www.randstadholding.com analyst day, london london may 16, 2003

TRANSCRIPT

www.randstadholding.com

Analyst day, LondonAnalyst day, London

London

May 16, 2003

WelcomeWelcome

Program aimed at providing better

insight into Randstad concepts

Zoom into developments in the UK and

North America

In-depth look at tax structure

ProgramProgram

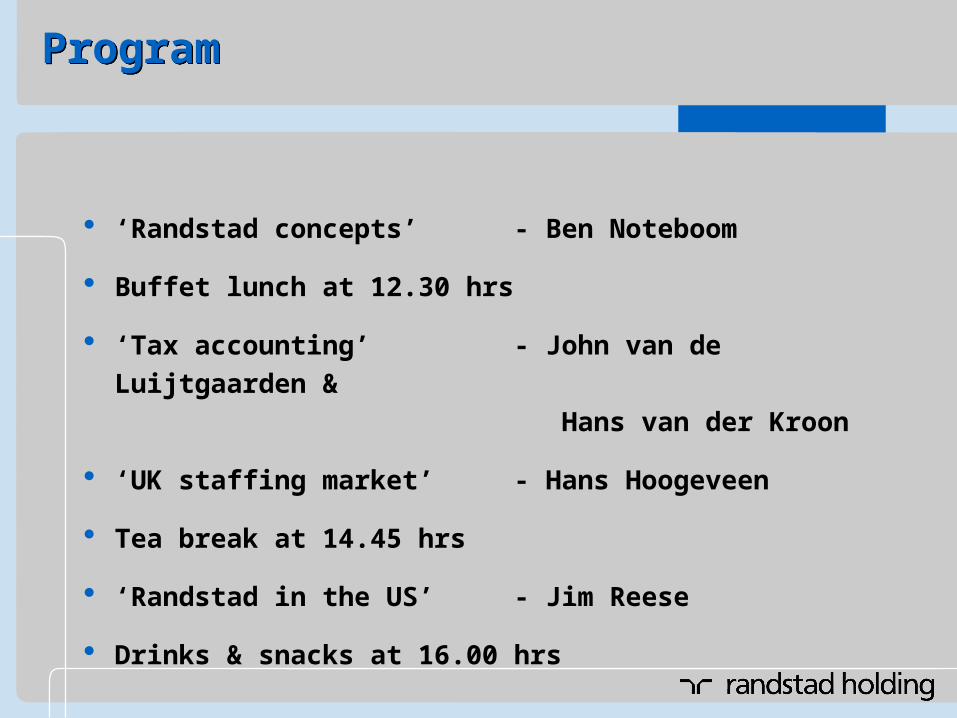

‘Randstad concepts’ - Ben Noteboom

Buffet lunch at 12.30 hrs

‘Tax accounting’ - John van de Luijtgaarden &

Hans van der Kroon

‘UK staffing market’ - Hans Hoogeveen

Tea break at 14.45 hrs

‘Randstad in the US’ - Jim Reese

Drinks & snacks at 16.00 hrs

Ben Noteboom

Chairman of the Executive Board and CEO

Randstad conceptsRandstad concepts

Building blocks and organic growth model

Strong concepts

- Mass-customized and specialties

- In-house services

- Yacht

Market and margin development in the Netherlands

AgendaAgendaAgendaAgenda

Building blocksBuilding blocksBuilding blocksBuilding blocks

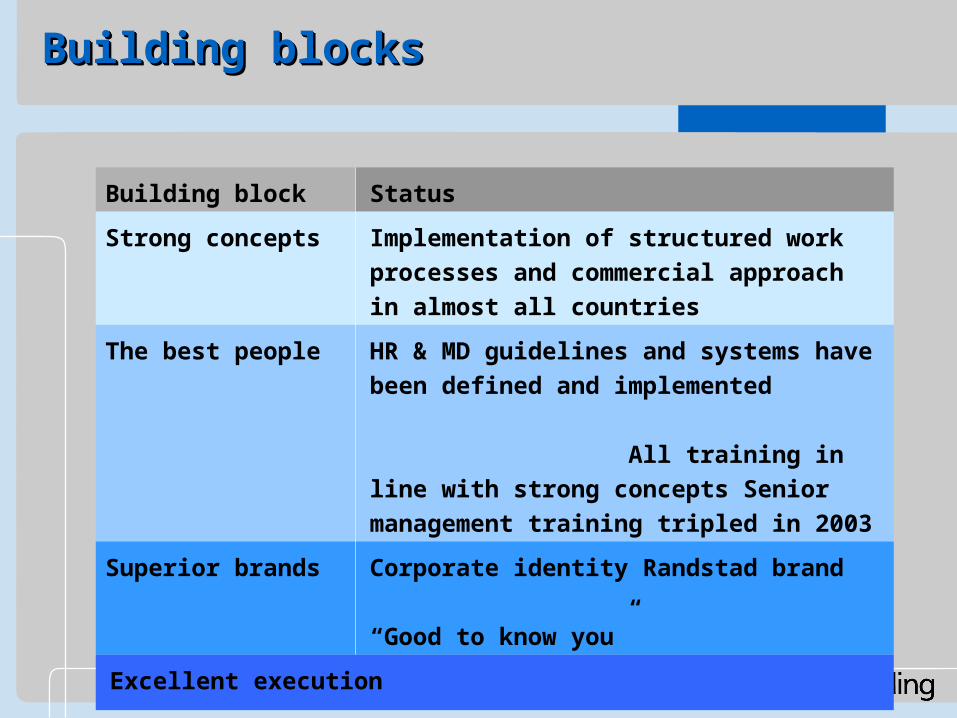

Building block Status

Strong concepts Implementation of structured work

processes and commercial approach in

almost all countries

The best people HR & MD guidelines and systems have been

defined and implemented

All training in line with

strong concepts Senior management

training tripled in 2003

Superior brands Corporate identity Randstad brand

“Good to know you”

Excellent execution

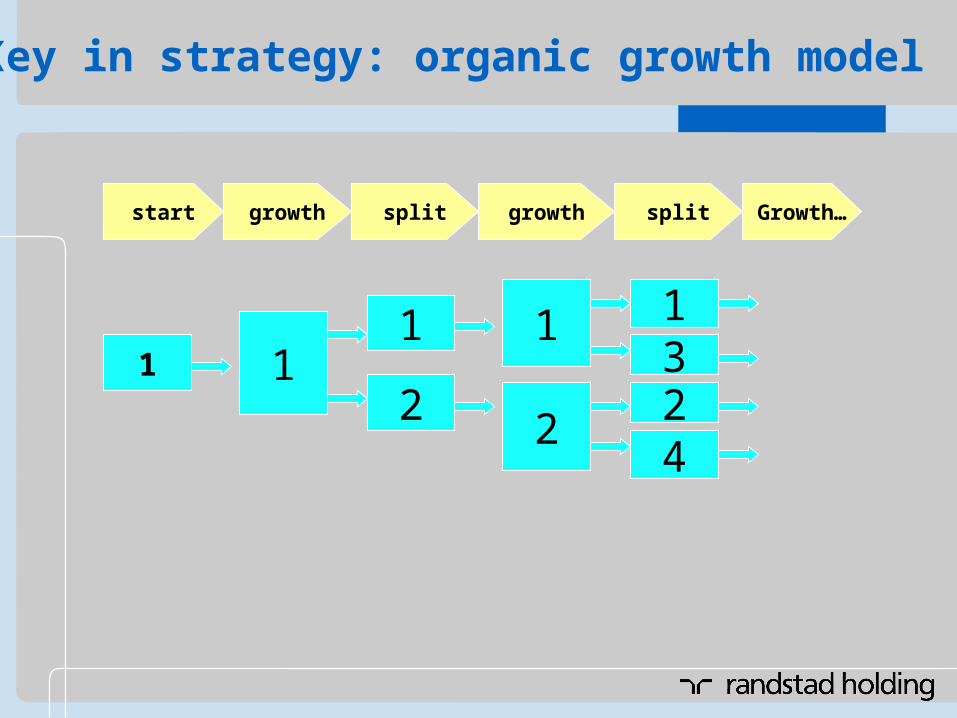

1 11

24231

2

1

growth split growth split Growth…start

Key in strategy: organic growth model

Strong concepts: mass-customizedStrong concepts: mass-customized

Branded as Randstad and Tempo-Team

Offers a total package including general administrative,

industrial, production

Specialties designed for specific sectors or groups of

flexworkers

Specialties in mass-customized: 2-way approach in definitionSpecialties in mass-customized: 2-way approach in definition

1. Target business/sector

- Call centers, healthcare, transport services, outplacement,

outsourcing etc.

2. Flexworker

Secretaries, IT, young professionals, logistics, education,

etc.

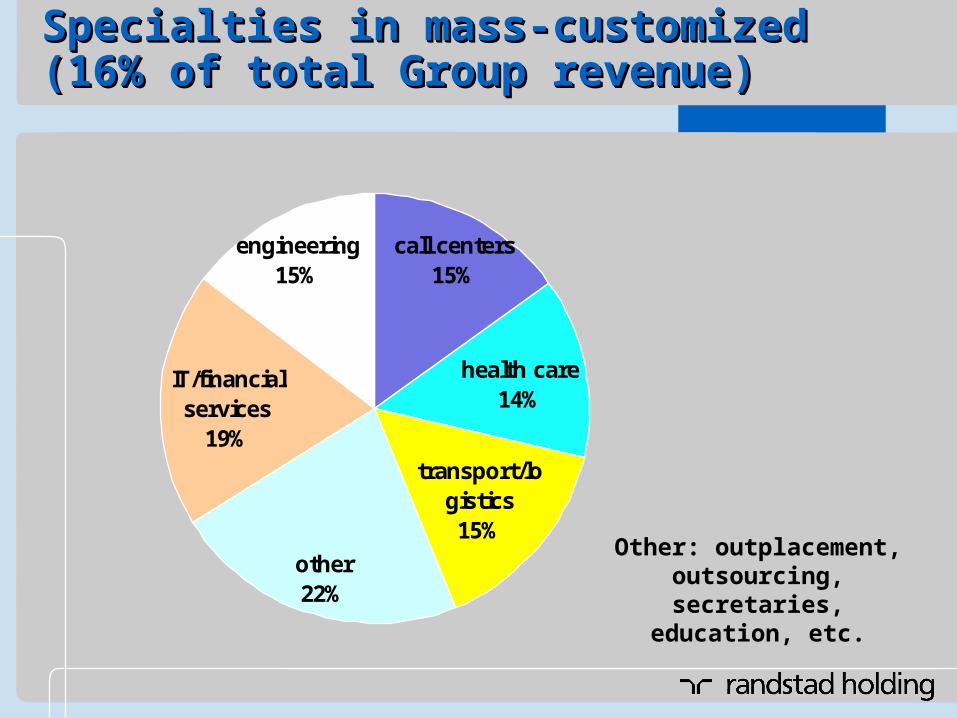

Specialties in mass-customized Specialties in mass-customized (16% of total Group revenue)(16% of total Group revenue)Specialties in mass-customized Specialties in mass-customized (16% of total Group revenue)(16% of total Group revenue)

call centers15%

health care14%

transport/logistics15%

other22%

IT/financial services

19%

engineering15%

Other: outplacement, outsourcing, secretaries,

education, etc.

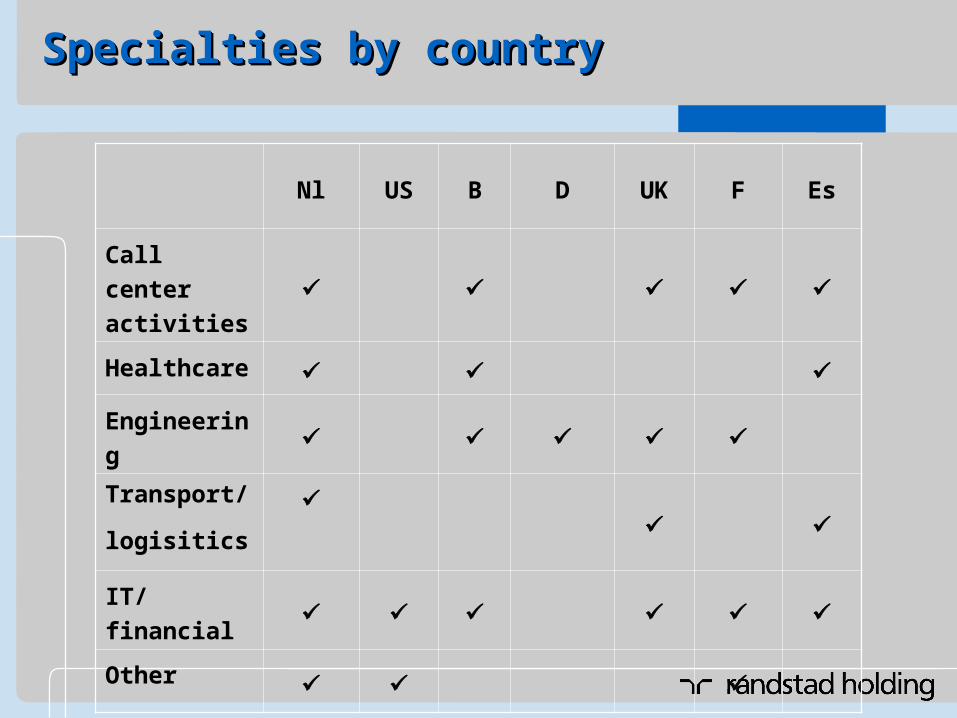

Specialties by country Specialties by country Specialties by country Specialties by country

Nl US B D UK F Es

Call center

activities

Healthcare

Engineering

Transport/

logisitics

IT/financial

Other

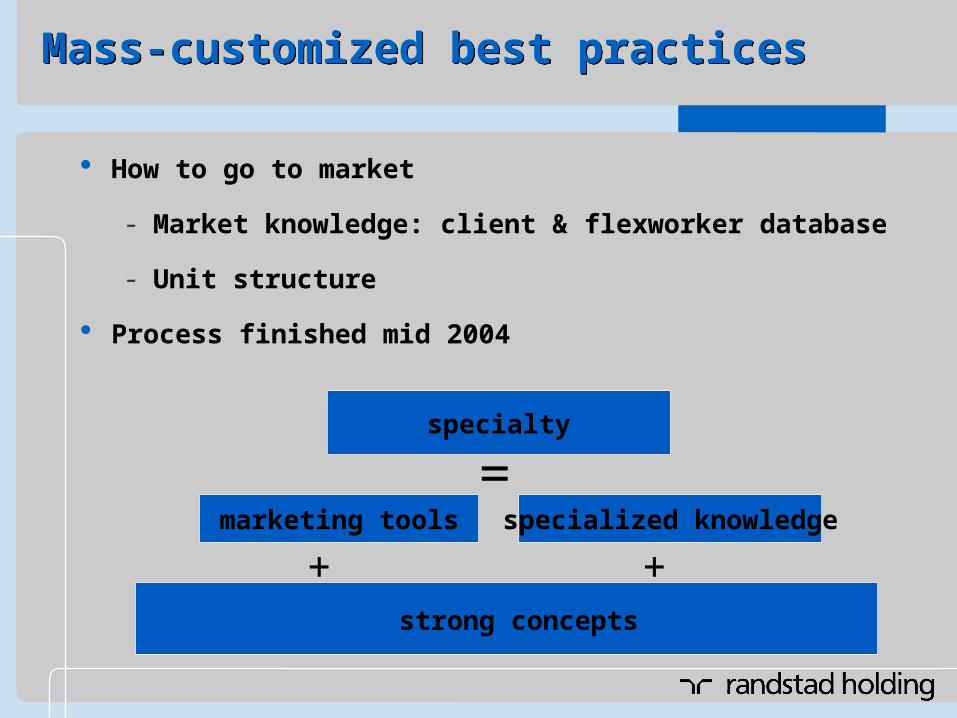

Mass-customized best practicesMass-customized best practices

How to go to market

- Market knowledge: client & flexworker database

- Unit structure

Process finished mid 2004

marketing tools specialized knowledge

strong concepts

specialty

+ +

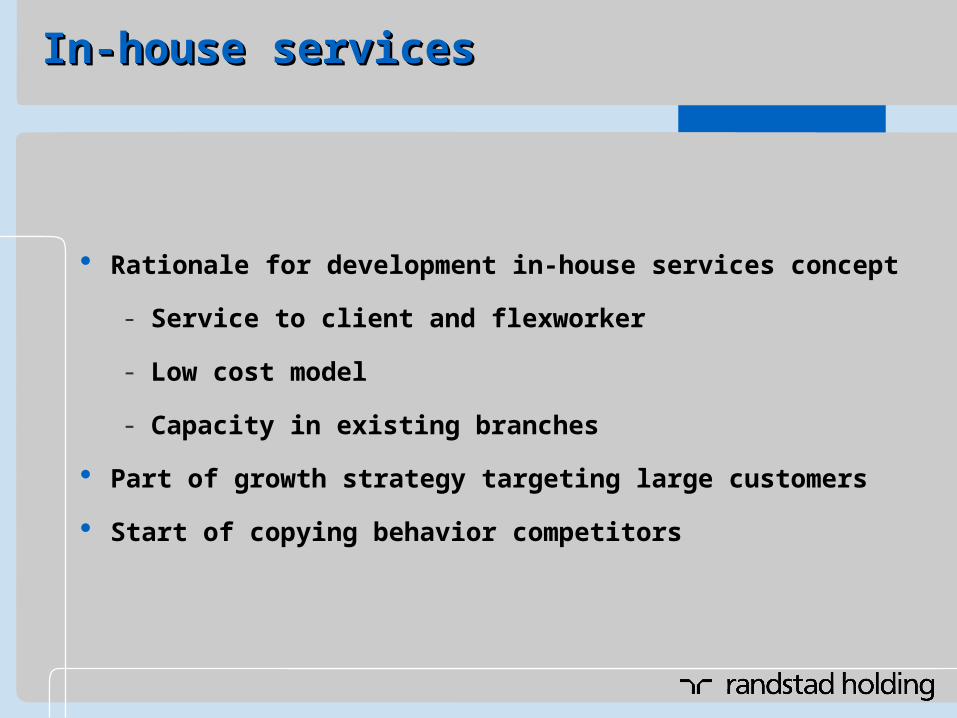

Rationale for development in-house services concept

- Service to client and flexworker

- Low cost model

- Capacity in existing branches

Part of growth strategy targeting large customers

Start of copying behavior competitors

In-house servicesIn-house servicesIn-house servicesIn-house services

Capac videoCapac videoCapac videoCapac video

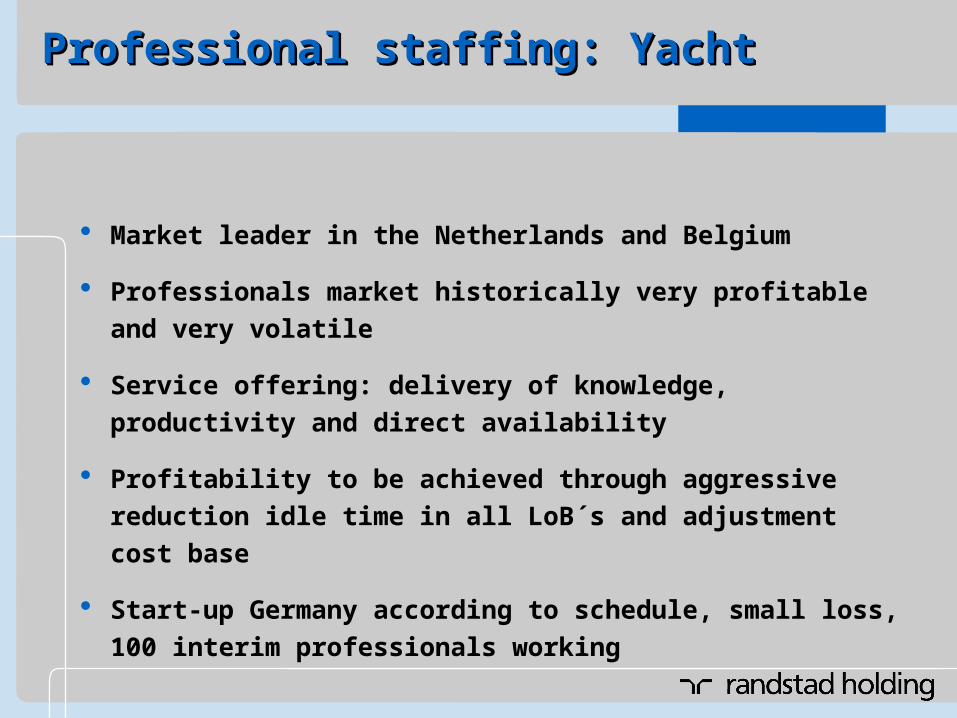

Market leader in the Netherlands and Belgium

Professionals market historically very profitable and very

volatile

Service offering: delivery of knowledge, productivity and direct

availability

Profitability to be achieved through aggressive reduction idle

time in all LoB´s and adjustment cost base

Start-up Germany according to schedule, small loss, 100

interim professionals working

Professional staffing: YachtProfessional staffing: YachtProfessional staffing: YachtProfessional staffing: Yacht

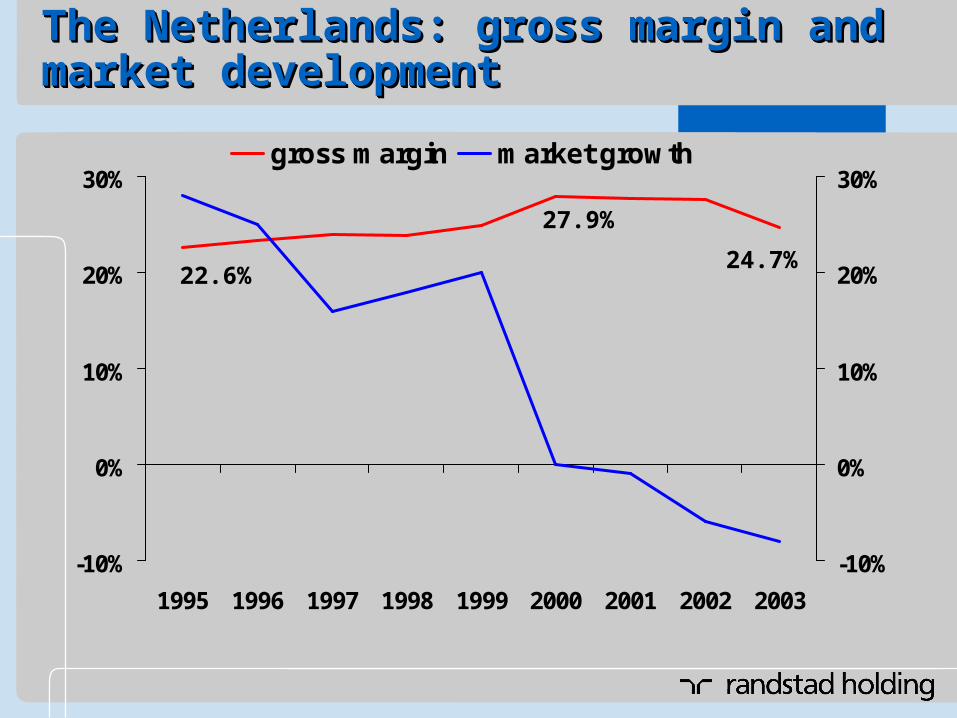

The Netherlands: gross margin and market The Netherlands: gross margin and market developmentdevelopmentThe Netherlands: gross margin and market The Netherlands: gross margin and market developmentdevelopment

-10%

0%

10%

20%

30%

1995 1996 1997 1998 1999 2000 2001 2002 2003

-10%

0%

10%

20%

30%gross margin market growth

22.6%24.7%

27.9%

> 1200 new staffing companies since abolishment license system

Non-associated companies have taken market share

Market data “Flexmarkt”: smaller companies disappearing

2 factors behind decline in market

- Scarcity on labor market

- Price elasticity

Larger companies organize their own flexibility

Changed market structure in the Changed market structure in the NetherlandsNetherlandsChanged market structure in the Changed market structure in the NetherlandsNetherlands

3 components in cost price flexworker

- Pay rate

- Social security

- Margin

No price war: Randstad as market leader always involved in tenders

Decline in market causes erratic price behavior by competition

Importance of market share gain biggest in declining market

Price elasticityPrice elasticityPrice elasticityPrice elasticity

New decline in market was largely unexpected

Identifying cost saving opportunities

Maintain external focus

Maintain branch network

The Netherlands: optimizing unit structure through unit clustering

IT costs

Further adjustments to cost base in Germany and North America

Cost base adjustmentsCost base adjustmentsCost base adjustmentsCost base adjustments

Thank you!

Any questions?

Thank you!

Any questions?

John van de Luijtgaarden

Managing director corporate accounting

& tax affairs

Hans van der Kroon

Head of corporate tax department

Tax accounting & IFRSTax accounting & IFRS

Tax aspects of group structure

Presentation in annual report

Short introduction of IFRS issues

AgendaAgenda

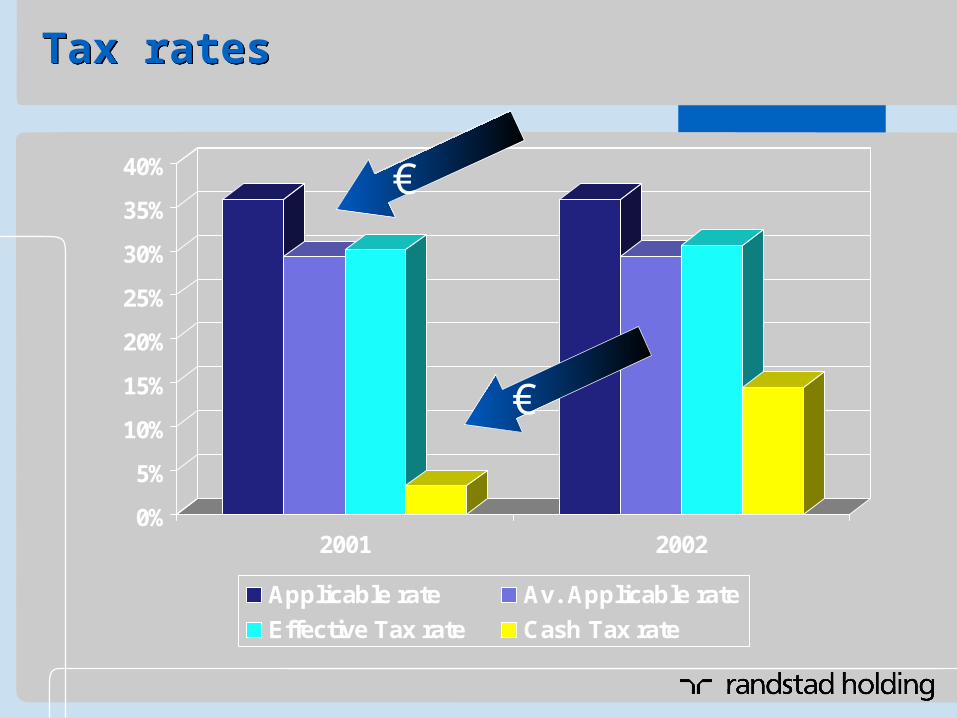

Tax ratesTax rates

0%

5%

10%

15%

20%

25%

30%

35%

40%

2001 2002

Applicable rate Av. Applicable rate

Effective Tax rate Cash Tax rate

€

€

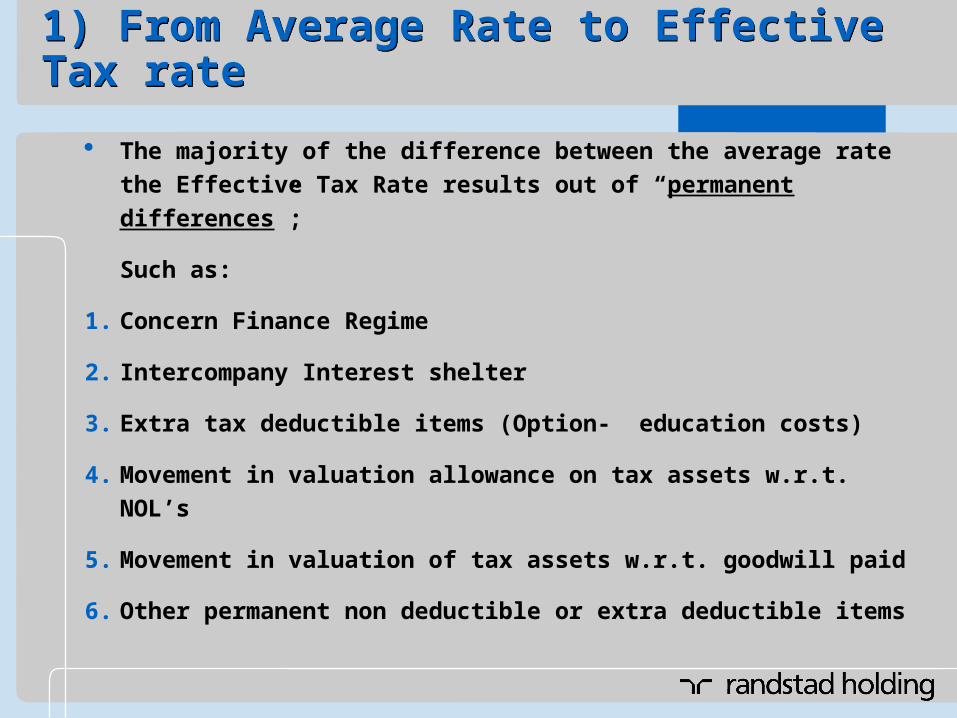

1) From Average Rate to Effective Tax rate1) From Average Rate to Effective Tax rate

The majority of the difference between the average rate the

Effective Tax Rate results out of “permanent differences”;

Such as:

1. Concern Finance Regime

2. Intercompany Interest shelter

3. Extra tax deductible items (Option- education costs)

4. Movement in valuation allowance on tax assets w.r.t. NOL’s

5. Movement in valuation of tax assets w.r.t. goodwill paid

6. Other permanent non deductible or extra deductible items

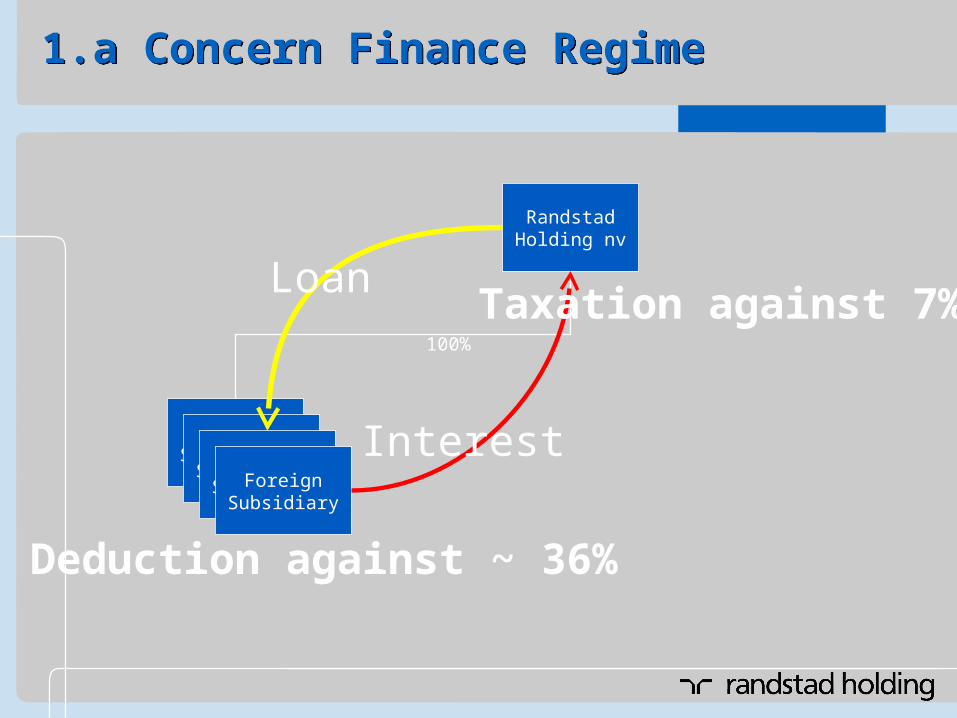

1.a Concern Finance Regime1.a Concern Finance Regime

RandstadHolding nv

ForeignSubsidiaryForeign

SubsidiaryForeignSubsidiaryForeign

Subsidiary

100%

Loan

Interest

Deduction against ~ 36%

Taxation against 7%

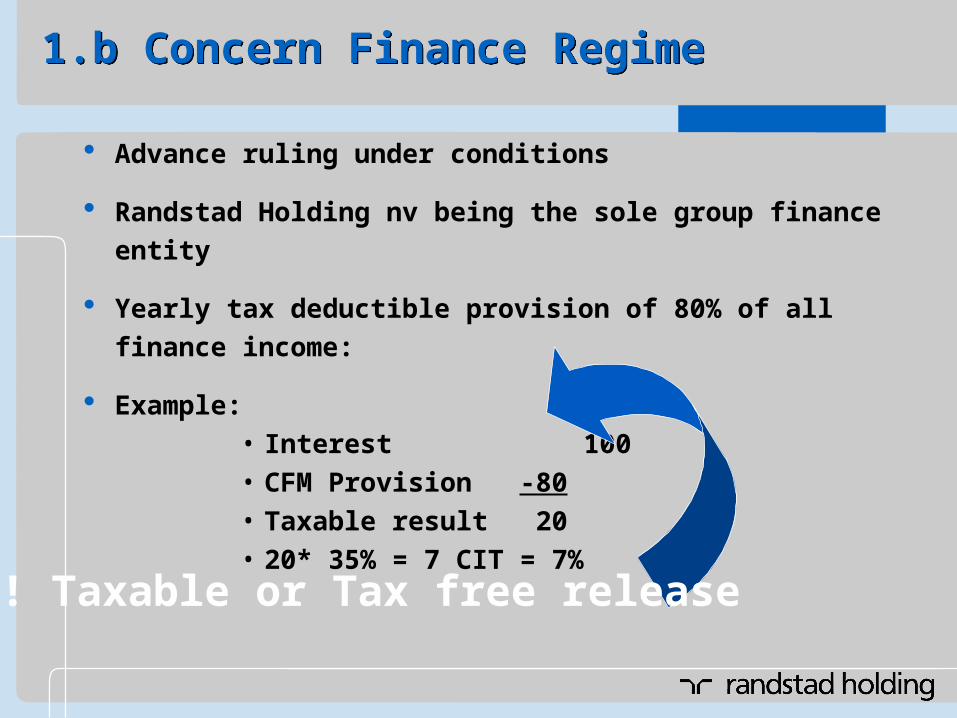

1.b Concern Finance Regime1.b Concern Finance Regime

Advance ruling under conditions

Randstad Holding nv being the sole group finance entity

Yearly tax deductible provision of 80% of all finance income:

Example:• Interest 100 • CFM Provision -80• Taxable result 20 • 20* 35% = 7 CIT = 7%

! Taxable or Tax free release

1.c Intercompany interest shelter1.c Intercompany interest shelter

RandstadHolding nv

ForeignSubsidiaryForeign

SubsidiaryForeignSubsidiaryForeign

Subsidiary

100%

RandstadHolding

Nederland bv

RandstadNorth America

LP

RandstadDeutschland

KG

LoanInterest

US Tax deduction

No Dutch taxation

1.d Tax assets w.r.t NOL’s & Goodwill1.d Tax assets w.r.t NOL’s & Goodwill

In various countries group companies are generating taxable

losses (also due to goodwill amortization and interest

deduction). Most of the countries do provide for a so called

carry forward of those losses to the future to be offset against

future profits (some countries even a carry back).

This future setting off of losses is reflected in the annual

account as an asset.

Upon acquisition of some companies in the past goodwill paid

has been made tax amortizable but for accounting purposes

this goodwill amount has been deducted from equity.

The future tax amortization has been booked as an asset in the

annual account.

2) From Effective tax rate to cash tax rate2) From Effective tax rate to cash tax rate

The majority of the difference between the Effective tax rate

and the cash tax rate comes from “timing differences”;

Note that they do not influence the P&L but only have an effect

on the balance sheet.

Most important beneficial timing difference comes from the

fact that our German and US Randstad activities are structured

in form of so called transparent entities (KG & Lp).

The taxable results of both the LP and the KG after tax

amortization of goodwill paid upon acquisition (which is

negative) is deducted from Dutch profits.

2.a. US and German transparent structure2.a. US and German transparent structure

RandstadHolding nv

ForeignSubsidiaryForeign

SubsidiaryForeignSubsidiaryForeign

Subsidiary

100%

RandstadHolding

Nederland bv

RandstadNorth America

LP

RandstadDeutschland

KG

Tax losses including to goodwill amortization -/-

Taxable profits from Dutch operations +/+

Cnt’d: From Effective tax rate to cash tax rateCnt’d: From Effective tax rate to cash tax rate

As mentioned: Taxable results Germany and USA after tax

amortization of goodwill are deducted from Dutch profits.

This results in a zero current tax payable for the fiscal unity of

Randstad Holding Nederland bv

BUT: For the cumulative amount of tax losses deducted no

future relief for double taxation will be granted for future

profits i.e. any € corporate income tax not paid now will have to

be paid “back” if and to the extent both Germany and North

America do generate a taxable profit. This is called a

“recapture obligation”.

Given the big amounts involved and the timing this is a huge

value driver!

Tax assetsTax assets

Consist of:

1. Deferred tax asset (DTA) w.r.t. Net Operating Losses

2. Deferred tax asset on Goodwill charged to equity (up to 2000)

3. Deferred tax assets on other timing differences

Total book value 2002: € 353 million

Valuation Valuation

Valuation allowance as per ultimo 2002:

1. DTA on Goodwill: At acquisition a valuation allowance was made with a view to the long amortization period for tax purposes (being 15 years in Germany and the USA).

2. DTA Net Operating Losses: prudent valuation, based on annual estimation of future taxable results over a reasonable period

Up to 2002 this resulted in:

Partial release of valuation allowance on DTA w.r.t. Goodwill;

Additions to valuation allowance on DTA w.r.t. NOL’s

Tax liabilitiesTax liabilities

The provision for Deferred Tax Liabilities consists mainly of

so called “recapture obligations”, which are the result of

German and USA tax losses being set off against Dutch

taxable profits;

Note: this structure does not hit taxes in the P&L but is “only”

a cash item.

1. In present: leads to a reduction of the tax cash out.

2. In future: depending on development of taxable profits

in Germany and USA the tax cash out will rise.

Effective tax rate 2002Effective tax rate 2002

Effective tax rate 2002 30.2%

Average applicable rate 29.2%

Permanent Differences (tax exempt) -22.7%

Changes in valuation of tax losses 34.6%

Release of val. all. On DTA wrt Goodwill -17.8%

Non-deductible items 6.6%

Total 30.2%

IFRS implementationIFRS implementation

Randstad has to apply IFRS as from 2005

Starting with the first quarterly report 2005

Comparative figures 2004 must be “comparable”

Material effects of differences between present GAAP and IFRS on equity and P&L to be communicated with interim results 2004

A number of changes of international standards and interpretations are pending or still expected between today and early 2004. These changes will effect final transition.

IFRS implementationIFRS implementation

Main issues identified:

- Goodwill of acquisitions prior to 2001 (charged to equity by

Randstad)

- Pension plans

- Stock options

- Preferred shares and dividend

A number of not or less material items

Thank you!

Any questions?

Thank you!

Any questions?

The UK staffing marketThe UK staffing market

Hans Hoogeveen

Managing director Randstad UK

UK marketUK market

Market volume: € 30.8 billion

92% temporary business, 8% permanent business

>3% penetration

Market mature but unprofessional

Fragmented market: 85% of companies independent

Top 10 players only 36% market share

Image flexwork and flexworker very low

UK flexible labor market increasingly driven by EU labor legislation

History of Randstad UKHistory of Randstad UK

Established in the UK in 1989

1999: 18 branches and £ 18 million turnover

2001: 36 branches and £ 34.5 million turnover

2001: acquisition of Securicor Recruitment Services

2002: over 85 branches and £ 104 million turnover

Top 25 recruitment company

StrategyStrategy

Local market leader

International expertise for local markets

Labor market specialist, opinion leader

Build long term client relationship

Attractive employer for flexworkers and corporate staff

Employment legislation opportunity to add value to our clients and flexworkers

Quality player

Randstad Inhouse Services in the UKRandstad Inhouse Services in the UK

2000: introduction of Randstad Inhouse Services

2002: Randstad Inhouse Services 21 branches

Focus on industrial areas in the North West, Midlands and

South

Yacht in the UKYacht in the UK

Restart in the UK in 2003

Solely focused on attracting engineers in the utilities and

infrastructure sectors

Concentrating on clients in North West, North East and

West Midlands

Superior BrandSuperior Brand

Implementation of corporate identity with tag line ‘good to

know you’ completed

Cardiff branch pilot for new branch corporate identity

Strong concepts in the UKStrong concepts in the UK

Randstad mass-customized

Callflex

Driving

Permanent

Randstad Inhouse Services

Yacht

Best people: our consultantsBest people: our consultants

Staff is key component in the building blocks upon which

Randstad is developing

No commission

One-stop-shop: consultants are responsible for the full

selection process: sell Randstad to client and deal with

searching and matching

Zero to hero programme

Investors in People

Excellent executionExcellent execution

The way we work: standardization of work processes

Workpocket

Flexworker Charter

Labor market survey

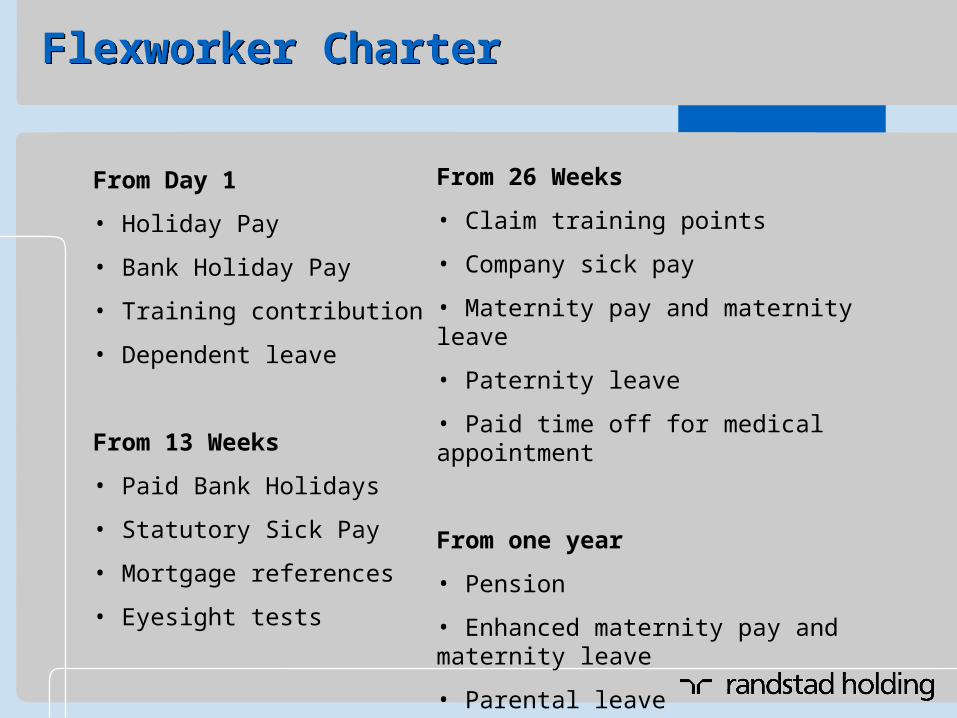

Flexworker CharterFlexworker Charter

From Day 1

• Holiday Pay

• Bank Holiday Pay

• Training contribution

• Dependent leave

From 13 Weeks

• Paid Bank Holidays

• Statutory Sick Pay

• Mortgage references

• Eyesight tests

From 26 Weeks

• Claim training points

• Company sick pay

• Maternity pay and maternity leave

• Paternity leave

• Paid time off for medical appointment

From one year

• Pension

• Enhanced maternity pay and maternity leave

• Parental leave

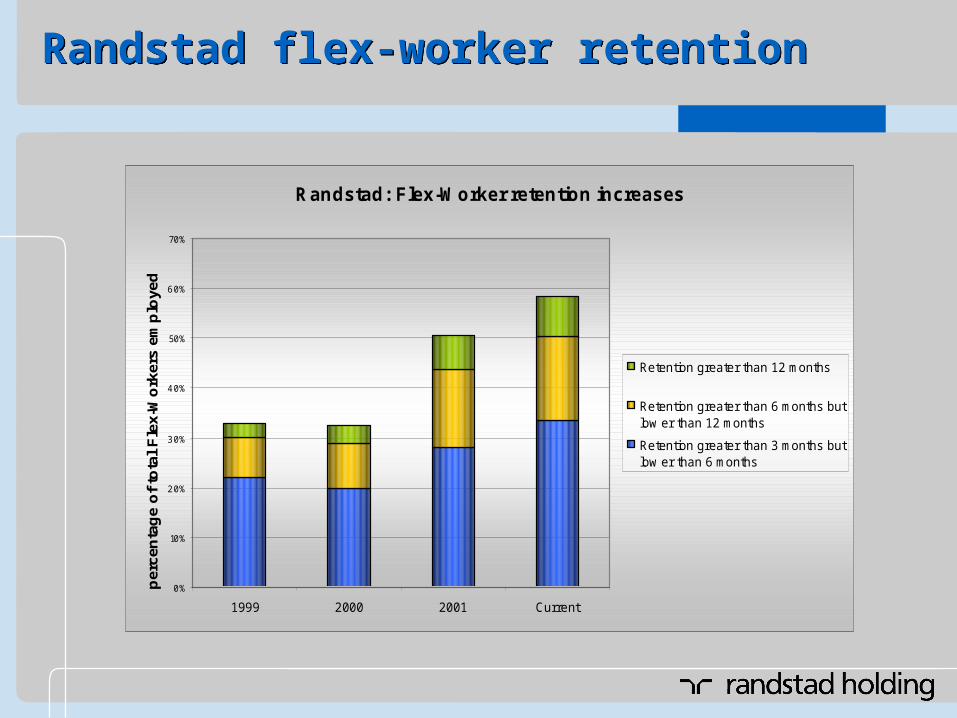

Randstad flex-worker retentionRandstad flex-worker retention

Randstad: Flex-Worker retention increases

0%

10%

20%

30%

40%

50%

60%

70%

1999 2000 2001 Current

per

cen

tag

e o

f to

tal

Fle

x-W

ork

ers

emp

loye

d

Retention greater than 12 months

Retention greater than 6 months butlow er than 12 months

Retention greater than 3 months butlow er than 6 months

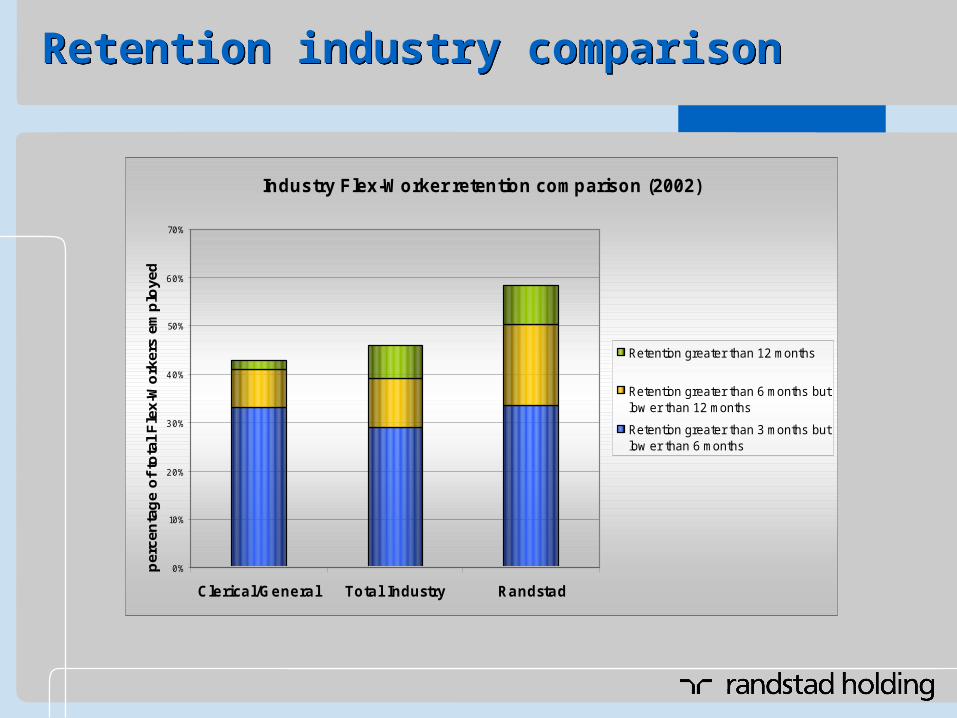

Retention industry comparisonRetention industry comparison

Industry Flex-Worker retention comparison (2002)

0%

10%

20%

30%

40%

50%

60%

70%

Clerica l/Genera l Tota l Industry Randstad

per

cen

tag

e o

f to

tal

Fle

x-W

ork

ers

emp

loye

d

Retention greater than 12 months

Retention greater than 6 months butlow er than 12 months

Retention greater than 3 months butlow er than 6 months

Randstad labor market surveyRandstad labor market survey

Positive outlook on employment market

Use of non-permanent workers

Ways to attract and retain staff

The UK working week

Staff loyalty

Impact of legislation

Thank you!

Any questions?

Thank you!

Any questions?

Randstad in the USRandstad in the US

Jim Reese

Member of the Executive Board

CEO Randstad North America

Randstad in the USRandstad in the US

Overview of the company

Who we are

Where we are

What we offer

Our focus

Priorities

Moving forward

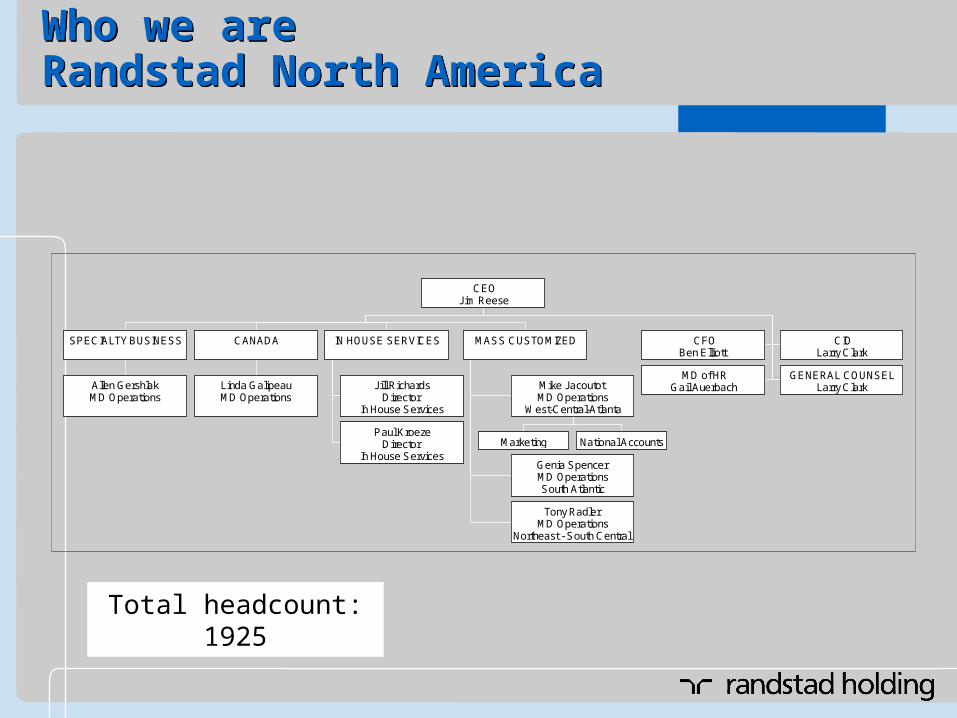

Who we are Randstad North AmericaWho we are Randstad North America

CEOJim Reese

SPECIALTY BUSINESS

Allen GershlakMD Operations

CANADA

Linda GalipeauMD Operations

IN HOUSE SERVICES

Jill RichardsDirector

In House Services

Paul KroezeDirector

In House Services

MASS CUSTOMIZED

Mike JacoutotMD Operations

West-Central-Atlanta

Marketing National Accounts

Genia SpencerMD OperationsSouth Atlantic

Tony RadlerMD Operations

Northeast - South Central

CFOBen Elliott

CIOLarry Clark

MD of HRGail Auerbach

GENERAL COUNSELLarry Clark

Total headcount: 1925

Randstad North America Divisions

357 TOTAL BRANCHES

113 TOTAL ON-SITES

West/Atlanta/Central Division (106)

South Atlantic Division (141)

Northeast South/Central Division (96)

Canadian Division (14)

States/ provinces w/o RNA Offices

Randstad North America On-sites (113)

521

3

2

20

4

5

20

1

6

1

2

7

15

4

2

12

9

7

6

35

2 2 40

17

8

221

2

6

18(1) 3 (3)

14(5)

16

31

DC: 6(1)

9(7)

(6)

(1)

(1)

(6)

(1)(2)

(1)

(1) (3)(18)

(18)

(6)

(2)(18)

(1)

(1)

(4)

(2)

(2)

(2)

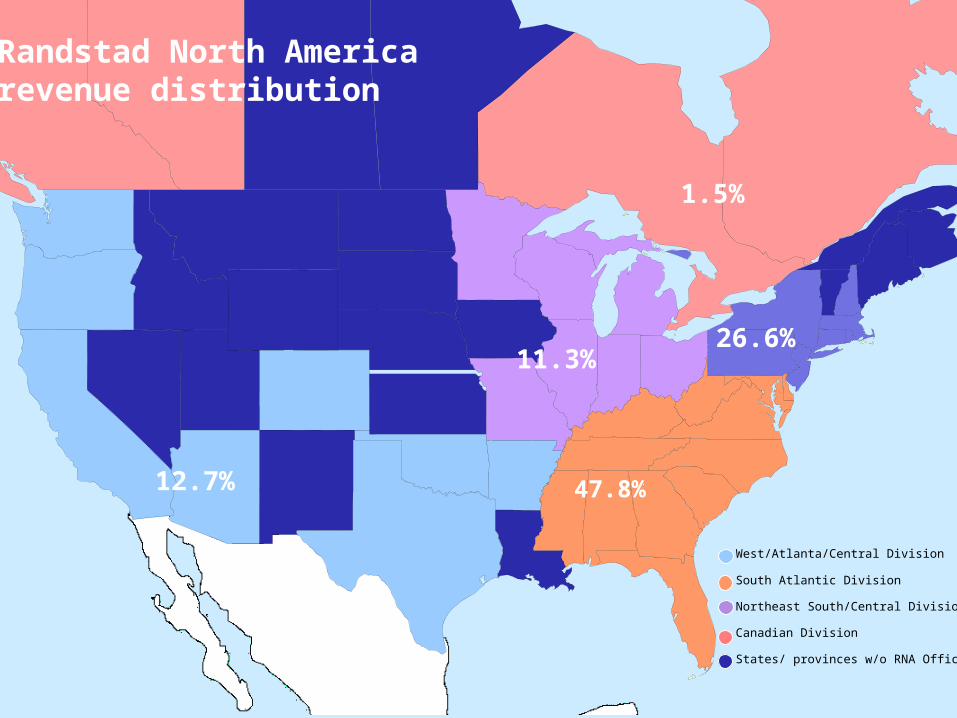

Randstad North America revenue distribution

West/Atlanta/Central Division

South Atlantic Division

Northeast South/Central Division

Canadian Division

States/ provinces w/o RNA Offices

1.5%

47.8%12.7%

11.3%26.6%

What we offerWhat we offer

Mass-customized concept: Office, Industrial, IT, Creative and Professional

Randstad Inhouse Services:Manufacturing, Logistics, Warehousing

STRATEGY: DIFFERENTIATORS:

Strong concepts Same people – Sell and service

Best people Local people – Local decisions

Excellence in execution Right people – Talent focus

Superior brands Smart people – Better solutions

Must compete with local, regional and national competitors

Our focusOur focus

Put more people to work

Implement and effectively use systems

Hire and retain the best people

Continuously improve costs

Put more people to workPut more people to work

Ensure consistency of implementation & execution

of strong concepts: Mass-customized and Randstad Inhouse

Services

Drive sales activities through our unit structure

Build our business locally first, along with national and

corporate business

Manage pricing based on business and location

Implement and effectively use systemsImplement and effectively use systems

PeopleSoft system

Front office:- Platform for future- Consistency of application to support concepts- Monitoring of performance- Management of pricing and controls

Shared Service Center- Customer billing- DSO- Overall platform for process improvements

Leverage technology for transactions and people for relationships

Retain and hire the best peopleRetain and hire the best people

Hire the best people to match concept expectations

Training and development

- New hires- Managers- High performers

Communication

Rewards and recognition

Staff retention

Continuously improve costsContinuously improve costs

Drive efficiency with technology platform

Shared Service Center

- Continue to drive DSO improvement

Improve overall productivity

Leverage purchasing power

Moving forwardMoving forward

Keep our focus and continue to develop discipline

Win right both locally and nationally

Leverage excess branch capacity to grow

Build our brand and reputation

Continue strong cost control and improvement

Thank you!

Any questions?

Thank you!

Any questions?

Concluding remarksConcluding remarks

DisclaimerDisclaimerDisclaimerDisclaimer

Certain statements in this document comprise forecasts on Randstad Holding’s future financial condition and results from operations and certain plans and goals. By their nature, such forecasts generate risk and uncertainty because they concern events in the future and depend on circumstances which then apply.

Any number of factors can cause actual results and developments to deviate from those expressed in the forecasts stated here. Such factors can be, but are not limited to, general economic conditions, scarcity on the employment market, the variation in the demand for (flexible) personnel, changes in employment legislation, future currency exchange rates and interest rates, future corporate mergers, acquisitions and divestments and the speed of technical change.

The forecasts speak only as at the date of this document.