world intellectual property organization · world intellectual property organization ......

TRANSCRIPT

Annual Audit Work Plan

External Auditor

World Intellectual Property

Organization

For the period

June 2013 to May 2014

Overall Audit Strategy Document for Audits of WI PO for the year 2013-2014

Introduction ·

1. This document aims at detailing the external audit assignments planned for the period June 2013 to May 2014. We will perform our audit in conformity with the International Standards of Auditing.

Audit Mandate

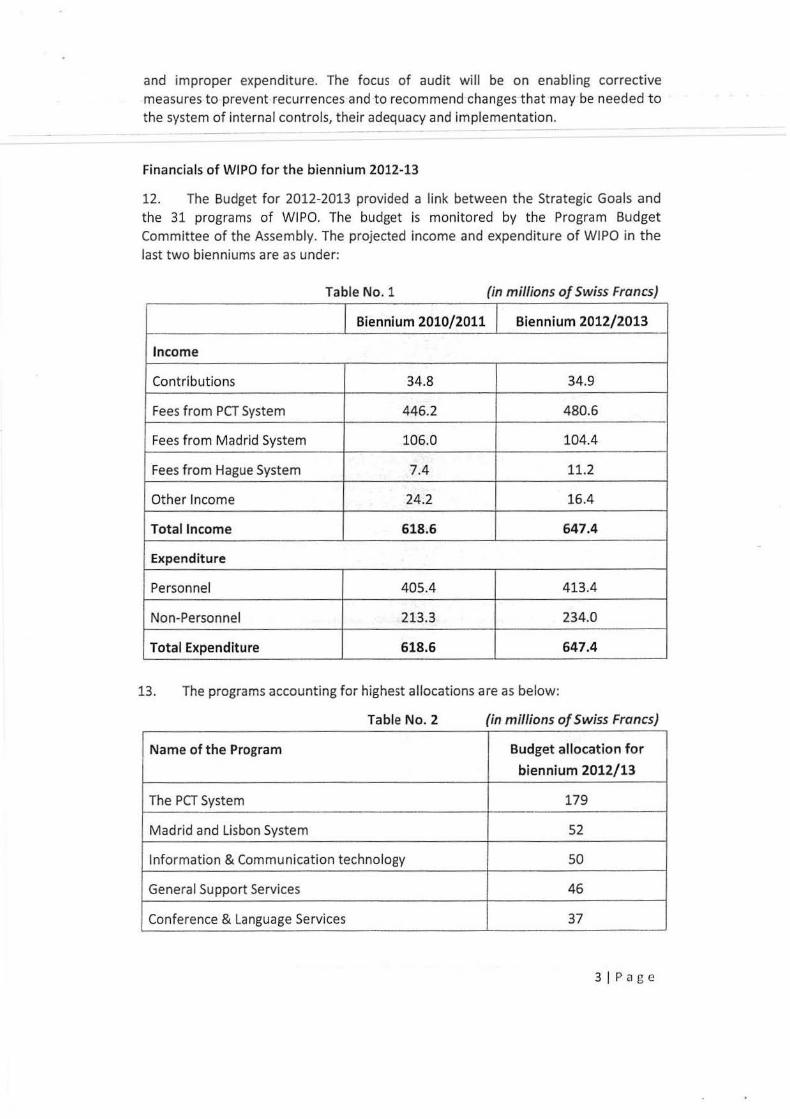

2. Chapter 8 of the Financial Regulations of WIPO and its Annex II define the mandate for the External Auditor. As per Regulation 8.10, the External Auditor shall issue an opinion on the financial statements for each year of the financial period, and a report on the audit of the financial statements for the financial period, which shall include such information as the External Auditor deems necessary with regard to matters referred to in Regulation 8.5 and in the annex to the present Regulations referred to in Regulation 8.4.

3. Broadly, two outputs are expected from the External Auditor of WI PO. These are:

• The External Auditor is required to express an opinion on whether the financial statements fairly represent the financial position and results of the operations, that the financial statements were prepared in accordance with the stated accounting policies, that the accounting policies were applied on a consistent basis and on the compliance of transactions with the Financial Regulations and legislative authority.

• The External Auditor is required to submit a report on the financial operations to the WIPO. This report may include observations on the efficiency of financial procedures, accounting system & transactions, internal controls and, in general, the administration and management of the Organization.

Audit Approach

4. As in 2012, a comprehensive audit approach is planned for the current audit cycle to address our mandate and terms of reference. This would integrate:

• Financial attest auditing • Compliance auditing • Performance Audit

l iPage

5. The working relationship with the WIPO management has been constructive and the- audits performed at different levels - were facilitated by excellent cooperation from the Finance as well as other wings. The Internal Control environment will be-evaluated to decide the extent of relia-n-ce thereon- basea on which the nature and extent of substantive audit testing will be determined. Coordination has been established with the office of the Internal Audit and Oversight Division to avoid duplication of effort.

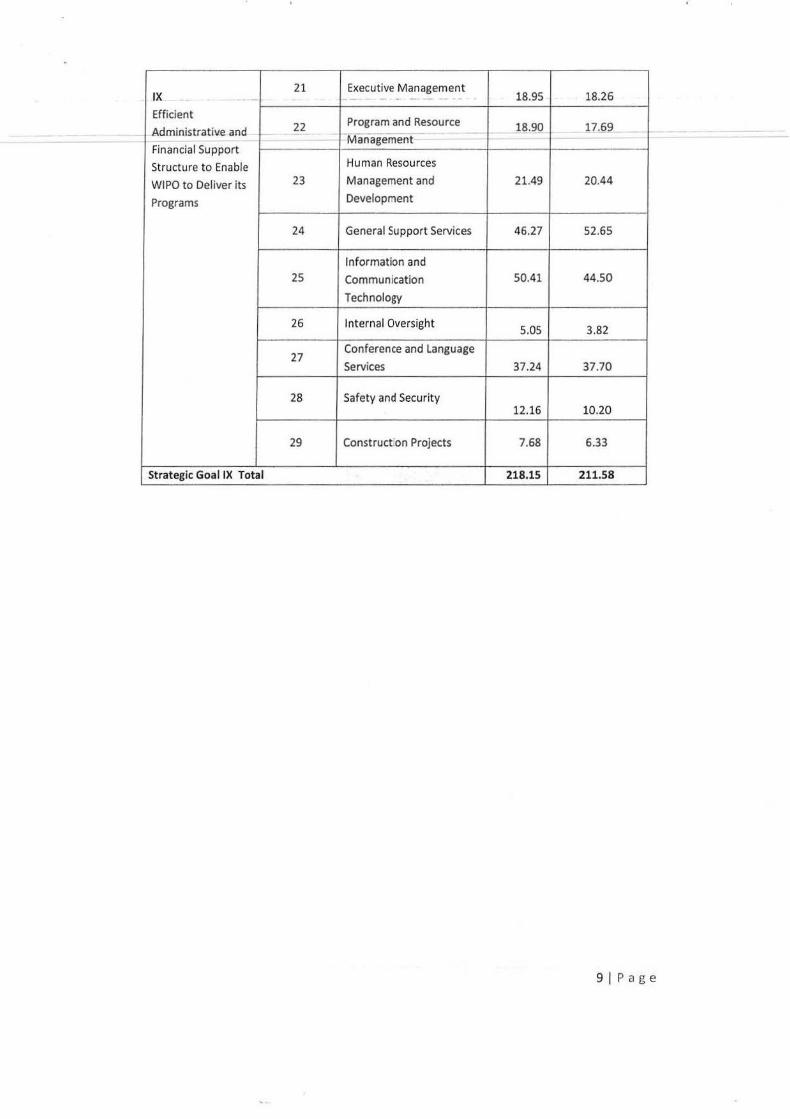

6. While developing our annual work plan, we have consulted senior management of WIPO inviting them to make suggestions for audits that would address areas of concern.

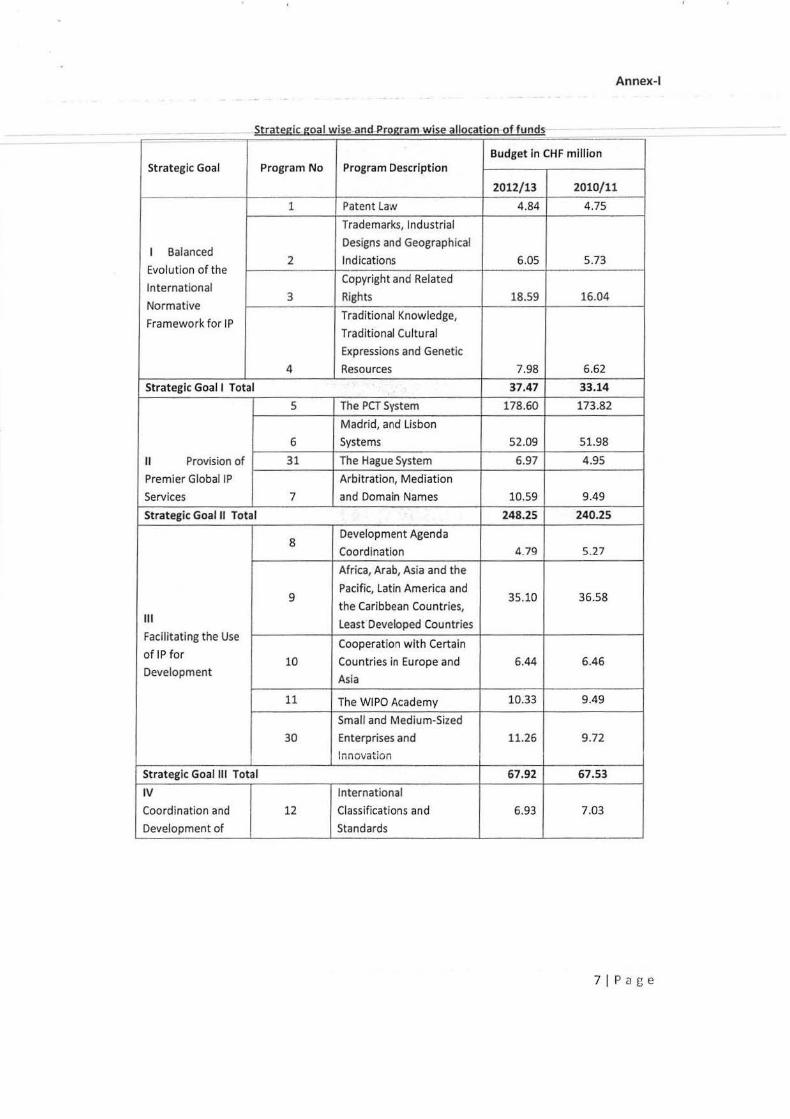

7. WIPO has established nine Strategic Goals, which provide the framework for Medium Term Strategic Plan and Biennial Program and Budget. These goals are expected to be achieved through 31 programs. Strategic goal wise allocation of funds is placed at Annex I .

8. We had carried out risk assessment of WIPO during July 2012 taking into account the specificities of the organization. Based on risk assessment conducted with reference to strategic issues, financial materiality, compliance and operational issues, we have prioritized the programs for audits for the year 2012-18.

Financial Audit objective

9. WI PO has switched over to IPSAS with effect from 2010 and has prepared the 2010 financial statements in accordance with IPSAS. The Audit strategy will include attest functions of the financial statements and providing an opinion on the financial statements prepared under IPSA$. Our opinion and report shall conform to the requirements prescribed in the relevant clauses of 'Financial Regulation 8' and 'terms of reference governing External Audit' as set out in the Annex to the WIPO financial regulations. This will involve examination and evaluation of financial records to obtain competent, relevant and reasonable evidence to support our conclusions. The overall objective is to ensure that the Financial Statements are f ree from material misstatements and the underlying transactions comply with WIPO regulat ions.

Performance Audit objective

10. The areas for performance audit will be selected on the basis of the quantum of resources allotted to them and the risk that the operations have not been carried out with due regard to economy, efficiency and effectiveness.

Compliance Audit objectives

11. In compliance audit, we will examine the propriety of transactions and compliance to rules and regulations of WIPO, and report cases, if any, of wasteful

and improper expenditure. The focus of audit will be on enabling corrective measures to prevent recurrences and to recommend changes that may be needed to the system of internal controls, their adequacy and implementation.

Financia ls of WIPO for t he biennium 2012-13

12. The Budget for 2012-2013 provided a link between the Strategic Goals and the 31 programs of WIPO. The budget is monitored by the Program Budget Committee of the Assembly. The projected income and expenditure of WI PO in the last two bienniums are as under:

Table No.1 {in mmions of Swiss Francs)

Biennium 2010/2011 Biennium 2012/2013

Income

Contributions 34.8 34.9

Fees from PCT System 446.2 480.6

Fees from Madrid System 106.0 104.4

Fees from Hague System 7.4 11.2

Other Income 24.2 16.4

Total Income 618.6 647.4

Expenditure

Personnel 405.4 413.4

Non-Personnel 213.3 234.0

Tot al Expendit ure 618.6 647.4

13. The programs accounting for highest allocations are as below:

Table No. 2 (in m illions of Sw iss Francs)

Name of the Program Budget allocation for

biennium 2012/13

The PCT System 179

Madrid and Lisbon System 52

Information & Communication technology 50

General Support Services 46

Conference & Language Services 37

3jP age

Africa, Arab, Asia and the Pacific, Latin America and 35 -- -- -· ------ ----· - -·-· the Caribbean Countries, Least Developed Countries

14. WIPO being a knowledge centric organization, spends 64 percent of its budgetary resources on personnel costs which include posts, short term professional, consultant and short term employees. Non Personnel costs include travel and fellowships, contractual services, operating activities and equipment and supplies. On the receipt side, unlike other UN bodies, it has its own sources of funding namely fees received from private parties for providing services. The contribution of Member States accounts for only 5.4 percent of resource generation. The biggest source of revenue for WIPO is the PCT Union followed by Hague and Madrid Unions.

15. Over the years, WIPO has built up substantial reserves (surplus income from fees that exceed the amounts required to finance the program and budget appropriations) which are invested as per the Investment Policy of WIPO. A portion of the reserves are also utilized for financing specific projects. To that extent some of the projects are actually not part of the Program Budget. Some of the significant programs t hat are being funded out of reserves include ERP, capital investment in IT, etc. A separate report is presented to the Assembly on utilization of Reserves.

Audit Coverage during 2012

16. Following was the Audit coverage during 2012.

Year Financial Financial Performance audit Compliance Audit

audit of audit of

interim annual

f inancial financial

st atements statement s

2012 Geneva (2 Geneva {4 Performances audit Compliance Audit of

weeks) weeks) of 'Patent 'sourcing and engagement

Cooperation of special service

Treaty' agreements and

commercial service

providers'

PROPOSED AUDIT COVERAGE FOR 2013-14

17. The probable risk areas were discussed by the Sr. Director, Ext ernal Audit and his team with the head of IAOD, head of Finance and Financial Controller. Based on the discussions, past audit coverage and risk assessment following is proposed for financial, performance and compliance audit during 2013-14.

4 1P a ge

18. Financial Audit: Interim audit of the Financial Statements of first three quarters for the year 2013 is-proposed·to be carried out at Geneva (as was done for 2012 accounts) for two weeks (November 2013). Final audit will be conducted for four we-eks during- April/May 2014 at Geneva.

19. Performance Audit: Based on the discussion with the management and areas identified in our risk assessment report, performance Audit topics of 'Madrid and Lisbon Systems', Strategic Realignment Programme, 'Human Resources Management and Development', 'Africa, Arab, Asia and the Pacific, Latin America and the Caribbean Countries, Least Developed Countries' and 'ERP systems' were considered for audit during 2013.

(i) Madrid and Lisbon Systems- Madrid and Lisbon system accounts for the 2nd highest budget allocation of CHF 52 million during 2012/13 and was considered as high risk in our risk assessment. However, internal audit would be covering this topic during 2013 and therefore inclusion of this topic in our work plan would amount to duplication of effort.

(ii) Human resource management- Staff costs account for 64 per cent of the expenditure. Thus, human resource appears as a major risk area from the financial point of view. Further, based on our previous year audits, issue of resources and mismatch of skills of human resource was noticed. However, reports on human resource management were presented both by external auditors and internal auditors in 2011.

(iii) Strategic Realignment Program (SRP) is the flagship program of WIPO for organizational improvement. As the programme will be reviewed by Joint Inspection Unit of the United Nations this year, we propose to take it up later.

(iv) Performance Audit of ERP- ERP System is being expanded as part of strategic realignment program and is funded out of reserves. The current ERP system called AIMS is proposed to be expanded and enhanced to serve the whole organization. The finance, procurement and travel modules have been in place for some years. AIMS have facilitated transition to IPSAS. Three distinct projects, viz., Core HR and Payroll; Performance Management; and Business Intelligence analytics have commenced in 2012. New initiatives of ERP are likely to be completed by 2013. However, it has been covered extensively by Internal as well as External audit in recent years. Hence, it could be taken up as Performance audit during subsequent years.

(v) Performance audit of 'Africa, Arab, Asia and the Pacific, Latin America and the Caribbean Countries, Least Developed Countries'. This is under Strategic goal Ill (programme 9) with a budget of 35.10 million Swiss francs during 2012-13. This topic also emerged as a high risk area in our risk assessment.

In view of above, we decided to take up 'Africa, Arab, Asia and the Pacific, Latin America and the Caribbean Countries, Least Developed Countries' as topic for

SIPage

Performance Audit during 2013, as the audit results would add value to WIPO operations.

~o-. -- Compliance Audit: Tliere ·are 257 units in WI PO covering the activities off e programs. Whi le many units correspond to specific programs, one to one correspondence in many cases cannot be established. Similarly, in many cases unit refers to an administrative office e.g., office of Director General or a small support unit. The Internal Audit or previous External Auditors have not reported results of such unit wise audit.

21. In view of above, we decided to cover Strategic Goal IX, program no. 29, construction projects with the budget of CHF 7.67 million. In addition, CHF 24 million from the WI PO reserves and CHF 40 million loans has been provided for construction of new conference hall. In the meeting of IAOC during September 2012, the Committee informed that the contract for construction of conference hall was awarded to the same contractor who defaulted in completion of Administration Building and a penalty was imposed on the contractor. The Committee also informed that this contractor had been removed from construction of conference hall and no new general contractor was to be appointed and that the project would instead be managed by inducting additional resources through "internal redeployment, secondment from other UN agencies or temporary engagements".

22. Previous External Auditor (Swiss) had also not audited the final accounts related to construction project and IAOC suggested that we consider including in our work plan an audit/inspection of the new construction projects as a priority issue, as well as audits until the successfu l completion of the project.

23. Audit of the construction projects as Compliance audit during 2013-14 will be conducted by a three member team for four weeks time during March 2014.

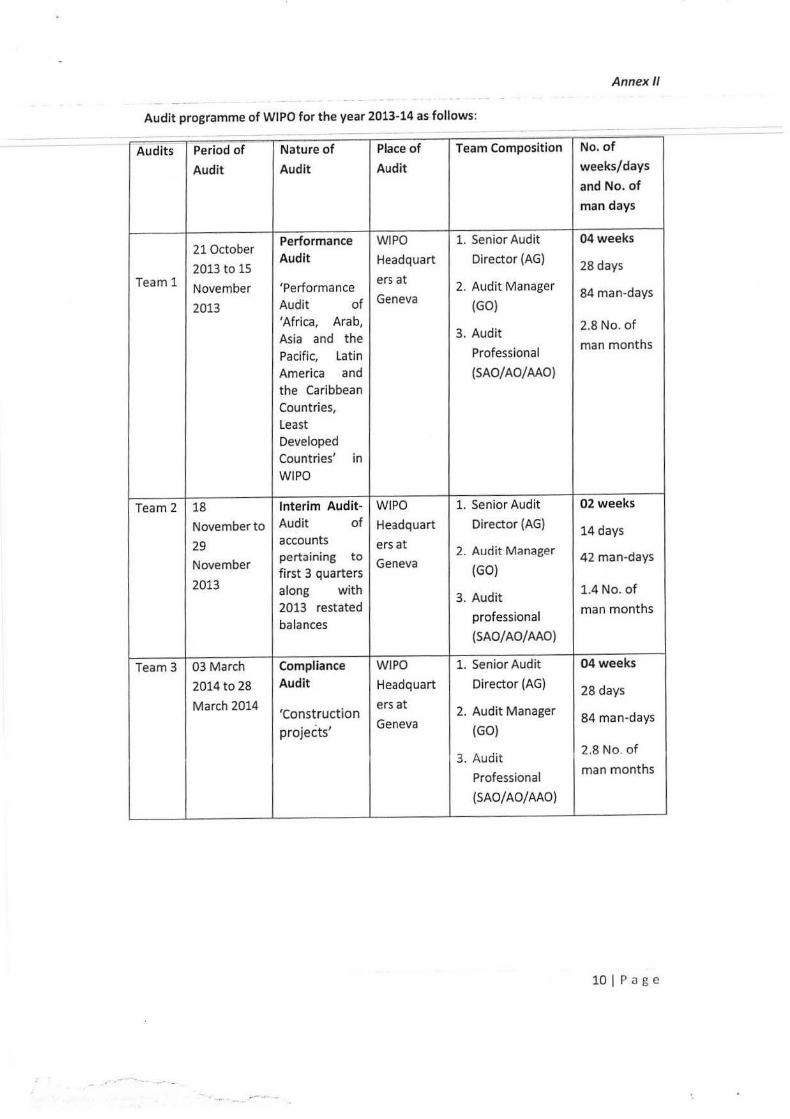

24. The time schedule of various audits is set out in Annex-//.

6IP age

Annex-1

Strate2ic 2oal wise an<LRro2ram wise allocation of funds - -

Budget in CHF million Strategic Goal Program No Program Description

2012/13 2010/11

1 Patent law 4.84 4.75

Trademarks, Industrial

I Balanced Designs and Geographical

2 Indications 6.05 5.73 Evolution of the

Copyright and Related International

3 Rights 18.59 16.04 Normative

Framework for IP Traditional Knowledge,

Traditional Cultural

Expressions and Genetic

4 Resources 7.98 6.62

Strategic Goal I Total 37.47 33.14

5 The PCT System 178.60 173.82

Madrid, and lisbon

6 Systems 52.09 51.98

II Provision of 31 The Hague System 6.97 4.95

Premier Global IP Arbitration, Mediation

Services 7 and Domain Names 10.59 9.49

Strat egic Goal II Total 248.25 240.25

8 Development Agenda

Coordination 4.79 5.27

Africa, Arab, Asia and the

9 Pacific, Latin America and

35.10 36.58 the Caribbean Count ries,

Ill Least Developed Countries Facilitating the Use

Cooperation with Certain of IP for

10 Countries in Europe and 6.44 6.46 Development

Asia

11 The WI PO Academy 10.33 9.49

Small and Medium-Sized

30 Enterprises and 11.26 9.72

Innovation

Strategic Goal Ill Total 67.92 67.53

IV International

Coordination and 12 Classifications and 6.93 7.03

Development of Standards

7 1P a ge

13 Global Databases 4.50 1.91

- - - Service-s-tor Access to - -

14 Information and 7.04 8.80 - l(now reage-

- -Business Solutions for JP

15 Offices

7.81 7.21

Strategic Goal IV Total 26.29 24.96

v World

Reference Source 16 Economics and Stat ist ics 4.59 3.94 for IP Information

and Analysis

Strategic Goal V Total 4.59 3.94

VI International

Cooperation on Building Respect for IP 2.99 3.02

Building Respect for 17

IP

Strategic Goal VI Total 2.99 3.02

VII

Addressing IP in JP and Global Challenges 18 6.77 5.56

Relation to Global

Policy Issues

Strategic Goal VII Total 6.77 5.56

VIII A 19 Communications

Responsive 16.60 15.84 Communicat ions

Interface between External Relations, WIPO, its Member 20 Partnerships and External 10.91 11.35 Stat es and All Offices Stakeholders

Strategic Goal VIII Total 27.51 27.19

8IPage

IX 21 Executive Management

- - - 18.95 18.26

Efficient

Administrative and 22 Program and Resource 18.90 17.69 1- -- Management

-

Financial Support

Structure to Enable Human Resources

WI PO to Deliver its 23 Management and 21.49 20.44

Programs Development

24 General Support Services 46.27 52.65

Information and

25 Communication 50.41 44.50

Technology

26 Internal Oversight 5.05 3.82

27 Conference and Language

Services 37.24 37.70

28 Safety and Security 12.16 10.20

29 Construcfon Projects 7.68 6.33

Strategic Goal IX Total 218.15 211.58

9 I P a ge

Annex II

Audit programme of WI PO for the year 2013-14 as follows : - - -

- -- - - -Audits Period of Nature of Place of Team Composition No. of

Audit Audit Audit weeks/days

and No. of

man days

21 October Performance WI PO 1. Senior Audit 04 weeks

Audit Headquart Director (AG) 2013 to 15 28 days

Team 1 November 'Performance ers at 2. Audit Manager 84 man-days

2013 Audit of Geneva (GO) 'Africa, Arab, 2.8 No. of Asia and the 3. Audit

Pacific, Latin Professional man months

America and (SAO/AO/AAO) the Caribbean Countries, Least Developed Countries' in

WI PO

Team 2 18 Interim Audit- WI PO 1. Senior Audit 02 weeks

November to Audit of Headquart Director (AG) 14 days 29 accounts ers at

pertaining to 2. Audit Manaeer 42 man-days November

first 3 quarters Geneva (GO)

2013 along with 1.4 No. of 3. Audit

2013 restated man months balances

professional

(SAO/AO/AAO)

Team3 03 March Compliance WI PO 1. Senior Audit 04 weeks

2014 to 28 Audit Headquart Director (AG) 28 days March 2014

'Construction ers at 2. Audit Manager

projects' Geneva (GO)

84 man-days

3. Audit 2.8 No. of

Professional man months

(SAO/AO/AAO)

10 I P a g c

Team2 7 April 2014- Financial WI PO 1. Senior Audit 04 weeks

- 2 May 2014 Audit of the Headquart -oirector (AG) -

Financial ers at 28 days

1- statements for Geneva ~ Audit Mangger ~ -

(GO) 84 man-days-the year ending 31 3. Audit 2.8 No. of December professional man months 2013 (SAO/AO/AAO)

11 I P ag e