world council of credit unions, inc. - usaid

TRANSCRIPT

World Council of Credit Unions, Inc.

Expanding Caja Popular Mexicana Sustainable Outreach

USAID Award No: GEG-A-00-01-00004-00

Final Report January 2008

Prepared by: Barry Lennon, Senior Vice President, Technical Services Janette Klaehn, Vice President, Marketing and Communications

Submitted to: Tracy Miller, Regional Agreement Officer

World Council of Credit Unions 5710 Mineral Point Rd.

Madison, WI 53705

World Council of Credit Unions, Inc. 5710 Mineral Point Road . Madison, WI 53705-4493 Phone: (608) 395-2000 Fax: (608) 395-2001 E-mail: [email protected] . Website: nww.woccu.org

World Council of Credit Unions

Executive Summary

In September 2007, World Council of Credit Unions, Inc. (WOCCU) completed a six-gear technical assistance program with Caja I'opular Mexicana (CI'hl), the largest single financial cooperative in Mexico and in all of Latin iiinerica. l'he Cl'M program was frst fmanced by the Microentcrpl:ise I~evelopmcnt Office of the U.S. Agency for International I>eveloptncnt (USAID) in Washington, 13.C., through a four-year Cooperative ilgrecmcnt (GEG-il-00-01-00004-00). It was later extended for an additional hvo years with financing from the USAID Mission in Mexico City.

In a counuy where well over half the population does not have access to financial services from formal financial institutions, the success of the CI'M prograin is noteworthy. CI'M has cinerged as a profitable, innovative and effective financial institution that provides safe and affordable financial seivices to over a million low-income clients in urban and rural Mexico. It is growing at an annual rate of inore than 20%, and has plans to penetrate and deliver financial sclvices to rural cominunities that today are woefully undcrscrvcd.

'The 2001 decision of USAID to finance the technical partnership between CI'M and WOCCU was v e q timely. CPM had negative capital, loan delinquency was very high and CI'M was being scrutinized by the regulatory authorities. A change in direction was needed. Over the past six years, WOCCU has helped CI'M to overcoine its financial management problems, improve operational efficiency and develop staff capabilities while substantially increasing the quality and range of services. T111:ough its international partnership, CPM has also received technical assistance from the C:alifornia and Texas credit union leagues in the United States.

' Source: Years 2002 & 2003fi.um WOCCUprogrun? report and 2004-2007fi.oni MlXNeln~ork, oil bused on CPM jinancial data.

Wotld Council of Credit Unions

In June 2007, CPM had more than 1.15 tndlion inernbers with savings totaling US$1.26 billion. Loans outstanding totaled over US$1.06 billion, and delinquency was approxilnatcly 4.6%, much improved over the 18.7% rate that existed in Decclnbcr 2001. ~lsscts, loans and savings are growing at more than 20% every ycar and 14,000 new members are joining every month.

CI'M membership is still coillposed of pcople from ever)^ segment of the population, from farmers to teachers, office workcrs to taxi drivers and micro en~eprctleurs. CPM provides its members with sc l~ices through 348 branch offices located in 22 of the 32 Mexican states. The branches are organized into 27 regional offices and six sub-directorates, each of which reports to the headquarters in Leon, Guanajuato, Mexico.

I7inally, a new information tccllnology (11') system was i~lstalled in 2006 that permits real-time opcratiotls and daily reporting in all branches, sotncthing that was impossible in 2001. 'l'he new system not only permitted (:I'M to standardize operations and improve efficiency, but it will also enable CPM to offer lnorc sophisticated finatlcial products such as international rc~nittances, sharcd branching and debit and credit ca~:ds on a mass scale.

At the close of the technical assistance program ul September 2007, CI'M was operating as an itltegratcd fi~~ancial intcrrncdiary that is well positioned to penetrate new markets and expand the range of financial products and sei-vices now offered.

Wot.Id Council of Credit Unions

Challenpes f a c i n ~ Caia Po~ular Mexicana in 2001

'She credit union inoveinent in Mexico dates back to 1951. Un1:egulatcd for more that] 40 ycars, in 1994 the Mcxican C.;overninent acted in response to widely publicized cases of fraud and deteriorating public confidence in the c u j i sector to prolnulgate new legislation (tbc i4)r Ge~~elzrlN'c Sociciicii/es ~oope,zrti7~as) to establish two types of financial coopcrativcs - so~icciaiie~~ cie a i i onoyp7~s fn l~o [SAl'] and so~9edurie.r coopemliuas iic a h o m y iriciito [CJIC]. 'l'hc newly formcd Caja Popular Mcxicana (CI'M) became a savings and loail society, or SAP, that would be regulated (albeit from a distance) by the fcdcral govcmment.

CPM was crcatcd twelve years ago whcn 62 credit unions, state federations and one national association incrgcd to form the Iargcst non-bank financial institution in Mexico. 'l'he mergcr required years of difficult negotiations, and over half of the original group of iildependent cooperatives decided not to join the 62 that eventually created (:I'M. Thc early years were filled with many challcngcs as the newly forincd institution st1:uggled to introduce ncw fu~aiancial management and intcrnal coiluol mcchanisins and ovcrcoinc a debilitating lack of cohesion atnong its 300+ branches, over two-thrds of which wcrc generating losses.

When WOCCU began working with (;I'M, the merger was six gears old but consolidation was far from complete. I\/Iany branch managers, particulai:ly those in the larger branches and regional offices, fclt little loyalty to CPM hcadquartcrs. 'l'hey had been Cl<Os of thc ci:cdit unions that were merged, and they resisted what they felt was a loss of identity and position in their home cotnmunities. ~ l t t cmpts to standardize policies and procedu1:es were opposed, and that opposition had a dclctcrious unpact on CPM's efficicncy and financial pcrforinancc.

'l'hc mergcr of so Inany institutions presented an array of challenges. l'hc inergcd institutions were operating with 13 different information systcms, 23 charts of accounts and 62 boards of directors, supel~~isory coinmittees and credit approval committecs. Each branch prcscnted a unique brand to the inarkct and offered different products and services. The forinerly independent credit unions tended to be highly bureaucratic with excess staff; most of the existing products were outdated and unattractive to clieilts; and loan approvals wci:e determined by a siinple leverage of member share balances (i.c., 2:1 or 3:1), a practice which led to high rates of loan default.

Each branch manager used dfferent criteria to analyze and approve loan applications, and loan collcction policies were at best, lax. In 2001, (;I'M'S delinquency rate averagcd a crippling 19%. 'Thc few profitable branches had to subsidize thc opcrations of the unprofitable ones, creating strong internal disscnsion atnong some managcrs and meinbers as profitable branches wcrc unable to pay the expected dividends.

'The final major challenge facing CI'M was the passagc in 2001 of the new regulatory framework for financial coopcrativcs. ' n ~ e ncw legislation created four ticrs of institutions, each with different regist~:ation criteria and levels of perinissible service offerings. CI'M was far frotn meeting the requirements of that new lcgislation and the banking coinn~issioi~ (Co1nisi6n Nacional Bancaria 7 de Valores) was closely monitoring its opcrations. 'rhc risk of govcrnn~cnt inteivcntion was real, but this helped the Cl'M's senior management convince the board of directors to approve a tcchnical partnership with WOCCU and an aggressive consolidation agenda.

World Council of Credit Unions

WOCCU's Implementation Strategy

WOCCU's initial four-year technical assistance program followed a step-by-step process to identif)~ the most pressing operational deficiencies affecting (:I'M and devise strategies to confront them by priority. It became quickly apparent that reaching and assessing the operations of 340+ branch offices, many of which were distant from CI'M's headquarters i11 I.,con, would be tune-consuming and expensive.2 As a result, WOCClJ and C13M developed a phased strategy that targeted one rcgional office and its affiliated branches for analgsis before lnoving to the nest region and its branches.

X concerted effort was also made to train headquarters and regional office staff and to create specialized assessment teams to complement WOCCU's technical personnel. It took almost two years to visit and evaluate the operations of each of the branch offices, but by the end of that process, CPM had the tools and a cadre of staff who were (and are) capable of monitoring branch operations.

In 2005-07, a follow-on two year technical assistance program, funded by USAlIl/Mexico, enabled WOCCU and Cl'M to colnpletc the installation of the new itlformation techtlology (I73 ssystcm, institutioilalizc many of the changes that had begun in the fust phase of the program, launch international rclnittances and develop training programs for staff in each regional officc and branch.

Staff training remains an important clement of Cl'M's development planning. As CPM's rnetnbership grows, so does the number of personnel. C:131vI's policy to control branch sizes tneans new staff are joining and roles and responsibilities arc constantly evolving. When a branch reaches 7,000 inembers, a new branch is fortned with 2,000 of the inembers to maintain a more personalized tnetnbcl: senlice. Additionally, management cncouiltered great staff demand for coilti~lucd uaining.

2 The number of CPM branches decreased kom 3401- in 2001 to about 325 by 2005 as CPM closed losing branches. As of June 2007, the number of branches was back up to 348 as CPM expanded its capacity to respond to a growing membership.

World Council of Credit Unions

Number of Caja Popular Mexicana Employees3 N v r n b ~ r ~ f i m p l o y e ~ r

Throughout the six-year program, WOCCU technicians pi:ovided on-the-job training for l~eadquarters and regional officc managers and staff, but tnorc itnportantly, they developed a curricululn to be uscd it1 "training the trainers." liegional training centers were established at each of the 27 regional officcs, and as new policies and procedures were rolled out, or new systctns- such as I'Ef1lU.S-implemented, WOCCU technicians trained CI'M staff who, in turn, trained thcit peers.

The Approach WOCCU technical staff worltcd within Cl'hf's institutional decision-making cu1tu1:e and sought to avoid being seen as external consultallts who only communicated with top managcmeilt. Broad communication and frequent discussion of thc program strategy was tiinc consuming, but it permitted WOCCU to overcorne many existing institutional barrie~s. l i t sral:tup, lines of authority at all lcvcls of thc institution were unclear; policies and procedures were not standardized in the brailches; and local managers opcratcd however they wishcd and were suspicious of 'outsiders.' Engaging thc board, top managers and mid-level staff at cveq step of thc way was an effectirre strategy.

'l'hc stcp-by-step branch diagnostic process also permitted WOCCU to demonstrate the value and potential of the I'EI\RL,S monitoring systcln while pl:oviding time to build trust among senior CI'M and branch managers, Initial priority tasks identified by CPM managers included: cleaning- up the loan portfolio; improving financial performance, profitability and CPM's ability to build capital reservcs; creating a strategic plan; integrating the brailchcs and personnel into one institution; and striking a balance behvecn CPM's social mission and a hcalthy business culture. Standardization of policies and procedures was essential, as was the creation of a specialized credit and collections departlncnt and a product development group to address member and market detnailds for better scnice.

International Partnerships In 2003, WOCCU dcveloped a partnership arrangcrnent among CI'M and two U.S, credit union partners, the California Credit Union 1,eague and the Texas Credit Union I<caguc. 'nlc two leagues provided CPM with access to specialized technical assistance and helped build a lasting relationship that contiilucs today. During the f ~ s t year of the partnership, techilical assistailce targeted

"nless otherwise noted, all data is from CPM reporrs as of June 2007

6

World Council of Credit Unions

adjustments to CI'M's institutiotlal suucture, credit and collections, human resources and markcting policies and procedures. As CPM's needs evolved, so did the tecli~lical support provided by the partners. The California and the 'Texas leagues provided critical guidance on the purchase of and migration to the new I'T system.

Both leagues colltitlue to provide tcclinical assistance today, fine tuning CI'M's marketing program, particularly as it relates to remittances from the United States, and assisting with training. CI'M also helps the leagues in their marketing to Mexicans living in the United States. The partners are exploring the possibility of linking CI'IVI to the U.S. national shared branching network, a move that would enable Mexicans in the Unitcd States to acccss their CPM accounts directly and ilmcrican credit union tnctnbers in Mexico to access their accounts at any CI'M branch.

Implementation of the new IT system was a critical step in colinecting CI'M onto the existing credit union shared branching network in the Unitcd States. Now that CPM's 300+ branches form a nationwide network in Mcsico, the partners are positioned to connect their networks ac1:oss bordcrs. The regulatoty hurdlcs have been lug11 on the U.S. side, but ciuring the life of the program, WOCCU worlred with rcgulato~y officials and the Credit Union Service Coll>oration (CUSC) service provider in the Unitcd Statcs to lay the groundwork for: international shared branching wit11 Mcxico. WOCCU piloted the international conncction in 1':cuador (a dollarizcd economy) as a step in setting up the conncction with CPM."

The Outcome Over the past six ycars, CI'M has expc1:ienced remarkable growth of all key indicators. Growth of assets, loans, dcposits and membership has been exceptional, particularly in light of the fact that public confidence in thc crcdit uniotl sector had detc1:iorated duc to a few widely publicized fraud cases within the cqu scctor.

,I WOCCIJ worked with U.S, service providers and credit unions in Ecuador to establish the first international shared branching network in November 2007.

World Council of Credit Unions

Six Years of Growth at Caja Popular Mexicana

Inflniion

CI'M's ability to accumulate capital during this growth process is worth noting. illthough still short of the optimal level of 10% of assets and just short of the 5% goal set for the WOCCU pI:ogram, the leadership at CI'M now understands the importance o f building resewes and capitak~lng earnings to protect member savings and shares. CPM has overcome the old approach of maintaining loan loss reserves and capital accounts in zero. The institution is now fully provisioned according to international best practices (and the local law).

The sustained growth is itnprcssivc, but perhaps CPM's greatest achicvcment during this time has been the creation and disse~rination of a uniform strategic vision that is sharcd by the board of dxectors, senior managcmcnt and staff. The 3,700 employees of CPM now sharc a common vision, and a new sense of institutional pride permeates the organization. CI'M has eliminated many of the bureaucratic constraints that once fueled ctnplogec apathy. Institutional decision-malung has been strcatnhned, get the impo~:tance of input from members and staff has been maintained. Clear tiers of leadership ;low represent the interests of different branches and regions of the counuy. Some communities actually hold prc-ant~ual general tnectillgs in which up to 60% of the metnbersllip is reported to attend. Rcnewed member interest in CPM is especially saong in rural communities, where most members had no formal financial options before CPM arrived.

World Council of Credit Unions

Linking Branches with Information and Communications Technolo~ies

il benchmark in CIiM's transformation was the unification of the once vety fragmented network of branches. Branch coilsolidation was successfully accomplished (in part) through C;PM's adoption and use of WOCCU's PEARLS Monitoring System. 1'l'iillU.S created a common financial language for managers and staff, as well as a set of standards against which performance could be measured and evaluated. By the end of the sccolld year, most of the 325 branch offices were using the liEAIII,S Monitoring Spstein software, Individual branch managers reported feeling empowered and more capable of managing opei:ations, but headquarters managers still lacked information about what was happening in the branches. 'l'he branchcs rvere not online and daily 1:econcibation of thc information flowing from all the branches was virtually impossible.

The second benchmark in CI'M's collsolidation was the selection and installation of a single info1:mation and comtnunications technology. CI'M had struggled to link the branches with a single management information systetn since it was first created. In 1998, it purchased and installed software developed specifically for use by savings and loan u~stitutions called the 17tfoiv?a~ii/~ S is ten~at i~ada lie Scniicios dt A b o r r o j C~e'dilo or the ISSAC system. ISSAC was installed in about 20% of the branches before cointnunication and data accuracy problems and very slow proccssing times halted installation. i l s a result, many branches continued to operate using their own systems and wcrc unable to operate online, making dependable consolidated financial information impossible for C;PM to compile. CPM's headquarters in Ideon did not have a clear picture of individual branch performance, or cotlsolidated institutional performance as a result.

While the 26 regional offices continued to manage their own finances, they were beginning to use and apply the I'Ei\lU:,S standards. They hired staff and maintained their owl> salaq~ scales, ran their own marketing programs and developed sttmtegies and business plans as indcpendeilt operatioils. They did not entirely view thelnselves as part of a larger institution, and this led to inefficiencies, high operating costs and slow progress towards consolidation.

'l'hc sclectioll of a ne\v IT systeln was thorough, timc-consu~ning and inclusive, hut the result was worth the effort. CPM foi:med a 45-inember cotntnittee of staff from across the organization and undertook a r igo1.o~~ process to analyze tleeds and options for the new TI' system. WOCCU was a close advisor on the process and the partnership with the U.S, credit union leagues was particularly important during this period. CPM officials visited partner credit unions in California, Texas and North Carolina to analyze IT systcm options. IT experts also traveled from the U.S. to 1,con to help refine system requiremetlts and further support the evaluatioil process.

Today, CPM is operating as an integrated fu~ancial institution with a single IT system. ?'he r' '1ser.i. system was purchased and illstalled in 2006, and thc migration of the final group of CPM branchcs was coinplcted in 2007. rllmost immediately, the new systcm cnabled utliforln operations in the branches and quiclter product development and roll-out. Perhaps most important, CPM's management finally had daily access to all branch data, ~naking it easier and faster to monitor system performance, idcntifp problem branches and provide effective solutions.

' f i e introduction of standard operating policies and procedures was cased by having all branches online and, over time, CPA4 has seen a steady improvement in ope1:ating efficiency as measured by

World Council of Credit Unions

the ratio of operating costs to average assets. At 6.6%, CPM is one of the most efficient non-bank financial institutions in Mexico.

'The Fisetv system has also pesmittcd CI'M to add new programs for risk management, crcdit scoring and loan collections, as well as controls for money laundering. 11s a result, CI'M has been able to expand its linc of credit offerings. In 2008, CI'M plalls to develop a11 IYTM network, expand its line of credit products, introduce card scnrices and experiment with "virtual branches" using POS devices.

Strenetheninp CPM's Credit Svstems

In 2002, CPM did not possess a s)~stctnatic approach to CI-edit delively, and with the accclcration of new lending (i.e., 26% in 2003), a mix of problclns werc affecting poi:tfolio quality. 'The branches had thck own loan psoducts and credit procedures, intcrcst rates varied widely and capacity-to-pay analysis was not practiced in approving loans. Share lcvcragc (i.c., 2:l or 3:l) was bcing uscd to determine maxiinurn loan size and, in general, the quality of thc outstanding portfolio was poor.

Furthcrmorc, many CI'M branches wcre slow to collect delinquent accoutlts because loan tracking was not a high priority, and some managers viewed strict collection practices as bcing anti- cooperative. In 2002, only two individuals wcre specifically responsible for collections for the entire institution. In actual practice, many delinquent loans wcre classified as unrecoverable without any serious efforts being made to collect. CPM's portfolio at risk was 19% by the time the WOCCU program started, and reducing that rate was among the fu:st tasits of the technical assista~~ce team

During the fust ):car of the WOCCU program, CPM's rnallagclnellt illtroduccd ncw loall policies and procedures and trained headquarters staff to transfer those procedures to the branches. Loan application procedures werc streamlined, loan al~alysis and appi:oval c1:itel:ia wei:e tightened, and loan collection policies werc cnforccd. The result was a dramatic and steady reduction in loan dclinquency from 18.6% in 2001 to an acceptable 4.6% by June 2007.

World Council of Credit Unions

Loan Delinquency at Caja Popular Mexicana

Source: CPMfinancial data

New Product Development With the new crcdit standards and II' system, branches were operating in real time, and clear loan approval and collection policies were in place. CI'M began testing a new ]nix of loan products based upon a series of regional market assessments. One of the lnost popular new products developed was a line-of-credit offered to the "best" CI'M clients (i.c., those who saved regula1:ly and paid thek loans on-time). Both consumers and ent1:epi:eneurs were eligible for these credit lines, which established a ceiling on loan balances and permitted clients to withdraw funds at any time aud whenever they desired with tninitllal paper-ivork.

Other innovative products targeted the recipients of remittances, special purpose borrowers (e.g., immediate emergency loatis or vacation loatls for people traveling to the United States.), and members who wishcd to attract clients to their businesses by advertising in the branches (i.e., dentists, furniture makers, etc.).

An innovative rural outreach methodology was developed by a separate WOCCU program ill the State of Veracruz and pilot tested in three CPM branches. l h c methodolog):, called "Setnilla Cooperativa," takes financial selviccs to clients who live in remote communities, A crcdit union's field officer Q-avels to villages up to 30 kilolncters from the branch office, convenes a community meeting to introduce the group delivery methodology and helps potential clients to form groups of 10-30 people. 'l'he groups decide how often they will meet (usually once a month), and elect a president, secretsly and treasurer, each of whom help capture and verify loan application information and collect installments and savings deposits.

During periodic visits, crcdit union extension personnel disburse loans, collect loan payments as well as savings, cash checks and pt.ovide other transaction services for the people who live in those communities. It is a low cost, profitable way to bring financial selvices to people who have no access. While the field officers provide financial education on products of interest to clients, the lack of an obligatory education component has been cited repeatedly by clients as a benefit compared with other siluilar methodologies targeting low-income people in rural ai-cas.

World Council of Credit U~lions

Loan Interest Rates CPM is a highly competitive lender in Mexican markets. CPM's interest rates-averaging bchveen 20% and 24% annually o n a declining balance-are atnong the lowcst in the countt-y. CPM has been ablc to keep interest rates low by maintaining a high level of operating efficiency (opera&g costs equaled 6.6% of average assets it1 Tulle 2007) and by using inembcr deposits to finance its loan portfolio. Savings wcrc financing 85% of total assets in June with the reinainder being financed by retained earnings and member shares. T h e following tablc illustrates how CI'M's loan intcrest rates compare with other major financial institutions in Mexico.

Commercial Banks

Comparison of Annual Loan Rates in the Mexican Financial Sector

Finance Companies Commercial Stores

Annlnal interest

rate

Annual interest

rate

Annual interest

rate

I I I I I

CON SU I'h(iO 1 135% 1 CU.,\l.l.l S l~ l l \ l l ( : lO~ 1 69% 1 I~IIKNi>,\ OltO 1 138% 1

SOFOLES - non-deposit taking finance companies

l ~ l N ~ \ N ( : l l ~ I t ~ \ I\IS:,\N'L>\

~;ltl:l>l'l'~l l~ . \h~l l l . l~\ l t

The coinpetitivc loan intercst rates and the variety of new loan l~roducts arc fueling rapid gro\vt11 of Cl'IvI's loan portfolio. Loans outstanding grew by 28.4% in 2006 and the same o r a larger increase is expectcd in 2007.

SOPOMES - special purpose, non-deposit finance

431%

15 5%

Pawnshops companies

l~ltS(::YI>\

~ ~ l t l < i > I l ' l Z l ~ S ~ ~ l

85%

85%

l'lZl~Nl>~\hfl~X

l'ltl~Nll:\l~:\<~ll.

227%

218%

World Council of Credit Unions

Breakdown of Outstanding Loan Portfolio at Caja Popular Mexicana

in USD

Total

Distribution of loans outstandinr

Number of Loans % of Number of 1,oans Volume of

11 breakdown of CPM's loan portfolio illustrates that CI'M selves a wide variety of bon:owers, with a focus on small borrowers. In June 2007, 34% of the loans outstailding ( U S 5 3 million) were for amounts below $500, and 66% of loans (1JSS206 million) were for amounts less than $1,400.

$10 - 500

Marketing and Member Services

242,256

33.7%

millions)

Membership growth is a direct result of CPM's increased ability to attsact new tnetnbers and deliver products and services that lead to greater member satisfaction.

8 0 % of 1,oan

\'olume

When the WOCCU technical assistatlce program began, CI'M's marketing department was srnall with very few resources selative to the size of the institution. 'l'hc department's focus was the organization of annual tneetings and a few small, rudimental-y campaigns (although national marketing in the cqfl sector had been outlawed after the fraud cases). Before launching the national marketing stsategg, CPM did not possess a unique institutioilal image and there was little name recognition among existing and potential members.

$10,000 + $500 - 1,400

231,694

32.2%

100%

WOCCU staff worked with CPM staff to d e v c l o ~ a national marlteti~lg plan that created consistent branding throughout the branch network and was ticd closely to the busitless plan. 'l'he marketing department at headquarters now oversees all publicity and proinotion initiatives and disburses marketing materials to every branch.

5.0%

Today, one cannot pass through parts of Mesico without a billboard beckoning them to C:PM. Thc credit union's green stamp is unmistakable-cvc~?, branch, every sign, every passbook, every employee and even the CPM-sponsored soccer team casry the same look.

$1,401 - 5,000

214,015

29.8%

O n e component of the national strategy has been market sesearch. CI'M members are diverse in their need for and use of financial services. The primary goal of the new marketing plan was to accentuate that CPM would takc care of all of any person's financial needs. 11s the graph below dcmonstsates, CPM is reaching a broad base of clicnts.

$5,000 -10,000

19.3%

26,762

3.7%

50.8%

4,644

0.7%

17.0%

719,371

100%

World Council of Credit Unions

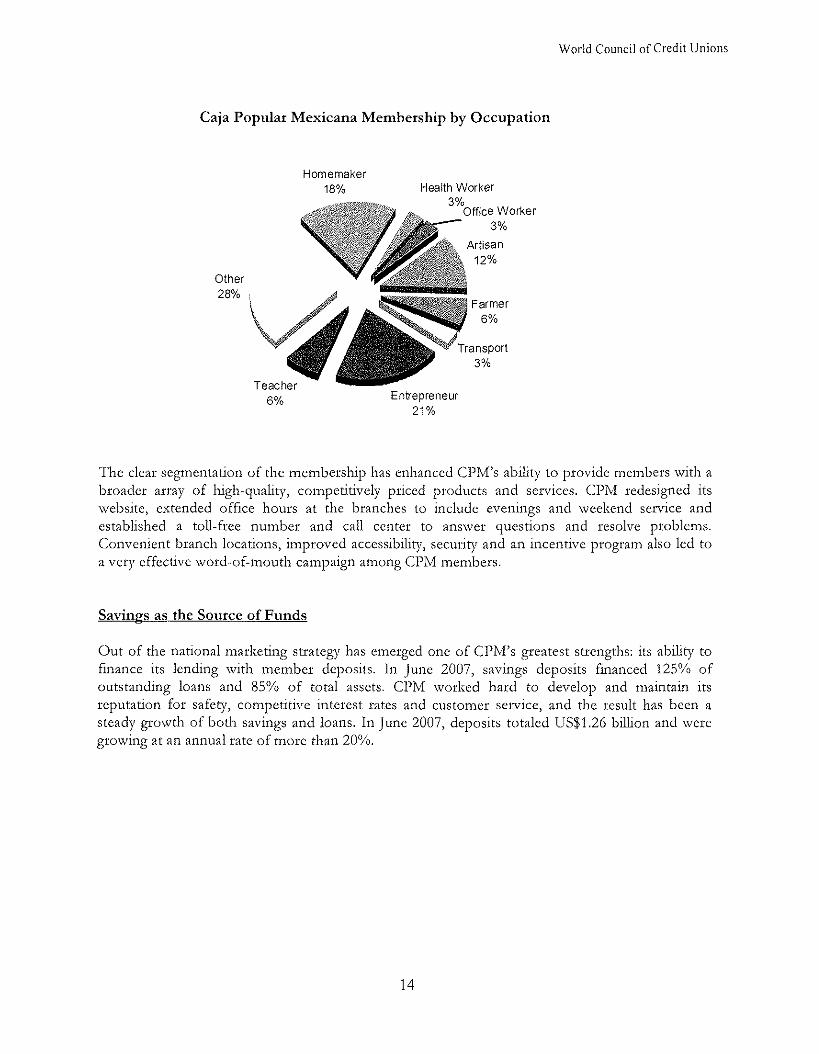

Caja Popular Mexicana Membership by Occupation

Homemaker 18% Health Worker

Other 28% ;

'The clear scgmcntation of the membership has enhanced CI'M's ability to provide tnclnbers with a broader array of high-quality, competitively priced pl.oducts and scrviccs. CI'M redesigned its website, extended officc hours at the branchcs to include evenings and wccltend service and established a toll-free numbel: and call ccntcr to answer questions and resolve problems. Convenient branch locations, improved acccssibiliq, secui:ity and an incentive progratn also led to a very effcctivc word-of-tnoutli campaign atnong CI'M metnbess.

Savin~s as the Sourcc of Funds

Out of the national marketing strategy bas ctnesgcd one of CPM's greatest stscngths: its ability to finance its lending with tne~nbcr deposits. In JUIIC 2007, savings deposits filialiced 125% of outstanding loans and 85% of total assets. CI'M worked hard to develop and maintain its reputation for safety, competitive intercst rates and customcr service, and the rcsult has been a steady growth of both savings and loans. 111 June 2007, deposits totaled LISS1.26 billion and wcrc growing at an annual rate of Inore than 20%.

World Council of Credit Unions

Savings and Loan Growth a t Caja Popular Mcxicana

Loans Savings

Remittances

CPM began distributing reinittanccs on a pilot basis in August 2003, expanding distribution to all branches by Noveinbex of that year. By September 2007, CPM was averaging 25,800 remittance transfers a month, with a total of US$90.5 million being txansferred in 2007 t11i:ough Septeinber. The greatest voluine of reinittances comes froin California, North Carolina, Texas and Georgia, states with large populations of Mexican iminigrants. Wotncn represent the ovc~lvhelming tnajority (90%) of remittance recipients, Inany of them are Cl'hf members.

CPM Remittance Transactions and Volume

World Council of Credit Unions

Non-members are permitted to receive remittance txansfefs in CI'M branches because they add to the visibility of CPM in the local cotnmunity and they rcprcsent a source of future business. Branch staff members (particularly tellers) arc trained to encourage non-member r e ~ ~ t t a n c e recipients to join by opening a savings account. They promote savings as the doorway to the full range of financial setvices that arc available.

Remittances are now considered by CI'M as a sourcc of incotnc when determining a clicnt's capacity to pay in loan applications. Experience suggests this practice has pernutted some lnembcrs to qualify for larger loans without excessively increasing the risk of default. Protnotitlg savings has also hclped CPM clients make more productive use of the money they receive (e.g., accutnulating savings to provide a down payment on the putchase of a home or a parcel of land).

Challen~es for the Future

CI'M has made remarkable progress over the past six years. It has successfully consolidated the operations of hundreds of once independent branches into one well-run financial institution. It is truly a success story, and the results are telling. CI'M is profitable and growing at more than 2I0/u annually, and it is providing high-quality, cotnpetitively priced financial sct-vices to over 1.2 iniliio~l Mexican people, with 14,000 new members joining each month.

CPM leaders and management havc no intention of slowing down, but the road ahead is liltcly to be challenging, and there remain some specific challenges to be o\rcrcome:

Managing growth and remaining competitive. The tapid expansion of C:PM and the sheer size of the institution will requke close and very regular monitoring, as well as clear communication between the board, headquarters staff and branch tnanagcrs to maintain CIJM's ability to respond effectively, quickly and uniformly to the changng delnands of the market.

Maintaining financial discipline. Over the past foul: and a half years, CI'M wrote off US81 1.9 tnillion in accu~nulated losses, retained another US821.4 tnillion in capital reselves and attained a capital-to-assct ratio of 3.3% while paying competiti\~c rates on savings and charging vet11 competitive ratcs on loans. Continued financial discipline will be needed to enable CIJM to reach the ideal 10% capital ratio as recotnmcnded by WOCCU.

Institutionalizing the change. CPM is a very 1a1:ge institution with aggressive growth plans. 11s new policies are put into place and products released, CPM will need to make active use of the internal training capacity it has developed to ensure that all ctnployees understand and elnbracc the changes.

Regulation. CPM has transformed itself into a robust financial institution, but maintaini~lg equilibrium bcnveen regulatory adherence and sen~ice to the poor may prove to be its greatest challenge yet. For example, the government has tightened the rules surrounding the opening of fixed branclles, now requiring the same level of construction and internal security that is required of branches in urban locales. CPM management expects these new

World Council of Credit Unions

rules to limit its ability to open new branches in rural communities, and it hopes to develop "virtual branches" as an alternative.

Faster credit delivery. Cl'M's crcdit delivery system is much more efficient than it used to be, but there is sull room for improvement. ?Today, when a inembet: applies fot: a frst-time loan, the wait time is approxinlately five days, a long time for someone in need of quick financing. CPM is exploring ways to strcainlinc credit alq~roval without losing the level of control and risk inanagement it has achieved.

Maintaining internal controls and efficiency. Many branch staff perforin multiple roles such as promoting the credit products, analyzing loan applications and collecting loans. 'l'his practice helps keep the costs down, but it also represents a potcntial conflict of interest. CI'hl will need to reallocate some functions in the bt:anches; and it is also cxploring expanded use of credt scoring and other tools to further standardize and speed up the loan approval process and help members build credit histories.

New products and new markets. CI'M's lnaritet is becoming increasingly cotnpetitive as new entrants (such as international banks and banlis that have grown out of local retailers and microfinance institutions) begin to offer competitively priced products to traditional credit union clients. Competition could become particularly stiff in the middle-income markets where individuals seek convenience as well as low price.

CPIvI intends to confrout the competition by developing card services, iYT'Ms and online banking. None of this was possible before the consolidation of CPM's financial performance and the conversion to a new IT system. Now the stage is set and CPM is ready. WOCCU technicians helped CIIM to conduct a market study on card senlice options in Mexico, develop a business plan for card seivices, create policies and procedures for cards and open negotiations with major card sclvicc providers. Cl'M is now awaiting authorization to offer meinhers electronic paginent services and long-term loans. Once approved, CPM will be the fust crcdit union in Mexico to offer online banlung and credit cards.

In the short term, CPM is einploying technology to increase dclivcq~ of financial services to rural areas, a vast market that is still largely untouched.

Today C1)M is a v e q competitive institution, and there is little idtclil~ood it will be undersold any time soon in Mexico's financial markets. However, in order to maintain its coinpetitioe position, CI'M needs to remain vigilant in its financial management as it continues to develop and refine products and se~vices that will attract new mcinbers and increase member satisfaction and loyalty

In 2008, the partnership between CI'M and WOCCU will continue for an additional t1it:ee years, this tiine with financing from the Mexican Minist.1-y of ligriculture and liural I>evelopment (SI~GI\IZI)I\). WOCCU was selected by SAG11111'11 to strengthen the operations and enhance of ability of financial cooperatives to provide services to rural coininunities. Building on the success of the past six years, WOCCU will work with CPM to expand the i~nple~nentation of the "Se~nilla

World Council of Credit Unions

Cooperativan methodology, as well as experiment with the creation of "virtual bcancllcs" using 1'0s devices and other IT solutions to extend its outreach to morc remote communities.

Attachment

PEARLS Report 2002-2007

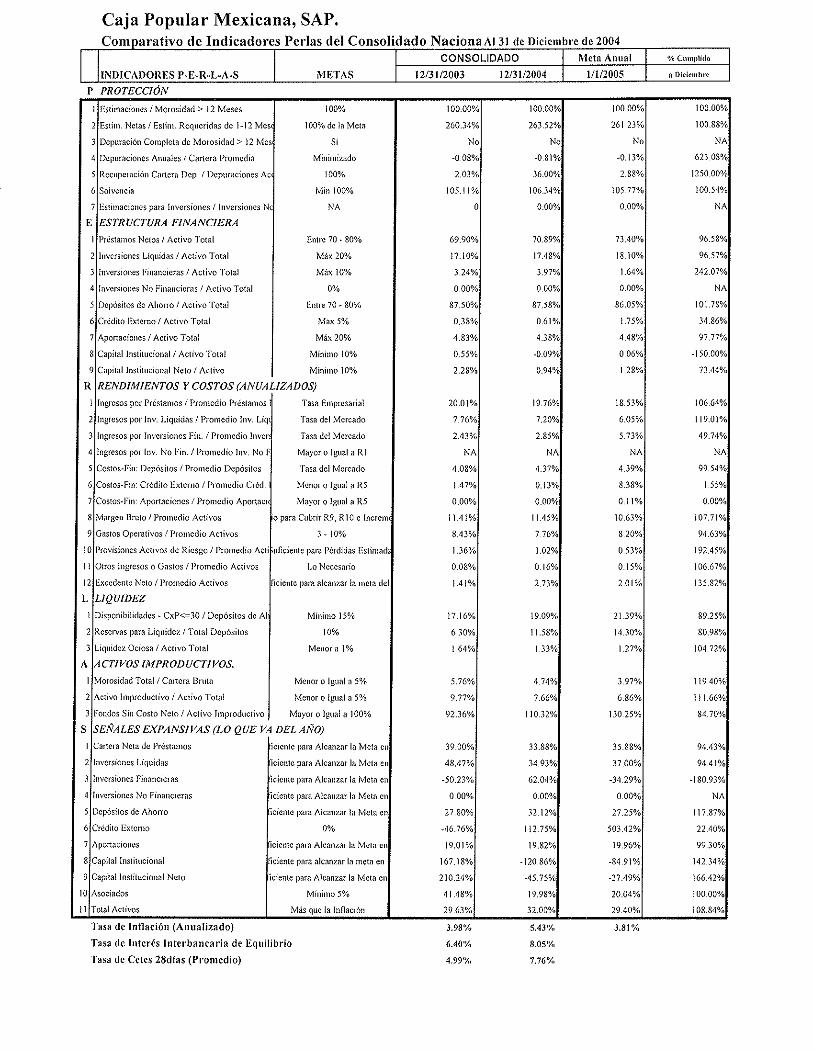

Caja Popular Mexicana, SAP. Comparativo de lndicadores Perlas del Consolidado Nacional Al 31 de Diciembre de 2002

I

<2 41 ' .

S.fc enlc para .' canzar a lAeia c.r, E 4

INDICADORES P-E-R-L-A-S P PROTECCI~N

METAS

10 11

12/31/2002

Asociados -~p~~ .. . ~ .~ .--- ~ ~ ~ ~ p - ~ ~ ~ ~. .. Total Activos

Minimo 5% ~ ~ ~~~ .

Mas que la lnflacion

49.44% 24.53%

Caja Popular Mexicana, SA Cornparativo de lndicadores Perlas del Consolidado Nacional

T a s a d e Istelx!s I n t c r b n n c a r i a de E q s i l i b r i o

'l'asa d c Cc tcs 2 8 d i a s ( I ' romcd io )

I I

I N U I C A D O R E S P-E-It-1,-A-S Dec-02 M K I ' A S

l'asa d c l n f l a c i 6 e ( A s a a l i z a d o ) 5.70'%, 3.98%

Tolnl Act iws

Dec-03 I

10000%

243.41%

N o

-0.08%

2.03%

104.81%

N A

70.44%

1728%

3 38%

0 0 0 %

87.88%

0 38%

4.85%

0 5 5 %

2.10%

20.00%

7.67%

2.66%

N A

409%

1.22%

0 0 0 %

1 1.46%

8.47%

1.13%

-028%

1.30%

17.54%

6.30%

159%

5.71%

891%

94.83%

39 49%

49.36%

-48.30%

000%

27.79%

4 6 5 6 %

1901%

167.18%

185.34%

41.48%

M6, que la l#~llaeiO#l 2451% I

100 00%

278 11%

N o

1.73%

0

104 39%

0

65 18%

14.93%

8 43%

0.00%

88.76%

0 92%

5.26%

-105%

0.95%

22.35%

8.43%

185%

N A

4.23%

000%

000%

12.42%

10 40%

0 59%

0.32%

171%

17 27%

-051%

1.74%

5.97%

11.46%

61.67%

37.13%

-18.60%

-4.22%

0 00%

24 13%

100.00%

1838%

42.41%

162.54%

49.44%

29.07%

100%

100% de In Mela

Si

Mi~l is i i rado

100%

M81l 100%

N A

Ealic 70 - 80%

MIX 20%

MAX 10%

0%

Entle 70 - 80%

Man 5%

Mdr 20%

Miii88llo 10%

Mirl imo 10%

Tasa l:n~prernrial

Tasu dcl Meicado

Tara del Morcado

M a y a i o lgual s R I

Tasa del Meicado

Meiior o lgibal a R5

Mayor o lgllal s R5

1.0 Neccsrrio para Cubiir 119. 1110 c liiclelllcnlal CspiInl

3.10%

SiiRcienre par;, Penlidas Esliizirdas

1.0 Nccesaiio

Seficic81te pnra alcaszai la ~nletn del E8

Mi i i i l l io 15%

10%

Meaor a 1%

Meiior o lgiinl a 5%

Mei io i o lgiisl a 5%

Mayor o lgtlal a 100%

Siificicstc para AIC~IIZPI la Mcta CII E l

Silliciellle para A l c a i ~ r a i la Mcla eii E2

Sllficiciae para Alcallrai la Mcta co E l

Se(icio8llc para Alcasrar la Meia a, i i4

St8ficieste para Alcarllar la Meta ei l C5

0%

S&ificicsle /para AICBI~ZBI la Meta ca E7

Siificiente pain alcantar la cmcta cn E8

Sllficiciite para A lca~ l rv i la Mcla cs 1:9

Minitno 5%

P

I

2

3

4

5

6

7

E

I

2

3

4

5

6

7

8

9

R

I

2

3

4

5

6

7

8

9

10

1 I

12

L

I

2

3

A

I

2

3

s I

2

3

4

5

6

7

8

9

10

P R O T E C C ~ N

Estitnac8oiics / Movosidad > 12 Meaer

Cstiln Nclar I Esti#l>. R~q i>c i ida r de 1-12 Merer

DcpiiraciOl? Cornpiela dc Moiosidad > I 2 Merer

Dept~ivciones Anlialcs I Canera IVioaedU

ReeapeirciOa Cartern Dep, I Deji~~rac8oiici Acciiiil.

Sol\,cncia

listiinaciosles para l ~ ~ v c r r i o ~ ~ e s 1 iliverrioses N o Kegitladas

ESTRUCTURA FINANCIERA

Prestaeos News I A c l i v o Total

l~iversiones 1.igaidns / Aclivo Tola1

liiveisiones l:i#lancicrar I Activo 'Sotnl

lc~verrioner N o l'iiiancieiai / Ac f i~ lo Total

Dcpbrilos de Al iono 1 Aclivo Total

Crddito Extcnlo I A c l i v o Total

A p ~ l l a ~ i o l i ~ ~ I Aclivo Tala1

Capital Ilistitacioilal 1 Activo 'Solal

Capital l i~slit leiol lal Neto / Activo

RENDIMIENTOS Y COSTOS (ANUALIZADOS)

litgiesos por PrOslaii>os / I'roincdia PrLstiinos Nctos

lltgieros por l r l v Liqc~idar / Pioincdio l i i v 1.iqiiidas

liigresos 1'0' 181vcrsiorles F81i I l'ro8t~edio 11we8riotier I2iii.

lngiesos ],or In". N o Fin IPro~nedio 1s". N o F i n

Cosios-Fin Depdsitos / I'roiiicdio DepOsilos

Coslos-Fin C l ld i to 1:xlomo / Proaedlo Cred Eslcnlo

Coilor-Fw: Aponacioner / l'roii~edio Aponacioaes

Margel, Rnlio / Proiriedio Aclivos

Carlos Opeislivos I Pionledio Aclivos

Piovirioi>es Aclivos de 11ieigo 1 I'ioa~cdio Aclivos

Olios 18tgiesos o Gaslosi Pro~tiedio Aclivor

Excedellie Neto 1 l 'ioo~cdio Activos

LIQUIDEZ

Diq,oiiibilidadcs - Cxl'c=30 I DepO~ifos dc Aliono

Keicrvar para Liqii ider I T a i a l DepOrilor

Liqisidcr Ociora / Aciivo Tolal

ACTIVOS IMPRODUCTIVOS.

Morosidad Tola1 I Carlciit Hnllir

Aclivo IIII~~OLIUC~~VO I Activo 'Total

Folidos Sin Coslo N c l o l Actlvo l l~ lp io l l~ l c l i vo

SEIVALES EXPANSIVAS (LO QUE VA DEL AIVO)

Canera Neta dc l'r4rlainor

l# i~,c is io~le i 1.iqaidar

l i ivcrrloiar f'isascierar

lclversiollei N o 1:ioascieras

Degbsitos rlc A l l o m

ClCdilo Exlenio

Apo#lacio#t~b

Capital l~, r i i t t#eio~~ai

Caliilal liiililacioiial Nelo

Asoeiadoi

Caja Popular Mexicana, SAP. Estado de Resultados En Base a la Moncda Local

N -

YP

-m

-P

N

UP

"

Y

0 -

- -

w

,

- *

- N

-a

.-

-"

pp

*

:y

, -"'

-"

-

"Z

<X

;"

"

Y"

.:

!, b

c.

2&

;k

+

&

.L. -

h o

~z

~.

z.

;~

;~

$

Zg

XN

48

-

,,

w-

O-

k~

CZ

O

,U

__

ao

ao

_

- -e

g

2 L

SS

SS

S~

S~

SS

sss S

~S

ssrrsrss>xss axsssssrs ,ss~gZ

- a""

- -

- -

- -

- 4

- t

.,

"

""

""

"X

Z'

=

Y;

,,

,-

=

;.a

-

-

-k

g

NO

--

-

.,

--

-a

2

2;

-

?*

z

e;

"s

og

.2

z

PB

X&

,

yo

,

- Z =

mU

c.

NU

wO

AY

m

w-

x ,,,

wc

.N

,U

,,

,z

~~

~

,,

,a

zz

rm

U

LZSSXSSSSXS LSX SSS SSSSSSSS>SSX SSLSSSSIS SSSSzz

, ,

U

- U

NN

,-

"w

i""

"

- N

-

- ,

- .,

- " w

og

~A

yy

~o

a.

-~

o

wo

m

"

-2

2

Z2

Z

Z2

zx

~4

+

,w

o-

-

en

-n

-

-u

o

-~

b "

u

.- 4

:

A-

z*

NU

O,

a"

-

-4

.,"a

-

A

"4

"-

N

W

~o

u-

,U

z,

sa

-

s$

28

z%

s,

A,,,

ps*sss+sSsS SSS sss SSssssSs"sSs SsSsSssss sssszz

--

--

-

- -

- -

- -

- -

- -

- -

N

- U

2

-D

,

W

- ,a

- =

"-

Pa

w-

"

U*

"

--

o

m,

"

"U

p"

"

""

""

""

"

22

y

x"!

=.E

,

gz

0y

g-

*

"0

,

uX

SY

O

- ---

.- ?

X2

E

8 E

P$

Xk

2S

zS

-,

0

-0

N

-u

8-

W

L" A

Z2

PE

%

OZ

kZ

~Q

Zz

z

18

Zz

Z

s~

~r

~s

sr

~s

~

sss s

~s

~2SS2S2s>sss sxssr>sss >SSSX-S

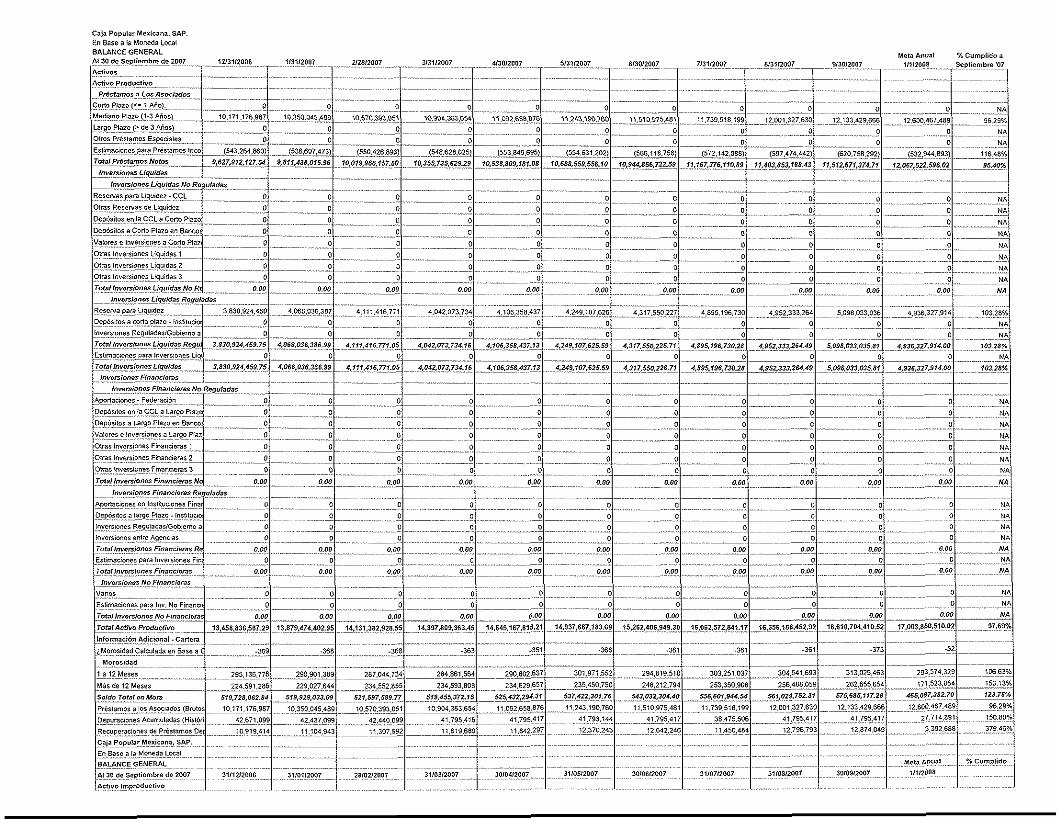

Caja Po[,ulnr Merieaea, SAP. En Unic a In Moned~ Lorn1

BALANCE GENERAL At31 de Dirieniblr i le2001

Aclivos AcLiro Proilh~cLivo

Prz.', r,,, ,r,r,, ,.ur"r"cii,,l,,,~ can0 Piria(r- 1 *:o1 M~dnnoPla,a(i-I Ailoil

Lorso ?lamP dc 1 hior) Olrai P,eiis#llni 61hxialc1

~ ~ ~ t ~ n ~ ~ c # o ~ e ~ oar0 Pr&4a,><o% $htebrabIes

IY,"lR*,"n,vt **,or

,,,ve,.,?",,e, ,.~,(,,!,,,,, ,,,~~~,,~O,,~S,.,",,~d,,,*~,,R<~',,",,"~

Rcrinn or,. Lqliider - CCI. Olrrl Rer~nurdi Linllid~l "cpbilL.8 <" i3CCL" c0.o Pirm

D ~ ~ b l l D l a Cone P I ~ , o ~ I I Ulii<coi

\'#lore, e i",eicion"i r "orla PiilD

Oilrl IIIIE.I.I,E, I.iUilldd. , O l i r i i n i i r i i a n t i Liqltldai 1 o,,ms ,"v"s,O"CS ,.;,t,i*>z 3

Ir*nlh,o.rin,i#., ,.qni""r,"o ,l<f,,i",,"" ,,,ir,'~",,c-,.,"""ln,Rr~,,,"d".

RIIt"8 prrr Llqliidci

Dipblllo, a ion0 plr,o - lilrllilicloilcr RCgil3d..

im~nioner R~glildrriCabicmorrono~lr,a

~O,",,,,~.~,.~~",>~S,.,~,,~<,,~S~~~,,,"~",

crllnsi,ollrr *ro i " lCrn0n~i i iquldoi TWO ,,,, ,.<,,,m,<., ,,,",,!,,",

bi.ersnnle8 Ein",,eiiiiii ,,,1.z,,io,,n Fiiia,,"rra.7N,N no#",",,,,,

*yo"rc,o,lcI - Fcdcilridn

i>cpbriloi en $2 CCI.0 h r c o Piwa D~obll lol . L,-,reo PinioPn "l"i9,

""!or<s 0 l ~ t ~ ~ ! ~ ~ ~ ~ > ~ s a br80 ? t a m

otrrr im.rnon.r Fi.n.l.rri I Oii", i n i ~ n , ~ n F r F,"ii,r,"ri 2

Olmi IniSolot3ei Fmmcltrn 1

~,","!D,,rr*i",,e., l innnlirr"~ NNN nr~r,ia,,#r

b,rr.i,>,irs Wf,,iiirm, n~.,",,", A"~"oc,o"~,e" , , , , , > , , , C , ~ " C ~ r,"a"c,cr"s

DEDOI~~OI i lii80 Plnlo- i".iilllti01%~1 HED'lld.i

llliemlonri R~golrd.ilG.bl.m~r irlgopb,. Ini*rriollrrclllrFAg.>rii,

TdniL,~r,.,in,irr ?~j,,a,i<j<,n'n<~ ,,,,,,,,, r u,,mac,o,,e, ,"VC,~,O,,t$ F;"a,,c,cra9

li,,,ih".~rtiO,,rrF!,,n,,cij.,"> h,rrrrio,,csNo na,,r,ri .,,a c

vanor E3,:,,,a',o"c, pa," ,"v MO F,,!o,,c;c,~, Ih lnl l r i r r r lnnrr N" t~~, ,n , i r ieml

Toml Acrivo Proilr,crivo lnrornlnridn Adicionnl - Cnrterll

,.hl~lorld:dCrirllirdr cn " l i e r cancr. Alk iadi"

Mllrniildil

i 8 l i MElC8

hWidF i i M E I C I

.S",d,,)i,#,,,l,,* l,,,,, Pr6slrnloi # t o $ Arothdoi (Bnroi l D~pvrrrioncr iiriinlvlrOss (lilnbiirri)

Ktcii*,rt,onti dC I'rciin,,or Deparrdoi (l i ,rio,an

Caja Papular Meriennn, SAP. l i t7 l i i i a a IhLlor"dnl.ocr1

BALANCE GENERAL A l l , de Agoslo 2004 Acliva i.l"rod,,ctiro "',!,,,,., ,,, ,,,, t,,".,

cur CutnlrCoirirnli(Ci,rq."nI

h<oncdr E\,rni,Eir

Rrrrnli psra I.iqrdi,. - CCL oirri Rirrriri d* L,q.ldo OliOi AC<iio, I.iqrdo'

,'#,alAc,lmr li",,i,,", Li,enW'J,,,,Cohr.r

DcudorEI

Il,lC,t,ti "0, COblU

"mu,"ei,,o* BoiCobrrr

D~duielot! d ~ P l a i l l l i l p o i C ~ b r l l

O,r.iCaci,,.i purcvbrri

Lri,i,iriioari p,rCliri,,r, ,"to,,

Cliniialpur <.',,b,,,,

nciix.,jr rgor

Tenma

Edlll~lOI",~,,",

Inmlriioilcr hnendrdir

Mlicbicr ) i ~ l l , p o

OGP>~tOL,6,> Ac,t,,,t>lad~. Edtfic,o,

"c"r'<,oc,">, Ac,>m,t,,,"da- !,,8,8,8C,O,,~3

Oqx~ti i t iOl l hellillul.d8 - MlltbIc~) Equip0

Tiiuinbcbln rln,.n..bi,~.,,v..,,'

0,ror Acirvoz

Blinrr m ,.i~,i>drc,6" Giitoi dc Or~mmi i6 " G"sLo, A>,#,C~,>O~O, 08r.i *rliior "irnldar htlinnimcioner Act11111111Bs

IY,oi,,,ru.r,,cti,,,r

,,c,i,~"'Pr,,,,,c,,,,!,;'.,,<

Ai i i .O* dr. ">,or Dlldalo

Dirri~nrnila Conlrblr. hi,,>.,

alms hC,,..i Prob,cn>~,..,

Yiublm, Aimis Aiionn.ai

%il,A'b,.", R"h,midLor

Tolnl Ac8ivan No. dc Anxisc$ssm lil CAC

Hal>!brei Muierer Gdiiaro no Rc,,anado w,im..,m Ibi,,l"ei(m"",,"'

N~I I IE~, , tdc oti~s usitnr)<,s nr smakir lnfnnloiuvellil reiceroi mi",'.,<, ilro<rvr "rln,;~rilr.Prr,~ii"rdr,o W<

Il,li,lN4",cn,,lr*I,xi;ids,, OlrllrUrurn ,,,,I e

C ~ j n Popular Mexierrla, St\13. !!" ,%ns" 8 la M0,,*<i% Local

BALANCE GENI<HAL A131 de Agortode 2001 PnSlYOS PASIVOS CON COSIO

I>~,,,l.,ii"r de ,,,,",,a *hoii.C~.ic,,i"

DEIIUIIID 8 Piria PbO ALO"0 i,,Li,oi.~enii hiioilol Pragrlillada#Olro Ahoiia

AIlo"oObi5galono

r,~!",,><~,;"i,"..,Jc",,",,t, Crddilllo Erremo

Crtdllo E ~ l r n o - CCI. C= i M o l

Credllo E\lcmo - CCI. P i hila) Ciidilo E\,E,,,~. "lnro.

oiioi c , r d , , ~ ~ ~~t~~~~ - Piirm,l,oi c n r " Agrnii..

TC,,,~ c,<";,<, Z~,<,,I" loll brim?, Con Cuilo

Parivor sin carto C,l.tii.r nor Prerr (c-3" Din,, Pow:or dr C r i d 7 , E%i?n$o(c-30 Dir i l

Y,oi>r ionei lc j Prrr,.?,oi,e,l

Dlrri~pillilnColllrblr-Prri~ai

0,ror Poshor li,"lp"ri,", ,sir, C,,.,"

T<,,"l P<<s~,,,,.Y CAPI'I'AI.

","rri.io,,ar

An~""ri"rr Obil~n.,,n hPO"><,O,,C, "o,,,,>,ac>s~

TO,", cop;,,?, ,,c ,"**A"cro,,"a

(IIWI lin,lri,"no R c ~ v ~ l i r c i b n

R l r e n r i rdrro,i..r, suri.,er REIEW.T h.loaElllr,Tr

Oilr i Krlrnnr U,icrcomrir Coilable. Crn#l8l

E\'ed"n,.r ,lo, *pi,c.,

E ~ ~ c ~ ~ C 8 7 8 c lP6r,li~d8# Xet,,<fcl ,<~,tlAcrs~:%~

T<>!,2,S,,,>!,<,, r,,?,,\l,r,,;,> CCC,I~,,,~ nemucio,,,,,

Xcrcn. ircri

RErmm I"<,>l",biE

oirrs Rrrcnar Donrnonii P i i d i d l i por Apll'a,

T\<E"C"IEI (Ytrditlnildrl .\LoporCi9,riiml

lorn, C",,i,"i,,,r,;,,,~io~,~,

7-,l,"i crrj>i,al T O L l l Pnriror ). Cnpilal

Caja Popular Mexicans, SAP. Estado de Resultados En Base a la Monedii Local Del01 de Enero a131 de Dicien~bre de 2004

INGRESOS INGRESOS 1'011 I ' I~~SI 'AMOS

lntereses Sobre Prestamos Recargos por Mora Comisioncs Sobrc Prcsiamos Prima de Seguros Sobrc PrCstamos INCRESOS NETOS DE PRZSTAMOS

lngresos por Invcrsiooes Liquidas Ingresos por Inversiones 1:inancieras Ingresos por lnversiones No Financieras Ingresos pol. Donaciones lngresos por Otras 1:oentes Total Ingreso Br14lo

COSTOSIGASTOS COSTOS FINANCIEROS

Intcreses Sobre Depdsiios de Al,oiro Seguros para Ahorros lmpl~estos Sobl-e lntereses I'agados Coslo 17iiimtciero - Depdsilos de Ahowo Costo Finaociero Sobre Credit0 lixterno Costos Financie1.o~ sobre Prestamos entre Agencias Intereses Sobre Aportaciones Scguros para Aportaciones Impuestos poi lnlereses Pagados sobre Aportaciones Coslo F' ino~lciero - Apo~lncio,,es Otros Costos Financieros TOTAL COSTOS FINANClEROS MARCEN BRUT0

(XS1'OS OPERATIVOS I'ersonai Gobernabilidad Mercadco AdministraciOt1 Depreciacidn TOTAL CASrOS OPEI1ATlVOS

ProvisiOn para Activos de Iliesgo UTILIDAD DE OPERACIONES

O'I'ROS INGRCSOS IGASI'OS Ajustcs de ARos Anteriorcs (Neto) Extraordinarios (Neto) TOTAL OTROSINGRESOS/GASTOS

lmpuestos Res~~ltados del Ejercicio

hlcta Alnml 11112005

Caja Popular Mexicans, SAP.

Comparative de lndicadores Perlas del Consolidado Nacional

A1 30 de Septiembre de 2007

CONSOLIDADO I I I I I I Meta ~ n u a b Cumplido a INDICADORES P-E-R-L-A-S METAS 1213112006 1 113112007 1 212812007 1 313112007 [413012007 15131120071 613012007) 713112007 1 813112007 1 913012007 1 11112008 leptiembre'07

P PROTECC~ON

TRUCTURA FINANCIERA

TlVOS IMPRO ~-~~.. .,

Tasa de lnflaci6n (Anualizado) 4.05% 3.98% 4.11% 4.21% 3.99% 3.95% 3.98% 4.14% 4.03% 7.23% 3.95%

Tasa de Inter6s lnterbancaria de Equilibria 7.34% 7.41% 7.43% 7.45% 7.46% 7.70% 7.70% 7.70% 7.71% 7.74%

Tasa de Cetes 28 dias (Promedio) 7.04% 7.04% 7.08% 7.03% 7.00% 7.24% 7.20% 7.19% 7.20% 7.23%

...~. .. . .. ~~ ~~ ~ ~~~~

onl~npalaull tinluv ~ ~ . , . . . .

~~ ~~~~~~~~ ~ . . - ~~ ~~ .. aGs 'cuo!xow,l.,"dod ~1~3

-- Yew YO ,0291 OPlDS

~ ~ ~

..p$n6a8swnb!7 ~UOIIIIII~~

~~~ ~-~~~~~~

soou,~cE ~ . , -~ --.-

' OP!ldlu"J % jenvv claw 100~ op wqru.!sdas op oc $i(

7m3N3333NV7VB

Caja Popular Mexicans, SAP. Estado de Resultados En Base a la Moneda Local Del 01 de Enero a130 de Septiambre de 2007

I!nsres05po~l~~~~~~l...- 0 l ~ L 01 - - 01 . . ~i 01 I . . . . . 01 I . . . 0 1 - 4 NAI

COSTOS FiNANClEROS

Seguros p a a Aportacion

TOTAL COSTOSFINA 645,929,339

1,426,147.066 ~ ~

~ ~~

~ ~ . . 509.278.?4_4 rj Meicadeo ~~~~~~~~~~ ~ - ~ 54.381.981 13,153,537

Administracibn . . 289,199.342 ~

60,256,832 DePr-iaubn .. .

TOTAL GASTOS OPE 9236.917 Piovisibn para Anivos d 91,921,182 ..

.UTILlDAD D E OPE-ZC, 407,955957

62,220,358 122,918,683

153,595,254 255,599,086 ---- ~..

..

1?.055:L?? -a5:7Q'L'O?

- 3.545.263 . 896.055 ~ 1 ~~ 6.972.022 1.833.698 ~~

-- 18,726,736 ~~ ~~~ 46.780.232

4,986,517 _ 10,256,826

65.2579.5302 151,550,478

(3.029.800) 8.957.076

71!41_5,852 95!!?2>532

186,991,051 -248302!637 3<5256,625 360,193,088

398,704,236 53SSi53!Jj1._691,5553,059 , , ~~~ ~.

~~ ~~ ~~ ~~~

191,389,562 243,665,387 231,265,486 166.?!0.393 10.250.073 ~ 2,587,053 1 - . 15.887.806 3,556,648 1 ~~ ~~~ 22296 .352 4 4,544,815 -2264316 5.634.163 -

~ ---- 71.857.436 ~ 95,400,399 119.047.162 . 143.549.917

15,733,198 20,988,7D, ,-_?6.261.137 31,689,223

246,738,152 37,_0z5LTP0 .4_16,174,853 499,/!3,106

7.283.216 15.60- -.~,?8_623,631 30.514.892

!M,682,867 . ?q6!5?*17 156,!!383 .~-315,24?055

430,205,f~O 04,262,777 575,722,289 660,327,410_--8/.!9%

s_45.340,052,99$,914,754 , , 1,152,251,129 2,3?0398,093!.8231210,2562/.

-~~ ~ ~ . ~~ ~~ .. 342,193,319 409.844.127 460.060.232 599.701.558 7671% . . . . .

-32-345632 6,747,068 1 . 3853239 8.068.040 4 , a3797.009 j 8,931,456 ' 3 .642 .316 544469698_2 1 65.4\ 6793% -~

~~ 166.i15.380 200.163.229 2 3 0 . 6 1 2 . 5 8 6 3 8 8 3 7 6 : ~ 2 2929%

37.685.962 3479 .166 49,250,051 67,181,256 73.311/a

,.,5835'8I.36!, _ 700,089.822 ._.79265!C?!! x 3 2 ? 3 ; 1 6 3 .....6?go.?-

-375995,962 65533553Z_3J1319 2 . 9 4 2 . 6 2 4 _..-_5?1??%P_?!?? 1 7 5 8 8 % ~

_.37'~231,43! . 386!H25,978 ..-%?!??9;126 -6?,95',290 - 66.85.01: