world bank document file1 hectare (ha = 10,000 square meters (m2) = 2.47 acres (a) 1 kilogram (kg) =...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 9558-BO1Vo I) 1 i. 1'4tv ,§ ,',1; ) I

STAFF APPRATSAL REPORT

BOLIVIA

SECOND PUBLIC FINANCIAL MANAGEMENT OPERATION

JUNE 4, 1991

Public Sector Management DivisionTechnical DepartmentLatin America and Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EOUIVALENTS

Currency Unit - Boliviano (Bs)

US$1 $b 3.45(February 1991)

WEIGHTS AND MEASURES

1 hectare (ha = 10,000 square meters (m2) = 2.47 acres (a)

1 kilogram (kg) = 2.205 pounds (lbs)

1 metric ton (m ton) = 1,000 kg

ABBREVIATIONS

BAB - Banco Agricola de Bolivia

BCB - Banco Central de Bolivia

BANEST - Banco del Estado

BAMIN - Banco Minero de BoliviaCGR - Contraloria General de la RepGblica

COMIBOL - Corporaci6n Minera de Bolivia

CONSAFCO - Consejo del Sistema de Administracion Financiera y Control

EMSO - Economic Management Strengthening Operation (1977-BO)

ENDE - Empresa Nacional de Electricidad

ENFE - Empresa Nacional de FerrocarrilesENTEL - Empresa Nacional de Telecomunicaciones

ENTA - Empresa Nacional de Transporte Automotor

FDR - Fondo de Desarrollo Regional

FONEM - Fondo Nacional de Exploracion Mineral

GAO - General Accounting OfficeGOB - Government of Bolivia

IMF - International Monetary Fund

INE - Instituto Nacional de Estadistica

IDB - Inter-American Development Bank

LAB - Lloyd Aereo Boliviano

MACA - Ministerio de Asuntos Campesinos y Agricultura

MF - Ministerio de FinanzasMPC - Ministerio de Planeaci6n y Coordinaci6n

PE - Public EnterprisesPFMO - Public Financial Management Operation (Cr.1809-BO)

RDC - Regional Development Corporation

SAFCO - Sistema de Administracion Financiera y Control

SAFCOLaw - Law on Financial Administration and Control Systems

SAC - Proposed Structural Adjustment Credit

TGN - Tesoreria General de la Naci6n

UNDP - United Nations Development Program

USAID - United States Agency for International Development

YPFB - Yacimientos Petroliferos Fiscales Bolivianos

FOR OFFICIAL USE ONLY

STAFF APPRAISAL REPORTBOLIVIA

PUBLIC FINANCIAL MANAGEMENT OPERATION II

TABLE OF CONTENTS

Page No.

PROJECT SUMMARY ............................................ i-iii

I . THE PUBLIC SECTOR ....................... 1

A. Economic Context . ....................................... 1B. Structure of the Public Sec'tor . . . 3C. Reform Measures . ....................................... 5D. Remaining Constraints . . .8............. E. Donor Assistance and Coordination . . . 11F. Rationale for IDA Involvement . . . 12

cI. THE PROJECT ................................................ 14

A. Project Objectives ...................... 14B. Project Description ......................... , 14C. Project Costs ........................ 26D. Financing Plan ........................ 27E. Procurement ........................ 28F. Project Implementation .................... 29

III. PROJECT JUSTIFICATION ........................ 31

A. Project Benefits ........................ 31B. Project Risks ........................ 32

IV. AGREEMENTS TO BE REACHED . . .................... 33

This report is based on the findings of an appraisal mission consisting of AlainTobelem (LATPS) Task Manager, Eduardo Talero (ITFUS), Luisa Ardila (LA3C1), SaraHoffman (LEGLA), and John Davison (USAID), which visited Bolivia in February1991. Jim Wesberry from USAID is the author of the Government Auditing ComponentAnnex. Peer Reviewers are Donald Winkler (LATPS) and James Hicks (LATIE). Theresponsible managers are: Shahid Chaudhry, Division Chief (LATPS); Marie Garcia-Zamor, Projects Advisor (LA3DR) and Ping-Cheung Loh, Director (LA3DR).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ANNEXES

1. Project Implementation Schedule, Inputs and Costs

per Component, per Year

2. Project Detailed Inputs and Costs

3. Summary Account by Project Component

4. Summary Disbursement Schedule

5. Consultants Requirements

6. Ministry of Finance Organization Chart

7. Interinstitutional Relationships Chart

8. Performance Indicators

9. Integrated Information System Program

10. Administration and Control Systems Chart

11. Training Component and Costs

12. Government Auditing Component

13. Accounting Component

14. The SAFCO Law

15. The Elimination of Subtreasuries

16. Lessons Learned PFMO I: Objectives, Performance, and Shortcomings

MAP: IBRD No.16591

FISCAL YEARJanuary 1 - December 31

SECOND PUBLIC FINANCIAL MUNMGEINT OPERATION

Credit and Proiect SummarX

80Kr2row rRepublic of Bolivia

BUenL^gfcart Ministry of FinanceComptroller General's Office

Amountt SDR 8.5 million (US$11.3 million equivalent)

Terms: Standard IDA terms

ProiectObiectives andD2aarit.Lon: Building on progress made under the First Public Financial

Management Operation, the broad objectives of a second operationin Public Financial Management are to: (a) institutionalizebudgeting, accounting, cash management, and auditing proceduresat various levels of government; (b) enhance the institutionalcapacity both at the central and regional government levels toimplement the new procedures; (c) provide GOB with ex postcontrol functions vital to the enforcement of accountability forresults in the public sector; and (d) develop skilled manpowerto sustain the new procedures. The project would consist of: (a)financial management and control component to create and/ormodernize budgeting, accounting, cash management and governmentauditing norms and procedures at the central administratioi leveland disseminate them at other public sector levels; (b) thedevelopment of standards and regulations, to review and/or draftregulations called for by the SAFCO Law in operations-programming, personnel management, procurement and administrationof goods and services, and the rationalization of the non-financial public sector; and (c) training of existing and futurefinancial management specialists and their managers.

Benefitat The main benefit of the project is that it will assist theGovernment to institutionalize the public financial managementsystem throughout the public sector to: (a) improve the budgetformulation process; (b) establish coherent uniform publicaccounting and control systems; (c) provide instruments tointegrate the overall financial status of the public sector; (d)enhance the capacity to hold public servants accountable fortheir decisions and actions through ex-post audit controls; and(e) develop a cadre of skilled financial and audit experts tooperate the system. Overall, the proposed pro,ect would beconsistent with IDA' a strategy to increase GOB' s capacity to

-iL-

make use of, and account for the large volume of donorcommitments of external resources, thus contributing to thelonger-term instLtutional development effort.

Proiect Riokes Three major project riske ares (a) high turn over of staff; (b)ad hoc changes in the financial management procedures; and (c)lack of consistant applicatlon of information generated by theSAFCO system to the Gover.ment's decision-making process. Thestaff turn over, caused mainly by low salaries and high privatesector demand for skillod manpower (e.g., accountants, auditors),iœ being addressed through the establishment of the Public SectorManagement Scheme, where civil service conditions of pay andemployw.,nt are being adjusted to compete with the prlvate sector.In regard to the ad hor changes in procedures, it was agreed withthe Government during negotiations that all institutional andprocedural changes regarding the SAFCO system would be made afterconsultation with IDA. While the largely political riskregarding the Government's possible disregard of SAFCO-generatedinformation in its decliion-making process cannot be entirelymiLtgated, specific actions would be taken to reduce thispossibility. It was agreed at negotiations that: (a) annualreports would be submitted to Congress on the progress ofimplementing the SAFCO Law, thus ensuring that Government policy-makers would be aware of the available information; and (b)satisfactory review of project implementation and following-yearwork program o. an annual basis would be a condition of continuedproject 'inancing by IDA.

-iii-

BOLIVIX

PUBLIC FINANCIAL MANAGEMENT OPERATION II

Estimated Costa and Financinia Plan

Estimated Costs: a/

Local Foreign Total---- US$ million----

Financial Management 3.8 5.4 9.2Standards and Regulations 0.2 0.8 1.0Training 2.0 1.4 3.4Line rositions 3.0 -- 3.0Project Management 0.3 0.7 1.0Management Fee (4% of IDA) -- 0.4 0.4PPF Refinancing 1.5 1.5Base Costs 9.3 10.2 19.5

Physical Contingencies 0.3 0.3 0.6Price Contingencies 1.4 0.8 2.2

Total Project Costs 11.0 11.3 22.3

Financing Plan:Local Foreign Total----US$ million----

Government 11.0 ---- 11.0 b/IDA _ 11.3 11.3Total 11.0 11.3 22.3

a/ The project is exempted from taxes and dutiesb/ Counterpart funds generated from USAID economic support funds.

Note: Due to rounding totals may not always add.

SECOND PUBLIC FINANCIAL MANAGEMENT OPERATION

I. THE PUBLIC SECTOR

A. Economic Context

1.1 Background. Bolivia faces a particularly difficult set of developmentchallenges. Its difficult terrain and landlocked position result in hightransport costs and higher costs for its goods, both internally and externally.Endemic political instability has made Bolivia virtually incapable of sustainingdevelopment policies and strategies for long. Annual population growth rates of3.8% have been too high and economic growth too low for eustained improvementsin living standards. As a result, Bolivia is one of the poorest countries inLatin America; its 6.3 million inhabitants are poorly educated (functionallyilliteracy at 50%); its health indicators are among the worst on the continent(infant mortality at 117 per 1000); a large proportion of its population facespoverty (80% of the population earns less than 70% of the income required tocover a basic needs basket); and it has extremely poor infrastructure and socialservices (e.g., only 30% of the urban population is connected to a seweragesystem and only 15% has latrines). About one-half of the economically activepopulation is employed in agriculture, particularly in the highlands of thealtiplano where subsistence farming predominates. The investment climate, whileimproving, remains highly uncertain particularly due to the continued, dominancece the state in the mineral, hydrocarbon, and energy sectors. The economycontinues to rely heavily on a few export commodities in hydrocarbon and miningsectors for growth, making it vulnerable to external market fluctuations.

1.2 Bolivia, however, has important a.sets and advantages that offer hopefor its future growth and development. It has abundant supplies of hydrocarbons,primarily gas; minerals such as tin, silver, gold, and tungsten; and extensiveforests and fertile land for agriculture and livestock production in the easternlowlands. These resources have not been fully explored or exploited. Bolivianow has direct access to the sea via the Paraguay River, opening the possibilityof reducing transporz costs for its import and export goods. While humanresources are limited in terms of formal education, a small but well educatedcadre of managers, professionals, and technocrats in the public and privatesectors are well able to provide responsible and skilled leadership. Theefficiency cf Bolivia's labor force and peasant farmers is constrained bytechnological and other factors, which could be overcome by investment and goodmanagement.

1.3 Structural Reform Program. Following several years of decliningoutput, culminating in hyperinflation of over 24,000% in annual terms, theGovernment of Bolivia (GOB) in late 1985 launched its New Economic Policy (NEP).This program stopped hyperinflation and introduced a long-term adjustment programto reduce the role of the state and rebuild a free market economy. The exchangerate was freed and set through an auction system, which resulted in an immediatedevaluation of the official rate by 93%; strict budgetary controls wereintroduced to keep expenditures to the levels of revenues; most price controlswere eliminated and specific prices and tariffs increased to bring them close tointernational levels (for gasoline, electricity, and transport). Far-reachingreform of the tax system reduced the basic tax categories from 400 to nine; trade

-2-

restrictions were drastically eased, including elimination of most quantitativetrade restrictions and reduction of tariff rates; and steps were taken toreorganize some pC lic enterprises and abolish or reduce others (COMIBOL - statemining company - was reduced in svze by the termination of 23,000 workers). ThefinanciRl system was liberalized, removing regulatory constraints on financialtransactions and freeing the determination of interest rates. An important startwas made tr, improve public sector administration by est&bliebing the FinancialAdmtnistration and Control System (SAFCO) for monitoring public expsnditures andbetter data systems for planning and monitoring public investment. In early1987, GOB launched an ambitious program to alleviate the impact of the economiccrisis on the poorest groups through the Emergency Social Fund, which supportssmall projects to generate productive employment and social assistance efforts(e.g., maternal health care and school feeding). GOB sustained the adjustmentprogram in the face of the collapse of the international tin price in 198M-1986and difficulties caused by delays in payment by Argentina for Bolivian gasshipments. The new policy stance succeeded quickly in restoring macroeconomicstability. Immediately following introduction of the NEP, inflation felldramatically and has generally remained between 10% and 20%. However, resumptionof economic growth has been slow. GDP grew for zhe first time in six years in1987. albeit at only 2.1% and by an average of 2.6% in :98P-89.

1.4 The Paz Zamora Government, inaugurated in 1989, has adhered to theprevious Government's commitment to economic stability and a market-orientedstructure of incentives; it has also made progress in crucial structural reformsnecessary for growth. For example, the present Government has removedrestrictions on the interest rate charged to final borrowers for developmentcredits and has retired some of its commercial bank debt as well as a portion ofits debt to Brazil. In addition, Bolivia received a highly concessional debtrescheduling agreement from the Paris Club in October 1990. As a result of theseefforts, the Bolivian economy continues on the path of recovery, with annualinflation of 18% in 1990, and the fiscal deficit falling from 5% of GDP in 1989to slightly over 3% in 1990.

1.5 To summarize, GOB has maintained macroeconomic stability thriugh tightcontrol of expenditures, tax reform, realistic public sector goods and servicesprices and a market determination of the exchange rate. At the same time, theadjustment program has achieved a comprehensive liberalization of markets,including rules governing trade, wages employment, interest rates, and capitalflow. Although these changes have brought about economic stability and providea solid framework from which growth is possible, further effort is required inthe areas ofs (i) creating a more attractive environment for private investment;(ii) continued reduction of GOB involvement in the productive sectors; (iii)continued reorientation of public sector involvement towards basic infrastructureand social services; and (iv) increased effort in alleviating poverty.

1.6 In the medium-term (1990-92), GOB's strategy is targeted to achievea 4% GDP growth rate per year, reduce inflation to levels in industrializedcountries, decrease the overall deficit of the nonfinancial public sector toaround 3% of GDP, increaec public savings to 4% of GDP (from 1.1% in 1989), andmaintain a stable monetary and exchange rate policy to foster irternationalcompetitiveness. To resume an acceptable rate of economic growth, GOB fullyappreciates; the additional reforms that need to be undertaken. First, as a

-3-

prerequisite to growth, macroeconomic stability must be maintained through aflexible exchange rate policy, continued reduction in the fiscal deficit andprudent external debt management. Second, to resume growth, further structuralreforms are required to increase investments in the productive sectors by fine-tuning the incentive system for the private Bector, and reduction of the role ofthe utate in the productive sectors through privatization. Third, to improve theefficiency of GOB and to reorient the role of the state, furtier improvement isrequired in public sector administration at a global level, and in sectoralpolicy administration at the micro level. Fourth, to create the human capitalbase for sustained long-term growth, attention muse be pdid to povertyalleviation. Within this context, strong public sector financial andadministrative management continue to be at the heart of GOB's commitment tosustain its macroeconomic policy objectives.

1.7 This is especially the case given GOB's program of further structuralreforms to increase investments in the productive sectors by fine-tuning theincentive system for the private sector, and reducing the role of the state inthe productive sectors through privatization. Public enterprises currentlycontribute 72% of total bud'-eted current resources (US$1,481 million in 1991, ofwhich 39% is hydrocarbons) and 49% to total public expenditures (US$817 millionout of a total of US$1,663 million current expenditures in 1991). GOB's intentionis to: shift the relative importance of key export sectors away from thedominance of hydrocarbons and mining (hydrocarbons constitutes 31% of foreignexchange earnings and 44% of Government revenues); to improve the performance ofthe remaining public sector enterprises through performance contracts; and toimprove basic infrastructure services to complement the productive investmentsof the private sector. In this respect, improving the efficiency of the state andreorienting its role will require significant strengthening in public sectoradministration at the global level, in sectoral policy administration at themicro level, and in public sector involvement to create the human capital forsustained long-term growth.

B. Structure of the Public Sector

1.8 Organization. The Government is subdivided into centraladministration, regional governments, and local governments. Centraladministration consists of the central government, universities, and the socialsecurity system. It includes the executive, legislative, and judicial branchesof the central government. The executive branch comprises the presidency, thevice-presidency, and the ministries. All policies emanate from the Office of thePresident and the Ministerial Councils. There are 18 key ministries, with thecentral administration comprising 26 institutions, which institutions represent23% of total budget expenditures (US$613 million of US$2,697 million in 1991).Some ministries oversee decentralized agencies (13 total), which are stillconsidered part of the central government. Of these, the only significant agencyis the National Road Service (SNC). The central administration and centralgovernment account for about 80% and 60%, respectively, of the expenditures ofthe General Government.

1.9 Local governments are municipalities in urban areas and similar localgoverna.nt entities in rural areas (referred to as "municipios"). Regional

-4-

governments include regional development corporations (RDCs) and prefectures.A prefecture is the regional arm of the executive branch of government and playsa rather limited, almost purely ceremonial role. Recently, there has been muchdiscussion of the role of regional government entities, since some of the RDCshave come to exert disproportionate influsnce over regional development relativeto their role as origina,ly envisaged in the 1974 Law of Regional DevelopmentCorporations.

1.10 The state enterprises are numerous. By far the most important are thestato petroleum company (YPFB) And the state mining company (COMIBOL). There are13 other state enterprises. In addition, the Armed Forces control 11enterprises, and there are 8 mixed enterprises (joint ventures with the privatesector among which is the national airline (LAB). As part of the Government'seconomic program, many small state enterprises that previously belonged to aNational Development Corporation (CBF) were trarsferred to RDCs. xhus, the RDCsare both Government entities and owners of public enterprises (50 in total: todate, no reliable data exist for these enterprises). Finally, the sixmunicipalities of the regional capitals oversee 24 enterprises, mainly in watersupply and electricity distribution.

1.11 Decentralized Public Institutions. This category includes both whollyowned and mixed enterprises. They fall under the jurisdiction of sectoralministries; however, they have been set up as independent entities with legal andadministrative autonomy. The number of these entities grew rapidly between 1977and 1936, public institutions from 89 to 103 and public enterprises from 48 to70. The total number making budget submissions to the central government is now135: 75 public institutions and 60 public enterprises. There are also 157nonfinancial public enterprises, many of which are quite small or are notoperational (even though legally established).

1.12. The major public institutions include the Central Bank of Bolivia, theBolivian Social Security Institute (IBBS) (under which 25 independent socialsecurity funds operate), the National Institute of Statistics (INE), theEmergency Social Fund (ESF), the Social Investment Fund (SIF), the Bolivianinstitute for Agricultural Research (IU3TA), and the National Roads Service (SNC).Mixed and wholly owned public enterprises are expected to provide productivegoods and services at a profit. The major wholly owned public enterprises arethe railways (ENFE), telecommunications (ENTEL), and mineral exploration (ENAF).The Government controls 80% of the Hydrocarbon sector (YPFB), 70% of airtransport, 70% of electrical energy (ENDE), and 70% of the mining industry(COMIBOL). It also owns three banks that together constitute 13% of total bankassets totalling US$1,479 million and have caused a serious drain on theTreasury. The Treasu 's subrogation of Banco Agricola Boliviano debt in 1989equalled US$51 million and for Banco del Estado US$50 million.

1.13 Currently, all of Bolivia's nine regions (La Paz, Cochabamba, SantaCruz, Chuquisaca, Potosi, Oruro, Tarija, Beni and Pando) operate withregional/departmental, and local administrations. Much of the political andadministrative responsibilities are located in the Regional DevelopmentCorporations (RDCs) in each region. The RDCs operate enterprises in the areasof agribusiness, cement, textile and glass, with mixed results. Total

-5-

expenlitures attributable to the departmental governments accounted for only 6%of the total consolidated budget in 1990. The Government is beginning a majorprivatization effort that would inciude the liquldation or sale of tneoeenterprises along with the above mentioned enterprises.

1.14 Inatitutional Canacity at the Municip Levagel. Although substantialcapacity differences exist among municipalities, they all share commoninstitutional shortcoimings, includings (a) poor admintstrative structures, withconsiderable overlap of functions necessary for iAnplementing routineresponsibilities called for in the Organic Law of Municipalities; (b)inadequate tax administration procedures and poor information systems (or nosystem at all) for revenue control; (c) outdated or no municipal property recordsthat could serve as the basis for determining and verifying payment of propertytaxes, which io potentially the main source of local revenues: (d) inadequate orno planning system, in part due to the short tenure of municipal officials (twoyears); (e) low coverage and administration of servicee for which they areresponsible; (f) general deficiencies in financial and administrative systemo;and (g) deficiencies or no personnel management system.

C. Reform Yeasures

1.15 Backaround. Bolivia's economic crisis of mid-198S, was fueled by thevirtual nonexistence of a public financial management system, which permitted anexplosive growth of the fiscal deficit and spurious financing of expenditures.The multiplicity of antiquated and conflicting legal provisions governing publicfinancial management resulted in an arbitrary budgetary process; a completevacuum of accounting systems in the absence of reliable financial data on theexpenditures and performance of public institutions; cash and debt managementbased solely on the availability of cash; and the audit control function with inexternal pre-controls in which auditors interfered with the entity's managerialprocess. In parallel, with the adjustment process initiated in late 1985, GOBbegan a reform process of public financial management to establish the financialinformation, administration, and control systems critical to efficient managementand controlled use of public resources.

1.16 Despite the consolidation of public functions in La Paz, theGovernment nas declined to exercise control over the division of responsibilitiesamong its myriad constituent entities. With no strict administrative policyframework, many government agencies havre freely undertaken activities atdepartmental and local levels without conforming their efforts to nationalobjectives or coordinating within and aniong related sectors. High operatingcosts and inefficient outputs have been frequent outcomes. Also, some regionalagencies have become quite strong and influential, able to negotiate their owninvestment programs (e.g.. Santa Cruz), while others lack basic administrativecapacity and cannot present viable investment projects (e.g., Pando and Beni).

1.17 The proposed decentralization process considered by the currentadministration includes administrative, financial, and institutional aspects.A proposed law to reorganize the departmental governments has already been sentto Congress, but its scope is limited to administrative structures, with no cleardivision of responsibilities or new revenue-sharing schemes. Although muchremains to be done to implement this reform program, the dissemination of the

-6-

SAFCO Law throughout the public administration at all levels should do much tomove the process forwn.d.

1.18 The SAFCO Law. The SAFCO Law, passed by the Bolivian NationalCongress on July 9, 1990, sets the normative framework for country-wide publicfinancial management. One of the major objectives of the first Public FinancialManagement Operation (PFMO-Cr. 1809-80) was to replace the multiplicity ofantiquated and conflicting legal provisions that governed public financialmanagement with a single comprehensive statute. In the area of budgetina, PFMOI assisted in the design of a budget process based on the modern participatoryapproach. Within the Ministry of Finance, a General Accounting Offica has beenestablished, which will be responsible for promulgation of accounting standardsthroughout the public sector. A short-term Emergency Program (introduced withPFMO asqistance) now provides aggregate statistics for the nonfinancial publicsector. This information has proved crucial for public expenditure planning andcontrol, and helped Bolivia to negotiate an Enhanced Structural AdjustmentFacility with the IMF. An integrated accounting system has been created formedijm- and long-term use (the text of the translated SAFCO Law is in Annex 14).

1.19 In the area of cash management, PFMO facilitated the transformationof the Treasury from a mere check-writer to a full-fledged manager of budgetexecution. Resorting to ad hoc disbursements to influential or persistentcreditors has been replaced by a system of setting clear priorities for paymentwith automation of payment requests. The SAFCO Law abolished the ComptrollerGeneral's ex ante functions, and thereby rids the system of its built-inincentives for corruption. The theoretical framework for a modern system ofexternal control has been established and internal audit guidelines have beenproduced.

1.20 The SAFCO Law established the following interrelated systems:

Budget-Programming and Plannina Systems - RequiLed to delineate the inputsand expected results of every public entity. These systems include:operations programming; management of personnel to determine number andquality of human resources needed to carry out these operations, as wellas procedures for hiring, promoting, and firing public servants; managementof goods and services, including their procurement; and budget formulation,whereby every entity provides in financial terms the inputs determined bythe application of the preceding systems.

Cash Management System in Treasury - The Treasury (TGN) becomes the onlyentity responsible for executing the financial plan of the national budget.These systems provide the TGN with budget execution procedures so it canmaintain a balance between disbursements, the availability of funds, andthe governmental policy priorities, and at the same time minimizesubjectivity in actual disbursements.

Integrated Accounting Systems - Financial information will be recordedthrough accounting systems separate from the producers of that informationand from the decision-making agents; thus, accounting information canprovide feedback into the decision-making process without compromising itsindependence.

-7-

1.21 Applying the three systems of financial administration should bringabout an organizational equilibrium between operations programming and budgeting,budget execution and Treasury disbursements, and the recording of financialtransactions and results. Accounting becomes the core of financial informationfor the management information system of the public sector. Its role must beindependent from management decisions. Only this independence, and anappropriate hierarchy within the established organization, can assuretransparency in the exercise of public functions by governmental authorities,auditors, and society as a whole.

1.22 Structural Implications. Two important institutional changes cameabout as a result of the SAFCO Programs the reorganization of both the Ministryof Finance and the Comptroller General's office.

1.23 (a) Ministry of Finance. Suprew.ie Decree 22106, passed iL 1988,reorganized the MF, creating the General Accounting Office (GAO) as asubsecretariat. This change is a major accomplishment of the SAFCO Program,since it established the functional equilibrium required fur efficient managementof public funds. This change brought about the transformation of the TGN froma cashier to the actual manager of public funds. It also allowed forimprovements in the budgeting function by developing detailed methodologies forbudget formulation. In addition, the GAO began to produce, for the first timein Bolivian history, financial statements, useful for managers of publicentities.

1.24 The Ministry of Finance essentially was reorganized into fivesubsecretaries: Treasury, Public Budgeting, Tax Collections, General AccountingOffice, and General Coordination. This reflects the separation of incompatiblefunctions in the management of public funds and was based on the followingnotions: (a) external control should not interfere with the administration andfunctioning of public entities, i.e., ex Post control should obtain, which shouldthen feed back into management as an element for corrective action; (b) externalpost-control (auditing) is irrelevant if the administrative systems required toplan and execute functions are not in place--since the lack of suchadministrative systems endangers the efficiency of governmental policies, sinceit calls into question the executing capacity of those public entitiesresponsible for implementing policies; and (c) the lack of administrative systemsthat have characterized the Bolivian public sector must be corrected, especiallythose relating to the management of public funds.

1.25 The SAFCO Law then legitimized this structure and identifies the MFas responsible for the implementation of financial administration systems, withthe GAO responsible for the establishment of accounting systems government-wide.The SAFCO Law gives the MF clear responsibility for implementation and review ofoperations programming, organization of the public sector, budgeting, personnelmanagement, procurement of goods and services, Treasury and public credit, andintegrated accounting (Annex 13). The law also defines "public indebtedness,"external and internal, and establishes the State (in practice the TGN) asguarantor of all public sector indebtedness. Finally, the law separates fiscaland monetary authorities, making the Central Bank an independq.nt monetaryauthority, no longer dependent on MF.

-8-

1.26 Supreme Decree 22726, paosed on February 6, 1991, reestablished theGAO as a subsecretariat in the MF. (A previous decree had proposed making GAO a

separate entity reporting simultaneously to the MF and the Presidency.) Thus,

the current organization of the MF includes four subsecretariats: Accounting,

Operations Programming/Budgeting, Treasury (which now includes Tax Collections),

and Financial Administration (formerly the Coordination Subsecretariat) (see

Annex 6).

1.27 (b) The CQomtrgller General. CGR is responsible for external control

and auditing functions, and for establishing norms and standards for internal

control systems in public entities. The Comptroller General is appointed by the

President for a 10-year term. The current Comptroller General has taken a lead

in preparing GOB's program to improve financial information, administration and

control in public sector entities. During his administration, CGR staff was

reduced by 50% (from 1,186 to 592). Efforts to reorganize CGR and develop a core

of competent auditors continues. An important breakthrough of CGR was also the

removal of ex-ante control functions.

1.28 The SAFCO law outlines CGR's functions and calls for a change in the

organization and functions of the Comptroller's Office so that it can fulfill its

responsibilities as the standards issuing entity of the governmental control

system and as the senior public auditing institution. Furthermore, all

activities that are incompatible with its auditing function, including fiscal

claims proceedings, have been eliminated.

1.29 Substantial additional effort is now needed to develop this control

system by CGR. The implementation of the auditing component during the SAFiCO

program lagged significantly behind the other components, basically due to the

absence of adequate accounting systems which has delayed the auditing progran,

as there was no information available to audit. Yet, it is expected that with

the legal authority established by the SAFCO law, and a financial administration

system in place, CGR will be able to develop the control functions by producing

reliable audit reports and orienting public entities in their own development of

internal controls.

1.30 These reforms, though constituting only the first phase of

improvements to the system, have had measurable impact on public financial

management, including: (a) reduction of budget deficit from 7.5% of GDP in 1987

to 0.8% in 1988, and has been instrumental in attaining the agreed IMF targets

for 1989 and 19901 (b) production of budgets that reflect Government's priorities

in terms of expenditure ceilings and individual entity's operational goals; (iii)

public investment decisions being made based on financial analysis of requesting

entities; (iv) closer monitoring of wage bill increases by the Cabinet; and (iv)

the aggregate statistics for the non-financial public sector produced under the

Emergency Program have been crucial for public expenditure planning and control

and helped Bolivia to reach an agreement with the IMF.

D. Remaining Constraints

1.31 Imglementing the SAFCO Law. Given the narrow margin in managing its

public finances, the Government of Bolivia must be able to monitor expenditures

-9-

with greater precision. To this end, clear financial reporting on theperformance of governmental entities and enterprises must take place by makingthem accountable for their performance. The SAFCO program has gone a long waytoward giving MF the oversight capacity it needs to monitor expenditures andprogram its resources. It has also developed the framework for CGR to enforcepublic accountability. Yet, additional work is needed to: (a) bring thesefinancial administration tools (budget formulation, integrated accounting, andcash management) to every public entity; (b) strengthen basic financial andoperational audit capabilities of CGR; and (c) introduce similar administrativesystems and standards for non-financial systems--operations programming,procurement of goods and services, personnel management, and organization of thepublic sector.

1.32 The importance of extending the SAFCO reforms to the entity level isbased on the need for appropriate budget execution mechanisms, which involve thesupervision, review of operations, costs and requirements. While it may beeasier to establish methods and devices for control of entity expenditures (ashas been done through the TGN's budget execution system at the central level),than to develop entity's responsibility for effective participation of budgetexecution, without such responsibility, budget execution will become a processof reviewing transactions for compliance and considering requests for deviationsin account transfers, rather than an actual management and control of financesby every entity. The danger with the latter is that all systems introduced runthe risk of becoming merely formalities rather than self-management tools forpublic sector entities.

1.33 Cash management and public credit is probably the most poorly definedfunction in the structure of the Bolivian public administration, since there areso many entities and administrative units. There is a special Public Credit Unitin the MF Treasury Secretariat but it is small and weak. In addition, MPC alsohas a special unit to expedite external credit. The Banco Central de Bolivia(BCB) has an external Credit Management Unit and the Ministry of Foreign Affairsalso has a special unit for international agreements, specifically includingcredit. The SAFCO Law determines how this should be reorganized forsimplification and efficiency. Public Credit should be a fully capableDirectorate under the MF Treasury Secretariat, able to formulate policies,implement them, and manage the debt while not duplicating functions and systemsalready in place.

1.34 Also, interinstitutional relationships governing the management ofpublic credit need to be implemented, as provided for in the SAFCO Law. Forexample, BCB performs functions such as debt management on behalf of MF, and moregenerally acts as a financial agent for MF. It performs these functions,however, without systematically providing accounts reports or other informationto MF. GOB is attempting to establish an information flow between the twoagencies and to ensure that all of BCB's efforts on behalf of MF are transparentin the national budget.

1.35 New arrangements should also be installed between MF and MPC. TheSAFCO law confers public investment responsibility on MPC. Since the Bolivianpublic sector generates no savings, this means that MPC prepares a plan to benegotiated with international donors. This plan, however, is formulated within

-10-

the public credit policy guidelines spelled out by MF. Whenever a project is

proposed, it should first undergo evaluation by the relevant sectoral ministry,

RDCs or other public sector entity, and then be presented to MPC for approval in

conformance with the public investment plan. Only after this review is performed

should the plan be negotiated with international donors, with the support of the

Ministry of ioreign Affairs. Currently, the system does not work like this, and

there is a duplication of functions and responsibilities.

1.36 The TGN, once a simple check-signer, now controls expenditures and

disbursements in accordance with budget quotas, availability of funds and within

macroeconomic ceilings but needs to concentrate on its accounting function. In

this regard, PFMO I helped: (a) prepare manuals describing how to formulate and

execute budgets; (b) design systems for monitoring quotas, actual disbursements,

simplifying payments and ultimately :educing substantially the past TGN

"subjectivity"; (c) design systems to he'p reconciliate Bank statements informing

rapidly on fund availability; (d) allovw for public pensions to be more regularly

paid and greatly simplified; (e) enable Public Credit to take stock of

outstanding debts as well as payment schedules for principal and interest due;

and (f) issue manual for the public credit function within TGN.

1.37 Current information systems are limited in coverage to the central

administration, and lack a module to consolidate and maintain a financial data

base suitable for frequent and high-level consultation. While the existing

integrated system tracks budget execution, cash flow information, and budgetary

assignmenc in real time, much work is needed to integrate existing software and

improve processing time. The provisional budget formulation and evaluation

systems are extremely slow to operate and difficult to modify. And no support

is provided for auditing and Treasury functions. CGR also lacks minimal audit

operations and resources control systems and computer equipment to speed audit

work in the field. Similarly, the Treasury lacks a basic cash management control

system. This is aggravated by a lack of integration between budgeting systems

and other GOB's systems, i.e., accounting and planning. Furthermore, systems

currently operating are not compatible reducing the benefit of the information

flows throughout the public administration.

1.38 Although the SAFCO Law has been successful in defining how the

auditinc function should be linked to other functions of public sector financial

management, the original goals are far from being met. Indeed, the first training

course for auditors was just completed in early 1991. It will take a few years

for auditors to gain practical experience and develop professional judgment, and

even longer to develop into skilled audit managers. There is an urgent need to

perform financial and compliance audits throughout the public sector but CGR

cannot meet this challenge for lack of an appropriate organizational structure,

well established norms and procedures, and an adequate number and quality of

specialized staff. Internal auditing has been studied, but to date there is no

real internal audit function in the public sector, since those called internal

auditors perform other, often incompatible duties.

1.39 Moreover, formal training courses have just begun to scratch the

surface of potential trainees who must learn basic principles of accountability

and control, not to xiention those needing specialized training. Thus far, less

than 5% of potential trainees have been reached. In this respect, PFMO I was

-11-

less successful in reaching its stated objectives. The CGR did develop basicstandards for governmental auditing and organization of internal auditing unitsin public entities; however, the numerous revisions of these standards delayedthe training in governmental auditing. In addition, the delay in performingexternal post-control was due to lack of administrative systems required to planand execute functions in the public entities. Furthermore, CGR's recentactivities were concentrated on lobbying for the passage of the SAFCO Law, sincethe law represents the essential legal basis for the enforcement ofaccountability through CGR's audits.

1.40 Traditional civii service issues make it difficult to retain qualifiedpublic servants and to modernize the public sector. Programs such as economicrecovery and social development are constrained in this regard. This also appliesto financial management and cont..ol functions. However, GOB's dependence oninternational donors requires that adequate salaries for key officials and neededprofessionals be assured and harmonized to avoid unnecessary andcounterproductive competition for the limited human resources available in thecountry. A Public Sector Management Program was originally discussed with GOBand the donor community in mid-1988 to remedy this situation, with a concreteproposal made by GOB to the July 1988 Consultative Group. This has recently madeprogress and a pilot project in MF is at the implementation stage.

E. Donor Assistance and Coordination

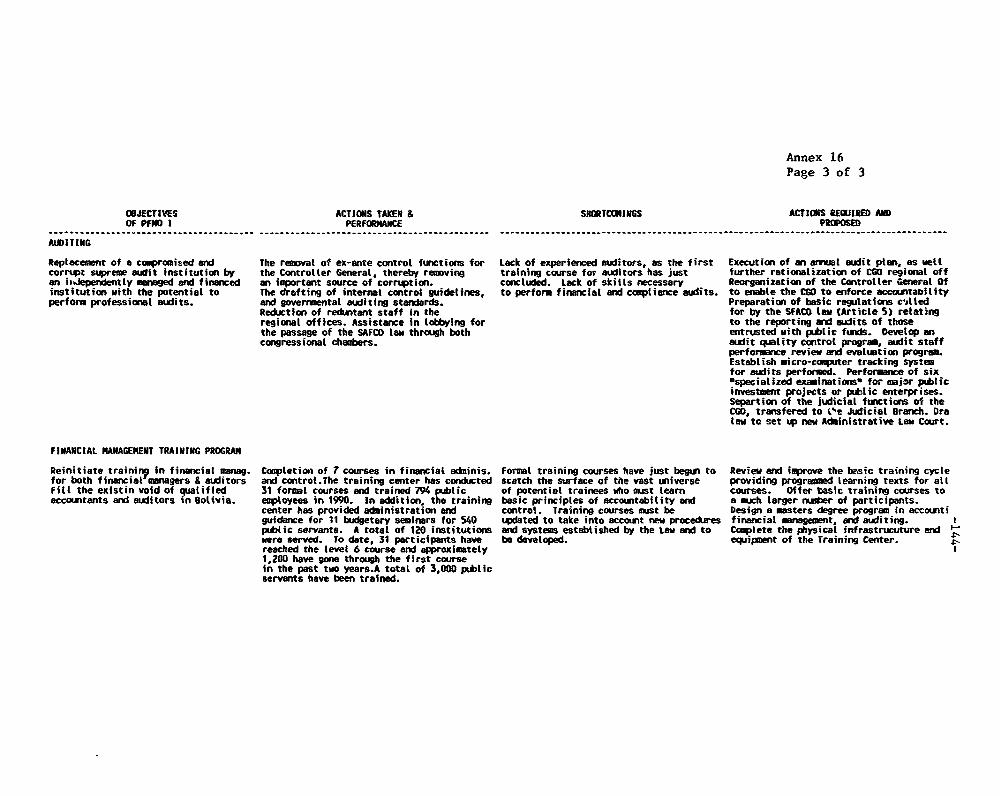

1.41 IDA helped the Government initiate major changes in its fiscal andfinancial systems as early as 1984, when it contributed to diagnose weaknessesin public accounting and auditing. IDA intensified its efforts as part of itscommitment to support GOB's New Economic Policy by working alongside CGR indesigning a program to improve financial management and control of public sectorentities. This program resulted in Public Financial Management Operation (PFMOI) (US$ 11.5 Million, SDR 9 Million), which became effective in December 1987,and was fully disbursed in March 1991. PFMO I provided financial information,administration and controls, and build related staff's know-how in the mostimportant central and decentralized public entities and built an efficient taxadministration system to enable implementation of the 1986 tax reform. PFMO I hasbeen highly successful in achieving its objectives, particularly in improving theavailability and quality of financial information required to exert financialcontrol and discipline. Annex 16 provides a tabular presentation of PFMO I' sperformance, shortcomings and resulting further actions required.

1.42 Indeed, the most notable improvements financed by PFMO I have been thesignificant advances in tax administration, with statistical and audit functionsfor the Internal Revenue Department and institutional support for thesubsecretariat of Tax Collection in MF, as well as its predecessor the Ministryof Tax Collections. A comprehensive tax collection system through the banksbecame the centerpiece of the new tax administration effort. Technical assistancein this area was instrumental to an increase in tax revenues of 480% in the firstyear of implementation as a result of reduced tax evasion and corruption.

1.43 USAID has also a long tradition of supporting Bolivia' s financialmanagement. In the late 1969's and in the 1970's it provided technical assistance

-12-

for financial management and it financed the CGR building. A new accountingsystem was set up under responsibility of MF and a professional approach toauditing was introduced in CGR through an intensive nine month training programoffered over several years for the audit staff. New decree-legislation set forthmodern accounting principles and standards, a new structure for CGR and a"National System of Control".

1.44 Additionally, an IDB project, recently approved by its Board, includesa substantial institutional development component (US$5.5 million) to helpstrengthen the municipal capacity of at least 9 Department capitals and El Altoand 22 more regional entities participating in its urban development programthrough technical assistance, training, information systems and equipment. Thiseffort will be channelled through the Regional Development Fund (FRD).Coordination in preparing the new financial management systems under PFMO II, hasbeen ensured and is expected to continue during implementation. The proposedPFMO II, described below, will support efforts in financial managementcapabilities for other municipalities, so that SAFCO law principles, norms, andregulations can be implemented and institutionalized.

F. Rationale for IDA Involvement

1.45 IDA's broad country strategy is based on an effort to assist GOB inimplementing its medium-term economic program for achieving growth andinvestment. Bolivia faces severe constraints on its resources which allow itlittle room for deviation from the current macrostabilization program, makingpublic financial management essential in maintaining control over publicexpenditures. Supporting these financial management reforms through broad-basedinstitutional efforts is at the core of the country strategy. An IDA proposed SACwould address these issues supporting the following: (a) maintenance of acoherent macroeconomic policy aimed at continued stability; (b) financial sectorreform to strengthen banking supervision, privatize or close and liquidate loss-making public banks, improve the allocation of donor-financed credit, establisha mechanism for handling bank crises and improve the laws and regulationsgoverning pensions, insurance, and securities markets; (c) signature ofperformance contracts and improvements in operation of the major stateenterprises; (d) a comprehensive privatization program with the medium-term goalof divesting all state enterprises in productive sectors (with the exception ofmining and hydrocarbons due to Constitutional restrictions); (e) streamlining oftrade and registration procedures, including customs reform, a duty drawbacksystem, simplification of export approvals and simplification of firmregistration and control mechanisms; (f) cooperation with the Bank in improvingpublic sector investment project selection; and (g) increase in the share ofcurrent expenditures devoted to primary health care and primary education. Itis important to complement such a reform program with modern financial managementprocedures and standards to achieve a higher level of efficiency in the publicsector, in harmony with this trend in the PEs. This goal is a feature of thepublic sector financial management reforms throughout the centralized anddecentralized public sector agencies as called for by the SAFCO law.

1.46 IDA has actively supported GOB's efforts to consolidate itsstabilization reforms. In addition to an operation in public financial

-13-

management, IDA has taken a lead role in assisting GOB in investment planning,statistics, and regional planning through an IDA-financed Economic ManagementStrengthening Operation (EMSO). EMSO is also supporting GOB's critical problemof low salaries and little continuity of middle level public servants(complicated further by its ad hoc payment and recruitment arrangements) throughthe rationalization of the salary structure in the short term (through the PublicSector Management Scheme) and the establishment of a sound management andpersonnel system in the long run. In the financial sector, IDA has contributedto the establishment of a sound framework for financial intermediation throughthe previous Financial Sector Adjustment Credit. These basic reforms areprerequisites to building coherent financial and economic decision-making. GOBhas now requested that the Association support expansion of public financialmanagement reforms introduced throughout the central government with theassistance of the Public Financial Management Operation (PFMO I) Cr.1809-BO.

1.47 The proposed Public Finar.ial Management Operation II (PFMO II) aims atenhancing GOB's financial management capabilities, critical for policy execution,implementing uniform and compatible guidelines and procedures for publicfinancial management government-wide so as to ensure a more efficient use of itsscarce resources. This would be achieved through: (a) expanding comprehensiveaccounting reforms to representative decentralized institutions; (b) broadeningthe scope of existing financie.l administration and control systems to localgovernments and decentralized institutions; (c) including other nonfinancialsystems needed for efficient allocation of resources; and (d) training. The mainobjective of this effort is to create financial management and controlcapabilities at the entity level, not only at the integrated central ministries,to extend financial discipline throughout the public sector. Furthermore, theproposed project would strengthen the capacity of the Comptroller General of theRepublic to enforce accountability for results in the exercise of its publicresponsibilities.

1.48 If successful, this second IDA-assisted operation would greatlystrengthen GOB's capacity to manage efficiently its scarce resources and at thesame time increase accountability for cost-efficient results in the publicsector. Additionally, it would contribute to a leaner, more efficient stateapparatus better able to facilitate and stimulate private sector development.However, public financial management is not a function that can be improvedpermanently by any given technical assistance. The dynamic of the sector willrequire continued attention and enforcement on the part of future Boliviangovernments before the current administrative culture can progressively absorbaccountability principles and procedures on a sustained basis. It is expectedthat other international donors (USAID and IDB and other bilateral assistance)would also help GOB progress further in this regard. IDA continues to have alonger-term commitment to the improvement of public financial management ofBolivia as embodied in the proposed project.

-14-

II. THE PROJECT

A. Proiect Obiectives

2.1 The Government of Bolivia continues to confront a broad array ofconstraints in its attempt to redress the dire economic environment andadministrative chaos of the Bolivia public sector in the early 1980s. Efforts todevelop the legal framework for financial control and auditing of public entitiesbegan with the formulation of the SAFCO Law, approved by special session ofCongress in July 1990. Under PFMO I, success was achieved in developing anintegrated financial administration and control system at the central level ofgovernment. The Government of Bolivia has now requested a follow-up operation tostrengthen financial administration and control norms and procedures introducedunder PMFO I. The objective is to create financial management capability in thedecentralized institutions to facilitate implementation of the SAFCO Law andenforce public sector accountability.

2.2 The proposed PFMO II would complemelt EMSO's efforts to diagnose thefinancial and organizational capacity of t: .-centralized levels of governmentand administration. Whereas PFMO I developed initial financial management,control, and oversight capacity of MF and CGR, PFMO II would concentrate on theothar public sector entities at tne national and local levels, completing theeffort to provide the Government with management information systems critical toexecute policy and take appropriate corrective measures. Also, PFMO II wouldalso focus on helping the CGR implement accountability measures so vital to the

transparent management of public funds. Ultimately, the project would contributeto the long-term institutional building process and in particular, to theenhancement of the absorptive capacity through enabling GOB to take moreefficient advantage from the community of donors' assistance in general.

B. Proiect DescriPtion

2.3 The proposed project comprises four main components: I. FinancialManagement and Control; II. Regulatory and Legal fi.mework; III. Training; andIV. Institutional Support. The specific objectives under each component aredescribed below.

I. Financial Manaaement and Control:

(i) budgeting capacity at the public entity level, transferringthe responsibility for budget formulation from MF to everyentity based on planned activities and investments, andimproving the Budget Subsecretariat's ability to evaluatebudgets;

(ii) cash management, strengthening the Treasury's functions, fine-tuning the disbursement and quota mechanisms for budgetexecution, rationalizing TGN payments by eliminatingsubtreasuries, replacing them by payment through the banking

-15-

system, as well as rationalizing commissions charged forpublic services;

(iii) developing comprehensive accounting systems consistent withguidelines already developed under p%evious operations butspecific to 14 representative entities, for replication inother decentralized entities and local governments, thusensuring uniformity of procedures and classifications notlimited to the reporting of cash flows; and

(iv) government auditing, to enable CGR to assume theresponsibilities outlined in the SAFCO Law, specifically toenforce public accountability in a coherent and harmonizedmanner.

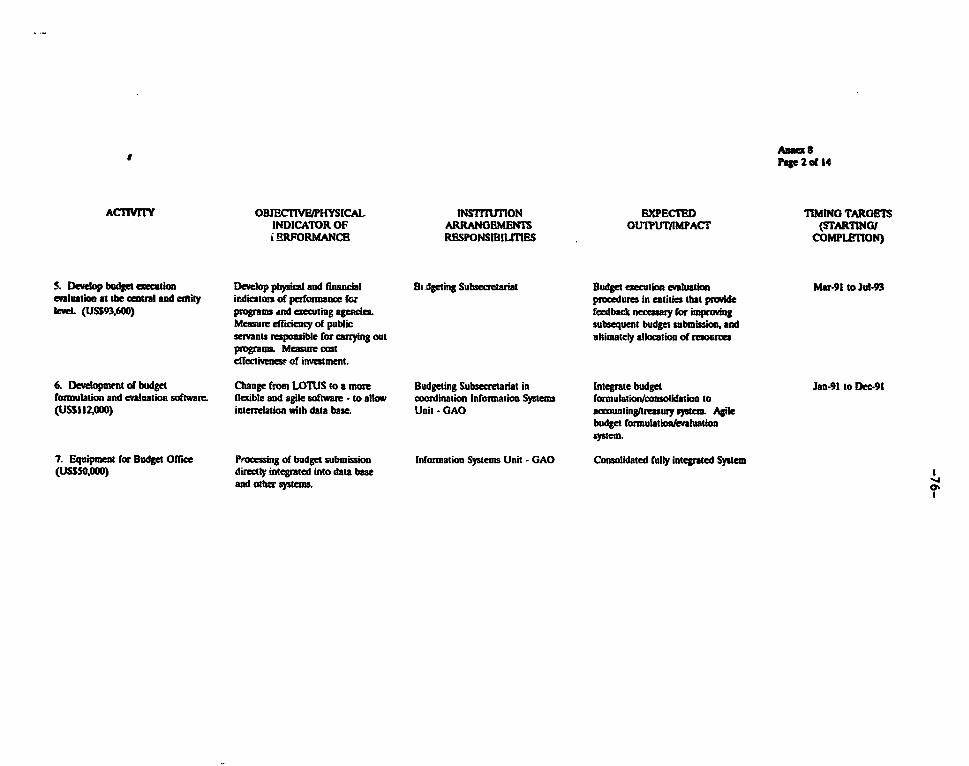

2.4 Budgeting. This element is intended to generate program-basedbudgets for the major public entities at all administrative levels, as well asproviding these entities with evaluation information to progressively improvetheir own budgeting practice. Under this component: (i) use of the newlydeveloped manuals and standards will be disseminated to line ministries, in thefirst instance, and subsequently disseminated to major decentralized entitiesunder these ministries; (ii) evaluation methodologies will be developed toassist the ministries and decentralized entities to improve their budgetingtechniques; and (iii) further fine-tuning of the budgeting manuals andstandards will be made by the MP Budget Subsecretariat to incorporate moredetailed techniques on operational programming (physical targets), procurementprocedures and personnel management standards developed under a separatecomponent (para. 2.11). In this regard, it was agreed at Negotiations, that theprogram-based budgets would be fully operational at central government ministriesand at major public enterprises by the end of 1992, and Regional DevelopmentCorporations and major municipalities by the end of 1993. In addition, thecomponent will assist the MF budget Subsecretariat to improve its capacity toevaluate the implementation of approved budget submissions and to generatemacroeconomic indicators and national accounting statistics on public investmentsbeing undertaken. In this regard, existing computer software will be improvedto make it compatible with the newly established accounting and budgetingprocedures.

2.5 Budaetina Comiponent Inputs and Activities (US$O.6m)

i. complete the budget formulation methodology developed byintroducing procedures and standards for operationsprogramming, personnel management and administration of goodsand services, as well as adjusting the budget formats andclassification to reflect new organizational patternsintroduced (US$64,000);

ii. transfer budget formulation responsibilities from MF's BudgetSubsecretariat to the public entities (US$74,000);

iii. provide periodic reviews of budget formulation and evaluationprocedures (US$103,000);

-16-

iv. strengthen the Budget Subsecretariat's ability to adjustindividual and consolidated budget submissions tomacroeconomic targets (USS 94,000);

v. develop budget execution evaluation procedures at central andentity levels (US$94,000);

vi. make compatible budget formulation and evaluation softwarewith that developed for accounting and treasury disbursements(US$112,000); and

vii. expand the computer equipment of the Budget Subsecretariat fora greater coverage of institutions and information (US$50,000)

2.6 Financing of 43m/m of foreign and 152m/m of local specialists wouldbe required to guide the process of reviewing norms and procedures, prepare thecorresponding guidelines and manuals. Local specialists would carry outdissemination efforts and support local and decentralized entities to implementthe new systems. Periodic reviews of the budgeting system would take place thefirst four years of project implementation. Annex 5 provides a description ofconsultants' proposed terms of reference.

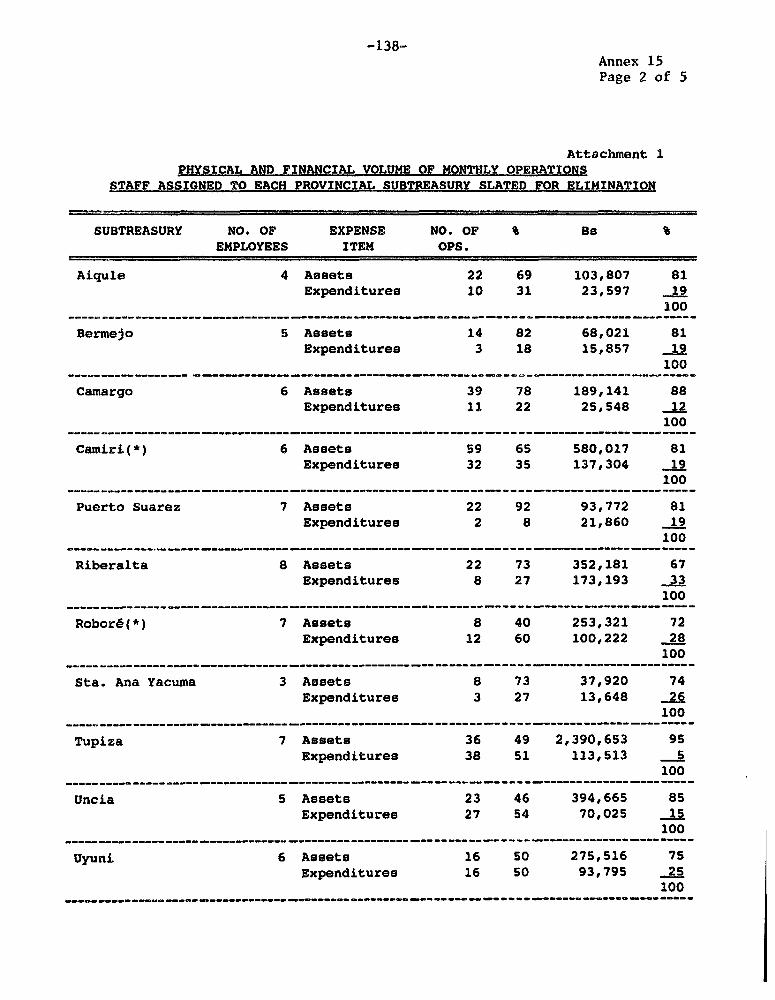

2.7 Cash Manacement and Public Credit. The proposed project would assistGOB in: (i) operationalizing the legal framework for consolidating a cashmanagement system under Treasury by drafting procedures and regulations andi.ndertaking the necessary organizational changes in the Central Bank, theMinistry of Planning, and the Treasury; (ii) improving the efficiency of paymentsystem of Treasury by eliminating the use of subtressuries and replacing them bythe commercial banking network; (iii) improving cash management of publicentities through provision of new procedural guidelines and standards; (iv)rationalization of commissions charged for public services under "valoresfiscales"; and (v) improving the Treasury' s income and payment projectioncapacity through provision of a computer-based system to track tax revenueinformation, cash disbursement, and public debt payment schedules. In thisregard, it was agreed at negotiations that (a) organizational changes for cashmanagement in Treasury would be achieved by the end of 1992; (b) the privatecommercial banking network for cash transfers would be used starting no laterthan June 1992; and (c) a timetable, acceptable to IDA, for elimination ofsubtreasuries would be submitted by the end of 1991 and actual implementation ofthe agreed timetable achieved by the end of 1992. Annex 15 provides details onthe elimination of the subtreasuries.

2.8 Cash Management Component Inputs and Activities (US$0.6m)

i. design and implement systems for public cLedit, defininginstitutional responsibilities (between the Central Bank, thePlanning Ministry, and the TGN) as outlined in the SAFCO law,translating it into clear regulations and procedures to beenforced (US$273,000);

ii. substitution of payments made through subtreasuries bypayments directly through the banking network, thereby

-17-

eliminating oubtreasuries1. MF has had a favorable experienceof using the banking network for tax collections (for ananalysis of advantages/disadvantages of eliminatingsubtreasuries see annex 15) (US$77,000);

iii. disseminate new treasury/cash management regulationo to thedecentralized levels of governments and review of theapplication of these standards once the entities haveformulated and begun to apply them (US$172,000);

iv. rationalize the issuance of public service commissions,including an inventory of exiating fiscal paper as well as theestablishment of clear rules for the provision of publicservices (US$64,000); and

v. provide computer equipment to support above-defined upgradedfunctions, track cash payments and record public credittransactions (US$25,000).

2.9 Provision of 44m/m of foreign financial management specialists wouldbe needed to help review current systems, fintlize the definition of new normsand procedures at the center, namely in the MF the TGN Public Credit Directorate.They would also help launch a dissemination program to be carried out by 186m/mof local financial management specialists, financed by the proposed project, toensure adequate enforcement of the system throughout the public administrationat all levels. Annex 5 provides a description of the consultants ' proposedterms of reference.

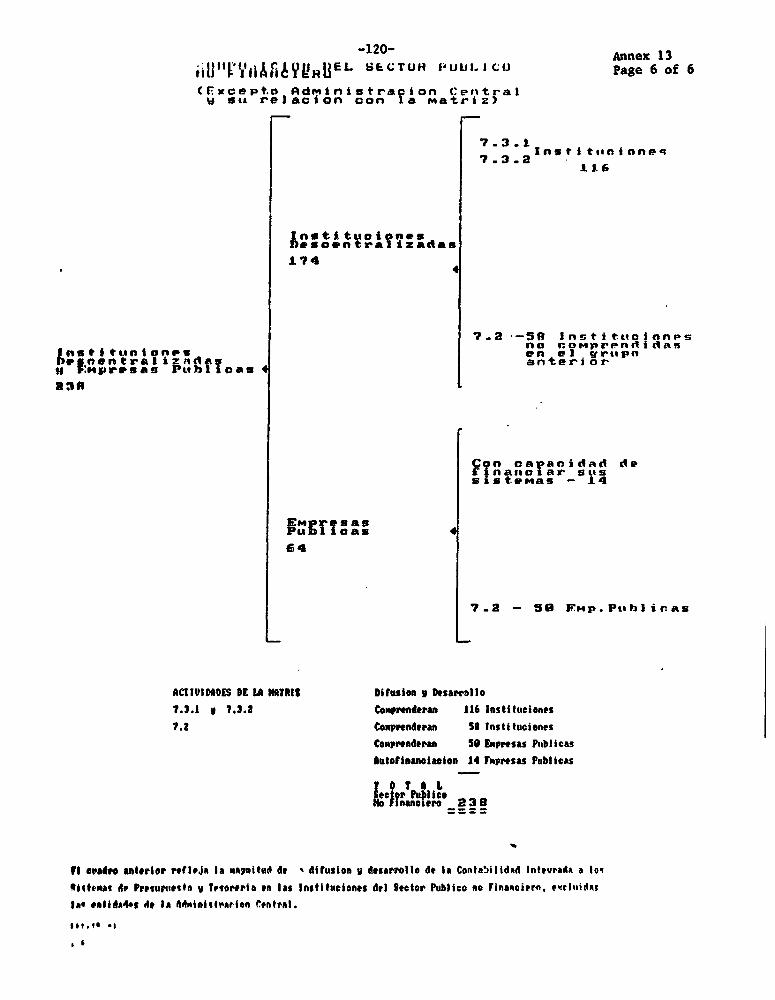

2.10 Accounting System. The objective is to develop comprehensiveaccounting systems throughout the public sector, consistent with the accountingguidelines already developed by PPMO I, to ensure uniformity of accountingprocedures and classification. It would help entities recognize accountingrequirements and their basic relationship to budgeting. This would be done by:(a) the development of accounting systems in 14 representative decentralizedinstitutions, with dissemination of these models to 116 decentralizedinstitutions; (b) the adaptation of the existing generalized "Manual forDecentralized Institutions" to 58 decentralized institutions not part of the

representative sample; and (c) adoption of existing "Guidelines for PublicEnterprises" to 50 enterprises that cannot finance the development of their ownaccounting systems; and (d) the development and implementation of simplified

versions of accounting, budgeting, and cash management systems to 90representative smaller local institutions (provinces, hospitals, educationalcenters, airports). In this regard, it was agreed at negotiations that GOB would

complete the development of accounting system and implement it for each group ofentities as follows: (i) by the end of June 1993 for the 14 representativedecentralized institutions and by June 1994 for the dissemination of the

corresponding models to 116 decentralized institutions; (ii) by the end of 1994

It is important to note that 56% of the TGN's current staff is located in

the sub-treasuries.

-18-

for the adaptation of the existing generalized Manual for DecentralizedInstitutions to 58 decentralized institutions not part of the representativesample; (iii) by the end of June 1994 for the adoption of existing Guidelinesfor Public Enterprises by 50 enterprises of a smaller size; and (iv) by theend of 1994 for the development and implementation of simplified versions ofaccounting, budgeting, and cash management systems to 90 representative smallerlocal institutions (provinces, hospitals, educational centers and airportw.Annax 13 provides a description of the strategy to be adopted for reaching suchoutputs.

2.11 The GAO will take on the responsibilitl for consolidating fiisancialstatements of the public sector, including cash flow information, which LS

currently handled by the "Emergency Program" of the SAFCO program. Assistancewould be given to GAO to: (a) develop the capacity to incorporate balances fromthe public entities into its integrated governmental accounting balance; and (b)review existing accounting systems and the proposed modified systems, especiallyin those not directly financed by the project such as public enterprises. In thisregard, it would be at negotiations that the Emergency Program staff would beabsorbed by the end of June 1992.

2.12 Accounting Component Inputs and Activities (USS 3.8m)

i. develop auxiliary detailed accounts and supplementary accountsof the central administration, completing the financialinformation the ministries currently provide GAO by broadeningthe detail of accounts, and disaggregating the accountingclassification they currently use for their own financialmanagement. This also includes the development ofinstitution-specific modules to feed data into thecomputerized financial information system. (US$234,000);

ii. install integrated accounting systems to the 14 decentralizedentities, including: one Prefectura, two Regional DevelopmentCorporations, two Pension Funds, the National Road Service,two Hospitals, one university, two municipalities, and threeother decentralized institutions that carry out variouscommunal services (see Annex 13 for selection criteria,implementation schedule, etc. ). This activity includes thedevelopment and implementation of a transportable version ofthe computerized information system, as well as theintegration of budgeting and treasury functions into thesystem (US$1.5 million);

iii. adopt accounting procedures and classification by adjustingand applying: a. the accounting "Manual for DecentralizedInstitutions" to 58 institutions not covered in point ii, andb. the "Accounting Guide for Public Enterprises" to those 50enterprises that cannot finance their own accounting systems(see Annex 13 for the list of these instituJtions)(US$483,000);

iv. implement simplified procedures and standards for budgeting,

-19-

treasury/public credit, and accounting to 90 representative

smaller entities in the decentralized government by nelectingin each Department. two non-capital municipalities, two

hospital, two educational units, two agencies repreoentingMACA, and two sports centers (US$309,000);

v. implement the Public Sector Financial Data Base2 . As the use

of the new accounting, budgeting, treasury/public creditprocedures iB extended to the entire public sector, it ls

possible to consolidate all financial, budgetary, and cashtransaction information country-wide. X national data base

will be created for this purpose, as well as a sophisticatedquery and reporting capability for government-wide financial

management. This data base would gradually replace the

existing "Emergency Program" operation (US$223,000);

vi. acquire computer hardware/software for the GAO's InformationSystems Unit to expand coverage of the information system

described in point iii above. Larger configuration of the

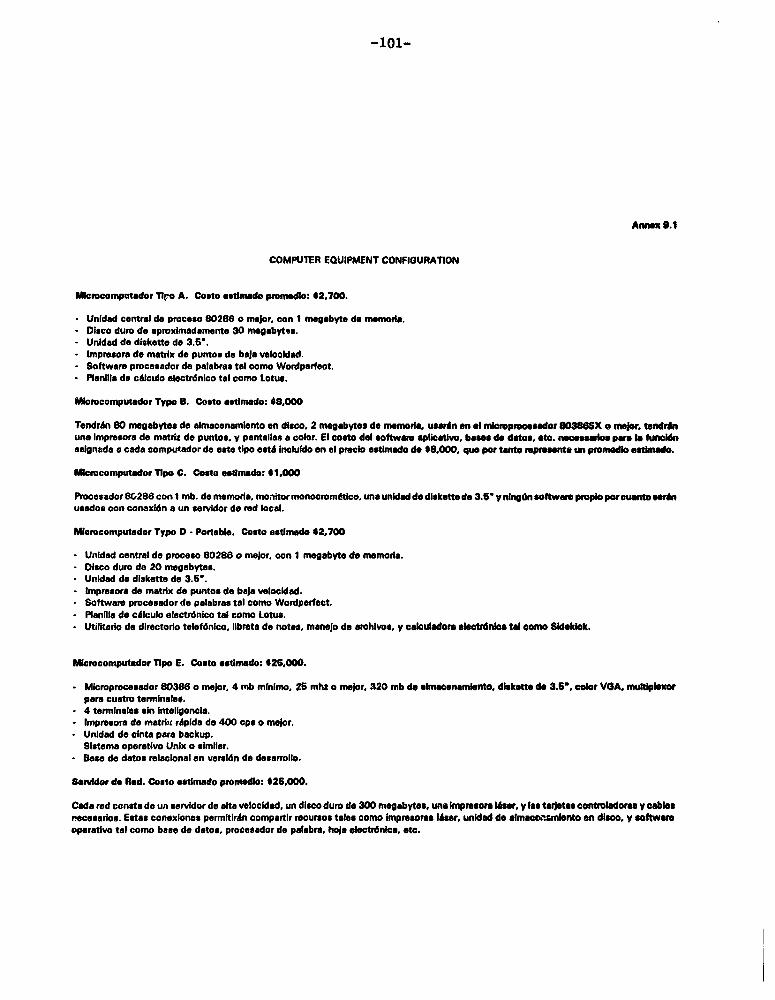

minicomputer and operation of open version of system(US$300,000). Annex 9 provides a description of the proposedoffice technology for GAO; and

vii. maintain the "Emergency Program" functioning and providing

statistical data on cash flows from the major public entitiesuntil the accounting systems and information are in place

(US$600,000).

2.13 Financing would be provided for short-term, local (88 man/month) and

foreign (16 m/m) accounting specialists to develop auxiliary accounts at the

Central Administration (activity i); short-term local (96 man/months) and foreign

(46 m/m) to adapt the integrated accounting procedures and system to 108

decentralized entities (activity iii); short-term local (12 m/m) and foreign (6

m/m) systems specialist to transform the computer system into an transportable

open version (part of activity ii); short-term local (78 m/m) and foreign (24

m/m) accounting specialist to implement the simplified systems to the smaller

entities (activity iv); local (42 m/m) and foreign (20 m/m) system specialists

for creating the necessary data base and information flows already described

(activity v); and local (600 m/m) to maintain the "Emergency Program" for three

years (activity vii). In addition, the development and implementation of the 14

representative financial systems would be subject to international competitive

bidding. An approximate cost of US$44,000 for 12 of these entities was

calculated, taking into consideration economies of scale and bidding out groups

of entities. The remaining two entities (the pension funds) are more complex and

would require an estimated cost of US$140,000 each (see Annex 13). Since the

reporting function, i.e., accounting, is the core of the financial administration

information system, this component includes information systems recuirements and

2 Note that information systems is included in the "accounting" sub-

component because the General Accounting Office is responsible for "Information

Systems"

-20-

integration of accounting data with budoeting and treasury/public creditfunctions. Annex 5 provides a description of the sonsultants ' proposed termsof reference.

2.14 Audit'na. Assistance would be provided to gradually expand CGR'sintervention in public financial control through enhancing the audit scopetowards generating recommendations for the improvement of government efficiency.In addition, an annual audit plan would be defined and implemented reducingaudits upon request from 70% to about 30% of those performed and reducing CGR'sOffices from eight to three with a consequent upgrading of staff.

2.15 Foreign and local specialist assistance would be provided to reviewand/or prepare specific regulations called for by Article 5 of the SAFCO lawrelating to reports and audits of those entrusted with, or receiving publicfunds. This would expand the audit universe beyond the entities which composethe public sector to ensure accountability over public resources handled byothers including the private sector. A new Technical and Programming Officewould be established to become responsible for the issuance of all standards andguidance and follow up of compliance. This unit would carry out trainingactivities (see below) as well, since it would produce many of the materials onwhich training would be based. It would also prepare and monitor the annual auditimplementation plan and provide guidance for the internal audit function.

2.16 The most important task facing CGR is the establishment of a cadreof professional auditors and the performance of audits, which contributesignificantly to establishing GOB's credibility and making it able to enforceaccountability. As a result of this assistance, professional audits would beperformed in a timely fashion in accordance with the annual audit plan so as toprovide cyclical coverage of major resource flows. Also internal control supportunits would be creattd in CGR. Due to limited supply of trained managers andmanagement consultants available to GOB, these units would assist public entitiesin establishing the .nternal control systems prescribed by the new law andmonitor progress the:effter routinely. The CGR would be assisted to set up theoffice of the Depvi'; Comptroller for Legal Affairs, replacing its formeradministrative court .':nction. CGR's judicial functions have been transferredto the Judicial Erancl, of GOB by the new law. Once accomplished, the legalfunction still at CGR would provide counsel to the Comptroller General and hisstaff regarding aspect-s of legal compliance auditing and assuring that legalprocesses are efficier. y carried out. A new administrative judgment processwould thus be developer. n the judicial branch and CGR would provide the legalservices necessary for -he audit process on a timely basis as audits areperformed. A draft law X_auld be prepared with PFMO II's support, to set up thenew Administrative Law C( ut t. In this regard, it was agreed at negotiations that(a) the Contraloria Genexal de la Republica would have established the TechnicalProgramming Office, the Legal Affairs Office and the office of the DeputyComptroller and carried out other organizational adjustments by the end of 1994;(b) an annual audit plan to carry out external audits of a representative sampleof public sector entities would be made available to IDA and USAID in the POAsand in the opportunity of reviewing draft contracts with audit firms selectedthrough bidding processes; by the end of 1993, CGR would undertake or requirethat external audits be completed for at least 100 entities and would expand thiscoverage over the following two years so as to have achieved external audits on

-21-

90% of public expenditures; emphasis would be on developing government auditingquality as staff skills would be enhanced; (c) the Contraloria General de laRepublica will inform IDA of the key results of the "special examinations" alongwith the response that the Government intends to give to the correspondingfindings; and (d) the Deputy Comptroller would have extensive training andinternational experience in the application of general accounting principles,auditing standards and management and the General State Accountant would have astrong background in management systems especially accounting and governmentfinancial management. Annex 12 provides more details on past achievements anda description of the proposed program and implementation strategy.

2.17 Government Auditina Component Innuts and Activities (US$S.5m)

i. develop manuals and guidelines for: contracting of independentauditors by CGR and internal auditing units of publicentities, regulations concerning the internal organization ofthe CGR; regulations outlining reporting requirements of allentrusted with public fund or receiving public funds;personnel evaluation systems, tracking systems for audits,results, training and legal proceedings (US$802,000);

ii. reorganize the CGR (see description Annex 12) s0 that it cancarry out the SAFCO articles, namely: a. improveadministrative information and internal control systems in thepublic sector entities; b. audit information systems,especially accounting statements; c. assess the efficiency andeffectiveness of public services, holding those responsiblefor results accountable (including the performance of tenspecial examinations on major projects and enterprises -US$2.25m); d. facilitate the identification of corruptpractices and bringing forward those responsible. Thisincludes the development of the Office of the DeputyComptroller for audits to enable it supervise the execution often special examinations and develop the capacity to performoperational audits through the process(for more detail on theactivities to be financed see annex 12)(US$3.2 m);

iii. create and develop CGR's capacity to manage legal affairsrelated to its responsibilities and work program as outlinedand required in the SAFCO law. This includes drafting of theSupreme Decree regulating the exercise of public function andcorresponding responsibilities, as well as disseminating thisDecree by holding a seminar. In addition, it includes thedrafting of the law creating judicial fiscal tribunals and adata base of administrative law cases (US$821,000); and

iv. upgrade the CGP's computer processing capacity by providingadditional equipment, including minicomputers andmicrocomputers, and printers (US$427,000). Annex 9 providesa description of the proposed office technology for CGR.

-22-