© 2015 ihs ihs.com ihs automotive us vehicle market outlook adapting to the next stage april 14,...

TRANSCRIPT

© 2015 IHS

ihs.com

IHS AUTOMOTIVE

US Vehicle Market OutlookAdapting To The Next StageApril 14, 2015

John McBride, Vice President, IHS Automotive, Americas

2

Contents

© 2015 IHS

• Economic Backdrop

• Beneath The Surface: Understanding Distinct Markets

• Makes and Segments

• Conquest Marketing

• Major Trends

Comcast Spotlight | April 2015

© 2015 IHS 3

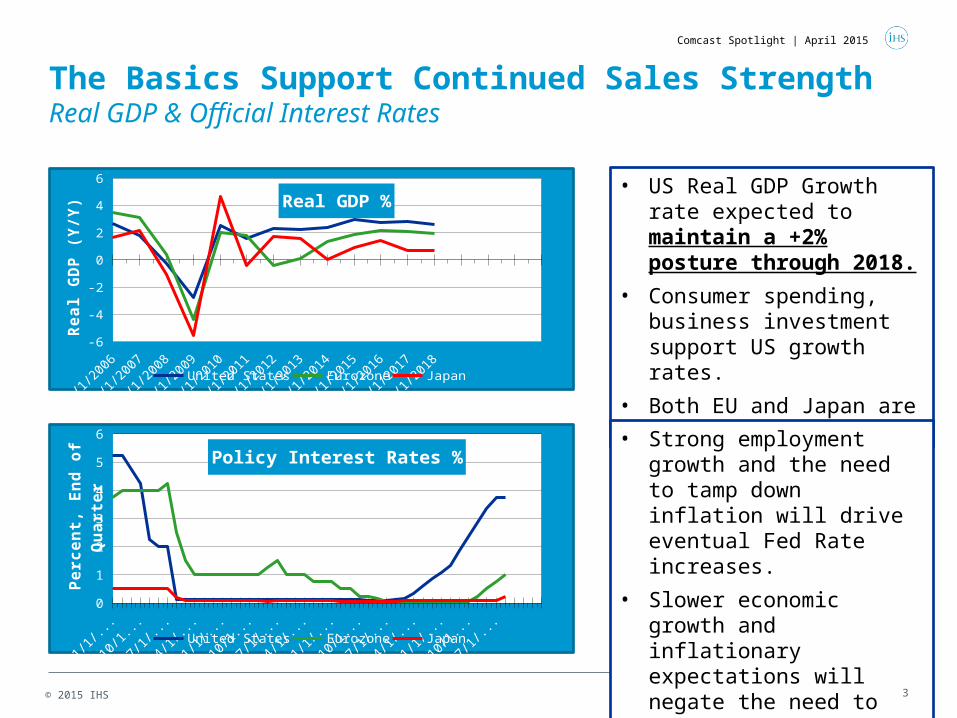

The Basics Support Continued Sales StrengthReal GDP & Official Interest Rates

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018-6

-4

-2

0

2

4

6

Real GDP %

United States Eurozone Japan

Re

al G

DP

(Y

/Y)

• US Real GDP Growth rate expected to maintain a +2% posture through 2018.

• Consumer spending, business investment support US growth rates.

• Both EU and Japan are challenged.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20170

1

2

3

4

5

6

Policy Interest Rates %

United States Eurozone Japan

Pe

rce

nt,

En

d o

f Q

ua

rte

r • Strong employment growth and the need to tamp down inflation will drive eventual Fed Rate increases.

• Slower economic growth and inflationary expectations will negate the need to raise official rates in Japan and EU.

Comcast Spotlight | April 2015

© 2015 IHS 4

Comcast Spotlight | April 2015

2007

2007

2007

2007

2008

2008

2008

2008

2009

2009

2009

2009

2010

2010

2010

2010

2011

2011

2011

2011

2012

2012

2012

2012

2013

2013

2013

2013

2014

2014

2014

2014

2015

2015

2015

2015

2016

2016

2016

2016

2017

2017

2017

2017

0

2

4

6

8

10

12

Unemployment Rate

An

nu

al p

erc

en

t c

ha

ng

e

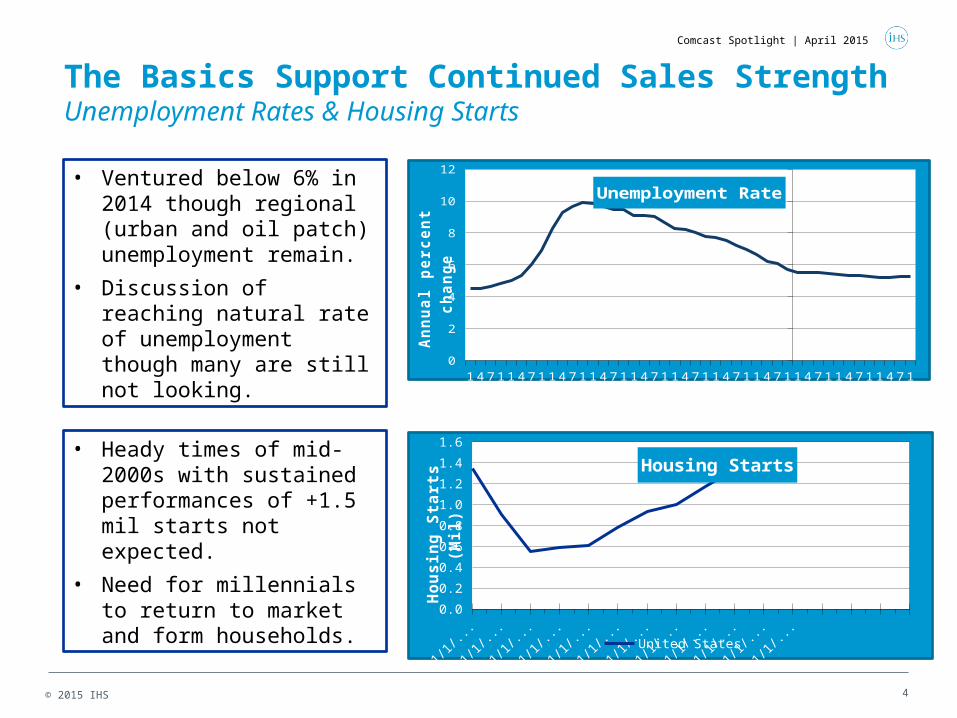

• Ventured below 6% in 2014 though regional (urban and oil patch) unemployment remain.

• Discussion of reaching natural rate of unemployment though many are still not looking.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20170.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Housing Starts

United States

Ho

us

ing

Sta

rts

(M

il)• Heady times of mid-2000s

with sustained performances of +1.5 mil starts not expected.

• Need for millennials to return to market and form households.

The Basics Support Continued Sales StrengthUnemployment Rates & Housing Starts

© 2015 IHS 5

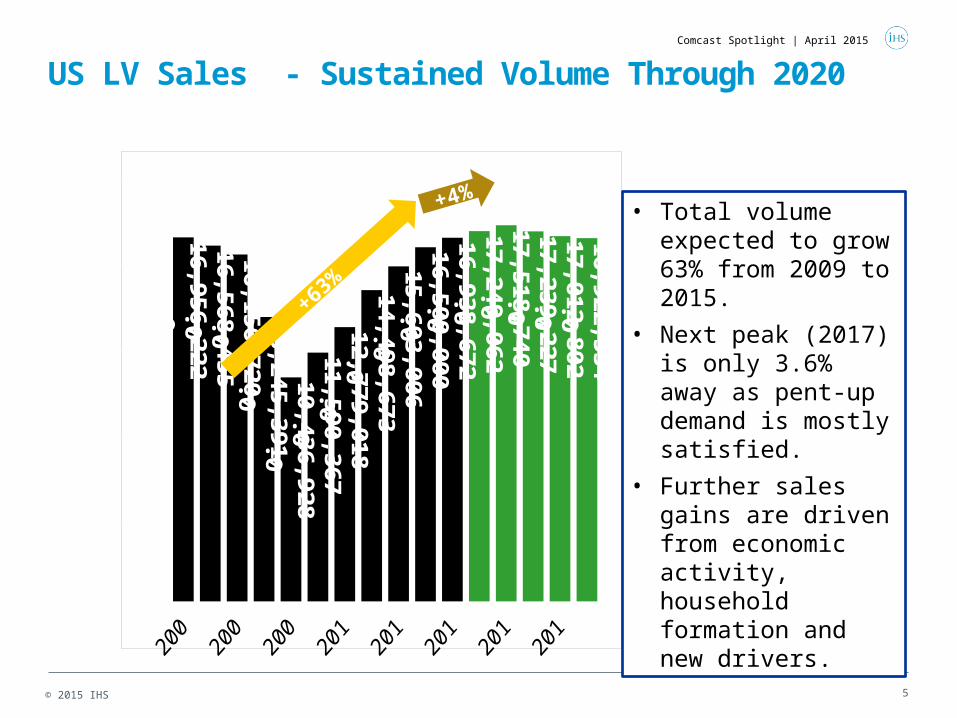

US LV Sales - Sustained Volume Through 2020

0

4,000,000

8,000,000

12,000,000

16,000,000

20,000,000

16,956,222.016,568,455.016,156,720.0

13,245,391.010,436,928.0

11,590,367.012,779,018.0

14,498,673.015,603,006.0

16,500,000.016,938,672.0

17,249,062.017,518,740.017,239,227.017,012,802.016,922,534.0

• Total volume expected to grow 63% from 2009 to 2015.

• Next peak (2017) is only 3.6% away as pent-up demand is mostly satisfied.

• Further sales gains are driven from economic activity, household formation and new drivers.

+4%

+63%

Comcast Spotlight | April 2015

6

Contents

© 2015 IHS

• Economic Backdrop

• Beneath The Surface: Understanding Distinct Markets

• Makes and Segments

• Conquest Marketing

• Major Trends

Comcast Spotlight | April 2015

© 2015 IHS 7

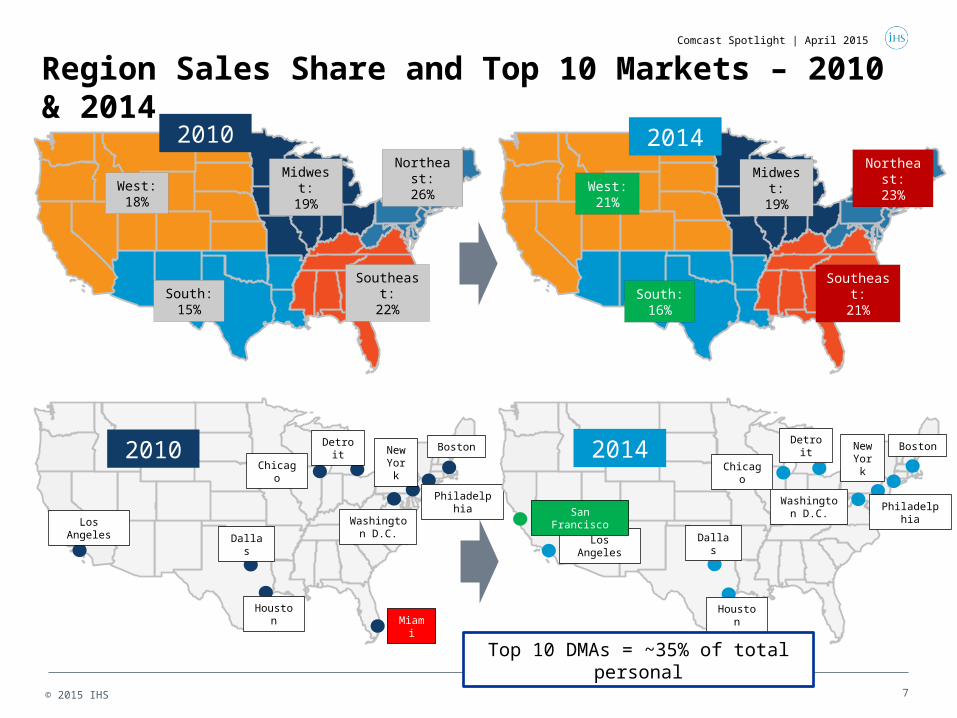

Region Sales Share and Top 10 Markets – 2010 & 2014

2010

Dallas

Houston

Chicago

Detroit

Washington D.C.

Philadelphia

New York

Los Angeles

Miami

Boston 2014

Los Angeles Dallas

Houston

San Francisco

Chicago

Washington D.C. Philadelphia

BostonNew York

Detroit

West:18%

South:15%

Midwest:19%

Southeast:22%

Northeast:26%

2010

West:21%

South:16%

Midwest:19%

Southeast:21%

Northeast:23%

2014

Top 10 DMAs = ~35% of total personal

Comcast Spotlight | April 2015

© 2015 IHS 8

2014

Los Angeles

Dallas

Houston

Chicago

Detroit

Washington D.C.

Philadelphia

BostonNew York

Miami

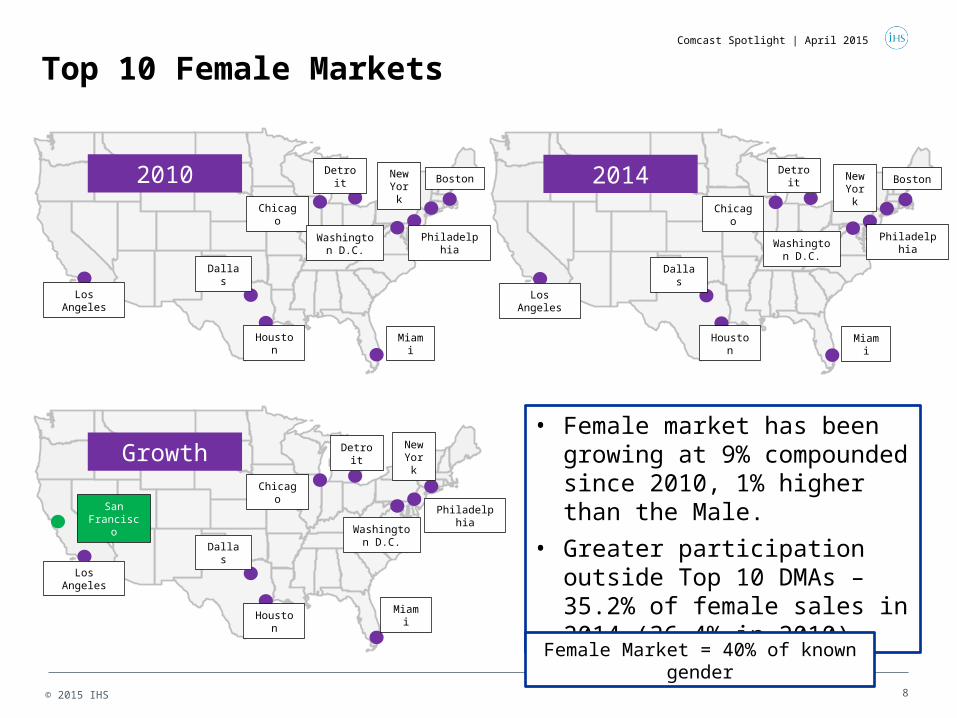

Top 10 Female Markets

2010

Los Angeles

Dallas

Houston

Chicago

Detroit

Washington D.C.

Philadelphia

BostonNew York

Miami

Growth

Los Angeles

Dallas

Houston

Chicago

Detroit

Washington D.C.

Philadelphia

Miami

New York

San Francisco

• Female market has been growing at 9% compounded since 2010, 1% higher than the Male.

• Greater participation outside Top 10 DMAs – 35.2% of female sales in 2014 (36.4% in 2010)

Female Market = 40% of known gender

Comcast Spotlight | April 2015

© 2015 IHS 9

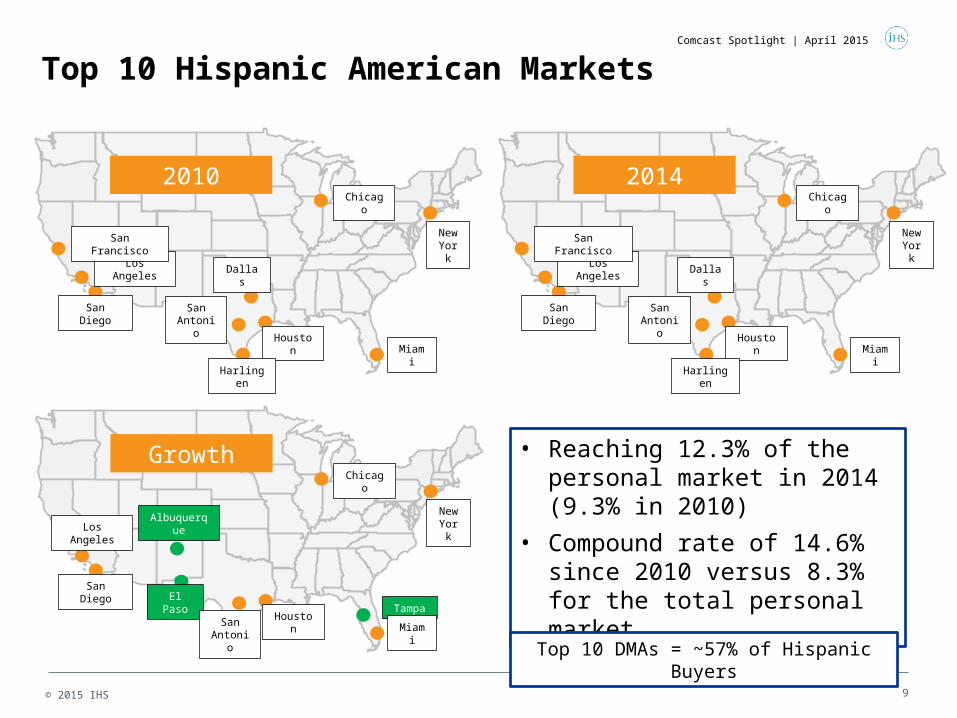

Top 10 Hispanic American Markets

2010

Los AngelesDallas

Houston

Chicago

New York

San Diego

San Francisco

San Antonio

Harlingen

Miami

2014

Los AngelesDallas

Houston

Chicago

New York

San Diego

San Francisco

San Antonio

Harlingen

Miami

Growth

Los Angeles

El Paso

Houston

Chicago

New York

San Diego

Albuquerque

San Antonio

Tampa

Miami

• Reaching 12.3% of the personal market in 2014 (9.3% in 2010)

• Compound rate of 14.6% since 2010 versus 8.3% for the total personal market.

Top 10 DMAs = ~57% of Hispanic Buyers

Comcast Spotlight | April 2015

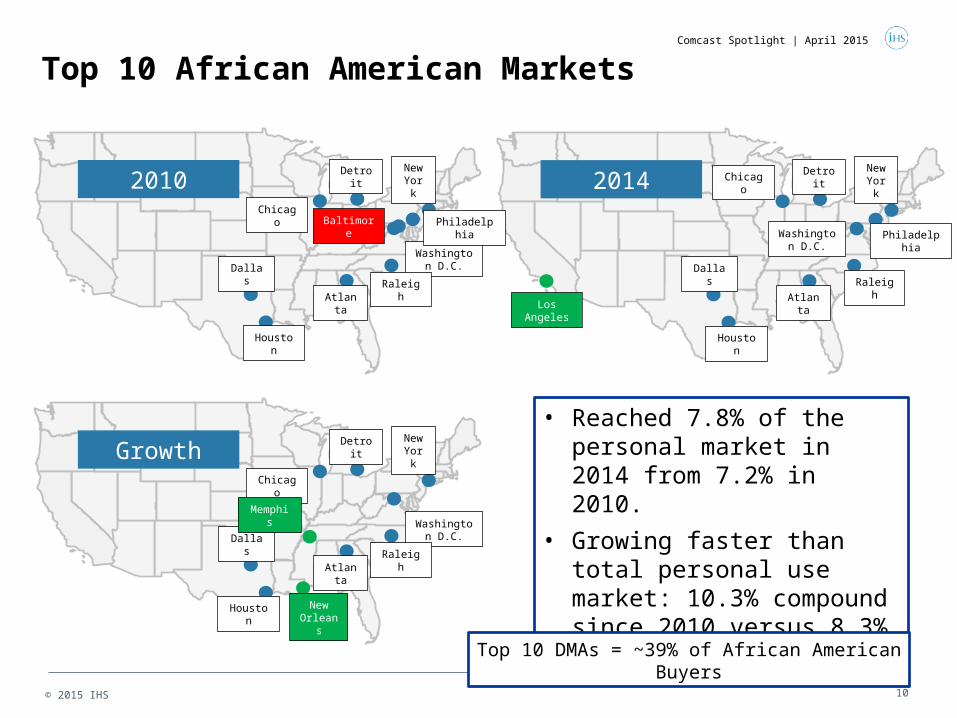

© 2015 IHS 10

2014

Dallas

Houston

Chicago Detroit

Washington D.C. Philadelphia

New York

Los Angeles

Raleigh

Atlanta

Top 10 African American Markets

2010

Dallas

Houston

Chicago

Detroit

Washington D.C.

Philadelphia

New York

Baltimore

RaleighAtlanta

Growth

Dallas

Houston

Chicago

Detroit

Washington D.C.

Memphis

New York

New Orleans

RaleighAtlanta

• Reached 7.8% of the personal market in 2014 from 7.2% in 2010.

• Growing faster than total personal use market: 10.3% compound since 2010 versus 8.3%

Top 10 DMAs = ~39% of African American Buyers

Comcast Spotlight | April 2015

© 2015 IHS 11

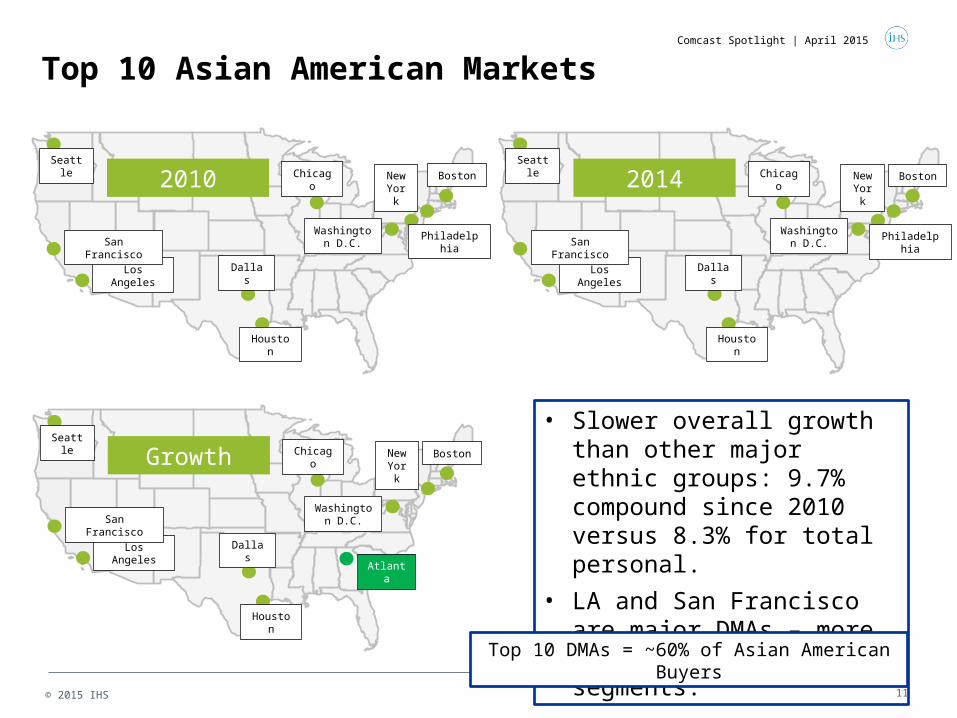

Top 10 Asian American Markets

2010

Los Angeles Dallas

Houston

San Francisco

SeattleChicago

Washington D.C.

New York

2014

Los Angeles Dallas

Houston

San Francisco

SeattleChicago

Washington D.C. Philadelphia

BostonNew York

Philadelphia

Boston

Growth

Los Angeles Dallas

Houston

San Francisco

SeattleChicago

Washington D.C.

Atlanta

BostonNew York

• Slower overall growth than other major ethnic groups: 9.7% compound since 2010 versus 8.3% for total personal.

• LA and San Francisco are major DMAs – more skewed towards luxury segments.

Top 10 DMAs = ~60% of Asian American Buyers

Comcast Spotlight | April 2015

© 2015 IHS 12

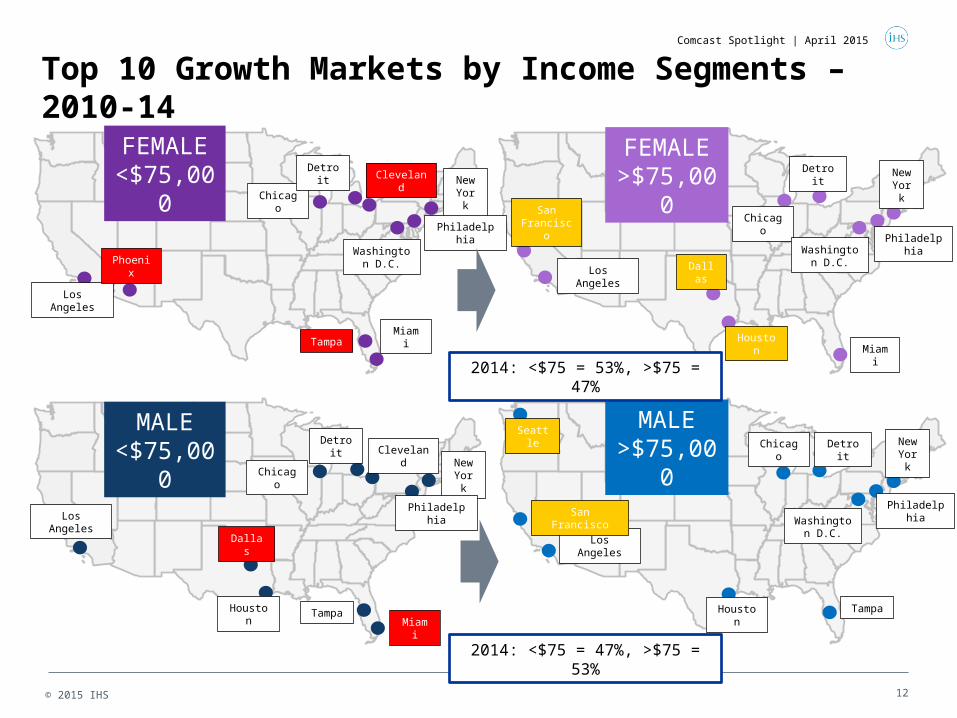

Top 10 Growth Markets by Income Segments – 2010-14

FEMALE<$75,000

FEMALE>$75,000

Los Angeles

Cleveland

Tampa

Chicago

Detroit

Washington D.C.

Philadelphia

Miami

New York

Los Angeles

Detroit

Houston

Chicago

New York

San Francisco

Dallas

Miami

Phoenix

Washington D.C.

Philadelphia

MALE<$75,000

MALE>$75,000

Dallas

Houston

Chicago

Detroit

New York

Los Angeles

Houston

San Francisco

SeattleChicago

Washington D.C.

New York

Los Angeles

Miami

Tampa

Philadelphia

ClevelandDetroit

Tampa

Philadelphia

2014: <$75 = 53%, >$75 = 47%

2014: <$75 = 47%, >$75 = 53%

Comcast Spotlight | April 2015

© 2015 IHS 13

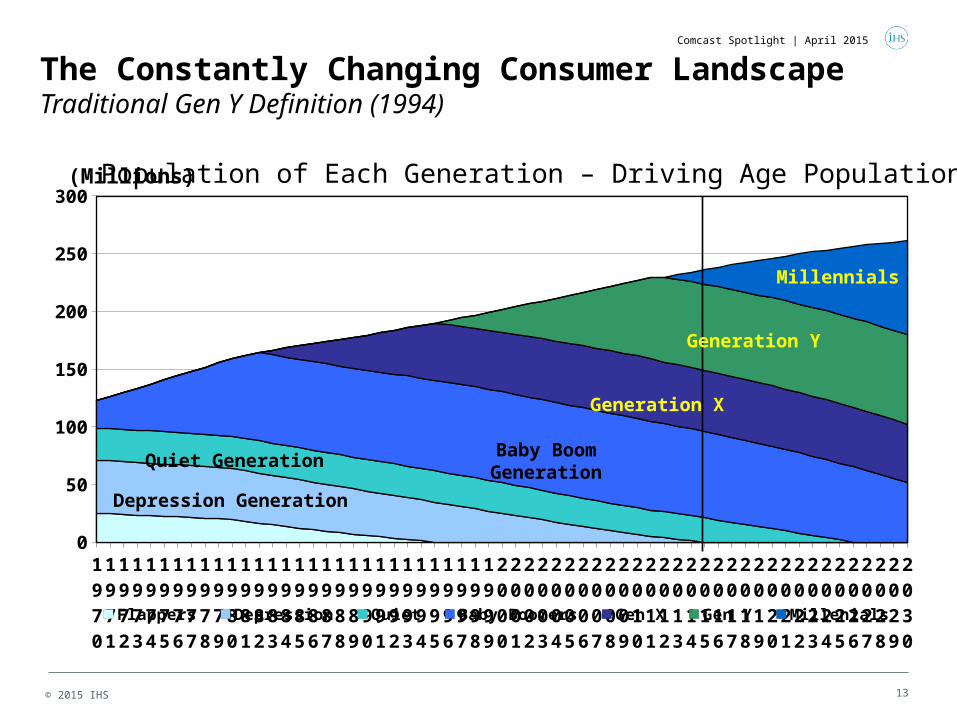

The Constantly Changing Consumer LandscapeTraditional Gen Y Definition (1994)

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

0

50

100

150

200

250

300

Flappers Depression Quiet Baby Boomers Gen X Gen Y Millenials

(Millions)

Generation Y

Generation X

Baby Boom GenerationQuiet Generation

Depression Generation

Population of Each Generation – Driving Age Population

Millennials

Comcast Spotlight | April 2015

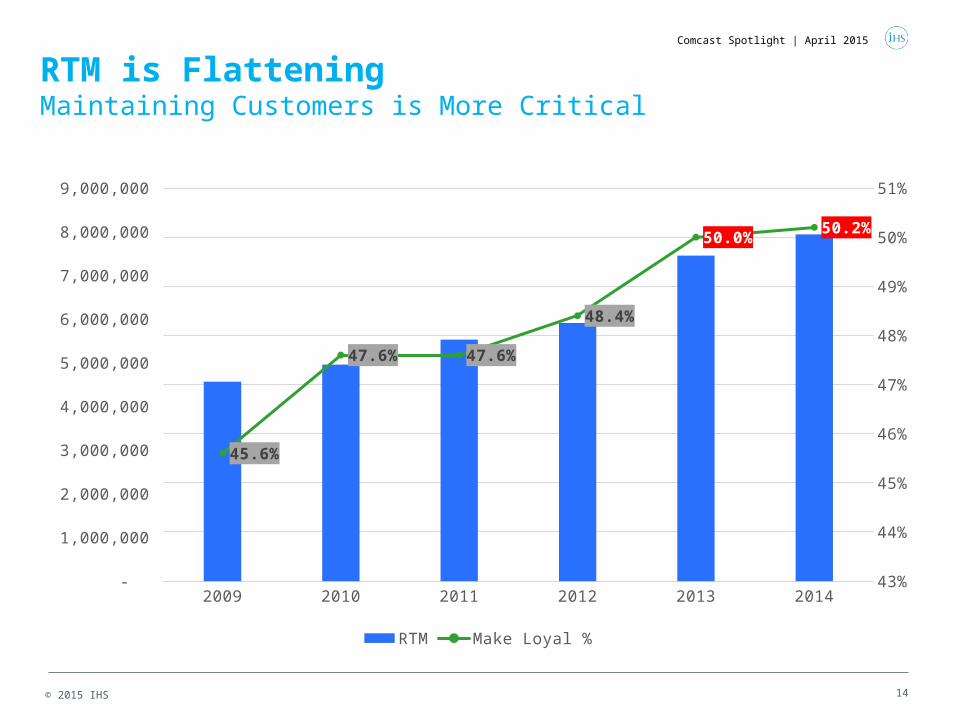

© 2015 IHS 14

2009 2010 2011 2012 2013 201443%

44%

45%

46%

47%

48%

49%

50%

51%

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

45.6%

47.6% 47.6%

48.4%

50.0%50.2%

RTM Make Loyal %

RTM is FlatteningMaintaining Customers is More Critical

Comcast Spotlight | April 2015

15

Contents

© 2015 IHS

• Economic Backdrop

• Beneath The Surface: Understanding Distinct Markets

• Makes and Segments

• Conquest Marketing

• Major Trends

Comcast Spotlight | April 2015

© 2015 IHS 16

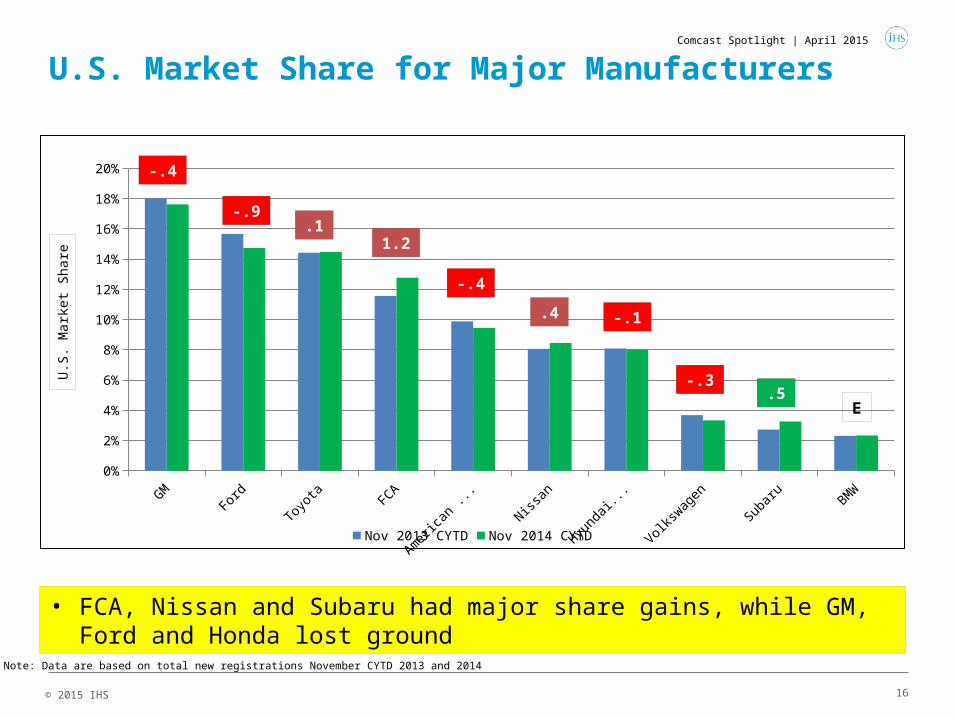

U.S. Market Share for Major Manufacturers

GM Ford Toyota FCA American Honda

Nissan Hyundai/Kia Volkswagen Subaru BMW0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Nov 2013 CYTD Nov 2014 CYTD

-.4

1.2

-.4

.4 -.1

-.3.5

E

.1-.9

• FCA, Nissan and Subaru had major share gains, while GM, Ford and Honda lost ground

U.S

. Mar

ket S

hare

Note: Data are based on total new registrations November CYTD 2013 and 2014

Comcast Spotlight | April 2015

© 2015 IHS 17

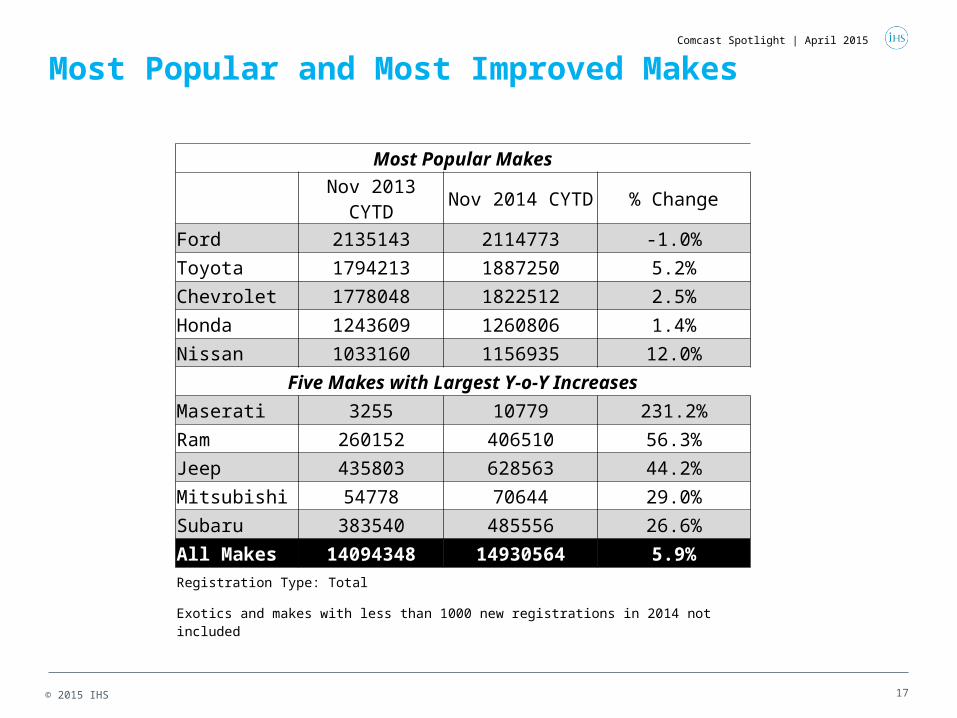

Most Popular and Most Improved Makes

Most Popular Makes

Nov 2013 CYTD Nov 2014 CYTD % Change

Ford 2135143 2114773 -1.0%

Toyota 1794213 1887250 5.2%

Chevrolet 1778048 1822512 2.5%

Honda 1243609 1260806 1.4%

Nissan 1033160 1156935 12.0%

Five Makes with Largest Y-o-Y Increases

Maserati 3255 10779 231.2%

Ram 260152 406510 56.3%

Jeep 435803 628563 44.2%

Mitsubishi 54778 70644 29.0%

Subaru 383540 485556 26.6%

All Makes 14094348 14930564 5.9%

Registration Type: Total

Exotics and makes with less than 1000 new registrations in 2014 not included

Comcast Spotlight | April 2015

© 2015 IHS 18

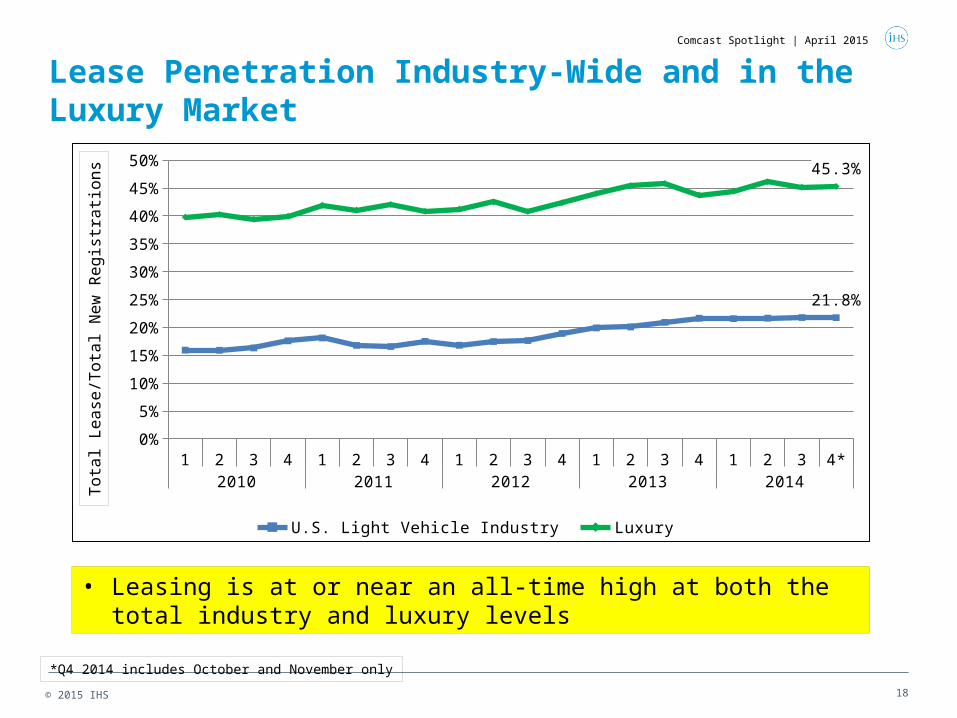

Lease Penetration Industry-Wide and in the Luxury Market

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4*2010 2011 2012 2013 2014

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

21.8%

45.3%

U.S. Light Vehicle Industry Luxury

Tota

l Le

ase

/To

tal N

ew

Re

gis

tra

tion

s

*Q4 2014 includes October and November only

• Leasing is at or near an all-time high at both the total industry and luxury levels

Comcast Spotlight | April 2015

© 2015 IHS 19

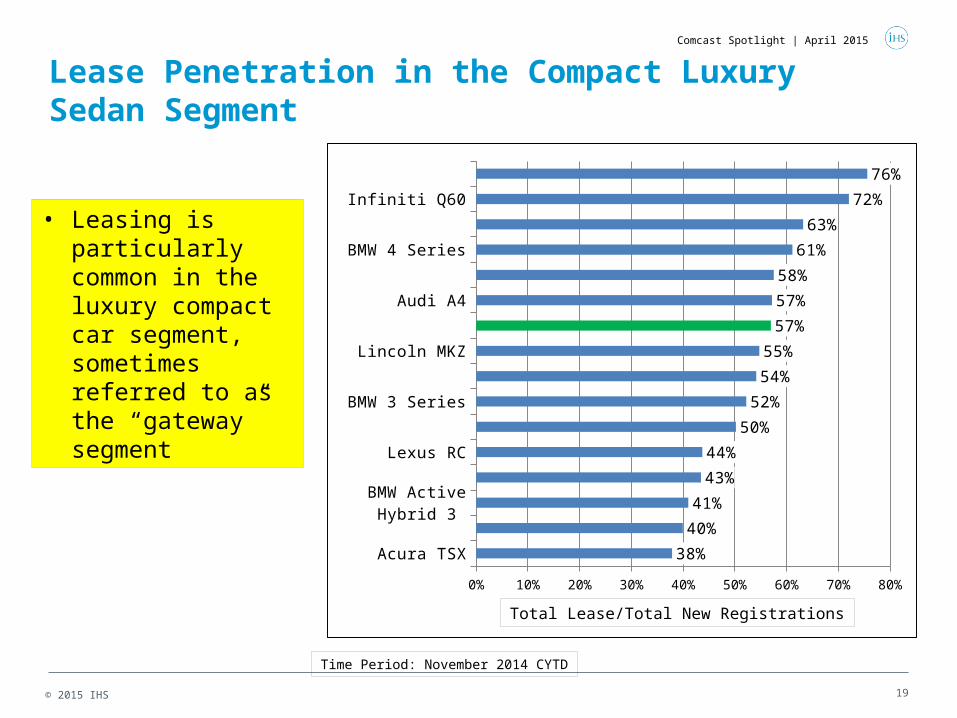

Lease Penetration in the Compact Luxury Sedan Segment

Acura TSX

Volvo S60

BMW Active Hybrid 3

Acura TL/TLX

Lexus RC

Cadillac ATS

BMW 3 Series

Cadillac ELR

Lincoln MKZ

Segment

Audi A4

Mercedes-Benz C Class

BMW 4 Series

Lexus IS

Infiniti Q60

Infiniti G/Q40/Q50

0% 10% 20% 30% 40% 50% 60% 70% 80%

38%

40%

41%

43%

44%

50%

52%

54%

55%

57%

57%

58%

61%

63%

72%

76%

• Leasing is particularly common in the luxury compact car segment, sometimes referred to as the “gateway” segment

Time Period: November 2014 CYTD

Total Lease/Total New Registrations

Comcast Spotlight | April 2015

© 2015 IHS 20

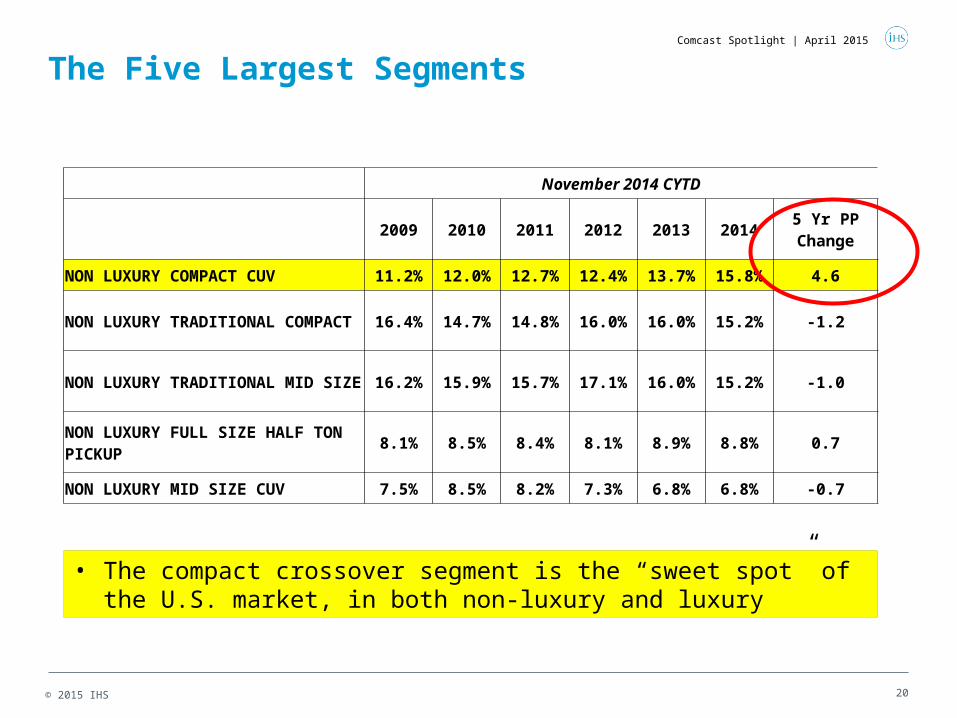

The Five Largest Segments

November 2014 CYTD

2009 2010 2011 2012 2013 20145 Yr PP Change

NON LUXURY COMPACT CUV 11.2% 12.0% 12.7% 12.4% 13.7% 15.8% 4.6

NON LUXURY TRADITIONAL COMPACT

16.4% 14.7% 14.8% 16.0% 16.0% 15.2% -1.2

NON LUXURY TRADITIONAL MID SIZE 16.2% 15.9% 15.7% 17.1% 16.0% 15.2% -1.0

NON LUXURY FULL SIZE HALF TON PICKUP

8.1% 8.5% 8.4% 8.1% 8.9% 8.8% 0.7

NON LUXURY MID SIZE CUV 7.5% 8.5% 8.2% 7.3% 6.8% 6.8% -0.7

• The compact crossover segment is the “sweet spot” of the U.S. market, in both non-luxury and luxury

Comcast Spotlight | April 2015

© 2015 IHS 21

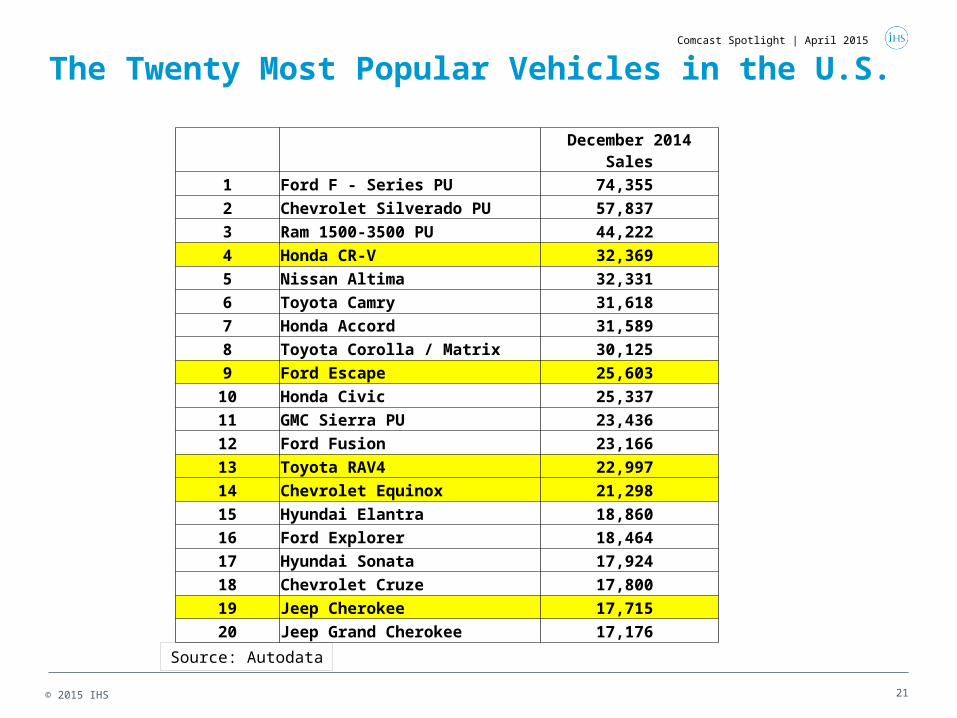

The Twenty Most Popular Vehicles in the U.S.

December 2014 Sales

1 Ford F - Series PU 74,355

2 Chevrolet Silverado PU 57,837

3 Ram 1500-3500 PU 44,222

4 Honda CR-V 32,369

5 Nissan Altima 32,331

6 Toyota Camry 31,618

7 Honda Accord 31,589

8 Toyota Corolla / Matrix 30,125

9 Ford Escape 25,603

10 Honda Civic 25,337

11 GMC Sierra PU 23,436

12 Ford Fusion 23,166

13 Toyota RAV4 22,997

14 Chevrolet Equinox 21,298

15 Hyundai Elantra 18,860

16 Ford Explorer 18,464

17 Hyundai Sonata 17,924

18 Chevrolet Cruze 17,800

19 Jeep Cherokee 17,715

20 Jeep Grand Cherokee 17,176

Source: Autodata

Comcast Spotlight | April 2015

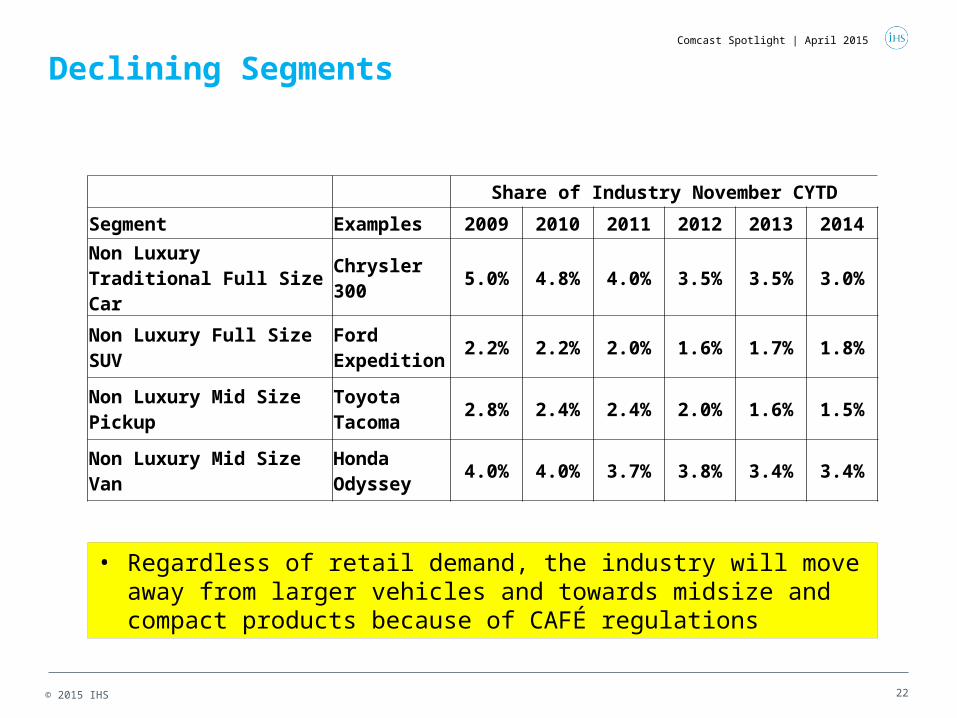

© 2015 IHS 22

Declining Segments

Share of Industry November CYTD

Segment Examples 2009 2010 2011 2012 2013 2014

Non Luxury Traditional Full Size Car

Chrysler 300 5.0% 4.8% 4.0% 3.5% 3.5% 3.0%

Non Luxury Full Size SUVFord Expedition

2.2% 2.2% 2.0% 1.6% 1.7% 1.8%

Non Luxury Mid Size Pickup

Toyota Tacoma

2.8% 2.4% 2.4% 2.0% 1.6% 1.5%

Non Luxury Mid Size Van Honda Odyssey

4.0% 4.0% 3.7% 3.8% 3.4% 3.4%

• Regardless of retail demand, the industry will move away from larger vehicles and towards midsize and compact products because of CAFÉ regulations

Comcast Spotlight | April 2015

© 2015 IHS 23

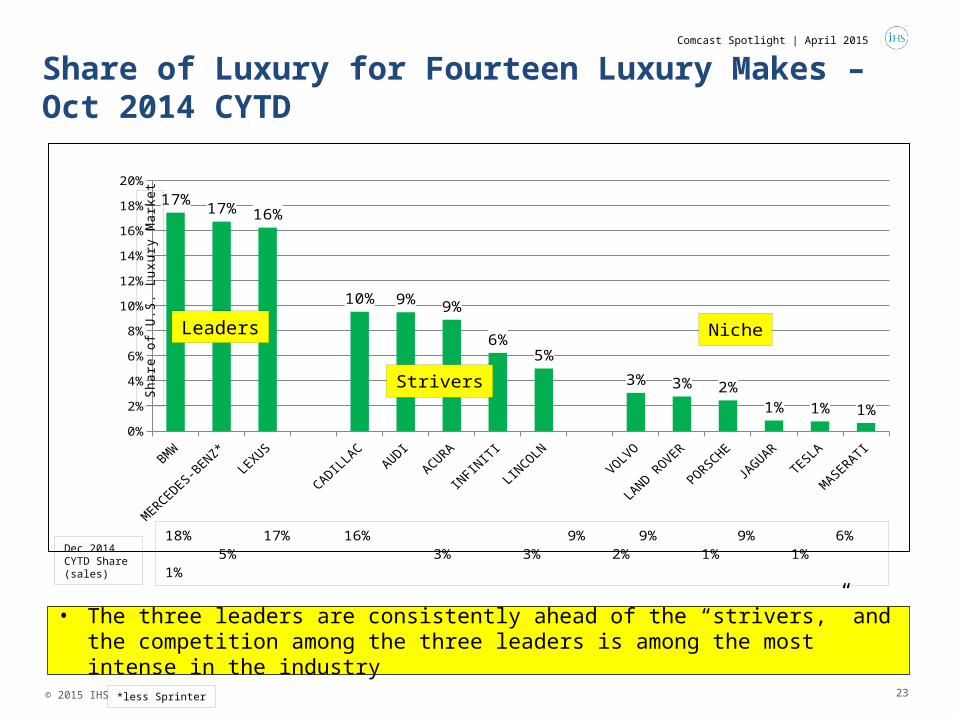

Share of Luxury for Fourteen Luxury Makes – Oct 2014 CYTD

• The three leaders are consistently ahead of the “strivers,” and the competition among the three leaders is among the most intense in the industry

BMW

MERCED

ES-BEN

Z*LEX

US

CADILLAC

AUDI

ACURA

INFINITI

LINCOLN

VOLVO

LAND ROVER

PORSCHE

JAGUAR

TESLA

MASERATI

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

17% 17% 16%

10% 9% 9%

6%5%

3% 3% 2%1% 1% 1%

Sha

re o

f U

.S.

Luxu

ry M

arke

t

18% 17% 16% 9% 9% 9% 6% 5% 3% 3% 2% 1% 1% 1%

Strivers

Niche

Dec 2014 CYTD Share (sales)

*less Sprinter

Leaders

Comcast Spotlight | April 2015

© 2015 IHS 24

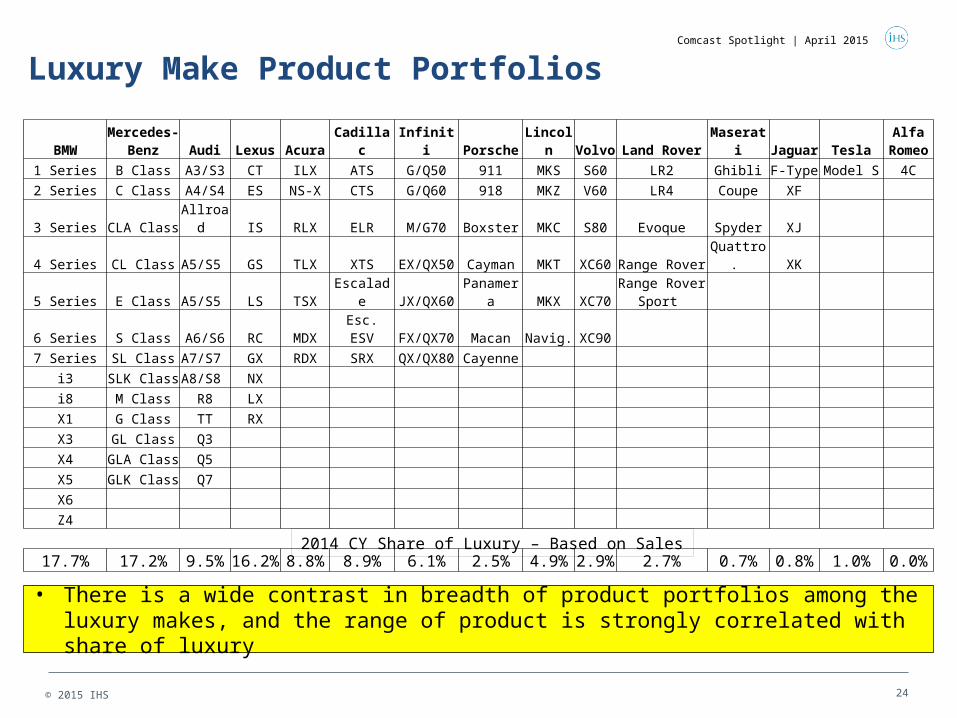

Luxury Make Product Portfolios

• There is a wide contrast in breadth of product portfolios among the luxury makes, and the range of product is strongly correlated with share of luxury

BMWMercedes-

Benz Audi Lexus Acura Cadillac Infiniti Porsche Lincoln Volvo Land Rover Maserati Jaguar TeslaAlfa

Romeo

1 Series B Class A3/S3 CT ILX ATS G/Q50 911 MKS S60 LR2 Ghibli F-Type Model S 4C

2 Series C Class A4/S4 ES NS-X CTS G/Q60 918 MKZ V60 LR4 Coupe XF

3 Series CLA Class Allroad IS RLX ELR M/G70 Boxster MKC S80 Evoque Spyder XJ

4 Series CL Class A5/S5 GS TLX XTS EX/QX50 Cayman MKT XC60 Range Rover Quattro. XK

5 Series E Class A5/S5 LS TSX Escalade JX/QX60 Panamera MKX XC70Range Rover

Sport

6 Series S Class A6/S6 RC MDX Esc. ESV FX/QX70 Macan Navig. XC90

7 Series SL Class A7/S7 GX RDX SRX QX/QX80 Cayenne

i3 SLK Class A8/S8 NX

i8 M Class R8 LX

X1 G Class TT RX

X3 GL Class Q3

X4 GLA Class Q5

X5 GLK Class Q7

X6

Z4

17.7% 17.2% 9.5% 16.2% 8.8% 8.9% 6.1% 2.5% 4.9% 2.9% 2.7% 0.7% 0.8% 1.0% 0.0%

2014 CY Share of Luxury – Based on Sales

Comcast Spotlight | April 2015

25

Contents

© 2015 IHS

• Economic Backdrop

• Beneath The Surface: Understanding Distinct Markets

• Makes and Segments

• Conquest Marketing

• Major Trends

Comcast Spotlight | April 2015

© 2015 IHS 26

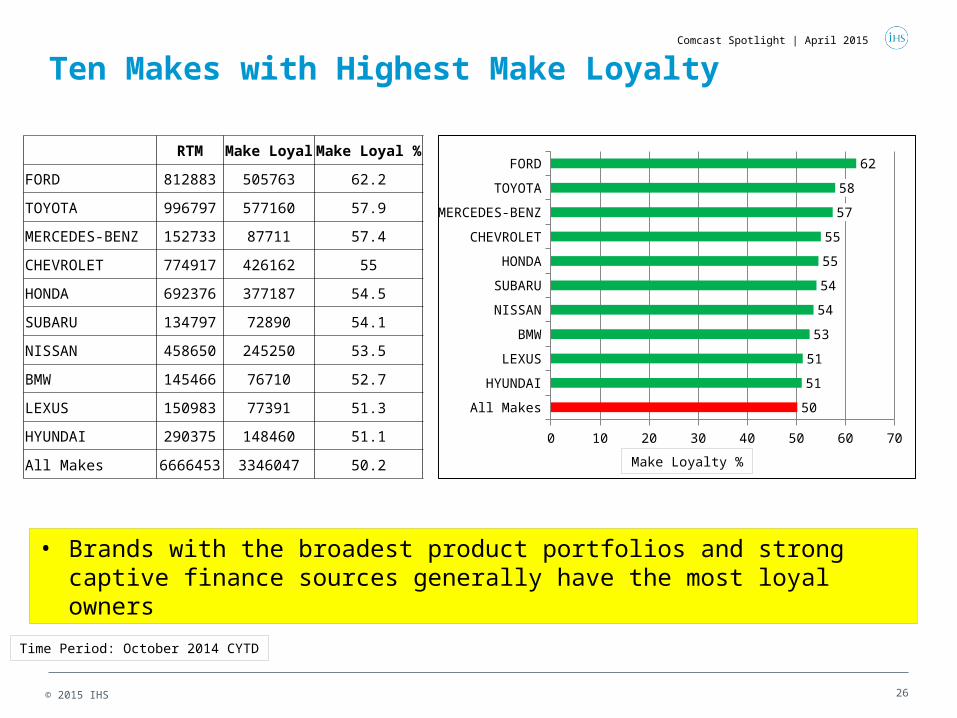

Ten Makes with Highest Make Loyalty

All Makes

HYUNDAI

LEXUS

BMW

NISSAN

SUBARU

HONDA

CHEVROLET

MERCEDES-BENZ

TOYOTA

FORD

0 10 20 30 40 50 60 70

50

51

51

53

54

54

55

55

57

58

62 RTM Make Loyal Make Loyal %

FORD 812883 505763 62.2

TOYOTA 996797 577160 57.9

MERCEDES-BENZ 152733 87711 57.4

CHEVROLET 774917 426162 55

HONDA 692376 377187 54.5

SUBARU 134797 72890 54.1

NISSAN 458650 245250 53.5

BMW 145466 76710 52.7

LEXUS 150983 77391 51.3

HYUNDAI 290375 148460 51.1

All Makes 6666453 3346047 50.2

• Brands with the broadest product portfolios and strong captive finance sources generally have the most loyal owners

Time Period: October 2014 CYTD

Make Loyalty %

Comcast Spotlight | April 2015

© 2015 IHS 27

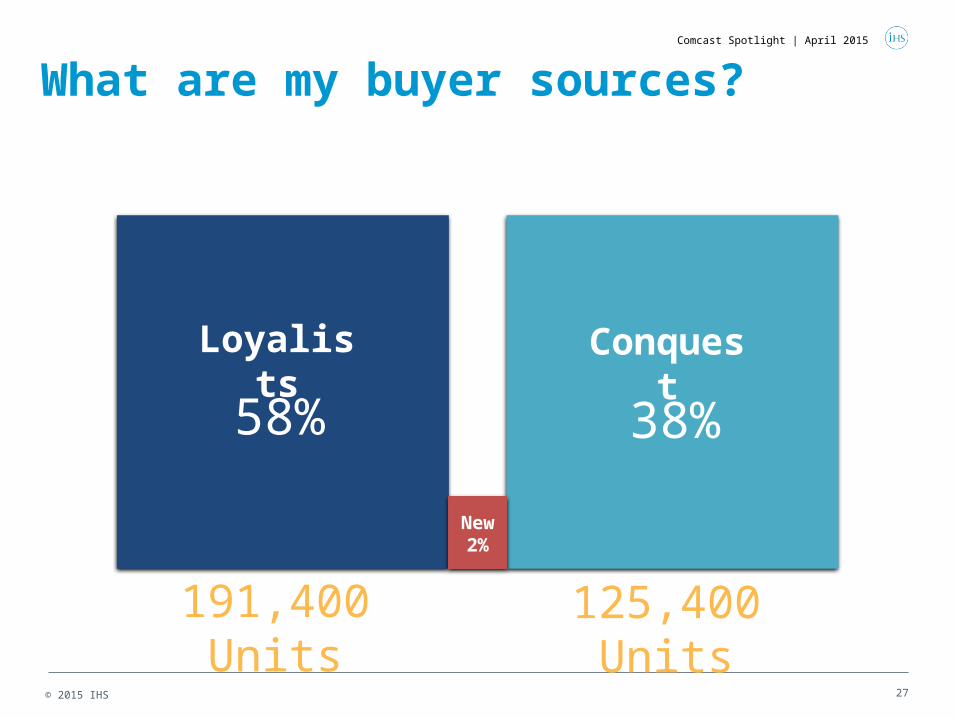

What are my buyer sources?

Loyalists Conquest

58% 38%

191,400 Units 125,400 Units

New2%

Comcast Spotlight | April 2015

© 2015 IHS 28

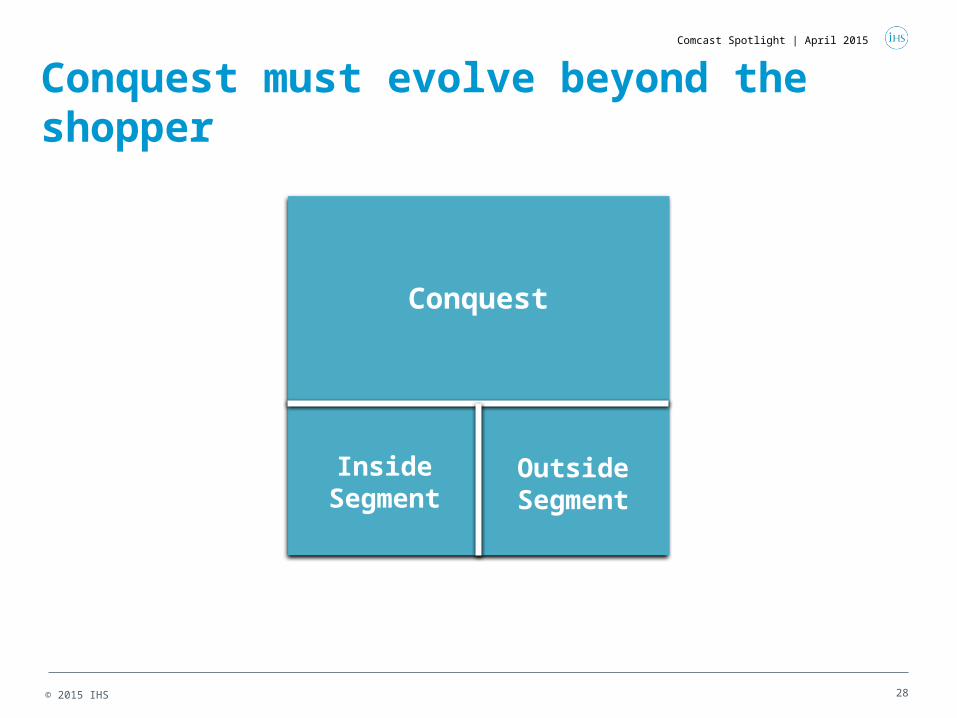

Conquest

Inside Segment

Outside Segment

Conquest must evolve beyond the shopper

Comcast Spotlight | April 2015

© 2015 IHS 29

Inside SegmentLuxury (New-to-New)

Conquest: 7,943Conquest Rate: 5.0%

Conquest: 474Conquest Rate: 2.9%

Comcast Spotlight | April 2015

© 2015 IHS 30

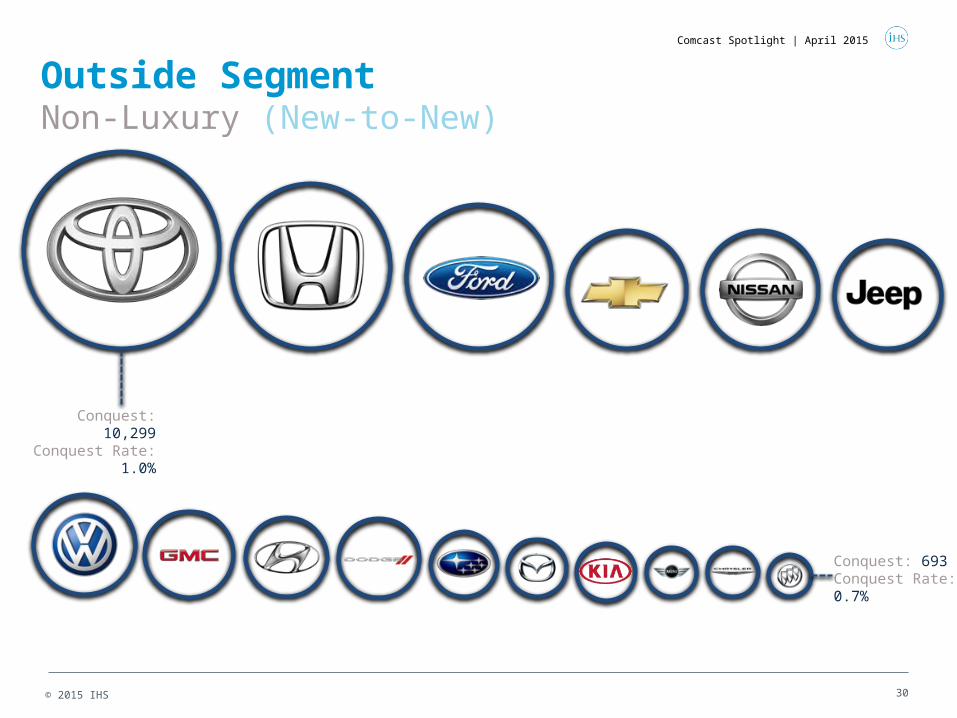

Outside SegmentNon-Luxury (New-to-New)

Conquest: 10,299Conquest Rate:

1.0%

Conquest: 693Conquest Rate: 0.7%

Comcast Spotlight | April 2015

© 2015 IHS 31

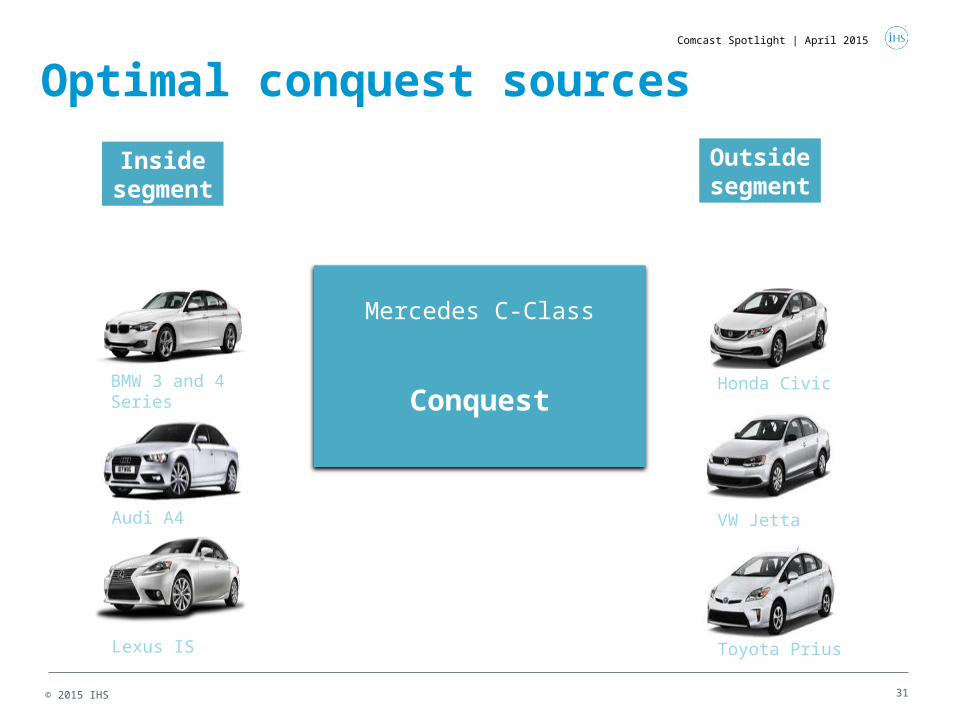

Optimal conquest sources

Conquest

Outside segment

Mercedes C-Class

VW Jetta

Toyota Prius

BMW 3 and 4 Series

Audi A4

Lexus IS

Honda Civic

Inside segment

Comcast Spotlight | April 2015

32

Contents

© 2015 IHS

• Economic Backdrop

• Beneath The Surface: Understanding Distinct Markets

• Makes and Segments

• Conquest Marketing

• Major Trends

Comcast Spotlight | April 2015

© 2015 IHS 33

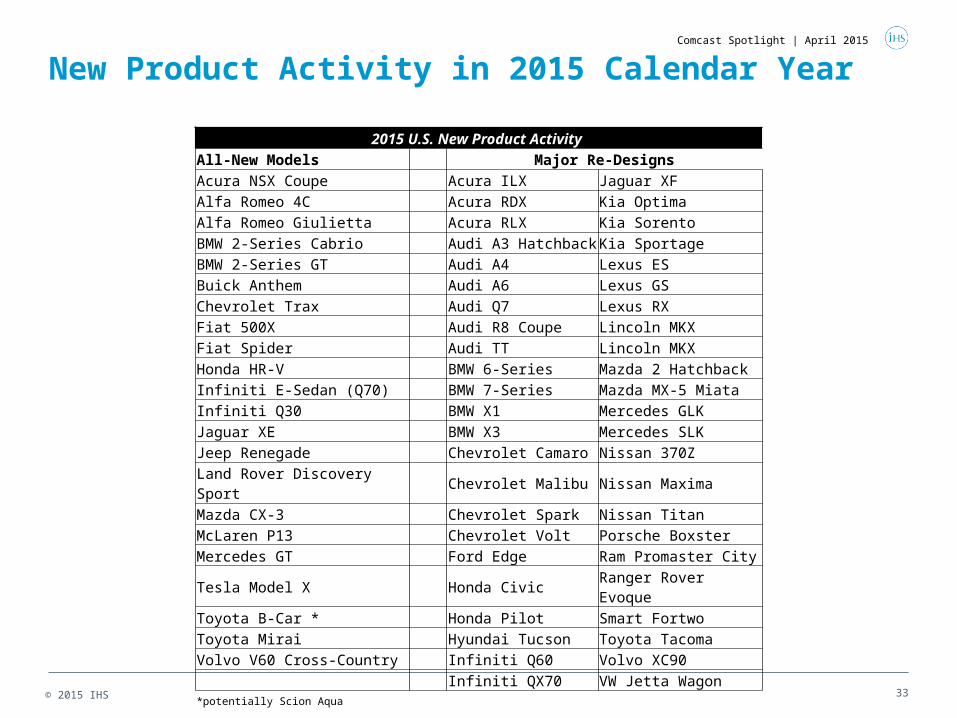

New Product Activity in 2015 Calendar Year

2015 U.S. New Product Activity All-New Models Major Re-DesignsAcura NSX Coupe Acura ILX Jaguar XFAlfa Romeo 4C Acura RDX Kia OptimaAlfa Romeo Giulietta Acura RLX Kia SorentoBMW 2-Series Cabrio Audi A3 Hatchback Kia SportageBMW 2-Series GT Audi A4 Lexus ESBuick Anthem Audi A6 Lexus GSChevrolet Trax Audi Q7 Lexus RXFiat 500X Audi R8 Coupe Lincoln MKXFiat Spider Audi TT Lincoln MKXHonda HR-V BMW 6-Series Mazda 2 HatchbackInfiniti E-Sedan (Q70) BMW 7-Series Mazda MX-5 MiataInfiniti Q30 BMW X1 Mercedes GLKJaguar XE BMW X3 Mercedes SLKJeep Renegade Chevrolet Camaro Nissan 370ZLand Rover Discovery Sport Chevrolet Malibu Nissan MaximaMazda CX-3 Chevrolet Spark Nissan TitanMcLaren P13 Chevrolet Volt Porsche BoxsterMercedes GT Ford Edge Ram Promaster CityTesla Model X Honda Civic Ranger Rover EvoqueToyota B-Car * Honda Pilot Smart FortwoToyota Mirai Hyundai Tucson Toyota TacomaVolvo V60 Cross-Country Infiniti Q60 Volvo XC90 Infiniti QX70 VW Jetta Wagon*potentially Scion Aqua

Comcast Spotlight | April 2015

© 2015 IHS 34

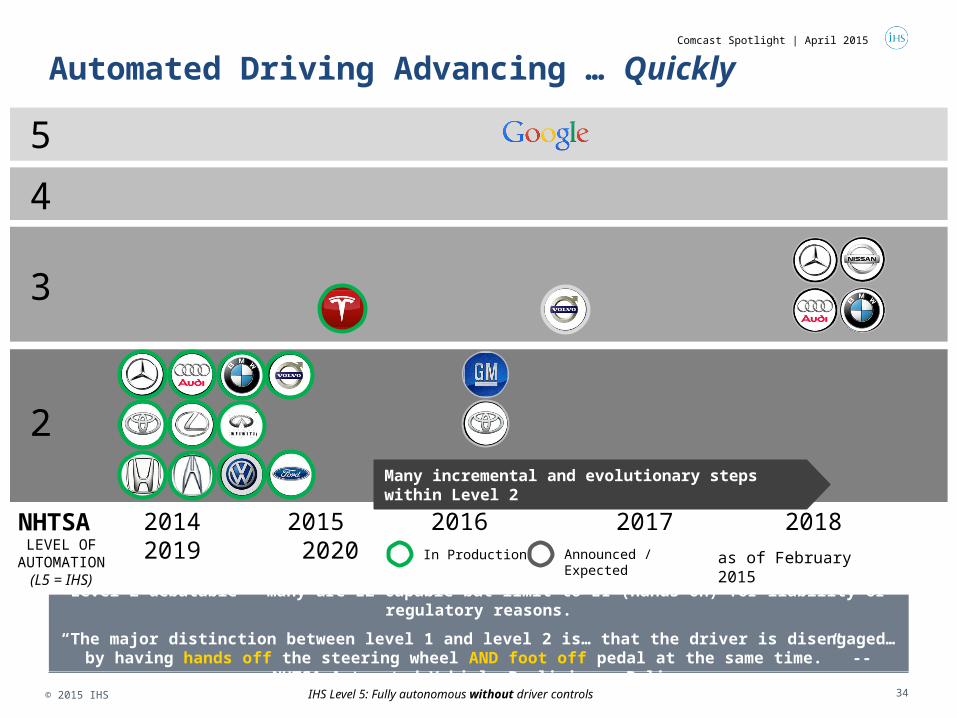

Automated Driving Advancing … Quickly

2

3

4

In Production Announced / Expected

Many incremental and evolutionary steps within Level 2

Level 2 debatable – many are L2-capable but limit to L1 (hands on) for liability or regulatory reasons.

“The major distinction between level 1 and level 2 is… that the driver is disengaged… by having hands off the steering wheel AND foot off pedal at the same time.” -- NHTSA Automated Vehicle Preliminary Policy

5

IHS Level 5: Fully autonomous without driver controls

NHTSA LEVEL OF

AUTOMATION(L5 = IHS)

2014 2015 2016 2017 2018 2019 2020 as of February 2015

Comcast Spotlight | April 2015

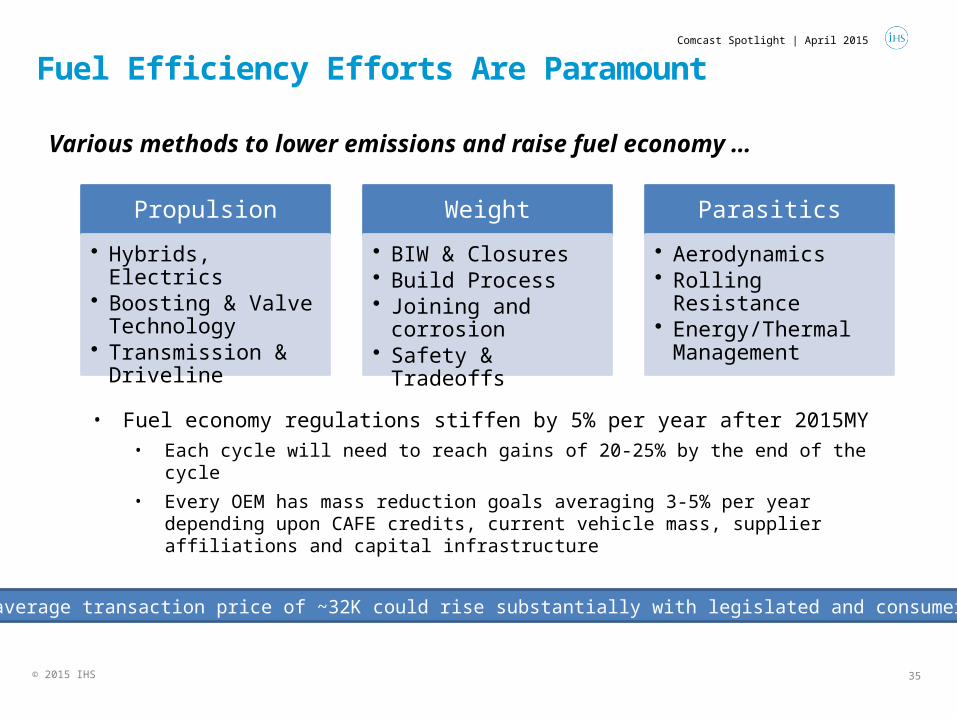

Fuel Efficiency Efforts Are Paramount

• Fuel economy regulations stiffen by 5% per year after 2015MY• Each cycle will need to reach gains of 20-25% by the end of the cycle

• Every OEM has mass reduction goals averaging 3-5% per year depending upon CAFE credits, current vehicle mass, supplier affiliations and capital infrastructure

Propulsion

• Hybrids, Electrics• Boosting & Valve

Technology• Transmission &

Driveline

Weight

• BIW & Closures• Build Process• Joining and corrosion• Safety & Tradeoffs

Parasitics

• Aerodynamics• Rolling Resistance• Energy/Thermal

Management

© 2015 IHS

Various methods to lower emissions and raise fuel economy …

Today’s average transaction price of ~32K could rise substantially with legislated and consumer content

Comcast Spotlight | April 2015

35

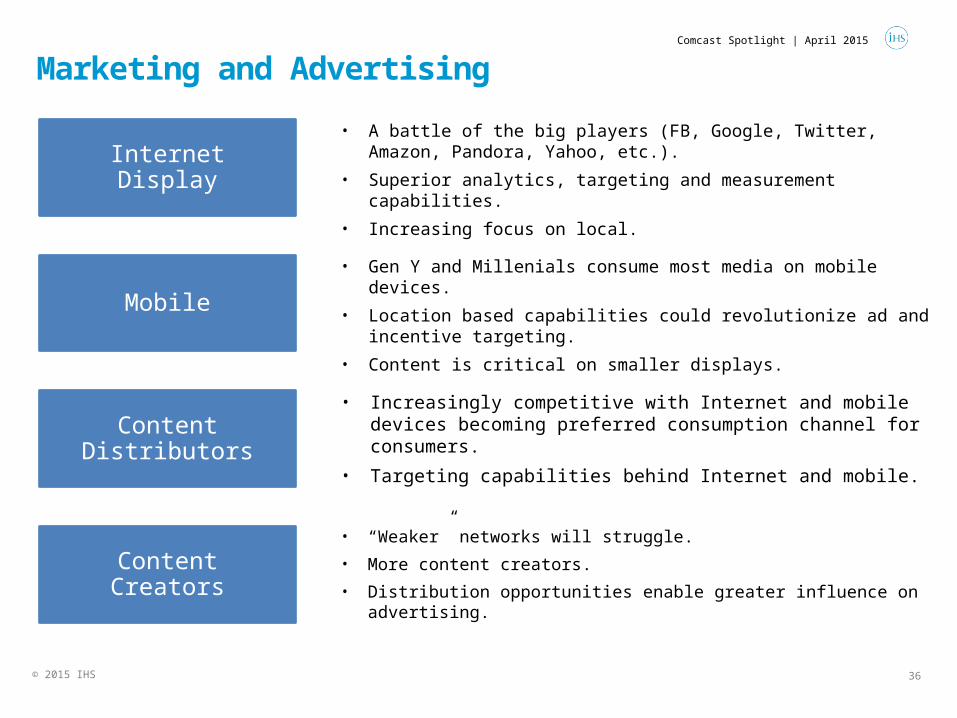

Marketing and Advertising

© 2015 IHS

Comcast Spotlight | April 2015

Internet Display

Mobile

Content Distributors

Content Creators

• A battle of the big players (FB, Google, Twitter, Amazon, Pandora, Yahoo, etc.).

• Superior analytics, targeting and measurement capabilities.

• Increasing focus on local.

• Gen Y and Millenials consume most media on mobile devices.

• Location based capabilities could revolutionize ad and incentive targeting.

• Content is critical on smaller displays.

• Increasingly competitive with Internet and mobile devices becoming preferred consumption channel for consumers.

• Targeting capabilities behind Internet and mobile.

• “Weaker” networks will struggle.

• More content creators.

• Distribution opportunities enable greater influence on advertising.

36

IHS Customer Care:• Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected] • Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected] • Asia and the Pacific Rim: +604 291 3600; [email protected]

© 2015 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, please contact IHS at Customer Care (see phone numbers and email addresses above). All products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.

Thank You

John McBrideVice President, IHS Automotive, Americas [email protected]