yue yuen industrial 2019 annual resultsinvestor.yueyuen.com/202003301832151728532209_en.pdf ·...

TRANSCRIPT

30 March 2020

Yue Yuen Industrial 2019 Annual Results

Disclaimer

Yue Yuen and Pou Sheng have taken every reasonable care in preparing this presentation. However, please be reminded that the

information, materials, opinions and statements contained or referred to in this presentation are all provided on an "as is" basis.

None of the aforesaid information, materials, opinions and statements constitutes or will be viewed as investment advice or an

offer, or a solicitation, recommendation or suggestion by Yue Yuen or Pou Sheng to deal in any investment products including

securities, or other financial products and instruments.

If there is any forward-looking statements contained or referred to in this presentation, these forward-looking statements are

based on current expectations and assumptions, of which many are beyond our control. In addition, these statements are subject

to a number of risks, uncertainties and factors and if any of these risks or uncertainties materialize, or if underlying expectations

not occur or assumptions prove incorrect, actual results, performance or achievements of Yue Yuen and/or Pou Sheng may vary

materially from those described explicitly or implicitly in the relevant forward-looking statement. Neither Yue Yuen nor Pou Sheng

intends or assumes any obligation, to update or revise these forward-looking statements in light of any difference from those

anticipated.

Yue Yuen and Pou Sheng including their respective subsidiaries, associated or affiliated companies, or any of their respective

directors, employees, agents, representatives or associates accepts no liability for and shall not be responsible or liable for any

loss or damage of whatever kind or nature, directly or indirectly, arising from action taken, or not taken, in reliance on, or

resulting from access to or use of the aforesaid information, materials, opinions and statements (including forward-looking

statements, if any) contained or referred to in the presentation.

2

Retail Sales – Shoes, Apparel & Leasing

38.9% (FY18: 35.3%)

Company Profile

Founded in 1988, and listed on the HKEX in 1992 (551.HK)

Core Businesses:

Footwear manufacturing – Predominately athletic and casual / outdoor shoes

Pou Sheng (3813.HK) – Sportswear retail & sports services in the Greater China Region

A yield play with solid performance – committed to driving return and value for shareholders

FY19 Revenue by Business Segments

FY19 Total Revenue reached US$ 10,105.4 million

*Revenue from Texas Clothing Holding Corp. (“TCHC”) Group, which became subsidiary of the Group on April 7, 2017 and was then disposed on May 31, 2019 3

Soles, Components & Others

4.4% (FY18: 5.1%)

Athletic Shoes

44.9% (FY18: 44.0%)

Casual / Outdoor Shoes

9.0% (FY18: 10.6%)

Sports Sandals

1.1% (FY18: 1.0%)

Apparel Wholesale*

1.7% (FY18: 4.0%)

HK$ per share*VolumeRevenue

2019 Financial Performance Overview

Source: Company audited financial statements and management accounts * FY19 Total Dividend: HK$1.10/share (Total dividend for FY18 was HK$1.50/share, including HK$1.10/share final dividend and HK$0.40/share interim dividend)

74% 65%

56% 61%

101%

76%

1.15 1.20

1.40

1.50 1.50

1.10

2014 2015 2016 2017 2018 2019

Payout ratio*

17.53 17.25 16.88 16.87 16.53

17.24

307

318

322 325

326 322

2014 2015 2016 2017 2018 2019

Avg. selling price

331 390 535 519

307 301

8,013

8,435 8,481

9,121

9,695 10,105

2014 2015 2016 2017 2018 2019

Profit attrib. to owners

4

USD 10,105.4 mn

Profit Attrib. to Owners

Revenue

USD 300.5 mn

322.4 mn pairs

ASP (USD)

Volume

$17.24

HK $1.10 per share

Dividend Payout Ratio

Dividend*

76%

18.64*7.7532/100=1.445 1.1/1.46=76.1%

Current rate on 30 Mar 2020

Our Growth Strategy

5

Speed

Sustainability

Flexibility

Innovation

Quality

Design

OEM / ODM

Material

Process

Equipment

Apparel

Accessories

Footwear

Retail

Values

5

Directions

4

Segments

3

End to End Platform

2

World’s Leading Sporting Goods

MFG Platform

1

Corporate Social Responsibility

6

The social compliance program of Pou Chen Group (comprising Pou Chen Corporation and Yue Yuen) obtained accreditation from Fair Labor Association (FLA) in June, 2018, as a result of our efforts and commitments in promoting workplace standards, responsible production as well as factory condition improvement.

The Only FLA Accredited Footwear OEM/ODM Globally

A Top-ranking Responsible Investment Target

Pou Chen and Yue Yuen are constituents of world-famous Environmental, Social and Governance (ESG) indexes, including the FTSE4Good Emerging Index and the MSCI World ESG Leaders Index.

Our Focus on Sustainability

Employee Relations

Compliance

Education Implementation Communication Risk Control

ESH & ESG

FY 2019

Group and Operation Highlights

Key Financial Highlights for FY 2019

8

Group

* Excludes TCHC Group

Revenue

US$ 10,105.4 mn + 4.2%

Operating Profit

US$ 470.7 mn

- 5.6%

MFG* GP Margin

18.5% -1.0pp

Shoe Volume

322.4 mn pairs

-1.1%

ASP

US$ 17.24 per pair

+4.3%

Retail Revenue

RMB 27,190 mn +19.9%

OP Margin

5.4%

+1.1pp

Same Store Sales Growth

5.0% -2.4pp

Earnings Per Share

18.64 US cents

-1.1%

Financial Implications of Disposal of TCHC

9

TCHC Group

(US$ million, audited) Jan – May 2019 Jan – Jun 2018 FY 2018

Revenue 171.85 191.50 395.02

Net profit after taxation 10.01 7.61 17.08

Net Asset Value 127.25 85.65 93.28

Disposal

Rationale

Consideration

TCHC Group Financials

* Purchase Price listed above has not yet taking into account the working capital adjustment, the indebtedness and other adjustments

Texas Clothing Holding Corp. (“TCHC”) was disposed on 31 May 2019, upon which it ceased to be a subsidiary of the Company.

The Group’s benefits from the disposal:

- Realizing investment in the TCHC

- Remaining focused on core business

- Releasing working capital and lowering debt levels

Consideration = Purchase Price* (US$230.0 mn) + Earnout Amount (max. US$24.15 mn)

Net proceeds at Closing after debt repayment: approx. US$97.2 mn per cash flow,

which was used to pay down outstanding debt held by the Group

Net gain on disposal is approx. US$18.6 mn, TCHC Group accounts for 1.7% of revenue

and 2.8% of profit of the Group in 2019

Financial Impact

4,541.6

906.2

110.1

3,933.0

171.8

442.7

4,267.7

1,031.0

91.8

3,421.7

392.1

491.0 FY19 FY18

Y-o-Y Revenue by Product Category

10

(US$’ mn)

FY19 Shoe Revenue by Product Categories

Casual/Outdoor Shoes

Sports Sandals

Athletic Shoes

82%

16%

2%

Shoe Rev: US$ 5,557.9 mn (+3.1% YoY)

* TCHC Group (disposed on May 31, 2019) ** Soles, Components & Others *** The decline is due to different comparative base: 5M sales in FY19 vs. 12M sales in FY18

FY19 Total Revenue US$10,105.4 mn FY18 Total Revenue US$9,695.3 mn

***

Athletic Shoes

Casual/Outdoor Shoes

Sport Sandals

Retail

Apparel Wholesale*

Others**

6.4%

12.1%

19.9%

14.9%

56.2%

9.8%

FY19 Manufacturing Revenue by Destination

11

US 31.3% FY18: 31.3% YoY: +1.8%#

Europe 28.5% FY18: 30.2% YoY: -3.5%#

Mainland China 14.7%

FY18: 13.3% YoY: +13.0%#

Others* 25.5%

FY18: 25.3% YoY: +3.1%#

FY19 MFG Revenue: US$ 6,000.6 mn FY18 MFG Revenue: US$ 5,881.5 mn

# YoY changes in revenue amount * Others include Rest of Asia, South America, Canada, Australia and Other Area

China 881.3/6,000.6=14.68%

Europe 1,712.3/6,000.6=28.53%

US 1,875.2/6,000.6=31.25%

Others 1,531.8/6,000.6=25.53%

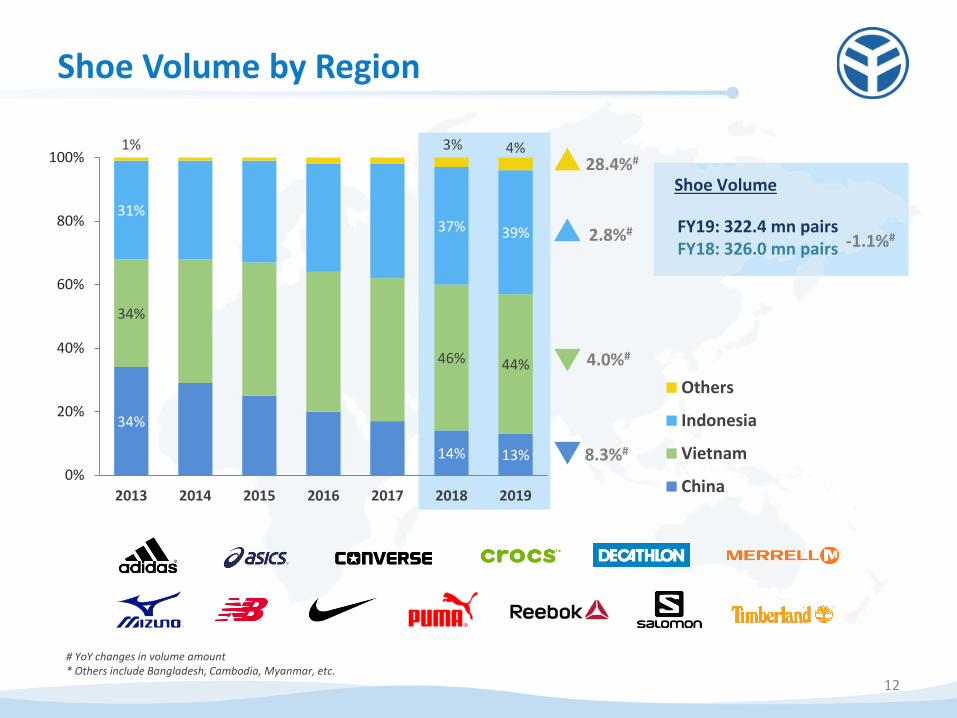

Shoe Volume by Region

12

34%

14% 13%

34%

46% 44%

31% 37% 39%

1% 3% 4%

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 2017 2018 2019

Others

Indonesia

Vietnam

China

# YoY changes in volume amount * Others include Bangladesh, Cambodia, Myanmar, etc.

Shoe Volume

FY19: 322.4 mn pairs FY18: 326.0 mn pairs -1.1%#

28.4%#

2.8%#

4.0%#

8.3%#

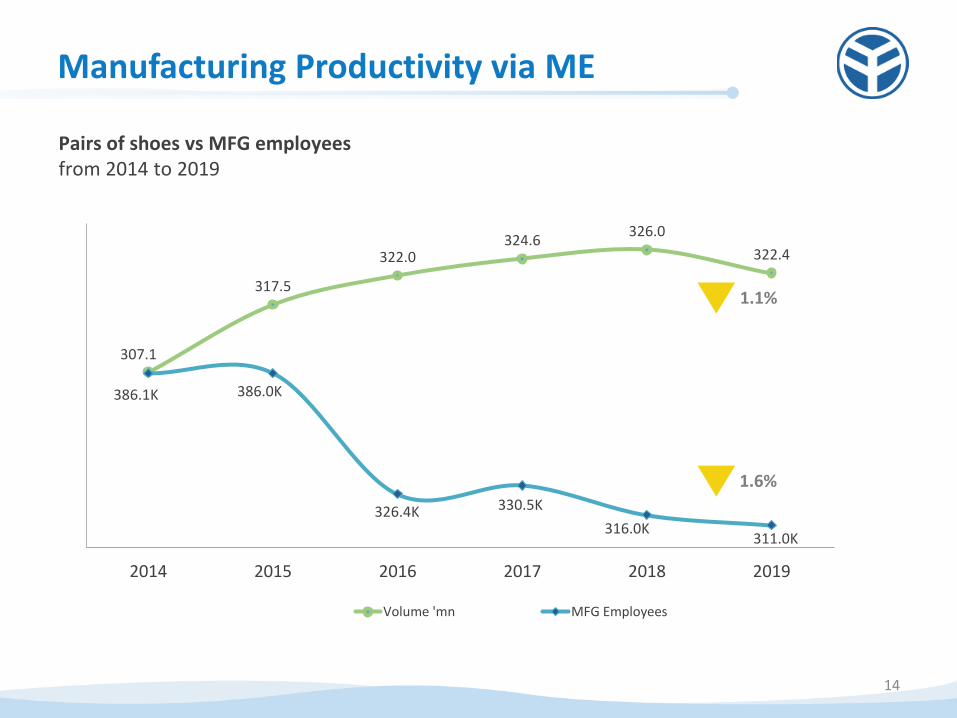

Manufacturing Productivity via ME

13

795.3

822.5

986.5

982.1

1,031.6 1,036.7

2014 2015 2016 2017 2018 2019

Pairs per person during the year

Pairs per Person during the year

PPH Index – Pairs per person per hour from 2014 (index from 100) to 2019

100.0

104.4

115.6

122.2

133.3

128.9

2014

2015

2016

2017

2018

2019

Base Year

0.5%

307.1

317.5

322.0 324.6

326.0

322.4

386.1K 386.0K

326.4K 330.5K

316.0K 311.0K

2014 2015 2016 2017 2018 2019

Volume 'mn MFG Employees

Manufacturing Productivity via ME

14

Pairs of shoes vs MFG employees from 2014 to 2019

1.1%

1.6%

YY Group Financial Highlights

15

(US$’000)

FY 2019 FY 2018 Y-o-Y

Revenue 10,105,387 9,695,282 +4.23%

Gross Profit 2,513,053 2,446,058 +2.74%

Gross Profit Margin 24.87% 25.23% -0.36pp

Operating Profit 470,670 498,591 -5.60%

Operating Profit Margin 4.66% 5.14% -0.48pp

Profit attrib. to Owners 300,546 307,116 -2.14%

Profit attrib. to Owners Margin 2.97% 3.17% -0.20pp

Non-recurring Profit (Loss) attrib. to Owners 18,254 (18,542) N/A

Recurring Profit attrib. to Owners 282,292 325,658 -13.32%

Source: Company accounts Please refer to the announcement on the HKEX website for the audited consolidated income statements of FY2019 & FY2018 For more details, please refer to Appendix

YY Group Financial Ratios

16

Source: Company accounts (figures rounded) Please refer to the announcement on the HKEX website for the audited consolidated income statements of FY2019 & FY2018 *Total borrowings and net borrowings exclude lease liabilities. Lease liabilities was US$ 402.7mn as at 31 Dec, 2019 # Total Debt to Equity and Net Debt to Equity (including lease liabilities) would be 55.0% and 33.3% as at 31 Dec, 2019 respectively

(US$’mn) FY 2019 FY 2018

Depreciation & Amortization 495.1 337.6

EBITDA 957.0 825.9

Capital Expenditure 398.1 494.4

Product Development 208.6 205.9

31 December 2019 31 December 2018

Total Borrowings* 2,089.9 2,123.9

Net Borrowings* 1,107.8 1,272.5

Total Borrowings to Equity # 46.1% 46.7%

Net Borrowings to Equity # 24.4% 28.0%

Quick Ratio (X) 1.1 X 1.1 X

Current Ratio (X) 1.8 X 1.9 X

FY 2019 FY 2018

Total Borrowings to EBITDA (X) 2.2 X 2.6 X

Net Borrowings to EBITDA (X) 1.2 X 1.5 X

Depreciation & Amortization 340,414+139,369+15,320

=495,103 EBITDA=956,968=957.0mn

Capital Expenditure=398,129 TB=2,492,611-130,368-272,364

=2,089,879 NB=1,510,532-130,368-

272,364=1,107,800

暫使用total equity (應使用board paper數據)

TB/Equity=2,089.9/4,533.1 =46.10%

NB/Equity=1,107.8/4,533.1 =24.43%

QR=(4,492,655-1,822,845) /2,458,995=1.08

CR=4,492,655/2,458,995=1.82

Total Debt to Equity 2,492,611/4,533,091=54.98%

Net Debt to Equity 1,510,532/4,533,091=33.32%

Equity使用board paper資產淨值(without IFRS 16)

TB/Equity=2,089.9/4,537.3 =46.06%=46.1%

NB/Equity=1,107.8/4,537.3 =24.41%=24.4%

Total Debt to Equity 2,492.6/4,537.3=54.93%

Net Debt to Equity 1,510.5/4,537.3=33.29%

YY Group’s Cash Position Increased 15.4% in FY19

17

851.4 982.1

Beginning Cash 1 Jan 19

Ending Cash 31 Dec 19

(US$’mn)

+874.9 -398.1

CAPEX

Cash from Operations

Interest Borrowing

Others

US$321.3mn Return to Shareholders

Disposal of TCHC

Net Borrowings Raised

+97.2

Lease Liabilities

Repayment and Interest

Share Buyback

Cash Dividend

-144.8

-12.2 -309.1

-72.3 +76.3 +18.8

4.8

6.4

5.8

6.5

7.6

7.4

6.6

5.3

4.1

4.4

4.0

7.5

9.9

8.7

9.4

11.3 11.3

12.1

10.0

7.4

8.0

7.3

FY14 1H15 FY15 1H16 FY16 1H17 FY17 1H18 FY18 1H19 FY19

ROA ROE

YY Group ROE & ROA Trend

18

Remark: ROE = Profit attributable to owners of the company/ (Total Equity - Minority Interests); half year data is on LTM basis ROA = Net Profit / Total Asset; half year data is on LTM basis

(%)

ROE 300,546/4,098,706

=7.33%=7.3% ROA

353,000/8,789,391 =4.01%=4.0%

18.7 18.9 18.9 19.7 19.8 20.2 20.3

20.9 21.0 20.8 20.7 21.0

18.7 18.8 19.3 19.5 18.2 18.0 18.2 18.5

22.3 22.6 22.7 23.4

24.4 24.7 24.8 25.1 25.0 25.4 25.4 25.8 25.2 25.0 25.0 25.2 25.2 25.1 24.8 24.9

30.9 32.2 32.5

33.3

34.9 35.6 35.8 35.5

33.6 34.6 34.5 35.0

33.8 33.5 33.1 33.5 33.9 34.5 34.2 34.1

1Q 1H 9M 12M 1Q 1H 9M 12M 1Q 1H 9M 12M 1Q 1H 9M 12M 1Q 1H 9M 12M

MFG Group PS

YY Group GPM Analysis

19

Remark: GPM information is YTD basis

(%)

FY 2015 FY 2016 FY 2017 FY 2018 FY2019

Group excl. PS Note:

The figures in the following slides cover the core manufacturing and other operations of the consolidated entity of Yue Yuen Group, and are for analytical purposes only (prepared using the management accounts).

Group excl. PS Financial Highlights

21

(US$’000) MFG only

FY 2019 FY 2018 Y-o-Y FY 2019 FY 2018 Y-o-Y

Revenue 6,172,422 6,273,625

-1.61% 6,000,573 5,881,494

+2.02%

Gross Profit 1,171,368 1,299,557 -9.86% 1,107,034 1,149,027 -3.65%

Gross Profit Margin 18.98% 20.71% -1.73pp 18.45% 19.54% -1.09pp

Operating Profit 256,528 351,760 -27.07% 244,560 323,361 -24.37%

Operating Profit Margin 4.16% 5.61% -1.45pp 4.08% 5.50% -1.42pp

Profit attrib. to Owners 225,574 256,035 -11.90% 215,562 240,038 -10.20%

Profit attrib. to Owners Margin 3.65% 4.08% -0.43pp 3.59% 4.08% -0.49pp

Source: Company management accounts For more details, please refer to Appendix

4.09 3.59

Product Mix & Capacity Migration

Manufacturing – Net Profit Margin

22

Material

-0.96

-0.13

FY18 Net Profit Margin

-0.04 +0.54 +0.08

+0.11

-0.29

+0.19

FY19 Net Profit Margin

Hedging Fair Value & Realized

Other Income & Expenses FX Loss

Others

(%)

Labor & Overhead

SG&A Gains from Disposal of Subsidiaries & Asso. Disposal of TCHC Group

Share of results of A&JV

Gross Profit

14.5% 14.2%

29.2% 30.4%

36.8% 36.9%

Manufacturing – COGS Decomposition and Y-o-Y

Amount (Y-o-Y)

Labor *

6.3%

2.4%

Overhead

FY19 FY18

% of Revenue % of Revenue

3.7%

FY19 GPM 18.5%

0.3%

Material

23 * Cost of labor includes cost of direct labor and indirect labor

46%

36%

18%

45%

37%

18%

FY19 vs. FY18 COGS Composition

Material Labor Overhead*

18.7

19.1

18.9

21.9

19.8

20.5 20.5

22.8

21.0 20.7

20.4

21.8

18.7

18.9

20.2

20.3

18.2 17.9

18.5

19.2

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Profit Margin (MFG only)

Manufacturing - GP Margin Trend

24

GP Margin % - Group excl. PS (including MFG and TCHC)

3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

21.6 22.7 20.1 19.9 21.4 21.3 19.6 18.7 18.5 19.2

(%)

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

19.7% 20.9% 21.0% 19.5% 18.5%

Remark: TCHC became subsidiary of the Group on April 7, 2017 and was then disposed on May 31, 2019

5.3

6.1

3.7

6.8

5.9

7.5

6.7

9.8

6.9

7.2 7.8

8.6

5.7

4.8

4.8

6.7

4.5

3.6 3.6

4.6

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Operating Profit Margin (MFG Only)

Manufacturing - OP Margin Trend

25

OP Margin % - Group excl. PS (including MFG and TCHC)

3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

8.0 8.4 6.0 4.7 5.2 6.5 4.7 3.7 3.6 4.6

(%)

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

5.5% 7.6% 7.7% 5.5% 4.1%

Remark: TCHC became subsidiary of the Group on April 7, 2017 and was then disposed on May 31, 2019

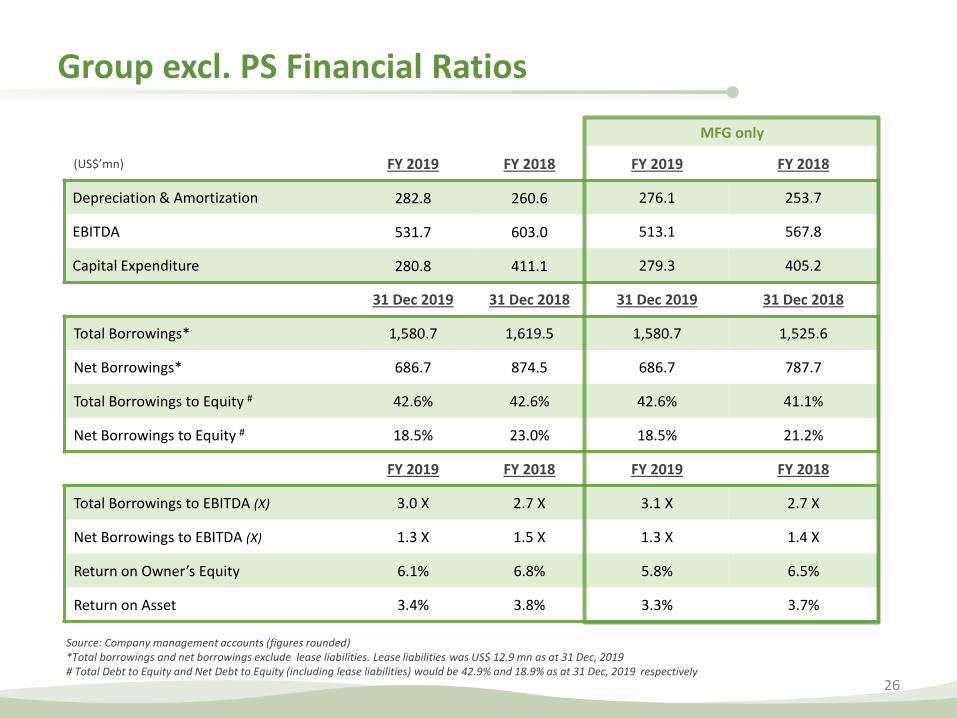

Group excl. PS Financial Ratios

26

MFG only

(US$’mn) FY 2019 FY 2018 FY 2019 FY 2018

Depreciation & Amortization 282.8 260.6 276.1 253.7

EBITDA 531.7 603.0 513.1 567.8

Capital Expenditure 280.8 411.1 279.3 405.2

31 Dec 2019 31 Dec 2018 31 Dec 2019 31 Dec 2018

Total Borrowings* 1,580.7 1,619.5 1,580.7 1,525.6

Net Borrowings* 686.7 874.5 686.7 787.7

Total Borrowings to Equity # 42.6% 42.6% 42.6% 41.1%

Net Borrowings to Equity # 18.5% 23.0% 18.5% 21.2%

FY 2019 FY 2018 FY 2019 FY 2018

Total Borrowings to EBITDA (X) 3.0 X 2.7 X 3.1 X 2.7 X

Net Borrowings to EBITDA (X) 1.3 X 1.5 X 1.3 X 1.4 X

Return on Owner’s Equity 6.1% 6.8% 5.8% 6.5%

Return on Asset 3.4% 3.8% 3.3% 3.7%

Source: Company management accounts (figures rounded) *Total borrowings and net borrowings exclude lease liabilities. Lease liabilities was US$ 12.9 mn as at 31 Dec, 2019 # Total Debt to Equity and Net Debt to Equity (including lease liabilities) would be 42.9% and 18.9% as at 31 Dec, 2019 respectively

Depreciation & Amortization 271,889+10,782+148=282,819

269,456+6,630=276,086 EBITDA

531,748=531.7 mn 513,057=513.1 mn Capital Expenditure 280,785=280.8 mn 279,250=279.3 mn

TB/EBITDA=1,580.7/531.7=2.97 TB/EBITDA=1,580.7/513.1=3.08 NB/EBITDA=686.7/531.7=1.29 NB/EBITDA=686.7/513.1=1.33

ROE=225,574/3,695,251=6.10% ROE=215,562/3,695,251=5.83% ROA=225,574/6,575,946=3.43% ROA=215,562/6,575,946=3.27%

Total Debt to Equity =1,593.5/3,710.4=42.94%

Net Debt to Equity 699.6/3,710.4=18.85%

TB=1,593,535-2,629-10,231 =1,580,675

NB=699,567-2,629-10,231=686,707

TB/Equity=1,580.7/3,710.4 =42.6%

NB/Equity=686.7/3,710.4 =18.50%

FY 2018 MFG only 250,128+3,577=253,705

FY 2018 MFG only

TB/EBITDA=1526.6/567.8=2.68 NB/EBITDA=787.7/567.8=1.38

Working Capital Days

Manufacturing Operation Efficiency

Trade Receivable Days

Inventory Days

Trade Payable Days

52

60

30

82

FY18

27

FY19

50

57

29

78

Pou Sheng International

Note:

The figures in the following slides are based on Pou Sheng’s management accounts and announcements, and Pou Sheng adopts RMB as its

reporting currency

Agenda

01 Financial Highlights p31-35

02 Business Update p37-40

03 Omni-channel Strategy p42-44

04 Summary and Outlook p46-47

Distinguished Partners and Sports Services

30

VISION MAKE SPORTS YOUR LIFE!

Products Sports Events Sports Services

Pou Sheng Financial Highlights

31

RMB'mn US$'000

FY 2019 FY 2018 Y-o-Y FY 2019 FY 2018 Y-o-Y

Revenue 27,190 22,677 +19.90% 3,932,965 3,421,657

+14.94%

Gross Profit 9,275 7,599 +22.06% 1,341,685 1,146,501 +17.02%

Gross Profit Margin 34.11% 33.51% +0.60pp 34.11% 33.51% +0.60pp

Operating Profit 1,472 967 +52.22% 212,936 145,887 +45.96%

Operating Profit Margin 5.41% 4.26% +1.15pp 5.41% 4.26% +1.15pp

Profit attrib. to Owners of PS 833 543 +53.41% 120,533 81,913 +47.15%

Profit attrib. to Owners Margin 3.06% 2.39% +0.67pp 3.06% 2.39% +0.67pp

Source: Based on Pou Sheng’s announcement on the HKEX website for the audited consolidated income statements of FY2019 & FY2018 For more details, please refer to Appendix

For FY 2019, the profit for the period decreased by RMB27.9 million due to the application of HKFRS16.

30.9

33.4

33.2

35.8

34.9

36.3

36.2

34.8

33.6

35.6

34.5

36.3

33.8 33.3

32.2

34.6

33.9

35.2

33.5

33.9

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Profit Margin

Pou Sheng GP Margin Trend

32

(%)

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

33.3% 35.5% 35.0% 33.5% 34.1%

3.5

5.8

4.3

2.9

6.6 7.2

5.5

3.5

4.5

6.1

2.9 2.8

4.6 4.9

3.0

4.5 5.4

6.2

4.9

5.2

1Q15*2Q15*3Q15*4Q15* 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Operating Profit Margin

Pou Sheng OP Margin Trend

33

* The figures have been restated due to the application of merger accounting

(%)

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

4.1% 5.7% 4.1% 4.3% 5.4%

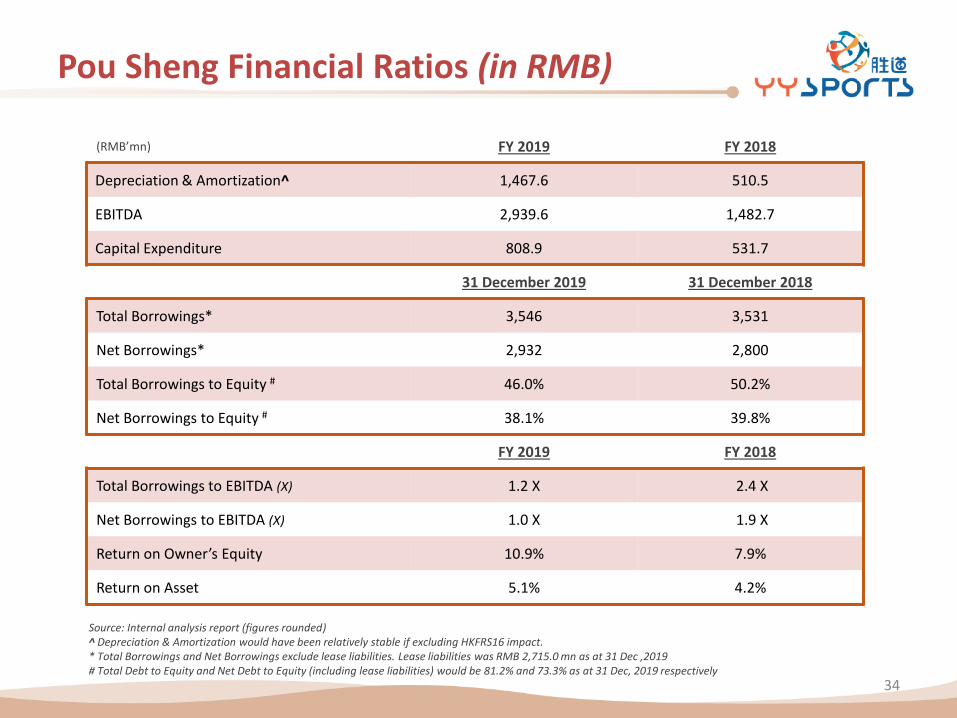

Pou Sheng Financial Ratios (in RMB)

34

(RMB’mn) FY 2019 FY 2018

Depreciation & Amortization^ 1,467.6 510.5

EBITDA 2,939.6 1,482.7

Capital Expenditure 808.9 531.7

31 December 2019 31 December 2018

Total Borrowings* 3,546 3,531

Net Borrowings* 2,932 2,800

Total Borrowings to Equity # 46.0% 50.2%

Net Borrowings to Equity # 38.1% 39.8%

FY 2019 FY 2018

Total Borrowings to EBITDA (X) 1.2 X 2.4 X

Net Borrowings to EBITDA (X) 1.0 X 1.9 X

Return on Owner’s Equity 10.9% 7.9%

Return on Asset 5.1% 4.2%

Source: Internal analysis report (figures rounded) ^ Depreciation & Amortization would have been relatively stable if excluding HKFRS16 impact. * Total Borrowings and Net Borrowings exclude lease liabilities. Lease liabilities was RMB 2,715.0 mn as at 31 Dec ,2019 # Total Debt to Equity and Net Debt to Equity (including lease liabilities) would be 81.2% and 73.3% as at 31 Dec, 2019 respectively

Total Borrowings 3,545,995

Net Borrowings 3,545,995-613,591

=2,932,404

3,545,995/7,706,078=46.0% 2,932,404/7,706,078=38.1%

ROE 833,275/7,612,574=10.94%

ROA 879,910/17,390,782=5.1%

Lease Liability

889,552+1,825,445 =2,714,997=2715.0 mn

Total Debt=3546+2715=6,261

Total Debt to Equity 6,261/7,706 =81.24%

Net Debt=2,932+2715=5,647 Net Debt to Equity

5,647/7,706=73.28%

Total Borrowings to EBITDA (X) 3,546/2,939.6=1.2

Net Borrowings to EBITDA (X) 2,932/2,939.6=0.997=1.0

Working Capital Days

Operation Efficiency

35

Trade Receivable Days

Inventory Days

Trade Payable Days

FY19

150

21

15

156

149

27

15

161

FY18

Based on RMB

Agenda

01 Financial Highlights p31-35

02 Business Update p37-40

03 Omni-channel Strategy p42-44

04 Summary and Outlook p46-47

Pou Sheng Retail Strategy

7

88%

12%

FY2019 Revenue by Channel Mix

FY 2018 FY 2019

Sub-Distributors

Directly Operated Stores

78% 78%

22%

22%

Pou Sheng is one of the largest retailers and sports services providers for world renowned sportswear brands in the Greater China region

Brick & Mortar Retail Omni-channel

• Mono Brands Stores: 5,795 stores

• Multi-Brands Stores: 88 stores

FY 2018 FY 2019

B2B B2C

19%

50% 81%

50%

B2C Channel:

• 3rd party platforms: T-Mall, JD,

Vipshop, etc. • WeChat stores (+ExP services)

• Shopping mall platforms

37

Directly Operated Stores:

Pou Sheng Store Performance

38

Sub-Distributor (Franchisee)

As at December 31, 2018

5,648 235

Directly Operated (Own-Store)

Total Store Net

New Store +/(-)

5,883

3,551 3,551 399 3,950

9,833

Number of Stores

634 9,199

As at December 31, 2019

Pou Sheng Retail Coverage

PS retail channel covers more than 300 cities in the Greater China

> 300 stores 100- 300 stores <100 stores

39

1.9%

5.6%

1.5%

12.0%

10.1%

2.2%

8.9%

8.7% 8.4%

4.2%

6.0%

1.9%

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Same Store Sales Growth

Pou Sheng Same Store Sales Growth (SSSg)

40

(%)

FY 2017 FY 2018 FY 2019

5.3% 7.4% 5.0%

Agenda

01 Financial Highlights p31-35

02 Business Update p37-40

03 Omni-channel Strategy p42-44

04 Summary and Outlook p46-47

Pou Sheng Product Sharing Platform (PSP)

Logistics of omni-channel will be facilitated through all-rounded channels: RDC, YYsports.com, 3rd party online platform, 27-Zone inventory sharing and Direct B&M

PSP

B&M1 ….. B&Mn

12.12

YY Sports app

YY Sports app

6.18 11.11

365-day O2O, earlier sales, higher price, via PSP

Warehouse 1,2,3,4

Products

RDC: Regional Distribution Center Direct B&M : Directly operated Brick and Mortar Stores

42

3rd party platforms ExP services WeChat stores

Pou Sheng Product Sharing Platform (PSP)

Participation rate: more than 60% Direct B&M stores participate PSP at the end of 2019

43

Kunshan

Taicang

Dongguan

Regional Warehouse

PSP Contribution - Top 6 Regions

Participating PSP Regions

New Service Hub to Enhance Omni-channel Capability

44

“Low Conversion Offline Network” +

“Discount Online Network”

Service Hub (Next Store) Series of 1-day event & 364 days fun services Products with stories & outfit consultations

M Mono Brand Stores Convert shoppers into loyal members

(Less stores more sales) Membership w/ privilege to Service Hub

(Higher sales conversion rate) Modularized services in mono brand stores (Uniqueness)

M

M

M M

M

M

M

M

M

M

Online 24/7 Communication Platform Magazine-like contents to

“Make sports your life” APP, mini-program & other strategic resources to enact inactive target audiences

“Normal price + premium services” by omni- platform connecting to efficient retail network

Sports Services & ExP Program Expand and engage active membership

Agenda

01 Financial Highlights p31-35

02 Business Update p37-40

03 Omni-channel Strategy p42-44

04 Summary and Outlook p46-47

Pou Sheng COVID-19 Reaction Plan

46

• Accelerate B2C sales & PSP contribution

• Roll out WeChat mini stores to drive sales growth

• Brand collaboration & inventory management e.g return inventory, reduce in-season purchase, support promotion discount

• Rent reduction negotiation

• Government support

• Closely monitor and maintain cash flow & gearing ratio at a healthy level

• Real-time monitor daily sales & store re-open progress

• Monitor wholesaler & provide appropriate support

1

Operation

2

Brick & Mortar Stores 3

Omni- Channel

Future Target: Profitable Growth

Future Target

• Total revenue growth in mid-teens, with omni-channel contributing 20% of total revenue • More in-season sales and more effective off-season products sales through various 3rd party channels • Integrating the Service Hub model into our strong brick and mortar stores foundation • Turnaround of emerging brands and licensee brands • Operating margin improving by 2 percentage points

Retail Network

Omni-Channel

Next

Store

“Creating Value-added Services and Quality Experiences to Customers”

47

Appendix

Shareholding Structure

49

Pou Chen (9904.TT)

Yue Yuen Industrial (Holdings) Ltd. (551.HK)

62.19%

51.11%

* As at December 31, 2019

100%

Manufacturing and Others Pou Sheng (3813.HK)

From Queenie: As at Dec 31, 2019, PCC holds 51.1197% of YY while YY holds 62.1967% of PS.

Company Milestones

50

Started first overseas production in south China

Established production bases in Vietnam

Established production bases in Mexico

Established production bases in eastern and inland China

Began operations at the new headquarters in Taichung, Taiwan

Established production bases in Bangladesh & Cambodia

Established production bases in Myanmar

1988

1992

1994

1998

2001

2002

2006

2008

2009

2014

2015

Expanded into retail business in China

Became sole licensee for Hush Puppies in Taiwan

Pou Sheng International listed on HKEX (3813.HK)

Became sole licensee for Pony in Taiwan & China

Yue Yuen

Pou Sheng

2012 Ms. Tsai Pei Chun, Patty appointed as CEO of Pou Chen Group

Yue Yuen Industrial listed on HKEX (551.HK) Established production bases in Indonesia

Yue Yuen Industrial founded

2019

Parent Pou Chen Group is accredited by FLA 2018

Parent Pou Chen Group’s 50th Anniversary

Recorded RMB 22 bn revenue. Sales channels over 9,000

Omni-channel contributed ~12% of total sales in 2019

Became sole licensee for Rockport footwear and GEOX in China

2016

Revenue crossed the US$10 bn mark

FY18 FY19

3,421.66

6,273.63

3,932.97

6,172.42

9,695.29 10,105.39

FY18 FY19

Revenue & Profit Attributable to Owners

51

Revenue

In US$’mn

Profit Attrib. to Owners

In US$’mn

Pou Sheng

Group excl. PS

The above figures of Pou Sheng exclude profit attributable to “Non-YY” shareholders (i.e. FY19: 37.8% minority interests; FY18: 37.6% minority interests)

Pou Sheng

Group excl. PS

-2.1% +4.2%

+14.9%

-1.6%

+46.8%

-11.9%

51.08

256.04

74.97

225.57

307.12 300.54

YY Group Financial Highlights

52

Source: Company accounts Please refer to the announcement on the HKEX website for the audited consolidated income statements of FY2019 & FY2018 *Finance Cost in FY19 grew by 14.4% due largely to the US$15.5 mn effects of the application of HKFRS16

FY 2019 FY 2018 Y-o-Y

US$'000 % US$'000 % + / -

Revenue 10,105,387 100.00 9,695,282 100.00 +4.23%

Cost of Sales (7,592,334) -75.13 (7,249,224) -74.77 +4.73%

Gross Profit 2,513,053 24.87 2,446,058 25.23 +2.74%

SG&A (1,904,794) -18.85 (1,818,348) -18.76 +4.75%

Other Income & Expenses, net (137,589) -1.36 (129,119) -1.33 +6.56%

Operating Profit 470,670 4.66 498,591 5.14 -5.60%

Finance Cost* (92,122) -0.91 (80,551) -0.83 +14.36%

Share of Results of A&JV 51,995 0.51 39,480 0.41 +31.70%

Other Gains and Losses 17,895 0.17 (17,956) -0.19 N/A

Income Tax (95,438) -0.94 (98,448) -1.01 -3.06%

Profit for the Period 353,000 3.49 341,116 3.52 +3.48%

Profit attrib. to Owners 300,546 2.97 307,116 3.17 -2.14%

Other Gain and Loses (%) =17,895/10,105,387

=0.177%=0.17%

Group excl. PS Financial Highlights – MFG and TCHC

53

Source: Company management accounts

FY 2019 FY 2018 Y-o-Y

US$'000 % US$'000 % + / -

Revenue 6,172,422 100.00 6,273,625 100.00 -1.61%

Cost of Sales (5,001,054) -81.02 (4,974,068) -79.29 +0.54%

Gross Profit 1,171,368 18.98 1,299,557 20.71 -9.86%

SG&A (726,648) -11.66 (779,464) -12.42 -6.78%

Other Income & Expenses, net (188,192) -3.05 (168,333) -2.68 +11.80%

Operating Profit 256,528 4.16 351,760 5.61 -27.07%

Finance Cost (56,318) -0.91 (57,942) -0.92 -2.80%

Share of Results of A&JV 51,837 0.84 39,620 0.63 +30.84%

Other Gains and Losses 19,273 0.31 (17,956) -0.29 N/A

Income Tax (45,598) -0.74 (58,996) -0.94 -22.71%

Profit for the Period 225,722 3.66 256,486 4.09 -11.99%

Profit attrib. to Owners 225,574 3.65 256,035 4.08 -9.16%

Group excl. PS Financial Highlights – MFG only

54

Source: Company management accounts

FY 2019 FY 2018 Y-o-Y

US$'000 % US$'000 % + / -

Revenue 6,000,573 100.00 5,881,494 100.00 +2.02%

Cost of Sales (4,893,539) -81.55 (4,732,467) -80.46 +3.40%

Gross Profit 1,107,034 18.45 1,149,027 19.54 -3.65%

SG&A (674,076) -11.23 (658,261) -11.19 2.40%

Other Income & Expenses, net (188,398) -3.14 (167,405) -2.85 +12.54%

Operating Profit 244,560 4.08 323,361 5.50 -24.37%

Finance Cost (53,894) -0.90 (52,670) -0.89 +2.32%

Share of Results of A&JV 51,837 0.86 39,620 0.67 +30.84%

Other Gains and Losses 19,273 0.32 (17,956) -0.31 N/A

Income Tax (46,066) -0.77 (51,866) -0.88 -11.18%

Profit for the Period 215,710 3.59 240,489 4.09 -10.30%

Profit attrib. to Owners 215,562 3.59 240,038 4.08 -10.20%

Pou Sheng Financial Highlights (in RMB)

55

FY 2019 FY 2018 Y-o-Y

RMB’mn % RMB’mn % + / -

Revenue 27,190 100.00 22,677 100.00 +19.90%

Cost of Sales (17,914) -65.89 (15,078) -66.49 +18.81%

Gross Profit 9,275 34.11 7,599 33.51 +22.06%

SG&A (8,181) -30.09 (6,913) -30.49 +18.34%

Other Income & Expenses, net 377 1.39 281 1.24 +34.16%

Operating Profit 1,472 5.41 967 4.26 +52.22%

Finance Cost, net* (239) -0.88 (144) -0.64 +65.97%

Share of Results of JV 1.1 0.01 (1) -0.00 N/A

Other Losses (9) -0.03 - N/A N/A

Income Tax (345) -1.27 (261) -1.15 +32.18%

Profit for the Period 880 3.24 561 2.47 +56.86%

Profit Attrib. to Owners of PS 833 3.06 543 2.39 +53.41%

Source: Based on Pou Sheng’s announcement on the HKEX website for the audited consolidated income statements of FY2019 & FY2018 *Finance Cost in FY19 grew by 66.0% due largely to the RMB 101.1mn effects of the application of HKFRS16

Cost of sales (%) =17,914,296/27,189,765

=65.89%

Profit for the Period(%) =880/27,190 =3.236=3.24

Share of Results of JV(%) =1.1/27,190 =0.004=0.01

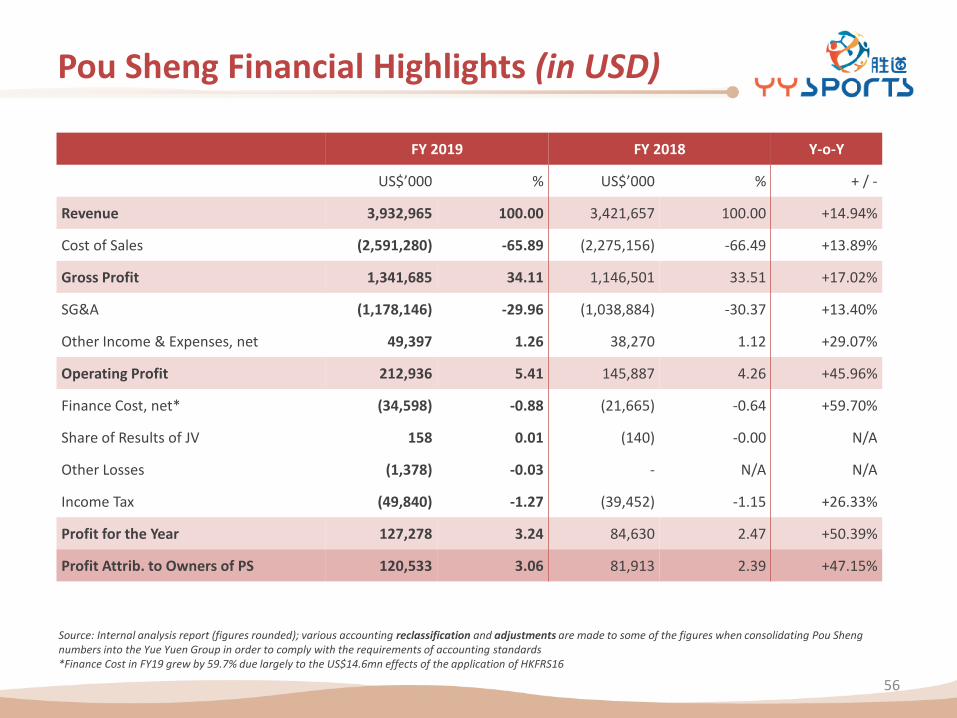

Pou Sheng Financial Highlights (in USD)

56

FY 2019 FY 2018 Y-o-Y

US$’000 % US$’000 % + / -

Revenue 3,932,965 100.00 3,421,657 100.00 +14.94%

Cost of Sales (2,591,280) -65.89 (2,275,156) -66.49 +13.89%

Gross Profit 1,341,685 34.11 1,146,501 33.51 +17.02%

SG&A (1,178,146) -29.96 (1,038,884) -30.37 +13.40%

Other Income & Expenses, net 49,397 1.26 38,270 1.12 +29.07%

Operating Profit 212,936 5.41 145,887 4.26 +45.96%

Finance Cost, net* (34,598) -0.88 (21,665) -0.64 +59.70%

Share of Results of JV 158 0.01 (140) -0.00 N/A

Other Losses (1,378) -0.03 - N/A N/A

Income Tax (49,840) -1.27 (39,452) -1.15 +26.33%

Profit for the Year 127,278 3.24 84,630 2.47 +50.39%

Profit Attrib. to Owners of PS 120,533 3.06 81,913 2.39 +47.15%

Source: Internal analysis report (figures rounded); various accounting reclassification and adjustments are made to some of the figures when consolidating Pou Sheng numbers into the Yue Yuen Group in order to comply with the requirements of accounting standards *Finance Cost in FY19 grew by 59.7% due largely to the US$14.6mn effects of the application of HKFRS16

Share of Results of JV(%) =158/3,932,965

=0.004=0.01

Other Losses(%) =1,378/3,932,965

=0.035=0.03(配合P.53)

Thank you

Q&A