world bank documentdocuments.worldbank.org/curated/en/345681468913813477/pdf/multi... · bangladesh...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 3245

PROJECT PERFORMANCE AUDIT REPORT

BANGLADESH:

CHITTAGONG WATER SUPPLY PROJECT

(CREDIT 367-BD)

AND

DACCA WATER SUPPLY AND SEWERAGE PROJECT

(CREDIT 368-BD)

December 29, 1980

Operations Evaluation Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OFFICIAL USE ONLY

PROJECT PERFORMANCE AUDIT REPORT

BANGLADESH: CHITTAGONG WATER SUPPLY PROJECT (CREDIT 367-BD) AND DACCAWATER SUPPLY AND SEWERAGE PROJECT (CREDIT 368-BD)

TABLE OF CONTENTS

Page No.

Preface ...........................................................Project Performance Audit Basic Data Sheets

Credit 367-BD ................................................ iiiCredit 368-BD ............................................... ivCredit 41-PAK ........................................................... vCredit 42-PAK ............................................... vi

Highlights ...................................................... vii

PROJECT PERFORMANCE AUDIT MEMORANDUM

I. Project Summary ......................................... 1

II. Main Issues .......................... ................. 3Project Justification and Achievements - Chittagong 3Project Justification and Achievements - Dacca ... 5Unaccounted-for Water ................................... 8Financial Performance ............... .................. 8Institutional Aspects ................................... 10Covenants ....... ............... ....................... 11Supervision .............................. .............. 11

III. Conclusions ................................ ............ 12

Attachments:

PROJECT COMPLETION REPORT - CHITTAGONG

I. Introduction ........................ .................. 14II. Project Preparation and Appraisal........................ 16III. Project Implementation, Operation and Cost .............. 17IV. Operating Performance ....................................... 20V. Financial Performance ....................................... 20

VI. Institutional Performance and Development ............... 22VII. Project Justification ....................................... 22

VIII. Bank Performance ............................................ 23IX. Conclusions ................................................ 23

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Table of Contents (Cont'd)

Page No.Annexes

1. Disbursements ........................................ 262. Income Statement 1974-1979 .............................. 28

Balance Sheet Summary 1975-78 ....................... 293. Charges for Water ..................................... 304. Training Provided under Credit 367-BD ................... 31

PROJECT COMPLETION REPORT - DACCA

I. Introduction .......................................... 32II. Project Preparation and Appraisal ....................... 34

III. Project Implementation, Operation and Cost .............. 35IV. Operating Performance ....................................... 39V. Financial Performance ....................................... 39

VI. Institutional Performance ............................ 41VII. Project Justification ................................... 41

VIII. Bank Performance ...................................... 42IX. Conclusions .. ...................................... 42

Annexes

1. Disbursements ....................... .................. 44

2. Population, Water Production and Consumption .......... 463. Charges for Water ....................................... 474. Income Statement Summary 1975-1978 ...................... 48

Balance Sheet Summary 1975-1978 ......................... 495. Training Provided under Credit 368-BD ................... 50

Abbreviations used

PCR = Project Completion ReportPCRC = Project Completion Report, ChittagongPCRD = Project Completion Report, DaccaWASACH = Water and Sewerage Authority, ChittagongWASADC = Water and Sewerage Authority, DaccaPPAM = Project Performance Audit MemorandumPPAR = Project Performance Audit ReportIMg = million Imperial gallonsIMgd = million Imperial gallons per dayIgd = Imperial gallon per day

- 1 -

PROJECT PERFORMANCE AUDIT REPORT

BANGLADESH: CHITTAGONG WATER SUPPLY PROJECT (CREDIT 367-BD) AND DACCAWATER SUPPLY AND SEWERAGE PROJECT (CREDIT 368-BD)

PREFACE

This report presents the results of a performance audit of theChittagong and Dacca Water Supply and Sewerage Projects in Bangaladesh, forwhich Credits 367-BD and 368-BD were approved in March 1973 in the sum ofUS$7.0 million and US$13.2 million, respectively. The credits permittedcontinuation of the projects previously financed under Credits 42-PAK and41-PAK which had been approved in August 1963. Credits 367-BD and 368-BDwere closed in February 1979.

The Project Performance Audit Report consists of a combined ProjectPerformance Audit Memorandum (PPAM) for the two projects, prepared by theOperations Evaluation Department (OED), a Project Completion Report for theChittagong Water Supply Project (PCRC), and a Project Completion Report forthe Dacca Water Supply and Sewerage Project (PCRD). The two PCRs were pre-pared by the South Asia Regional Office, taking into account reports writtenby WASACH, WASADC and their consultants. The two projects have been covered

in a combined PPAM since they were parallel efforts with common objectives; in

the event, the projects have also faced very similar experiences and problemsand they both give rise to a set of similar lessons learned.

OED has reviewed the PCRs, the Appraisal Reports of the revisions of

the original projects in Chittagong and Dacca (Nos. TO-369d and TO-363d

respectively, dated September 27, 1968), the President's Report on the two

projects (No. P-1203-BD), dated March 10, 1973, and the Credit Agreements,dated April 9, 1973. Correspondence with the Borrower and internal Bankmemoranda on the projects' issues, as contained in relevant Bank files,

have also been consulted and discussions with Bank staff associated with the

two projects have been held.

An OED mission visited Bangladesh in August 1980 and discussed

the main issues with officials of the Ministry of Local Government, Rural

Development and Cooperatives, the Ministry of Planning, External Resources

Division, and the two executing agencies. The mission also visited some of

the project facilities. The valuable assistance provided by the Government of

Bangladesh and the two WASAs is gratefully acknowledged.

On the basis of the review of project documents and the discussions

described above, OED is generally in agreement with most of the principalanalysis and conclusions in the PCRs. However, in the view of the audit, it

is not possible to assess adequately the achievements under the two projectson the basis of the discussion in the PCRs. In particular, the progress made

- ii -

under the original credits for the two projects (41-PAK and 42-PAK) and theobjectives set out at the time of reactivation of the projects in 1973 are notidentified sufficiently in the PCRs, although they are crucial referencepoints for an assessment of the achievements under Credits 367-BD and 368-BD.Aside from the issue of the projects' achievements, the PPAM comments on fourother principal issues which are not dealt with adequately in the PCRs:unaccounted-for water, financial performance, institutional problems andcovenants. Finally, the PPAM introduces a comment on supervision and adds anumber of lessons learned.

Following normal OED procedures, a draft copy of this report wassent to the Government and the two WASAs for comments. While no writtencomments were received, the views of the Government and the two WASAs on themain project issues, which were discussed with OED staff during the OEDmission of August 1980, have been taken into account in finalizing the report.

(iii)

PROJECT PERFORMANCE AUDIT BASIC DATA SHEET

BANGLADESH: CHITTAGONG WATER SUPPLY PROJECT

(CREDIT 367-BD)

KEY PROJECT DATA

Item Appraisal Actual

Expectation

Total Project Cost (US$ million) 9.1 16.5

Overrun (%) 81

Credit Amount (US$ million) 7.0 7.0

Disbursed 7.0 7.0

Date for Completion of Physical Components 12/31/74 2/79 1/

Proportion Completed by Appraisal Target Date (%) - 70

Proportion of Time overrun (%) 238

Incremental Financial Rate of Return n.a. n.a.Financial Performance Satisfactory Unsatisfactory

Institutional Performance Satisfactory Unsatisfactory

Cumulative Estimated and Actual Disbursements

(US$ million)

As of June 30: 1973 1974 1975 1976 1977 1978 1979

(i) Appraisal Estimate 4.1 6.0 7.0 7.0 7.0 7.0 7.0

(ii) Actual 3.5 3.8 4.6 5.1 6.1 6.4 7.0

(ii) as % of (i) 85 63 66 73 87 91 100

OTHER PROJECT DATA

AppraisalItem Expectation Actual

Board Approval 3/27/73

Credit Agreement Data 4/9/73

Effectiveness Date 6/7/73Closing Date 6/30/75 2/15/79

Borrower Peoples Republic of Bangladesh

Executing Agency Chittagong Water Supply & Sewerage

Authority (WASA)Financial Year of Borrower July 1 - June 30Follow-on Project Name Second Chittagong Water Supply Project

Credit Number 1001-BDAmount (US$ million 20.0Credit Agreement Date April 4, 1980

MISSION DATA

Item Month/Year No. of No. of Date of

- - Weeks Persons Manweeks Report

Identification ) Following a request by COB this credit was made to complete

Preparation ) works started under Credit 42-PAK prior to Bangladesh'sP a iindependence. Leading up work was covered while processing

Preappraisal ) the earlier credit.

Appraisal 7/72 1.5 3 4.5 3/10/73

Supervision 1 11/73 1 2 2 12/20/73

Supervision 2 03/74 1 2 2 04/03/74

Supervision 3 07/74 1 2 2 08/09/74Supervision 4 11/74 1 3 3 01/03/75

Supervision 5 02/75 2 1 2 03/25/75Supervision 6 05/76 1 2 2 06/07/76

Supervision 7 02/77 1.5 2 3 04/07/77Supervision 8 10/77 1 2 2 11/18/77

Supervision 9 06/78 1 2 2 09/18/78

Total 20

Country Exchange Rates

Year Currency: Taka (TK) Exchange Rate US$1 =

Appraisal year average (1973) 7.7 TK

Intervening years average 12.1 TK

Completion year average (1978) 15.5 TK

1/ The major physical components were completed by September 1977 (PPAM paras. 5 and 12).

(iv)

PROJECT PERFORMANCE AUDIT BASIC DATA SHEET

BANGLADESH: DACCA WATER SUPPLY AND SEWERAGE PROJECT

(CREDIT 368-BD)

KEY PROJECT DATA

Item Appraisal ActualExpectation

Total Project Cost (US$ million) 17.27 19.8Overrun (%) 15

Credit Amount (US$ million) 13.2 13.2Disbursed 13.2

Date for Completion of Physical Components 12/31/74 2/79 1/Proportion completed by Appraisal Target Date (%) 71Proportion of time overrun (%) 243

Incremental Financial Rate of Return (%) No forecast n.a.

Cumulative Estimated and Actual Disbursements

(US$ million)

As of June 30: 1973 1974 1975 1976 1977 1978 1979

(i) Appraisal Estimate 7.7 11.7 13.2 13.2 13.2 13.2 13.2(ii) Actual 6.7 7.4 10.7 11.5 11.8 12.8 13.2(ii) as % of (i) 87 63 81 87 89 97 100

OTHER PROJECT DATA

AppraisalItem Expectation Actual

Board Approval 3/27/73Credit Agreement Date 4/09/73

Effectiveness Date 6/07/73Closing Date 6/30/75 2/15/79

Borrower Peoples Republic of BangladeshExecuting Agency Dacca Water Supply and Sewerage

Authority

Fiscal year of Borrower July 1 - June 30Follow-on Project Name Second Dacca Water Supply and

Sewerage ProjectCredit Number 941-BDAmount (US$ million) 22.0Credit Agreement Date June 29, 1979

MISSION DATA

Item Month/Year No. of No. of Date ofWeeks Persons Manweeks Report

Identification ) Following request by GOB this credit was made to completePreparation ) works started under Credit 41-PAK prior to Bangladesh's

Preappraisal ) independence. Leading up work was covered while processingthe earlier credit.

Appraisal 7/72 1.5 3 4.5 3/10/73Supervision 1 11/74 2 2 4 12/20/73Supervision 2 3/74 1 2 2 4/15/74

Supervision 3 7/74 1.5 2 3 8/16/74Supervision 4 11/74 1 3 3 12/30/74Supervision 5 2/75 2 1 2 4/07/75Supervision 6 5/76 1.5 2 3 6/07/76Supervision 7 2/77 1.5 2 3 4/14/77Supervision 8 10/77 1 2 2 11/29/77

Supervision 9 6/78 1 2 2 9/18/78

Total 24.0

Country Exchange Rates

Currency: Taka (TK)

Year Exchange Rate US$1 =

Appraisal year average (1973) 7.7 TKIntervening years average 12.1 TK

Completion year average (1978) 15.5 TK

(v)

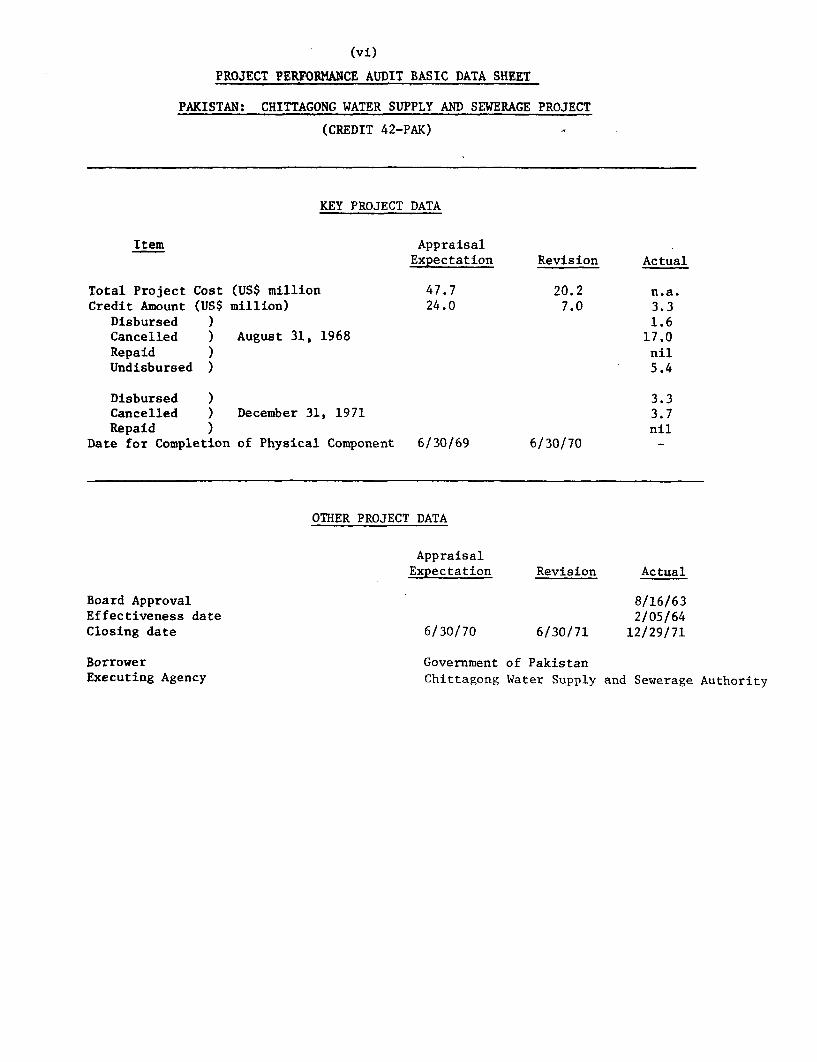

PROJECT PERFORMANCE AUDIT BASIC DATA SHEET

PAKISTAN: DACCA WATER SUPPLY AND SEWERAGE PROJECT

(CREDIT 41-PAK)

Item AppraisalExpectation Revision Actual

Total Project Cost (US$ million) 54.7 37.2 n.a.Credit Amount (US$ million) 26.0 13.2 6.0

Disbursed ) 1.4Cancelled ) August 31, 1968 12.8

Repaid ) nilUndisbursed ) 11.8

Disbursed ) 6.0Cancelled ) December 31, 1971 7.2Repaid ) nil

Date for Completion of Physical Components 6/30/69 6/30/70

OTHER PROJECT DATA

AppraisalExpectation Revision Actual

Board Approval 8/16/63Effectiveness date 3/06/64Closing date 6/30/70 6/30/71 12/29/71

Borrower Government of PakistanExecuting Agency Dacca Water Supply and Sewerage Authority

(vi)

PROJECT PERFORMANCE AUDIT BASIC DATA SHEET

PAKISTAN: CHITTAGONG WATER SUPPLY AND SEWERAGE PROJECT

(CREDIT 42-PAK)

KEY PROJECT DATA

Item AppraisalExpectation Revision Actual

Total Project Cost (US$ million 47.7 20.2 n.a.Credit Amount (US$ million) 24.0 7.0 3.3

Disbursed ) 1.6Cancelled ) August 31, 1968 17.0Repaid ) nilUndisbursed ) 5.4

Disbursed ) 3.3Cancelled ) December 31, 1971 3.7Repaid ) nil

Date for Completion of Physical Component 6/30/69 6/30/70

OTHER PROJECT DATA

AppraisalExpectation Revision Actual

Board Approval 8/16/63Effectiveness date 2/05/64Closing date 6/30/70 6/30/71 12/29/71

Borrower Government of PakistanExecuting Agency Chittagong Water Supply and Sewerage Authority

- vii -

PROJECT PERFORMANCE AUDIT REPORT

BANGLADESH: CHITTAGONG WATER SUPPLY PROJECT (CREDIT 367-BD) AND DACCAWATER SUPPLY AND SEWERAGE PROJECT (CREDIT 368-BD)

HIGHLIGHTS

The two projects provided funds to complete the expansion of thewater supply network in Chittagong and the water and sewerage systems inDacca, and replaced Credits 42-PAK and 41-PAK, respectively, under which workon the project had started. After some delays in the aftermath of the civilwar, the project works were eventually completed.

Physical achievements under the project in Chittagong fell short ofexpectations, while in Dacca they were closer to those set out at the time ofreappraisal in 1973. Institutional objectives were not achieved under eitherproject and the authorities' finances remained unsatisfactory. The projectsdid increase the water supply in both cities, from about 6 IMgd in 1973 toabout 10.5 IMgd in 1978 in the case of Chittagong, and from about 32 IMgd in1973 to about 46 IMgd in 1979 in the case of Dacca; however, water supply inthe two cities is still on an intermittent basis. The sewerage system inDacca is under-loaded due to the failure of customers to connect.

The following points are of special interest:

- justification for reactivating the projects and their physicalachievements (PCRC paras. 1.02 and 9.11, PCRD paras. 1.02 and9.09 and PPAM paras. 4,6 and 8-21);

- the problem of unaccounted-for water and the need for establish-ing a sound waste detection and prevention program (PCRs para.5.03 and PPAM paras. 23 and 36 (iv));

- problems with billing and collection of revenues, for example inthe case of public standpipes, and the effect on the authorities'finances (PCRs paras. 5.03 and PPAN paras. 25-26 and 36 (i));

- the authorities' management problems (PCRC paras. 6.01 and9.07, PCRD paras. 6.01 and 9.08, and PPAM paras. 28-31 and 36(ii-iii));

- shortcomings in accounts and audit delays (PPAM paras. 24, 32 and36(v)); and

- reasons for the unsuccessful operation of the sewerage systemin Dacca (PCRD paras. 3.11, 4.02 and 9.02, and PPAM para. 21).

PROJECT PERFORMANCE AUDIT MEMORANDUM

BANGLADESH: CHITTAGONG WATER SUPPLY PROJECT (CREDIT 367-BD) AND DACCAWATER SUPPLY AND SEWERAGE PROJECT (CREDIT 368-BD)

1. PROJECT SUMMARY

1. The two projects, as originally conceived, commenced in 1963, whenIDA extended Credits 41-PAK and 42-PAK of US$ 26.0 million and US$24.0 millionfor water supply and sewerage for the cities of Dacca and Chittagong, respec-tively, then part of the Province of East Pakistan. The credits were made to

the Government of Pakistan, the funds were made available to the Province ofEast Pakistan, which in turn onlent the amounts to Dacca and Chittagong Water

Supply and Sewerage Authorities (WASADC and WASACH, respectively). Bothagencies were established as a condition of effectiveness under the two credit

agreements of 1963. Since then, the projects have been characterized by aseries of problems and originally proved to be too ambitious in relation to

the country's immediate needs, resources and capabilities, requiring a toorapid expansion of Dacca's and Chittagong's water supply and sewerage system.

Consequently, revisions to the credits were appraised in 1968, the projectswere reduced in scope and the two credits were reduced to US$ 13.2 million(Dacca) and to US$7.0 million (Chittagong). Most investments in long-termcapacity which would not be fully utilized within the next few years wereeliminated, including the sewerage component of the project in Chittagong.

2. After the revision in 1968, the principal project components inDacca were: provision of 26 new large tubewells, construction of elevatedtanks, modifications of an old surface water plant, distribution pipes, 1,500

new or rebuilt public street hydrants, 15,000-20,000 new house connections,construction of lateral and main sewers, construction of pumping stationsand provision for 8,000-14,000 new sewer connections (PPAM para. 15). Theprincipal project components in Chittagong after the revision in 1968 were:the construction of a surface water treatment plant, development of water from

about 13 tubewells, iron removal facilities, a booster pumping station, a

storage reservoir, distribution pipes, 800-1,000 new or rebuilt public stand-pipes and 10,000-12,000 new house connections (PPAM para. 8). The revisedprojects were estimated to cost US$37.2 million (Dacca) and US$20.24 million(Chittagong), including expenditures already made, resulting in a total proj-ect cost reduction of about 32% in Dacca and 58% in Chittagong compared to

the original projects. The new closing date for both credits was set at June

30, 1971, one year later than the completion goal and the original closing

date.

3. Progress was made on the revised projects until the internal strifebroke out in 1971 in what is now Bangladesh. On December 29, 1971, IDA, in

consultation with the Government of Pakistan, suspended disbursements underboth credits. By this time, US$7.2 million remained undisbursed from Credit

41-PAK and US$3.7 million from Credit 42-PAK. The war seriously disrupted the

- 2 -

implementation of the projects and no foreign currency was available fromDecember 29, 1971 until June 1972 when Sweden agreed to provide an interimcredit to finance urgent expenditures under these two projects and otherinterrupted IDA projects. In August 1972, Bangladesh became a member of theIMF, the Bank and IDA. The two projects were reactivated on March 27, 1973under Credit 367-BD and Credit 368-BD for the same amounts as under the formerCredits 42-PAK and 41-PAK, respectively. Of the US$7.0 million under Credit367-BD, US$3.3 million was to be used to repay IDA for amounts withdrawn underthe cancelled credit (42-PAK), leaving US$3.7 million to complete the projectin Chittagong and to reimburse Sweden for disbursements made under the interimfinancing arrangements. From the proceeds of the US$13.2 million under Credit368-BD, US$6.0 million was to be used to reimburse IDA with respect to Credit41-PAK, and about US$0.7 million was to be used to meet commitments forservices performed prior to the suspension of the credit, leaving US$6.5million to complete the project in Dacca and to reimburse Sweden.

4. The reactivated projects were justified on the grounds that com-pletion of the physical works which had started under Credits 41-PAK and42-PAK was necessary in order to satisfy the rapidly growing demand for waterin Dacca and Chittagong and to avoid a deterioration in public health con-ditions (PPAM paras. 10-11, 16 and 18). In Chittagong, work had not startedon construction of the treatment plant and the reactivated project includedprovision only for its detailed design. On the other hand, provision was madefor additional mains and distribution pipes (PPAM para. 10). In Dacca, onestorage tank was eliminated, but provision for 20 additional tubewells,distribution pipes, sewers, and one pumping station was included in thereactivated project (PPAM para. 17). The important institutional objective ofthe original credits was retained, namely, to establish the two WASAs asefficient and viable commercial undertakings. No incremental financial ratesof return were calculated in 1973 or at the time of the audit. Forecasts ofwater and sewerage demand also were not made in 1973 but it is clear that theadditional water production envisaged under the projects was needed and thatsewerage services would help improve the existing sanitary conditions.

5. The reactivated projects in Chittagong and Dacca were expected tocost US$9.1 million and US$17.3 million, respectively, to complete. Actualcosts are now estimated at about US$16.5 million for Chittagong and US$19.8million for Dacca, i.e. overruns of 81% and 15% respectively, due mainly tothe extended duration of the implementation period for the two projects (PCRsparas. 3.08-3.09). The expected completion date was December 31, 1974 and thecredits were to be closed on June 30, 1975. In fact, the credits were notclosed until February 1979, although the major physical components of theprojects were in service by September 1977 and mid-1978 for Chittagong andDacca respectively (PCRC paras. 3.02-3.03, 3.10 and 4.01 and PCRD paras. 3.02,

- 3 -

3.11 and 4.01-4.04). The implementation delay was caused mainly by procure-ment delays and managerial, financial and technical problems 1/.

6. With the completion of the projects, Chittagong's water supplyincreased significantly, from 2 IMgd in 1963 to about 6 IMgd in 1973 and 10.5IMgd in 1978. In Dacca, the water supply increased from about 32 IMgd in 1973to about 46 IMgd in 1979, although the per capita supply of water has de-creased during the same period due to the high population increase. Physicalachievements under the project in Chittagong fell short of expectations whilein Dacca they were closer to those expected at reappraisal in 1973. Institu-tional achievements under both projects were disappointing and the two WASAs'financial, management and staffing situation remains weak and requires a greatdeal of further improvement (PPAM paras. 25-27 and 29-31). Several covenantswere not observed, although the application of an audit covenant, requiringthe submission of audited financial statements to IDA by June 30, 1973, wasprobably not realistic in view of the two WASAs' known weaknesses in account-ing and finance (PPAM paras. 24 and 32). With the completion of the projects,80% of Chittagong's population and 75% of Dacca's have access to safe watercompared to 100% estimated in 1973, but the supply is on an intermittentbasis. The sewerage system in Dacca is underloaded due to the low demand fromthe public for connections (PCRD para. 3.11). Unaccounted-for water is at afairly high level (PPAM para. 23). In the view of the audit, however, it isnot clear that additional supervision could have resulted in better achieve-ments under the two projects (PPAM para. 33).

7. A number of lessons have emerged from the experience of the twoprojects, both of a detailed and general nature. Several of these lessonshave been applied in the follow-on projects to Dacca and Chittagong (Credits941-BD and 1001-BD), which were approved in June 1979 and March 1980, respec-tively (PPAM para. 36, PCRC paras. 9.01-9.11' and PCRD paras. 9.01-9.09).

II. MAIN ISSUES

Project Justification and Achievements - Chittagong

8. After the revision to the project was made in 1968 and the creditwas reduced to US$7.0 million, the project included: (i) the construction ofa surface water treatment plant and a scheme to collect and divert industrial

1/ With regard to procurement, WASADC has expressed the view that having tosend the bidding documents to Bank headquarters for approval was afactor causing delays. It was suggested that the availability of aprocurement expert, at the Bank's resident mission in Dacca, with theauthority to approve procurement matters, would have shortened theimplementation period of the project.

wastes away from the intake areas; (ii) development of ground water from awell-field at Kalurghat, comprising about 13 tubewells plus iron removalfacilities and a booster pumping station; (iii) about 72 miles of water dis-tribution pipes, a 6 IMg storage reservoir, 800-1,000 new or rebuilt publicstandpipes and about 10,000-12,000 new water connections; and (iv) provisionfor engineering and management consulting services, a training program,equipment, tools, workshops, and stores facilities.

9. When the project was reactivated in 1973, the major justificationwas to complete the physical work that had already started under Credit42-PAK. Despite the serious political disturbances in 1971, considerableprogress on the project had been made and about 60% of the work had beenexecuted. Ten wells had been drilled of which five were in service and thetransmission mains and distribution pipes were in use. The iron removalfacility and booster pumping station were under construction. About 700public standpipes had been installed although only 50% of them had beenconnected to the distribution system. About 2,000 house service connectionshad been made of which 1,870 were metered. All major contracts under theproject revised in 1968 had been awarded except for the 6.0 IMg storagereservoir and the surface water treatment plant. Land had been purchased forthe water treatment plant and some site development work was underway.

10. The reactivated project in 1973 aimed essentially at completingthe works envisaged in 1968, with the exception of the treatment plant. Thereactivated project provided only for the preparation of detailed design forthis plant and its related facilities; actual construction was to be deferredto the next stage of the program. On the other hand, 33 additional miles ofmains and distribution pipes were to be installed, increasing the pipes to befinanced from the credit to about 105 miles (including the 72 miles alreadylaid).

11. No revised demand forecasts were made in 1973, but it was pointedout that water demand had been increasing rapidly in Chittagong due to anincrease in population, and industrial demand was expected to increase appre-ciably as Chittagong's importance as a port increased. Without the project,it was argued, water demand could not be met and the existing water supplywould deteriorate further, with part of the population having to use watersources that posed a continuing health hazard. With the project, continuouson-premise water service would be possible to about 70% of the population andthe remaining 30% would be served by public standpipes.

12. The reactivated project, approved by the Board in March 1973, wasto be completed by December 31, 1974, with the closing date of the creditfixed for June 30, 1975. In the face of a number of managerial, technical andfinancial problems, the project was not completed until early 1979, althoughthe major physical elements were completed and in service by September, 1977,about 33 months later than envisaged. However, in mid-1978, some US$500,000of the credit, relating to equipment, vehicles, spare parts and meters, stillremained undisbursed. To permit disbursements on these outstanding items, thecredit was eventually closed in February 1979.

-5-

13. Actual achievements under the project fell short of expectations.With completion of the project, production from the tubewells at Kalurghataveraged 8.5 IMgd in FY78 compared with 10.5 IMgd envisaged at appraisal.Water production from the tubewells has been reduced by power outages and byiron deposits in the pumps and pipes while the iron removal plant suffers fromdesign faults (PCRC paras. 3.10 and 4.01); however, the follow-on project isfinancing design modifications to the iron removal plant and is making provi-sion for standby generating plant to counteract power outages. WASACH hasalready introduced a program for cleaning iron deposits from the tubewells(PCRC para. 4.01 and 9.03). The capacity of the reservoir was reduced to 3IMgd (PCRC para. 3.05); the reasons for the reduction are related to the factthat water production was lower than originally envisaged and the fact thatthe project as a whole was experiencing cost overruns. A design for thesurface water treatment plant and related facilities was finished in early1974, but by then the project was already falling about two years behindschedule and the original. master plan on which the design was based wasoutdated. A new design study was included in the feasibility studies for theSecond Chittagong Water Supply Project, which is financing construction of thetreatment plant l/. It appears that the US$200,000 provided under thereactivated credit to finance the original design did not play any useful rolein preparing the feasibility studies for the second project.

14. By mid-1978, the number of public standpipes had reached the lowerend of the range envisaged in 1973 (800) but the number of new connections(3,400) fell far short of the target (10,000-12,000). The project has in-creased water production from about 2 IMgd in 1963 to about 6 IMgd in 1973and about 10.5 IMgd in 1978, and the water supplied from the Kalurghat fields(80% of total supply) is available to the city for 24 hours a day; watersupplied from the city's old wells is still on an intermittent basis. Around20% of Chittagong's population does not have access to safe water, while theproject aimed at securing 100% coverage V. Some 18% is supplied throughhouse connections (compared to 70% expected at appraisal), 50% is suppliedthrough public standpipies (compared to 30% expected at appraisal) and 12% issupplied by employers from private sources.

Project Justification and Achievements - Dacca

15. The original project, as financed under Credit 41-PAK, was basedon the use of water from the Lakhya River, requiring a heavy initial invest-ment. By 1966 there had been sufficient investigation on the utilizationof ground water sources in the vicinity of Dacca to demonstrate that properly

1/ The feasibility studies were financed under technical assistanceCredit 622-BD.

2/ Chittagong's population has grown from 550,000 in 1972 to its presentlevel of about 600,000.

- 6 -

constructed tubewells in and around the city could be expected to meet Dacca'swater requirements more economically in the near future. Consequently, afterthe project was revised in 1968 and the credit was reduced to US$13.2 million,the project included: (i) the provision of 26 new large tubewells; (ii)improvements and modifications of an old surface water plant to double itscapacity (to about 5 IMgd); (iii) about 114 miles of distribution piping,three 1.0 IMg high level elevated tanks and modification of most of the lowlevel tanks, 15,000-20,000 new connections, 21,000 -34,000 meters, and 1,500new or rebuilt public street hydrants; (iv) 100 miles of lateral and mainsewers and modification and repairs of the old sewers; (v) construction ofseven small pumping stations and a main pumping station including treatmentworks; (vi) provision for 8,000-14,000 new sewerage connections; and (vii)engineering and management consulting services, a training program, equipment,tools, workshops and stores facilities.

16. As in the case of Chittagong and Credit 42-PAK, the major justi-fication for reactivating the Dacca project in 1973 was to complete thephysical work which had already started under Credit 41-PAK. Also, likeChittagong, considerable progress had been made on the Dacca project by thetime the credit was reactivated in 1973. All the 26 tubewells had beendrilled, of which 15 were in operation and the distribution pipes were in use.Equipment for the modification of the old surface water treatment plant hadbeen delivered and the work on rehabilitation was starting. The three highlevel 1.0 IMg elevated storage tanks were about 95% completed. About 11,000new connections had been made for a total of about 28,000 of which about12,000 were metered. However, no progress had been made on improving thepublic. street hydrants and the sewerage component of the project had notprogressed as well as the water supply component. About 40% of the laterals,main sewers and intermediate pumping stations had been completed. The mainlift station and treatment facilities were about 70% completed and about 2,400new connections had been made.

17. The reactivated project remained basically the same as providedfor in 1968. However, in order to meet the water needs of new areas notpreviously the responsibility of WASADC and to meet the increasing domesticand industrial demand, the number of tubewells was increased from 26 to 46 and55 additional miles of distribution pipes were to be installed, increasing thepipes to be financed from the credit to about 169 miles (including the 114miles already laid). The length of lateral and main sewers was increased from100 miles to about 150 miles, the number of pumping stations was increasedfrom seven to eight, and about 12,000 new connections were to be installed,including the 2,400 already made.

18. As in Chittagong, no revised demand forecasts were made in 1973.However, the demand for water and sewerage services was expected to continueto increase since Dacca was the capital of an independent country as well asthe main government, commercial and business center. It was further pointedout that unless both parts of the project were completed, the existing sani-tary conditions would deteriorate with definite adverse implications with

- 7 -

regard to the public health of the city. With the completion of the project,continuous on-premise water service would be possible to about 70% of thepopulation, with the rest being served by public hydrants, and sewerageservice was expected to be available to about 60% of the population.

19. The reactivated project, approved by the Board in March 1973,was to be completed by December 31, 1974, with the closing date set forJune 30, 1975. Due to a number of managerial and financial problems, themajor physical elements of the project were only completed by mid-1978,about 42 months later than envisaged. To permit disbursements for materialsand spare parts requiring foreign exchange, the credit was eventually closedin February 1979.

20. Actual physical achievements in Dacca were close to expectations.48 tubewells were constructed under the project compared to 46 envisaged in1973, but production of water from these wells has been reduced by sand enter-ing the wells and by power outages (PCRD paras. 4.01-4.02). However, withcompletion of the project, production of water has increased from an averageof about 32 IMgd in FY73 to about 46 IMgd in FY79. No forecasts were providedat the time the project was reappraised in 1973. The modification of the oldtreatment plant was completed by late 1978 and all water lines provided underthe project had been laid by early 1977. Construction of the three elevatedstorage reservoirs was completed in early 1977, but due to the greater demandfor water than the system is able to supply, the reservoirs are not being used(PCRD para. 3.11). By mid-1978, about 1,400 standpipes were in operationcompared to 1,500 envisaged in 1973, and the number of new connections (about25,000) exceeded the target (15,000-20,000). In spite of the increase inwater production, the per capita supply of water has decreased from about 21Igd in 1973 to about 19 Igd in 1979 illustrating the fact that extensions tothe water supply system failed to keep abreast of the population increaseduring the same period Y'. Although the quality of the water is good, cer-tain areas of the old city, especially at the extremities of the local distri-bution systems, are receiving inadequate supplies due to very low mainspressures. About 25% of Dacca's population is without convenient access tosafe water, while the project aimed at securing 100% coverage 1/. Some 66%is supplied through house connections (compared to 70% expected at appraisal)and 9% is supplied through public standpipes, compared to 30% expected atappraisal.

21. The sewerage system was completed by the end of 1977. It wasfundamentally unchanged from what was envisaged in 1973, with the exception ofthe mileage of sewers which was reduced from 150 to 120. By the time thiscomponent of the project was completed, only 8,500 customers had sewer con-nections compared to about 20,500 envisaged in 1973, although the trunk

1/ Dacca's population has grown from about 1.0 million in 1973 to about2.3 million in 1978 (latest available estimate), a much faster ratethan expected.

- 8 -

sewerage system covers about 75% of the city's total area. The low connectionrate was partly due to WASADC not pursuing a vigorous connection program andthe fact that many of the potential customers were unwilling to meet theexpense of a connection because they did not fully appreciate the need forimproved sanitation and were content to continue using septic tanks or opendrains along the edges of the street (PCRD paras. 3.11 and 4.01). WASADCrecognizes that connections to the sewer system must be increased and hasstarted to accelerate sewer connections for properties or households within100 feet of a sewer. As an incentive to connect to the sewerage system,WASADC is charging sewerage fees whether or not a household is actuallyconnected.

Unaccounted-for Water

22. High unaccounted-for water was noted at the time the credits werereactivated and it was hoped that improvements in operation would help reducethe gap between water produced and sold. A meter repair shop was implementedin both Dacca and Chittagong under the projects, all new service connections(excluding public standpipes) were metered, and a program to install meters onexisting connections was implemented with some success. It should be noted

that, by early 1980, all the existing water connections in Chittagong had been

metered while about 34% of all the water connections in Dacca were stillunmetered.

23. For 1979, the two WASAs estimated that their total system lossesrepresented about 34% of production in Chittagong and about 22% in Dacca I/.Furthermore, water sales accounted for only about 50% of water produced inChittagong and 43% in Dacca during the 1974-1979 period (PCRs para. 5.03). The

high level of unaccounted-for water has resulted in the loss of substantial

amounts in revenues for the two WASAs and can partly be explained by theinefficiency in billing and meter reading; a large number of the meters aredefective; repairs of meters were slow; none of the public standpipes weremetered as of June 1978; excessive consumption by unmetered customers is notdiscouraged; and no assistance in waste detection techniques and surveys wasprovided under the two credits. The two WASAs are now making an effort toestablish sound waste detection and prevention programs which are requiredunder the follow-on IDA-financed water projects to Chittagong and Dacca.

Financial Performance

24. The two WASAs have had a long history of serious financial andaccounting problems, including an inability to achieve a satisfactory standard

of financial viability, lack of timeliness and accuracy in financial reports,

lack of financial control, poor collection performance and defects in basic

record keeping. Because of the lack of reliable information, no financial

forecasts were made at the time the two credits were reactivated in 1973.

1/ The latter estimate must be assumed to be conservative in view of theinsufficient metering.

-9-

However, a thorough review of the two authorities' accounts as of June 30,1972 was to be carried out by competent auditors and made available to IDAby June 30, 1973. This requirement formed one of the covenants under bothcredits. It was hoped that the audited statements would provide a firmbasis for reviewing the water rates and setting future financial targets.Furthermore, the Government was to cause the two WASAs to set and maintain newrates for water supply and sewerage services by December 31, 1974 (PCRC para.2.06 and PCRD para. 2.07).

25. The financial performance of the two WASAs remained unsatisfactoryin each of the years since the credits were reactivated. In spite of threetariff increases between FY74 and FY79, WASACH incurred an operating deficitin each year since 1974 while WASADC was able to generate a low operatingsurplus from FY76 onwards (PCRs paras. 5.01-5.03). Prior to FY76, it wassometimes necessary for the two WASAs to use government funds advanced forcapital works expenditures to meet operational expenses. The Governmentappears to have been sometimes unaware of this, and the auditor did not alwaysdraw attention thereto. Billing and collection, notably related to publicstandpipes (PCRs para. 5.03), remained unsatisfactory and the two WASAs havebeen slow to resort to disconnection.

26. The Bank made numerous representations to the two WASAs and theGovernment about the seriousness of the financial position of the two author-ities. In order to meet the rate covenant under the two credits, financialtargets were set as a condition for extension of the closing dates. The Bankalso considered cancelling the credit if the Government did not take satisfac-tory steps to end default on the financial covenants by June 30, 1976. AnAction Program was agreed upon in mid-1976 to improve the financial viabilityof the two WASAs. The program had some positive results, for example, tariffswere increased in July 1976 and January 1978, and Government loans were con-verted to equity in 1976. However, the Government has been slow in clearingits accounts with the two WASAs. At June 30, 1979 (a few months after the twocredits were closed), accounts receivable at WASACH were estimated at Taka15.7 million, which were equivalent to about 13 months billings, the Govern-ment sector being responsible for about Taka 8.9 million (57%). All remainingarrears are to be settled by the Government prior to disbursement of thesecond credit (1001-BD) to Chittagong which includes a covenant whereby theGovernment is to pay all future water bills within 30 days. The authority inDacca was successful in reducing its accounts receivable from about Taka41.6 million (13 months billings) at the end of FY78 to Taka 24.9 million(about 9 months billings) at the end of FY79. The reduction in the accountsreceivable position reflects the payment of outstanding Government bills priorto approval of the second credit (941-BD) which was signed in June 1979.

27. The two authorities' poor performance reflected partly the socialand economic conditions of the country, but the understaffing of qualifiedaccountants in the two WASAs and the absence of a senior financial manager inWASACH for more than three years, were serious drawbacks. Since both reap-praisal missions in 1972 recognized that the WASAs had serious financial and

- 10 -

accounting problems, it would have been reasonable to have included in thetwo credits some provision for the finance of experts in the financial andaccounting fields. Although the two credits did provide for training foraccountants, the appointment of qualified experts, working within the organi-zation, could also have served as an effective on-the-job training medium.

Institutional Aspects

28. The two WASAs were established under the East Pakistan Water Supplyand Sewerage Authority Ordinance of 1963 as a condition of effectivenessunder the original Credit Agreements (Credits 41-PAK and 42-PAK). Theyare responsible for the construction, operation and maintenance of water andsewerage works and other facilities relating to environmental sanitation inthe Dacca and Chittagong metropolitan areas.

29. Immediately upon their establishment, the two WASAs assumed respon-sibility for consolidating and operating on commercial lines the very poorwater supply systems that existed in both Dacca and Chittagong and, at thesame time, they each attempted to carry out a large project. There was nostaff background or capacity for properly contending with these new responsi-bilities. The magnitude of the problems should have been anticipated by IDAand appropriate allowances made for them, particularly in the financial areaand the timing and size of the projects.

30. Even after the projects were reduced in scope and the credits werereactivated in 1973, the WASAs performance remained unsatisfactory in allactivities. The social and economic situation of the country had adverseeffects on the WASAs (PCRs para. 6.01). Key staff left and the authoritieshad difficulties in hiring qualified staff. The financial management andoperations of the two WASAs were neglected, particularly in Chittagong, wherethe position of Commercial Manager who normally functioned as the ChiefFinancial Officer was vacant for more than three years. Consequently, therewas no individual during this period with the authority and the requiredqualifications to oversee and coordinate WASACH's financial operations and toadvise on financial matters in general. Both WASAs have had difficulties inattracting qualified accountants, though training in this area was provided.Recruitments for higher level posts appear to have been partly hampered by thecontrol of salary levels which are tied to civil service scales.

31. The two WASAs have relied heavily upon foreign technical consultantsfor many years to do even routine work, although some improvements haverecently been noticed, particularly in Chittagong. This undue dependence hasresulted in unnecessarily high foreign exchange expenditures and deprivedWASAs' staff, particularly in the earlier years, of the opportunity to trainfor and perform more interesting work. However, funds for the training ofstaff were provided under the two reactivated credits, including advancedstudies for WASAs engineers and accountants in the U.S.A., the Netherlands,and U.K., and on-the-job training with a water utility in Singapore. Most ofthis training was directed at the upper levels of the organization, although

- 11 -

some was given at the operational level. In consequence, the WASAs' perfor-mance has suffered in that they have lacked trained mid-level managerial,financial and technical staff. In the follow-on projects financed by IDA, a

training element is included, which is directed principally at the operationalstaff, including the development of an in-house training capability. Trainingin commercial and financial management is also included. It is aimed atproviding a foundation for further institutional development.

Covenants

32. Several covenants included in the two credit documents were notobserved. Reference has already been made to the WASAs' failure to complywith the rate covenant (PPAM para. 26). Furthermore, audited reports werenever received on time. Delays in appointing the auditors, combined withdelays by the two WASAs in preparing the accounts for audit, prevented submis-sion of audited accounts to IDA within the required six months of the author-ities' financial year-end. The two credit agreements required the WASAs totake out and maintain insurance against such risks as would be consistent withsound public utility practice. Until recently, the WASAs had made no arrange-ments for such insurance. The Bank made repeated representations on thesematters and under the Second Chittagong Water Supply Project, WASACH isrequired to appoint auditors prior to the start of each fiscal year whileunder the Second Dacca Water Supply and Sewerage Project, appointment ofauditors is required at the start of each fiscal year. A self-insurance fundwas established by WASACH prior to negotiating the second credit. WASADC ispresently investigating the relative merits of either establishing a fund forself-insurance or of entering into insurance contracts with the nationalinsurance company.

Supervision

33. In retrospect, it is not clear that more intensive or more frequentsupervision would have resulted in better achievements under the two projects,given the absence of reliable financial and operating data and the generalconditions prevailing in the field. Useful assistance was given by theBank's resident mission; supervision missions took place at average intervalsof six months, which is in line with normal Bank practice, and indeed thefrequency averaged four months until early 1975. There was a lack of con-tinuity of Bank staff in the earlier years, due to frequent personnel changes,but it is not apparent that this handicapped significantly the implementationof the two projects. Certainly the Action Program introduced as a directresult of the Bank's supervision work contributed towards improving thefinancial position of the two WASAs and expedited completion of the projects(PPAM para. 26). The audit notes that the WASAs appreciate, in particular,the technical assistance which they received from the Bank's supervisioneffort.

- 12 -

III. CONCLUSIONS

34. The two projects, as originally conceived in 1963, were too ambi-tious in relation to the country-s immediate needs, resources and capabilitiesand were, consequently, substantially revised in 1968. Following seriouspolitical disturbances, the projects were reactivated in 1973 and eventuallycompleted in mid-1978 and early 1979. This unusually long implementationperiod for the two projects should be seen against the difficult social andeconomic conditions prevailing in the country at large; these conditionsundoubtedly affected the financial and institutional objectives of the twoprojects and at times rendered progress and achievements barely visible.Nevertheless, as a result of the two projects, the supply of good qualitywater has increased significantly in Chittagong and Dacca, although the supplyis on an intermittent basis and the two systems are still inadequate to meetthe demand fully. The sewerage system in Dacca is, as yet, underloaded, butconnections are steadily increasing as a direct result of a new connectionprogram. The Bank is continuing its efforts to develop the water supply andsewerage sector in Bangladesh under a follow-on project to both Dacca andChittagong.

35. The PCRs contain several conclusions and lessons learned fromthe project, summarized in PCRC paras. 9.01-9.11 and PCRD paras. 9.01-9.09,with which the audit generally agrees. One lesson in particular deserves tobe underlined, since it has a general relevance to water supply projects:if an increase in the supply of safe water is to be accompanied by a signifi-cant diminution in the incidence of water-borne diseases, it may be necessary,especially in rural areas, to initiate a parallel health education programaimed at improving personal hygiene and sanitation practices 1/.

36. The following principal lessons learned can be added to those inthe PCRs:

(i) adequate arrangements should be made, prior to loan or crediteffectiveness, for the water supply authority to collect revenuessufficient to cover the cost of supplying water through publicstandpipes; various arrangements are possible, e.g. cross subsidyfrom domestic consumers by including an appropriately calculatedelement ,or surcharge in the domestic tariff, subsidies from theGovernment or payment from the local authority, based upon meteredpublic standpipe consumption 2/;

1/ This lesson is being implemented as part of the follow-on projects toDacca and Chittagong and the GOB's health education program is to becommended (PCRs paras. 1.06 and 9.01).

2/ During negotiations for Credit 941-BD and Credit 1001-BD, GOB agreed topay the WASAs for water supplied through public standpipes (PCRC para.9.06).

- 13 -

(ii) during project preparation and appraisal, sufficient attentionshould be given to the training aspect of management, not only forupper-level staff, but also for lower-level managers and operationalstaff.l/;

(iii) where weaknesses or vacancies in key positions have been identifiedand where difficulties in recruiting experienced and qualified stafffrom the local market are known to exist, for example due to rela-tively unattractive salaries, international recruitment of qualified

experts may be necessary, at least in the short term;

(iv) Action Programs, specifying clearly and in detail how a project-sproblems may be resolved, can play a key role in improving projectimplementation;

(v) the application of an audit covenant, requiring the audit of finan-cial statements by independent auditors, is not realistic beforemeasures have been identified and steps have been taken to ensurethat the entity has the capability to keep appropriate records andto prepare the necessary financial statements in a timely manner;

(vi) expectations concerning reductions in unaccounted-for water shouldbe supported by detailed leak detection and survey programs; fastrepairs, efficiency and incorruptibility in billing and meterreading, good metering of production and efficient meter workshopsare also vital to a successful campaign to reduce unaccounted-forwater! 2/; and

(vii) prior to credit approval, proper arrangements should be made toensure that customers will connect to the sewerage system as soonas it becomes operational 2/.

1/ These lessons are being implemented under the follow-on projects (PPAMparas. 23 and 31).

2/ c.f. PPAR No. 2861, dated March 3, 1980 on Ethiopia: Addis Ababa WaterSupply and Sewerage Project (Loan 818-ET).

3/ c.f. PPAR No. 1683, dated August 1, 1977 on Ghana: Accra/Tema WaterSupply and Sewerage Project (Credit 160-GH).

- 14 -Attachment

BANGLADESH: CHITTAGONG WATER SUPPLY PROJECT

(CREDIT 367-BD)

PROJECT COMPLETION REPORT

I. INTRODUCTION

1.01 IDA's interest in Chittagong's water supply began in 1963 whenCredit 42-PAK for US$24.0 million equivalent was made to the Government ofPakistan (GOP) to help finance a water supply and sewerage project for the city.Chittagong WASA was established to complete the work and run the undertaking.The project proved to be over ambitious and in 1968 the Credit was reduced toUS$7.0 million, mainly by eliminating the sewerage component. Politicaldisturbance and war interrupted progress and in December 1971, after consulta-tion with GOP, the Association suspended disbursements. Up to that timeUS$3.3 million had been disbursed under the Credit. There was a hiatus whenforeign currency was not available but in June 1972 the Kingdom of Swedenagreed to provide interim finance until, in April 1973, an IDA credit to theGovernment of Bangladesh (GOB) of US$7.0 million equivalent (367-BD) replacedthe US$7.0 million Credit (42-PAK) to GOP.

1.02 The project inherited the following objectives from the earlierGOP project:

(a) To establish and develop Chittagong WASA as an authoritywith the powers necessary to carry out the project effectivelyand to manage and operate the undertaking in a professionaland businesslike manner; and

(b) To provide sufficient additional supplies of wholesome waterto meet the needs of Chittagong's growing population andindustry.

1.03 The work covered by the project was substantially completed bythe closing date of February 15, 1979 and US$7.0 million was disbursed byend FY79.

1.04 This project completion report is based on information obtainedfrom appraisal reports, President's Report No. P-1203-BD, supervision reportsand a project completion report prepared by Chittagong WASA with the help ofits consultants.

- 15 -

The Sector

1.05 The Government of Bangladesh (GOB) has been trying to satisfy theincreasing demand for water arising from rapid population expansion, particularlyin those urban areas where the effects of natural growth have been aggravatedby rural migration. The main constraints upon sector development are shortageof funds and insufficient numbers of qualified and experienced personnel.GOB has used its limited resources to concentrate on developing safe watersupply facilities rather than disposal of waste. Over the past 7 years,investment in the water supply and sewerage sector has been about 7% ofGOB's development expenditures, and about 56% of the population now hasaccess to wholesome water and about 8% benefit from waste disposal services.

1.06 In rural areas, a program sponsored by the United Nation'sInternational Children s Emergency Fund (UNICEF) and the World HealthOrganization (WHO), by sinking about 200,000 hand pump tubewells and bringingthe number in service to about 380,000 made available safe water to a totalot about 40 million people. UNICEF plans to continue this program through1985; its contribution, about 50% of the total cost, takes the form ofmaterials. GOB obtains contributions amounting to about 10% of the costfrom local consumers and provides the renaining 40% in the form of grants.Despite !this signiticant increase in the supply of sate water in rural areas,water borne diseases have not diminished as much as was anticipated becausepersonal hygiene and sanitation practices have not improved sufficiently.GOB has developed a health education program in recognition of this problem.(See para. 9.01)

1.07 The Asian Development Bank (ADB) has indicated its intention toassist in financing projects for water supply in district towns. An ADBtechnical assistance grant has been approved for the-preparation of feasibi-lity studies for projects designed to satisfy the needs through 1990 of thetowns of Comilla, Bogra, Barisal, Mymensingh and Jessore which would benefitsome 500,000 people; other district towns may be included in subsequentprojects. In addition, GOB has obtained assistance from the Government of theNetherlands (GON) to conduct feasibility studies for water supply projectsin Khnlna and Rajshahi.

1.08 GOB exercises control over the sector through the Ministry of LocalGovernment, Rural Development and Cooperatives (MLGRD). The agencies operatingunder MLGRD are the Department of Public Health Engineering (DPHE), themunicipalities and, in Dacca and Chittagong, Water and Sewerage Authorities(WASAs). DPHE develops water supply projects countrywide and operates andmaintains water works throughout the rural areas. In urban areas, DPHEgenerally hands over operational and maintenance responsibilities to themunicipalities except Dacca and Chittagong where the WASAs have responsibilityfor all aspects of water supply and sewerage.

- 16 -

II. PROJECT PREPARATION AND APPRAISAL

Origin

2.01 The project originated with a request from GOP for a developmentcredit to help finance water supply and sewerage works in Chittagong.

2.02 The pre-project water sources comprised a number of old drilledwells of various capacities; some supplied water to an old iron removalplant near the city center but, in general, the wells filled a few smallelevated tanks which supplied water for short periods, mornings and even-

ings. The better off used roof storage tanks but the great majority carriedtheir supplies in containers to their homes trom standpipes or handpumptubewells. Most industries, including the Port Trust and Railway, and manyindividuals had private water supplies, generally tubewells.

Appraisal

2.03 The project in its initial form was appraised in 1963 but, due to

difiiculties in project execution and higher than expected costs it was agreed

with the Government that the original project had been too ambitious. Arevised project was appraised in 1968; events leading eventually to war inter-

rupted progress from 1969. It was not until 1973 that the project in itsfinal form was appraised.

Project's Role in the Long-term Plan

2.04 The project scope lessened at each stage of revision. The firstconcept was for a surface water abstraction and treatment plant on the river

Halda with supporting ground water development, but in the end ground waterbecame the exclusive source. The role of the project, as conceived, was toestablish a water supply base which could be expanded in stages as needsincreased; the project as executed provided valuable additional short-term

supplies of water but the need to build an expandable base was only deferred.

Project Description

2.05 Thn project included the following:

(a) Completion of 13 tubewells, iron removal facility and booster

pump station. (These items were all built at Kalurghat.)

(b) Construction of about 175,000 feet of mains and distributionpipe, and completion of a program for installation of street

hydrants, service connections and meters.

1/(c) Construction of a 6.0 IN- reservoir on Battali Hill.

1/ Later reduced to 3.0 IMg.

- 17 -

(d) Acquisition ot land, access road and site development work andpreparation of detailed design for a surface water treatmentplant and related facilities.1/

(e) (i) completion of stores facilities and workshops, and instal-lation of equipment;

(ii) provision of vehicles, and maintenance of office equipment.

(f) Training of staff.

Covenants

2.06 Because of the need to improve WASA's financial position, GOB cove-nanted to cause WASA to set and maintain rates for water supply and sewerageservices which would provide sufficient revenues:

(i) to cover operating expenses, including taxes, if any, andinterest and to provide adequate maintenance and depreciation;

(ii) to meet repayments on long-term indebtedness to the extentthat such repayments exceed the provisions for depreciation;and

(iii) to finance the normal year to year extension of the water supplyand sewerage systems and to provide a reasonable portion of thecost of future major expansion of such systems.

III. PROJECT IMPLEMENTATION, OPERATION AND COST

Loan Effectiveness and Start-up

3.01 The standard conditions of etfectiveness having been met the creditbecame effective on 7 June 1973 just under two months after the Agreement wassigned. Within a year, however, a supervision mission reported shortage ofmaterials, procurement problems, labor problems, poor consultants' performanceand unsettled social conditions following the 1971 war and estimated thatproject completion would consequently be at least two years beyond the appraisaltarget date.

Implementation

3.02 The project had a very slow start-up due mainly to a shortage ofmaterials, particularly cement and pipes; other contributing factors wereinsutficient strength in the consultant's design staff and constructioncontractor inefficiency. These problems were quickly recognized and attempts

1/ Later limited to acquisition of land.

- 18 -

were made to deal with them but unsettled social conditions had a widespreadeffect and response to treatment was slow. Experienced reinforcements to theconsultant's staff resulted in improved construction supervision which brought

benefits in contractor's performance. The first signs of improvement beganto appear late in 1974 but it was not until mid-1976 that progress was reportedas satisfactory; quality of work improved and the consultant's performance inthe construction phase showed to much greater advantage than in the destgn

phase.

3.03 As a result of these problems completion by the closing date, June 30,1975, could not be achieved and extensions to the closing date were made, bystages, to February 15, 1979.

Procurement

3.04 Discussions on procurement were held with the WASA prior to thecredit effectiveness date as well as subsequently. Equipment and materialscontracts were awarded on the basis of international competitive bidding.Civil works contracts, with a single exception, were awarded to local con-tractors.

3.05 The exception was a turn-key contract for construction of the 3 IMgreservoir on Battali Hill. The award was made to an Indian contractor whichhad a Bangladesh associate; soon after commencement, however, the two firmsseparated and the Bangladesh firm completed the work. Structural design wasby an Indian consultant but proved to be inadequate so that, despite goodconstruction quality by the contractor and careful supervision by the consul-tants (not the designers), the tank failed under test. The faults werecorrected at the contractor's cost.

3.06 Procurement delays were common, particularly in the early stages;most of the local agents of international bidders were inexperienced inhandling technical questions and had to refer to their foreign principals.They also acted as middlemen for questions and answers and this process, inaddition to being slow, frequently led to misunderstandings.

3.07 In the first year of the project WASA's and the Chairman's powerswere temporarily suspended. These powers were later restored but duringsuspension considerable delays were experienced as result ot WASA having tosubmit equipment tenders to GOB for final award.

Project Costs and Disbursements

3.08 The costs of the project (original estimate and actual) are shownin the following table.

- 19 -

Original Estimate ActualUS$ US$

Millions Millions

Land and Site Work 0.3 1.2

Tubewells 0.36 1.8

Distribution System 1.45 4.8

Booster Stations 0.86 2.0

Battali Hill Reservoir 1.44 1.6

Service connections 0.55 0.9

Buildings and Equipment 0.68 0.8

Total Works 5.64 13.1

Contingencies 2.21 -

Sub-total 7.85 13.1

Engineering ConsultingServices and Training 1.26 3.4

9.11 16.5

The accuracy of actual costs is doubtful as the accounting was continued fromthe start of the original project and the lines were not clearly drawn betweenthe end of that project, the period when Sweden provided finance and the startof the finalized project. The extended duration of the project, the fluctu-ations in relations between the dollar and the taka over the period and thechanges in the content of physical work frustrate attempts to make worthwhilecomparisons between the estimate and actual cost out-turn.

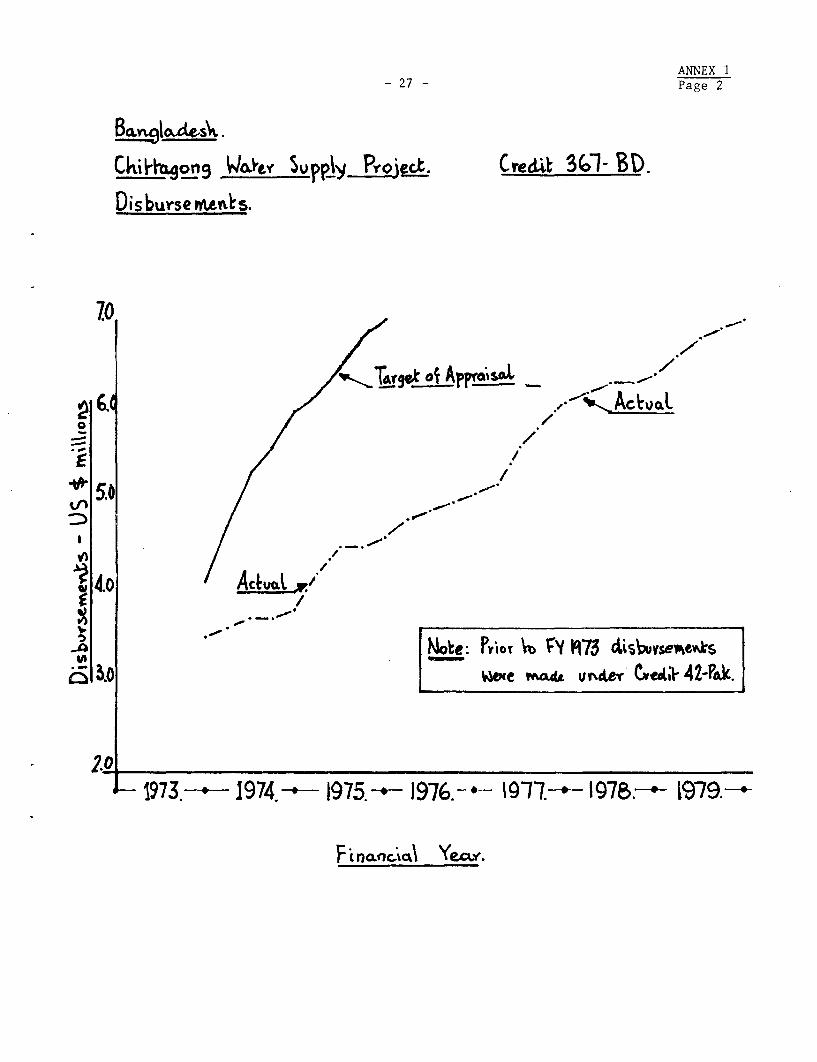

3.09 The credit, amounting to US$7.0 million and scheduled to be completedby October 1974, was not fully disbursed until the last quarter of FY1979. Thepattern of disbursements is shown in Annex 1.

Operations

3.10 The Kalurghat iron removal plant has operated constantly since itwas commissioned in September 1977; it treats Kalurghat well-field productionsatisfactorily. There are some design faults which can be corrected at thenext state of development; the outlet weirs on the lagoons are too low andextreme simplicity of filter design has made them inflexible in operation;

- 20 -

the tubewells lose productive capacity quickly because iron accumulation onpumps and pipes restricts flow. (See para 9.03)

Performance

3.11 (a) Consultants were responsible for planning, design and super-vision of construction. The weakness in design which showed early in thecourse of project execution was balanced by the quality of supervision. Inaddition, the firm provided valuable training and operational guidance andadvice for WASA's staff. Overall, performance was satisfactory and theconsultants were retained to prepare the follow-on project.

(b) Contractors. Inexperience and financial weakness showed clearlyin the early years; in addition, skilled manpower was scarce. Gradually,however, skills developed and the last major work, Battali Hill reservoir,showed great improvement over earlier work. Pipe-laying experience gainedwill be of future benefit as WASA still requires many miles of pipe lines.Finishing abilities (e.g. painting) are lacking and will be slow in develop-ing, but the basic skills have been acquired.

(c) Supply deliveries were frequently delayed while goods awaitedcustoms clearance. Arrangements have recently been made by GOB to eliminatethis bottleneck.

IV. OPERATING PERFORMANCE

4.01 The project aimed at a production level of about 57 mld (12.5 mgd)made up of 45 m1d from Kalurghat and 12 mld from the city wells. Power out-ages and down-time of tubewells for repair and removal of accumulations ofiron (Para 3.10) affect production, which has been as low as 47 mld (10.5 mgd)for periods of two to three months at a time. WASA has introduced a programfor cleaning iron deposits from tubewells and plans to introduce standbyelectric generation arrangements to counteract power outages. (See para 9.03)

4.02 Design of the various components ot the project applied moderntechnology in a manner suitable for the local operational capacity.

V. FINANCIAL PERFORMANCE

5.01 Financial projections were not prepared at the time of appraisal but,

measured against WASA covenanted obligation, financial performance was unsatis-factory for the duration of the project. WASA was covenanted to maintain tariffsat levels sufficient to finance normal annual system extensions and a reason-able proportion of future major system expansion (Para 2.05). Despite three

- 21 -

tariff increases l/ between FY74 and FY79 WASA consistently failed to meetthis covenant and has incurred an operating deficit each year since 1974.Details of its financial operations from FY74 through FY79 are summarizedin the table below and are shown in greater detail in Annex 2.

WASA INCOME STATEMENT (FY74 THROUGH FY79)(Taka million)

1974 .1975 1976 1977 1978 1979

1. Revenues 2.7 3.5 5.5 9.0 11.5 15.32. Expenditure: Direct Expenses 1.8 2.7 3.8 5.2 6.5 8.3

Administration 2.0 2.6 2.6 2.6 3.2 4.63.8 5.3 6.4 7.8 9.7 12.9

3. (1) minus (2) (1.1) (1.8) (0.9) 1.2 1.8 2.44. Add: Administrative Costs

Capitalized 1.0 2.0 2.2 2.4 2.9 -

5. Surplus/(deficit) BeforeDepreciation (0.1) 0.2 1.3 3.6 4.7 2.4

6. Depreciation and DeferredExpenses .(.) (7.0) ( (3.8) (5.8)(12.2

7. Deficit (2.1) (1.8) (2.2) (0.2) (1.8)(9.8)

5.02 WASA's practice of capitalizing and tinancing from GOB projectfunds an increasing proportion (from 50% in FY75 to 90% in FY78) of itsadministrative costs was not justified as most staff were not directly en-gaged in project work. The practice merely served to reduce WASA's publishedoperating deficit. WASA intends to discontinue this practice and to writeoff all such capitalized expenses.

5.03 The reasons for WASA's unsatisfactory financial performance are:

(a) Water sales accounted for only about 50% of water producedeach year; there were no satisfactory arrangements forrecovering the cost of water supplied through standpipesand no satisfactory programs for the detection of leakageor illegal connections or for waste prevention;

1/ Water charges (Taka/1,000 gallons) at project start and finish were:

FY74 FY79--------Taka----- ---

Domestic 2 4.5Industrial 3 9Commercial 4 18

(For fuller details see Annex 3)

- 22 -

(b) Cash collected, has generally not exceed 70% of annualbillings (although an improvement to 83%-- was recorded inFY79);

(c) Expenses, staffing costs in particular, have increasedsignificantly; and

(d) Understaffing at senior staff level on finance and revenue.

VI. INSTITUTIONAL PERFORMANCE AND DEVELOPMENT

6.01 At the start WASA's performance was poor in all activities. Laborrelations were difficult and the threat of strikes and violence was always in

the air. WASA's and consultants' organizations were affected alike and it wasdifficult even for a strong manager to show results. Remedies were hard tofind because the conditions transcended WASA and reflected the social andeconomic situation of the country. From the start it was recognized thatmanagement would have to strive patiently to achieve small measures of changes.WASA has three branches; administration, commercial and engineering, andalthough each has shown improvement in varying degrees during the course ofthe project, the following still require attention:

(a) Low productivity affects WASA in some critical areas. For

example, monthly billing, on which revenues depend, is invariablyless than 100%; dependable meters are necessary for billingpurposes but slow meter repair work affects the number ofserviceable meters in use; and

(b) Staffing levels are too high but this condition is commonthroughout the country. Labor is organized and protectionistand improvement in this area will materialize only slowly.

VII. PROJECT JUSTIFICATION

7.01 At appraisal, the project was justified by the following principalreasons:

(a) To complete the work started under Credit 42-PAK;

(b) To provide continuous on-premise water service to about 70% ofthe population (the rest of the population, it was forecast,would be dependent on public standpipee); and

(c) Increasing demand for domestic and industrial consumption,unless met by increased production would lead to part of the

1/ Cash collected in FY79 in respect ot billings inFY79 is about 50%. Thebalance of collections was for billings in prior years.

- 23 -

population reverting to traditional sources of supply such astanks and dug wells, which are frequently contaminated.

7.02 The project completed the work started under the earlier credit and

it produced the quantities of water needed to meet demands in the service area.

The public has expressed its satisfaction with the quality and quantity of

available supplies. However, only about 25% of the serviced population have

on premise connections and 75% still rely on standpipes.

VIII. BANK PERFORMANCE

8.01 The Bank Group, through the Chittagong project and a parallelwater supply and sewerage project in Dacca, developed and maintained a goodworking relationship with those government departments concerned with watersupply and Chittagong WASA. This relationship was nurtured by the residentmission as well as supervision missions and it was successfully tested whenWASA was under pressure to improve its financial position as a condition ofextending the closing date. The need to obtain an extension of the closingdate provided motive for WASA to take positive actions to improve its finan-cial position (for example, to reduce arrears), but, unfortunately there wasanother eftect; WASA, concerned lest the credit closed (instead of beingextended), stopped procurement activities which brought unwelcome delays toproject completion.

8.02 The normal rotation of bank staff over the extended project dura-tion resulted in a succession of engineers and Anancial analysts visitingChittagong. Arrangements were made to achieve a smooth hand-over and theseappear to have been effective; certainly neither GOB nor WASA made any adversecomment when changes occurred.

8.03 The Bank Group's interest in Chittagong will be continued througha follow-up project which was approved by the Board on March 25, 1980; itsprincipal objectives are to:

(a) provide a new source of water which will produce the addi-tional supplies needed by Chittagong's growing population anddeveloping industry;

(b) achieve further managerial and financial improvements;

(c) establish WASA as sole authority for water basin control andwater supply within the area; and

(d) prepare a feasible sewerage/sanitaiton plan.

IX. CONCLUSIONS

9.01 The need for health education has been demonstrated and, as part

- 24 -

of the follow-on project GOB will, through their Health Education Department,introduce a program for training voluntary health workers and for publiceducation by means of posters, hand bills and leaflets, radio and television(para 1.06).

9.02 Some procurement delay arose as a result of inexperience of thelocal agents of foreign suppliers. WASA has introduced the requirement thatlocal agents may represent only one supplier and a principal may only berepresented by one local agent (for any particular contract). Communications,especially those relative to clarification of specifications, will be madedirectly by WASA to principals with copy correspondence to local agents.It is expected that direct correspondence will eliminate the confusion thatsometimes arose when communicating through middlemen (para 3.06).

9.03 Water production has been reduced by power outages and by accumu-lations of iron on pipes and pumps. The follow-up project makes provision forstandby electrical generation and contractual arrangements have already beenactivated for regular cleaning and descaling of iron deposits (para 4.01).

9.04 WASA's strength and capability grew significantly during theproject but further improvement is needed. Commercial and technical expertisemust both be improved and WASA should aim at reducing dependence on foreignconsultants.

9.05 Commercial performance has been adversely affected by under staffingat the senior staff level and the follow-on project has made provision forstrengthening the leadership of the finance and revenue sections. In addition,arrangements are being made for the engagement of an expatriate counterpartto the commercial manager on a contract extending over two years (para 5.03).