world bank documentdocuments.worldbank.org/curated/en/575971468087555953/...hbl habib bank limited...

TRANSCRIPT

Document of

The World Bank

FOR OMCIAL USE ONLY

Rqtort Now 11843

PROJECT COMPLETION REPORT

PAKISTAN

INDUSTRIAL INVESTMENT CREDIT PROJECT(LOAN 2380/CREDIT 1439)

MAY 3, 1993

Country Operations, Industry and Finance Division

Country Department IIISouth Asia Region

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS(annual averages)

Rs per US1.00 USS per Rs. 1.00

FY83 12.75 0.078FY84 13.48 0.074FY85 15.16 0.066FY86 16.13 0.062FY87 17.17 0.058FY88 17.55 0.057FY89 19.18 0.052FY90 21.39 0.047FY91 22.37 0.045

Note: Since January 8, 1982, the exchange rate for the rupee has been managedwith respect to a weighted basket of currencies.

ACRONYMS AND ABBREVIATIONS

ACT Needs use of formal remedies to bring about complianceADB Asian Development BankDER Debt/equity ratioDFIs Development Finance InstitutionsDSCR Debt Service Cover RatioFSAL Financial Sector Adjustment LoanGOP Government of PakistanHBL Habib Bank LimitedIDBP Industrial Development Bank of PakistanIIC Industrial Investment CreditKSE Karachi Stock ExchangeMCB Muslim Commercial BankN.A. Not applicablen.a. not availableNBP National Bank of PakistanNCBs National Commercial BanksNDFC National Development Finance CorporationOK Covenant complied withPBC Pakistan Banking CouncilPICIC Pakistan Industrial Credit and Investment CorporationPFIs Participating Financial InstitutionsSALs Structural Adjustment LoansSAR Staff Appraisal ReportSBP State Bank of PakistanSFYP Sixth Five-Year PlanUBL United Bank Limited

GOVERNMENT OF ISLAMIC REPUBLIC OF PAKISTANFISCAL YEAR

July 1 - June 30

FOR OFFICMIL USETHE WORLD BANK

Washington, D.C 20433

U. S. A.

omce of Director-GeneralOperations Evaluation

May 3, 1993

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on PakistanIndustrial Investment Credit Project (Loan 2380/Credit 1439)

Attached is a copy of the report entitled "Project Completion Report on Pakistan- Industrial Investment Credit Project (Loan 2380/Credit 1439-PAK)", prepared by theSouth Asia Regional Office. No comments have been received from the Government.The loan/credit was approved on February 2, 1984 and closed on December 31,1990, three years behind schedule.

The PCR provides a candid assessment of project design and implementationbut lacks information on sub-project performance. Its analysis of the ParticipatingFinancial Institutions' (PFIs) performance with respect to the covenants is confined to1984-87, instead of the full implementation period.

The main objective of the project was to promote private sector industrialinvestment by improving the credit delivery system to ensure a stable flow of termfinancing to private industries. This objective was partially met. But sustainability ofbenefits is uncertain because of the PFIs' weak financial position and poor loancollection performance, a consequence of legal barriers to loan recovery, lack ofinstitutional autonomy, and systemic breakdown in credit discipline.

The impact of the project on institutional strengthening was limited. It failedto rehabilitate the two ailing development finance institutions (DFIs), although thetechnical assistance was helpful in developing project finance skills of the commercialbanks. Overall, the project outcome is not satisfactory.

An audit of the project is being carried out.

Attachment

This document has a restricted distribution and may be used by recipients only in the performance of theirofficial duties. Its contents may not otherwise be disclosed without World Bank authorization.

FOR OFFICIAL USE ONLY

PAKISTAN

FIRST INDUSTRIAL INVESTMENT CREDIT PROJECT (IIC I)

(LOAN 2380/CREDIT 1439-PAK)

PROJECT COMPLETION REPORT

Table of ContentsPage No.

Preface .............................................................. iEvaluation Summary ................................................... ii

PART I PROJECT REVIEW FROM BANK'S PERSPECTIVE

A. Project Identity ......................................... 1Background ............................................... 1

B. Project Obiectives and DescriRtionProject Objectives .................................... 1Project Description ................................... 2

C. Proiect Design and OrganizationProject Preparation ................................... 2Project Design ........................................ 3

D. Proiect ImRlementationImplementation Schedule ........................ 3Allocations and Issues ........................ 4

E. Project ResultsObjectives and Targets ........................ 7Shortcomings ...... .................................... 7

F. Project Sustainability. 7

G. Bank Performance. 8

H. Borrower Performance. 9

I. Lessons and RecommendationsFor Bank Performance. 9For Borrower Performance .10

PART II COMMENTS FROM THE GOVERNMENT (NOT YET RECEIVED)

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

PART III STATISTICAL INFORMATION

Related Loans and Credits ................................... 11

Project Timetable ........................................... 12

Loan/Credit Disbursements ................................... 13

Project Implementation: Selected Financial Indicators ...... 14

Project Results: Studies .................................... 15

Status of Covenants ......................................... 16

Use of Bank Resources ....................................... 20

ANNEXES

Annex 1: Sectoral Allocation ................................ 24Annex 2: Ex-Ante Profile of Subprojects ..................... 25

PROJECT COMPLETION REPORT

PAKISTAN

FIRST INDUSTRIAL INVESTMENT CREDIT PROJECT (IIC I)

(LOAN 2380/CREDIT 1439-PAK)

PREFACE

(i) This Project Completion Report (PCR) covers the First IndustrialInvestment Credit Project (IIC I), for which Loan 2380 and Credit 1439-PAKin the respective amounts of US$50 million and SDR 47.3 million, totalling theequivalent of US$100 million, were approved on February 2, 1984. Theloan/credit closed on December 31, 1990, three years behind schedule. The loanand credit were substantially disbursed, except for US$0.38 million for theloan and SDR3.52 million for the credit representing largely unused amountsfor industrial finance.

(ii) The PCR's Preface, Evaluation Summary, and Parts I and III wereprepared by the Country Operations, Industry and Finance Division of theCountry III Department in the South Asia Region.

(iii) The last supervision mission for the project, scheduled for August15, 1990, did not materialize due to the Gulf Crisis. Hence, preparation ofthe PCR began during the fall of 1991 and was based, inter alia, on thePresident's Report and Recommendation; the Staff Appraisal Report; President'sReports and SARs of associated projects; Loan/Credit and Subsidiary LoanAgreements; Supervision Reports; Annual Reports on Implementation andSupervision; Project Correspondence Files; internal Bank memoranda; FinancialStatements and Audit Reports of PFIs; Subproject Files; data provided throughthe Resident Mission in Islamabad; and interviews with Bank staff who dealtwith the project at various stages.

- ii -

PROJECT COMPLETION REPORTPAKISTAN

FIRST INDUSTRIAL INVESTMENT CREDIT PROJECT (IIC I)(LOAN 2380/CREDIT 1439-PAK)

EVALUATION SUMMARY

(i) Obiectives and Design. The project was aimed mainly at improving theindustrial credit delivery system and focussing on the rehabilitation of twodistressed development finance institutions (DFIs), Pakistan Industrial Creditand Investment Corporation (PICIC) and Industrial Development Bank of Pakistan(IDBP). The strategy shifted from traditional single institution lines to amulti-institutional approach. The GOP onlent the funds to 3 DFIs (PICIC, IDBP,and NDFC) and 2 NCBs (HBL and UBL). The DFIs were fully appraised and coveredby quantitative financial covenants. Due to the NCBs' reluctance to discloseintimate financial and operational information, Bank scrutiny was confined tothe NCBs' term lending operations and no tests of creditworthiness weredefined. The following elements were serious constraints at the outset: noprovision for DFI recapitalization plans, the lack of autonomy ofparticipating financial institutions (PFIs), the substandard state of theaccounting profession, and the absence of broad policy reforms in the real andfinancial sectors. (Paras. 3.01-3.04)

(ii) ImRlementation ExRerience and Issues. Negotiations, Board approval,signing, and effectiveness were basically within schedule. Economic,political, and institutional factors caused a three-year slippage in closing.Appraisal estimates of disbursements were overly optimistic as these did notconform to the DFI disbursement profile; but the Bank flexibly responded tocommitment and disbursement problems. (Paras. 4.02 & 4.08) Subprojectallocation, an area where the Bank's role was prominent, substantiallyconformed to priorities defined by the Sixth Five Year Plan (SFYP). PICIC'scommitments showed a high utilization rate and pronounced concentration ontextiles, contrary to SAR expectations. The analysis of all availablesubproject files showed 74% having debt/equity ratios (DERs) higher than 60:40and 43% with debt service cover ratios (DSCRs) below 2.0:1, breaching thebenchmarks normally acceptable to the Bank. The ratio of green field toexisting borrowers was 1.9:1, indicative of the risk level. The ex-ante rangewas 14-50% for IERRs and 15-50% for IFRRs. Wide IERR-IFRR disparities wereobserved for a number of projects, especially textiles, suggestinginefficiency in resource utilization. (Paras. 4.03-4.04)

(iii) The systemic breakdown in credit discipline, legal recovery obstacles,and highly-leveraged projects were pressure points for the PFIs. Bank effortsat rationalizing capital structures were frustrated by conflicting publicpolicies toward the treatment of bridge finance used by borrowers as debt.Nonetheless, PICIC and IDBP substantially met the required absolute collectiontargets. But their low total collection ratios (47-55% in 1987) implied thatthe targets set by the Bank were modest. Ironically, two of PICIC's directorswere cited during supervision as willful defaulters. In sharp contrast to thelow collection ratios, both DFIs showed healthy debt service cover ratios wellabove the prescribed minimum. This financial inconsistency implied

- iii -

noncompliance, without the Bank's awareness and loss of eligibility for theDFIs. (Para. 4.05)

(iv) TA grants were useful in upgrading and diversifying PFI manpowerskills. However, actual outlays for training exceeded targets by 91%. Therewas no midstream review of global training needs, depriving the Bank of amechanism for optimizing results and minimizing abuse. Subsector studies werenot adequately circulated to all PFIs. Diversification studies for PICIC andIDBP were not fully synchronized with subsequent organization and systemsstudies. Diversification moves of PICIC and IDBP suffered setbacks due to thelack of expertise and management turnover caused by political interference.(Para. 4.07)

(v) Results and Sustainability. The project has succeeded in ensuringcompetitive and uninterrupted retailing of loans with the inclusion of NCBs,eventually removing DFI operating anomalies, and enhancing PFI project financeskills. Institutional restructuring has not been achieved. IDBP is ineligibleunder all IIC projects. PICIC, HBL, and UBL became ineligible under other IICprojects, although PICIC was later reinstated. PICIC's real condition hasbeen masked by massive reschedulings. (Paras. 5.01-5.02) There are doubtswhether uninterrupted industrial finance delivery can be sustained underpresent circumstances. The real performance and solvency of additional NCBsmobilized as retail outlets are in question. The inherent balance sheet andoperational structure of PFIs, their profitability and cash flowcharacteristics, and the real/financial sector environment constitute seriousviability threats. (Paras. 6.01-6.02). However, reforms in the financialsector and other measures, pursued jointly by the Bank and the GOP, would tendto strengthen sustainability in the long run.

(vi) Performance. Limited access to NCB information weakened the appraisaland supervision process. The SAR unrealistically assumed that DFIrestructuring would succeed without providing for a recapitalization plan.Bank efforts in helping reduce GOP interference with PFI were ineffective,partly due to the absence of appropriate legal provisions. There were notenough supervision missions. Efforts to develop the data base to trackcompliance with covenants were inadequate. GOP action in enacting requisitepolicy reforms to strengthen the real and financial sectors were slow andinconsistent. PFIs themselves were not forthright in disclosing their truefinancial situation. (Paras. 7.01-8.01)

(vii) Lessons Learned and Recommendations. (Paras. 9.01-9.04) The absence ofsustained policy and institutional reforms in the real and financial sectorsrenders the sustainability of PFIs, which have to operate in an extremelydistorted environment, highly unlikely. There are important lessons for Bankperformance that flow from this main insight: (1) Future credits should bereinforced by systemic reforms, through FSAL and related programs, thatspecifically address the elements jeopardizing PFIs' sustainability. (2)Institutional restructuring is unlikely to succeed without theseprerequisites, among others: full institutional autonomy; prudentialregulations on income recognition, provisioning, capital adequacy, and loanconcentration; an effective legal recovery system; and internationally-acceptable accounting/auditing standards. Vis-a-vis the latter, it should also

- ----- - ----

- iv -

be noted that the effectiveness of Bank auditing requirements is severelydiminished when these are applied to entities operating in a nationalenvironment where accounting/auditing standards are not at internally acceptedlevels. (3) SAR risk assessment should address institutionalcreditworthiness, not just credit delivery, issues. (4) Bank legal leverageagainst adverse Borrower/Guarantor behavior should be exercised decisively,even after full commitment of funds, if other initiatives applied in earnestfail. (5) Even in the absence of an explicit stipulation, the Bank's GeneralConditions should be invoked to allow Bank access to relevant informationfrom all PFIs.However, the possibility of pursuing remedial measures due to aclear deterioration in performance or condition can only be pursued ifspecific covenants are in place. (6) To optimize TA grants and minimize abuse,there should be a projectwide reassessment in case of significant deviationsfrom estimates. (7) Bank Head Office should be spared heavy time involvementwith small TA ticket items through formal delegation to the Resident Mission.There are also parallel lessons for Borrower performance: (1) The GOP canpromote the success of PFIs if it refrains from assigning non-financial andnon-economic roles to them. (2) Serious consideration should be given totenured managerial positions to provide for institutional stability. (3) PFIsshould initiate and welcome mergers if these constitute real options forsurvival and growth. (4) There must be clear, formalized, and strict rulesgoverning insider transactions among PFIs. (5) Non-proprietary TA components,such as subsector studies, should be widely circulated.

PROJECT COMPLETION REPORT

PAKISTANFIRST INDUSTRIAL INVESTMENT CREDIT PROJECT (IIC I)

(LOAN 2380/CREDIT 1439-PAK)

PART I: PROJECT REVIEW FROM THE BANK'S PERSPECTIVE

A. Project Identity

Name First Industrial Investment Credit ProjectLoan/Credit Number Ln 2380/Cr 1439-PAKRVP Unit EMENA RegionCountry PakistanSectors Finance and Industry

Background

1.01 Starting in 1977, the GOP aimed at promoting private sectordevelopment through divestment of industrial units nationalized in 1972,restrictions on public sector manufacturing, and limited industrial policyderegulation. The SFYP pursued the strategy. Substantial advances wereexpected in engineering goods, selected textiles, and efficient import-substituting manufactures. IIC I was prepared within a macro environmentcharacterized by improved, broad-based economic performance, with GDP growingby 6% p.a. in real terms. However, there were weaknesses in industrial/tariffpolicy and procedures, infrastructure bottlenecks, and inefficiencies in thefinancial system. Corporate savings and self-investment were low and theactive expansion in private investment created pressures on the deliverysystem for industrial finance. The system was constrained by a fragmentedinstitutional structure, centralized and detailed system of credit allocation,and distortions in the interest rate structure. The Bank supported the GOP'sindustrial strategy through its sector credits and project lending.

1.02 For more than two decades, PICIC and IDBP were the principal,functionally-specialized term lending institutions for industrial development.NDFC, organized later to finance public enterprises, diversified intofinancing medium and large-scale private firms, emerging as the largest DFI inPakistan. By end-1982, these three DFIs had received from the Bank 14 loanstotalling US$384 million. As other institutions such as national commercialbanks (NCBs) expanded into term lending operations, the role of DFIs declinedin importance. The clientele and operations of DFIs and NCBs tended tooverlap. These financial institutions were largely owned by the GOP, exceptfor PICIC which was 51% privately-owned. The portfolios of PICIC and IDBPsuffered severely from the loss of assets with the independence of Bangladesh,the 131% devaluation in 1972, and the subsequent nationalization measures.

B. Project Objectives and Description

2.01 Proiect Objectives. There was continuing need for an uninterruptedflow of industrial term finance to the private sector. Accordingly, the mainobjectives of the project were to improve the industrial credit deliverysystem and focus on the institutional restructuring of two weaker DFIs, PICICand IDBP. Systemic improvements were to be achieved through greater

competition with the inclusion of NCBs, the equalization of rules for DFIs,improved product selection by the PFIs, and institutional strengtheningthrough TA programs.

2.02 Project Description. The equivalent of US$100 million was extendedto finance US$98 million in subloans and US$2 million for TA. Three DFIs(PICIC, IDBP, and NDFC) and two NCBs (HBL and UBL) were designated as thePFIs. Fixed assets and permanent working capital requirements of principallyprivate industrial projects were eligible for financing. The Bank lent to theGOP on standard terms. The onlending terms were for 15 years, including a 3-year grace period, and an end-user rate of 14%. PICIC and IDBP, which weretaxable, were afforded a 4% spread. NDFC and NCBs, which were tax exempt, wereallowed a 3% spread. As was the case for many Bank borrowers at the time, theGOP bore the foreign exchange and interest rate risks. Subloan size persubproject had a minimum of US$1.0 million and a maximum of US$4.0 million.Exceptions to subloan limits and free limits were considered on a case-by-casebasis. A total of 40 to 50 subprojects was targeted for financing.

2.03 The TA component of US$2 million, structured to ensure flexibility inits uses, was available for grants for training PFIs' officers in projectevaluation, preparation of project appraisal manuals, organizational andsystems studies, and sectoral studies. The training programs envisionedindepth exposure to prevailing practices in working capital finance,development banking, including economic aspects of project evaluation.Subsector studies would assist PFIs in their project work. At projectpreparation, US$750,000 were allotted each to organization studies andtraining, while US$500,000 was earmarked for subsector studies. DFIs plannedto utilize the organization and systems studies component, while all PFIscould benefit from project skills development. HBL, NDFC, and PICIC wereexpected to undertake subsector studies to guide their operations.

C. Project Design and Organization

3.01 Project Preparation. The project departed from the traditionalsingle institution credit lines and introduced a multi-institutional approach.The new strategy provided the Bank some leverage for introducing a short menuof reforms aimed principally at strengthening the ailing DFIs rather than abroader agenda of policy reforms. The Bank decided not to pursue identifiedissues relating to interest rate distortions, especially the crossing ofrates. The GOP committed that systemic interest rates would be positive,which they were. Furthermore, the process of Islamization being introducedwould start to address interest rate reform. The project was viewed as thefirst step in strengthening the financial sector and related dialogue underIIC II, IIC III, and FSAL.

3.02 The project generated conflicting convictions within the Bank, theGOP, and PFIs as to its merits and prospects. There was Bank recognition thatthe weaker DFIs were on the "verge of bankruptcy" and were considered poorcredit risks. Their inclusion apparently deviated from the Bank's then

prevailing guidelines.' This decision was considered a necessary cost togenerate the benefits expected. GOP leverage would be utilized in intensifyingthe collection efforts on accounts of the distressed DFIs. Close cooperationwith the Asian Development Bank, a major creditor of the DFIs, increased theleverage in the rehabilitation process. The GOP, the Bank, and the two DFIswould embark on a major rehabilitation program anchored on recoveries,diversification, and internal improvements. The NCBs themselves wereapparently reluctant to participate, while the DFIs lobbied against theirentry. NCBs were apprehensive about disclosing to the Bank intimate aspectsof their operations and financial status, a sentiment shared by the GOP.

3.03 Project Design. The five PFIs were subject to meeting eligibilitycriteria, the common features of which were: (i) approval by their respectiveBoards of Policy and Corporate Strategy Statements, acceptable to the Bank;and (ii) the implementation of training programs agreed with the Bank. Thereview of policy and strategy statements afforded a constructive opportunityfor Bank-PFI interaction in asset rationalization guidelines. As part oftheir rehabilitation program, PICIC and IDBP were subject to collectiontargets, while the other PFIs were not. All DFIs were required to maintain aminimum 1.1:1 debt service coverage ratio. The maximum DER was set at 5:1 forIDBP and NDFC and 7:1 for PICIC. No covenants were imposed on the NCBs, asreliance was placed on the liquidity and operational ratios monitored byPakistan Banking Council. PFIs were required to submit quarterly reports andannual audited financial statements.

3.04 The circumstances surrounding the project's conception and thecompromise reached on the treatment of NCBs generated a number of designcharacteristics. These elements derived from a mismatch between the broadersectoral objectives of the project (and the Bank's strategic view of theproject) with non-sectoral conditionalities and absence of sectoral reform.There was a formal agreement on the part of the Bank to confine the initialand subsequent review of NCBs to their Bank-financed term lending operations,thus limiting comprehensive assessment of creditworthiness. The state ofsubstandard accounting and auditing practices, and the reliability offinancial data were taken as given. There was no recourse against GOPinterference in PFIs' operations since it controlled them. This issue wasrelevant to the autonomy of PFIs, especially on matters relating to managerialappointments and credit decisions. The rehabilitation program did not includea recapitalization plan and was not sensitive to the time lag for policyreforms to be implemented and fully felt by the real sector.

D. Project Implementation

4.01 Implementation Schedule. Negotiations, Board approval, signing, andeffectiveness were substantially within schedule. Commitments were generatedmuch faster than expected. Subsequent subloan cancellations and decelerationoccurred due to a confluence of events. These factors included lowinternational interest rates, volatile foreign exchange markets, the tapering

1 See: OMS 3.73, Sept. 1976, para. 41; Nov. 1986, para, I. 7; and Nov. 1986., paras. III 14 and 19.

-4-

off of industrial investments, inability of sub-borrowers to comply with loanconditions, competition from subsidized GOP credits, preoccupation by DFIs'management with requisite GOP clearances for special operations, managementchanges, and strategic and organizational adjustments. Subloan cancellationsarising from these events prompted three postponements of the closing datefrom December 31, 1987 to December 31, 1990. The postponements allowed formaximum utilization of the loan/credit proceeds. Loans for 51 subprojectswere finally disbursed. Commitments for a total of 30 subprojects werecancelled. Therefore, post-commitment subloans survived at a rate of 62%. Theloan/credit was substantially disbursed (99.62%). There was a three-yearslippage noted in actual disbursements vis-a-vis appraisal estimates, whichwere overly optimistic and did not follow the DFI disbursement profile.

4.02 Allocations and Issues. Based on the IIC I SAR estimates, NDFC hadthe most active, while PICIC had the leanest, project pipeline among the DFIs.There were no project pipeline data for NCBs. Reflecting its strategy, PICICplanned on a slow growth pattern to ensure higher quality portfolio. Agro-based, steel/engineering, cement, and chemical industries, priority areasunder the SFYP, accounted for 64% of the DFIs' pipeline. Textiles representedonly 15% of the total pipeline. Textile projects in PICIC's pipelinerepresented 11% of its pipeline. It was the DFIs' strategy to reduce exposurein textiles and promote projects in the priority activities. Duringimplementation, sub-sector studies were commissioned by IDBP and NDFC versusthe original plan of having these undertaken by HBL, NDFC, and PICIC. Thesestudies provided asset rationalization guidelines but were not adequatelycirculated to other PFIs.

4.03 Based on an inventory of the final projects disbursed after IIC Iclosed, PICIC turned out to be the most active retailer of funds, accountingfor 23 subprojects (US$21.78 million and SDR14.73 million). Less active wereIDBP (10 subprojects totalling US$11.25 million and SDR9.40 million), NDFC (11projects totalling US$12.00 million and SDR8.71 million), and HBL (7subprojects totalling US$2.34 million and SDR11.43 million). UBL was theleast active with one subloan amounting to US$2.11 million. By the time UBLwas declared eligible, most of the project funds had been committed to othersubprojects. Of the total actual commitments, 32% were allocated to textiles,20% to food manufacturing, 16% to paper production, and the balance to othersubsectors. PICIC's commitments were highly concentrated on textiles (62%),while 50% of the commitments of other PFIs were allocated to paper, food, andengineering products. Although PICIC deviated from allocation expectations,the subproject commitments of the other PFIs were largely within the desiredpriorities.

4.04 The 42 subproject files available in the regional files were examinedon an ex-ante basis (Annex 1). The appraisal reports of HBL and PICIC were ofgenerally acceptable quality. While the fuller appraisal reports of NDFCtended to be of acceptable quality, the summary reports were poorly presented.The report on UBL's sole subproject was comprehensive in coverage. Theappraisal reports of IDBP on file had uneven quality. Of those examined, 31subprojects (74%) had effective DERs exceeding 60:40, while 18 (43%) had DSCRsbelow 2:1, minimum standards acceptable to the Bank. Green field projectsoutnumbered existing borrowers by a ratio of 1.9:1, indicative of the risk

- 5 -

profile. The IERR range was 14%-50% (24 subprojects showing 20% or greater),with the IFRR range being 15%-50X. Of the 6 textile subprojects with IERRdata, 2 showed wide disparity between the IERR and IFRR figures, indicatingproject vulnerability to exogenous swings such as changes in internationalprices for cotton and yarn, cotton subsidy, and other policies. Thedisparities between the IERRs and IFRRs, for textile projects in general,would probably be higher than indicated,2 raising doubt as to efficiency inresource allocation. The Bank's role in asset rationalization was reinforcedduring subproject review, as it emphasized the critical importance of havinghigh IERRs and group exposure limits.

4.05 There were no serious delays in the submission of periodic auditedfinancial statements by the PFIs. However, the statements did notrealistically reflect PFI performance and condition. This notwithstanding, inthe course of project implementation/supervision, it was evident thatcollection and portfolio problems were of universal concern to the PFIs,rendering their operations high risk in nature. The PFIs were exposed to thesystemic breakdown in credit discipline, legal obstacles to the recoveryprocess, and highly leveraged capital structures of borrowers. During theperiod 1984 to 1987, 3 both PICIC and IDBP substantially met absolutecollection targets as part of IIC I conditionality. But the 1987 totalcollection ratio stood at a low level of 47% for PICIC and 55% for IDBP.Portfolio infection was brought down by PICIC, through subprojectrestructuring and concerted collection efforts, from 32% in 1984 to 15% in1987. IDBP's infection ratio remained high at 35%. Ironically, PICIC'srehabilitation program was hampered by the fact that two of its directors wereconsidered as willful defaulters. The low collection ratios for both PICIC andIDBP were inconsistent with high DSCR ratios reported. A February 1987 Banksupervision report cited a DSCR of 1.2 for PICIC and 1.5 for IDBP, materiallyhigher than the covenanted minimum of 1.1. If more credible DSCR figures couldbe extracted, both DFIs would probably be in violation of this eligibilitycriterion then. The November 1989 supervision reported a marked drop in theDSCRs of both DFIs below compliance level, without the DFIs being declaredineligible. Subsequent figures showed a recovery to high DSCR levels, side byside with low collection ratios.

4.06 To improve collection performance (and in the absence of an effectiveaccounting and auditing framework), the Bank acted with initiative insuggesting the formation of special tribunals to handle exclusively recoverycases for the PFIs. While there was delay in GOP response, the initiativeeventually bore fruit. One of the most contentious issues running throughoutthe implementation phase, unidentified at the preparation stage for IIC I, was

2 While textiles represented a major share of manufacturing value-added in Pakistan (about 16X), the20-count variety has been identified as being a relatively low-value added activity. Projects in thissubsector tended to have optimistic revenue forecasts and low domestic cotton price assumptions via-a-viainternational levels.

3 To minimizo complex cross references to covenants and indicators among the IIC projects, this PCRfocuses on the period from 1984, the start of IIC I, up 1987, the scheduled closing. IIC II was approved in1985 and IIC III in 1988. The data in this PCR analysis, drawn from SARa and supervision reports on IIC II

projects, differ in some instances from data recently available from the DFIs.

- 6 -

the incidence and treatment of bridge finance in the subproject financialplans. Many subprojects showed bridge finance provided by financialinstitutions, with refunding against future equity underwritings, as part ofequity. This prevalent practice effectively reduced the real equity stake ofsubproject sponsors to minimal or negative levels. The financial structureincreased the debt service and default risks of subprojects and loadedfinancial institutions with accumulations of potential non-performing assets.The Bank took the position during sub-loan approval4 that at least 22.5% ofproject cost should represent sponsors' stake in a subproject, and that bridgefinance should be treated as debt in the calculation of a project's DER. TheGOP's response to the key issue showed vacillating and inconsistent policysignals and measures. The issue remained unresolved even after IIC I closed.

4.07 The diversification moves of PICIC and IDBP were stymied by the lackof adequate, trained personnel. TA training outlays proved to be useful to allPFIs, a situation not otherwise possible under the currency control program.Training expenditures funded by TA grants exceeded original estimates by 91%.There were numerous requests for training grants but there was no reassessmentduring implementation of the aggregate and institution-specific needs,suggesting that TA processing might have been ad hoc in nature. In 1987,three years after IIC I was approved, diversification studies werecommissioned for both DFIs under the TA component. The follow-on organizationand systems studies were not fully synchronized with the earlierdiversification studies, implying the probable absence of careful Bankscrutiny of the TOR. As a result, the second round of studies was of verylimited utility. While diversification moves were being pursued, the PFIswere subjected to high top management turnover due to GOP appointments.Starting in 1989, civil servants without banking experience were appointed aschief executives. As a consequence, institutional instability delayeddiversification moves and weakened the rehabilitation programs.

4.08 In the course of project implementation, a number of commitment anddisbursement problems emerged. There was initial misunderstanding on themaximum subloan allowed for each PFI. The SAR cited a US$4 million subprojectlimit, while the legal documents indicated a U$4 million subloan. Someprojects considered involved foreign currency funding in excess of US$4million, but there was lack of familiarity in handling subprojects to befunded by more than one PFI. The Bank resolved the situation by allowing, ona case-by-case basis, subproject commitments by PFIs beyond US$4 million.Disbursement bottlenecks developed, in the absence of a special account, giventhe multiplicity of PFIs and disbursement requests for many small ticketitems. PFIs' disbursements tended to exceed subloan authorizations of between10-20% due to currency fluctuations. The Bank authorized deviations butrequired the PFIs to clearly and more cogently factor currency fluctuationsinto project cost estimates.

4 This issue, not formally addressed in IIC I loan conditionality, appeared as a formalized conditionunder IIC III in 1989.

-7-

E. Project Results

5.01 Objectives and Targets. IIC I was partly successful in achieving itsobjectives. The inclusion of NCBs facilitated uninterrupted retailing offunds, ensuring the substantial disbursement of the loan and credit. In theprocess, NCBs were able to internalize project finance skills. DFI operatinganomalies were corrected over time and they were eventually authorized widerproduct lines to offer their clientele. Expanded services of DFIs and NCBs(which could offer long-term loans covering foreign currency requirements)tended to promote competition and better services to clientele, i.e., fasterservice and broader product options. Operational skills, particularly inproject finance, were enhanced. There was overall dispersal of funds intopriority areas identified under the SFYP. The target of 40 to 50 subprojectswas exceeded, with 52 actually being funded. 5

5.02 Shortcomings. The objective of institutional restructuring was notachieved. IDBP could not meet eligibility tests under all IIC projects, withits prospects for its eventual recovery deemed highly uncertain. IDBP showedinitial nominal improvements in collection performance and product linediversification. But portfolio infection was generally high during projectimplementation. PICIC likewise showed initial progress in collectionperformance and some diversification into new product lines. However, thelevel of portfolio infection was a recurring issue. Rescheduling proceduresmasked the real financial standing of PICIC. The real DSCRs were probablylower than indicated in the light of low collection ratios (para. 4.05).Compliance with the DER covenant at the time of IIC I PCR preparation wasdifficult to determine. While there were external auditors' certificatesindicating compliance, an independent check on the computations yieldedmaterial deviations from the governing loan agreement. As a minimum, there wasno full knowledge on the part of the Bank, during supervision and PCRpreparation stages, as to compliance with this basic financial covenant.

F. Project Sustainability

6.01 It is doubtful whether the gains under IIC I of ensuring theuninterrupted flow of industrial term finance can be sustained under currentcircumstances. PICIC lost eligibility in 1989 under IIC II and IIC III butwas reinstated in 1990. UBL became ineligible in 1990 and HBL in 1991 due tofailure to meet the collection ratio covenant under the other IIC projects.The collection performance of UBL in 1989 dropped to 55%, considerably shortof the covenanted 80% ratio, while HBL's 1990 ratio declined to 64%. As partof the strategy of ensuring uninterrupted flow of industrial finance and otherobjectives, two other PFIs were added to the eligibility list under IIC II andIIC III, namely, MCB and NBP. Options have been narrowed down for furtherexpanding the retail outlets for industrial finance and maintaining thecompetitive element.

5 Ex-post data were requested from the five PFIs during PCR preparation. Two PFIs submitted data on 21subprojects or 402 of the total number of IIC I subprojects. Of the 21 subprojects reported, 11 had ex-postIERRs/IFRRs which were identical or almost identical with the ex-ante data. Eight subprojects reportedly hadhigh IEMRs and IFRRs but were unprofitable. The apparent inconsistency and unroliability in the *x-oxtdata could not be verified at PR preparation.

- 8 -

6.02 The sustainability of PFIs is threatened by the decline in thequality of their balance sheet and operational structure, their profitabilityand cash flow characteristics, and the real/financial sector and policyenvironment within which they operate. The asset profile and product lines ofDFIs reflect the characteristics of high risk banking without commensuratereturns. Project lending is inherently risky, considering that manysubprojects are highly leveraged and have low liquidation values. Assets andequity tend to be overstated since provisions do not meet prudentialstandards. Real margins are tight or negative due to low collection ratios,low locked-in margins on old loans (i.e., potential liability sensitivebalance sheets), and insufficiency of real interest margins to cover cashcosts. The environment within which the PFIs operate has been characterized byinefficiencies and distortions in the real and financial sectors, the absenceof financial discipline, and a narrow capital market. PFIs face uncertaintiesarising from the profitability and capital adequacy impact of strictlyapplying prudential regulations. Furthermore, the short/medium-termperformance of rescheduled projects is highly uncertain. A major consequenceof these factors is a setback in the PFIs' institutional development. Thelong-awaited privatization moves adopted by the GOP during the latter part of1991 would tend to ensure autonomy, but the issues of capital adequacy,weaknesses in the regulatory/supervision framework, and sustained viability ofPFIs should be clearly addressed. These and other measures, pursued jointly bythe Bank and the GOT, would tend to strengthen project sustainability in thelong run.

G. Bank Performance

7.01 IIC I was an approach that marked a departure from the singleinstitution lines. But for reasons discussed in para. 3.04, the Bank did notundertake a comprehensive appraisal and periodic review of thecreditworthiness of the NCBs. Based on hindsight, the Bank should haveinsisted at appraisal stage on collection ratios for the NCBs, and addressedcapital adequacy and related issues. The weakness was later partly addressedthrough policy dialogue under FSAL. relative to the attainment of capitaladequacy by NCBs. The Bank demonstrated consistency in following through therestructuring and collection efforts of PICIC and IDBP, and other aspects ofthe project relating to institution building, product line enhancement, andequalization of rules. But the Bank's dialogue with the GOP did not bearfruit in significantly reducing interference in the management and operationsof PFIs. Notwithstanding these impediments, the Bank responded flexibly torequirements of PFIs and sub-borrowers. The Bank allowed the maximum sub-loans per project to exceed US$4 million and permitted disbursements beyondauthorizations as a result of unforseen currency fluctuations. It alsoinitially approved highly leveraged projects to proceed, the wisdom of whichmight be questioned in the light of the collection performance of the PFIs.

7.02 There were only 6 supervision missions during the eight-year spanfrom the project's approval and closing. There was no supervision mission in1988 as a result of the 1987 Bank reorganization, while the last missionscheduled for August 15, 1990 was cancelled due to the Gulf Crisis. Thesupervision reports did not provide data continuity to facilitate trackingcompliance with the financial covenants. Many of the financial statements and

- 9 -

related reports on PFIs were not on file. Efforts to develop the data base totrack compliance with covenants were inadequate (para. 4.04). Ten of the 52appraisal reports on subprojects financed were missing. There werediscontinuities in correspondence files that hindered fuller appreciation ofissues raised. Of the 6 supervision reports prepared, the 2 latest ones weresubmitted within about 3 weeks from the return of the missions, while the 4earlier ones were submitted within 1.5 to 3.5 months . 6

H. Borrower Performance

8.01 The GOP has demonstrated lack of sustained commitment to theobjectives of the project and related activities covered under other Bankprojects. Consequently, its performance has impacted negatively on thesuccess of the project in attaining objectives relative to the quality ofindustrial finance. The GOP has been slow in carrying out requisite policyreforms to strengthen the real and financial sectors. It took 5 years for theoperating anomalies among the PFIs to be completely eliminated. PICIC receiveddeposit taking powers only in 1989. Recurring political interference inmanagerial appointments and credit decisions of PFIs have adversely affectedin a material way their financial performance and soundness. The resultingmanagement instability and absence of professional motivation and commitmenthave exacerbated disruptions in both strategic and crisis management efforts.Additionally, the disruptions have created discontinuities in Bank-borrowerrelationship. Notwithstanding their generally regular submission, thereliability of financial reports submitted by the PFIs is subject to question,especially in terms of income/expense recognition and provisioning, due, inlarge part to the absence of internationally accepted accounting and auditingstandards.

I. Lessons and Recommendations

9.01 For Bank Performance. Future credits should be reinforced by systemicreforms, through FSAL and related programs, that specifically address theelements jeopardizing PFIs' sustainability. In an institutional restructuringprocess involving financially-distressed PFIs which are wholly orsubstantially government-owned, it is necessary but not sufficient to rely on:collection targets and efforts; strengthening of internal management, systemsand appraisal/supervision capability; business diversification; and supportivepolicy reforms. There are at least three additional prerequisites foreffective results (para.3.04): (i) measures to achieve full autonomy, such asprivatization; (ii) the application of prudential regulations governing incomerecognition, provisioning, capital adequacy, and loan concentration; and (iii)the existence of a credible national accounting and audit/supervisionstandards and framework based on international standards. Without prudentialregulations and rigid accounting/auditing standards, financial covenants andindicators become highly unreliable benchmarks during implementation (para.4.05). Risk assessment in future SARs should appropriately address not justthe risks that affect the channelling of credit. Consideration should be givento the current and future creditworthiness of the PFIs themselves since this

6 As compared to Bank guidelines of 5 to 10 days.

- 10 -

issue materially affects project sustainability. Therefore, accounting andauditing requirements, based on internationally acceptable standards, must beconsistently insisted upon, both at the national and at the entity levels.

9.02 Bank effectiveness and the amount of staff time devoted duringimplementation were directly affected by the Borrower's adverse behavior,among others. Rather than taking GOP control of PFIs as a given constraint,the Bank could have spelled out more definitive measures to ensure greaterautonomy. Bank leverage can be effective if exercised even after commitmentof loans/credits (para. 7.01), if other initiatives applied in earnest fail.While end-users might be prejudiced, the Government should assumeresponsibility for noncompliance.

9.03 To facilitate adequate appraisal and supervision, it would be idealto emphasize Bank access to all relevant information on the operations andstatus of all PFIs, including NCBs (para. 3.04). If necessary, the Bank'sGeneral Conditions may be invoked to require the submission of relevantinformation. However, cognizance is made of the fact that invoking drasticaction is feasible only if defined covenants are operative. It would also beuseful to have a standard form for tracking a time series on financialcovenants and indicators (para. 7.02). Significant deviations in TA requestsduring implementation should be reviewed on a projectwide basis to optimizeresults and reduce possibilities for abuse (para. 4.07). Bank time utilized inreviewing a large number of small TA ticket items may be released for someother urgent tasks by possibly delegating items below a cutoff point to theResident Mission. The Resident Mission in Pakistan was informally assignedthis task but the delegation of authority was never formalized. Accordingly,the Resident Mission exercised caution, resulting in the Head Office carryingout this responsibility substantially.

9.04 For Borrower Performance. There are important lessons for borrowerperformance: (i) It is important to explicitly stipulate in an appropriatePFI document, such as the Policy Statement, the transparency, rules, andsafeguards relating to insider transactions, especially loans to directors andother related interests (para. 4.05). (ii) The benefits of TA grants will beenhanced by circulating non-proprietary components, such as sub-sectorstudies, to other PFIs and parties that can benefit from them as instrumentsfor improving market knowledge (para. 4.02). (iii) Due consideration might begiven to the possibility of tenured positions or management contracts toensure managerial continuity, without prejudice to sanctions or disincentivesin case of shortcomings relative to defined performance standards (para. 8.01)(iv) PFIs should welcome, or preferably initiate, merger prospects with otherentities, if this move represents the only sound basis for sustained survivaland growth (para. 6.02). (v) The GOP cannot expect PFIs to succeed asfinancial institutions if it requires them to perform non-financial and non-economic activities.

PART III

STATISTICAL INFORMATION

1. Related Loans/Credits

Loan/Credit Date of Status/Title Purpose Approval Comments

Ln 2648/Cr 1646-PAK To assist the GOP develop the proj. closingSecond Industrial Invest- capital market, improve cre- ahead ofment Credit (IIC II) dit delivery for industrial 12/31/92

finance and continue institu- target, buttion building for PFIs 1/07/86 disbs. lag

Ln 3019/Cr 1982-PAK To assist the GOP hasten the 12/31/94Third Industrial Invest- growth of equity markets, closing; pro-ment Credit (IIC III) improve credit delivery for commitments

industrial finance, address ahead butcorporate finance issues and disbs. lagassist PFIs diversify 1/31/89

Loan 3029-PAK To assist the GOP in financial 12/31/90Financial Sector sector reforms: gearing cre- closingAdjustment Loan dit allocation to market sig- extended;

nals, improving health and slow imple-efficiency of banking system, mentation;and creating more efficient 2nd tranceGovernment debt system 04/14/89 release

pending ful-fillment ofconditions

Credit 1499-PAK To promote investments in 06/30/91Second Small Scale promising SSI subsectors and closingIndustry Project improve productivity of extended to(SSI II) existing SSI units 06/14/84 06/30/91;

deterioratedcollections

Loan 2839-PAK To provide SSI financing, 12/31/95Third Small Scale expand PCIs' SSI funding closing;

Industry Project capabilities, and develop NCBs prefer(SSI III) export marketing system 06/16/87 larger

clients; com-petition fromsubsidizedcredits

- 12 -

2. Proiect Timetable

Date Date DateItem Planned Revised Actual

- Identification 03/82

- Preparation 12/82

- Appraisal Mission 03/01/83- Loan/Credit

Negotiations 10/83 11/83 11/28/83-12/02/83

- Board Approval 12/83 01/84 02/02/84

- Loan/Credit Signature 02/27/84

- Loan/CreditEffectiveness 05/31/84 04/26/84

- Loan/Credit Closing 12/31/87 12/31/88 &12/31/89 12/31/90

- Loan Account Closing 04/30/91

Comments: The Pre-Appraisal Mission scheduled for March 1, 1983 served asthe Appraisal Mission. Considering that the project was the first multi-institutional package introduced in Pakistan, loan effectiveness was more thana month ahead of schedule. Recurring cancellations of commitments forsubprojects caused delays in the closing, prompting three extensions beforethe final closing date. There were a total of 30 cancelled projects comparedto 51 finally committed. The Bank advised the PFIs to carefully ensure thatsubloan commitments would be in place to meet the scheduled closing, butfactors beyond the control of both the Bank and the PFIs came into play. Theseexternal elements included: low interest rates in international markets andaccess by entrepreneurs to these sources; subsidized long-term credits madeavailable by the GOP; tapering off on industrial investments; and disruptionscaused by managerial, strategic and operational changes within PFIs.

- 13 -

3. Loan/Credt Disbursements

Cumulative Estimated and Actual Disbursements(US$ Millions)

Forina I lyFiscal Actual SAt. Profile PAt. Revised SAt. Original Amt. Revised Ant.Year Cumulative Cumulative Cumulative Cumulativ Cumulative

1984

Sep. 1983Dec. 1983Mar. 1984 .06Jun. 1984 .12 .12

Sep. 1984 .21 .21Dec. 1984 .47 .29 9.70 .47Mar. 1985 2.31 .48 28.40 2.31Jun. 1985 8.63 5.13 45.70 8.63

Sep. 1985 10.60 9.68 59.00 10.60Dec. 1985 21.68 15.50 72.30 21.68Mar. 1986 24.90 21.31 84.60 24.90Jun. 1986 35.77 30.99 94.90 35.77

Sep. 1986 45.70 40.68 100.00 45.70Dec. 1986 53.28 50.36 100.00 53.28Mar. 1987 58.29 60.05 100.00 58.29Jun. 1987 62.74 65.86 100.00 62.74

Sep. 1987 65.83 71.67 65.83Dec. 1987 70.11 75.54 70.11Mar. 1988 72.51 79.41 72.15Jun. 1988 79.00 81.35 78.64

.1989

Sep. 1988 80.95 83.29 80.59Dec. 1988 84.68 85.23 84.32Mar. 1989 86.78 87.16 86.42Jun. 1989 87.61 89.10 87.41

L2Q

Sep. 1989 88.62 91.04 88.42Dec. 1989 89.24 92.01 89.04Mar. 1990 90.86 92.97 90.66Jun. 1990 94.80 93.94 95.66

1991

Sep. 1990 97.00 94.91 97.66Dec. 1990 100.25 95.88 100.00Mar. 1991 102.97 96.85Jun. 1991 102.98 96.85

- 14 -

4. Project Implementation: Selected Financial Indicators (IIC Project)

Covenant 1984 1987 1990

PICIC

DSCR 1.1 minimum 1.2 1.2 1.4

DER 7:1 maximum 4.9 4.2 4.0

Portfolio infection N.A. 32% 15% 14%

Total collection ratio N.A. 37% 47% 78%

IDBP

DSCR 1.1 minimum n.a. 1.5(a) 1.2

DER 5:1 maximum(b) 4.2 4.1 5.1

Portfolio infection N.A. 52% 37% 37%

Total collection ratio N.A. 37% 55% n.a.

NDFC

DSCR 1.1 minimum n.a. 5.8 6.5

DER 5:1 maximum(b) 3.8 7.7(c) 5.9

Portfolio infection N.A. 5% n.a. 15%

Total collection ratio N.A. 64% 65% 85%

N.A. - not applicable n.a. - not available(a) The figure was reported in the 02/05/87 supervision report.(b) This limit was later raised to 7:1.(c) This excess was corrected by equity infusion.

Notes: (1) At PCR preparation time, questions were raised about the actualDERs reported for PICIC and NDFC as these differed substantially fromindependent computations. (2) Collection targets in absolute amounts weredefined as covenants and substantially met according to supervision reports,but data from the files are spotty.

Sources of data: SARs, supervision reports, and the DFIs. Where there was aconflict of data, the SARs and supervision reports were utilized.

- 15 -

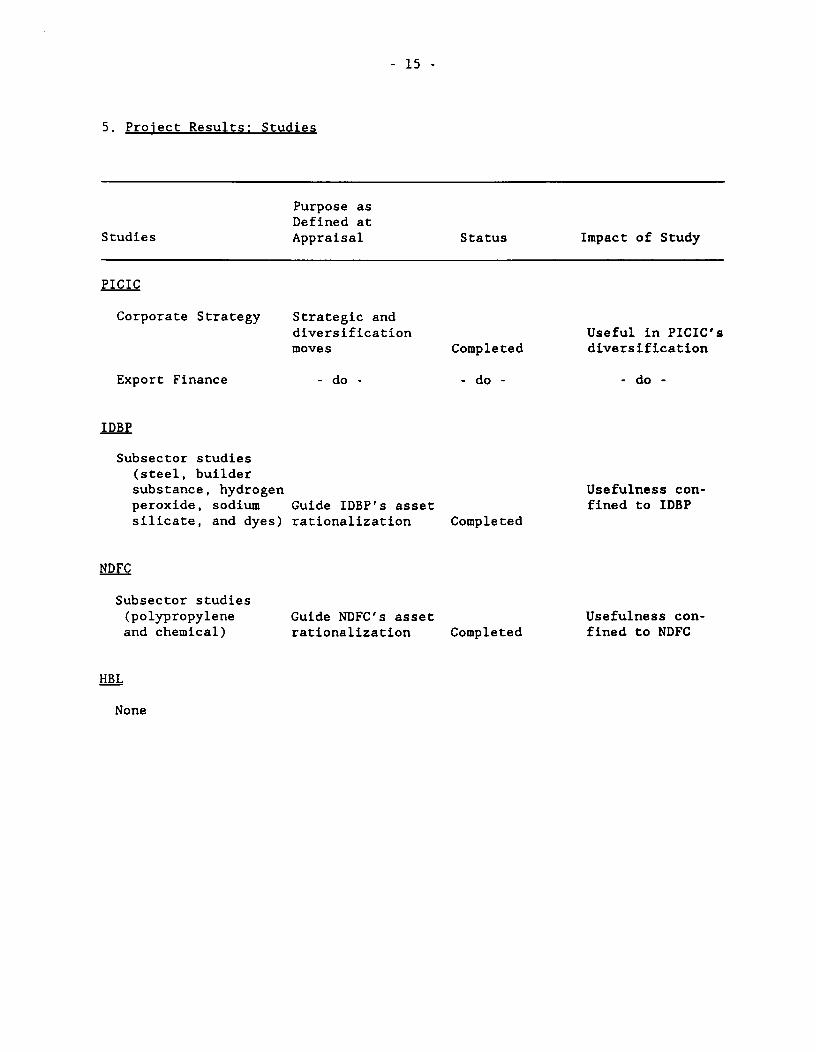

5. Project Results: Studies

Purpose asDefined at

Studies Appraisal Status Impact of Study

PICIC

Corporate Strategy Strategic anddiversification Useful in PICIC'smoves Completed diversification

Export Finance - do - - do - do -

IDBP

Subsector studies(steel, buildersubstance, hydrogen Usefulness con-peroxide, sodium Guide IDBP's asset fined to IDBPsilicate, and dyes) rationalization Completed

NDFC

Subsector studies(polypropylene Guide NDFC's asset Usefulness con-and chemical) rationalization Completed fined to NDFC

HBL

None

- 16 -

6. Status of Covenants

Name of PFI/ Com-Legal Basis Covenant Description pliance Remarks

1. Under IIC I

Minutes of tech-nical discussionsof 11/28/83-12/02/83

PICIC - DSCR: 1.1:1 min. OK Questions raised aboutcompliance computationsafter loan/credit closing.

- DER: 7:1 max.

- Collection targets Deficiencies noted infor CY1983-85 OK actual performance but

progress was deemedacceptable.

IDBP - DSCR: 1.1:1 min. OK Nominally complied,although breached inthe past.

- DER: 5:1 max. OK- Collection targets Almost nominally met

for FY1984-86 OK but the Bank expressedconcern about risingarrears. Serious deterio-ration later promptedineligibility.

NDFC -' DSCR: 1.1:1 min. OK- DER: 5:1 max. OK Questions raised aboutbut could be raised compliance computationsto 7:1 at NDFC's after closing.request OK

- Collection targets:none N.A.

NCBs - No financial covenants N.A. The DSCR and D/E covenantswere not deemed appro-priate; reliance wasplaced on liquidity andand operational ratios asmonitored by PBC.

Note: The date of the PCR preparation was used as the benchmark date fordetermining compliance with IIC I covenants. N.A. - not applicable

- 17 -

Name of PFI/ Com-Legal Basis Covenant Description pliance Remarks

2. Under IIC II

Minutes of tech-nical discussionsof 10/29/85-11/05/85

PICIC Eligibility Criteria- DSCR: 1.15:1 min.

in FY86 & 1.2:1 thence OK- DER: 7:1 max.

(special def. of debt) OK- Return on average

equity: 12% min.Collection targets OK

for FY86-90:Cash collections: fr.Rs. 575 to 1000 million OKTotal collections: fr.40 to 60% OKColl. of current dues underpost '81 loans:75% throughout OKPortfolio infection:fr. 30% to 20% max. OK

Viability Indicators- Return on ave. total

assets: 2% min. OK- Return on ave. capital Initially complied with;

employed: 2.25% min. OK later declared ineligible- Adm. exps./ave. total but was reinstated in

portfolio: 1% max. OK 07/90.

IDBP Eligibilitv Criteria- DSCR: 1.15:1 min.

in FY86 & 1.2:1 thence OK- DER: max. 7:1(special def. of debt) OK

- Return on averageequity: min. 12% OK Computations include provi-

sions as part of profit.Collection targets

for FY86-FY90:Cash collections: fr.Rs. 500 to 1000 M ACT Noncompliance is traced toTotal collections: fr. the highly problematic

- 18 -

40% to 65% ACT portfolio of IDBP (seeColl. of current dues: paras. 1.02, 3.02, 4.05,75% throughout ACT and 6.02 of the PCR text).Portfolio infection: Ineligible.fr. 40% to 15% max. ACT

Viability Indicators- Return on ave. total

assets: 1.2% min. ACT- Return on ave. capital Partial compliance:

employed: 1.25% min. OK declared ineligible- Adm. exps./ave. total later due to failure

portfolio: 1.2% max. ACT to meet covenants

NDFC Eligibility Criteria- DSCR: 1.25:1 min. OK- DER: 5:1 max.

(requested increaseto 7:1 to be reviewedbased on FY86 results) OK

- Return on averageequity: 20% min. n.a.

Collection Targetsfor FY85-90:Cash collections: fr.70% to 80% OK

Overall collections:fr. 75% to 85% OKPortfolio infection:20% max. OKSatisfactory arrearsrecovery/restruct.program OK

Viability Indicators- Return on ave. earning

assets: 2.5% min. OK- Adm. exps./ave. total

portfolio: 1% max. OK

NCBs - No DSCR/DER covenants The DSCR and D/E covenants(audit satisfactory N.A. were not deemed appropriate;to the Bank) reliance was placed on

liquidity and operationalratios as monitored by PBC

Collection Targetsfor Bank-financedprojects: 75% min.HBL ACT Breached '90; inelig. '91UBL ACT Breached '89; inelig. '89

portfolio infection:15% max.

HBL OKUBL ACT Ineligible in 1989

- 19 -

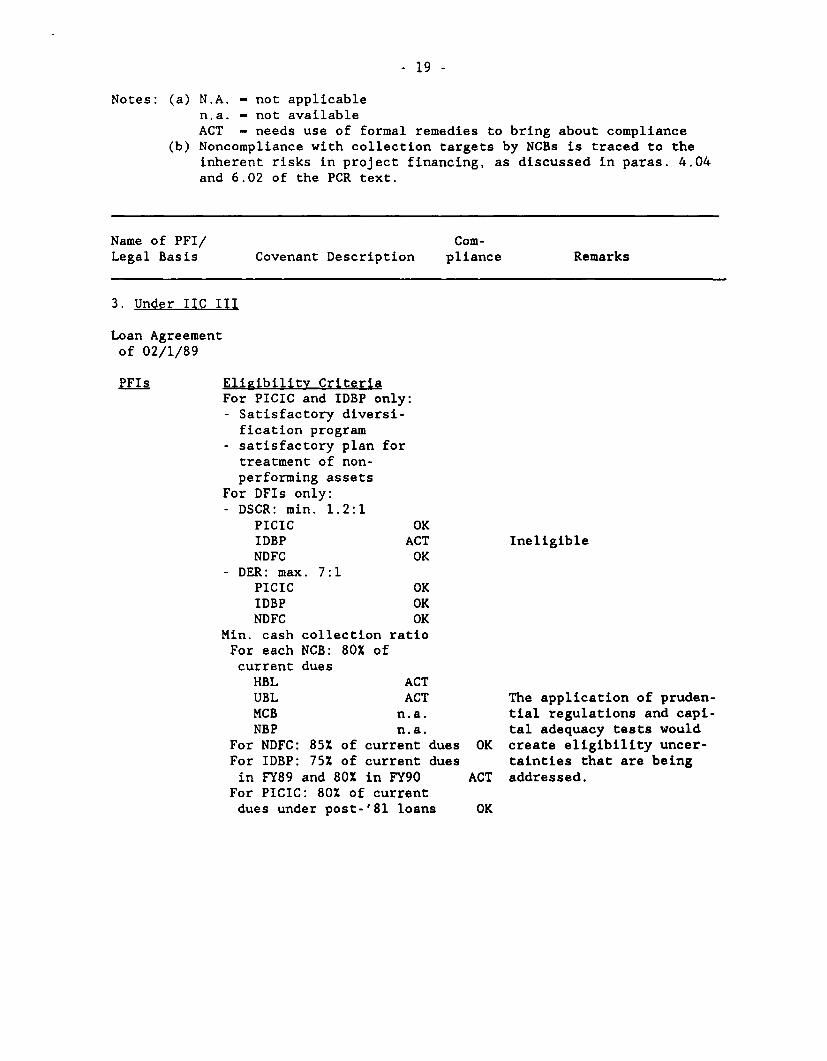

Notes: (a) N.A. - not applicablen.a. - not availableACT - needs use of formal remedies to bring about compliance

(b) Noncompliance with collection targets by NCBs is traced to theinherent risks in project financing, as discussed in paras. 4.04and 6.02 of the PCR text.

Name of PFI/ Com-Legal Basis Covenant Description pliance Remarks

3. Under IIC III

Loan Agreementof 02/1/89

PFIs Eligibility CriteriaFor PICIC and IDBP only:- Satisfactory diversi-fication program

- satisfactory plan fortreatment of non-performing assets

For DFIs only:- DSCR: min. 1.2:1

PICIC OKIDBP ACT IneligibleNDFC OK

- DER: max. 7:1PICIC OKIDBP OKNDFC OK

Min. cash collection ratioFor each NCB: 80% ofcurrent duesHBL ACTUBL ACT The application of pruden-MCB n.a. tial regulations and capi-NBP n.a. tal adequacy tests would

For NDFC: 85% of current dues OK create eligibility uncer-For IDBP: 75% of current dues tainties that are beingin FY89 and 80% in FY90 ACT addressed.

For PICIC: 80% of currentdues under post-'81 loans OK

- 20 -

7. Use of Bank Resources

A. Staff Inputs(Staff Weeks)

Stage of StaffProject Cycle Period Weeks

Up to Preparation FY83 27.9

Preparation through Approval FY83-84 46.4

Negotiations FY84 7.4

Processing FY83-84 15.9

Project Administration FY84-86 2.2

Supervision FY83-91 57.7

PCR Preparation FY92 8.0 1/

Total 165.5

1/ Budgetary estimate.

Notes: The regional average coefficient for sector loan project is normally125 staff weeks, which is below the estimated 165.5 staffweeks for IIC I. Thefigure of 57.7 staff weeks for supervision is below the budgetary norm, giventhe assumed normal frequency of two supervision missions per year and 12staffweeks of supervision coefficient. It appears that the staff time devotedto preparation up to approval was higher than normal in the light of thecontroversy that the project initially generated.

- 21 -

B. Missions

OverallActivity Period/ No. of Days in Project Comments

Report Date Persons Field Rating

Identifi- 03/82 N.A. N.A. N.A. Project's design discussedcation within the context of the

overall findings of theFinancial Sector Review.

Prepara- 12/01/82-tion 12/22/82 4 1/ 21 N.A. Coverage: industrial and

financial sector reviews;project design.

Pre-Apprai- 03/01/83-sal 03/19/83/ 7 Z/ 18 N.A. Progress achieved in re-

12/30/83 viewing term lenders; pro-ject arrangements andissues defined; missionconverted into appraisalmission.

Post-Appraisal 08/14/83-

08/30/83/ 2 14 N.A. DFIS lobby against inclu-12/30/83 sion of NCBs; GOP reserva-

tions about inclusion ofNCBs; compromise that theBank will limit supervisionof NCBs to term lending.

Supervision 08/17/84-08/26/84/ 2 3 1 Satisfactory progress10/15/84 noted; project ahead of

schedule; all PFIs exceptPICIC show operational andappraisal improvements;need for extensive supervi-sion of PICIC and IDBPdue to problem portfolios.

Supervision 01/08/85-01/27/85/ 3 5 1 5 PFIs eligible; highly03/12/85 satisfactory implementa-

tion; competition and

- 22 -

better PFI services;PICIC and IDBP show notableimprovements in collectionsand infection, and diversi-fy into money market opera-tions; NDFC expands butshows deterioration inappraisal standards; HBLand UBL highly regarded.

Supervision 10/11/86-10/21/86/ 3 5 2 Slowed implementation due02/05/87 to external factors; TA

proceeding well; creditdelivery system workingwell; low collections asource of continuedconcern; PICIC and IDBPcommission organizationand diversificationstudies; HBL and UBL port-folio problems becomeevident.

Supervision 03/24/89-04/07/89/ 4 5 2 Subloan cancellations05/24/89 prompt extended closing;

management turnover atPFIs and GOP interferenceimpact negatively; PICICand IDBP delayed in imple-menting diversificationmoves, in violation ofBank agreement; IDBP alsoin violation of financialcovenants under IICprojects; NCBs performwell but subject tomanagement turnover.

Supervision 10/20/89-11/03/89/ 4 5 2 Similar observations as11/29/89 in 05/24/89 report; PICIC

DSCR and collection ratiosdrop below covenants; 2PICIC directors viewed aswillful defaulters; IDBPsuffers liquidity problem;IDBP remains ineligible;growing arrears problemfor other PFIs.

- 23 -

Supervision 03/26/90-04/04/90/ 2 3 2 Three-year delay in04/26/90 closing; management turn-

over and GOP interferenceimpacted negatively; PICICdeclared ineligible underIIC II and III, subjectto review; IDBP prospectsdoubtful; NDFC stretched;UBL declared ineligibleunder IIC II.

/ In addition, the Division Chief joined the mission for 4 days.2/! In addition, the Division Chief joined the mission for 2 days.

Note: Where there were multiple projects covered in a given supervisionreport, the time allotment for IIC I was accordingly prorated. This estimationmethodology was used in the absence of an alternative existing Bank mechanism.Please note, however, that this estimation process yields an aggregatesupervision manpower input materially higher than the figure shown in theimmediately previous table on "Staff Inputs" derived from MIS data. Thisdiscrepancy is partly explained by TRS recording discrepancies vis-a-vis: (a)the actual time spent in the field; and (b) the estimation methodology usedabove.

- 24 -

Annex 1

PAKISTAN

Project Completion ReportFirst Industrial Investment Credit

Sectoral Allocation(Percentage Distribution & No. of Projects)

DF Is NCBsTotal PIO NOFC HSL NCSs

Subsector AmI No Amt No Amt No Amt No Amt No Amt No

Textile 32 16 62 12 14 2 4 1 29 1Paper, paperproducts & printing 16 4 - - 20 1 32 1 33 2 - -

Food products &processing 20 8 16 3 41 3 13 1 11 1Engineering 7 7 - 9 1 38 3 20 2 100 1Chemical &petrochemicaLs 8 6 19 5 - 6 1 - - -

Cement, cermic >ass 2 4 1 1 5 1 9 2 - - -

AgricuL. & forestproducts 4 4 2 1 11 2 - 6 1 -Minerals 9 - - - - - - - -

MisceLLaneous 1 2 - - - 4 2 - - -

Totat 100 51 100 2 100 10 100 11 100 7 100 1

Source of basic data: Bank records

Annex 2

PAKIStAN

Project Cmpltion *eport

first irsatrisl Iwvestment Credit

Ex-Ante Profile of StAWrojects

Tit.o

PfI Jdb at rm*mment fInanel New vs. lw tmntI ts ofSm Sib-Borrowers Subt*Ctor IEN flkS Full Ce. D/E DtCt Strength of Sposure Existing (. milli.er Appraisel Report

PICIC Shsksrgsnj Nille ChmIcal V.A 34 N.A. 50:50 2.2 Experlenced Adeate Exieting 26 only gt_nry with Ink launsPICIC Automotive Sattery Clmlcel 42 25 I" T0:30 2 Experlenced Adqete New 56 AdeqLate with ** issuesPiCIC lextoriuI Ltd. Textite-other 20 IS 110 u3:11 1.h Experlenced Adequate new 112 Adeqate with Bnk issuesPICIC Pakistan Polypropylen Chemical 41 20 -0- 60:40 1.4 Experiemned Aderate Existing 20 Ader=tePICIC teckitt k Colt_n food 50 4U 22 59:61 11.8 Experlenced Adequate Exsltin it Ad tPICIC Zehur Textile textile-cotton 25 22 130 00:20 2.2 Exprlenced Adequte New 91 Adeate with Eank lsasLrPICIC Surewala lextiles Textile-cotton N.A l.A 0 56:44 4.1 Experienced Adequte Existing 55 AdeatePICIC Amin Synthetics Ch_mical 37 It 15e6 0:40 1.6 Experlenced Adequate New 63 AdeqatePICIC English Biscuit food 50 22 *5 66:32 4.1 Experienced Adequate Existing 29 AdeutePICIC Star lextite Textile-cotton N.A N.A 40 69:31 2.3 Experlenced A t Existing 43 AdquatePICIC $Srene Textiles Textite-other 4? 24 46 65:35 2.1 Experienced Adquat ow U AdequatePICIC Crescent Textile lextile-cotton N.A. 1.A l.A. 53:47 5.2 Eerlenced Adequate Existing 49 AdeqatePICIC Jetol Foods food 32 25 130 5: 1.6 Limited exper. Ade"te Sew MI Ade 'atePICIC Ovta Textile Textile-cotton 26 17 N.A. 71:29 3.5 Eprlenced Adaquate Exliting 14 Ade teID1 Pak Selt Agrit. A Forest e 30 70 67:33 2.3 Exriened Adequate New 33 Adequatteiow AI-Axlf Suwar Food 19 is 8o9 65: 1.6 Experilamd Ada"te, Nw 346I1P Al-Neyst Dairiee food 25 30 97 79:21 4.0 Experienced Adte Sew oo Adeute19 Big Miak Foode Food 40 23 00 79:21 1.3 J ustioneble Adeqte Sew 5S Defi c1nt on _npnt. ineysisleow Sind Glass Glass I? 1 3" nl 23 1.5 Experlenced Limited W 222 eficientIlUO Punial Cables Engin ering 15 26 92 6o:20 1.o Limited esper. Limited SeW 119 Deficient In tktng.q tin ncletIMP Cloroe Textiles lextile-cotton 33 32 132 61:39 2.9 limited e*per. UrInau New 133 Adeute with me sBtk Issueslow Service Indtutries Agric. A forest 10 16 21 60:40 3.6 Experleneed Adequate Existing 29 Deficient en mkt. 9 prod. aspectsIop Setimntal Woolen Textile-others I.A 32 N.A. 60:40 2.2 N.A s.A Existing 34 NO textua IU tysia: only dateIDU Century Papr 20 21 de- tSO15 1.5 Experimned Adeqte Stw 306 Adutten fin. 2 tech, issuesIFC Crescent Steel Englneering le 25 62 *5:15 2.4 tUtnoewn Inot Sew 165 Ad t with unk leesnDtC Alltin Engineer Engineering 16 22 N.A. 75:25 2.4 ExperI end Adequate Existing 30 Deficient In neltyis eot akt E firniellsxecoefC footilb Ltd. NiscellaeoWua N.A r.A N.A. 79:21 I.6 Experienced La*nmon Sew 3S Only * swry reportDFC Zesl Pak C_nt Cent 50 23 19 n5:25 4.6 Exrriened Adqute Existing 25S Deilcient on technical mirketigqIfC flull fourdation per 14 21 69 57:43 2.0 Limited Adequat Sew 191 Adete except for tagmnt aspectsIDfC D.I.Khn uck CGovEt.org.) Ceramic 1.A *.A N.A. 100I0 Ao.7 tliIted We k Se 19 Deficient In et ectIFC Precisien Engineering Englneering 1.A *.A 47 30:20 S.A Limited Week Sew IZ enly sairy report bxut deficientIfC Req Dairies food 16 19 as 78:22 1.9 Experienced tUknown Sew 62 Adeq. extept for finenisla of sponsors*FC ronars Corp. Nisceetn 16 51 sY 80:20 3.1 Limited UknkeWn Sew 17 Snr report onlyDFC teer Broas Chmicel 34 31 N.A. 59:41 5.0 Experienced Adequate Existing Si Adqute"Sal Amaeios food IS 20 121 00:20 1.6 Experlenced Adate W 54 Adte: Well prentedIIU Century Ppr 20 21 445 15:15 1.5 Experlenced Adequate Sew 306 Adte with fin 6 t issueML Agriunt Engineering 22 16 422 S9:41 1.7 Eprlenced Adequat Exiatin 109 Ad te wexept for no IEttIbt lletlenttl AdeegIv, Paper 2? 22 45 60:40 2 2 Experi need Adequate SeW 26 AdauteNK feres foods Agric. I Forest 26 0 S2 10:30 I17 Experieced Ade S 39 AdeqttteUi Gets Aumtive_ EIngineeIng 50 20 104 70:30 1.0 Experienced Adte Sew 39 adte (conratuted)_ a_r Cottotn Textile-cotton 30 10 299 65:35 1.4 Experienced Adeqate Se t33 Adeacte

UK Atles Autee Enginteerin 24 26 91 77:23 2.4 Experinced Ad te Existin 65 A46quote with 6t issues

Notees: at) rlde finatg Is trated as dubt for pjPoees Of ctAting the DE ratio.tb) N.A. * not *pticMbte or talatbte