xerox corp. –xrx 2020 2goizuetaimg.com/wp-content/uploads/2017/07/xrx-pitch-final.pdf · product,...

TRANSCRIPT

Xerox Corp. – XRX 2020 2.8

December 2018Pitch Team: Feng | Atlas | Zhao | Wang | Lee

1

Table of Contents

I. Security Overview

II. Industry and Company Overview

III. Recent Performance

IV. Investment Merits and Risks

V. Financial Model and Analysis

VI. Security Analysis

VII. Appendix and Supplemental Figures

2

Security Overview

Informational Characteristics

§ CUSIP – 984121cH4

§ Coupon – 2.8% Fixed, Semi-Annual

§ Maturity – 05/15/2020

§ Senior Unsecured

§ Amount Issued / Outstanding – 400,000M / 312,767M

§ Credit Rating – Moody’s (Baa3), S&P (BBB-) , Fitch (BB+)

§ Face Value – 1,000M

Source: Bloomberg

Industry and Company Overview

4

Industry Overview

Current State of Industry

Since 2013, the office equipment industry has not grown. The industry generated $42 billion in revenue in 2018 with the

number of businesses in the sector growing by 0.7% and the number of employees declining by 2.4%. Consumer

preferences are favoring lower end, smaller printers as the demand for large printers has significantly decreased. This

trend has occurred because print industry products, such as retail catalogs and banking forms, are in low demand due to

e-commerce and online financial transactions. Market segments that the office equipment industry can expand into are

packaging and 3D printing. However, the 3D printing market is far from being fully commercialized.

Source: IBIS World

5

Industry Overview

Low End Market

The low end printer market is currently dominated by HP (17%), Canon (16%), and Ricoh (15%). Xerox only controls

5% of the low end printer market. Industry experts do not expect Xerox to take market share from the market leaders. If

Xerox is to gain market share in the low end printer market, then it would have to come from the 39% of the market that

is held by smaller businesses.

Source: UBS & Morningstar

6

Industry Overview

Similar Revenue Trends Among Competitors

The industry is experiencing secular headwinds due to the improvement of technology. While Xerox has struggled to

find innovative channels to increase top-line growth, key competitors such as HP Inc. have also experienced gradual

revenue losses, too. Since 2008, HP’s net revenue from printing has fallen from $29.61 billion to $18.8 billion in 2018.

Source: Statista

0.

5.

10.

15.

20.

25.

30.

35.

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

HP’s Net Revenue from the Printing Segment from 2008 to 2017 (in billion US dollars)

7

Industry Overview

YoY Revenue Growth % Compared to Industry

Source: Bloomberg

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

4Q2013 1Q2014 2Q2014 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017 3Q2017 4Q2017 1Q2018 2Q2018 3Q2018

XeroxYoYRevenueGrowth%vs.Competitors

Xerox Canon KonicaMinolta HPQ Fujifilm

8

Industry Overview

HP – Samsung Merger

In 2017, HP completed a purchase of Samsung’s printer business for $1.05 billion. This will drastically change the

office equipment industry and Xerox’s market leading segment of A3 printers ($55 billion); Samsung’s technology

allows HP to produce and sell A3 printers at a significantly lower cost. With Samsung’s tech, HP now offers the

industry’s strongest portfolio of A3 multifunction printers that deliver the simplicity of printers with the high

performance of copiers. The fully integrated portfolio, including next generation PageWide technologies, offers

opportunities to grow managed print and document services as sales models shift from transactional to contractual.

Customers will have greater choice, reliability and uptime, with lower cost of ownership and more affordable color. The

combined portfolio also features security such as HP Connection Inspector, HP Sure Start, run-time intrusion detection

and whitelisting.

Source: CNBC, UBS & Morningstar

9

Company Overview

Xerox’s business is currently operating in a market estimated at approximately $85 billion and is composed of three

main business segments: Managed Document Services, Workplace Solutions and Graphic Communications. Managed

Document Services focuses on workflow automation service, targeting customers like insurance companies, higher

education institutions, retail banks, manufacturers, retailers, governments and healthcare providers. This service is aimed

to optimize printing infrastructure and establish the efficient communication channel of a company by adopting IT

solutions. Workplace solutions consists of sales of entry and mid-range level workplace printing devices through

resellers and partners. It targets small, medium and large-scale businesses. Graphic Communication Solutions consists of

product, software, and supply sales for customers in graphic communications, in-plant and production print

environments with high-volume printing requirements. This includes publishing, transaction printing, print on demand

and one-to-one marketing.

Source: Xerox 10K

10

Company Overview

Xerox distributes its products to unaffiliated third parties throughout the world and has manufacturing and distribution

facilities located around the world. Two of its largest manufacturing sites are located in Webster, N.Y. and Dundalk,

Ireland. Xerox also has a long-standing relationship with FLEX LTD (formerly known as Flextronics), a global

electronics manufacturing services. In addition, Xerox also acquires products from various third parties to increase the

breadth of its product portfolios.

In 2017, 75% of Xerox’s total revenue was related to post-sale streams including document services, equipment

maintenance, consumable supplies and financing, etc. However, both equipment and post-sale revenue has decline

since 2014. Geographically, Xerox has a diverse base of customers spanning 160 countries, and has established sales

through resellers and partners. Approximately 40% of all sales are generated by customers outside the US. Xerox has

a total of 68,540 granted patents that mainly encompass printing and hardware technologies.

Source: Xerox 10K

Recent Performance

12

Recent Performance

Bond and Stock Charts

Source: Bloomberg

Bond

Stock

13

Recent Performance

TTM Bond Performance

Xerox’s bonds have performed poorly in the last 12 months in response to the Fujifilm / Xerox merger falling through.

At the moment, our 2020 bond is trading close to its 12-month low (97.606), down from its 12-month high (100.168) on

February 1, 2018. Since then, there’s been a consistent down trend in the price of the bond. Xerox’s stock also had an

adverse reaction to the merger falling through. Xerox is currently trading at $26.92, down from its 12-month high on

January 31, 2018 ($34.13). Its low was $24 on June 29, 2018.

Source: UBS and Bloomberg

14

Recent Performance

Decline in Revenue

Xerox’s TTM earnings (from June 30, 2018) has more than halved from the same point in 2017 ($101M USD to $598M

USD). They had already been in decline, with average earnings growth of -17.32% over the last 5 years. Earnings

growth decline is exceeding revenue growth decline, which is a red flag. This implies Xerox has increased expenses,

which is not good practice when revenue is declining. This directly harms margins and earnings and isn’t sustainable;

however, this is part of Xerox’s restructuring. Free Cash Flow (FCF) consistently declined from 2012-2017; however,

recently Xerox has seen an influx in cash, which bodes well for bondholders. In the most recent quarterly report,

management also released positive guidance for FCF. Since 2012, Xerox has also seen a strong increase in operating

margin; at 8.8% they’re above the printing industry average.

Source: FactSet and Bloomberg

Investment Merits and Risks

16

Investment Merits

New CEO and Potential Sale of Xerox

John Visentin, Xerox’s new CEO, a track record of successes throughout his career, serving in executive roles for big

tech firms such as HP and IBM. He has expanded and enhanced service offerings, delivery and overall client

satisfaction. Vistentin also contributed to successful acquisitions for Apollo Global Management, including its

acquisitions of Presidio and Pitney Bowes’ Management Services (creating Novitex Enterprise Solutions). Vistentin was

made CEO and Executive Chairman of Novitex. In 2017, Novitex merged with SourceHOV to form Exela Technologies

in a transaction valued at approximately $2.8 billion, representing a 7.3x multiple of the projected 2017 pro forma

EBITDA for the combined company of $385 million. With Visentin on board, there is hope that Xerox will sell at a

higher price, fulfilling Icahn’s wishes.

In May of 2018, news broke that Apollo Global approached Xerox about a possible acquisition. Although there has not

been much about it in the media recently, this sale has a reasonable chance to succeed. Visentin has worked with Apollo

a number of times. Due to the strong financing influence of Apollo, Xerox would likely refinance their debt in that

situation. If Apollo were to raise additional debt, it would be junior to current debt.

Source: Reuters and Xerox

17

Investment Merits

Carl Icahn and his Strategy

Carl Icahn is a major shareholder in Xerox, holding a combined 13% with Darwin Deason. Known as a corporate raider

and shareholder activist, Icahn is very involved with all of his investments. He uses the “Greenmail” method, in which

he buys publicly traded companies reflecting poor P/E ratios (or with book values that exceed the current market

valuation) and then burdens them with debt. He then significantly increases leverage ratios, generating cash flow and

raising the company’s share price. Once he reaches his desired share prices, Icahn sells his shares and exits with a large

profit.

Icahn recently did this with Xerox, threatening the company after learning about the FujiFilm deal and ultimately

replacing the company’s management team. Icahn believes that Xerox is worth at least $40 a share and will not settle for

less. Once this target share price is met, Icahn will likely exit. Icahn increases leverage ratios without regard for debt

structures. This poses a challenge because Icahn will likely leave the company with a poor credit rating and lots of debt.

Source: Business Insider

18

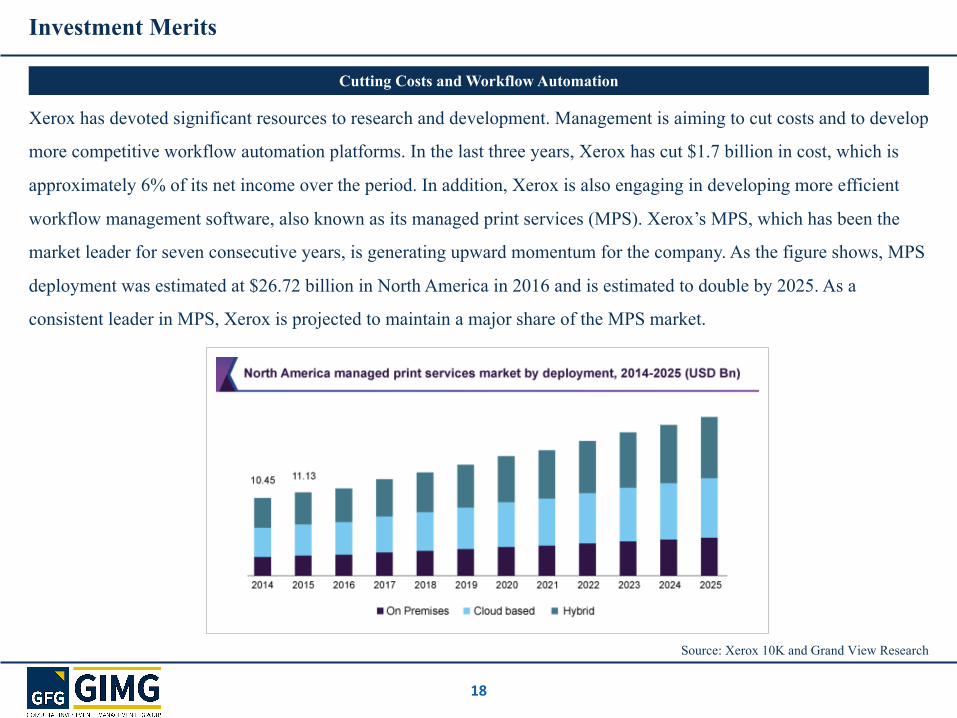

Investment Merits

Cutting Costs and Workflow Automation

Xerox has devoted significant resources to research and development. Management is aiming to cut costs and to develop

more competitive workflow automation platforms. In the last three years, Xerox has cut $1.7 billion in cost, which is

approximately 6% of its net income over the period. In addition, Xerox is also engaging in developing more efficient

workflow management software, also known as its managed print services (MPS). Xerox’s MPS, which has been the

market leader for seven consecutive years, is generating upward momentum for the company. As the figure shows, MPS

deployment was estimated at $26.72 billion in North America in 2016 and is estimated to double by 2025. As a

consistent leader in MPS, Xerox is projected to maintain a major share of the MPS market.

Source: Xerox 10K and Grand View Research

19

Investment Merits

Industry Leading Technology

Xerox leads the printing industry in terms of technology. One of its technological highlights is ConnectKey and

VersaLink technology, which integrate the cloud into printing and document services. This has provided Xerox with a

competitive edge when it comes to workflow efficiency, security and post sale services. In addition, Xerox has also

devoted its R&D to analyzing big data and providing more efficient workflow automations. This is being accomplished

by its subsidiary PARC, a prominent R&D center located in Silicon Valley. R&D expenses totaled $76in 2016 and $446

million in 2017.

Source: Xerox 10K and Grand View Research

20

Investment Merits

Industry Leading Technology

Compared to its competitors, Xerox has superiority in its software integrations, including the integration of big data,

cloud computing and advanced optimization strategies. This technological advantage is helping Xerox lead in workflow

solution services, namely managed print services (MPS) and other post-sales business. Although Xerox’s growth is

largely software driven, its patents are mostly hardware related. So, even though Xerox is the industry leader in

document services, there’s potential for someone to create their own, equally efficient MPS service. Xerox also benefits

from its customer relationship maintenance. Over the years, Xerox has broadened its customer relationship resources by

layering additional services.

The printing industry is declining and Xerox is facing many competitors, but its revenue is likely to sustain at the

current level due to its long term contracts with customers and its advantage in post sales services. In the long term,

however, as more competitors enter the shrinking market, Xerox needs to distinguish itself with cutting edge printing

technology or unique document services platforms.

Source: UBS

21

Investment Merits / Risks

Accelerated Productivity and Cost Initiatives Justify Icahn’s Desired M&A Share Price, but also hurt credit rating

Xerox’s top-line growth is virtually non-existent, as total 3Q revenue declined 5.8% year over year and post-sale

revenue fell 6.4%. However, free cash flow guidance for 2018 was increased to $900 million-$1 billion from $750-950

million. Revenue has declined by mid to low single digits over the past five years, while free cash flow has fallen by

more than 50%. During the Q3 earnings conference call, CEO John Visitein voiced his displeasure for these numbers.

Free cash flow guidance for 2018 increased due to productivity and cost saving initiatives such as “Project Own It”.

Started three years ago, the initiative focuses on getting profitable contracts rather than just the dollar volume. During

the first two years, the program delivered over $1.2 billion in gross productivity gains and cost savings. In 2018, we

expect approximately $475 million of additional cost reductions, which translates to approximately $1.7 billion in

savings over the three-year period. This outperforms the $1.5 billion target that was set three years ago. This Strategic

Transformation period incurred restructuring cash payments of $118 million in 2016 and $224 million in 2017 due to

employee severance and lease termination costs. On the whole, Xerox’s accelerated productivity and cost saving

initiatives have been effective.

Source: UBS & Morningstar Report, Bloomberg, XRX 10K

22

Investment Merits / Risks

Accelerated Productivity and Cost Initiatives Justify Icahn’s Desired M&A Share Price, but also hurt credit rating

Xerox plans to use free cash flow for share repurchases, as the board increased its 2018 share repurchase expectations to

$700 million from $500 million, highlighting shareholder returns as the highest priority. This is likely part of the

strategy that major shareholders, Carl Icahn and Darwin Deason, are implementing so that Xerox’s operating strategy

and assets are attractively positioned for a potential sale at a later date. Icahn and Deason are trying to justify the $40 per

share price that they have publicly voiced as the starting point for M&A negotiations.

Since Xerox is allocating the majority of its free cash flow towards shareholders, the company may require another debt

issuance as $950 million in bonds are due in 2019. At least 50% of 2018 free cash flow expectations of $900M - $1

billion will be returned to shareholders, decreasing cash available to reduce debt levels. Almost $1 billion annually will

mature over the next three years. Furthermore, credit and ratings risks are rising as there are concerns regarding secular

declines in Xerox’s core business, reduced diversification and less-conservative financial policies. Downgrade potential

over the next six months is high, which could significantly influence the company’s debt issuance.

Source: UBS, Morningstar, Bloomberg, Xerox 10K

23

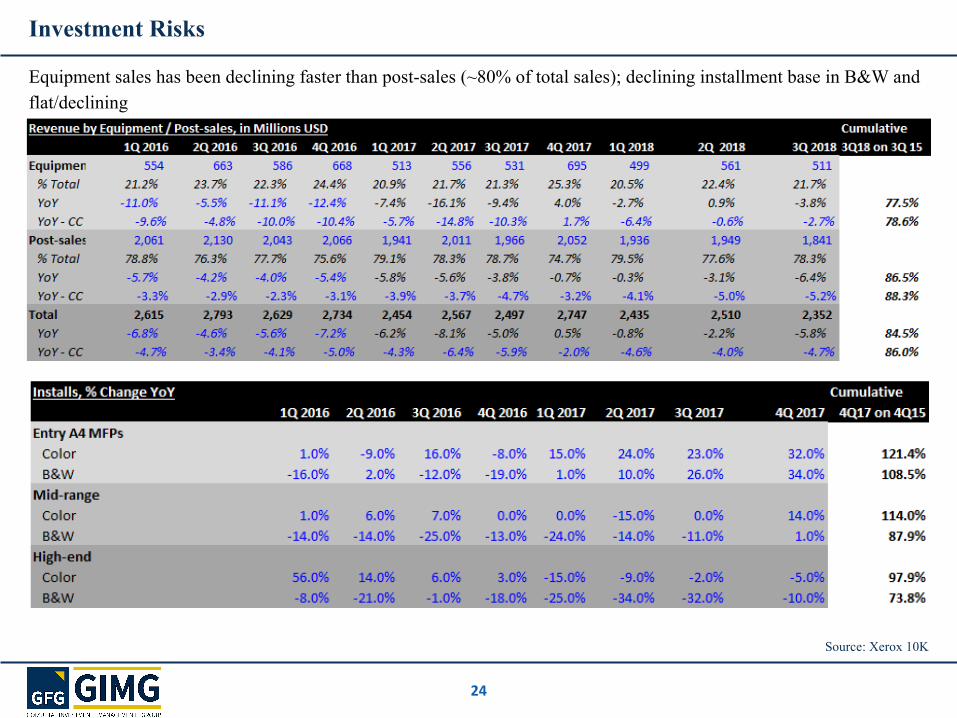

Investment Risks

We foresee post-sales declining (~80% of total)Decline in Post-Sales and Equipment Sales

Xerox’s sales are currently distributed as ~80% post-sales and ~20% equipment sales. Post-sales include document

services, equipment maintenance, consumable supplies, financing, and other elements. Per management, post-sales is a

function of print volume times installment base. Thus, post-sales growth will likely trail equipment sales & installment

base. Coupled with declining print volume, post-sales revenue will continue to struggle. Within equipment sales, high-

end equipment suffered the largest decline ~16% YoY 3Q18 through 3Q16. Although we do not have specific numbers,

it is safe to say high-end equipment sales generate the highest post-sales per unit due to higher maintenance costs,

higher demand for technical support and more advanced software. Declining high-end sales will impact post-sales.

The impact of installment on post-sale is delayed because customers may enter into contracts with Xerox for years at a

time. If Xerox fails to sell equipment to these customers, these contracts may not be renewed. This is evident in the poor

renewal rate and signing rates management reported. Renewal rates are 79% and 75% in 3Q18 and 2Q18, respectively,

far below the target 85% - 90% target set by management. New signings for 3Q18 and 2Q18 are 15% and 20%,

resulting in a total signing decline of 2.8% and 5%. Xerox is losing customers faster than it is acquiring new customers.

Fortunately for investors, the sales decline slowed down in 2018 for both equipment and post-sales.

Source: Earnings Call, Xerox 10Q

24

Investment Risks

Equipment sales has been declining faster than post-sales (~80% of total sales); declining installment base in B&W and flat/declining

Source: Xerox 10K

25

Investment Risks

Among equipment sales, high-end is suffering the largest decline

Source: Xerox 10K

26

Investment Risks

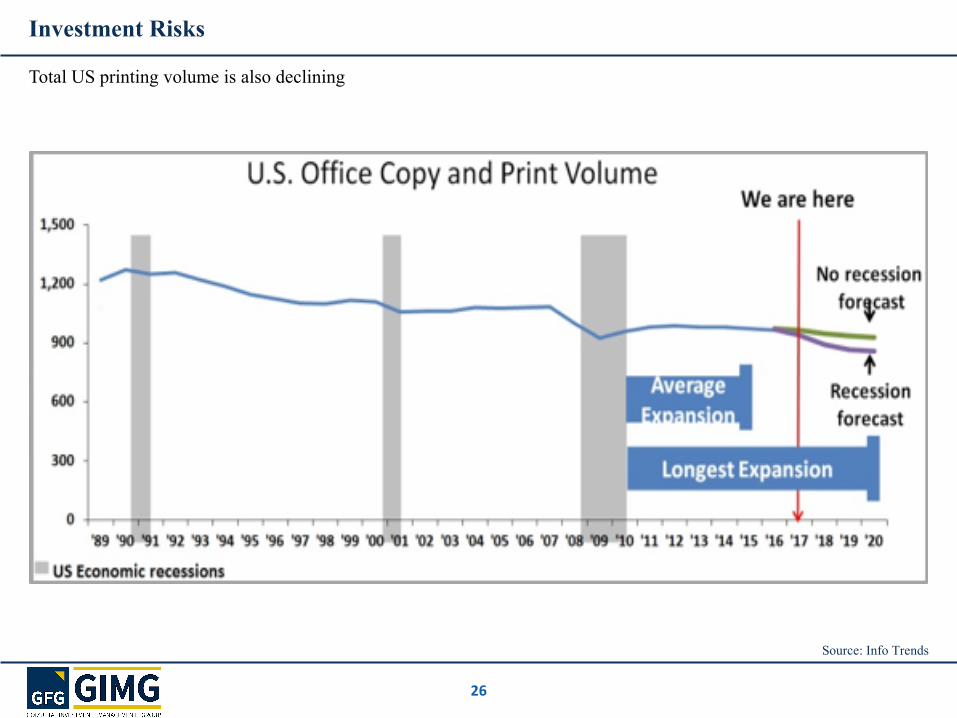

Total US printing volume is also declining

Source: Info Trends

27

Investment Risks

Company Growth Rates Slightly Trailing Industry Growth

As we already know, Xerox’s TTM earnings (from June 30, 2018) has more than halved from the same point in 2017.

Looking at growth on a sector-level, the US tech industry has grown by double digits (14.27%) in the last 12 months.

This shows that though the industry has profited from the recent economic uplift, Xerox hasn’t been able to gain

anything relative to similar companies. On a more precise level, the printing industry as a whole is trailing the tech

industry. Xerox’s revenue is in decline, as are major competitors’ Canon and Ricoh. Others, like Konica Minolta and

Fuji, have positive, but slowing revenue growth. The only clear frontrunner in the printing solutions industry is HP. It’s

important to note that the industry as a whole, and not just Xerox, is going through a rough patch. Thus, we know that

industry headwinds, not mismanagement, is the reason for declining revenue.

Xerox, unlike their competitors, is going through a major restructuring phase. Companies that are going through a major

reinvestment phase or transitional period nearly always experience diminished earnings. This reinvestment phase

demonstrates that Xerox is trying to reposition itself for success.

Source: FactSet and Bloomberg

28

Investment Risks

Potential Growth Markets are Limited due to Misallocation of R&D

In the past, Xerox allocated a significant amount of resources to its R&D. Since 2015, though, R&D spending has

decreased. In 2015, R&D spending totaled $511 million. In 2017, it fell to $446 million. Although R&D spending has

gradually decreased, Xerox squandered R&D funds before the Conduent spin off. Xerox primarily used R&D to focus

on expanding its services business, which is now under the new company. As a result, Xerox has neglected potential

market expansion sectors such as packaging. To catch competitors in the hardware business, Xerox is going to have to

delve into new R&D.

Furthermore, Xerox is trying to target growth markets such as Entry A4 MFPS and small/medium business (SMB)

managed print services. These areas are already dominated by competitors such as HP, Ricoh, Canon, and others. Rather

than trying to expand into a new market, Xerox should actually allocate R&D funds to its leading market segment: A3

and other large scale printers. The HP-Samsung merger provided HP with a lot of valuable IP and provides HP with the

capability to mass produce an A3 printer at a $6-9k price point, which is $10k cheaper than Xerox’s current signature A3

printer. Xerox could lose a significant market share to HP in its market leading segment.

Source: Xerox 10K, UBS and Morningstar

29

Investment Risks

Xerox Strategy in Low End Market

Xerox’s strategy is to increase Small and Mid-sized (SMB) coverage through resellers and partners (including multi-

brand dealers) and continued distribution acquisitions. In 2017, Xerox acquired MT Business Technologies, Inc. (MT

Business), an Ohio-based multi-brand dealer, and two smaller multi-brand dealers in Iowa and North and South

Carolina. MT Business provides printing equipment and services to organizations throughout Ohio and southeastern

Michigan. The lower-end market for printers is a price-sensitive and commoditized market. Since 2007, print spending

by enterprises has decreased by 2-3% per year due to declining pages and customer cost controls. Gartner predicts 3%

declines through 2021. Consumables, which represent the majority of profits, are forecasted to decline 4-5%.

Due to commoditization, xxperts view products like Xerox’s ConnectKey as an unattractive feature to customers; apps

are not necessary when it comes to printing.

Managed Print Services (MPS) for SMBs generally works best when administered by multi-brand dealers. Xerox has

little presence in multi-brand dealer channels because of the company’s reliance on direct sales and dedicated Xerox

dealers. Building a channel takes time so competitors remain ahead in the market. Xerox is also not entering the market

with distinguishable/competitive products or prices. Entry A4 may also come at the expense of A3 ($10-20k) if

businesses decide to cut down on costs and purchase multiple A4 printers ($1k) for less instead of one A3, causing a net

decrease in print spend.Source: Xerox 10K and UBS

30

Investment Risks

Refinancing Risk

Xerox has 4,670M of debt (excl. the loan which is a revolver and currently undrawn) and thus has large refinancing

needs. Xerox was lowered to junk status in August by Fitch as a result of challenging fundamentals (shriveling revenue)

and capital allocation strategy (prioritizing on shareholder return by stock repurchase). This poses a challenge to

refinancing needs. Moreover, Xerox just increased their share repurchase plan to $700M from $500M after they updated

their 2018 free cash flow guidance. This increase in share repurchase is to some extent a result of pressure from activist

shareholder Carl Icahn.

Management has listed maintaining investment grade status as their top capital allocation strategy. Creditors are worried

by management’s decision to increase the dollar amount on the share repurchase program. This is a signal that they are

confident that they can refinance their debt. No responsible management team would repurchase shares at the cost of

defaulting on debt. If the new management team can achieve some success with its turnaround plan, it will help restore

investor’s confidence in the company. With two activist hedge fund investors taking control and the CEO in place who

is well connected to the big PE firm Apollo, they have better access to capital markets and should be better positioned to

refinance their debt.

Source: Bloomberg

31

Investment Risks

Government Contracts

Recent legal drama that surrounding Xerox poses a severe risk to the company. As the market for large-scale printers is

shrinking, Xerox relies heavily on existing long-term government contracts for a steady stream of revenue. The forward

looking statement and risk factor sections in the 10K, however, both emphasize the potential threat of terminating

contracts. If governments decide that Xerox has become unreliable due to the bad publicity generated by the recent

FujiFilm merger back out, contracts may be terminated. This would significantly hurt Xerox’s already shrinking

revenue. In addition, negative publicity could also hamper Xerox’s ability to compete for future contracts. Currently,

total finance receivables from government contracts is approximately $700 million.

Furthermore, volatility in government budgets and spending, including deficits, could substantially alter and lower

government sales and limited projects in the future.

Source: Xerox 10K

Financial Model and Analysis

33

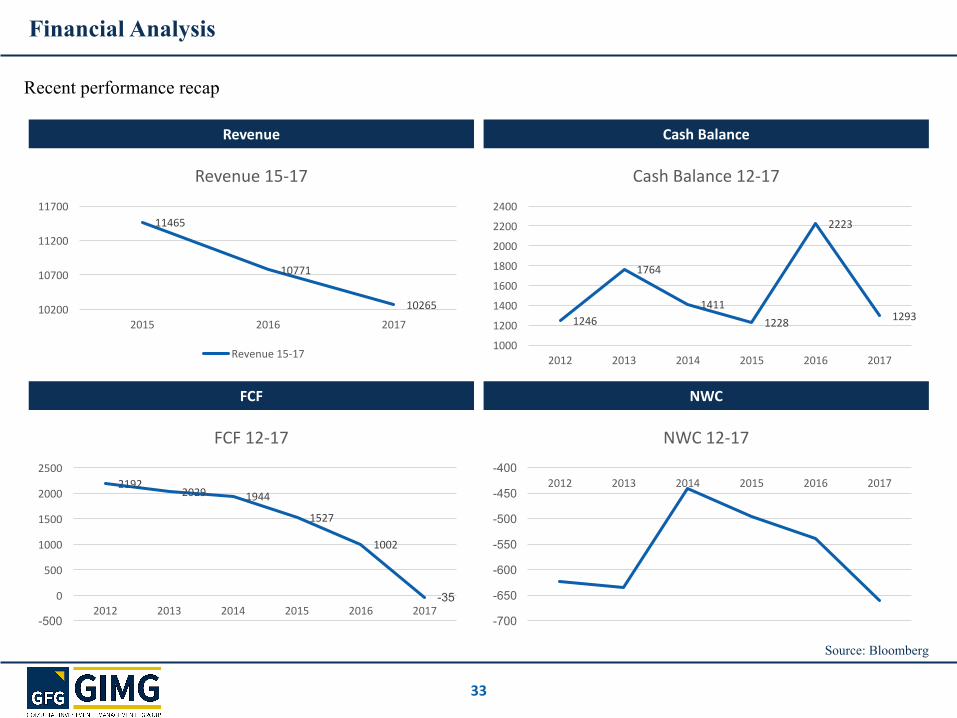

Financial Analysis

Recent performance recap

Revenue CashBalance

FCF NWC

Source: Bloomberg

11465

10771

1026510200

10700

11200

11700

2015 2016 2017

Revenue15-17

Revenue15-17

1246

1764

14111228

2223

1293

1000

1200

1400

1600

1800

2000

2200

2400

2012 2013 2014 2015 2016 2017

CashBalance12-17

21922029 1944

1527

1002

-35

-500

0

500

1000

1500

2000

2500

2012 2013 2014 2015 2016 2017

FCF12-17

-700

-650

-600

-550

-500

-450

-4002012 2013 2014 2015 2016 2017

NWC12-17

34

Financial Analysis

FCF bridge and summary of key margins

Source: Xerox 10K

35

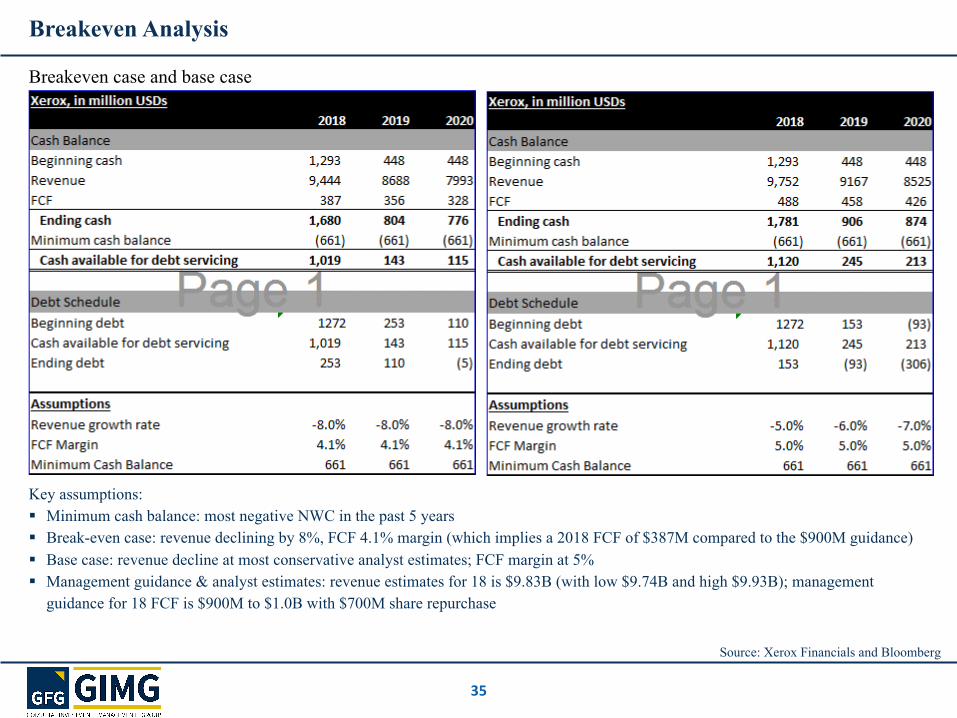

Breakeven Analysis

Breakeven case and base case

Xerox’sfinancials,Bloomberg

Key assumptions:§ Minimum cash balance: most negative NWC in the past 5 years§ Break-even case: revenue declining by 8%, FCF 4.1% margin (which implies a 2018 FCF of $387M compared to the $900M guidance)§ Base case: revenue decline at most conservative analyst estimates; FCF margin at 5%§ Management guidance & analyst estimates: revenue estimates for 18 is $9.83B (with low $9.74B and high $9.93B); management

guidance for 18 FCF is $900M to $1.0B with $700M share repurchase

Source: Xerox Financials and Bloomberg

36

Financial Analysis - Appendix

Source: Xerox Quarterly Reports

Security Analysis

38

Investment Merits and Risks

Xerox Debt Repayment Schedule

Source: Bloomberg

39

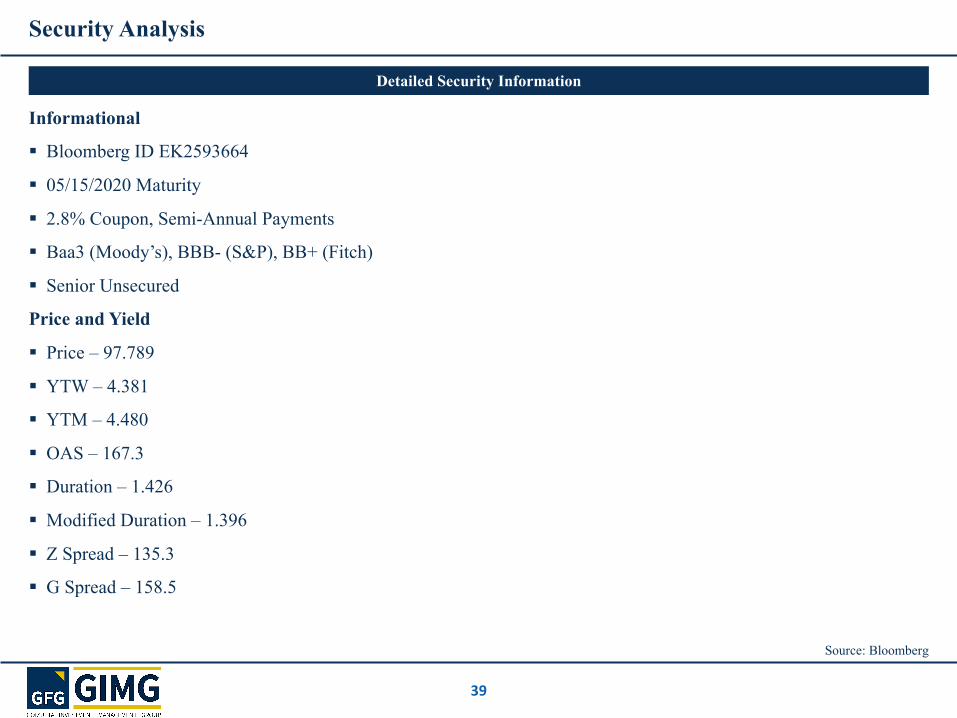

Security Analysis

Detailed Security Information

Informational

§ Bloomberg ID EK2593664

§ 05/15/2020 Maturity

§ 2.8% Coupon, Semi-Annual Payments

§ Baa3 (Moody’s), BBB- (S&P), BB+ (Fitch)

§ Senior Unsecured

Price and Yield

§ Price – 97.789

§ YTW – 4.381

§ YTM – 4.480

§ OAS – 167.3

§ Duration – 1.426

§ Modified Duration – 1.396

§ Z Spread – 135.3

§ G Spread – 158.5

Source: Bloomberg

40

Security Analysis

ComparableSecurities

§ Nocomparablesecuritiesbecausetheircompetitorsareeither10xmorelargerormuchlessleveraged.However,ourbondhasveryattractivereturnsothekeyofthispitchistohaveadeepdiveatthecreditrisk.

41

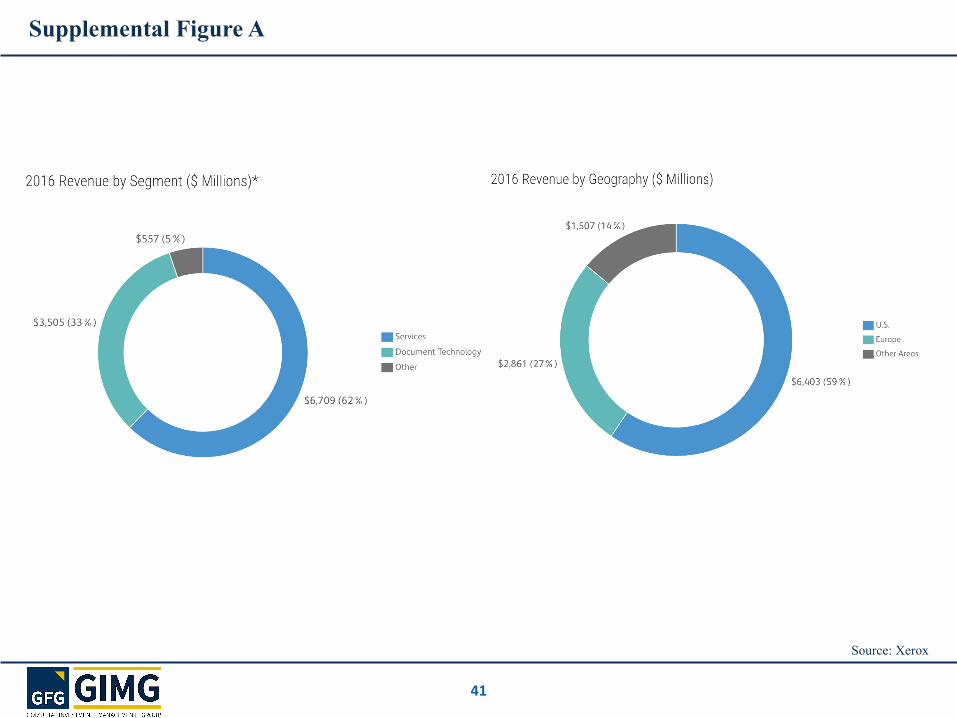

Supplemental Figure A

Source: Xerox

42

Supplemental Figure B

XRX Total R&D Spending (in millions)

Source: Xerox 10K

Disclaimer: These materials has been prepared by the Goizueta Investment Management Group. This document is for information and illustrative purposes only and does not purport to showactual results. It is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are currentopinions as of the date appearing in this material only and are subject to change without notice. Reasonable people may disagree about the opinions expressed herein. In the event any of theassumptions used herein do not prove to be true, results are likely to vary substantially. All investments entail risks. There is no guarantee that investment strategies will achieve the desiredresults under all market conditions and each investor should evaluate its ability to invest for a long term especially during periods of a market downturn. No representation is being made that anyaccount, product, or strategy will or is likely to achieve profits, losses, or results similar to those discussed, if any. No part of this document may be reproduced in any manner, in whole or in part,without the prior written permission of the Goizueta Investment Management Group, other than to your employees. This information is provided with the understanding that with respect to thematerial provided herein, that you will make your own independent decision with respect to any course of action in connection herewith and as to whether such course of action is appropriate orproper based on your own judgment, and that you are capable of understanding and assessing the merits of a course of action. The Goizueta Investment Management Group does not purport toand does not, in any fashion, provide broker/dealer, consulting or any related services. You may not rely on the statements contained herein. The Goizueta Investment Management Group shallnot have any liability for any damages of any kind whatsoever relating to this material. You should consult your advisors with respect to these areas. By accepting this material, you acknowledge,understand and accept the foregoing. © 2015 Goizueta Investment Management Group. All Rights Reserved.