world bank document€™s assume that the leased asset’s original book value is $1,000. lease...

TRANSCRIPT

MAY-JUNE 2001, Issue 3 (15)

THEORY AND PRACTICEHow Lessees Should Analyze the

Financial Terms of Lease Agreement

pg. 2

The Lease Agreement: a Lessee’s Perspective, Part 2

pg. 4

How Leasing Companies Can Minimize Risks

pg. 7

LEASING IN REGIONSLizing-Biznes Tymen Leasing Company

pg. 10

Petersburg Leasing Association

pg. 13

Leasing in the Northwest Region of Russia

pg. 14

SMALL AND MEDIUM-SIZED BUSINESSKontinent Plast, St. Petersburg

pg. 16

Telefonstroy Company, Novocheboksarsk,Republic of Chuvachia

pg. 17

OUR PROJECTNews, training

pg. 19

LEGISLATIVE NEWS

pg. 22

NEWSPress Digest

pg. 25

QUESTIONS AND ANSWERSpg. 30

KONTINENT PLAST, ST. PETERSBURG

Packaging Company Expands Production UsingLeasing

As we walk through Kontinent Plast’s polyethylene pack-aging plant, located on the outskirts of St. Petersburg,Igor Bobylev, Financial Director of Kontinent Plast,

explains how his company first began and how it works today.

The Russian packaging industry took off in the mid-1990s asRussian consumers grew more accustomed to seeing a wideselection of goods on store shelves and became more dis-criminating shoppers. Although the shelves were stocked withboth imported and Russian goods, consumers neverthelesspreferred imported goods over their Russian counterparts.One of the main reasons for this choice was the attractivepackaging of the imported goods.

The present managers of Kontinent Plast were among thosewho understood that Russian products were no worse thanwestern ones, and that all that was needed was to packagethem better. At first the entrepreneurs began to import poly-ethylene packaging from Finland. Then, in 1997 they decidedto produce their own packaging. In order to do so, they rent-ed a factory and began to renovate it.

Continued on page 16

C O N T E N T S :

INF

OR

MA

TIO

NB

UL

LE

TIN

http://www.ifc.org/russianleasing

Published by the Leasing Development Group of the International Finance Corporation (IFC), a Member of the World BankGroup, with financial support from the Canadian International Development Agency

39585P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

2

Russian law allows for considerable freedom indetermining the size, methods and forms oflease payments. Lessors and lessees are free

to negotiate terms that they find mutually agreeable.

In this article, we will discuss some important fac-tors that lessees should consider during the negoti-ating process.

The leasing company’s essential aim, when calcu-lating lease payments, is to cover all of its relatedexpenses and turn a profit. Lease payments usuallyinclude compensation for the cost of the leasedasset, the leasing company’s loan interest, the costof any additional services that the leasing companyhas to provide the lessee either before or during thelease term, and any taxes that the leasing companyincurs in connection with the lease.1 Perhaps themost important question of all is the leasing compa-ny’s commission, so let’s begin our discussion there.

The Leasing Company’s Commission

Inexperienced lessees often make the mistake ofasking leasing companies the following question

during their preliminary negotiations: «How much isyour commission?» One leasing company might say5%, another 10%, and a third 12%. But a closer lookright reveal that all three figures work out to beexactly the same. How can that be?

Not only does the name of this payment vary from onecompany to the next («margin,» «commission,» etc.),so does its actual composition. Some leasing compa-nies include taxes, insurance payments and otherexpenses in their stated rate of commission, while oth-ers do not. One way or another, every leasing company

will require compensa-tion for these expenses;the only question iswhether they will bedefined as part of thecommission or as sepa-rate components withinthe lease payments.

As we mentioned atthe beginning of thisarticle, lessors andlessees are free todetermine the sizeand methods of the lease payments as they see fit.Therefore, the sums on which the commission isbased can also vary from one company to the next.For example, a 5% commission based on the leasedasset’s original book value may be identical to a10% commission based on its residual value at thebeginning of each payment period or a 12% com-mission based on its residual value at the end ofeach period. Let’s consider an example:

Example:Let’s assume that the leased asset’s original book

value is $1,000. Lease payments are made quarter-ly. The asset depreciates at an annual rate of 12%,and the parties have agreed to apply an accelera-tion factor of 3, so the asset depreciates fully overthe term of the lease.

Leasing Company A charges a 5% annual commis-sion on the leased asset’s original book value. Thus,the lessee must pay a commission of $12.50 everyquarter. Over a three-year term, this adds up to $150.

Leasing Company B charges a 10% annual com-mission on the leased asset’s residual value at thebeginning of each payment period. The amount ofcommission therefore decreases over time, andafter three years it adds up to the same total: $150.

May-June 2001THEORY AND PRACTICE

HOW LESSEES SHOULD ANALYZE THE FINANCIALTERMS OF A LEASE AGREEMENT

Veronika Shtelmakh, Economist

IFC Leasing Development Group

Veronika Shtelmakh, Economist

IFC Leasing Development Group

The LeasingCourier has already devoted several articles to the subject of lease payments, but until now we havealways written from the perspective of the lessor. In this article, we will write about the interests of the lessee.We hope that these materials will enable lessees to make judicious comparisons of the financial terms offeredby different leasing companies.

1 Potential lessees should not be put off by this long list of

expenses. Because leasing enjoys a number of tax benefits and

other privileges, it is not as expensive as this list might suggest.

Commission for Leasing Company B(1) – Payment Number(2) – Residual Value at Beginning of Payment Period(3) – Lessor’s Commission (Based on Residual

Value at Beginning of Period)

(1) (2) (3)

1 1,000 24.752 910 22.523 820 20.304 730 18.07First Year Total 85.645 640 15.846 550 13.617 460 11.398 370 9.16Second Year Total 50.009 280 6.9310 190 4.7011 100 2.4812 10 0.25Third Year Total 14.36Overall Total 150

Leasing Company C charges a 12% annual com-mission, but it bases these charges on the leasedasset’s residual value at the end of each period, sothe end result is the exactly the same.

Commission for Leasing Company C(1) – Payment Number(2) – Residual Value at Beginning of Payment Period(3) – Lessor’s Commission (Based on Residual

Value at Beginning of Period)

(1) (2) (3)

1 910 27.002 820 24.303 730 21.604 640 19.00First Year Total 91.905 550 16.306 460 13.607 370 11.008 280 8.30Second Year Total 49.209 190 5.6010 100 3.0011 10 0.3012 0 0.00Third Year Total 8.90Overall Total 150

Asking about the lessor’s rate of commission clear-ly isn’t very helpful. This is the wrong question to ask.Even if the lessor tells you exactly how he calculateshis commission, you still need additional informationbefore you can make a wise decision. What do youneed to know in order to compare the financial termsoffered by different leasing companies?

Comparing the Financial Terms Offeredby Different Leasing Companies

Imagine a company, Boxes Inc., that specializes inmanufacturing cardboard boxes and wishes to

expand its production. It decides to lease a newpiece of equipment that carries a price tag of$350,000 (10 million rubles at an exchange rate of28.57 rubles to the dollar). It wants to pay off thelease over a three-year period (12 quarterly pay-ments). It submits applications to three leasingcompanies. Some time later, it receives the follow-ing estimates:

Total Lease Payments (in rubles)2

Aurora 17,573,600Babochkin & Co. 17,573,600Mona Lizing 17,573,600

Does this mean that the estimates are all thesame? Not at all. Even if the total sum of the leasepayments is the same for all three companies, thereare several other factors that will affect the lessee’scash flow:1) The distribution of the payments over time2) The payment due dates (beginning or end of fis-

cal period)3) The frequency of the payments.

In the next issue of the Leasing Courier, we will take

a closer look at how these three factors actually affect

the lessee’s expenditures. We will also consider what

happens if the leasing company pegs the value of the

lease payments to exchange rates.

May-June 2001 3THEORY AND PRACTICE

2 Let’s assume that the lessee will have no other expenses in

connection with the lease — just the lease payments themselves.

4 May-June 2001THEORY AND PRACTICE

THE LEASE AGREEMENT: A LESSEE’S PERSPECTIVE

Olga Shishlyannikova, Attorney

Continued from Issue #3 (14) IFC Leasing Development Group

R e s c h e d u l i n gLease Payments

One of thel e s s e e ’ smain obliga-

tions under a leaseagreement is tomake regular leasepayments. In thisarticle we will notconsider the financialaspects of lease pay-ments, but instead

focus on a single legal aspect: how to restructurethe lease payment schedule during the term ofthe lease.

Since every entrepreneur depends on finan-cial stability in his business and must be able topredict his expenses, lawmakers have estab-lished that rent payments (including lease pay-ments) may not be rescheduled except by themutual consent of all interested parties. More-over, lease payments may not be rescheduledmore than once per year, even by mutual con-sent, according to Article 614, Clause 3 of theRussian Civil Code.

In order to protect themselves against theinstability of the Russian ruble, leasing compa-nies generally quote the value of the lease pay-ments in dollars (or any other freely convertiblecurrency), which is permissible under Russianlaw. However, this arrangement offers no pro-tection to lessees. This became painfully evi-dent after the financial crisis of August 1998.The arbitration courts did not find the several-fold devaluation of the ruble a sufficient reasonfor freeing lessees from their financial obliga-tions. The Federal Arbitration Court of theNorthwest Region ruled that companies thathad entered into agreements prior to the Crisisshould have foreseen high levels of inflation.Those that committed themselves to financialobligations in dollar equivalents were subjectingthemselves to high currency risks.1 Thus,lessees essentially had no legal recourse if

lessors refused to reschedule their lease pay-ments. In order to protect themselves againstthis sort of scenario in the future, lesseesshould be sure to write provisions into the leaseagreement requiring the lessor to reschedulethe lease payments under certain circum-stances, such as drastic changes in exchangerates.2

One often sees lease agreements where thevalue of the lease payments is not expressed as afixed sum, but rather as a formula. A provisionthat allows one of the parties to adjust the valueof the lease payments under certain circum-stances (such as major fluctuations in interestrates or the Central Bank’s refinance rate) canalso be considered a kind of formula. If the leas-ing company wishes to write such a provision intothe lease agreement, the lessee should keep thefollowing points in mind:• If the lease payments are pegged to interest

rates or the Central Bank’s refinance rate, theywill have to be adjusted whether these factorsrise or fall. Considering that both have beenfalling recently, it will be in the lessee’s interest,not the lessor’s, to restructure the lease pay-ments.

• Be sure to write a clear formula for restructur-ing the lease payments into the lease agree-ment. Lease agreements often stipulate thatthe lease payments will increase in proportionto any increases in the size of their compo-nents. However, they sometimes fail to specifywhether this proportional increase pertainsonly to the relevant component (e.g., compen-sation for the lessor’s loan interest) or to thetotal value of the lease payment.

• Also be sure to include a precise and unam-biguous definition of the possible grounds forrescheduling the lease payments. Such phras-es as «significant changes in the Russian econ-omy» are far too vague.

Olga Shishlyannikova, Attorney

IFC Leasing Development Group

1 See the Federal Arbitration Court of the Northwest Region’s

ruling on case #A56-14871/99 (09/27/99).2 The parties should agree beforehand on a formula for

restructuring the payments.

The Lessor’s Control over the LeasedAsset and the Lessee’s Actions

As the lessee’s creditor, the leasing companyalways has a vested interest in the lessee’s sol-

vency. For this reason, the leasing company willalways wish to maintain some control over both theleased asset and the lessee’s actions. Most leaseagreements contain provisions that authorize theleasing company to exercise this kind of control.However, these provisions often violate corporatelaw, particularly the Federal Law on Leasing.

The lessor’s right to exercise control over theleased asset is dealt with explicitly under Articles37 and 38 of the Law on Leasing. These two arti-cles are terribly flawed, especially where theygive lessors the right to audit the lessee’sfinances and sit in on the lessee’s board meet-ings (Article 38, Clause 4), both of which areclear violations of Russian corporate law. Everycommercial enterprise has its secrets; forcinglessees to divulge every scrap of informationabout themselves to their lessors could endan-ger their businesses. That is why corporate lawmakes very specific provisions regarding corpo-rate governance and the procedures for auditinga company’s finances. The Law on Joint-StockCompanies, for instance, is very specific aboutwho has the right to attend shareholder meetings(Article 51) or initiate a financial audit (Article86). The Law on Leasing’s generosity towardslessors, in allowing them to attend their lessees’board meetings and audit their finances, is bothlegally dubious and ethically unacceptable, as itconstitutes a clear infringement of the lessee’sinternal affairs.

Therefore, the lessor should be made tounderstand that he will not be able to exercisehis «rights» under Article 38, Clause 4, of theLaw on Leasing without the lessee’s consent.We should also note that the Law on Leasingonly gives lessors the right to attend thelessee’s board meetings or launch a financialaudit if the lessee has defaulted on his leasepayments. We should add, however, that it willreflect well on the lessee and serve as proof ofhis good intentions if he does allow the lessor toexercise these rights.

In practical terms, we would like to offer lesseesthe following recommendations:

• Unless your business works 24 hours a day, besure to restrict the lessor’s access to the leasedasset to working hours only.

• Specify which documents the lessor may requisi-tion and under which circumstances; also stipu-late how much time you will have to prepare andsubmit these documents.

• Limit the lessor’s access to your board meetings(i.e., the topics of discussion that he may hear).

Contract Annulment Due to Non-Compliance or Payment Default by the Lessee

All of the parties to a lease have a vested inter-est in seeing that the terms of the lease agree-ment are fully observed. In real life, however, itoften becomes necessary to terminate the agree-ment. For the wronged party, this is usually a last,desperate resort. Since the lessee is the debtorunder a lease agreement, it is usually the lesseewho precipitates annulment by failing to honor hisobligations.

Article 450 of the Russian Civil Code stipulatesseveral grounds for annulling an agreement. Itmakes a clear distinction between the right todemand annulment and the right to renege onone’s obligations. Allowing the lessor the right torenege on his obligations makes the lease agree-ment less stable and therefore less attractive tothe lessee. In this section we will focus on one ofthe most common grounds for annulling a leaseagreement: the lessee’s failure to meet his leasepayments for three or more consecutive periods.

Russian law is somewhat inconsistent on thisquestion. Article 619 of the Russian Civil Codegives lessors the right to sue for annulment if thelessee fails to make his lease payments for morethan two consecutive payment periods. Article13 of the Law on Leasing, on the other hand,simply gives lessors the right to renege on theirown obligations under these circumstances. TheCivil Code has precedence and cannot be over-ridden by either the Law on Leasing or the par-ties’ mutual consent. Therefore, the lease agree-ment cannot legally authorize the lessor to uni-laterally annul the agreement in the event of pay-ment default.3

May-June 2001 THEORY AND PRACTICE 5

3 Current legislation also gives the lessor the right to sue for

annulment if the lessee misuses or significantly impairs the

leased asset, or if he fails to perform required maintenance.

Leasing companies often try to get around Arti-cle 619 of the Civil Code by stipulating that theyhave the unilateral right to annul the lease agree-ment if the lessee fails to make his payments with-in, say, 30 days of their due date. While such pro-visions are not in direct violation of Article 619,they can hardly be considered legal. The courtsare unlikely to uphold such practices, since it isunfair to institute a simpler procedure for annullingan agreement (unilateral termination, rather than alawsuit) for a lesser offense (30 days’ lateness,rather than 3 or more consecutive non-payments).

In conclusion, we should add that the partiesare free to stipulate provisions for unilateralannulment under any other circumstances thatare not covered under the Civil Code or otherlegislation.

Provisions for Redeeming the LeasedAsset

Lessees generally opt for leases in the first placebecause they do not have enough working cap-

ital to make an outright purchase of the equipmentthey need, and most lessees would generally like toassume ownership of the leased asset upon expira-tion of the lease. If the lessee intends to assumeownership of the leased asset, he should be sure toinclude provisions for redeeming the asset withinthe lease agreement itself. Current legislation doesallow the parties to conclude this kind of «mixed»agreement, consisting of both a lease agreementand a sales agreement.

Lessees should bear in mind that a lease agree-ment cannot be considered anything more than apreliminary sales agreement if it fails to specifythe exact terms for redeeming the leased asset.These include a time frame for transferring own-ership rights and an exact redemption price.

According to Article 429, Clause 4 of the Russ-ian Civil Code, a preliminary agreement shouldspecify the date on which the parties will con-clude the primary agreement. Otherwise, theprincipal agreement must be concluded withinone year after the preliminary agreement wassigned. Therefore, unless the lease agreementspecifies an exact date or other time frame forconcluding the redemption agreement, the lattermust be signed within one year. Otherwise, thelessee will lose his right to redeem the leased

asset (Article 429, Clause 4, of the Russian CivilCode). From the lessee’s perspective, it would bebest to stipulate a time frame for concludingredemption of the lease asset,4 rather than forconcluding the primary agreement.

It is extremely important to stipulate the leasedasset’s redemption price within the lease agree-ment. Because prices are not considered anessential condition for a sales agreement,5 omit-ting the redemption price from the preliminaryagreement (the lease agreement) will not affectthat agreement’s validity. However, it will makethe redemption price subject to Article 424,Clause 3 of the Russian Civil Code, which definesthe redemption price of a leased asset as «theprice that is normally charged for similar goodsunder similar circumstances.» The lessee shouldmake certain that the lease agreement containsspecific provisions for calculating the leasedasset’s redemption price.

Finally, we should point out that the commonpractice of simply transferring the leased asset tothe lessee without so much as a nominal redemp-tion payment is inappropriate and may invalidatethe transfer itself. Russian leasing law does notrequire the lessor to transfer ownership of theleased asset to the lessee upon expiration of thelease. Therefore, the parties must conclude alegal agreement capable of serving as a legalbasis for transferring ownership. Article 218,Clause 2 of the Russian Civil Code lists threekinds of agreements that may serve this purpose:sales agreements, barter agreements and dona-tion agreements. However, Article 575 of theRussian Civil Code prohibits donations betweencommercial entities. Therefore, the only way forthe lessee to assume ownership of the leasedasset is by concluding a sales agreement for aspecified sum.6

This article only begins to address some of the provi-

sions that can affect lessees. We would like to return to

this topic in future issues of the Leasing Courier.

Therefore, we ask that you, our readers, tell us about

your own experiences with lease agreements and the

provisions that serve to protect the lessee’s interests.

Please join our ongoing discussion!

May-June 2001THEORY AND PRACTICE6

4 Upon expiration of the lease agreement, for example.5 Unless the sales agreement is for a piece of real estate.6 See Article 454, Clause 1 of the Russian Civil Code

Analyzing the Lessee’s Financial Situation

Sources of Information

The main source of information about alessee’s current financial situation are thecompany’s own financial records. As every-

one knows, accounting records do not always givean accurate reflection of an enterprise’s real cashflow. Therefore, one must be cautious about draw-ing any direct conclusions from them. The only wayto check the accuracy of a company’s accounts isto conduct an independent audit.

A private enterprise’s accounting records includethe following:

Accounting Balance Sheet (Form #1)Report on Profits and Losses (Form #2)

Supplements to the Accounting Balance Sheetand the Report on Profits and Losses, including:Report on the Movement of Capital (Form #3),Report on the Movement of Monetary Funds (Form#4) and Supplement to the Accounting BalanceSheet (Form #5). Form #5 details an enterprise’sassets and liabilities, including its non-liquid assets,financial investments, outstanding debts and tradeliabilities.

In addition to these five documents, the leasingcompany may also request to see the following:

• An auditor’s report confirming the accuracy of thelessee’s bookkeeping records

• Tax inspection reports• A list of all debtors and creditors, including sums

and due dates• Bank statements

• A certificate of goodstanding from theState Tax Inspectorate

• Statements for allguarantee accountsnot recorded on thebalance sheet

Methods of AnalysisThe main goal in

analyzing a potentiallessee’s financial sit-uation is to determinewhether the enterprise will be able to generatesufficient cash to make lease payments and fulfillall obligations under the lease agreement. Theleasing company should try to identify some ofthe financial problems that the lessee may experi-ence over the course of the lease and to deter-mine whether these problems can be averted.When analyzing the lessee’s financial records, theleasing company should try to see the big picture:the main trends in the lessee’s financial history.The usual practice is to look at data from the lastthree years.

There are several different methodologicalapproaches to conducting a financial analysis:

• Horizontal analysis: comparing the same finan-cial indicators from one period to the next anddetermining both absolute and relative changes.This method allows one to see trends in thelessee’s financial development and calculate theoverall rate of growth. This, in turn, will help you topredict the lessee’s future cash flow.

May-June 2001 7THEORY AND PRACTICE

HOW LEASING COMPANIES CAN MINIMIZE RISKSAnalyzing the Lessee’s Current Finances and

Predicting Future Cash FlowsElena Degtiaryova, Financial Analyst

IFC Leasing Development Group

This article is a continuation of our series on risk management for leasing companies.In our last issue, we considered the main aspects of analyzing a potential lessee: why it is necessary to analyzea potential lessee in the first place, the stages of this analysis, what to do with the results of the analysis andwhich aspects of a potential project should be analyzed.In this article we will take a closer look at the kinds of information a leasing company can use to analyze apotential lessee’s financial situation - in other words, to predict whether the lessee will be able to make all leasepayments in a timely fashion. We will focus on one particularly important aspect of this analysis: analyzing thelessee’s balance sheet.

Elena Degtiaryova,

Financial Analyst IFC Leasing

Development Group

8 May-June 2001THEORY AND PRACTICE

• Vertical analysis: studying the lessee’s financialstructure in terms of relative indicators. This methodenables you to analyze the lessee in the context ofindustry conditions and external factors as inflation.

• Ratio analysis: calculating the relationshipbetween various financial data.

• Factor analysis: ascertaining the causes behindany changes in the lessee’s financial indicators.

• Comparative analysis: comparing the lessee’sfinancial indicators to industry averages or tothose of industry leaders and other competitors.

There are several aspects of the potential lessee’sfinances that one needs to examine:• Balance: an appraisal of the potential lessee’s

total assets• Liquidity: the potential lessee’s ability to meet short-

term obligations by converting assets into cash• Profitability: the potential lessee’s ability to gen-

erate profit using current assets• Return on Investment: the potential lessee’s abil-

ity to provide the lessor with a return on investment• Turnover: how the potential lessee manages

working capital

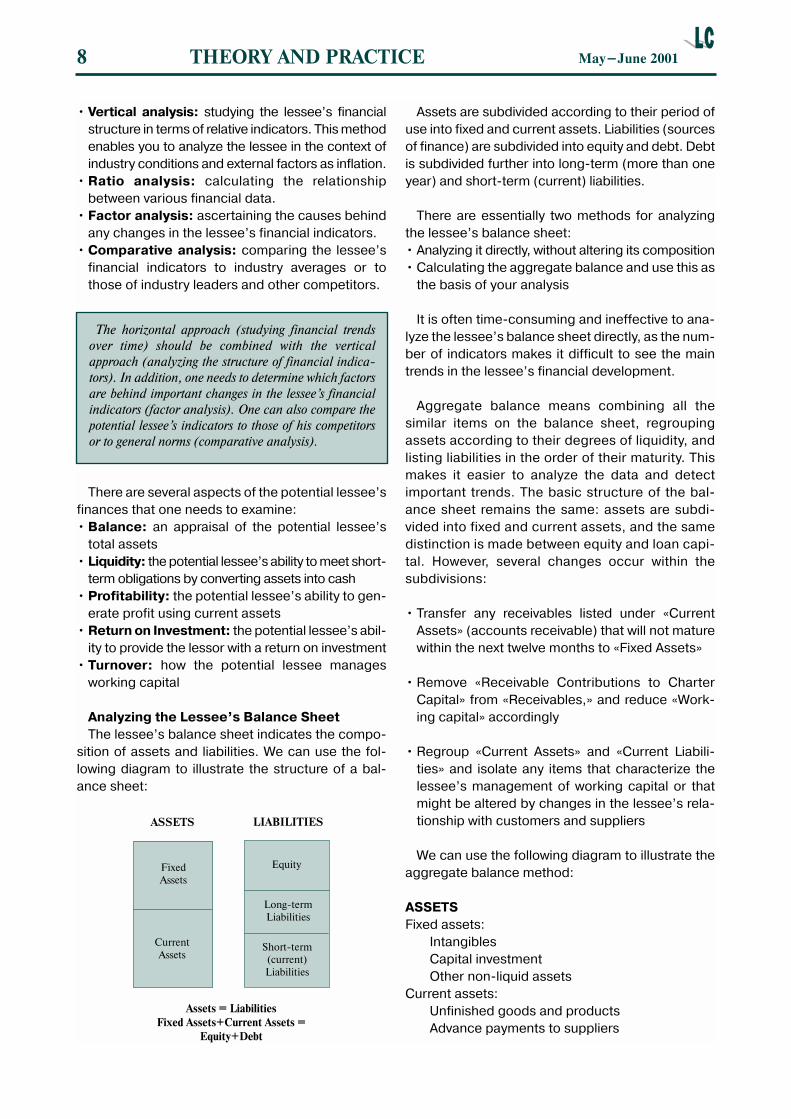

Analyzing the Lessee’s Balance SheetThe lessee’s balance sheet indicates the compo-

sition of assets and liabilities. We can use the fol-lowing diagram to illustrate the structure of a bal-ance sheet:

Assets are subdivided according to their period ofuse into fixed and current assets. Liabilities (sourcesof finance) are subdivided into equity and debt. Debtis subdivided further into long-term (more than oneyear) and short-term (current) liabilities.

There are essentially two methods for analyzingthe lessee’s balance sheet:• Analyzing it directly, without altering its composition• Calculating the aggregate balance and use this as

the basis of your analysis

It is often time-consuming and ineffective to ana-lyze the lessee’s balance sheet directly, as the num-ber of indicators makes it difficult to see the maintrends in the lessee’s financial development.

Aggregate balance means combining all thesimilar items on the balance sheet, regroupingassets according to their degrees of liquidity, andlisting liabilities in the order of their maturity. Thismakes it easier to analyze the data and detectimportant trends. The basic structure of the bal-ance sheet remains the same: assets are subdi-vided into fixed and current assets, and the samedistinction is made between equity and loan capi-tal. However, several changes occur within thesubdivisions:

• Transfer any receivables listed under «CurrentAssets» (accounts receivable) that will not maturewithin the next twelve months to «Fixed Assets»

• Remove «Receivable Contributions to CharterCapital» from «Receivables,» and reduce «Work-ing capital» accordingly

• Regroup «Current Assets» and «Current Liabili-ties» and isolate any items that characterize thelessee’s management of working capital or thatmight be altered by changes in the lessee’s rela-tionship with customers and suppliers

We can use the following diagram to illustrate theaggregate balance method:

ASSETSFixed assets:

IntangiblesCapital investmentOther non-liquid assets

Current assets:Unfinished goods and productsAdvance payments to suppliers

The horizontal approach (studying financial trends

over time) should be combined with the vertical

approach (analyzing the structure of financial indica-

tors). In addition, one needs to determine which factors

are behind important changes in the lessee’s financial

indicators (factor analysis). One can also compare the

potential lessee’s indicators to those of his competitors

or to general norms (comparative analysis).

ASSETS LIABILITIES

FixedAssets

Equity

Long-termLiabilities

Short-term(current)Liabilities

CurrentAssets

Assets = LiabilitiesFixed Assets+Current Assets =

Equity+Debt

Production stock and objects of little value orshort service life

Finished goods and products (Inventory)Accounts ReceivableCash and Cash EquivalentsOther current assets

LIABILITIES:EquityDebt

Long-term liabilitiesShort-term liabilities

Accounts payableAdvance payments from customersTaxes and dutiesPayrollOther current liabilities

Analyzing Changes in the Balance Sheet(Horizontal Analysis)By looking at changes in the balance sheet items

over time, you can determine how the lessee hasinvested or disbursed capital and financed thesetransactions.

Analyzing the Structure of the Balance Sheet(Vertical Analysis)Analyzing the structure of the balance sheet

means determining each section’s share of thetotal balance, as well as the share of individualitems within each section. This analysis will allowyou to see which items are most significant andwhich have changed the most; this in turn willhelp you determine which items require furtheranalysis.

What conclusions might you draw from the factthat the lessee’s current assets have been growing?On the one hand, it may mean that the lessee’sasset structure is becoming more flexible. On theother, it might simply mean that the lessee has beenmanaging his working capital irrationally, i.e.:

• Irrational procurement policies have increasedthe amount of raw materials in storage (this canonly be confirmed by analyzing the turnoverrate of stored materials, the specific composi-tion of these materials and the timing of theirdelivery; large surpluses may be explained bythe remoteness of suppliers and high trans-portation costs).

• Disruptions in production may have increasedthe volume of unfinished goods (one should

compare the growth rates for production andunfinished products on the balance sheet; oneshould also consider the turnover rate forunfinished products, analyze any changes inthis rate and compare it to the lessee’s normalproduction cycle).

• Sales problems have increased the volume of fin-ished goods in storage (one must compare stor-age volumes to the sum of advance paymentsreceived from buyers and analyze the lessee’snormal turnover rate for finished products).

• A decrease in consumer purchasing power hasincreased the lessee’s accounts receivable (oneshould analyze the lessee’s turnover and com-pare it to the sum of advance payments receivedand the volume of finished products).

Several factors can change the value of thelessee’s permanent assets:• The sale or purchase of new fixed assets• Depreciation of fixed assets• Revaluation of fixed assets (this can be seen in the

value of «Additional capital» under liabilities)

The lessor should also pay attention to changesin «Unfinished construction.» This item does notplay any role in the lessee’s production process,and its growth can have a negative effect on thelessee’s financial results. On the other hand, astable value under «Unfinished construction» mayindicate that the lessee has frozen his buildingprojects. A decreasing value usually indicates thatthe building projects are nearing completion(which should be accompanied by an increase in«Fixed assets»).

The lessor should analyze not only the changes inthe lessee’s assets, but also liabilities. Capitalinvestments should be drawn from long-termsources of finance, not from short-term liabilities.We will deal with this question in more detail whenwe examine the lessee’s financial stability.

In the next issue of the Leasing Courier, we will look

more closely at methods of analyzing the lessee’s liq-

uidity and financial stability.

This article incorporates materials from «How to

Analyze an Enterprise’s Financial Situation: Essen-

tial Methods,» ALT Investment Company, St. Peters-

burg, 1999

May-June 2001 9THEORY AND PRACTICE

May-June 200110 LEASING IN REGIONS

LIZING-BIZNES TYUMEN

Viktoria Struts interviews Marina Valyerevna Pushchina, deputy director of Lizing-Biznes Tyumen.

Marina Valyerevna, please tell us aboutthe history of your company. Who founded itand when?

Our leasing company, Lizing-Biznes Tyumen, wasfounded in May 1997 by Zapsibkom Bank and theTyumen Shipbuilding Plant. One of the main rea-sons for forming the leasing company initially wasto help the founders themselves acquire new equip-ment. Thus, our first deal was to supply twenty-fiveof Zapsibkom’s branches and subsidiaries with newcomputer equipment. Then came leases for auto-matic teller machines, money-sorting machinesand vehicles. At the same time, the company wasworking on a plan to modernize the Tyumen Ship-building Plant. Of course we didn’t limit ourselves tothese few contracts. We launched an aggressiveadvertising campaign and managed to expand ourportfolio by attracting new companies.

One thing that made it easy for us to expand wasthe relative weakness of our competitors. In 1997there were only four leasing companies in theregion, two of which specialized in agricultural leas-es and had financial support from the regional gov-ernment. A third focused exclusively on leasing itsown products (air conditioners).

What sort of equipment is most in demand inTyumen, and does Lizing-Biznes Tyumen doany business outside of the region?

Almost all of our lessees are located in Tyumen.The farthest we have ventured from home so far isto the neighboring districts of Khanty-Mansiysk andYamalo-Nenetsk. The reason we limit our geo-graphical range is to keep our overhead expensesdown. Expenses really start to add up when youhave to monitor assets in other regions.

As for the types of businesses that operate in Tyu-men, most of them are in the oil and gas industries.Tyumen is also beginning to develop new industries,particularly timber, printing and communications,where it previously relied on other regions, likeSverdlovsk, Omsk and Novosibirsk, for these ser-vices. We have been getting more and more appli-cations from companies in these industries.

At the moment, our lease portfolio includes a widevariety of equipment: bank equipment, officeequipment, cars, trucks, road-building equipment,dental equipment, specialized equipment for televi-sion studios, pharmacy equipment, etc. But the twothings that we lease most frequently are automo-biles and computers.

Who finances your company’s lease agreements?

We have two main sources of finance: first of allour own working capital, which we have managed toaccumulate over the years, and then commercialbank loans.

How many leases have you signed so far?What is the average size of your contracts andthe average duration of your leases?

Lizing-Biznes Tyumen has signed 64 leases todate. We do not restrict the size of our contracts inany way, so their value tends to vary quite a bit -from $1,000 to 8 million rubles. The leases vary inlength from one to seven years. So far this year wehave signed nine new leases. Most of these werefor automobiles (VAZes and UAZes). We also signeda lease for some wood-processing equipment andtwo leases for office equipment.

Obviously some of your equipment suppliersare not local.

That’s right. Our suppliers come from all overRussia: Novosibirsk, Yekaterinburg, Moscow, St.Petersburg and so on. We have even worked withsuppliers from as far away as Belarus and Germany.

Does Lizing-Biznes Tyumen ever workwith lessees that are just starting up theirbusinesses?

Yes, we do sometimes work with lessees that arestarting from scratch. We have signed four leaseswith private entrepreneurs, and we helped onesmall business get off the ground with a series offour equipment leases.

When working with small businesses, we havegenerally tried to make it easier for them by lower-ing our requirements as far as guarantees and col-lateral are concerned. We have found that even inthe face of real adversity, these lessees tend to beiron-willed and usually generate enough revenue tocover their own expenses and meet all of their finan-cial obligations.

Apart from leasing equipment, we have alsogranted some short-term loans to small businessesin order to give them an extra boost. This has gen-erally yielded good results. With only one exception,all of these businesses have thrived. Unfortunately,we did have to terminate one of our agreements.That particular project had the misfortune to beginon the eve of the August Crisis, which none of usforesaw, and to this day that is the only project weever had to cancel. Fortunately, we were able to sellthe equipment at a considerable profit.

What are some of the major risks that yourcompany faces, and how have you managed toavoid them?

The biggest problem is that some of our lesseeshave, at times, become temporarily insolvent for aslong as a month or two. In order to avoid that kind ofrisk, we try to obtain as much information as possi-ble about our potential lessees and their projectsbeforehand and to analyze that data thoroughly.Both our lawyers and our financial experts analyzethe client’s documents, and we always send ourexperts out to the potential site to get a better feelfor the people who will be running the project.

Another important way that we protect ourselvesis by requiring guarantees from our lessees. Everyone of our lessees has to provide us with a letterauthorizing us to deduct funds from his account inthe event that he defaults on his lease payments or

incurs penalties for violating the terms of the leaseagreement. We also require the lessee, or a thirdparty, to offer some highly liquid form of collateral.Finally, the director of the enterprise himself mustsign a guarantee agreement. All of these measureshelp discipline our clients and give them a greaterpersonal interest in the outcome of their projects.

Of course any lending institution takes similarmeasures to protect itself against the risk of default.However, there are certain subtleties in the relation-ship between a leasing company and its clients. Wego to great lengths to make sure that the lease pay-ment schedule is really feasible for the lessee andthat he still has enough cash left over after eachpayment period to cover his own expenses. If hisbusiness hits a snag, we do everything we can tohelp. We might, for example, grant him a paymentdeferral. We also try to use all of our connections(other clients, partners, etc.) to help our lessees.For example, we might persuade one of our otherclients to supply a lessee with raw materials or com-ponents at discounted prices, or to distribute hisproducts through his own retail network.

Do you face any other obstacles? If so, howdo you overcome them?

I would say that we have three main problems.The first is the lack of affordable, long-term capi-

tal. The banks that we work with are doing quite wellwith short-term loans and do not see any particular-ly need to invest in long-term projects.

The second problem is one that every leasing com-pany in Russia has to deal with: the instability of Russ-ian tax laws and leasing regulations. Unfortunately, thetax police and other inspection agencies often fail tokeep up with changes in government policy, which pre-vents us from finding reasonable, workable solutions

May-June 2001 11LEASING IN REGIONS

whenever the law changes in the middle of a deal.The same applies to the highway police, where auto-mobile leases are concerned, as well as the StateRegistration Chamber.

The third problem is the fact that many lesseesfail to understand how leases are supposed towork. Potential lessees often fail to recognize theadvantages of leasing over other means of acquir-ing new equipment. In the hope of educating them,we have published several articles on leasing in thelocal press. Our experts have also come up withsome educational materials that highlight theadvantages of leasing over bank loans. Last year,the Tyumen Regional Committee for Industry andEntrepreneurship helped us organize two confer-ences: «The Principles of Leasing» and «The Legal,Economic and Tax Aspects of Leasing.» We invitedcompany directors, financial managers andaccountants from throughout the region. That ishow we have tried to raise people’s awarenessabout the benefits of leasing.

Does the regional government do anything tosupport the local leasing industry? Has itpassed any regulations to encourage leasing?

In February 2000, the regional government ofTyumen passed Law #158 on the Creation of aLeasing Fund forRegional Agricul-ture. This fund hasbeen used to helpTyumen farmerslease equipment,property and live-stock. It was cre-ated not only tosupport localfarmers, but alsothe Tyumen leasing companies that specialize inagricultural leases (Tyumen Agricultural LeasingCompany and Tyumen Agropromsnab [AgriculturalSuppliers]). The regional government also drafteda Law on Investment in the Tyumen Region, whichwas aimed at improving the local investment cli-mate (for leasing companies as well), but this lawhas not gone into effect.

So this is what we have to work with. There issome hope that the new regional government willlearn from its neighbor, the government of Khanty-Mansiysk, which exempted leasing companies fromlocal profit and property taxes as early as 1998. We

hope that the new government will understand thatthe region’s leasing industry (and hence its overallinvestment climate) depends on well-functioningregulations and government support.

Finally, please tell us a little bit about Lizing-Biznes Tyumen’s plans for the future.

I think the chances are quite good that our com-pany will continue to grow. Our latest advertisingcampaign has brought in a lot of new potentialclients.

We are currently working on 11 new lease agree-ments with local small businesses. The municipalgovernment of Tyumen has shown an interest in

these projects, andwe are hoping that theFederal Fund forSmall Business Devel-opment will also giveus some financial sup-port.

We also hope thatbusiness will boomwhen our lending

bank starts expanding its investment activities.Certain industries in Tyumen, such as the timber,construction and food-processing industries, aregoing to take off in the near future, and all of thosecompanies will be looking to lease new equipment.

Thank you very much for speaking with ustoday. The Leasing Courier would like to wishLizing-Biznes Tyumen success in its leasingprojects!

May-June 2001

When working with small businesses, we have general-

ly tried to make it easier for them by lowering our

requirements as far as guarantees and collateral are

concerned. We have found that even in the face of real

adversity, these lessees tend to be iron-willed and usu-

ally generate enough revenue to cover their own

expenses and meet all of their financial obligations.

12 LEASING IN REGIONS

May-June 2001 13LEASING IN REGIONS

The PetersburgLeasing Associ-ation was

founded in 1999 by aconsortium of sixmajor leasing compa-nies: Baltic Leasing,Baltinvest, Rust, ThePetersburg LeasingCompany, AnkerIndustrial LeasingCompany and RT-Liz-ing, with additionalsupport from theRussian Association ofLeasing Companies.The consortium actu-

ally dates back to 1998, when the St. PetersburgCouncil for Foreign Investment invited these six com-panies to join its special committee for the improve-ment of local leasing laws. By 1999, we had all begunto realize that reforming St. Petersburg’s leasing lawswas going to be a very long and difficult process. Oursmall committee was not really up to the task, so wedecided to form a permanent body that would becapable of representing the interests of the entire leas-ing industry — not only leasing companies, but alsolessees and equipment suppliers. We called our non-profit organization the Petersburg Leasing Associa-tion. Despite the name, the organization is also opento banks, insurance companies, equipment suppliersand other interested parties.

The Association has set itself a wide variety ofgoals. First, it seeks to improve leasing laws at thefederal level. Several members of the Associationwere invited to join the State Duma’s WorkingGroup on Leasing Legislation under the Commit-tee for Economic Policy and Entrepreneurship.The Association contributed a number of impor-tant suggestions for improving the Federal Law onLeasing and the new Chapter on Profit Tax. TheAssociation pushed for consistent and stable reg-ulations and government support for the leasingindustry (in the form of tax incentives and other ini-tiatives). These conditions would enable the Russ-ian leasing industry to fuel the growth of Russianmanufacturing.

The Association also tries to improve leasing lawsat the regional level. The investment laws of St.Petersburg allow the city to offer certain tax bene-fits. With this in mind, we drafted a series of billsaimed at exempting lessees from local property,profit and highway taxes (on the condition that theyreinvest the money they save into production). TheAssociation’s other initiatives have included a driveto create the official title of «Authorized leasing com-pany of St. Petersburg» and an ongoing attempt toobtain government guarantees for leasing projects.All of our bills have been approved by local govern-ment committees, and we hope they will soon besubmitted to a vote by the Legislative Assembly.

The Association also provides consulting andtraining programs for all participants in the localleasing industry. Leasing is a complicated and fairlynovel concept in Russia. One of the reasons that ithas developed so slowly in this country is the factthat people are generally unaware of its benefits.We therefore have to enlighten the very parties thatstand to benefit from leasing. With this purpose inmind, the Association holds regular conferencesand seminars about leasing as a form of invest-ment. Last year we held two leasing seminars in St.Petersburg, one of which was organized by the IFCLeasing Development Group.

Earlier this year, the Association organized a round-table discussion on leasing at the international con-ference «Investment 2001: New Realities and NewPossibilities for Russia’s Northwest Region.» One ofthe Association’s strategic aims was to help localleasing companies prepare to do business with for-eign investors. Of course, foreign investors are unlike-ly to invest very heavily in the Russian leasing industryuntil the country itself earns a reputation as a reliableborrower. In the meantime, the Association’s authori-ty will continue to grow as financial institutions — bothforeign and domestic — turn to it for informationabout reliable partners. In the future, the Associationalso plans to help local leasing companies resolvedisputes with the tax authorities.

One of our most important aims is to recruit newmembers. The Northwest region is currently home toaround 60 registered leasing companies. We would be

PETERSBURG LEASING ASSOCIATION

Dmitry Viktorovich Korchagov, President

Petersburg Leasing Association

Dmitry Viktorovich Korchagov,

President of Petersburg Leasing

Association

14 May-June 2001

The Northwest region of Russia contains eleven distinct political entities, each with its own investmentclimate. Unfortunately, there are no general data about investment in the Northwest. Each of theeleven regions, districts and cities keeps its own statistics, and no one has yet undertaken to syn-

thesize the data into a unified whole. Nevertheless, by comparing the data that is currently available, one can draw a number of interesting

conclusions:• In virtually every region, the total residual value of all fixed assets is currently falling at a rate of about 5-

10% per year. This means that depreciation is outpacing the renewal of fixed assets.• Throughout the Northwest, the level of investment in fixed assets declined steadily from 1991 until late

1998, when it finally began to rebound. In 1999, it grew by 1.8 times in Murmansk and 1.5 times in Kare-lia. As one might have expected, the trend continued in the year 2000.As for the actual sources of investment, let’s consider some data from St. Petersburg as an example.

LEASING AS A FORM OF INVESTMENTIN THE NORTHWEST REGION OF RUSSIA

On a related topic, we present a survey of leasing in the Northwest region of Russia. The following articleis based on a speech delivered by D.V. Korchagov, general director of Baltisky Leasing, at a conference inSt. Petersburg (Investment 2001: New Realities and New Possibilities for the Northwestern Region ofRussia) in March 2001.

Investment in Fixed Assets: Financial Sources

1993 1994 1995 1996 1997 1998 1999Investment in Fixed Assets 100 100 100 100 100 100 100Local Governments 24 17 12 17 7 10 14Own Working Capital 38 53 53 49 50 53 46

- of which retained earnings - - - - - 19 19Federal Government 29 23 13 13 12 4 3Bank Loans - - - - - 11 11Other Lending Institutions - - - - - 9 16Joint Ventures and Foreign Firms 8 6 13 13 22 - -

Note: "-" indicates data not available. Figures in %

delighted if more of these companies joined our group,including some of the banks that have formed leasingsubsidiaries, such as the Industrial Construction Bank,Baltisky Bank and Sberbank of Russia. Our doors arealso open to local insurance companies.

Petersburg Leasing has clearly demonstrated thatthe development of leasing in Russia largelydepends on regional initiatives. We thereforestrongly encourage everyone to concentrate theirefforts locally in order to be heard in Moscow.

LEASING IN REGIONS

As you can see, the main source of funding forinvestment in fixed assets has always been, andcontinues to be, Russian companies’ own workingcapital, which accounts for some 46-53% of totalinvestment in Russian industry. You can also see aclear decline in government funding. At the sametime, external sources of capital have increasedrapidly. One of these sources is leasing.

Leasing has constituted a significant share ofthe region’s total investment:

• Russia as a whole invested around $23 billion(659.3 billion rubles) into fixed assets in 1999.

• According to V. Cherkesov, President Putin’s rep-resentative in the Northwest region, the Northwestattracts around 16% of total investment in Russia.That means that in 1999, some $3.5 billion (100billion rubles) was invested in the region.

• Throughout Russia, leasing accounts for some4.8% of total investment in fixed assets. Thatmeans that the Northwest region poured around

May-June 2001 15LEASING IN REGIONS

4.8 billion rubles ($1.6 billion) into investmentusing leases in 1999.

• The city of St. Petersburg received 29.7 billionrubles’ worth of investment in fixed assets in1999, including approximately 1.5 billion rubles inleases (one third of the Northwest region’s total).These are obviously very rough estimates, but

they give us some idea of leasing’s role in the localeconomy.

Over the last few years, leasing has become moreand more popular as a form of investment through-out Russia. Last December, the number of regis-tered leasing companies in Russia reached 1,162.Most of these (75%) were concentrated west of theUrals, including some 40% in the cities of Moscowand St. Petersburg. However, according to the StateRegistration Chamber, only 25% of all registeredleasing companies are currently active. This meansthat there are no more than 350 active leasing com-panies in Russia today.

What are the general prospects for leasing in theNorthwest region?

Leasing is most common among industries thatconstantly require new equipment:• Computers• Telecommunications• Automobiles• Highway construction• Machine building

There are several factors that could spur thegrowth of leasing in the Northwest region:

1. The strong demand for new equipment.Around 60-70% of the region’s equipment is obso-lete and will have to be replaced if we are to avert anindustrial crisis. The need for new equipment is par-ticularly acute in the following industries:• Mining• Metals• Electric power• Telecommunications• Pulp and paper• Logging and timber• Transportation• Shipbuilding• Fishing• Light manufacturing• Food processing

2. The availability and affordability of invest-ment capital. Let’s consider some of the mainsources of finance and their current drawbacks.

Russian banks. It is no secret that the level ofcapitalization among Russian banks is rather low.There is not enough long-term capital to financelarge-scale leases, and interest rates are high.

The main players in the Northwest region are theNorthwestern branch of Sberbank, the St. PetersburgIndustrial and Construction Bank, and a handful ofMoscow banks (Alfa Bank, Nikoil Financial Group,etc.). Regional banks are still too weak to invest inlarge-scale leases.

The regional government. This has never beena significant source of funding, and these days it isactually shrinking as Moscow continues to central-ize state spending.

Foreign investment. This largely depends ongovernment policy. The region will have to improveits credit rating if it hopes to be taken seriously byforeign investors. However, the region cannot realis-tically succeed at this task until such time as thefederal government begins to improve Russia’scredit rating as a whole.

Russian companies’ own working capital. Thiscan be an ineffective source of funding, since itdrains companies’ resources.

3. Developing the leasing industry itself. Thenumber of professional leasing companies in theNorthwest region currently includes:• Alfa Leasing• Baltic Leasing• Baltinvest• Delta Leasing and the RKM Leasing Center• Dorleasing• Leasing Ugol• The Novgorod Leasing Company• Promleasing (Cherepovets Metals)• Rosagrosnab [Russian Agricultural Suppliers]• RUST

Improving the region’s leasing laws would alsohelp stimulate the local leasing industry. The gov-ernment must take measures to support leasing inthe Northwest region. Such measures couldinclude:• Tax incentives for investing in leases• State funds to finance leasing, especially for small

businesses• State guarantees and collateral funds• Tenders for state leasing contracts.

16 May-June 2001SMALL AND MEDIUM-SIZED BUSINESS

KONTINENT PLAST, ST. PETERSBURGHow Packaging Company Expands Production Using Leasing

Eleonora Veitsman,

Public Relations Specialist

Continued from pg. 1 IFC Leasing Development Group

By 1998, Kontinent Plast had completed therenovations, installed all of the necessaryelectrical wiring and communication cables,

built a new warehouse and purchased a foreign-madeproduction line. The factory was up and running.

Almost immediately, Kontinent Plast’s new pack-aging products were in great demand. Not onlywere they of the highest quality, but also they wereless expensive than their foreign-made equivalents.Orders started coming in from firms not only inNorthwest Russia but also from firms in Moscow,the Moscow region, and other regions throughoutRussia. The company soon realized that they wouldhave to expand to keep up with demand. ThoughKontinent Plast had enough funds at its disposableto purchase new equipment, they could not reallyafford to deprive themselves of so much workingcapital in the long run. Financing the purchase witha bank loan was problematic.

In February 2000, Kontinent Plast turned to theBaltic Leasing Company with a request for threenew Kosmos injection molding packagingmachines (for making buckets, containers, glassesand the like) and a Battenfeld extrusion machine formaking bottles and canisters. The work involved indrafting the leasing contract was completed by thestaff of Baltic Leasing very efficiently; all the formal-ities were taken care of in less than one month. The

companies signed two separate lease agreements,each for terms of three years. The value of bothdealswas over $500,000.

The new equipment enabled Kontinent Plast tosignificantly diversify its production. Nine new typesof packaging were added to its product line, and asa result the company’s turnover increased by 20%.It hired 32 new workers to operate and maintain thenew machines.

Having experienced the benefits of leasing first-hand, Kontinent Plast is now convinced of the effec-tiveness of leasing as a financing instrument andplans to continue to use leasing in the future. Thefirm plans next to lease another Kosmos packagingmachine. After using Kosmos equipment in its pro-duction and being pleased with the results, Konti-nent Plast became the company’s official dealerand distributor in the CIS and the Baltics. Currentlythe firm is pursuing its new role as dealer and dis-tribut with the help of leasing and is negotiating anagreement with Baltic Leasing. If the negotiationsare successful, Kontinent Plast will enter into itsnext leasing agreement in a new role - as an equip-ment supplier.

Pictured: Kosmos packaging machine

Leased equipment has allowed Kontinent Plast to

expand greatly its product offering

May-June 2001 17SMALL AND MEDIUM-SIZED BUSINESS

TELEFONSTROY, NOVOCHEBOKSARSK,REPUBLIC OF CHUVASHIA

Telefonstroy Manufacturing and Constru-ction Company, the first and only cabletelevision operator in the city of

Novocheboksarsk (Chuvashia), specializes inbuilding infrastructure for the telecommunica-tions and electricity industries. To put it more sim-ply, Telefonstroy lays cables.

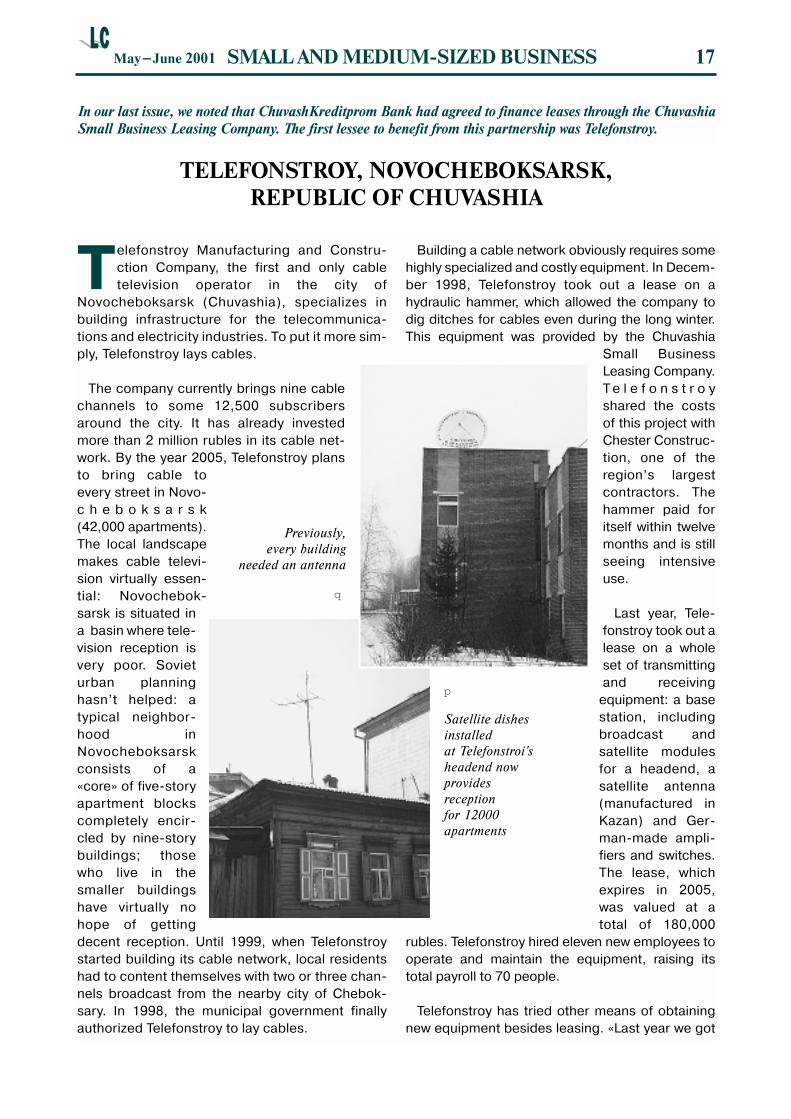

The company currently brings nine cablechannels to some 12,500 subscribersaround the city. It has already investedmore than 2 million rubles in its cable net-work. By the year 2005, Telefonstroy plansto bring cable toevery street in Novo-c h e b o k s a r s k(42,000 apartments).The local landscapemakes cable televi-sion virtually essen-tial: Novochebok-sarsk is situated ina basin where tele-vision reception isvery poor. Sovieturban planninghasn’t helped: atypical neighbor-hood inNovocheboksarskconsists of a«core» of five-storyapartment blockscompletely encir-cled by nine-storybuildings; thosewho live in thesmaller buildingshave virtually nohope of gettingdecent reception. Until 1999, when Telefonstroystarted building its cable network, local residentshad to content themselves with two or three chan-nels broadcast from the nearby city of Chebok-sary. In 1998, the municipal government finallyauthorized Telefonstroy to lay cables.

Building a cable network obviously requires somehighly specialized and costly equipment. In Decem-ber 1998, Telefonstroy took out a lease on ahydraulic hammer, which allowed the company todig ditches for cables even during the long winter.This equipment was provided by the Chuvashia

Small BusinessLeasing Company.T e l e f o n s t r o yshared the costsof this project withChester Construc-tion, one of theregion’s largestcontractors. Thehammer paid foritself within twelvemonths and is stillseeing intensiveuse.

Last year, Tele-fonstroy took out alease on a wholeset of transmittingand receiving

equipment: a basestation, includingbroadcast andsatellite modulesfor a headend, asatellite antenna(manufactured inKazan) and Ger-man-made ampli-fiers and switches.The lease, whichexpires in 2005,was valued at atotal of 180,000

rubles. Telefonstroy hired eleven new employees tooperate and maintain the equipment, raising itstotal payroll to 70 people.

Telefonstroy has tried other means of obtainingnew equipment besides leasing. «Last year we got

In our last issue, we noted that ChuvashKreditprom Bank had agreed to finance leases through the ChuvashiaSmall Business Leasing Company. The first lessee to benefit from this partnership was Telefonstroy.

Previously,

every building

needed an antenna

q

p

Satellite dishes

installed

at Telefonstroi's

headend now

provides

reception

for 12000

apartments

18

a loan for 300,000 rubles from the Small BusinessDevelopment Fund,» explains Nikolai Lisin, Tele-fonstroy’s general director. «But we had to pay80,000 rubles in interest out of our revenue, whichwas only 110,000, so the end gain was pretty small.Apart from the interest payments, we also neededmoney to develop our business, to cover our oper-

ating costs, to paypeople’s salaries,and so on. Wedecided to stickwith leasing. Leas-ing makes moresense to begin within a business likeours, since most ofour projects arefairly long-term.Banks rarely giveloans for more thanone year, whileleases usually lastfor three. And withleasing we canactually get ourhands on theequipment we needwithin a few daysafter signing thecontract.»

A few figuresabout Telefonstroy:between April 1999

and April 2000, the company set up 10 main-lineamplifiers, 52 local amplifiers and more than 7 kilo-meters of main-line cables. This enabled the compa-ny to bring cable service to 4,760 new homes. Sub-scribers now have access to 7 broadcast channels(ORT, RTR, Kultura, NTV, Channel 5, TV-Center andCheboksary Municipal TV) and 2 satellite channels(AST and TV-6). Chuvashia’s Antitrust Ministry hascapped subscription rates, so local subscribers payno more than the national average. It costs them 52rubles to have the service installed, after which theypay a monthly subscription of 12 rubles. Theseprices are within easy reach of the average resident.

Telefonstroy has continued to work with the Chu-vashia Small Business Leasing Company and is cur-rently negotiating a lease for some new diggingequipment. «Until now we always had to use old-fashioned excavators to dig our trenches,» explainsMr. Lisin. «With modern digging equipment, we’ll be

able to cut our expenses in half. It’s simple mathe-matics: our excavators can dig 200 meters of trenchin an eight-hour shift, while the new machine will beable to do 400-500 meters in the same amount oftime - and it even works in winter. We’ll be able toput the old excavators to better use, like laying high-voltage cables and telephone wires.»

The digging machine that Telefonstroy intends tolease is manufactured at the MTZ 82 Plant inMinkhevo (Moscow region). Telefonstroy is current-ly negotiating the terms of the lease with the Chu-vashia Small Business Leasing Company. The twocompanies are expected to sign a three-year leasevalued at 509,000 rubles.

In the future, Telefonstroy also plans to lease anew compressor to replace the one it has beenusing since 1996, as well as some specialized labo-ratory equipment for measuring cables.

By the end of this year, Telefonstroy will extend itscable network to two more neighborhoods, raisingits total number of subscribers to 18,492. Its ulti-mate goal is to reach every home in Novochebok-sarsk by the year 2004. The municipal governmenthas also approved a plan to create the first localtelevision station, to be operated by none other thanTelefonstroy.

PS. As we were writing this article, we wereinformed that Telefonstroy and the Chuvashia SmallBusiness Leasing Company have already signed anew lease agreement.

By Viktoria Struts

May-June 2001

Telefonstroi General Director N.A. Lisin explains the principles of

cable networking.

SMALL AND MEDIUM-SIZED BUSINESS

This compact piece of equipment is a

key piece of the headend station -

receiving and transmitting a high

quality signal

May-June 2001 19OUR PROJECT

We are pleased tointroduce a new staffmember:

This May the IFC Leas-ing Development Groupwelcomed a new DeputyProject Manager, GregAlton. Before joining the

Group, Greg worked for several years as SecondSecretary and Vice-Consul at the CanadianEmbassy in Moscow. He also worked as an analystat Troika Dialog Investment Bank. Greg holds aMaster’s degree in public policy and economicsfrom Princeton University and a Bachelor’s fromMcGill University in Montreal.

RUSSIA’S GOLD MINERS TAKE AN INTEREST IN LEASING

Aleksei Trepykhalin, Training Manager

IFC Leasing Development Group

On April 23-24, the city of Irkutsk hosted aninternational seminar on «IntegratedApproaches to Financing Gold Mining Com-

panies and the Advantages of Financial Leasing:Irkutsk 2001», organized by Western Pinnacle Miningof Canada and the IFC Leasing Development Group.

The Leasing Development Group’s interest in thesubject is not by chance. The Group is financed bythe Canadian International Development Agency(CIDA), and Canada occupies a leading position inmining projects throughout the world. While LatinAmerica draws some 27% of Canada’s total foreigninvestments, Russia attracts only 6%. The RussianMinistry of Natural Resources and its Canadiancounterpart have been working together toincrease Canadian investment in the Russian min-ing industry since 1997, when the two countriesformed a special Working Group on the MiningIndustry within the Canada-Russia Intergovernmen-tal Economic Commission. Last year, Russia andCanada signed a memorandum on the investmentclimate in the Russian mining industry, which identi-fied the steps that must be taken if Russia is toattract more investment.

For many years, Russia obtained all of its goldfrom placer deposits, since this was by far themost inexpensive method of extracting the pre-cious metal. Other countries, meanwhile, weredeveloping effective methods of extracting goldfrom large ore deposits that contained relativelysmall amounts of gold. Russia is now movingtowards this approach, and if the Russian gov-ernment succeeds in improving the investmentclimate, Russia’s output of gold should increaseseveralfold.

This means that Russia’s eastern regions will gainin significance as a source of natural resources.Russia’s railroad infrastructure will make it possibleto develop these new regions actively, to attractboth foreign and domestic investors to existing pro-jects and to use modern forms of finance in thegold-mining industry.

The Irkutsk region is a perfect example of a regionwith a highly developed infrastructure. In the 1990s,Irkutsk solidified its gold-mining industry, becomingthe fourth largest producer in Russia. The region’smines are currently at different stage of develop-ment. Gold placers are being mined fairly intensive-ly, but ore deposits have hardly been touched. Forexample, 80% of placer deposits have beenlicensed and are either being developed or can bedeveloped, while only 10% of ore deposits havebeen licensed for development.

Last year, Irkutsk produced 16 tons of gold -more than its previous record of 15,758 kg set in1915, and 42% more than it produced in 1999.The local mining industry employed more than10,000 people.

20 May-June 2001OUR PROJECT

Nevertheless, there are some serious obstacles tothe industry’s growth. The biggest problem for mostlocal enterprises is the shortage of investment capital.Financial leasing could help them overcome this diffi-culty. During the «Irkutsk 2001» seminar, the IFC Leas-ing Development Group gave a presentation aboutthe advantages of leasing as a form of investment.

The presentation was structured like all of theIFC’s seminars on «Leasing as a Means of AcquiringFixed Assets,» but tailored to address the specificneeds of the mining industry. Topics included a vari-ety of legal, economic and financial issues relatedto leasing, as well as tax policies and accountingprocedures for leasing transactions. The partici-pants also learned about strategies for buildingeffective partnerships with their leasing companies.The miners listened to these discussions with par-ticular attention, since very few of them had hadpractical experience with leasing before.

The audience included representatives from thegovernments of Irkutsk, Buryatiya and Krasnoyarsk;Russian and foreign investors; representatives fromthe gold miners’ associations and processors;domestic and foreign equipment vendors and Russ-ian financial institutions. Participants were invited toask questions and take an active part in the seminar.Both local and national media were on hand to coverthe event, and a separate press conference washeld after the seminar.

The seminar clearly demonstrated that Russianand Canadian businesses are interested in workingtogether to attract more forms of investment,including leases, to the Russian natural resourcesindustry. It also proved that Russia and Canada cancooperate by exchanging technical know-how in thefield of geological prospecting and by sharing infor-mation about possible joint activity in the raw mate-rials market.

KRASNODAR HOSTS SEMINAR FOR LESSEES

On May 24, «Leasing as a Means of Acquir-ing Fixed Assets,» a seminar targetedespecially for leasing recipients, was

conducted in Krasnodar with support fromKubaninvest, a state-owned leasing company,and the Krasnodar regional government . Thiswas not the first IFC event in the region. In 1999the Leasing Development Group held a seminaron «The Principles of Leasing» in Krasnodar,which played an important role in stimulatingactivity in the local leasing sector.

The Deputy Head of the Regional Adminis-tration for Finance, Budgeting, Economicsand Strategic Planning of the KrasnodarRegional Administration, A.A. Remezkov,opened the seminar by emphasizing theimportance of developing new financial ser-vices — particularly leasing — in theKrasnodar region. He also announced that theregional government has allocated 100 millionrubles this year from its budget for the devel-opment of leasing .

«Leasing as a Means of Acquiring FixedAssets,» a seminar designed for both potentiallessees and firms that already have experiencewith leasing, drew representatives from 170

local firms, including small- and medium-sizedbusinesses, insurance companies and finan-cial institutions. It is no surprise that local firmsshowed such a strong interest in leasing. Mostof producers in Krasnodar is in urgent need ofnew equipment but many are unable to investlarge sums of working capital or to committhemselves to expensive bank loans. Thedevelopment of leasing in the region will makeit possible for these companies to obtain newequipment, which in turn will raise productivityand create new jobs. As a result, the regionalgovernment will also receive more tax revenue.

Small- and medium-sized businesses play acrucial role in the region’s economic develop-ment. According to the Krasnodar city govern-ment, during the first quarter of 2001 therewere 27 individual entrepreneurs per 1000residents (a total of 20,600 people). Small-scale producers still account for approximate-ly 10% of the region’s manufacturing sector.This figure reflects a great potential for growthin small-scale production.

There are currently nine licensed leasingcompanies in the Krasnodar region, but onlysix of these are active on the market: Inko-

AND, Kubaninvest, The Municipal InvestmentCompany, Delta-Leasing, Krasnodaragro-promnab (Krasnodar Agricultural Suppliers)and Yug Bank. During his presentation in theseminar, M.V. Kaklyu-gin, Deputy Directorof The MunicipalInvestment Company,emphasized that thereis strong demand forleasing services in theregion. Nevertheless,local leasing compa-nies face some formi-dable obstacles, suchas an inadequate leg-islative and regulatoryframework, limitedaccess to financing,and a lack of understanding on the part oflocal entrepreneurs of the advantages of leas-ing. Despite these obstacles, The MunicipalInvestment Company continues to expand itsleasing services on the local market. Its cur-rent portfolio includes food-processing, man-ufacturing and dry-cleaning equipment, aswell as motor vehicles.

One of the main goals behind the IFC’s sem-inar was to raise the level of awareness aboutleasing among local entrepreneurs. Each topiccovered in the seminar was reinforced withconcrete examples and practical exercises.Participants were encouraged to ask ques-tions and to seek individual consultations withthe IFC’s team of experts. Potential lesseeswere also given the opportunity to meet withrepresentatives from those local leasing com-panies present (Inko-AND, Kubaninvest, TheMunicipal Investment Company and DeltaLeasing), learn about the requirements of spe-cific leasing contracts and choose their mostsuitable partners.

Local media devoted considerable coverageto the event. Representatives of the regionaladministration, local leasing companies andthe IFC all gave interviews to the local press.

* * *

On May 23 the Leasing Development Groupheld a seminar on «Leasing as a Means ofAcquiring Fixed Assets» for the region’s

women entrepreneurs with organizational sup-port from the Krasnodar Business Develop-ment Agency (KADR). KADR seeks to facilitatethe development of small- and medium-sized

businesses by orga-nizing seminars onRussian legislation,accounting regula-tions and tax policies.It also supports thecreation of a healthycompetitive environ-ment for businesses inthe region and acts asa mediator betweenthe Krasnodar’s busi-ness community andcity officials.

The seminar began with a speech by KADR’sdirector, Olga Andreyeva. Ms. Andreyevanoted that approximately half of Krasnodar’s10,000 small businesses are run by women.«When we started sending out the invitationsfor today’s seminar, some people asked whywe were discriminating against men. This iswhat I told them - women entrepreneurs distin-guish themselves by their extraordinarydynamism. They also have a better grasp ofmanagement techniques and are much betterat networking. Nevertheless, they rarely havethe opportunity to gather as we have gatheredhere today. It is meetings like today’s that canhelp businesswomen expand their knowledgeand improve their self-confidence.»

Seminar participants included directors ofsmall- and medium-sized businesses, includ-ing a bakery, a furniture manufacturer, a furfactory, a fashion design company, a craftsdistributor, and several auditing and consultingfirms.

The seminar drew the attention of the city’swomen entrepreneurs to leasing - an impor-tant source of financing that has yet to bewidely understood and taken advantage of bythe local business community. Leasing Devel-opment Group specialists provided compre-hensive answers to a large number of ques-tions from the audience. Two local leasingcompanies, Kubaninvest and Delta-Leasing,were also present and gave individual consul-tations to seminar participants.

May-June 2001 21OUR PROJECT

22 May-June 2001LEGISLATIVE NEWS

CURRENCY REGULATION

On July 6, 2001, Federal Law #72-FZ(05/31/2001) on Amendments and Addi-tions to the Federal Law on Currency Regu-

lation will go into effect. Several of the law’s provi-sions will have a positive effect on both foreign tradeas a whole and cross-border leases in particular:

1. Payment for the following export products willno longer require the approval of the Russian Cen-tral Bank: machinery, equipment, electronics (sec-tion XVI of the Foreign Trade Inventory of Goods(TNVED)), ground vehicles, flying vehicles andwaterborne vehicles (section XVII of the TNVED),provided that hard-currency revenue is receivedwithin three years of the export date.

2. The list of noncommercial agreements exempt-ed from control by the Central Bank has beenexpanded to include the following:• Payments for notary and legal services, as well as

court, arbitration or administrative fees. • Monetary payments, such as fines, imposed by

the courts or other law-enforcement agencies3. Currency regulators must decide within two

months whether or not to authorize a given transac-tion. They must also present valid reasons for allrefusals.

4. The Law’s summary procedures for imposingfines and other sanctions have been replaced bySection 4 of the Code on Administrative Violations.

AGRICULTURE

O n May 22, 2001, the federal govern-ment passed Resolution #404 on Mea-sures to Support Agricultural Leasing,

which authorizes the transfer of federal funds(in accordance with the Federal Law on the

Russian State Budget for the Year 2001) tofinance leases for agricultural machinery andpedigree livestock. Some federal funds will alsobe used to increase the charter capital ofRosagro Leasing Company.

CUSTOMS REGULATIONS

The State Customs Committee has suspended(until further notice) all interest charges ondeferred customs duties for goods subject to the

temporary import regime (Telegram #TF-9644 of April23, 2001).1 Considering that the time limit for tempo-rary imports is two years (after which the imported

goods must either be transported out of Russia orreclassified as regular imports), this is certainly a posi-tive development for the Russian leasing industry, as iteffectively lowers import costs for leased assets.

Furthermore, enterprises will now be able tochange the import status of their goods by submit-ting an application to the State Customs Commit-tee, provided that they do not have any outstandingdebts on customs duties.

ANTITRUST LEGISLATION