world bank documentdocuments.worldbank.org/curated/en/589931468281720911/pdf/multi0... · brfl bank...

TRANSCRIPT

Document ofThe World Bank

FOR OFFICIAL USE ONLY

Report No: 23337

IMPLEMENTATION COMPLETION REPORT(FSLT-70030)

ONA

LOAN

IN THE AMOUNT OF US$505.06 MILLION

TO NACIONAL FINANCIERA, S.N.C.

WITH THE GUARANTEE OF THE UNITED MEXICAN STATES

FOR A BANK RESTRUCTURING FACILITY ADJUSTMENT LOAN

12/21/2001

Mexico Country Management UnitLatin America and the Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance of theirofficial duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective )

Currency Unit = Mexican Pesos MXPMXPI = US$ 0.108US$ 1 = MXP9.26

FISCAL YEARJanuary 1 -December 31

ABBREVIATIONS AND ACRONYMS

BRFL Bank Restructuring Facility LoanBRFL II Second Bank Restructuring Facility LoanCAS Country Assistance StrategyCETES Treasury Certificates (Certif cados de Tesoreria de la Federacion)CNBV National Banking and Securities ComissionFOBAPROA Trust Fund for the Protection of Bank SavingsGDP Gross Domestic ProductIDB Inter-American Development BankIPAB Bank Savings Protection InstituteIMF International Monetary FundNAFIN Nacional Financiera S.A.NAFTA North American Free Trade AgreementSHCP Secretariat of Finance and Public CreditUDI Investment Units (Indexed)

Vice President: David de FerrantiCountry Manager/Director: Olivier Lafourcade

Sector Manager/Director: Danny LeipzigerTask Team Leader/Task Manager: Mariluz Cortes

FOR OFFICIAL USE ONLY

MEXICOBank Restructuring Facility Loan

CONTENTS

Page No.1. Project Data 12. Principal Performance Ratings 13. Assessment of Development Objective and Design, and of Quality at Entry 24. Achievement of Objective and Outputs 55. Major Factors Affecting Implementation and Outcome 126. Sustainability 157. Bank and Borrower Performance 168. Lessons Learned 179. Partner Comments 1710. Additional Information 18Annex 1. Key Performance Indicators/Log Frame Matrix 19Annex 2. Project Costs and Financing 20Annex 3. Economic Costs and Benefits 22Annex 4. Bank Inputs 23Annex 5. Ratings for Achievement of Objectives/Outputs of Components 24Annex 6. Ratings of Bank and Borrower Performance 25Annex 7. List of Supporting Documents 26Annex 8. Matrix of Policy Actions for Tranche Release 27Annex 9. Regulatory Reforms Implemented 30Annex 10. Description of IPAB Program at Inception - Shares of Total Assets by Group 32Annex 11. Transactions Underwritten by IPAB 33Annex 12. Additional Transactions 34Annex 13. Banking Credit as a Share of GDP 35Annex 14. Consolidation in the Banking Sector 36Annex 15. Non-Performing Loans 37Annex 16. Comments from IPAB 38

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

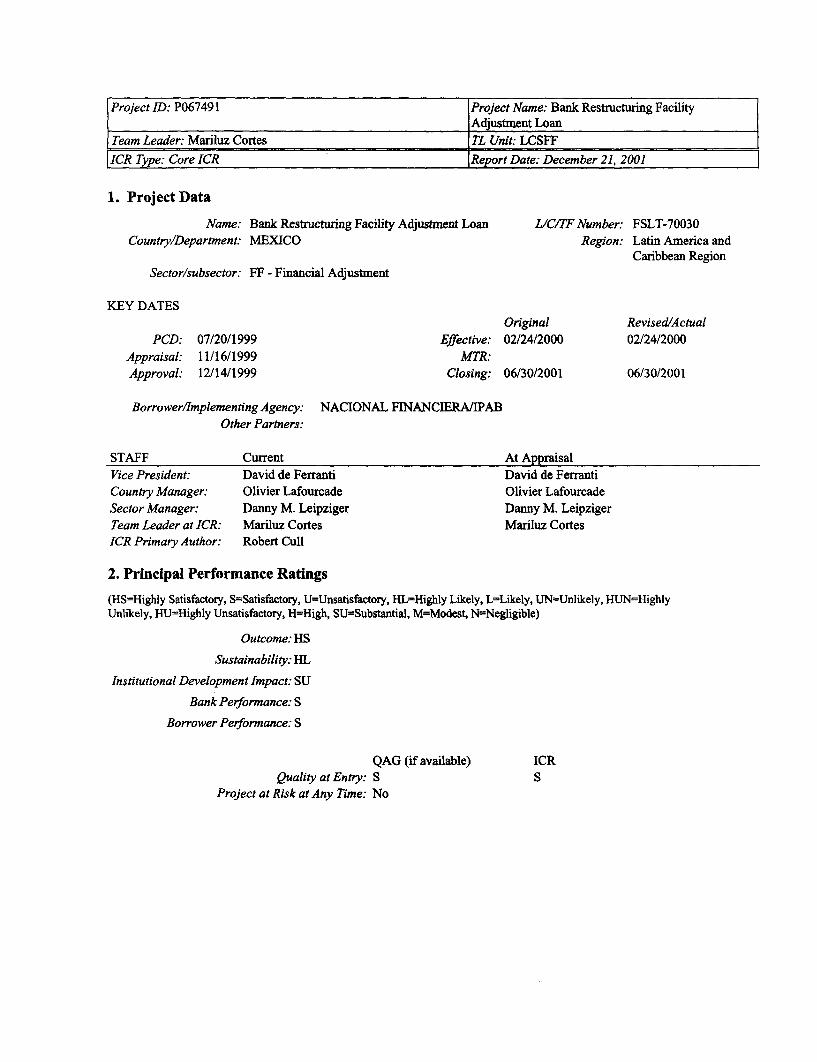

Project ID: P067491 Project Name: Bank Restructuring FacilityAdjustment Loan

Team Leader: Mariluz Cortes TL Unit: LCSFF

ICR Type: Core ICR Report Date: December 21, 2001

1. Project Data

Name: Bank Restructuring Facility Adjustment Loan L/C/ITFNumber: FSLT-70030Country/Department: MEXICO Region: Latin America and

Caribbean RegionSector/subsector: FF - Financial Adjustment

KEY DATESOriginal Revised/Actual

PCD: 07/20/1999 Effective: 02/24/2000 02/24/2000Appraisal: 11/16/1999 MTR:Approval: 12/14/1999 Closing: 06/30/2001 06/30/2001

Borrower/Implementing Agency: NACIONAL FINANCIERA/IPABOther Partners:

STAFF Current At AppraisalVice President: David de Ferranti David de FerrantiCountry Manager: Olivier Lafourcade Olivier LafourcadeSector Manager: Danny M. Leipziger Danny M. LeipzigerTeam Leader at ICR: Mariluz Cortes Mariluz CortesICR Primary Author: Robert Cull

2. Principal Performance Ratings

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HL=Highly Likely, L=Likely, UN=Unlikely, HUN=HighlyUnlikely, HU=Highly Unsatisfactory, H=High, SU=Substantial, M=Modest, N=Negligible)

Outcome: HS

Sustainability: HL

Institutional Development Impact: SU

Bank Performance: S

Borrower Performance: S

QAG (if available) ICRQuality at Entry: S S

Project at Risk at Any Time: No

3. Assessment of Development Objective and Design, and of Quality at Entry

3.1 Original Objective:

3.1.1 Economic Context: The objective of this loan is best viewed in light of the situation ofthe banking sector during the second half of the 1990s. Between mid-December 1994 and the firstquarter of 1995, Mexico's banking system suffered a major systemic, solvency and liquidity crisis,triggered by the massive devaluation of the peso. As described in detail in the President's Report(PR) that accompanied the loan, the inherent weaknesses of the banking sector can be traced to anumber of policy failures, including the nationalization of the commercial banking system in theearly 1980s, and the subsequent rapid and poorly implemented privatization of banks in the early1990s. The banks were acquired by domestic buyers that lacked the requisite banking skills, andoperated within a weak regulatory framework. To deal with the systemic crisis, the Governmentused the Trust Fund for the Protection of Bank Savings (FOBAPROA) to provide broad,discretionary support to individual financial institutions. Through a mix of programs,FOBAPROA provided liquidity and capital to the banks and relief to debtors. However, asdescribed by many commentators (Bubel and Skelton (1998), Graf (1999), and Klingebiel(2000)), FOBAPROA lacked the legal tools, resources, and independence needed to resolve thevolume of assets that eventually came under its possession. In fact, most of the capitalization andportfolio purchase programs involved the issuing by FOBAPROA of non-negotiable promissorynotes (zero-cupon bonds), to be redeemed in ten years, with interests being payable at maturity(there were some exceptions to this rule for foreign buyers of distressed banks).

3.1.2 The FOBAPROA program did avert the collapse of the financial system, but at a very highfuture cost. As of June 1999, the estimated net fiscal cost of the financial support programsamounted to about MXP873 billion, equivalent to 19.3% of GDP, although none of the failedbanks had been closed or sold at that stage. The financial sector eventually stabilized, butremained undercapitalized, with a high share of non-performing and restructured loans (Annex15). Moreover, real credit growth to the private sector remained negative since 1995, posing athreat to the sustainability of Mexico's economic recovery.

3.1.3 At the end of 1998, the Mexican Government adopted a new strategy to resolve thesituation of the banks that remained insolvent since the 1994-1995 crisis and introduced aprogram of financial sector reforms aimed at preventing the repetition of a banking crisis in thefuture, and at restarting prudent bank lending to the private sector. The Bank is providingfinancial and analytical support for this program through a sequence of loans. The First BankRestructuring Facility Loan (BRFL), supported the first stage of the Government's program,involving legal and regulatory reforms and the capitalization and resolution programs of threelarge insolvent banks. The Second BRFL, approved on June 21, 2001, supports the second stageof the Government's program, which involves additional legal and regulatory reforms, theresolution of the remaining failed banks under government control, and the divestiture of residualassets assumed from banks by the Government during the crisis. Provided these first two loansare deemed successful, further ones are contemplated in support of other phases of theGovernment's financial sector reform program, including the restructuring of public banks.

3.1.4 Objectives: The objective of the BRFL was to assist the Mexican Government toimplement the first stage of its Bank Restructuring Program, aimed at bringing about a better

- 2 -

functioning banking sector, able to withstand external shocks and to increase prudent lending tothe private sector, opening access to groups and enterprises today largely excluded from bankfinancing (micro, rural and financing of small and medium enterprises - SMEs) and to continuestrengthening the legal and supervisory framework for a safe and sound system. The expectationis that the financial sector reforms implemented in Mexico will contribute to poverty reduction inseveral ways. First, by reducing the risk of another banking crisis, because financial crisis entailhuge financial costs and crowd out social spending, with dramatic effects on poverty increases.Second, by improving financial depth, because stronger banks are better able to sustain growth,lead to better allocation of resources and, therefore, reduce poverty. Finally, the legal reformsaimed at strengthening contract enforcement would be conducive to greater access to credit bySMEs, which should create more job opportunities, an important objective in a country with a fastgrowing labor force.

3.1.5 Specifically, the BRFL supported the following reforms:

* Legal Reforms to improve incentives in the banking system. These included: (i) approvalin December 1998 of the IPAB (Bank Savings Protection Institute) Law establishing a gradualphase-out of the universal deposit insurance scheme, replacing it with one mandating limitedcoverage; (ii) presentation to Congress of the Secured Transactions Law (April 1999) and anew Bankruptcy Law (November 1999); and (iii) the adoption of a final debtor relief program("Punto Final").

* Regulatory Reform to Improve banks' capitalization and soundness. In September 1999,the regulatory authorities announced a series of regulatory reforms to improve banks'capitalization and soundness, to be implemented according to a preannounced schedulebetween 2000 and 2003.

* Resolution of the failed banks under IPAB's purview through mergers/acquisitions andclosures. The Law gives IPAB the authority to carry out restructuring and resolutionoperations for troubled banks, including banks under the previous FOBAPROA bank supportprogram. This operation supported the restructuring, sale, merger or liquidation of severalbanks that were under IPAB's restructuring program.

* Disposal of bank assets under IPAB's control. The loan supported the implementation ofIPAB's program of asset disposal (assets inherited from FOBAPROA), which establishes atimetable for outsourcing the sale of loans and other assets purchased from banks tospecialized asset management companies.

3.1.6 The BRFL clearly incorporated appropriate development objectives. Resolving thepending troubled banks was the major obstacle to creating a well-functioning financial system.The sustained post-crisis contraction in real lending to the private sector was due, in large part, tothe failure to fully resolve the crisis itself Many banks languished, relying on substantialgovernment assistance to survive, without truly operating as banks. Moreover, many of themwere saddled with a large amount of illiquid FOBAPROA notes in their balance sheets, whichobliged them to get funding in the inter-bank market at very high costs. By also focussing onlegal reforms to improve the contracting environment and regulatory reforms to improve banks'capitalization and soundness, the BRFL made significant contributions to improved bankingperformance on a going-forward basis, and contributed to reducing the risk of future banking

- 3 -

crisis, and attracted foreign investment into this sector.

3.1.7 The passing of the IPAB Law marked an important change in approach to handling bankclosing and resolution, and put in place mechanisms to address the pending issues that hadprevented the full resolution of the 1994-1995 banking crisis. The new legislation allowed theGovernment of Mexico to make explicit the cost of the banking resolution and to reach apermanent solution to the banking problems in a transparent way. However, IPAB had inheritedso many of FOBAPROA's remaining problems, including its massive stock of non-performingassets, that there were few options for resolving troubled banks. For example, so many fiscalobligations had been inherited from the FOBAPROA era that it would have been impossible toadopt a 'good bank/bad bank' solution in which the performing assets of troubled banks, packagedwith as much of their deposits as possible, could have been sold to another bank, with the residualassets and liabilities being resolved quickly by IPAB; a resolution option that could have beenmuch less costly for the country. Therefore, the loan was designed: (i) to assist in a handful ofacquisitions or mergers of large, troubled banks, and (ii) as the first in a series of programmaticloans in which further restructuring would be pursued as more resources became available. Whileit could be argued that by sequencing the restructuring in this way, the Government allowed somebanks to deteriorate further, there was no real alternative. The Government's Bank RestructuringPlan and this operation were designed to make the best of a difficult situation with limitedresources. The policy mistake, if there was one, was that FOBAPROA had assumed too manyobligations at too high a price, postponing but not resolving banks from a financial point of view.

3.1.8 Another well-crafted feature of the BRFL was that the Bank's assistance wastransaction-based, meaning that the disbursement of funds occurred only after appropriaterestructuring transactions had been worked out. The Government and the Bank agreed on a setof eligibility criteria for transactions, and a pool of funds was set aside to support transactions thatmet those criteria. IPAB used the proceeds of the Bank loan to service its "performing" notes(that is notes that paid in cash at least the real component of the interest rate) issued to helpcapitalize the banks involved in those transactions and/or to improve the quality of the bank'sassets by replacing the old FOBAPROA notes. By specifying only eligibility criteria, rather thanidentifying the transactions themselves, the BRFL had an inherent flexibility that contributed to itssuccess.

3.2 Revised Objective:The loan objective remained unchanged.

3.3 Original Components:The BRFL was designed as a three tranche loan to support the first stage of the Government'sbank restructuring program. The first tranche was to be awarded upon effectiveness of the loan.Two floating tranches were linked to agreed bank resolution transactions. Based on the Bank'sassessment that all the conditions under the loan agreement had been met, release of a firstfloating tranche of US$150 million was approved on June 19, 2000. Release of the secondfloating tranche, also of US$150 million, was approved on December 13, 2000.

3.4 Revised Components:The loan components remained unchanged.

- 4 -

3.5 Quality at Entry:3.5.1 Quality at entry was satisfactory. The operation came in the aftermath of a major crisis,that had left a number of failed banks still operating in the system, after unsuccessful attempts atrestructuring by the Mexican authorities. The operation was timely in that the Bank's involvementcame at a time when there was wide recognition of the failure of FOBAPROA's restructuringefforts, and a political consensus had emerged for the need to resolve the situation of the troubledbanks, and face past losses, no matter how large they might be. The earlier Bank operation toassist a weak FOBAPROA was rated unsatisfactory (see ICR, Report No. 18012), the operationlikely would have failed. Waiting until the better funded, more independent IPAB had beencreated, was a prudent course of action.

3.5.2 Quality at entry was further enhanced in a number of areas by the knowledge accumulatedin the Bank about Mexico's banking sector and policy framework, through economic and sectorwork carried out since the banking crisis. The quality of the operation was also enhanced by theBank's experience of what makes for successful financial sector reforms in other countries.

4. Achievement of Objective and Outputs

4.1 Outcome/achievement of objective:4.1.1 This adjustment loan has achieved its intended objective of supporting the first stage ofMexico's Bank Restructuring Program, aimed at bringing about a better functioning bankingsector, able to withstand external shocks and to resume prudent lending to the private sector,opening access to groups and enterprises today largely excluded from bank financing (micro, ruraland financing of small and medium enterprises - SMEs). All policy reform measures supported bythis loan were implemented within a year of loan approval by the Board. The achievement ofobjectives is rated as satisfactory, because the reforms have strengthened the banking sector byintroducing international standards of prudential regulation and by selling some of the failed banksto well run and financially strong foreign banks. Furthermore, the strengthened Mexican banksare fearing well despite the downturn in the economy, and seem to be insulated from contagionfrom the instability affecting other countries in Latin America. However, it is too early to judge ifthe expected long term effect of increased credit access to underserved sectors of the populationwill fully materialize, although there are some evidences that it is likely to be achieved.

4.1.2 The short-term objectives, which were achieved are highly satisfactorily. They aresummarized below, with some comments of additional actions needed to fully achieve theintended longer-term objectives.

A. Legal Framework to Improve Incentives in the Banking Sector

4.1.3 Deposit Insurance: In developing countries, which tend to have weaker supportinginstitutions, it is important to limit the range and amount of deposits covered. In thoseenvironments, overly generous insurance tends to lead to moral hazard, financial sector fragilityand slower long-run sector development (see World Development Report 2002 and Finance forGrowth (2001)). Under the first stage of the Government's Bank Restructuring Program,progress has been made in this area. The IPAB Law, provides for a gradual dismantling of the

- 5 -

universal deposit insurance scheme, replacing it with a Deposit Guarantee Fund, with limitedcoverage, to be administered by IPAB. Coverage will decrease in three stages, according to atimetable announced on May 31, 1999. By the end of January 2003, the guarantee will no longercover inter-bank credits, and by January 1, 2005 it will only cover deposits up to 400,000 UDIs(about US $130,000) per depositor. This is a high coverage both by regional standards and incomparison with per capita GDP. For reference, coverage per depositor in Brazil is aboutUS$10,000, which is about 3.3 times per capita GDP. In Peru, coverage per depositor is 8 timesper capita GDP. Under Mexico's new plan, coverage will be over twenty times per capita GDP.More encouraging, however, is the elimination of the government guarantee on inter-bankdeposits which will have a major impact on the banking system, because banks perceived as weakwill be rationed out of the inter-bank market, on which many now depend, and/or will face higherfinancing costs. The elimination of this guarantee should be a powerful incentive for banks tostrengthen their solvency, liquidity, and profitability conditions.

4.1.4 The PR for BRFL II identifies the need to improve the IPAB Law in order to clarifyIPAB's role as manager of the Deposit Guarantee Fund in three areas: (i) setting deposit insurancepremia; currently IPAB's Board lacks the flexibility to establish risk-based premia, (ii) establishingspecific rules to define recognition of deposit ownership; and (iii) change bank informationsystems to allow the authorities to determine the actual guaranteed deposit base in each bank. Inaddition, as noted above, although the new coverage limit is a substantial improvement overuniversal coverage, it is still high by international standards. Currently, the Mexican Governmentis in the process of reviewing the IPAB Law along these lines. Nevertheless, while some furtheradjustments may prove necessary, substantial gains have been made in this area.

4.1.5 Contract Enforcement, Creditor Rights: Two major legal reforms were passed under thefirst stage of the Government's Bank Restructuring Program, that aimed to improve contractenforcement and thus enhance creditors' rights. By removing many uncertainties associated withlending to the private sector, these reforms were designed to lay the groundwork for increasedaccess to credit, especially for underserved market segments such as SMEs. The CommercialReorganization and Bankruptcy Act of April 27, 2000, facilitates the recovery of assets in theevent of loan default by eliminating legal recourses that had enabled debtors to prolong theseizure process indefinitely and/or redeploy the corporate assets of failed firms. Although the legalframework is in place, the effect of this new legislation on credit expansion will depend on furtherstrengthening of the institutions in charge of implementing it. A positive sign is that federaljudges, who retain a central role in the new bankruptcy process, are being advised by technicalspecialists on legal, financial, managerial, and accounting matters associated with the institutecreated by the new law.

4.1.6 The second major legal reform was the Miscellany of Secured Lending, passed on April30, 2000. This includes amendments to the Commercial Code, the General Law on NegotiableInstruments and Credit Transactions, and the Credit Institutions Law. The reform facilitatessecured transactions by introducing new principles of collateral without the transfer of ownershipand the guarantee trust. The first principle enables borrowers to guarantee payment withinventories, goods in production, and other movable goods. The second permits these pledges ofgoods or future production without their physical transfer to the lender. The new legislation also

- 6 -

establishes two new procedures to execute guarantees: one judicial and the other extra-judicial,designed to shorten the process of foreclosing on borrowers' pledges of collateral in the event ofdefault. Since the new legislation by itself might be insufficient to foster greater secured lending,efforts should be made to monitor borrowers' ability and willingness to take advantage of the law.Complementary effort to convert Mexico's collateral registries to electronic form, which shouldimprove the efficiency and safety of pledging movable and non-movable assets, should also beencouraged.

B. Regulatory Reforms to Improve Banks' Capitalization and Soundness

4.1.7 In September 1999, under the first stage of the Government's Bank RestructuringProgram, the regulatory authorities announced a series of regulatory reforms which changed thedefinition of regulatory capital and required the disclosure of its composition; limited theincorporation of differed taxes in capital; improved the definition of risk-weighted assets;established loan classifications and new provisioning guidelines based on repayment capacity;improved accounting practices and standards; and improved disclosure. These represent majorattempts to improve CNBV's ability to monitor banks directly and through the market viaexpanded disclosure, and thus improve the safety and soundness and transparency of the system.The regulatory reforms and the timetable for their implementation are described in Annex 9.

4.1.8 These regulatory changes may make it easier for the CNBV to identify troubled banks. Asa further step in this area of reform, new regulations for early warning and prompt correctiveactions were introduced in an amendment to the Credit Institutions Law, supported by the SecondBRFL. The CNBV also issued Circular 1448, which conditioned regulatory forbearance on theexistence of a mandatory rehabilitation plan. The PR for BRFL II notes that such forbearance hasbeen granted in special cases. Still, the Mexican banking legal framework is geared towardsrehabilitation rather than closure in the event of severe difficulties. Future financial sector reformsshould incorporate more effective exit procedures for insolvent banks, since improvements inprudential regulations are generally insufficient to ensure bank soundness.

C. IPAB's Bank Capitalization and Resolution Program

4.1.9 IPAB inherited assets and liabilities from the failed FOBAPROA in late 1998. In addition,as time wore on, it became clear that many banks outside the FOBAPROA umbrella were alsofacing severe problems, and thus a number of them were intervened and later turned over to IPABfor restructuring. This section summarizes IPAB's bank restructuring/resolution transactionsunder BRFL I, and its planned restructuring/resolution efforts under BRFL II.

4.1 .10 To give the reader an understanding of the magnitude of the problems faced by IPAB, andto categorize banks according to their participation in the various restructuring programs offeredfirst by FOBAPROA and later IPAB, Annex 10 provides a chart based on CNBV data. WhileCNBV's bulletins provide information on banks currently in operation, from an historicalperspective they are incomplete since they exclude the assets of banks that have been taken overby the government. For this reason, we present data from December 1996, a point when datawere available for all but a handful of banks that had been intervened early on. As described

- 7 -

below, those banks, which comprised a relatively small share of the sector's assets, are currentlybeing liquidated under BRFL II. Annex 10, therefore, provides data on those banks that continueto exist in one form or another -- many banks were acquired or merged with others, and thus it istheir balance sheets and their branch networks that live on (see Annex 14 for data on sectorconsolidation). In choosing 1996 data, we also exclude banks that entered after that date. Asthose banks are also not very large, Annex 10 provides a reasonably comprehensive rendering ofthe banking sector. Perhaps the most striking feature of Annex 10 is that only 11% of totalbanking assets were held by banks that did not require assistance from IPAB. These were largelyforeign-owned banks such as Citibank, American Express, ABN Amro, and Bank Boston. Asindicated in Table 1 below, they comprise a relatively small share of retail banking in Mexico, buta large share of derivatives activities.

4.1.11 IPAB's Bank Restructuring and Resolution Program includes two large banks (Serfin andBancrecer) that were put under IPAB's management for not meeting the legal capital adequacyratio, and were put up for sale, and three other banks (Promex, Atlantico, and Inverlat) that wereto be merged or acquired by larger (domestic and foreign) banks. Under the Program, IPABissued notes to capitalize these banks prior to their sale and to replace the old FOBAPROA notes.IPAB has also in its program, for their closure or sale, ten small failed banks, that had beenintervened by the CNBV. Seven of these banks had received financial assistance fromFOBAPROA, and IPAB holds their capital shares and/or guarantees. In addition, IPAB isresponsible for the liabilities inherited from FOBAPROA with a number of banks that hadparticipated in FOBAPROA's private capitalization programs. Given the magnitude of theprogram, IPAB is implementing it by stages.

4.1.12 Bank resolution transactions under BFRL. Under BRFL I, IPAB issued MXP 100 billionto support the restructuring and purchase of Serfin by the Spanish bank Banco Santander CentralHispano (BSCH); MXP24.3 billion for Bancomer's purchase of Promex; and MXP46.5 billion forBank of Nova Scotia's purchase of Inverlat. As described below, Bancomer was later purchasedby the Spanish bank Banco Bilbao Vizcaya Argentaria (BBVA). As shown in Annex 11, thesetransactions brought in foreign ownership in banks that comprised 23% percent of total bankingsector assets (in 1996). This represents a remarkable transformation of Mexico's retail bankingmarket, 75% of which is now in foreign hands.

4.1.13 Bank resolution transactions under BRFLII Under BRFL II, IPAB will spend aboutMXP45.0 billion for the restructuring and sale of Atlantico to Bital, and MXP102.2 billion for therestructuring and sale of Bancrecer. Atlantico and Bancrecer represented 8% of the system'sassets in 1996 (see Annex 11). In total, IPAB's Program will have supported ownership changesin banks that comprised nearly a third of the system's assets in 1996.

4.1.14 There are seven banks to be liquidated: Capital, Cremi, Interestatal, Obrero, Oriente,Pronorte, and Union, which received assistance from FOBAPROA. In April, 2001, IPAB's Boardagreed upon a formal mechanism for liquidation, which will be undertaken as part of BRFL II.While none of these banks is particularly large, IPAB has set aside total support of MXP125billion to cancel their liabilities, prior to their liquidation. There are also two small intervenedbanks, Industrial and Sureste, that appear to have some remaining franchise value and could be

- 8 -

sold. As indicated in Annex 10, these banks comprised only 1% of 1996 banking sector assets.The closure and or sale of these banks is being undertaken as part of IPAB's second stage of theBank Restructuring and Resolution Program.

4.1.15 Banks Under Private Capitalization Programs. Under its Capitalization and LoanPurchase Program, FOBAPROA issued notes to purchase the impaired assets of many banks toimprove their balance sheets. IPAB conditioned the exchange of the old FOBAPROA notes forIPAB notes with the same terms, to the subscription, by each bank, of a "Financial ConsolidationPlan." The plans specified timetables of specific actions designed to enable these banks to meetthe new, more rigorous capital requirements. There are a number of large banks in this categoryincluding Banamex, Bancomer, Banorte, BBVA, and Bital. Together they represented over halfof the sector's total assets in 1996 (Annex 10). While these banks were not the major focus ofIPAB's efforts under BRFL or BRFLII, at least with respect to specific bank restructuringtransactions, they hold an important share of IPAB's liabilities. Some progress has been made inthis area. Most notably, two large banks in this category, BBVA and Bancomer merged on June29, 2000, and, as noted, IPAB had issued notes to support Bancomer's purchase of Promex.Therefore, through its indirect support via Promex and its direct assistance through the privatecapitalization program, IPAB helped facilitate the largest transaction undertaken. As indicated inAnnex 12, the banks that now comprise Bancomer-BBVA represented 21% of total sector assetsin 1996. Combined, the banks in that transaction and those sold under BRFL I represented 44%of the system's 1996 assets. When the transactions under BRFL II are complete, IPAB will havesupported restructurings of banks that account for 52% of the sector's assets. Moreover, underBRFL II, Banorte purchased Bancrecer, in late September 2001. To reiterate, in terms of sectorassets, IPAB has assisted in a remarkable amount of restructuring within a relatively short period.Banks under FOBAPROA's old Financial Strengthening "Saneamiento" Program were alsoeligible for the same IPAB note swaps as those under the capitalization and loan purchaseprogram. This category includes Banpais, Bancen, Santander-Mexicano, and Confia.

D. IPAB's Program for the Disposal of Bank Assets

4.1.16 Residual Asset Disposal: Based on cross-country experience, Klingebiel (2000) arguesthat asset management companies (or agencies) are only effective if used for the narrowly definedpurpose of resolving insolvent financial institutions and selling their assets. Satisfactory resultsalso require assets that are easily liquefiable, such as real estate, professional management,political independence, appropriate funding, adequate bankruptcy and foreclosure laws, goodinformation and management systems, and transparency in operations and processes. Klingebielpoints out that almost none of the conditions was satisfied in Mexico under FOBAPROA, and,compared to other countries, recovery of assets was abysmal -- from 1995 to 1999 FOBAPROAsold only 0.5% of its assets.

4.1.17 Under IPAB, many of these problems have been resolved. As noted above, improvementshave been made to bankruptcy and foreclosure laws, and also with respect to disclosure ofinformation and transparency. IPAB also enjoys better funding and management, and morepolitical independence, and some progress was made in terms of residual asset recovery. As ofDecember 1999, IPAB's assets for sale had total book value of MXP251.6 billion (US$26.32

-9-

billion), which was composed of a loan portfolio (MXP215.4 billion); equity participations(MXP19.4 billion); and real estate and other assets (MXPI6.8 billion). Between the last quarterof 1999 and the end of 2000, IPAB auctioned eight packages from the loan portfolio andrecovered MXP9.8 billion. During the same period, IPAB received MXP2.8 billion from the saleof goods and real estate. In addition, as a result of the restructuring of several corporate loansdone by commercial banks in 2000, IPAB obtained a recovery of MXP877.9 million.

4.1.18 IPAB Is Cash Flow. The viability of IPAB's program of bank resolution is interdependentwith the management of its cash flow over time. IPAB, therefore, has taken multiple steps torefinance its debt to lengthen its maturity profile and thus reduce its debt servicing costs. Theseinclude: (i) weekly issues of Bonos de Proteccion de Ahorro ("BPAs"; MXP73.6 billion issuedbetween March and December 2000); (ii) long-term loans from financial institutions (MXP140billion in 2000); (iii) banks sales and restructuring of their liabilities; and (iv) refinancing andprepayment of its most expensive obligations. The PR for BRFL II notes that these effortsresulted in a reduction of 7.2% in real terms of IPAB's debt between December 1999 toDecember 2000, reducing it from 14.3% of GDP to 11.2% of GDP. In addition, the financial costof IPAB debt declined from an average of CETES+1.20 to CETES+0.87, where CETES is therate on Mexican treasury certificates (Certificados de Tesoreria de la Federacion). By providingsubstantial financial resources to IPAB, BRFL I clearly contributed to improved debt servicingterms and a reduction in total debt. This will, modestly, help ensure IPAB's future financialviability.

E. Long-term Objectives: Access to Credit

4.1.19 As noted, the PR for BRFL I made it clear that long-run objectives in terms of improvedprivate access to credit would be unlikely to emerge until later in the larger program of bankrestructuring. Annex 13 indicates that, since the 1994-5 crisis, credit to the private sector hasdeclined from about 30% of GDP to 15% of GDP. Those figures extend only through 1999, butthe most recent figures from the IMF's International Financial Statistics also indicate that, in thefirst quarter 2001, the ratio remained at 15%. On the other hand, Annex 15 indicates that theshare of non-performing loans has declined from 22% in 1995 to 13% in 2000. These portfolioimprovements are largely the result of IPAB's restructuring efforts. Rapid GDP growth up to2000, and the general process of consolidation illustrated in Annex 14. There is now a smallernumber of banks, with much stronger balance sheets, including many that are foreign-controlled.Because cleaning necessarily involves retiring impaired credits, it is not surprising that therestructuring process coincided with a reduction in the ratio of private credit to GDP. Moreover,sluggish economic conditions during 2001 have also curtailed growth in lending. In the PR, 2.9%annual growth in per capita income was estimated for 1999 to 2003. The most recent WorldBank Unified Survey indicates that per capita income will contract by 1.2% in 2001. In thefuture, the combination of a roster of more qualified owners and general improvements in thecontracting environment should lead to credit growth. The credit situation should be monitoredclosely in the coming years, and, if access is not improved, additional changes to the legal andregulatory framework should be undertaken.

4.2 Outputs by components:A. Legal Framework to Improve Incentives in the Banking Sector

- 10-

* The IPAB Law, approved December 1998, provides a timetable for the gradual rollback ofthe universal deposit insurance system, characterized by explicit coverage limits and theremoval of guarantees on inter-bank credits.

* The Commercial Reorganization and Bankruptcy Act, passed April 2000, simplifies thebankruptcy procedure making it impossible for debtors to suspend payment indefinitely and itallows the quick redeployment of the assets of failed firms.

* The Miscellany of Secured Lending, passed April 2000, expands the range of collateralizableassets to movable goods, inventories, and goods in process, without requiring physicaltransfer to the lender. It also establishes new judicial and extra-judicial procedures forexecuting guarantees in the event of default.

B. Regulatory Reforms to Improve Banks' Capitalization and Soundness

Capital Rules* A resolution issued by the Ministry of Finance and Public Credit (SHCP), on October 1999,

provides new definitions of Tier 1 and Tier 2 capital, specific provisioning guidelines, limits onthe use of deferred taxes as capital, and new treatment of equity investments, intangible assets,and off-balance sheet items in measuring capital.

Asset Classification and Provisioning Rules* CNBV circular 1449, issued October 1999, bases credit portfolio classification for credit card

loans on probability of non-payment, and establishes new provisioning rules for those loans.* CNBV circular 1460, issued January 2000, bases credit portfolio classification for mortgages

on the probability of default, and establishes new provisioning rules for those loans.* CNBV circular 1480, issued October 2000, strengthens and clarifies credit portfolio

classification rules for commercial loans. The new classification is based in comprehensivecredit risk analysis, including country risk, for both the loan and the creditor. It requiresquarterly classification and provisioning for 80% of the credit portfolio based on probability ofdefault; the remaining 20% based on repayment experience. The quarterly classifications arenow disclosed. The number of risk categories has expanded from 5 to 7, and the treatment ofguarantees changed.

Accounting and Disclosure Standards* CNBV circular 1448, issued October 1999, provides new accounting standards for asset

securitization and asset transfer; valuation is now based on international standards. It alsorequires institutions to disclose components of regulatory capital and disclose any regulatoryforbearance, including its impact on financial statements. Forbearance is now conditioned onthe existence of a comprehensive rehabilitation plan.

* CNBV circulars 1484 and 1488, issued October 2000, refine some supervisory norms tofacilitate financial reporting and disclosure.

* CNBV circular 1456, issued December 1999, provides new rules for accounting and valuationof holding companies.

C. IPAB's Bank Capitalization and Resolution Program

* IPAB issued notes worth MXP 100 billion to support the purchase of Serfin (the third largestbanking group) by the Spanish bank BSCH on May 22, 2000.

* IPAB issued notes worth MXP24.3 billion to support the purchase of Promex by Bancomeron August 10, 2000. Bancomer (the second largest bank) was then purchased by the Spanishbank BBVA.

* IPAB issued notes worth MXP46.5 billion to support the purchase of Inverlat (the eighthlargest bank) by the Canadian Bank of Nova Scotia on November 30, 2000.

D. IPAB Program for the Disposal of Bank Assets

* Between the last quarter of 1999 and the end of 2000, IPAB auctioned eight packages fromthe loan portfolio and recovered MXP9.8 billion. During the same period, IPAB receivedMXP2.8 billion from the sale of goods and real estate. In addition, as a result of therestructuring of several corporate loans done by commercial banks in 2000, IPAB obtained arecovery of MXP877.9 million. For comparison, from 1995 to 1999, FOBAPROA disposedof only MXPO.7 billion in assets.

4.3 Net Present Value/Economic rate of return:NA

4.4 Financial rate of return:NA

4.5 Institutional development impact:The short-term institutional development impact of the BRFL has been substantial, and additionalinstitutional restructuring is being undertaken as part of BRFL II. The legal reforms taken toimprove banking sector incentives should lessen moral hazard problems associated with the olduniversal system of deposit insurance, and improvements in contract enforcement should make iteasier and cheaper for banks to lend to the private sector. The measures taken with respect tomeasurement of capital, asset classification, and disclosure of financial information has strengthenCNBV's ability to supervise banks and it has enhanced disclosure. IPAB's support for a numberof bank restructuring transactions among Mexico's most important banks has resulted in morecapable ownership of what now appear to be viable institutions. IPAB's plan for disposal ofresidual assets incorporates multiple lessons from past asset management experiences, both inMexico and abroad, and auctions of assets have become a recurrent activity. It remains to be seenhow much those institutional developments will contribute to a vibrant, inclusive banking sectorover the long term.

5. Major Factors Affecting Implementation and Outcome

5.1 Factors outside the control of government or implementing agency:5.1.1 The policy reforms and the bank restructuring transactions supported by this operationwere implemented as envisaged. As in any banking sector operation, there was the threat thatglobal economic instability, particularly instability originating in another developing country,could have negative implications for the Government's overall program of banking sector reform.

- 12 -

Such contagion effects did not materialize during the implementation of the reforms. Theinsulation of the Mexican banks to instability in other developing countries, during theimplementation period, was largely the result of the close ties forged between Mexico and theUSA in the context of NAFTA (North American Free Trade Agreement). Although as the USeconomy decelerates, Mexico's banking sector could become more vulnerable to the instability inother countries in the region, the presence of a strong and stable banking sector will protect theeconomy from any major negative effect.

5.2 Factors generally subject to government control:5.2.1 The successful implementation of IPAB's bank restructuring program is due, to largeextent, to the Government's decision to eliminate all legal restrictions to foreign ownership in thebanking sector. Under the previous legal framework, foreign investors were not permitted to holdmore than 20% of the shares of any bank that comprised more than 6% of the aggregate capital ofthe Mexican banking system. In effect, this rule prohibited foreign control of the three largestbanks in Mexico. In February 1995, in the wake of the 1994-95 financial crisis, Congress hadpassed legislation permitting foreign banks to take majority stakes in Mexican banks (except forthe Big Three). However, as part of the December 1998, banking reform approved by Congress,all limnitations on foreign ownership of banks were removed, which proved crucial to the successof the BRFL. Allowing full foreign participation resulted in much-needed injections of capital andsound management and know-how into the banking sector and substantial restructuring of thebanks themselves through merger and acquisitions.

5.2.2 IMF (2000) reported that in 1994, less than two percent of total banking sector assetswere held by majority foreign-controlled banks. Table 1 indicates that, by December 2000,fifty-six percent of banking sector assets and sixty percent of retail deposits were held byforeign-controlled banks. Four foreign banks were responsible for the recent increase inparticipation in the retail market. Spanish banks had majority ownership of Mexico's largestfinancial group (BBVA-Bancomer) and its third largest group (Santander). Bank of Nova Scotia,through its purchase of Inverlat, ranked as the eighth largest bank. Citibank ranked ninth. Thosefigures, however, do not include Citibank's purchase of Banamex, Mexico's largest bank, whichwas completed on August 3, 2001. Adding Banamex to the figures in Table 1, roughlyseventy-five percent of banking sector assets and eighty percent of retail deposits are now held byforeign-controlled banks.

5.2.3 Prior to Bancomer's sale to BBVA, IPAB notes had supported the purchase of Promex byBancomer. IPAB notes directly supported Santander's purchase of Banco Serfm and NovaScotia's purchase of Inverlat. In this way, IPAB was instrumental in the restructuring efforts ofthree of the four foreign banks most involved in Mexico's retail banking sector.

-13 -

Table 1. Foreign Ownership in Mexican Banking Sector (Dec. 2000)Type Number of Capital (US $ % of Assets % of Loans % of Retail % of

Banks bn) Deposits DerivativesMexican 14 7.0 44 44.7 40.3 12.6controlled

Large foreign 4 4.2 52 48.6 59.6 34.6affiliates &foreigncontrolledlarge banks

Small foreignaffiliates 14 0.7 - 4 6.7 0.1 52.8Source: Yacaman (2001).

5.2.4 Emerging empirical evidence across many countries indicates that the presence of foreignbanks is associated with higher profitability, and lower interest margins and overhead expenses fordomestic banks. This strongly suggests that foreign presence improves sector efficiency, andeffects are strongest in countries with poorly developed banking sectors. Cross-country evidencealso indicates that foreign presence reduces the probability of systemic crisis in the banking sector.Similarly, the evidence indicates that legal restrictions on foreign entry are associated with lowerloan quality and greater sector fragility. When financial crises do occur, foreign banks may be astabilizing influence. For example, there is evidence from Goldberg et al. (2000) that during theTequila Crisis private foreign banks in Argentina maintained higher loan growth rates than eitherthe domestic private or the state-owned banks. That study also finds that credit growth forMexico's foreign-controlled banks was less sensitive to macroeconomic fluctuations than wascredit growth at domestic banks from 1995 to 1998. The entire body of evidence, which issummarized in World Development Report 2002: Building Institutions for Markets and theBank's Policy Research Report Finance for Growth: Policy Choices in a Volatile World, stronglysuggests that by eliminating restrictions on foreign ownership of banks, the Mexican authoritiesnot only remedied a shortage of capital, but also set the groundwork for a more efficient andstable banking sector.

5.3 Factors generally subject to implementing agency control:5.3.1 As noted in the discussion of achievement of objectives and outputs, with respect to bothregulatory reforms and the restructuring of a handful of key banks, the Government hasaccomplished many of the policy actions that were under its control. These successes were, tolarge extent, the result of the capable management and the quality of the professional staff of bothIPAB and CNBV. In particular IPAB, which was a new agency when the BRFL was approved,had from the beginning a very capable management that was able to incorporate a number ofyoung, highly skilled, professionals, to its staff. In addition, IPAB's charter, dictates that itreports to Congress periodically and it submits to Congressional audits. This oversight brought

- 14 -

about much transparency and independence in IPAB's operations. The details of all of IPAB'sactivities are regularly posted on its website. The success of this operation owes much to thequality of IPAB's staff and the transparency of its operations.

5.3.2 IPAB's continued success in restructuring remaining troubled banks under BRFL II will bekey to ensuring the sustainability of the overall program of bank reformn. Similarly, theGovernment should monitor whether the regulatory reforms, especially those related toimprovement of the contracting environment, are having the desired effects with respect to accessto credit and its cost. If not, further regulatory reform may be required.

5.4 Costs andfinancing:NA

6. Sustainability

6.1 Rationale for sustainability rating:6.1.1 The reforms undertaken under the BRFL are likely to be sustainable in the sense that theywill not be overturned. The legal and regulatory reforms supported by this loan (summarized inAnnex 9) are necessary to support Mexico's growing participation in the global economy; and areunlikely to be repealed without causing great damage to the rest of the economy. Moreover, theBRFL II, which is already approved, contemplates additional regulatory reforms designed tofurther strengthen banking safety and soundness, including new guidelines for internal governanceand improvements in external auditing requirements. Also, although the threat of a financial crisiscan never be completely erased, increased participation by foreign banks, especially in the retailmarket, is likely to lend greater stability to Mexico's banking system. Although some foreignowners could conceivably sell their banks at some point in the future, it is likely that foreignpresence will remain high.

6.1.2 On the other hand, one of the key long-term goals mentioned in the BRFL is to foster abanking sector better able to lend to the private sector, opening access to groups and enterprisestoday largely excluded from bank financing (micro, rural and SME financing). As noted, becausethis was the first loan undertaken as part of a larger program of banking reform, there is littleevidence of improved credit access to date (studies on this topic are underway for the urban poorin Mexico City and Bogota, Colombia, and more broadly to all uder-served groups in Brazil).Improvements will no doubt depend on how well the new regulations are implemented, especiallythose relating to bankers' incentives, creditors' rights, and the general quality of the contractingenvironment.

6.1.3 In short, the sustainability of the loan's short-term objectives is highly likely, whilesecuring long-term objectives regarding access to credit are less certain. The overall sustainabilityof the policy reforms is, therefore, rated likely. This highlights the difficulties inherent inevaluating loans that are an early part of a larger program in the context of an ICR.

6.2 Transition arrangement to regular operations:NA

- 15 -

7. Bank and Borrower Performance

Bank7.1 Lending:The Bank's lending performance was satisfactory. The Bank devoted substantial attention to theidentification, preparation and appraisal phases. The reform proposals discussed with theGovernment authorities during loan preparation were based on very extensive, largelyconfidential, economic and sector work, as well as policy dialogue, carried out by the Bank duringthe years prior to loan preparation. The extensive knowledge of the sector accumulated by theBank strengthened the operation. Also, the Bank was very effective in applying the lessonslearned from other financial sector loans to the design of the BRFL. In particular, the decision tomake tranche disbursements based on completed bank resolution transactions, was a veryimportant element in the success of the loan and containing the risks for the Bank.

7.2 Supervision:The Bank's performance during supervision was also satisfactory. Prior to each tranchedisbursement, the staff carried out an in-deph review of all the evidence of compliance withtranche conditions. Particular attention was given to the review of all the completed bankresolution transactions to ensure compliance with agreed eligibility criteria and loan covenants.Given the complexity of the evidence of compliance with tranche conditions, it was a gooddecision to involve the Bank lawyer in each of the supervision missions.

7.3 Overall Bankperformance:Overall Bank performance was satisfactory.

Borrower7.4 Preparation:The Borrower's performance in identification and appraisal is assessed as satisfactory. One of thereasons for the success of the operation, was that during loan preparation the Borrower, throughits two agencies: CNBV and IPAB, showed a greater openness and willingness to shareinformation with the Bank than in the past. During long time after the banking crisis, theauthorities had been reluctant to recognize the need to reform the banking regulations and toresolve the situation of the insolvent banks. This reluctance affected negatively the policydialogue between the Bank and the authorities. The change in attitude of the authorities reflected,in part, the broadening of the political representation in Congress, which brought about a greateropenmess in discussing policy matters, including the failure of the FOBRAPOA program, and thepressure via more democratic system to disclose more information.

7.5 Government implementation performance:The Borrower has fully complied with the provisions of the loan, within the expected time frame.All three tranches were disbursed within the same calendar year.

7.6 Implementing Agency:The two main Government agencies involved in implementing the policy measures supported bythis operation were CNBV (National Banking and Securities Commission) and IPAB (BankSavings Protection Institute). The performance of both agencies was satisfactory.

7.7 Overall Borrower performance:

- 16-

Overall the Borrower performance is rated as satisfactory.

8. Lessons Learned

8.1 Set limited objectives. Over-ambitious objectives, such as the restoration of the solvency andsoundness of the banking system, is a long-term goal that goes beyond a single operation. It ismore realistic to support a program of reforms with a number of sequential operations that can beapproved based on the success of the previous ones.

8.2 Disburse against specific transactions. Banking restructuring operations should disburseagainst the completed resolution of specific banks' cases, not against the promise of future actionswhich may not materialize. However, the operation should not specify the transactions it willsupport ex-ante, but rather should develop criteria that determine which transactions are eligiblefor financial support (i.e. floating tranches). This approach builds important flexibility into theoperation.

8.3 Ensure that the main implementing agency is the main recipient of the Bank resources.Bank funds should be disbursed to the main agency in charge of implementing the policy reforms,to strengthen the incentives of these agencies to work in close collaboration with the Bank.

8.4 Bank support should come only after a political consensus in favor of restructuring banksandfacing past losses has been achieved. FOBAPROA's lack of resources and legal support wasa strong signal that such a consensus had not been reached immediately after the crisis. Had theBank tried earlier to assist a weak FOBAPROA, the operation likely would have failed. Waitinguntil the IPAB Law created an enabling framework for the resolution of insolvent banks, andIPAB had the resources to finance bank resolution transactions, was a prudent course of action.

8.5 Tools of evaluation may need to be better adapted to suit sequential operations within abroader program. Current tools of evaluation are not perfectly suited to evaluating programmaticloans. For loans that come early in the program, definitive answers regarding institutionaldevelopment and sustainability that are required by the ICR process are often not possible.

8.6 Restoring the viability of bank's cash flows. Prior attempts to "contain"the banking crisiswere excessively focused on "accounting solutions" (i.e., exchange of bad loans for governmentpaper) with no cash flow impact. The "least cash solution" was not the "least cost solution"andseveral banks, full of government paper had to be intervened since their cash flow continued todeteriorate.

9. Partner Comments

(a) Borrower/implementing agency:Comments by IPAB, the main implementing agency, are presented in Annex 16.

(b) Cofinanciers:

(c) Other partners (NGOs/private sector):

- 17 -

10. Additional Information

Report and Recommendation of the President on a Proposed Bank Restructuring FacilityAdjustment Loan in the Amount of US$505.06 million for Nacional Financiera. ReportNo.P7347-ME

- 18-

Annex 1. Key Performance Indicators/Log Frame Matrix

Outcome / Impact Indicators:

Indicator/Matrix Projected In last PSR Actual/Latest Estimate

NOT APPLICABLE BECAUSE THIS IS ANADJUSTMENT OPERATION

Output Indicators:

IndicatoriMatrix Projected in last PSR ActuaULatest Estimate

NOT APPLICABLE BECAUSE THIS IS ANADJUSTMENT OPERATION

End of project

-19 -

Annex 2. Project Costs and Financing

Project Cost by Component (in US$ million equivalent)Appraisal Actual/Latest Percentage ofEstimate Estimate Appraisal

Project Cost By Component US$ million US$ millionNOT APPLICABT.E 13CAUSE THIS IS ANADJUSTMENT JPER TION

Total Baseline Cost 0.00 0.00

Total Project Costs 0.00 0.00Total Financing Required 0.00 0.00

Project Costs by Procureme nt Arrangements (Appraisal Estimate) (US$ million equivalent)

Procurement MethodExpenditure Category ICB NCB Other2 N.B.F. Total Cost

1. Works 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00')

2. Goods 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00,)

3. Services 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00,)

4. Miscellaneous 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00)

5. Miscellaneous 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00)

6. Miscellaneous 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00)

Total 0.00 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00) (0.00)

- 20 -

Project Costs by Procurement Arrangements (Actual/Latest Estimate) (US$ million equivalent)

Procurement MethodExpenditure Category ICB NCB Otherd N.B.F. Total Cost

1. Works 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)2. Goods 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)3. Services 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)4. Miscellaneous 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)5. Miscellaneous 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)6. Miscellaneous 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)Total 0.00 0.00 0.00 0.00 0.00

(0.00) (0.00) (0.00) (0.00) (0.00)

" Figures in parenthesis are the amounts to be financed by the Bank Loan. All costs include contingencies.2 1Includes civil works and goods to be procured through national shopping, consulting services, services of contracted staff

of the project management office, training, technical assistance services, and incremental operating costs related to (i)managing the project, and (ii) re-lending project funds to local govermment units.

Project Financing by Component (in US$ million equivalent)Percenlag=e or Apprai%al|

Componeni Appraisal E%ilmate Aciual/Latesi Estimagep lBank Go't. CoF. Bank Go%i. CoF. Bank Govt. CoF.

- 21 -

Annex 3. Economic Costs and Benefits

NOT APPLICABLE BECAUSE THIS IS AN ADJUSTMENT OPERATION

- 22 -

Annex 4. Bank Inputs

(a) Missions:Stage of Project Cycle No. of Persons and Specialty Performance Rating

(e.g. 2 Economists, 1 FMS, etc.) Implementation DevelopmentMonth/Year Count Specialty Progress Objective

Identification/PreparationJuly 1999 1 Team Leader/Lead Ops. Officer

I Regional Financial SectorAdvisor

1 Bank SupervisorI Financial Economist1 Bank Restructuring Consultant

September 1999 1 Teamn Leader/Lead Ops. Officer1 Financial Economist2 Bank Supervisors

Appraisal/NegotiationOctober 1999 1 Team Leader/Lead

Ops.Officer1 Regional Financial Sector

Advisor1 Financial Economist1 Bank Restructuring

Consultant

SupervisionJune 2000 1 Team Leader/Lead Ops.

Officer2 Financial Economists1 Bank Restructuring

Consultant1 Bank Supervisor1 Sr. Counsel

December 2000 1 Team Leader/Lead Ops. OfficerI Bank Supervisor

ICRno rnission travelduring ICR stage

(b) Staff:

Stage of Project Cycle ] Actual/Latest Estirnate

No. Staff weeks US$ ('000)Identification/Preparation 27.46 106.6Appraisal/Negotiation 17.67 68.0Supervision 20.83 91.5ICR 6.18 25.7Total 72.14 291.8

- 23 -

Annex 5. Ratings for Achievement of Objectives/Outputs of Components

(H=High, SU=Substantial, M=Modest, N=Negligible, NA=Not Applicable)Rating

EZ Macro policies O H *SUOM O N O NAZ SectorPolicies OH OSUOM ON O NA

O Physical OH OSUOM ON *NAL Financial O H *SUOM O N O NAO Institutional Development 0 H O SU O M 0 N 0 NAC Environmental O H OSUOM O N * NA

SocialOi Poverty Reduction O H OSUOM O N O NALI Gender O H OSUOM O N * NAEJ Other (Please specify) O H OSUOM O N * NA

E Private sector development 0 H O SU O M 0 N 0 NAEl Public sector management 0 H O SU O M 0 N 0 NALI Other (Please specify) O H OSUOM O N O NA

- 24 -

Annex 6. Ratings of Bank and Borrower Performance

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HU=Highly Unsatisfactoiy)

6.1 Bankperformance Rating

El Lending OHS*S OU OHUrI Supervision OHS OS OLU OHUEl Overall OHS OS O U O HU

6.2 Borrowerperformance Rating

D Preparation OHS OS O U O HUEl Government implementation performance O HS O S 0 U 0 HUrO Implementation agency performance O HS OS O U 0 HUO Overall OHS OS OU 0 HU

- 25-

Annex 7. List of Supporting Documents

Bubel, Robert V. and Edward C. Skelton, "Fiscal Therapy: The Mexican Banking Industry inRehab," Financial Industry News, Fourth Quarter 1998, Federal Reserve Bank of Dallas.

Goldberg, Linda B., Gerard Dages, and Daniel Kinney, "Foreign and Domestic Bank Participationin Emerging Markets: Lessons from Mexico and Argentina," Federal Reserve Bank of New YorkEconomic Policy Review, vol. 6, no. 3, 2000.

Graf, Pablo, "Policy Responses to the Banking Crisis in Mexico," in Bank Restructuring inPractice, BIS Policy Papers, No. 6, August 1999, Bank for International Settlements, Basel,Switzerland.

IMF (International Monetary Fund), International Capital Markets Developments, Prospects,and Key Policy Issues (by a staff team led by Donald J. Mathieson and Garry J. Schinasi.)International Monetary Fund: Washington, DC, 2000.

Klingebiel, Daniela, "The Use of Asset Management Companies in the Resolution of BankingCrises: Cross-Country Experiences," World Bank, Policy Research Working Paper 2284, Feb.2000.

World Bank, Finance for Growth: Policy Choices in a Volatile World, Policy Research Report.New York: Oxford University Press, 2001.

World Bank, World Development Report 2002: Building Institutions for Markets. New York:Oxford University Press, 2001.

Yacaman, Jesus Marcos, "Competition and Consolidation in the Mexican Banking Industry afterthe 1995 Crisis," in The Banking Industry in Emerging Market Economies: Competition,Consolidation, and Systemic Stability, BIS Papers, No. 4, August 2001, Bank for InternationalSettlements, Basel, Switzerland.

- 26 -

Additional Annex 8. Matrix of Policy Actions

MEXICOPROPOSED BANK RESTRUCTURING FACILITY ADJUSTMENT LOAN

MATRIX OF POLICY ACTIONS FOR TRANCHE RELEASE

OBJECTIVES ACTIONS TAKEN BY MEXICO SECOND AND THIRD TRANCHETO DATE (First Tranche) ACTIONS

1. MACROECONOMIC POLICY FRAMEEWORKMaintenance of * Maintenance of sound * Maintenance of sound macroeconomicSupportive macroeconomic framework consistent policy framework consistent with policyMacroeconomic with policy objectives and program objectives and program described in LetterProgram described in Letter of Sector Policy of Sector Policy2. REFORM OF LEGAL FRAMEWORKImprove incentives The Mexican authorities have:in the financial * Obtained, in December 1998,sector Congressional approval of new

legislation creating the Institute forthe Protection of Bank Savings(IPAB). The Law phases-in a limiteddeposit insurance to replace theexisting universal insurance guaranteebetween June 1, 1999 and December31, 2004 (with the elimination ofcoverage on interbank liabilities by01/003)* Allowed full participation offoreign investors in existing Mexicanbanks* Submitted to Congress, in 04/99, adraft Federal Credit Guarantee Law,which if approved would strengthenforeclosure procedures and createconditions for lending based onmovable collateral* Has prepared and is ready tosubrnit to Congress a draft of a newBankruptcy law.

3. STRENGTHENING OF BANKING REGULATIONTo raise banking The Mexican authorities have: Second Tranche Actionssector regulation In September 1999, the SHCP/CNBV * That the Regulatory Reform Programtowards announced a series of regulatory has been implemented on a consistent basis,international reforms to be introduced gradually in accordance with its termsstandards to: between January 2000 and December* Improve the 2002. Within this program, Third Tranche Actionsquality of banks' regulations have been already issued * That the Regulatory Reform Programcapital in respect of: has been implemented on a consistent basis,* Enhance in accordance with its termsaccounting and * Changes in the definition of * Issuance of new regulation for loandisclosure standards regulatory capital which includes: (i) classification and loan loss provision for* Eliminate limiting the weight of deferred taxes either mortgage or commercial loansunjustified in Tier I capital; (ii) defining the

- 27-

forbearance characteristics of the non-cumulative* Improve loan subordinated debentures that could beclassification and counted as Tier I capital; (iii)provisioning rules deducting all equity investments in

non-traded, non-financial companiesfrom capital; and (iv) substitutingspecific provisions for generalprovisions in Tier 2 capital* requirements to disclose thecomposition of regulatory capital* improvements in the definition ofrisk weighted assets* new classification andprovisioning rules for credit cardloans* new criteria to grant regulatoryforbearance and requirements todisclose instances of regulatoryforbearance* requirements to disclose "troubled"debt, financial information bybusiness segment and aggregateinformation on transactions withrelated parties* improvement of accountingpractices towards internationalstandards regarding market valuationof investments and derivatives* introduction of accountingstandards applicable to assetssecuritization and assets transfers

4. RESTRUCTURING/RESOLUTION OF BANKS BY IPABTo restructure, sell, BANK RESOLUTION Second Tranche Actionsmerge or liquidate TRANSACTIONS * That IPAB has issued Eligible notes inbanks under IPAB's 2/98, an aggregate amount equal to at least US5.0bank restrcturing The IPAB Law, approved in 12/98, billion, in support of Eligible Bankprogram enables IPAB to assume the functions . . 2

. . , , . ~~Resolution Transactions .of a deposit insurer and a resolution T tagency to:~~~~~ That budgetary transfers to IPAB haveagency to: been made in a timely fashion so as to allow

p Manage the bank support IPAB to discharge its responsibilities underprograms and accelerate the financial the Programstrengthening of currentlyundercapitalized banks, and the sale Third Tranche Actionsor liquidation of intervened ones 3

a sell the assets purchased by * That IPAB has issued Eligible notes in anFOBAPROA from banks under aggregate amount equal to at least US8.0previous bank support programs billion, in support of Eligible Bankwithin a time frame of up to 5 years Resolution Transactions4

a That budgetary transfers to IPAB haveIPAB has already taken the following been made in a timely fashion so as to allowactions: IPAB to discharge its responsibilities under* taken control of Serfin in 7/99, the Programwritten-off shareholders equity and

- 28 -

started capitalization/sale process* taken control of Bancrecer in1 1/99 and, written off shareholdersequity and started capitalization/saleprocess

The Government has created aworking group with representativesfrom IPAB, SHCP and CNBV towork with the Bank to determine theeligibility criteria and verify thatIPAB's bank resolution transactionscomply with agreed eligibility criteria

IPAB's FINANCING

The Mexican authorities haveindicated their intention to ensure thestabilization of IPAB's debt in realterms. To achieve this purpose, theBudget Proposal for 2000, submittedto Congress, includes a budgetaryallocation of M$35.0 billion to IPAB

The Borrower will transfer theproceeds of each tranche of the Bankloan to IPAB to help finance IPAB'scash-flow needs resulting from thebank resolution transactions thatcomply with eligibility criteria

5. SALE/RECOVERY OF BANK ASSETS HELD BY IPABTo recover the IPAB has already initiated the Second Tranche Actionsmaximum amount auctioning of packages of bank assets * That IPAB's Asset Disposal Program hasfrom the bank assets under its 1999-2000 Asset Recovery been implemented on a consistent basis, inunder IPAB's Program accordance with its termspurview, within the * In 10/99 IPAB auctioned thetime frame provided administration of the bad loans of Third Tranche Actionsby the IPAB Law Serfin * That IPAB's Asset Disposal Program has

been implemented on a consistent basis, inaccordance with its terms

Notes:1. Eligible notes means notes (instrumentos de credito) issued by IPAB for partial financing of an eligiblebank restructuring transaction. These notes must pay in cash at least the real component of the interest rate.2. Eligible bank resolution transactions means the sale, merger or liquidation of any of the following bankinginstitutions: Serfin, Bancrecer, Promex, Atlantico and Inverlat, carried out in accordance with the eligibilitycriteria described in Attachments Bl, B2, B3, B4 and B5 of the Implementation Letter.3. Eligible notes means notes (instrumentos de credito) issued by IPAB for partial financing of an eligiblebank restructuring transaction. These notes must pay in cash at least the real component of the interest rate.4. Eligible bank resolution transactions means the sale, merger or liquidation of any of the following bankinginstitutions: Serfin, Bancrecer, Promex, Atlantico and Inverlat, carried out in accordance with the eligibilitycriteria described in Attachments Bl, B2, B3, B4 and B5 of the Implementation Letter.

- 29 -

Additional Annex 9. Regulatory Reforms, First Stage of Bank Restructuring Program

Re ulatory Reforms Im lemented in the First Stage of the Bank Restructuring Program

New Rules Norm Issued/In Rule Content Implementationeffect

Definition of SHCP 10/1999 New definition of Tier 1 and Tier 2 Some banks have alreadyregulatory Resolution 01/2000 - elements. adopted in full these rules.capital 12/2002 New capital instruments.

Substitution of specific provisionsby general provisions.Limit of 20% for deferred taxes.Deduction of equity investmentsand intangible assets.New weighing rules for off-balancesheet items.

Credit portfolio Circular 10/1999 Classification methodology based Regulations have notclassification 1449 01/2000 on the probability of entailed the necessity ofrules for credit non-repayment. additional provisions, butcard loans New provisioning rules. they have resulted in the

earrnarking of existingprovisions to specific credits.

Credit portfolio Circular 01/2000 Classification methodology based Regulations have notclassification 1460 06/2000 on repayment performance and entailed the necessity ofrules for probability of default. additional provisions, butmortgages New provisioning rules. they have resulted in the

earrnarking of existingprovisions to specific credits.

Credit portfolio Circular 09/2000 Classification methodology entailsclassification 1480 01/2001 comprehensive credit risk analysis,rules for including country risk, for both thecommercial loan and the creditor.loans Quarterly classification and

provisioning of 80% of the creditportfolio, including every operationabove certain amount, based on theprobability of default.The remaining 20% to be classifiedand provisioned according to therepayment experience.New rules for guarantees.Disclosure of credit classification.Risk categories increase from 5 to7.

Accounting Circular 10/1999 New accounting standards for assets As of June 2000 the banksand valuation 1448 01/2000 securitization and assets transfer. had carried out valuations ofrules for banks New and enhanced valuation rules, their premises and adjusted

according to international standards their capital accordingly.Full implementation of newvaluation rules is likely totake place in 2001, once theappraisal of foreclosed assetsis completed.

- 30 -

Transparency Circular 1448 10/1999 Disclosure of components of Some banks relinquishedand disclosure regulatory capital starting 12/2000. regulatory forbearance to

Disclosure of regulatory prevent its disclosure in theforbearance, including its impact on 12/2000 reports.the financial conditions, starting

Circular 1484 12/2000.10/2000

Refines some prudential supervisoryCircular 1488 norms and hence improve financial

information and disclosure.Regulatory Circular 10/1999 Forbearance conditioned to the The CNBV has allowedforbearance 1448 existence of a comprehensive forbearance in special cases,

rehabilitation plan. which have beenMandatory disclosure, including its communicated to the bankseffect in financial statements. and disclosed to the banks,

the market and the CNBV.Accounting Circular 12/1999and valuation 1456 01/2000rules forholding Circularcompanies 1489

- 31 -

Additional Annex 10. Description of IPAB Restructuring Program at Inception

Shares of Total Assets, Dec. 1996

No IPAB11% l New

ISaneamientoOld Cap/Loan 31%8%31

OldIntervened,

New Cap/Loan 1%49%

- 32 -

Additional Annex 11. Description of Transactions Underwritten by IPAB

Shares of Total Assets, Dec. 1996

8% 11%

* Old Intervened, Sell

o New Cap/LoanE* Old Cap/Loan

8% E No IPAB

* New San. (BRFL I)49% l C New San. (BRFL 11)

1%

-33 -

Additional Annex 12. Additional Transactions Assisted by IPAB

Shares of Total Assets, Dec. 1996

11%

8% o- New Saneamiento1% 0 ts -'ieie-l .,-,\ \ *Old InteRened, Sell

-28% * Old Cap/Loan

*No IPAB2 -' ;trS6?R;,,, BBV/Bancomer

0 Other

-34 -

Additional Annex 13. Bank Credit to the Private Sector (% of GDP)

Reprinted from Yacaman (2001).

Bank Credit to thePrivate Sector (percentage of GDP)

45%

30%

15%

0%/o 1990 1992 1998 1991 1995 1999

- 35 -

Additional Annex 14. Number of Commercial Banks

Reprinted from Yacaman (2001).

Number of Commercial Banks

60 ee4inns_ F 1 IP.UI AL~~~~~~~~~~~~~~~~~~~disI

45

30

15

01980 1982 1988 1991 1995 2000

- 36 -

Additional Annex 15. Past Due Loans as Share of Total Loans

Reprinted from Yacaman (2001).

Past due loans asa share of total loans

20%

15%

10%

5%

0%1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

- 37 -

Additional Annex 16. Comments from IPAB

(original in Spanish)

1. Como resultado de la crisis fmanciera de 1995 fue necesario desarrollar mecanismos para fortalecer elSistema Nacional de Pagos y salvaguardar los dep6sitos de los ahorradores. En este sentido, el Instituto para laProtecci6n al Ahorro Bancario (Instituto) ha buscado proporcionar un adecuado Sistema de Seguro de Dep6sitosque permita ofrecer a los ahorradores una cobertura eficiente, instrumentar una estrategia de administraci6n depasivos sustentable en el largo plazo y concluir las operaciones de saneamiento pendientes.

Evaluaci6n y cumplimiento de los objetivos del Prestamo del BIRF (programa)

2. El objetivo del programa consisti6 en apoyar parcialmente las operaciones de saneamiento y/o resoluci6nque se encontraban pendientes de realizar de Grupo Financiero Serfm, S.A, Grupo Financiero Inverlat, S.A. deC.V., Banca Promex, S.A., Bancrecer, S.A., y Banco del Atlantico, S.A. Durante el afio 2000, el Institutoconcluy6 los procesos de saneamiento fmanciero de Banca Promex y Grupo Financiero Inverlat, ademis derealizar la venta del Grupo Financiero Serfm en el tiempo programado.

3. En cuanto a la administraci6n de los pasivos del Instituto, se han realizado reestructuras que permitieronmejorar las condiciones generales de algunas obligaciones en lo que se refiere a plazo, tasa y esquema deamortizaci6n. Estas acciones lograron modificar el perfil original de vencimnientos, reduciendo con ellopresiones de refinanciamiento durante el periodo 2004 - 2006. Aunado a lo anterior, con las operaciones derefinanciamiento se redujo el costo financiero del Instituto en 33 puntos base en el periodo comprendido entrediciembre de 1999 y junio de 2001. En este sentido, el cr6dito otorgado por el Banco Mundial contribuy6 a lareducci6n del costo financiero de la deuda del Instituto dadas las caracteristicas de tasa y plazo que seotorgaron.

Sustentabilidad del programa, desempeno del prestatario y actuaci6n del banco

4. La facultad del Instituto de canjear o refmanciar su deuda, el monto de recursos presupuestariosrequeridos, y los ingresos por cuotas bancarias y recuperaciones que se podrian destinar al servicio de lasobligaciones fmancieras, pernitiran mantener las obligaciones fmancieras del Instituto en una trayectoriasostenible considerando un comportamiento estable en las tasas de interes reales. En el periodo de diciembre de1999 a junio de 2001 los pasivos del Instituto disminuyeron 3.3% en terrninos reales.