world bank document - documents & reports · second agricultural credit project april 7, 1987...

TRANSCRIPT

The World BankFOR OFFCIAL USE ONLY

Report No. 6040-MAG

STAFF APPRAISAL REPORT

NADAGASCAR

SECOND AGRICULTURAL CREDIT PROJECT

April 7, 1987

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contemts may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSIEQUXVALENCES MONETAIRES 1

Currency Unit M- alagasy Francs (FMG)US$1.00 FMG 752FMG 100 - US$ 0.13

WEIGHTS AND MEASURESWPOIDS ET MESURES

1 hectare (ha) = 2.47 acres1 kilometer (km) = 0.62 miles1 square kilometer (km ) 0.39 square rile1 kilogram (kg) 2.20 pounds-1 l'ter (X) - 0.26 US gallon1 tonne (t) 2,204 pounds

ABBREVIATIONS

APB Association Professionnelle des Banques (Bankers'Professional Association)

ADB African Development BankASAC Agricultural Sector Adjustment CreditDAMES Banque Malgache d'Escompte et de CreditBCRDM Banque Centrale de la Ripublique Democratique de

Madagascar (Central Bank).BFV Commercial Bank (Banky Fampandrosoana Ny Varotra)BNI Industrial Development Bank (Bankin' Ny Indostria)BNM National Development Bank for Madagascar (Banque

Nationale Malgache de developpement)BTM National Rural Development Bank (Bankin' Ny Tantsaha

Mpamnokatra,CG Consultative Group for MadagascarFOFIFA National Center for Applied Research on Rural

Development (also CENRADERU)FMR Rural Credit Program (Financement du Monde Rural)MPAEF Ministere de la Production Animale et des Eaux et

Forkts (Ministry of Livestock, Fisheries and Forests)MPARA Minist;re de la Production Agricole et de la Reforme

Agraire (Ministry of Agricultural Production andAgrarian Reform)

OCD Operations and Credit Department.ODRI Individual Smallholder Credit SchemePEs Public EnterprisesPRDD Planning and Rural Development Department.

I/The Malagasy Franc is pegged to a basket of currencies of Madagascar'smajor trading currencies of Madagascar's major trading partners and therate of exchange is adjusted quarterly. The exchange rate prevailing inSeptember 1986 has been used in this report.

FOR omcIA us ONLY

GOVRNMUENT ADMINISTRATION

Fokontany - villageFiraisam-pokontany a group of Fokontany

(or Firaisana) (former canton)Fivondronsm-pokontany - group of F_raisana

(or Fivondronana) (former sub-prefecture)Faritany - group of Fivondronana

(former province)

GOVERNMENT AND BTM FISCAL YEAR

January 1 - December 31

This tOCIUlt hs a _w-d disbbulion ll may be IISO bY lcipioots O*l i11 tho pOfOb lof thi oftk ddti Its ontmts maynot hofnrwbebodbeksed wkhout Wodd Bank audmwnsKn-

SECOND AGRICULTURAL CREDIT PROJECT

Table of Contents

"a i No.

I Protect Backaround -1

U The Asricultural Sector 1A - Sector Performanc 1B - Goverument Strategy and Objective. 2C - bank Group Support 4

III The Bankina Sector. BTM and the First AgriculturalCredit Proiect 6

A. Banking Sector Structure 6- Reorganisation of the Banking Sector 6- mHnagement 6- The Three Banks 6- The Central 8ank (BCRDM) 7- The Banker's Professional Association (APB) 7

B. Credit Policy 7- Objectives and Regulatory Instrum4nts 7- Interest Rates 8- Agricultural Credit Policy 8

C. Performance 9- The Banking Sector Crisis 9- Bwaking Sector Reform 10

D. The National Bank for Rural bevelopment - BTM 11- Structure 11- Mnagemnt 11- Organixation 11- Staffing 12- Operations 12- Resources 13- Financial Situation 13- The Action Plan 14- The Projections 15

E. The History of the First Agricultural Credit 15Project- Project Objectives and Design 15- Implementation Exprience 16- Conclusions- 18

IV The Proiect 18

A. Project Objectives 18

P4ge No.

B. Project Design 19- The Line of Credit Componeat 19- The Institution Building Component 20

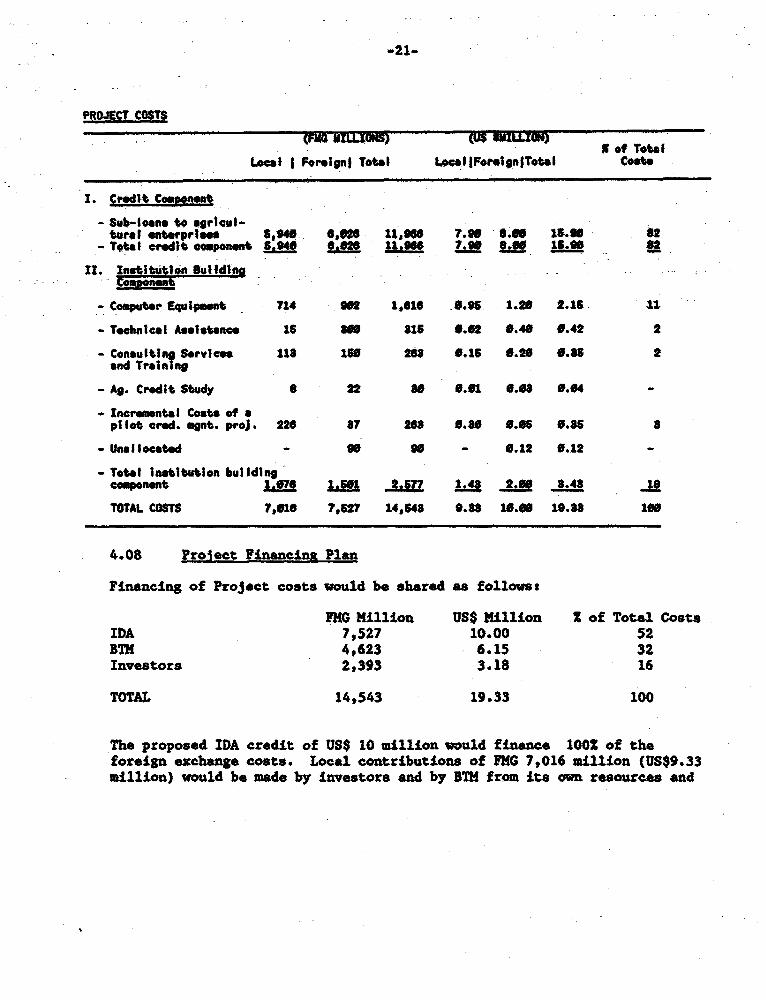

C. Project Costs and Financing Plan 20Project Costs 20

- Project Financing Plan 21D. Procurement and Disbursement 22

-- - Procurement 22- Disbursements 22

E. Accounts and Audit 22

V Project Implementation 23

A. - General 23B. Organization and Reporting 23

The Annual Work Program 23- Project Management 24- Reporting Requirements 25

C. Financial Aspects of Implementation 25

VI Project Benefits and Risks 26

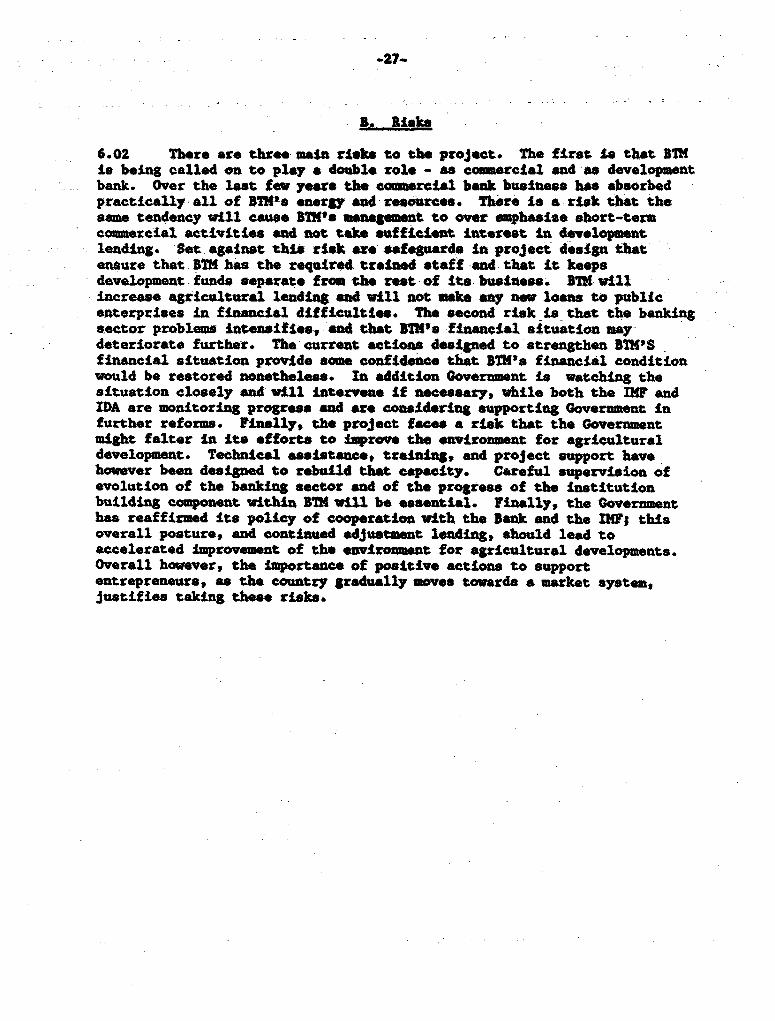

A. Benefits 26B. Risks 27

VII Agreements and Recommendations 28

ANNEXES

1. Credit Outstanding by Sector and Term2. Structure of Deposits3. Actual and Projected Balanco Sheets 1982-19884. Actual and Projected Income Statement 1982419885. Actual and Projected Financial Ratios 1982-19886. Projected Sources and Uses of Funds7. BTM's Interest Rate Structure8. Project Financing by Component and Source of Funds9. List of Identified Sub-projects10. Estimated Disbursement Schedule.11. Policy Statement12. TOR for Project Appraisal Coordinator.

Chart

BTM Organisation

Ea a

Madagascar - IBRD 19406

M ;|CAR

SECOND AGRICULDU9AL CREDIT PROJECT

CREDIT AND PROJECT SUMMARY

Borrowers Democratic Republic of Madagascar

Reneficisrv: - The National Rural Development Bank (BTM).

Amount: SDR 8.0 million equivalent to US$10.0 mnillon.

- Terms: Standard IDA terms,

Re-ending ts (i) The Government would transfer the IDA creditproceeds to BTM as an equity contribution to itscapital.

(ii) Sub-borrowers will have the option of borrowingsub-loans under the following alternative termsand conditions: (a) the IBRD lending rate at thetime of approval plus 42 p.a., the foreignexchange risk to be borne by the sub-borrower; or(b) BTH's prevailing lending rate and commissionsfor local currency lending, plus a front-end feeof 102 of the proposed sub-loan, and a fee of 3Zp.a. on the outstanding amount of the sub-loan.Interest rates will be reviewed with IDA twice ayear to ensure that they are positive in realterms. Repayment periods on sub-loans extended byBTh would be established on the basis of cash flowprojections of each sub-project and on the type ofasset to be financed. The repayment periods wouldnot exceed the average useful life of assets beingfinanced nor would they exceed a maximum period of15 years including a three year grace.

Obiectives and Proiect The project would provide foreign exchange for newDescriptlon: investment and rehabilitation and expansion of

existing businesses in agricultural production,primary processing/marketing, and contribute tothe rehabilitation of the BTM. The project wouldhave two components:

(i) A line of credit of US$ 8 million equivalent whichwould finance, over an expected two and a half yearcommitment period (from about September 1987), the

- ii -

foreign exchange cost of sub-projects. Anypromoter would be eligiblle, subject to criteriaapplied to both promoter and sub-projct.

(it) An Institution Building component of US$2million equivalent which vould finance compaterequpment, technical asistace for audit,manage_nt consultancy service ond training thecost of consultincy services for sub-prOjectprparationg and a study to formulate a suitableagricultural credit policy end system for

adgascar.

Benefitw: The benfits of ths project would accrue throughformers and entrepreneurs to the econamy as a whole, aidto the BT1. Benefits to farmers end entrepreneurs wmldcome from alleviation of two key constr*ints, lack offoreign exchange and lack of term funds, and from adviceand technical asistance provided to them by the BIN andits consultants. Benefits to BT31 will come through thelistitution building component, which would str*nghtenIt as a development bank and a term lender toagriculture. In addition the Project would enable thecreation of net investmont and employment opportunitiesfor Nalagasy nationals by promoting and financingagricultural sub-projects.

Risks: There are throe main risks to the project* Thefirst Is that BT51 being called on to play a double roleas both co_mercia and development bank, it mightcontinu to emphasize short term commercial activitiesand would not give sufficient priority to developmentlendlng. The second risk is that the banking Sectorcrisis gets worse, and BTI's financial situation coulddeteriorate furtber. Finally, the project face a riskthat the Government might falter in its efforts toiuprove the environment for agricultural development.Safeguards gainst these risks have been built In to theproject desiga including saures necessary to streaghenBTi's financial position and the meons to diversify itslending. BTm will lncrease agricultural lending andwill not make any new loans to public enterprises infinancial difflculties. In addition careful Supervisionof the evolution of the banking sector and theStrengthening of BTMi's institutional capability wouldact to offset the ebove risks. Finally, the Governmenthas reafflrmed its policy of cooperation with the lankand the ID; this overall posture, and continuedadjustment lending, should lead to acceleratedlmprovement of the environment for agriculturaldevelopment.

3stimatod Costt Loc For. Tnt*-..-.,... WiIllion......

Credit Compoent .90 8.00- 15.90Institution luld - ---Component 1.43 2.00 3.43Total Finang - - -

Required iQ1 ooIL.k

FLn_ancLf lsns frgiJa zelil Totl& cost

IDA 10.00 10.00 526.15 - 6.15 - 32

Investors 3.18 - 3.18 16

IDA9-.---10.00 19.33 100

Estimated Disbursement:(USSmions)

IDA FT MS n89 [MO Y91 Fn92 F293 F4

Annual 0.56 1.48 3.16 1.6I 1.36 1.20 0.56cumulative 0.56 2.04 5.20 6.88 8.24 9.44 10.00

MADAGASCAR

SECOND AGRICULTURAL C1tEDiT PROJECT

I. PROJECT BACKGROUND

1.01 Since 1980 IDA has been supporting the Agricultural DevelopmentBank of Madagascar (BTM) through an Agricultural Credit Project (cr.1064-MAG),-which was primarily designed to meet the need for smallholder credit.A number of factors (discussed-in Chapter III below) led to a substantialmodification of the design of this project in 1983-5. In early 1984,Government expressed interest in a follow-up project by IDA, to continuewith institution building effort at the BTM combined with an investmentline of credit directed primarily at the renascent entrepreneurs inagriculture and agro-industxy and a report for . follow-up project waaprepared. An IDA appraisal mission comprising Christopher Ward and OusmaneSissoko therefore visited Madagascar in September/October 1985 to appraisethis Second Agricultural Credit Project. Further processing of thisproject was delayed pending clarification of IDA's views regarding anoverall banking sector reform of which BTM vould be a part. It wassubsequently decided that such a reform would be carried out in the contextof the sixth IMF standby credit approved in 1986 and IDA Industrial andTrade Policy adjustment Cr%dit appraised in December 1986. The appraisalwas therefore amended and this appraisal report has been updated as ofJanuary 1987.

11. THE AGRICULTURAL SECTOR

A. Sector Performance

2.01 Sector Outline - Agriculture is Madagascar's dominant economicsector; it employs 852 of the population and accounts for more than 802 ofexport earnings. Production and farming systems vary widely, with manycommodities produced, but production-in value terms is dominated by paddy(302) and beef (16X). A small group of export crops, (coffee, cloves, andvanilla) accounts for about 152 of production but some three-quarters ofmerchandise exports. Industrial crops, notably sugar and cotton,contribute about 72 of agricultural production value. Approximately 802 oftotal production comes from smallholder activity, and small farmers (in the1 to 2 ha. range) are the backbone of Madagascar's agricultural economy.Over half of agricultural production by value Is for subsistence and theshare of subsistence production has been slowly increased over the pastdecade. In contrast to most sub-Saharan African countries, irrigation iswidely practiced in Madagascar, with water control systems in use on about1 million hectares, one third of cultivated land. Overwhelmingly,irrigated land is used to produce rice, Madagascar's main crop. The

-2-

country's rich aud varied agricultural potential offers excellent prospectsfor rais'ing incomes, improvfrg the supp:,r of indu.Frial inputs, and forincreasing foreign exchange earnings, but this potentia.. is far from beingrealized.

2.02 Recent Performance- Performance of the agricultural secto .

been poor since the mid 1970s. In the 1975 78 and 1984-86 periods,production growth was insufficient to k.ey up with population growt andbetween 1979 and 1983, agricultural production did not grow at all. Theproblems have been most serious in (a) the stagnation in rice-and veryserious decrease in edible oils production, and (b) the decline in coffeeexports (402 of merchandise exports) by about a third from peak quantities,..uncoupensated for- by-increased export-of other commodities. One of the fewbright spots in this picture has been Increased cotton production between1983 and 1986 but the serious price decline in world markets has recentlyled to ma:-r pricing and marketing problems.

2.03 Constraints to Growth. The causes of this disappointingperformance are mixed and include structural as well as short term factorsThe main elements have been (a) a major expansion of Government controlover production, processing and marketing functionsa this discouraged theprivate sector to contribute to economic activity, and public sectorenterprises proved generally too weak In management to perform their role,becoming a main drain on the budget; (b) pricing policies for majorproducts favoring urban consumers but discouraging farmers from producingfor tne market; (c) increasingly over-valued exchange rates which, topetherwith a deteriorating balance of payments situation, have led to acuteforeign exchange shortages, and (d) a public investments policy heavilyemphasizing Industrial development which, due to over design, weakmanagement and foreign exchange shortages has had poor results in terms ofproduction. In addition, the economic crisis which hit the country in1979-80 and the subsequent world recession caused further shortages oflocal budgetary funds and foreign currency for sector operations.

2.04 The consequences of these converging trends included the breakdownof essential services to farmers in many rural areas, limited availabilityof production inputs, and inadequate Incentives for Increasing output. Inparticular, input marketing and investment credit in agriculture deelinedmarkedly, also because the nationalized banks increasingly lacked thefinancial resources due to the need to finance parastatal debt.

B. Government Strategy and Obiectives

2.05 Govermentts New Strategy - The crisis in the agricultural sector,especially the decline in marketed output of food and industrialcommodities and shrinking exports, led to a fundamental rethinking ofGovernment strategy in the early 1980s. A new policy framework wasdeveloped which was ormally announced at the April 1983 Consultative Group(CG) Meeting and subsequently confirmed at the April 1986 CG meeting. TheGovernment's objectives are to increase production of foodcrops (above allrice and edible oil crops) In order to reduce Imports; revive production

-3-

and improve the quality of traditional export crops;.and diversifyagricultural exports. Better integration of the agricultural andindustrial sectors is an Important medium-term objective. The strategy toachieve those objoctiv.w recognizes that small and larger farmers are themain agricultural producers and that Govornment policy and investments mustcreate an onvironment which stimulates production by these key economicagent.. Equally important,th.ne new strategy recognizes that the privatesector has a positive role to play in the process of econamic andagricultural development. The practical consequences of this approach arethat the Government now suppoctst (i) moving towards a free market systemas a means of improving produzar incentivesa and (Ui) withdrawing mintsttyservices from activities better porformed by others, whether small farms(e.g. seed production) or commercial companios (e.g. input supply). PublicInvestments iv the sector are to be limited to rehabilitation over themedium term, and systematic efforts made to program and manage them better.

2.06 Imlementation of the Strstegy - Over the past three years andwith Bank Group support, the Government has made steady progress inImplementing this strategy. Perhaps the most significant actions haveinvolved removal of agricultural pricing and marketing controls on rice,meat, and pulses, and Increased farmgate prices for cotton and selectedexport crops. On resource management, the Government has prepared andreviewed with IDA a public investment trogrsm for agriculture, and isestablishing system to update the program annually. Parastatal operationsare now being subjec-ted to profitability tests and restructured to assureself-financing; selected divestitures have been undertaken. The GovernmentIs also reinforcing extension and research while vithdrawing from directproduction and some commercial activities. The agricultural ministries,the Ministry of Agricultural Production and Agrarian Reform (MPARA) and theMinistry of Animal Production and Forestry (MPAEF) have been substantiallyreorganized, and management strengthening programs launched. Largepersonnel reductions have been undertaken to position them to play a moredynamic but lses interventionrst role.

2.07 As a counterpart to the reduction-in Government intervention andthe reduced role of public enterprises in the economy, Government has takenactions to promote development of the private sector in order to reduce thebias which merged during the years of economic dirigisme. The steps takenso far include the passage of a new Investment Code in mid-1985 which givessubstantial protection, both legal and fiscal, to private businesses;gradual removal of price controls on both prfimary and manufactured goods;easier access to credit and foreign exchange, not only under regularallocation system but under Governmnt-promoted projects. such as theCotton Development Project (which provides investment funds for cottonfarmers, both smallholders and estate farmers alike); and the eliminationof state marketing monopolies in major crops, including paddy/rice, beefand beans. Further measures envisaged include a program to fosterdevelopment of oammercial marketing circuits; the elimination of pricediscrimination against the private sector In the marketing and processing

-4-

of export crops; and the handover of agricultural input and veterinaryproducts Import and distribution to private firms. Finally, under theAgricultural Sector Adjustment Credit (discussed below), all imports are tobe made under an open licensing and allocation system that will allow newentrepreneurs to enter the market at will. These measures, taken together,add up to the first phase of a-solid adjustment package which willhopefully revive business confidence and promote private sector Investmentin the development of agriculture and its downstream activities.

C. Bink GrOUP SUPDort

2.08 Relation to Government Stratelg - lank Group support foragricultural sector development in Madagascar has been comprehensive,including project financing, sector work, institutional develcpmentsupport, sad an intensive dialogue with the Government on key policyissues. The Bank Group has also played an important role in helping theGovernment to coordinate the activities of external financing agencies inagriculture by encouraging co-financing arrangements and through thevehicle of the Consultative Group (CG) meetings.

2.09 Bank Support to Agriculture as of December 1986 - Agriculturallending in Madagascar accounts for about $224 million for 15 operationsover a 13-year period, out of a total Bank Group portfolio of about $640million. Ten agricultural projects are currently under implementation,including an-IFAD project appraised and supervised by Bank staff. BankGroup lending has been primarily concentrated on priority commodities, suchas rice, livestock, and cotton and has sought to address the criticalsector issues sketched above. Since 1983, lending has become more directlyprogram and policy oriented.

2.10 Experience with Bank Lending - Project performance has been mixed,with virtually all projects affected both by the combination of policy andinstitutional problems affecting the agricultural sector broadly and by thedirect repercussions of the recent economic crisis. The principalconstraints to project implementation have been:

(a) the shortage of local funds and foreign exchange created byMadagascar's economic and financial situation.

(b) personnel and managerial probles, above all linked toinadequate training, low pay and difficult working conditions.Overstaffing is a frequent problem and reduces efficiency andmotivation. Complicated bureaucratic procedures and rigidaccounting systems have adversely affected several projects.

(c) weak formulation of subsector programs and priorities soinvestments do not reflect strategic objectives for the sectorand there is mch overlap and dissipation of effort. Problemsare amplified by difficulties in aid coordination.

(d) pricing and marketing policies which, until the turnaround insector policy in 1983, were incompatible with objectives forincreased production and parastatal financial viability.

2.11 The Bank Group has responded to specific project issues, as wellas to the sectoralleconomy-wide problems outlined in para 2.10, throughintensive supervision of on-going operations, sector work, and preparationand appraisal of a new generation of operations. It has reviewed carefullyand taken into account the experience of projects which have beencompleted. It has adapted new and on-going projects to resourceconstraints by providing fast-disbursing, balance-of-payments typeassistance, through existing and new projects. It has addressedinstitutional and policy issues through new operations. It is alsosupporting the formulation of subsector strategies through sector work and-consultant executed studiesj(e.g. livestock exports, oil. crops).

2.12 The lead operation in addressing policy issues is the firstAgriculture Sector Adjustment Credit approved in May 1986. This operationprovides a credit of SDR 56.5 million for needed imports of agriculturalinputs, veterinary products and animal protection materials, tractors andtransport equipment, and incentive goods for rural areas. The adjustmentprogram to which the credit is tied comprises the following main elements:

actions to improve market efficiency through continuedliberalization and development of the private sector;

- strengthening producer incentives by relying increasingly onmarket forces, and in parallel making the Government'sremaining intervention in pricing more efficient;

- setting up an effective rice management program ending theGovernment's marketing in the two zones which produce asubstantial rice surplus;

rationalizing public spending, notably through better choiceof agricultural investment; and

- preparing the next phase of the agricultural reform program.

2.13 The key component in this operation is the rice security strategywhich is designed to provide incentives for increased domestic production,thus reducing import requirements and at the same time to establish a riceintervention stock to stabilise prices during the scarcity period. Anotherimportant component is to increase coffee farmgate prices so as to expandcoffee production, Madagascar's principal export.

2.14 The Second Agricultural Institutions Development Project, alsoapproved in May 1986, is designed to improve the efficiency of publicsector institutions and follows from the successful first phase projectwhich provided institution building support notably to the agricultureministry (MPARA) and the livestock ministry (MPAEF). The second project

provides technical assistance, short torm consultants, and training andstudy tours for the ministries Involved In agriculture as well as for theresearch organisation (FOFIPA). Specific objectives are to improveresource management, strengthen policy analysis capability, and developmanagement capacity for key Government services - extension, research, datacollection and analysis, and market infomation. In addition, specificstudies will contribute to policy analysis and preparation of the -nex tslice of the-reform program.

2.15. The proposed Agricultural Credit Project i8 designed to addressthe third key element in redressing Madagascar's agricultural production,.namely to help private entrepreneurs invest in the agriculture sector. Itwill also provide funds to support further iAstitutional strengthening of-BTM and complement efforts to support a reform of the banking sector underthe forthcoming Industry-and Trade Policy Adjustment Credit-which tsscheduled for Board considetation in the current fiscal year (paras. 3.22and 3.12).

III. -THE BANKING SECTOR, BTM AIRT AGRICULTRAL CREDITPROJECT

A. Banking Sector Structure

3.01 Reortanization of the Bankins Sector - Before 1975, the bakingsector in Madagascar consisted of four commrcial banks (largoly foreignowned or affiliated to foreign financial institutions), plus a nationaldevelopment bank, the Banque Nationale Mblgach. de Dmesloppement (BmN), andthe Central Bank. The Government nationalized the fcur commercial banks in1975 and, in 1977 reorganized the banking sector into three government-owned banks, each of which vas to be responsible for a sector of theeconomy: the National Bank for Rural Development (BTM) for agriculture;the Industrial Development Bank (BNI) for Industry, and the Commercial Bank(BFV) for commerce and trade.

3.02 Manatement - The three banks are classed as parastatalsresponsible to the NMinstry of Finance. Although the establishinglegislation called for a broad Policy Council and separate Boards ofDirectors for each Bank, until November 1986 separate Boards were notestablished and all three banks were governed by a single Board. Inconnection with the sixth 1KV stand-by arrangements, separate Boards wereappointed for each of the commercial banks. Accordingly, BTM's Board wasstaffed with 12 members including 5 professional bankers and 2 privatesector representatives. The Boards are chaired by the Minister of Finance.

3.03 The Three Banks - Despite their sectoral specialization, the threebanks are in competition for collecting deposits and also, to some extent,for extending credit to Individuals or enterprises outside their sector ofspecialization. Purthermore, because of resource scarcity, the three banksmust often pool resources in consortium loans to meet corporate financingneeds. The relative Importance of the three banks Is shown in thefollowing tables

-7-

As of December 31, 1985(FMG billion)

BTM BNI BFV Total

Capital Stock 3 4.5 3 10.5Total Assets 141 165 120 426Loan Portfolio 111 113 87 311of which:Short Term (up to 2 years) 98 103 76 277Medium Tenm (2-5 years)- 10 3 11 24Long Term (over 5 years) 3 7 -- 10

Profits - 0.15 0.62 0.42 1.19

Number of staff (no) 1,558 1,198 1,270 4,026Of which professionals (no) 79 93 129 301Number of Branches (no) 44 14 -17 75

3.04 The Central Bank (BCRDM) - Following the decision to withdraw fromthe franc area the Government created the BCRDM on June 12, 1973 to replacethe Institut d'Emission Malgache (ISM), which had been jointly owned byFrance and Madagascar. The Bsanque Centrale de la Republique de Madagascar(BCRDM) closed the account with the French Treasury, in which the IEM hadbeen required to deposit all its international reserves, and took over themanagement of Madagascar's foreign assets. BCRDM is responsible forregulating all financial institutions in the country and for establishing andadministering national monetary and credit policies, including monitoringcredit distribution. It also sets credi. and rediscount ceilings for thebanks, and minimum liquidity and solvency ratios. At present there is ampleroom to improve the effectiveness of controls over banks. Under the creditproposed in this report the Government would adopt rules and proceduressatisfactory to IDA for bank supervision by December 31, 1988.

3.05 The Bankers' Professional Association - (Association Professionnelledes Banques or APB) is the Bankers' trade association. Its charter gives ita double role. It is to represent the interesta of the banking sector but atthe same time to play an advisory role to the Minister of Finance, to whom itreports. The APB began operations in June 1985, with a staff of 5professionals drawn from public institutions, i.e., a Secretary General whois a professional banker, an industrial expert and three officers secondedfrom BFV, BNI and BTS. The first major task of the Association's staff hasbeen to begin work on a case by case review of non-performing parastatal debtwhich is to lead to action programs for financial rehabilitation and recoveryof the debt.

B. Credit Policy

3.06 Obiective and Reaulatorv Instruments - At present the main objectiveof Madagascar's credit policy Is to limit credit expansion to a level-consistent with Internal and external stability, while increasing the shareof credit for production and for export. To meet this objective, the BCRDMrelies on a quantitative control consisting of an overall target on creditgrowth set in line with IMF recommendations. The credit growth is controlled

-8-.=

through the credit ceilings which are revised quarterly for each individualbank on the basis of Its liquidity position and Its expected needs. TheBCRDM sets a global ceiling (plafond global) and subeeilings on specificcategories of credit (encadrement du credit). There are also qualitativecontrols including prior authorization by the Central Bank for all creditextensions and renewals above FMH 100 million and the determination-ofinterest rates for Central Bank rediscounting. The Government is currentlyreviewing these Instruments with a view towards adopting a comprehensive andcoherent credit policy. Its work on the overall credit policy started a fewyears ago, is to be completed under the second review of the Sixth IMF Stand-by to be carried out in the next several months.

3.07 Interest Rates - The Central Bank has the authority to set therediscount rate as well as maximum and minimum interest rates on bankcredits. Interest rates which remained constant between 1974 and 1981, wereincreased in June 1982 and again In February 1983. In accordance with theDMF recommendations, Central Bank controls on interest rate structure weresiMplified in April 1985 and all interest rates except the Central Bank'srediscount rates and the deposit rate for 6-12 months, were liberalized. Atthe same time, the Central Bank lowered its rediscount rate by 1.52 to 11.5Z(the standard rate). In line with this, the three banks have reduced theirInterest rates to levels ranging from 13.52 to 212 p.a. on short termcredits; and to 14.52 to 15.52 for medium-term loans. The rate of inflationin Madagascar, which was 101 in 1984-85, accelerated in 1986 (reaching17.52). Effective January 1, 1987, the Central Bank raised its preferentialrediscount rate (for advances on export bills and on agricultural products)to 11.75Z p.a. and the standard rate (for all other credits) to 151 p.a.Accordingly, BTM raised its interest rates to 15%-242 p.a. on short termcredits and to 18Z-192 p.a. for medium term loans. For long term lending, anadditional 0.252 spread is charged. On deposits, interest rates varydepending on duration from 1.52 to 32 for demand deposits, to 20.50X p.a. forsix-year term deposits.

3.08 Agricultural Credit Policy. Traditionally, banks in Madagascardirected the bulk of their lending to the non-agricultural sectors, andlimited agricultural lending to large farms and project authoritiesimplementing specific agricultural development programs. The first coherentattempt at formulating an agricultural credit policy was made during the 1977banking sector reform, when the expansion of seasonal and medium-termsmallholder lending was made one of the major objectives for the newlyestablished BTM. This policy failed for sever-1 reasons. First, theGovernment's agricultural pricing policies were not conducive to making thesector profitable and made lending to the sector a risky proposition. Second, smallholder lending proved costly and the attempt to involve localgovernments (fokontany) in the selection of beneficiaries and therecuperation of loans, quickly led to an increase in doubtful debts. Third,especially since 1982, forced lending to parastatals reduced bank fundingavailable to the private sector. Finally, the increasing scarcity of foreignexchange has severely limited the availability of agricultural inputs,thereby restricting agricultural lending.

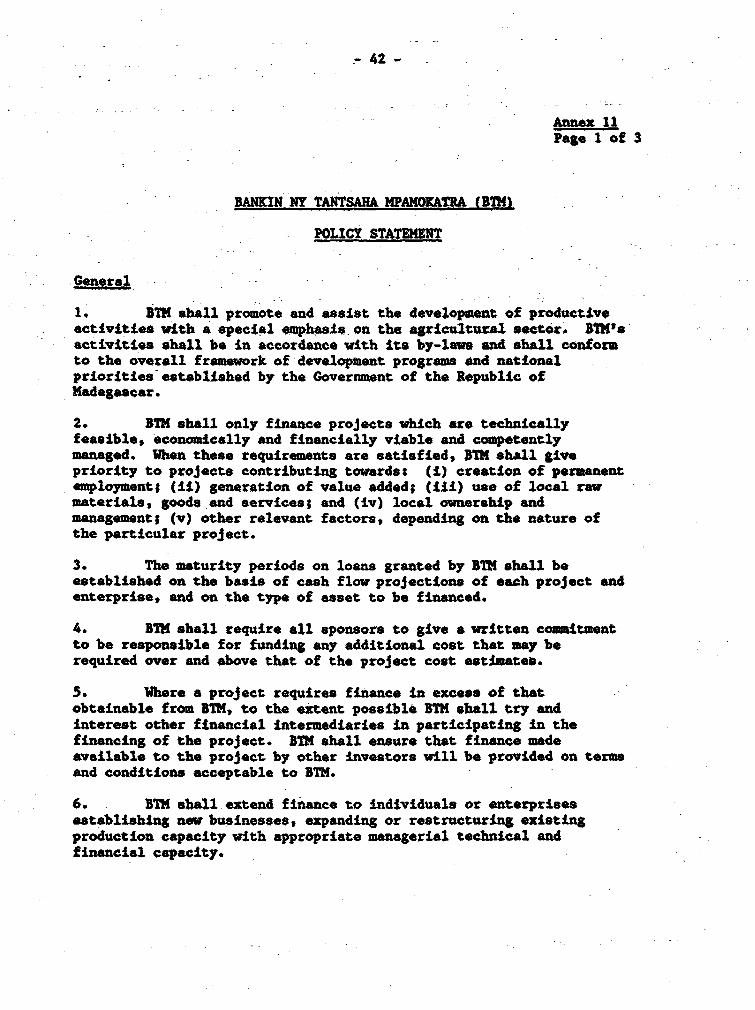

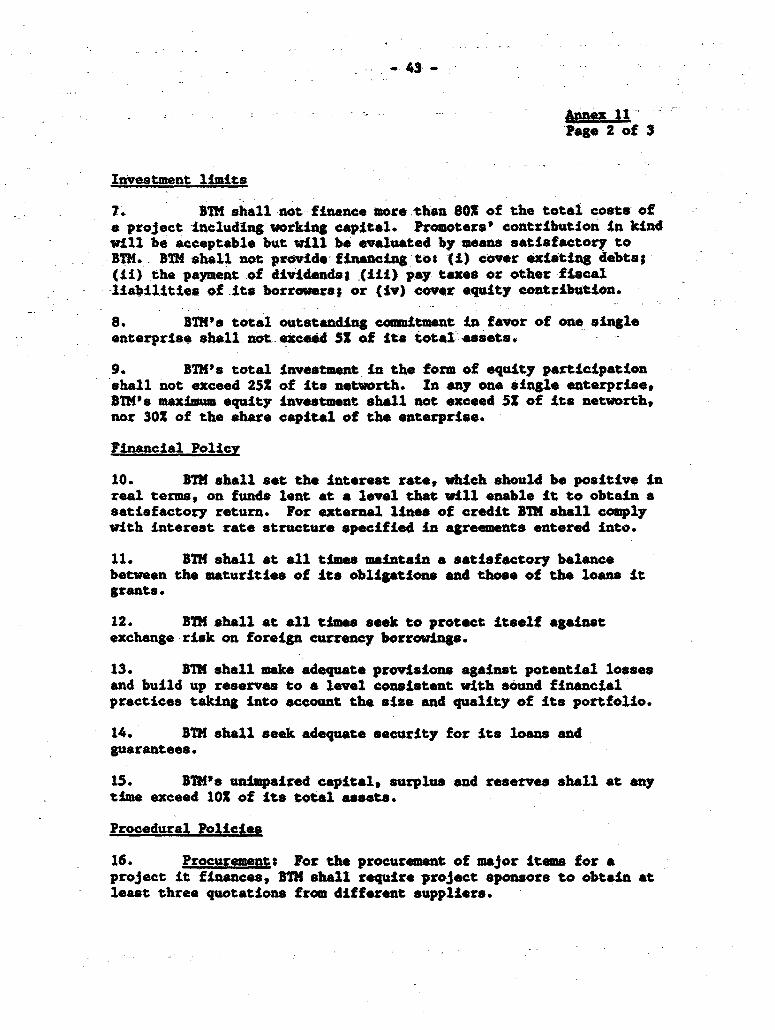

3.09 The results have been that agricultural lending has remainedextremely limited and the great majority of Malagasy farmers have no accessto iuistitutional credit. Several of the above factors are now beingaddresseds parastatal lending is being cut sharply; foreign exchangeavailability should increase following adjusted macro-economic policies andincreased foreign borrowing once banking sector reform has put the banks on asounder financing footing; an,' changed agricultural pricing policies shouldmake lending to the sector more remunerative. However, the main long-ternIssue is that smallholder lending will remain costly for institutional banks.and in order to overcome this the growth of other lending agencies (such asrural savings and loans institutions) will need to-be encouraged. A study toformulate a long-term agricultural credit policy and system, which wouldamong others address these issues, is included in the proposed Credit (para5.02). In its new Policy Statement BTM is committed to increase its newlending to agriculture and not to make any new loans to public sectorenterprises in financial difficulties. The objective of this policy is tochange BTMI's portfolio structure so that agricultural loans will represent amajority of BTM's portfolio. Progress towards this objective will bereviewed annually with IDA.

C. Performance

3.10 The Banking Sector Crisis - Following nationalization, the bankingsector in Madagascar lived through the years of extreme economic dirigismeand statism that characterized the 1977-82 period. Portfolios graduallyaccumulated parastatal "paper' but the banks retained a commercial approachthat allowed their banking decisions to remain for the most part independent.For example, the BTM successfully resisted Government pressures to lend tosmallholders at a time when the financial profitability of smallholderagriculture was nsufficient to generate an adequate recovery rate. Fromabout 1982 however the Government, constrained by ceilings on public sectorspending, was no longer able to offer financial support to the parastatalsector, much of which was running heavy losses, and the banking sector wasrequired by Government to allow parastatals to run up short term borrowings.These quickly occupied a large share of the banks' portfolios, and withdeteriorating parastatal performance, the recuperation of a major part ofthese loans became doubtful. This produced a banking sector crisis of majorproportions. The BNI auditors for exasmple considered over half of the valueof BNI's portfolio at December 1983 to be doubtful and more recent reportsare that 80Z of total loans of the banks are non-performing in the sense thatinterest is not being paid. The BTM situation (described in detail in para3.20) is somewhat better than that of the BNI but nonetheless very difficult.

3.11 BTM, ahead of the other two banks has its portfolio reviewed by anindependent, Internationally recruited auditor since 1983 and has agreed to:(i) a maximum transfer to bad debts reserve each year consistent withretaining depositor confidence and transfer of net profit to reserves (i.e.no distribution); (ii) an overhaul of bank management procedures to improvenew lending (e.g. BTM action plan, pars. 3.22; (iII) a review of par"statal

-10-

borrowers, starting with the worst. cases, in-order to work out means ofgenerating net repayments to-the banking sector; and (iv) Government'swillingness to consider structural reform of the bankin8 sector, includingdespecialisation of the banks to allow competition, and creation of separateboards for each bank, with the objective o ,romoting autonomous decision-making. Thus a decree establishing an inc._&pendent Board of Directors foreach bank was signed by the,President-on August 279 1986. -While Governmentand the banks have acted to defuse and begin to solve the crisis, the factremains that the Banks are fully Government-owned and a repeat of similarpressure on the Banks cannot a-priori be excluded. However, Government'sacceptance of strict budget and bank debt ceilings under its agreement withIMP-as- well as the creation of Boards of Directors for each bank, shoulddiminish such risks.

3.12 Bankint Sector Reform. Until recently the receptiveness of theGovernment to proposals for reform In the banking sector was limited.Although a beginning is being made under the sixth IMF stand-by, moresignificant reforms are necessary in respect to the three state commercialbanks. Tho Government has formulated a preliminary program of reforms of thebanking sector which has been reviewed by IDA and found satisfactory. A keyfeature of this program is the adoption, by December 31, 1988, of rules andprocedures satisfactory to IDA for the Central Bank's supervision ofcommercial banks. Furthermore, the Government undertook to maintain positiveinterest rates In real terms.

3.13 The current excess liquidity of all three banks, as a result oftight credit ceiling enforcement of the Central Bank, has affected negativelythe profitability of the banks. As part of the program mentioned in theabove paragraph, to alleviate this situation now and in the future, thecreation of monetary instruments such as special issues of short-teamtreasury bills is being investigated. However, due to the foreign exchangeshortage the banks have an increasing need for external financing. Finally,the program includes a study to address the followings (a) the capacity ofexisting financial Institutions to respond fully to the needs of the sector;(b) the consideration to allow additional financial Institutions to entertho sector, or to introduce private capital -- local andlor foreign -- intothe existing three banks once the financial restructuring is completed; (c)the legal framework In which the banks operate, including the possibility ofcalling guarantees, foreclosing on companies, and selling off pledged assets;(d) the adequacy of credit ceilings, rediscounting facilities and creditsupply; (e) the improvement of financial services to include exportfinancing, leasing, and housing finance; (f) mobilization of savings; and(g) degree of application of the 'liberalized' interest rate structure.

-11-

D. The National Bank for Rural Develoument - BET

3.14 Structure BTM is a8 autonomous parastatal with a share capital ofPMG 2 billion (US$2.66 million), 902 owned by the Government and 102 by theContral Bank. Its legal status is that of. "socialist enterprise"(Intreprise Sodaliste) regulated by the Charter on Socialist Enterprises.This status in theory involves wvrker participation on the board, profitsharing, etc. In practice W is run by its managment, reporting to theBoard and the provisIons of the charter have never been applied. Thearticles of thb company set Its objectives as promotion of rural developmentand the moblllsatlon of national savings.

3.15 Management - NTH's Goneral Manager is appointed by decree of thePrim. Minister and assisted by a deputy and experienced professionals. BTh'sanagement is competent. The General MaNager is responsible for theadministrative, financial, technical and commercial performance of the bankand is accountable to the Board (para 3.02). He also chairs the CreditCommittee, an internal body which examines loan requests and makesrecomuendations to the Board. All BTH loan requests except those to smallfarmers are reviewed by tho Credit Committee. The Credit Committee comprisesdirectors of the four main operational departments. It meets regularly twicea week.

3.16 Ortanisation - Of the three banks, BTM has by far the largest numberof branches. Its 44 branches and 22 field offices - which are organized IntofLve geographical groups - are distributed througbout the country with someconcentration In the major agricultural and population areas of the CentralPlateau and the last Cost. The S regional *groups" - in Toliary,Fiarananteos, Hohajonga, Toamasina and Antsiransna, exercise overallmnagement for the branches and field offices in their areas Itshoadquarters at Antanaarivo comprises the General Management and 8-departments: Internal Audit; Administration and Personnel; Loan Supervision;Operations and Credit; Accounting; Treasury and External Relations; Planningand Rural Development; and Tana Branch Operations. Each department comprises2-4 divisions which are headed by a Division Chief (see chart). TheOperations and Credit department ad the Planning and Rural Developmentdepartment have had the main rcsponsibility for mplementing the firstprojoct and will continue to be responsible for execution of the proposedproject. Theso departments are responslble for all credit operationslncluding appraisal, monitoring and recovery and for rural developmentactivities respectively. The headquarters and the Gzoups assumadministrative and control responslblllties, while the Branches and field

offices perform operational activities. The difference between the lattertwo is largely a function of their volume of business. The field office isthe smallest unit. It performs all banking activities but is above allresponsible for the rural credit program -- FMR. The branch normally Includesfour activities: loans, teller transactions, accounting, and marketing.BITM's organization, which reflects its dual role as a development and acommercial bank, appears to be appropriate. However, there is a need tostrengthen BTMHs technical capabilities for assisting sub-borrowers inpreparing, appraising, supervising and promoting development projects (paras.5.06-5.07).

3.17 Staffini - Current staffing levels which represent an 112 increaseover 1981 Is adequate. Overall, staff quality Is good, with the majority ofthe professionals having a solid academic background. In order to iprovefurther the quality of its staff, BTH provides permanent on-the-job traninagand training seinnars organized by the training specialist. It also sendsits staff for external training in project evaluation and financialmanagement provided by the Centre d'Etudes Financieres Economiques etBancaires (CEFEB) in France. Technical assistance and other institutionbuilding support was provided under the ongoing BTM project and will becontinued and extended under the proposed project. A personnel evaluationexercise with IDA-financed consultant started in June 1986.

Operations

3.18 Loan Portfolio and Provisions - BTM's loan portfolio as ofDecember 1985 amounted to FMG 111 billion net of reserves and isdistributed as followss agriculture 36Z, industry and comerce 602, andindividual lomas 42. Total loans to Parastatals amounted to FMG 33 billion(302). Short term loans amounted to GHO 98 billion or 88% of theportfolio. Seasonal loans for agricultural production stood at FMG 3billion (32) while those for crop marketing were FMG 33 billion (302). FMG1.6 billion or 1.42 of total portfolio were accounted for by smallholderlending. Medium and long term loans were FMG 13 billion (122). Non-performing loans and guarantees in favor of clients were estimated by theauditors at FMG 78 billion in December 1985, Including ?MG 44 billionclassified as high risks, of which over 502 comprised public enterprises inprecarious financial condition. As of December 31, 1985 only 82 (1MG 2.5billion) of BTM*s loans to Public Enterprises were covered by Governmentguarantee. Provisions made for doubtful loans and guarantees totalled FMG22 billion at the end of 1985 and BTM intends to increase provisionsagainst bad risks to FMG 7 billion per year over the next three years inorder to further cover non-performing loans extended to the publicenterprises. In addition, prediagnost.ic studies for the rehabilitation of16 selected public enterprises (accounting for about 40 percent ofoutstanding bank credit to public enterprises) were completed as part ofthe sixth IMF stand-by arrangement. Nine of these enterprises are BTM'sclients and when their rehabilitation Is completed, it is expected thatthey will repay part of their loans hitherto classified as irrecoverable byBTM's auditor.

-13-

3.19 Resources. BTM depends largely on deposits for its funds. As ofDecember 31, 1985 total deposits accounted for 73 X of total liabilities.Deposits went up rapidly in 1980-1985, from FMG 43 billion to FMG 103billion as BTM used a strategic expansion of its network to tap furtherdeposits. Demand deposits and certificates of deposits amounted to FMG 77billion, i.e. 752 of-aggregate-deposits,-while term deposits amounted toFlG 26 billion (25%). The share of Individuals and private companies intotal deposits is 791 and that of public entities 21X. BTM's second sourceof funds is its equity which accounts for 10% of total balance sheet as ofDecember 31, 1985. BTM's final- source of funds has been a number ofexternal lines of credit which have been transferred as equity funds or-aslong term-loans. Disbursements on these funds totalled FMG 2,311 million.as of December 31, 1985 which came principally from IDA (the FirstAgricultural credit project)#, Cooperation.Suisse, CCCE and the AfricanDevelopment Bank. They form only 21 of B3H's total liabilities, however.In view of the foreign exchange shortage in the country, BTM has anincreasing need for external financing which should enable it to expand itsdevelopment activities. The proposed credit would contribute to alleviatethis constraint. The proceeds of the IDA credit would be passed by theGovernment to BTM as Government equity contribution in view of theilliquidity of BTN's portfolio and the current difficulty for theGovernment to make any cash transfusion needed to strengthen BTM's equitybase.

Financial Situation

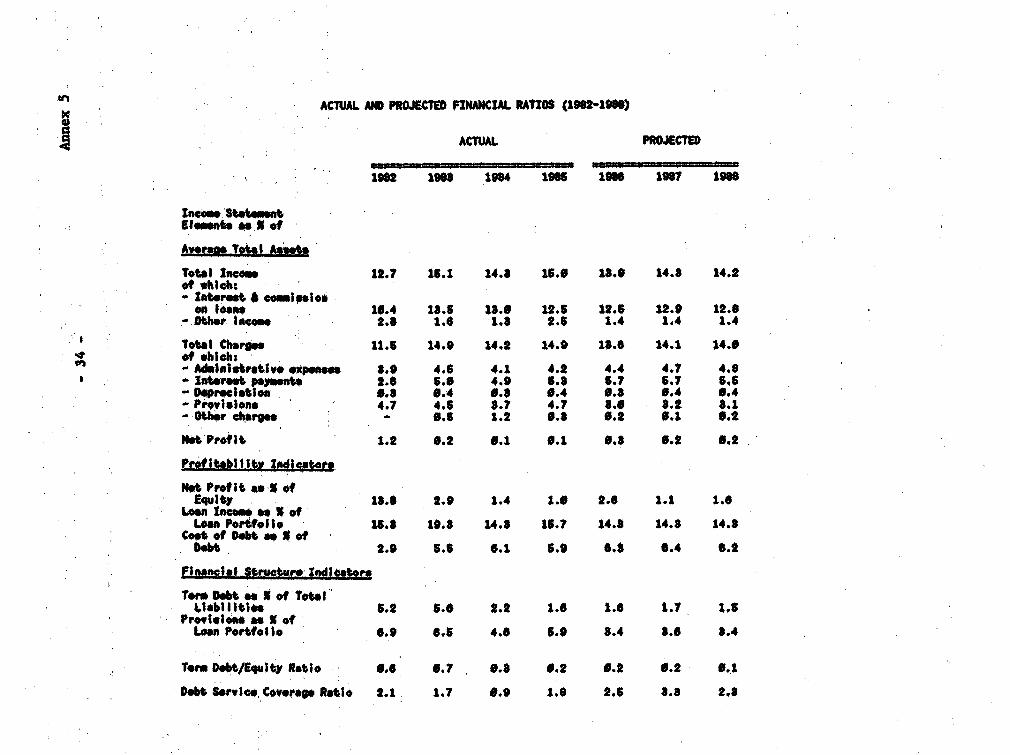

3.20 Annex 3 shows BT3's balance sheets, Annex 4 the income statementsand Annex 5 the basic financial ratios. BTM's balance sheets for the 1983-85 period are summarixed in the following table.

1983 1984 1985(7MG million)

AssetsCurrent Assets (cash, near-cash..) 28,183 1,483 26,054

Loan Portfolio (net of reserves) 71,180 104,048 111,249Fixed Assets 2.541 2.889 3,371Total 101,859 128,420 140,674

LiabilitiesCurrent Liabilities 87,467 114,023 124,042(of which deposits) (65,136) (88,845) (103,O94)Term Borrowings 5,371 2,841 2,309Equity 8.661 11.556 14.323

Total 101,859 128,420 140,674

While in 1984 both B3M's deposits and loans experienced a record expansion,BTM adopted in 1985 a more prudent approach in loan approval where loanportfolio increased only 72. Most of this took the form of increasedcredit to the private sector.

-14-

3.21 RIM's financial situation is shaky. (1) Its net earnings aftertax are low (return on equity in 1985 was I); (ii) Its equity base Issmall (equity to total liabilities wa 10% at December 1985); aud (iiI) thequality of its portfolio is poor, with the auditors classifying 522 ofBTM's total commitments about P1G 150 billion in 1985 as doubtful (FM 78billi3n). The auditors recommended further provisions of nMG 11.5 billionbeyond what BTI could provido and qualified the audit report. B1M's mainproblem is its lack of adequate equity or long term low-cost funding. Itsresources are basically ahort term, which makes epausion of developmentbusiness virtually impossible for a prudent bank. The reasons for thisdifficult situation are: (i) Govrnment pressure in the 1981-83 period tofinance parastatsl losses through the banks whon it ws no longer possiblethrough the budget, which resulted in a sizeable amount of parastattldebts among BTM's high risk loans (about FMG 25 billion out-of the MEG 44-billion); (ii) the Government's continued Insistence on taxing andcollecting dividends on what are effectively non-existent profits whichresulted in BTH paying about FMG 13 billion to the Government sincenationalisation; this money would have better been consolidated toreinforce the capital base and provid some funds for development lendingactivities. The proposed lending operation would correct this.

3.22 The Action Plan. In the face of this difficult situation, 3T1 andthe Government, have worked out and are plementing an Action Plan, that,when completed, should put BT3 back in a sound financial position. In thiscontext BTM has adopted a recovery program, which basically aims at makingmaximsm bad debts provisions to cover 8T3's doubtful debts over a five-yearperiod (1984-88). The action plan includes (i) an lnventory of substantialnon-performing loans and assessment of the risk on these lomans this phasehas been completed each year 1983 through 1985, the 1986 inventory is Inprogress; (ii) the establishment of a management information system aimedat better portfolio management and improved monitoring of currenttransactions; this phase is under implementationl and (Lit) a rapid growthof reserves against bad debts; this Is also betig implemented and over 1984and 1985 BTM's reserve against bad dobts has increased substantially,totalling FMG 22 billion or 50% of the high risk portfolio by the end 1985.In addition to the foregoing further actions vould be required from BTE andthe Government to further improve BTMs' financial condition. Such actions,which would constitute a part of the proposed project, include thefollowing, and assurances on this wero obtained at negotiations:

(a) acceptance by Government that BTM wmould not pay any dividendsuntil 1002 of its bad debts as determined by the auditors as of December31, 1985 are covered by reserves, and, continue with satisfactoryprovisions thereafter;

(b) payment to BT1 by Government to honor its past guarantees onIrrecoverable loans to parastatals, totalling PUG 2.5 billion, not laterthan June 30, 1987. A first payment has been made by the Government onschedule in September 1986, and the full payment of the guarantees is acondition of effectiveness;

-15-

(c) assurances oy RTH that It would (i) continue to retain anInternational firm of auditors; (ii) withhold taxes on Interest to holdersof Cer,ificates of Deposit (CDs) directly on CD holders' accounts Insteadof paying back to the Government these taxes out,of its own income - thiswas agreed at negotiations; (iII) establish a syqtem of loan portfolioanalysis that would include aging of receivables effective September.30S,1987; and (iv) improve loan collection so as to achieve for loans excludingthose that BTh's auditor classified as lrrecoverable, a recovery rate of801 by end of 1988 and 952 by end of 1989 and thereafter for interests andprincipal repayments. BTM and IDA would discuss each year measures by BThto attain this goal. Under the action plan, Irrecoverable loans will befully'covered by BTM making adequate bad -debt provisions. Duringnegotiations BTM agreed to make provisions for bad debt of at least FMG 7billion per year, adequate to cover over tae.next three years the fullamount of irrecoverable loans determined by auditors at end 1985. Inaddition BTM undertook to reinforce its internal organization to emphasizeloan recovery. A Loan Recovery Division has been created to Implement amore stringent recovery policy and an experienced lawyer appointed as chiefof its Legal Division.

3.23 The Projections - Financial projections have been prepared on theassumption that the above lmprovements will be carried out. Details aregiven in annexes 3 and 4. Despite the strength of its project pipeline(para 4.05), BTM plans to maintain a prudent approach to approvals of newloans. Therefore, projections assume a cautious 91 annual increase Inloan portfolio from FMG 111 billion in 1985 to FMG 142 billion in 1988.The growth of loan income was estimated to be about 5% p.a. and takes intoaccount the overall 1.51 decrease In BTM's lending rates in April 1985(par. 3.07). Thus loan income Is expected to grow from 1MG 17 billion toF1M0 20 billion and represent on average 14.31 of year end loan portfolioduring the 1985-1988 period. Provisions for bad debts were estimated torange between 3.41 to 3.61 of year ed loan portfolio given BTM's decisionto build up substantial provisions. Net profits are expected to rangebetween 0.3-0.2Z of total assets in 1986-through 1988. BTE's financialcondition is projected to improve gradually Vor the 1986-88 period. ItsEquitylAssets ratio would exceed 111 as BTN's equity base would beconstantly reinforced with retained earnings and the proceeds of theproposed IDA credit which would be transferred to BTN as Government equitycontribution. The Debt Service Coverage Ratio would also Improvesignificantly from the current insufficient level of 1.8 to 2.3 in 1988.

E. The History of the First Agricultural Credit Proiect (Cr. 1064-HAG)

Proiect Oblectives and Desin

3.24 In December 1977, the Government of Madagascar requested that IDAsupport a line of credit to smallholders through the BTM. The resultingproject (Cr. 1064-HAG) was appraised in 1980, and the credit becameeffective in August 1981. The objectives of the project vere: a) to

-16-

support the Goverr_ent's policy to extend credit for smaliholderagricultural development, with BTX as the principal intermediary, and (b)to strengthon BTM's managerial and financial capability as a ruraldevelopment bank. Potential beneficiaries of the project were to be 1.5million smallholder familis. The mait project components were:

(a) A smallholder Rural C-.dit Program (FMR- Financement du Monde Rural),initiated- by- WI's predecessor, the BN, to provide loans to smallholderswith under 5 hectares. The basic principle of the program was that loanswere extended to Individuals using local government institutions,specifically the fokontany, as the Intermediary;

(b) Credit for experimental projects. including some based. on collectivefarming;

-() Staff training for BTM in financial, managerial, and4compu:erdisciplines;

(d) Logistical support to BTM, including mobile banks; and

(e) Development of a computerised information system.

3.25 Total project costs were estimated at US$14.2 million with an IDAcredit of SDR 8.70 million (US$11.5 million equivalent), or 81 S of totalcosts. The project commitment period was originally set at three years(October 1980-September 1983).

Implementation Lxnerience

3.26 The project was clearly set in the context of the Government'scredit and rural development policies of the late 1970's (para 3.08).Their failure has thus markedly affected the project's history. In thelate 1970's, the Government sought to shift the emphasis squarely to smallfarmer lendiag, and to accomplish this by relying heavily on the fledglinglocal government institutions, which were to play a heavy role both inadministering loans and In guaranteeing repsyment. Loans to medium andlarge farmers and to private enterprises were to a large extent ruled out.This would have Implied a major shift In BTH's portfolio and policies, assmallholder lending had been limited up to that time. In practice, BTM'asmallbolder lending did not materialise as planned. Essentially, thePokonolona system could not fulfill its role and early experience withlending resulted in high arrears. BTf's strict recovery policies calledfor stopping lending in areas where recovery was poor, and by 1983, onlyabout one-third of Fokontanys remained eligible (open) for credit. Due toBTE's prudent policy of limiting its exposure in smallholder credit,however, actual smallholder lending was so small that IDA and other fundswere not used for this purpose. As a result, disbursements from the IDAcredit for this component have been minimal (SDR 142,000 to date, againstan allocation of SDR 7.5 million). 8mallholder lending remains a priorityobjective but the realities of lending (high costs, poor incontives) haverestricted active programs to areas where major development program areunderway, a number of them supported by IDA and IFAD (Lac Alaotra, CentralRighlands).

-17-

3.27 In the face of these difficulties, the project was largelyredesigned. Since 1982, the Government has moved away from insistence onsmall farmer lending and has permitted increased lending to commercialfarmers, a move fully supported by IDA. As, however, the countryexperienced increased foreign exchange scarcities, GoverDment requestedthat funds from the BTH credit be disbursed to finance imports ofagricultural inputs and equipment in ordor to ease the severe bottlenecksof these items.

3.28 Towards this end, the credit agreement has been amended threetimes. The first amendment was made in July 1982 which permitted BTH to

--import fertilisers. In October 1983, a further amendment enabledadditional Imports of fertilizer and a test operation for the import oftractorsr equipment and spare parts. A third amendment in April 1985,reallocated the balance of funds to import of inputs, tractors, trucks, andminor equipment and supplies for the agriculture sector. The amendmentsprovided that local funds generated from Import sales would be reserved forthe original purpose of financing farm credit, on the assumption that thecredit program would pick up again as agricultural performance improved.

3.29 The experience of these mports has served, during a period oftransition in Madagascar from extreme dirigisme toward a free marketapproach, to demonstrate the interest and capacity of the commercialimporter and distributor in taking over from Government agencies input andequipment import and distribution. It has also demonstrated that, despiteconstraints of capital, there is a growing market in Madagascar for theseImports. Lessons from this experience have been incorporated in the importand distribution prograt for the Agricultural Sector Adjustment Credit(para. 2.12). As a result of these changes the availability of inputs hasimproved and the demand from smallholders for credit has begun to pick up.Reflows have been allocated to finance Incremental samllholder and otherfarm credit in equal proportions. BTM is preparing a pilot smallholdercredit project which is designed to establish a field-oriented managementand supervision system. Modest project funding has been reserved under theproposed Credit to fund this pilot.

3.30 The institution building comp-onents of the credit assumed an evenlarger importance with the deterioration of BTM's financial position. Theyhave, on the whole, been successfully implemented. The internationalauditors, hired at IDA's Insistence, have performed very well, not only inthe auditing area, but also with advice on BIH's financial strategy,management improvements, and personnel management. Two technicalassistants have since 1983 been providing good support to staff training,the computerised information system is being installed and additionalcomputer equipment is being procured. Three mobile banks were procured asa test, but their operation has not justified further purchases. Thecredit closing date, initially June 30,1984 was extended to December 31,1986 with 83% of t e Credit disbursed.

Conclusions

3.31 Project implementation has shown mixed resulta. While theinstitutiopil strengthening of BTM has to a larg,e extent been attained, thesmallholder credit component has been very sub.stantially modified torespond to greatly altered conditions In the agriculture sector. Thesolution adopted, of converting refinancing of growth in smallholderlending into.financing of Input imports as an Intermediate step torefinancing portfolio growth, was a pragmatic one in the light ofMadagascar's extreme balance of payment problem*. The solution has provedsuccessful in easing the input constraint. With the allocation of reflowsto funding growth in B3M's portfolio, the project has made a substantialcontribution to the recovery of Madagascar"s agricultural economy during avery difficult period.

IV. THE PROJECT

A. Prolect Oblectives

4.01. The proposed projects a part of an IDA-supported broaderagricultural reform program, would respond to several major countrydevelopment strategy concernss need to reduce state involvement in theeconomy, to give greater emphasis to market forces to Increase efficiencyof resource utilization, and to strengthen key institutions. Within thecontext of this program, the project would have the following specificobjectivest

(a) to contribute to further institutional development of BTM,and

(b) to meet foreign exchange costs of new investments, andexpansion and improvement of existing ventures in agriculture(production and prime l processing/marketing).

4.02 A major objective of this project Is to pull BTh out of itsdifficult financial condition and put it on sounder tracks. In this, itaims to complete a process already started under the first BTM projectwhich so far has had encouraging results. It is supported by the fact thatBTM Is a commercial bank, which gets its resources from deposits andcurrent accounts bought in the market and, therefore, has to remaincompetitive and profitable. This implies that, at least within the projectperiod: BTM should (a) concentrate incremental agricultural lending to itsmost solvent clients, primarily medium-sixed enterprises in the privatesector, (b) not make new loans to those borrowers classified as poor riskby BTM's auditor (mainly parastatal borrowers) and (c) continue lendingcautiously to small farmers, as such operations on a larger scale haveproven to be very costly in the past, jeopardizing its profitability andsolvency. The Policy Statement approved by BTM's Board as a condition forthe IDA credit Board presentation (para 5.05) support these general linesof BTH lending policy.

4.03 In view of the factors listed above, the proposed project has beenconceived as an interim lending operation, with the purpose of assistingBTM to complete its full fineaneal recovery and contributing to theMalagasy agricultural sector by extending credit to productiveundertakings. Based on the obove criteria, under the project BTM wouldlimit its lending basically to BTM's borrowers Identified under para 4.02(a) through the uae of selective eligibility criteria. This Implies thatthe project -will not increase BTM's capability to substantially expand itssmaliholder rural credit financing. As the lack of smallholder credit is amaj.or Issue in Madagascar, the project woulds however (a) continue tofin-ance the Incremental cost of the pilot credit management project,started under the first project w<ich alms to improve recovery of ruralcredit through tight supervision; and (b) finance a consultant study to-formulate a long term agricultural credit policy for Madagascar which wouldaim at identifying and removing the basic constraints to smallholderlending.

B. Project Desi-n

4.04 The proposed IDA credit of US$ 10 million equivalent would be madeto the Government of Madagascar on standard terms. It includes a line ofcredit of US$ 8 million and an institution building component of US$ 2million.

4.05 The line of credit of USS 8 million would be committed over anexpected two and a half year period against the foreign excbange cost ofsub-projects. Sub-projects would be eligible that cover new investment,rehabilitation or extension of activities in agriculture; agriculture Isbroadly defined to Include agriculture proper, livestock, fisheries andforestry. It would mainly finance the fixed investment needs, notablypurchase of machinery, equipment, and spare parts, for subprojects inagriculture. While the ongoing Agriculture Sector Adjustment Credit (para.2.12) already makes foreig exchange available to the sector on a full cashpayment basis, the foreign exchange to be made available under projectwould serve those that would lack the liquidity in local currency and wouldneed credit. At present there is a large demand for foreign exchangeinvestment funds notably from farmers and private entrepreneurs who havebeen neglected in recent years but who are anxious to take advantage of thenew economic climate and more encouraging attitude of Government. Theproject would help to increase production of -rops and would provideinvestment opportunities to processing and marketing activities in theagriculture sector. It would allow an increase in foreign exchangeearnings through increased exports of pepper, seafood, wine, etc. Asprivate entrepreneurs play a critical role in processing and marketingactivities, the project's main target would be those private entrepreneursowning profitable businesses which operate at a relatively high capacity.Thus it Is not likely that public enterprises would be good candidates totake loans under the proposed credit. The project pipeline already

-20-

includes 31 promising projects for which detaile4 preparation is underway.All of these sub-projects are in the private sector and Involve eitherciltivation or agro-industries. Total value of these projects is about FMG,966 million (US$ 15.90 million). IDA would make 1MG 6,026 million (US$8

million) available for sub-project financing.

4.06 The institution buildina comoRnent - This component would financecomputer equipment, technical- assistance for audit, management consultancyservices and training; and the costs of the pilot credit managementproject. Thus this component would allow for (i) extension of the presenttechnical assistance to-BTM's training division and to the computerdivision; (ii) use of 8s0ort-term consultant services to help BTHstrengten its,project promotion and appraisal; (III) continued financingof- assistance to audit and Institution building from the internationallyrecruited firm already helping 8TM; (iv) financing of incremental costs ofthe pilot field level credit management project aimed at revivingsmallholder.credit; (v) Consultancy services to 8assit would-beentrepreneurs with further technical preparation of project ideas that areprime facie viable at the identification stage; (vi) consulting servicesfor a-study on agricultural credit policy; and (vii) procurement ofcomputer hardware and development of specialized banking operationsoftware. This last item, which would require about US$ 1.2 millionequivalent is urgently needed by BTM to initiate and monitor portfolioanalysis and improve its current banking operations. It would complementthe actions taken under the previous project.

C. Proiect costs and Financinz Plan

4.07 Project Costs - Total project costs during the commitment periodof two and a half years, (expected to be from September 1987 to February1990) are estimated at about FMG 14,543 million (US$ 19.33 million), ofwhich about MMG 7,527 (US$ 10 million) or 52S represent foreign exchangecosts. The investment component of the proposed IDA credit, FMG 6,026million (US$ 8 million) will help meet the full foreign exchange cost ofsub-projects. Project Costs are estimated at March 1987 prices. Projectcosts including taxes which would not be covered by IDA are summarized inthe following table:

-21-

PROJECT COS

(M MIILLIOWS) } (UMIL) # ot Totlse

Local I Foroigni Total LocellforolqnlTotal Coe"

I. Cedlt Comoonent

- Sub-loan to og9cul-trol .nterpuele 5,940 0,0 1t,966 7.9 0."9 16.90 92

- Total eit componen 6.90 gm 1it.ow 7.9 6.0J 16.90 S

IZ. Instiutin sultdid . .g

- Comper Equipment 714 902 1,616 9.95 1.29 2.16 l

- Technical Assistance 1S 89o 315 9.2 0.40 0.42 2

- Consultin Services 118 169 2" 0.15 0.29 9.85 2and Trl Tn*9

- Ag. Credit Study 8 22 89 0.01 0.03 0.04

- Incremntal Costa of apilot cred. mgnt. proj. 226 87 268 9.89 9.95 9.85 8

- Unallocated - 90 90 - 9.12 0.12

- Total Institution butidingomponent 1.A7 1.501 2. 1. 2 48 24 43 18

TOTAL COSTS 7,010 7,527 14,64 0.83 1.00 19.88 1O

4.08 Proiect Financint Plan

Financing of Project costs would be shared as follows:

FAG Million US$ Million Z of Total CostsIDA 7,527 10.00 52BiM 4,623 6.15 32Investors 2,393 3.18 16

TOTAL 14,543 19.33 100

The proposed IDA credit of US$ 10 million would finance 100Z of theforeign exchange costs. Local contributions of FMG 7,016 million (US$9.33million) would be made by investors and by BTM from its own resources and

-22--

counterpart funds generated by the First Agricultural Credit Project whichaccount for about SDR 5.8 million equivalent. Investors would contribute202 of total costs of sub-projects.

D. Procurement and Disbursement_

4 09 Procurement - Procurement for the subprojects financed under theline of credit vould be on the basis of competitive quotations fromdifferent suppliers, a procedure acceptable to IDA. Given the relativelymodest size of procurement packages for subprojectst there is little scopefor international competitive bidding.. Technical Assistance-for theproject would be open to international recruitment, to be selected inaccordance with Bank Guidelines. Computer equipment would be procuredthrough ICB.

4.10 Proceeds of the credit would be used for financing:

(a) BTH's subloans: 100I of the cif cost of Imported goodsand 100% of internationally procured services needed for theimplementation of eligible subprojects.

(b) Institution Building Component: 100% of the foreign exchangecost disbursed under the institution building component.

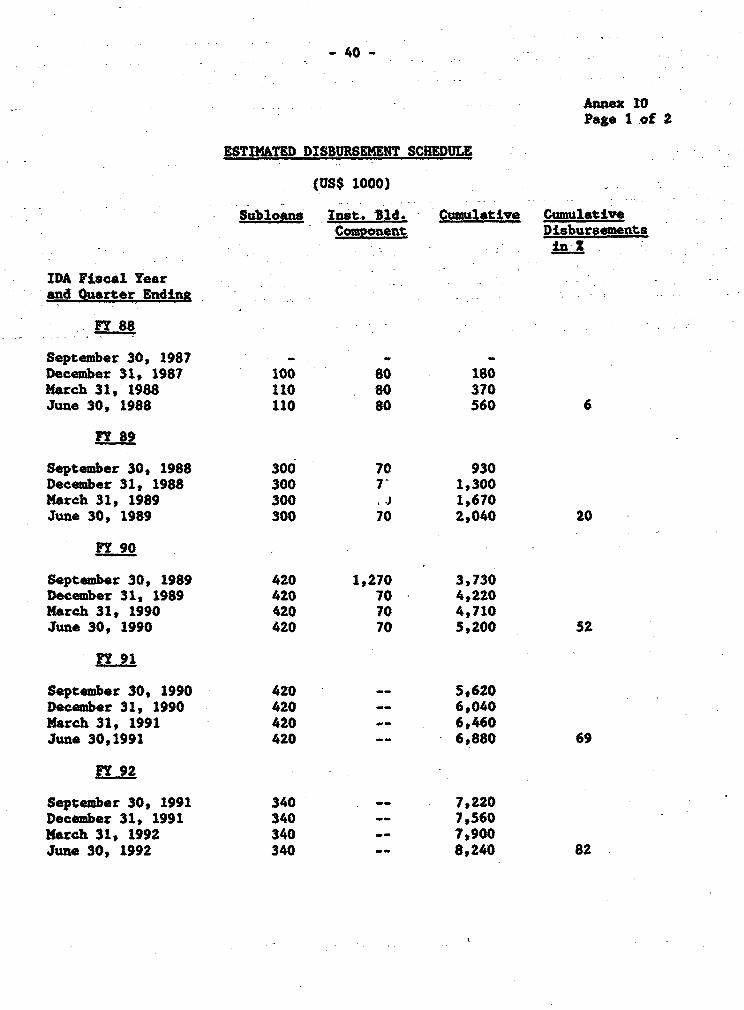

4.11 Disbursement. A special account of US$400,000 would be set up atthe Central Bank on terms and conditions acceptable to IDA. This amountrepresents an estimated average disbursement of funds over a four-monthperiod. The account would be replenished when the balance is belowUS$200,000. All credit withdrawals, except for the computer equipment, willbe financed from the special account unless otherwise previously agreedwith IDA. Withdrawal applicstions for replenishment of the special accountwould be-accompanied by a statement of the special account which wouldreflect all transactions. Subloan disbursements would be made on the basisof Statements of Expenditure (SOEs). The documentation for withdrawalsmade under S0K. would be reviewed by independent auditors and by IDAmissions. Disbursements under the Institution Building Component would befully documented. The project disbursement schedule is shown in Annex 10.The estimated disbursement profile for the proposed Project Is in line withthe Bank standard profile for financial intermedisiry loans. Disbursementsare expected to be completed by June 30, 1994. It is, however, possiblethat if the project is implemented more efficiently and with fewer delaysthe Implementation period could be reduced to five years.

S. Accounts and Audit

4.12 BTM's annual accounts are audited by an independent local firm,Fivoarana, with support from an international firm, Arthur Andersen. Thedraft audit report on the 1985 accounts has been submitted to IDA. Thisreport gives evidence of an audit satisfactorily carried out in accordancewith acceptable standards and gives a clear picture of BTM's situation.

-23-

Assurances were obtained at negotiations that during the project periodboth project accounts and the accounts of BTM as a whole would be auditedby auditing firms acceptable to IDA, and the auditors' report wouldspecifically include the auditor's opinion on SQEs and the special account.The cost of the International firm's fees will be paid from the IDA credit.BTM would maintain separate accounts adequate to show utilization ofProject funds and keep development funds separate from the rest of itsbusiness. Assurances to this effect were obtained at negotiations.

V. PROJECT IMPLEMENTATION

A. General

5.01 The project would be implemented by BTM, within the framework ofwork programs agreed with its Board and IDA. BTM will be responsible forall aspects of identification and promotion, assistance in preparation,appraisal and supervision. BTK will make decisions independently and applyselective technical and solvency criteria included in its current appraisalprocedures and Policy Statement. BM has qualified managers and staffwhich together with technical assistance, enabled BTM to achieve over thelast three years, an internal reorganization that tightened up creditreview and appraisal, a good training program, a computer master plan, andan assessment of the loan portfolio. In view of the assurances obtained atnegotiations on the financial recovery and staffing of the institution(para 3.22), BTM would be able to manage the project satisfactorily.

5.02 As a part of the proposed project, BTM would conduct a study byconsultants to formulate an agricultural credit policy for Madagascar, withparticular attention to the needs of smallholder farmers. Such a studywould supplement on ongoing study, conducted by the Central Bank,concerning the country's overall credit policy. It would cover among otherthings, aspects such as special provisions for develovm.nt of smallholdercredit; preferential rediscount of agricultural credit; and guarantee andpromotion (risk capital) funds for agriculture (para 3.09). In conductingits study, BTM has to make arrangements, satisfactory to IDA, with theCentral Bank, the Agricultural and Finance Ministries and the other twocommercial banks, so that their views on this matter will receive dueconsideration. The scope of the study, including an outline TOR, wasagreed with the Government and BTM during negotiations. BTM would submitto IDA for review and approval, the recommendations of the study by June30, 1988; the Government would implement the agreed recommendations notlater than December 31, 1988.

B. Organization and Reporting

5.03 The Annual Work Proaram and Quarterly Report. BTM would preparea draft annual work program for each project year. The program willinclude: (i) the pipeline of sub-projects identified, those being prepared,appraised, approved, or implemented plus execution schedule and comments on

-24-

each sub-project; (i1) BTf's recruitment and training programs under theproject; (lit) the project budgetg (iv) projected comm.metnts anddisbursements under the project indicating projected IDA disbursements,BTM's loan, Investors' contribution plus arrears analysis and loancollection data; (v) a comprehensive description of expenses related to theinstitution building component; (vi) BTM's projected balance sheets,operating accounts and Profit sad Loss accounts; and (vii) discussion ofserious problems which may arise and actions to deal with them.

5.04 The annual work program would be submitted to IDA with copies tothe technical ministries by end of October of eveTy year for the followingyear its approval by IDA would be a condition of ennroval of new.spibrojects for that year. For 1987, the annual work program has beenreviewed and approved. During the year BTM would convey to IDA with copiesto the technical ministries (Ministry of Finance, MPARA, MPARF), aquarterly ptogress report covering all Items Included in the annual workprogram. Assurances to this effect were obtained at negotiations.

5.05 Prolect Management. BTM's Board would have full autonomy toapprove or reject any sub-project within the program. In addition, aPolicy Statement specifying which decisions can be taken by BTMfsManagement was adopted by the newly appointed BTM's Board on March 12,1987. Such a Policy Statement was acceptable to IDA.

5.06 Two of BTM's Departments would have direct responsibility forproject implementation: the Planning and Rural Development Department(PRDD) and the Operations and Credit Department (OCD). While in PRDD* theexisting director and his professional staff are capable, a considerableincrease in project promotion and appraisal business as onvisaged wouldneed increased staffing. Therefore, under the project, PRDD staff would bereinforced by seven local professionals. Four of the professionals, i.e.,an economist, a statistician/economist, a financial analyst and anagronomist, would be assigned to the Projects and Research Division, and tobe responsible for project identification, preparation and evaluation. Theremaining three professionals including a rural development engineer, alivestock specialist and an economist would be assigned to the RuralDevelopment Division, to be responsible for promotion activities.Similarly, staffing of the OCD would be reinforced with the recruitment ofthree local professionals, i.e. two financial analysts and an economist tostrengthen credit monitoring. Assurances to this effect were obtainedduring negotiations that all these positions will be filled not later thanSeptember 30, 1987.

5.07 Sub-loan appraisal would be done by the PRDD for all BTM loanrequests under the project. Appraisal reports would be seviewed by theDirector of the PRDD before they are presented to the Credit Committee(para. 3.15). Current appraisal procedures are comprehensive and adequatewith the exception of the finascial analysis which needs Improvement. Theproject would provide funds for training BTM staff in the economic andfinancial analysis of projects and a technical assistant experienced inproject analysis would be recruited to provide short term training to BTM'sstaff.

-25-

5.08 Renorting Reouirements - BIm would submit to IDA quarterly reportswhich would Include a summary of operations, financial statements, resourceposition, statement of arrears, aollection ratios and-notes on projects indifficulty. The reports would also Include details of the subloansapproved and committed, and a summary analysis of the status ofImplementation and performance of aubprojects financed under-the creditcomponent. BTM would also convey to IDA progress reports prepared by theauditing firm on the progress of the action plan each year. In addition8TM annual reports and audited accounts prepared by qualified accountantsacceptable to IDA will be submitted to IDA vithin six months after the endof the year.- 8TM would also submit a draft Project Completion Report whenthe -project Is completed. Assurances to this effect were obtained atnegotiations.