world acceptance corporation acceptance has remained profitable while operating with strong and...

TRANSCRIPT

June 30, 2017

World Acceptance CorporationNASDAQ: WRLD

Certain statements in this presentation constitute “forward looking-statements” under the Private Securities LitigationReform Act of 1995. Statements other than those of historical fact, as well as those identified by the words “anticipate,”“estimate,” ”intend,” “plan,” “expect,” “believe,” “may,” “will,” and “should” or any variation of the foregoing and similarexpressions are forward-looking statements. Such forward-looking statements are about matters that are inherently subjectto risks and uncertainties. Factors that could cause actual results or performance to differ from the expectations expressed orimplied in such forward-looking statements include the following: recently enacted, proposed or future legislation and themanner in which it is implemented; the nature and scope of regulatory authority, particularly discretionary authority, that maybe exercised by regulators having jurisdiction over the Company’s business or consumer financial transactions generically,including, but not limited to, the Consumer Financial Protection Bureau (the “CFPB”), having jurisdiction over the Company’sbusiness or consumer financial transactions generically; the unpredictable nature of regulatory proceedings and litigation; andany determinations, findings, claims or actions made or taken by the CFPB, other regulators or third parties in connection withor resulting from the previously disclosed civil investigative demand from the CFPB that assert or establish that the Company’slending practices or other aspects of its business violate applicable laws or regulations; the impact of changes in accountingrules and regulations, or their interpretation or application, which could materially and adversely affect the Company’sreported financial statements or necessitate material delays or changes in the issuance of the Company’s audited financialstatements; the Company's assessment of its internal control over financial reporting, and the timing and effectiveness of theCompany's efforts to remediate any reported material weakness in its internal control over financial reporting; changes ininterest rates; risks related to expansion and foreign operations; risks inherent in making loans, including repayment risks andvalue of collateral; the timing and amount of revenues that may be recognized by the Company; changes in current revenueand expense trends (including trends affecting delinquencies and charge-offs); and changes in the Company’s markets andgeneral changes in the economy (particularly in the markets served by the Company). These and other factors are discussed ingreater detail in Part I, Item 1A, “Risk Factors” in the Company’s most recent annual report on Form 10-K for the fiscal yearended March 31, 2017 filed with the Securities and Exchange Commission (“SEC”) and the Company’s other reports filed with,or furnished to, the SEC from time to time. World Acceptance Corporation does not undertake any obligation to update anyforward-looking statements it makes.

2

Cautionary Note About Forward-Looking Statements

Table of Contents

3

Section 1 Company Overview and Key Investment Highlights.... 4

Section 2 Business Overview..................................................... 11

Section 3 Financial Summary.................................................... 23

Company Overview and Key Investment Highlights

4

5

World Acceptance Overview

Largest Domestic Branch Network…

…With a Presence in Mexico

50+ year old small-loan consumer finance company

Provides loans to individuals with limited access to credit

Well positioned to capitalize on favorable supply/demand imbalance within the non-prime lending space

Originated over $27 billion dollars worth of loans since 1994

Focused on relationship-lending business model Total: 1,169

Total: 162

Branch Count

FY2018 Data is through 6/30/2017

217 360 441

620

990

1,271 1,350 1,327 1,331

0200400600800

1,0001,2001,4001,600

'94 '98 '02 '06 '10 '14 '16 '17 '18

30

80 2975

39

292

73

4721 65

10476

93124

21

Jalisco 3

Sinaloa 7

Sonora12 Chihuahua

29 Coahuila 12

Chiapas 9

Yucatan 4

Quintana Roo 5

Nuevo Leon 23Tamaulipas 11

Guerrero 4

SLP 4Aguas Calientes 4

Guanajuato 5

Edo De Mexico 4Morelos 3

Queretaro 3

Hildalgo 3

Puebla 5

Veracruz 2

Campeche 1

Baja California Sur 2

Oaxaca 3

Baja Calif North 1

Zacatecas 1

Ciudad Mexico 2

6

Key Investment Highlights

Consistently Profitable through

Multiple Cycles

Experienced Management Team

Stable Business Model with Low

Volatility of Earnings and Losses

Attractive Market Supported by Strong

Supply/Demand Dynamics

High-Touch Business Model Enhances Risk

Monitoring Strong Balance Sheet with

Compelling Cash Flow Characteristics

Long Operating History

Consistently Profitable through Multiple Cycles

World Acceptance has remained profitable while operating with strong and stable margins in various economic environments

Net Charge-Offs

7

($ in millions)

_________________Note: Fiscal year-end is 3/31. FY 2018 numbers represent last twelve months. (1) Return on Average Assets is calculated as net income over the Average Total Assets for the respective period. Average Total Assets are defined as a 5-quarter average, ending at the respective period end(2) 20+ Year Average represents average from 3/31/1997 to 3/31/2017

20+ Year Average NCOs2: 13.7%

Net Income & Return on Average Assets1

$6 $9 $11 $8 $8 $7 $14 $16 $19 $23 $29 $34 $39 $48 $50 $56 $74 $91 $101 $104 $107 $111

$87 $74 $70

8.2%10.8% 11.9%

8.2% 7.2%8.4%

9.7% 8.8% 9.9% 10.4%11.7% 11.8% 11.9% 12.2%

11.0% 10.9%12.7%

13.9% 13.9% 13.0% 12.3% 12.5%10.0%

8.8% 8.3%

0.0%

4.0%

8.0%

12.0%

16.0%

$0

$40

$80

$120

$160

$200

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

7.6%

11.2%10.6% 9.4% 9.7%

12.0% 12.0%14.8% 14.6% 14.7% 14.6% 14.8%

13.3%14.5%

16.7%15.5%

14.3% 14.1% 13.9% 14.7%12.9%

14.8% 15.7% 15.4%

0.0%

5.0%

10.0%

15.0%

20.0%

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

Strong Balance Sheet with Compelling Cash Flow Characteristics

World Acceptance’s strong cash flows have allowed the Company to operate at low leverage levels

Leverage Profile (Debt/Equity)

Cash Flows From Operations

8

_________________Note: Fiscal year-end is 3/31(1) 20 - Year CAGR represents CAGR from 3/31/1997 to 3/31/2017(2) 20+ Year Average Leverage represents average from 3/31/1997 to 3/31/2017

($ in millions)

20+ Year Average Leverage2: .9x

1.3x1.1x 0.9x

1.5x 1.4x 1.3x 1.2x 1.1x

0.8x0.9x

0.6x 0.4x 0.5x 0.8x 0.8x 0.7x0.5x 0.4x 0.7x

1.1x1.6x 1.6x

1.0x0.6x 0.6x

0.0x0.5x1.0x1.5x2.0x2.5x3.0x3.5x4.0x4.5x

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

$21 $19 $21 $32 $39 $48 $55 $70 $88 $98 $110 $136 $154

$184 $200 $219 $232 $246 $242

$206 $219

$0

$50

$100

$150

$200

$250

$300

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Traditional Loan Product Provider to Underserved Clients

9

PaydayPawnTraditional InstallmentCredit Card

_________________Source: Company filings, CFPB, Center for Responsible Lending Report (Feb 2013), Wall Street Research(1) Center for Responsible Lending, “The State of Lending in America & its Impact on U.S. Households." Data represents 30-Day Balloon Payment Car-Title Loans(2) CFPB, “Payday Loans and Deposit Advance Products”

Auto Title Loans

Past Due Resolution

Auto debit bank account

Sale of loan collateralBranch calling

Centralized callingSale to a 3rd party

Repo automobile

Loan Amortization BalloonBalloon

Fully amortizingFixed, equal

monthly payments

RevolvingLow minimum

paymentBalloon

Credit Reporting No reportingNo reportingReport to bureausReport to bureaus No reporting

Renewals Borrower’s optionAverage 0 – 3 renewals/yearRevolving

Underwriting Approach

Bank account and employment

Solely collateral valueAbility to payAbility to pay and

credit historySolely collateral

value

8 renewals/year1 9 renewals/year2

World Acceptance provides an attractive product to an underserved customer base, focusing on the customer's stability, ability and willingness to pay

Average Term 2 - 3 weeks22 – 4 months

Large: 3-5 yearsSmall: 12-24 months

Revolving 30 days1

10

Experienced Management Team

Employee Hierarchy and Avg. Tenure With WRLD

Senior Management

Senior Vice Presidents

Vice President of Operations

Supervisors

Branch Employees

23 years

18 years

14 years

5 years

6years

7years

3 years

2 years

U.S. Mexico1

_________________(1) Mexico locations opened in 2005

Business Overview

World Acceptance Branch Overview

12

Managers have full P&L responsibility for their branch and are tasked with fostering an ownership attitude

United States

Representative Branch

Mexico

Typical Branch Portfolio Branch EmployeesCharacteristics

1,500 square feet

$1,470 per month lease

Rural America –typically downtown or small strip center

1,725 square feet

$1,800 per month lease

Medium to large cities –typically in small strip centers

$840,000 gross loans receivables

654 accounts

$418,000 avg. revenue during fiscal 2017

$794,000 gross loans receivables

1,012 accounts

$267,000 avg. revenue during fiscal 2017

2.8 employees per branch

Manager, Branch Service Representatives

8.0 employees per branch

Manager, Assistant Manager, Customer Service Representative and Security Guards

_________________Note: Data as of 6/30/2017

Historical Branch Growth

13

Branch Count Over Time

Conservative and disciplined manner of entering states and opening branches

1962 1974 1980 1991 1993 1996

July 1962: South Carolina

2000 2003 2005 2010 2013

December 1974: Texas and Georgia

October 1980: Oklahoma

May 1991: Louisiana

April 1993: Tennessee

1996: Illinois, Missouri and New

Mexico

March 2000: Kentucky

January 2003: Alabama

September 2005: Mexico

December 2010: Wisconsin

September 2012: Indiana

2012 2014

October 2014: Idaho

September 2013: Mississippi

_________________Note: Total branch count over time is as of 6/30/2017

State Date of Entry 1995 2000 2005 2010 2015 Total

South Carolina July '62 59 63 65 95 99 93Georgia December '74 38 48 76 101 113 124Texas December '74 93 135 164 229 300 292 Oklahoma October '80 33 43 51 82 83 73Louisiana May '91 15 21 20 38 49 47 Tennessee April '93 6 35 55 95 107 104 Illinois September '96 30 33 64 82 80 Missouri August '96 18 36 62 78 75New Mexico December '96 13 20 39 44 39 Kentucky March '00 4 36 61 79 76 Alabama January '03 21 44 68 65 Mexico September '05 80 148 162 Wisconsin December '10 28 30 Indiana September '12 22 29Mississippi September '13 12 21 Idaho October '14 8 21Total 244 410 577 990 1,320 1,331

All loans are fully amortized with a fixed rate and term Installment loans standardized by amount, rate and maturity Loans underwritten to allow customers to make affordable payments from their disposable income Mexican operations began in 2005; currently Mexico operations represent ~10% of the total portfolio

Payroll deduct loans are originated through state unions

14

Loan Characteristics

World Acceptance operates predominately in the small-loan installment space

Small Installment

Large Installment

Installment Lending -Payroll Deduct

Installment Lending –Branch-Based

Size Average Term

Average: $3,600 Range: $1,500 to $13,500 23 months

Average: $923 Range: $200 to $3,600 10 months

_________________Note: Data as of 6/30/2017(1) Mexican portfolio data displayed in USD; exchange rate is as of 6/30/2017, 1 USD = MXN 18.0540

Mex

ico1

U.S.

Average: $413 Range: $203 to $1,362 12 months

Average: $1,838 Range: $339 to $8,143 31 months

15

Portfolio By Geography1 U.S. Portfolio by Loan Size Amount2

Portfolio Overview

Diversified portfolio by size and geography

No state has greater than a 20% loan concentration Larger loans (>$1,500) have been growing as a percentage of the portfolio

Currently comprise approximately one-third of World Acceptance’s loan portfolio

_________________(1) Based on gross loans receivable as of 6/30/2017(2) Data as of 6/30/2017(3) Other states include Louisiana, New Mexico, Wisconsin, Indiana, Mississippi and Idaho

9%

19%

13%

12%

17%

11%

17%

2%

0-250

251-500

501-750

751-1000

1001-1500

1501-2000

2001-5000

5001+

17.1%

12.7%

11.4%

8.5%11.6%

8.5%

6.1%

6.2%

5.8%

4.3%7.8% Texas

Missouri

Oklahoma

Illinois

Kentucky

MexicoTennessee

Georgia

Alabama

South Carolina

Other

16

Portfolio By Beacon Score1 Portfolio By APR2

Portfolio Overview (cont’d)

World Acceptance’s deep knowledge of its borrower base has enabled the Company to lend effectively throughout the non-prime segment

Approximately 26% of the loans in the U.S. portfolio have APRs of 36% or less Approximately 90% of U.S. loans have an APR of less than 100% Portfolio spreads across a broad spectrum of borrowers

_________________(1) Represents U.S. portfolio, data as of 6/30/2017 (2) Data as of 3/31/2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

26.2%24.1%

12.6%

5.5% 4.6%3.4%

13.5%

9.8%

0.2%0.0%

8.0%

27.2%

18.7%

4.4% 2.5% 3.4%

35.8%

0.0%0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0%-36%

37%-50%

51%-60%

61%-70%

71%-80%

81%-90%

91%-99%

100%-149%

150%-200%

U.S. Mexico

Rigorous Loan Underwriting Process

Time-tested underwriting principles produce consistently strong performance

Mitigate net charge-off volatility through various economic cycles

Stability, ability and willingness to pay

Underwriting policies with objective credit evaluation criteria

Relationship-based branch lending enhances servicing effectiveness

Establishes initial contact with the borrower, building an ongoing customer relationship

Individual loan approval authority based on experience and position

Large loans approved at Large Loan Center

Generally decentralized loan approval and collections

Rigorous senior management oversight

17

World Acceptance’s time-tested underwriting process coupled with an understanding of the local demographic profile has yielded strong performance

Take Application

Budget Review

Verify Job, Residence and Credit References

Approve / Decline

Sign Documents

Disburse Funds

Review Credit Bureau

1

2

3

4

5

6

7

Robust Collections Process

Internal data system generates customizable notices on delinquent accounts

Friendly text message payment reminders sent once per week on Fridays; these go to every customer who has a payment due the following week from Monday to Sunday and has completed an opt-in form to receive texts.

Accounts 30+ days past due considered an advanced collection situation

Accounts charged off after 180 days Extensions allowed in special situations All charge-offs reviewed and approved by

supervisors

Branch managers earn up to 10% of Monthly Rating Sheet Profit if certain delinquency, profitability and growth goals are met

Other branch staff also earn a percentage of Monthly Rating Sheet Profit based on the performance of the branch

18

Collection Process

Branch Incentive Program

1 - 6+ Days 14 Days 90 - 180+ Days

Automatic reminder letters are mailed weekly

Phone calls from branch employees to home or cell phones

Phone place of employment

Phone customer references if customer not reachable

Account is charged off

Internal Recovery Unit (IRU) Calls 90+ Days

World Acceptance utilizes a rigid collection process and makes numerous attempts to work with the borrower prior to charging-off a loan

19

Net Charge-Offs

Credit Performance

Loan Delinquency – 61+ Days

Rigorous underwriting standards have led to stable loan losses and performance across economic cycles

_________________Note: Fiscal year-end is 3/31. FY 2018 numbers represent 3 months ended 6/30/2017

14.7% 14.6% 14.8%13.3% 14.5%

16.7% 15.5% 14.3% 14.1% 13.9% 14.7%12.9%

14.8% 15.7% 15.4%

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

24.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Net Charge-offs

2.3% 2.5% 2.1% 2.2% 2.6% 2.7% 2.4% 2.4% 2.5% 2.7% 3.0%

4.4% 4.7%5.5% 5.5%3.8%

4.1%3.4% 3.5%

4.0% 4.2% 3.8% 3.8% 4.0% 4.4%5.3%

7.0% 7.1% 7.8% 7.5%

0.0%

2.0%

4.0%

6.0%

8.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Recency Contractual

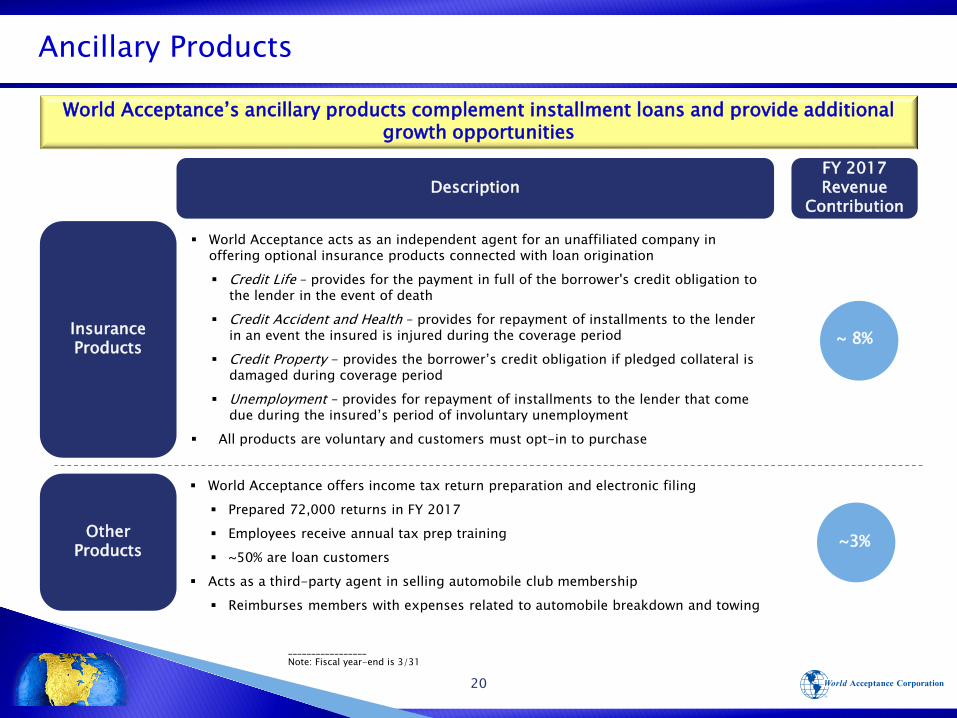

Ancillary Products

20

FY 2017 Revenue

Contribution

Insurance Products

Description

~3%

~ 8%

World Acceptance acts as an independent agent for an unaffiliated company in offering optional insurance products connected with loan origination Credit Life – provides for the payment in full of the borrower's credit obligation to

the lender in the event of death Credit Accident and Health – provides for repayment of installments to the lender

in an event the insured is injured during the coverage period Credit Property - provides the borrower’s credit obligation if pledged collateral is

damaged during coverage period Unemployment – provides for repayment of installments to the lender that come

due during the insured’s period of involuntary unemployment All products are voluntary and customers must opt-in to purchase

World Acceptance’s ancillary products complement installment loans and provide additional growth opportunities

Other Products

World Acceptance offers income tax return preparation and electronic filing Prepared 72,000 returns in FY 2017 Employees receive annual tax prep training ~50% are loan customers

Acts as a third-party agent in selling automobile club membership Reimburses members with expenses related to automobile breakdown and towing

_________________Note: Fiscal year-end is 3/31

21

Enterprise Risk Management

High Degree of Senior Management Involvement

Culture of Compliance

Management Controls

Regulatory matters Setting policy and procedures Risk oversight and management

Information technology Annual risk and fraud assessments Addressing state audit reports

Information System Controls

and Security Infrastructure

Internal Audit Department

Quarterly supervision of each branch Compliance monitoring Surprise cash counts Data Analytics

Monthly underwriting and loan documentation reviews

Detailed operational performance monitoring

3 Li

nes

of D

efen

se M

odel

Unified loan management platform (ParaData) provides strong IT control structure

Proprietary platform fully customizable Detailed branch statistics and monitoring

Video surveillance and on-site security in many Mexican branches.

12 full-time auditors All branches audited annually Loan documentation audits Detailed risk and fraud assessment process

Risk-based audit approach focused on high-risk areas and fraud prevention and detection

22

Risk and Compliance

World Acceptance has built a culture of compliance that understands and seeks to anticipate a changing regulatory environment

Implement controls to address weaknesses noted during risk assessments, branch audits, external compliance audits, state regulatory audits and customer complaints

Aligning the compliance program with changing business and regulatory conditionsControl

Continuously monitor branch audits, state regulatory audits and customer complaints for quick identification of systemic issues

Participate and consult on key business initiativesMonitor

Maintain a compliance program to identify deficiencies within our business processes Perform compliance and fair lending risk assessments Review all regulatory environment changes and translating those to changes in policies and procedures

Identify

Monthly detailed reporting throughout the business Quarterly summary reporting to the Board of Directors and senior management Escalate high-risk systemic issuesReport

Develop branch-level compliance training on key risk areas and systemic issues Ensure all employees and directors receive annual compliance trainingTrain

Financial Summary

24

Financial Highlights

_________________(1) Trailing Twelve Months(2) Compared to the three months ended June 30, 2016

1

Fiscal Year 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Three months ended

June 30, 2017(2)

Revenue Increase/

(Decrease)17.6% 15.4% 20.2% 18.4% 13.8% 12.4% 11.5% 9.9% 8.1% 5.8% 1.9% (8.6%) (4.6%) 1.4%

Net IncomeIncrease/

(Decrease)18.2% 13.3% 19.9% 8.8% 12.4% 30.4% 23.9% 10.4% 3.4% 2.4% 6.8% (21.1%) (15.8%) (21.4%)

EPSIncrease/

(Decrease)16.8% 16.1% 24.3% 15.1% 18.7% 29.7% 26.5% 18.3% 20.1% 20.0% 27.3% (15.5%) (16.6%) (21.9%)

Avg. Net Loan Growth

18.1% 14.2% 20.2% 20.0% 14.1% 13.7% 14.5% 11.6% 10.6% 7.0% 2.4% (2.5%) (4.6%) 0.4%

Return on Avg. Assets

11.8% 11.9% 12.2% 11.0% 10.9% 12.7% 13.9% 13.9% 13.0% 12.3% 12.9% 10.0% 8.8% 8.3% (1)

Return on Avg. Equity

20.1% 19.9% 20.9% 21.2% 21.2% 22.1% 22.8% 23.6% 27.0% 31.2% 37.6% 24.0% 17.8% 16.3% (1)

Same StoreRevenue

8.6% 10.1% 12.5% 8.9% 7.7% 8.1% 9.0% 6.8% 5.5% 3.7% .83% (6.9%) (3.4%) 1.2%

25

Gross Loans Receivables Loan Origination Volume

Revenue Earnings Per Share

Historical Financial Performance

($ in millions)

($ in millions)($ in millions)

_________________Note: Fiscal year-end is 3/31. Data is through 3/31/2017.

$2,261 $2,572

$2,820 $2,985 $2,954 $2,724 $2,621 $2,508

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2010 2011 2012 2013 2014 2015 2016 2017

$770 $875

$973 $1,067 $1,112 $1,110 $1,067 $1,060

$0

$200

$400

$600

$800

$1,000

$1,200

2010 2011 2012 2013 2014 2015 2016 2017

$441 $491

$540 $584

$618 $610 $558 $532

$-

$100

$200

$300

$400

$500

$600

$700

2010 2011 2012 2013 2014 2015 2016 2017

$4.45 $5.63

$6.63 $8.00

$9.60

$11.90

$10.05

$8.38

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

2010 2011 2012 2013 2014 2015 2016 2017

26

Stock repurchase program

$858,799,533*No shares were repurchased in Fiscal 2016

FISCAL YEAR SHARES PURCHASED AVERAGE PURCHASE PRICE PER SHARE

• Fiscal 1996 176,000 shares $10.00

• Fiscal 1997 1,810,000 shares $ 7.88

• Fiscal 2000 144,000 shares $ 5.03

• Fiscal 2001 275,000 shares $ 5.21

• Fiscal 2002 251,891 shares $ 8.65

• Fiscal 2003 1,623,549 shares $ 7.39

• Fiscal 2005 486,000 shares $18.01

• Fiscal 2006 800,400 shares $25.98

• Fiscal 2007 1,209,395 shares $44.73

• Fiscal 2008 1,375,100 shares $30.44

• Fiscal 2009 288,700 shares $27.19

• Fiscal 2010 38,500 shares $37.26

• Fiscal 2011 1,298,057 shares $41.09

• Fiscal 2012 2,181,045 shares $64.10

• Fiscal 2013 2,569,597 shares $71.24

• Fiscal 2014 2,091,699 shares $91.09

• Fiscal 2015 1,432,058 shares $80.53

• Fiscal 2017 95,703 shares $52.20

• Fiscal 2018 58,728 shares $78.57

• Total 18,205,422 shares $47.17

World’s return on assets and equity

12.7%13.9% 13.9% 13.0% 12.3% 12.5%

10.0%8.8%

22.1% 22.8% 23.6%

27.0%

31.2%

36.6%

24.0%

17.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2010 2011 2012 2013 2014 2015 2016 2017

Return on Average Assets Return on Average Equity

27