest on loans 2000 2000 2000 2000 2000 2000Taxes 500 500 500 500 500 500Advertising 12,000 13,000 12,000 15,000 12,000 14,000Total outflows 159,500 158,500 158,000 163,700 163,500 166,300

Monthly summaryOpening bank balance 20,000 23,500 15,000 66,000 87,300 118,800Net cash flow 3,500 -8,500 51,000 21,300 31,500 31,700Closing bank balance 23,500 15,000 66,000 87,300 118,800 150,500

© Boardworks Ltd 200710 of 22

Indicating a negative cash flow

Positive cash flow is when the inflows are greater than the outflows. Negative cash flow occurs when the outflows are greater than the inflows.

If any figure (net cash flow, opening balance, closing balance, etc.) is a negative number, then it is shown either with a minus sign or between brackets, e.g. (£8,500).

The money it is predicted will be lost is called the deficit. The money it is predicted will be gained is called the surplus. Be careful not to use the words profit and loss – these describe actual figures rather than future predictions.

© Boardworks Ltd 200711 of 22

Complete a basic cash flow forecast

© Boardworks Ltd 200712 of 22

Simon’s new car

Simon Harris wants to buy a new car to take to university in September. He has estimated that a good second hand car will cost him £2500. Simon’s dad has agreed to give him £1500 at the end of August as an early birthday present, to help him buy the car.

At the start of March, Simon had £450 in his bank account. He earns £150 a month working with his uncle.

Simon is going to try and cut down on his spending. He estimates that he will spend £30 a month on clothes, magazines and music, and £25 a month socialising with his friends.

© Boardworks Ltd 200713 of 22

Simon’s new car – a cash flow forecast

© Boardworks Ltd 200714 of 22

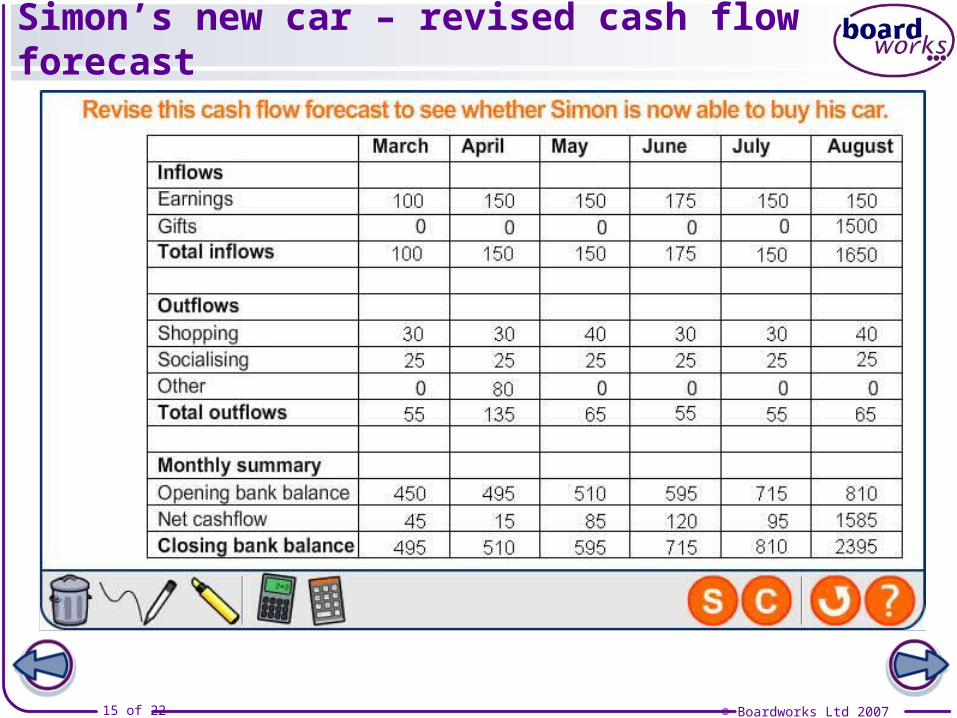

Simon’s new car

The following information is what actually happened to Simon. Revisit the cash flow forecast on the next slide and decide whether Simon can still afford his car.

Simon spent £40 shopping in May and August.He worked a few extra hours in June and earned

£175.He spent £80 going to a music festival in April.He only earned £100 in March.

© Boardworks Ltd 200715 of 22

Simon’s new car – revised cash flow forecast

© Boardworks Ltd 200716 of 22

How does cash flow work?

Ben Matthews is creating a cash flow forecast for his farm business, growing potatoes.

He plants the potatoes in March. The potatoes are harvested in September. Ben then sells them to the wholesaler and receives payment. Between March and September he has to pay for fertilizers, diesel for the farm vehicles, etc.

What cash flow problems might Ben face?

© Boardworks Ltd 200717 of 22

Consequences of negative cash flow

Negative cash flow can lead to serious problems for a business:

A lack of working capital, which could result in the business being unable to pay its bills.

Staff may not be paid on time which can lead to de-motivation and conflict.

Creditors may not be paid on time, which may lead to stricter terms of credit in the future, or even no credit at all. In extreme cases creditors may take a business to court to reclaim what they are owed.

Suppliers can offer discounts for prompt payments and the business may not be able to take advantage of these.

© Boardworks Ltd 200718 of 22

Planning ahead

Ideally, there will always be more money coming into a business than going out. However, income and expenses often occur at different times, particularly for seasonal businesses such as farmers. While some payments can be arranged to suit a business, many outgoings, e.g. salaries and tax, have to be paid on fixed dates.

Cash flow forecasts allow businesses to identify when they are likely to have a negative cash flow. This allows them to take actions to avoid or deal with the situation, e.g. by pre-arranging an overdraft.

What other solutions for managing or avoiding a deficit can you think of?

© Boardworks Ltd 200719 of 22

ICT and cash flow forecasts

© Boardworks Ltd 200720 of 22

True or false?

© Boardworks Ltd 200721 of 22

1. Give two reasons why businesses prepare cash flow forecasts.

2. Give two examples of inflows to a business.

3. Give two examples of outflows from a business.

4. Suggest two methods for avoiding negative cash flow.

5. Explain why spreadsheets are often used to prepare cash flow forecasts.

Question time!

© Boardworks Ltd 200722 of 22

Glossary