workshop on taxation of foreign remittances –ctc - mr...workshop on taxation of foreign...

TRANSCRIPT

1

Taxation of Royalty

Workshop on Taxation of Foreign Remittances – CTC

23 January 2016, Mumbai

CA. Shabbir Motorwala

Contents – Royalty

• Overview

• Taxation framework under the Income-tax Act 1961 (‘ITA’)

• Features of Model Conventions

• Taxation framework under Tax Treaties / DTAAs

• Concept of Beneficial Ownership

• Concept of Most Favored Nation Clause

• Selected issues

• Selected recent judicial precedents

• Case Study

• Questions & Answers

2

Royalty : Overview of Taxation Framework

• Scope of Royalty : Meaning and coverage

• Deemed accrual / arising of Royalty for the Non-Resident (NR) in India

• In which cases and when would the income be taxable in India?

• Nature of taxation of R/ FTS

• Gross basis (Non Permanent Establishment [‘PE’] situation) both under the Act as well as DTAA

• Net basis (When attributable / effectively connected to PE of NR in India) under the Act as well as DTAA

• Compliance aspects for Non-Residents

• PAN and Tax Residency Certificate to be obtained by NR payee

• Withholding tax by payer even if he is a Non-Resident and related compliances

• Post Vodafone (SC), Section 195 amended to include NR to NR payments in all cases

• Transfer pricing applies to demonstrate arm’s-length nature of the transactions with Associated Enterprises

• Filings of returns (with TP Report) by NR payee and undergoing Assessments followed by DRPs, Appeals, etc.

• Grossing up of TDS cases most complicated – unable to access easily position /taken by payers

3

4

R-FTS: Deemed Accrual / arising in India under ITA

• Section 5 – Scope of Total Income for Non-Residents

• Income received / deemed to be received in India

• Income accruing / arising in India or deemed to accrue or arise in India

• Section 9 – Income deemed to accrue or arise in India

• R / FTS taxation provisions introduced from w.e.f. 1 June 1976 i.e. AY 1977-78

• Royalty - Section 9(1)(vi) read with Explanations thereto

• FTS - Section 9(1)(vii) read with Explanations thereto

• R / FTS deemed to accrue or arise in India if paid by:

• Government

• Residents except when payment is for business / profession / source outside India

• Non-residents where payment relates to their business / profession / source in India

• Source = Not the payer of income but where activities / business carried out (Havells - Del HC / Other judicial precedents)

5

Meaning of Royalty under ITA

Section 9(1)((vi) - Royalty payable in respect of anyright, property or information used or services

Explanation 2 to Section 9(1)(vi)

Royalty means consideration for (includes lump sumconsideration but excludes income chargeable underthe head ‘Capital Gains’):

• Use of or Transfer of all or any rights in - includinggranting of any license:

• patent, invention, model, design, secret formula orprocess, trademark or similar property

• copyright, literary, artistic or scientific work includingfilms or video tapes but excludes consideration forsale, distribution and exhibition of cinematographicfilms

• Imparting of any Information concerning:

• working of or use of patent, model, design, secretformula, process, trademark or similar property

• technical, industrial, commercial or scientificknowledge, experience or skill

• Use or right to use:

• industrial, commercial or scientific equipment (excluding those covered under Section 44BB)

• Introduced from AY 2002-03

• Rendering of any services in connection with activities constituting Royalty

Knowledge of IPR law very relevant …..

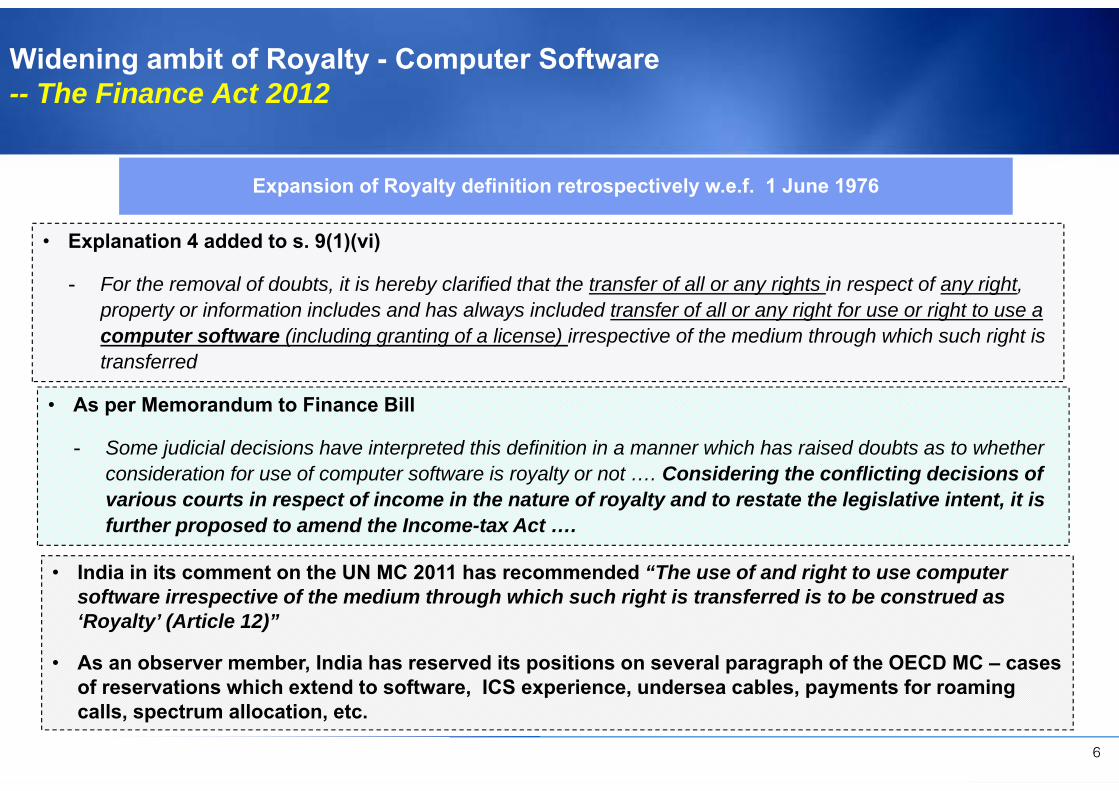

• Explanation 4 added to s. 9(1)(vi)

- For the removal of doubts, it is hereby clarified that the transfer of all or any rights in respect of any right, property or information includes and has always included transfer of all or any right for use or right to use a computer software (including granting of a license) irrespective of the medium through which such right is transferred

Widening ambit of Royalty - Computer Software-- The Finance Act 2012

Expansion of Royalty definition retrospectively w.e.f. 1 June 1976

• As per Memorandum to Finance Bill

- Some judicial decisions have interpreted this definition in a manner which has raised doubts as to whether consideration for use of computer software is royalty or not …. Considering the conflicting decisions of various courts in respect of income in the nature of royalty and to restate the legislative intent, it is further proposed to amend the Income-tax Act ….

• India in its comment on the UN MC 2011 has recommended “The use of and right to use computer software irrespective of the medium through which such right is transferred is to be construed as ‘Royalty’ (Article 12)”

• As an observer member, India has reserved its positions on several paragraph of the OECD MC – cases of reservations which extend to software, ICS experience, undersea cables, payments for roaming calls, spectrum allocation, etc.

6

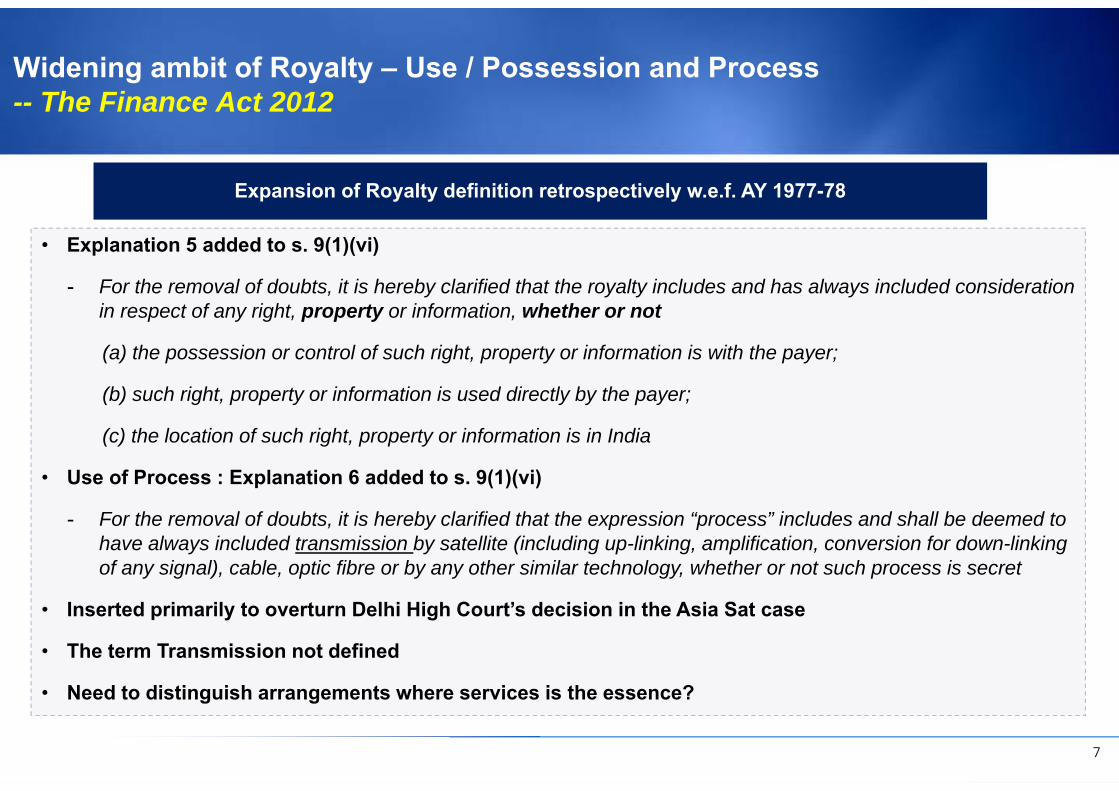

• Explanation 5 added to s. 9(1)(vi)

- For the removal of doubts, it is hereby clarified that the royalty includes and has always included consideration in respect of any right, property or information, whether or not

(a) the possession or control of such right, property or information is with the payer;

(b) such right, property or information is used directly by the payer;

(c) the location of such right, property or information is in India

• Use of Process : Explanation 6 added to s. 9(1)(vi)

- For the removal of doubts, it is hereby clarified that the expression “process” includes and shall be deemed to have always included transmission by satellite (including up-linking, amplification, conversion for down-linking of any signal), cable, optic fibre or by any other similar technology, whether or not such process is secret

• Inserted primarily to overturn Delhi High Court’s decision in the Asia Sat case

• The term Transmission not defined

• Need to distinguish arrangements where services is the essence?

Widening ambit of Royalty – Use / Possession and Process-- The Finance Act 2012

Expansion of Royalty definition retrospectively w.e.f. AY 1977-78

7

Taxation of R / FTS under the ITA (1 of 3)

• Section 90

• Relates to Agreements with Foreign Countries or Specified Territories

• Sub-Section 2: Provisions of the Act will prevail over provisions of DTAA to the extent they are more beneficial

• Sub-Section 3 : Term not defined in DTAA to have meaning as per Government Notification

• Sub-Section 4 : Tax Residency Certificate (TRC) from Overseas Authorities introduced from AY 2013-14

• Earlier TRC to contain prescribed details

• From 1 August 2013, stipulate prescribed details missing in TRC to be given in Form 10F by Payee

• Section 94A

• Relates to special Measures in respect of transactions with person located in notified jurisdictional area

• Parties deemed to be Associated Enterprise and transaction subject to Transfer Pricing provisions

• Deductibility of sum paid subject to certain conditions and Deemed income treatment for unexplained receipts

• Notwithstanding DTAA benefits, tax deductible to be 30% if higher as compared to applicable rates

8

Taxation of R / FTS under the ITA (1 of 3)

• Taxation on Gross basis under Section 115A

• Section encompasses gross basis of taxation for Interest, Royalties, Fees for Taxation of Services, etc.

• Prior to AY 2004-05, Gross basis of taxation applied only to R/ FTS income only of Foreign Companies

• R/ FTS - Stipulated conditions for agreements by NR with the Indian Concern (Payer)

• Agreement with Government, or

• Agreement to be approved by the Government; or

• In accordance with matter included in the Industrial Policy

• Currently, FEMA provisions should be relevant as it is the governing statute!

• Cases of NR to NR not fully covered as payer to be the Government or an Indian Concern

• Indian Branch of Foreign Company is an Indian Concern

• CBDT Circular 740 dated 17.4.96 and Bank of Credit & Commerce – Mum AT

• In absence of any written agreement or letter, beneficial rate does not apply [Six Continents Hotel (2015) Mum AT]

9

Taxation of R / FTS under the ITA (1 of 3)

• Position till AY 2013-14

• For agreements made on or after 1 June 1997 till 31 May 2005

• Taxation on gross basis under Section 115A read with Section 44D at 20% (+SC and EC)

• For agreements entered on or after 1 June 2005 - Basic rate of 10% on gross basis (+SC and EC)

• Section 44DA from AY 2004 -05 – Net basis taxation for PE (See Slide No. 12)

• Section 206AA introduced from AY 2010-11

• Initial withholding tax rate increased to 20% on gross basis if no PAN of NR.

• Rate not to be increased by Surcharge / Education cess

• The excess withholding tax can be claimed as refund in return of income post obtaining PAN

• If grossing up applies then the grossed up rate is to be compared with 20%

• This view is now supported by judicial precedents

• No lower deduction certificate under Section 197 unless PAN is available and quoted.

• Several other controversies surround Section 206AA including that it cannot override Tax Treaties

10

Taxation of R / FTS under the ITA (2 of 3)

• Position in AY 2014-15 & AY 2015-16

• Taxation on gross basis under Section 115A and net basis under Section 44DA

• Section 115A - Basic rate of tax increased to 25% on gross basis (+SC and EC) irrespective of agreement date

• In view of above, Section 206AA at 20% on gross basis not relevant if withholding tax rate if DTAA stipulates lower rate and TRC available but payee has no PAN in India

• Section 94A: Cyprus Notified from 1 November 2013

• Rate of withholding at 30% on gross basis if higher than applicable rate

• This is not a charging section but only withholding where payment is liable to withholding tax

• Position from AY 2016-17 for Section 115 A – Amendments by the Finance Act 2015

• Section 115A: Basic rate of tax reduced to 10% on gross basis (+SC and EC) irrespective of agreement date. Section 206AA results in higher initial withholding if no PAN.

• Section 115JB: R-FTS income of Non-Residents

• Specific exclusion of R/ FTS from books profits for Foreign Companies for purpose of Minimum Alternate Tax if R/FTS chargeable to tax at the rate or rates specified in Chapter XVII

11

Taxation of R / FTS under the ITA (3 of 3)

• Taxation on net basis - Section 44DA from AY 2004-05

• For R/ FTS effectively connected with PE of business / fixed place of profession of NR in India

• PE – As per Section 92F(iiia) of the Act

• The Supreme Court in Morgan Stanley (292 ITR 416) has held that PE definition in the Act is inclusive and would cover all types of PEs as per DTAA as well]

• Prior to AY 2004-05 / Section 44DA: R/ FTS were held to be taxable on gross basis even when attributable to PE

• This was due to gross basis taxation only under the ITA; and

• Where DTAA obliged computation of income in accordance with and subject to limitations of the ITA

• Several old Advance Rulings / Judicial precedents have upheld this position

12

Royalty -Model Conventions (MC)

• OECD MC

• Exclusive taxation in State of Residence unless attributable to PE of NR in the Source State

• Royalty = consideration for use / right to use of any copy right of literary, artistic or scientific work including cinematograph films, any patent, trademark, design or model, plan secret formula or process or for information concerning industrial, commercial or scientific experience

• UN MC

• Notable inclusions of industrial / commercial / scientific equipment

• Right to State of Source to tax on gross basis as well as net basis when attributable to PE / Fixed Base of Non-Resident

• Notable inclusions of Films / Tapes used for radio / TV broadcasting

• US MC

• Similar to OECD MC but no exclusive right to tax for State of Residence

• Notable exclusion of cinematographic films

• Notable inclusion for gains derived from alienation which is contingent on the productivity or use or disposition of the property

13

Brief Overview of Article 12 – Royalty in DTAA / UN MC

• Article 12(1) – Distribution of taxing rights between the Contracting States

• Article 12(2) – Right to taxation on gross basis by the State of Source subject to Beneficial Ownership

• Article 12(3) – Meaning of the term ‘Royalty’ – payments of any kind received as a consideration for the use or right to use of any copyright in …….or patents, trademarks, etc.

• Article 12(4) - Royalty taxation if effectively connected with PE / Fixed Base of NR in Source State

• Article 12(5) - Arising of Royalty in the State of Source

• Where payer is Resident; and / or

• If the Payer has a PE / Fixed Base in the State of Source and the Royalty is connected and borne by such PE / Fixed Base

• Article 12(6) – Adjustments for related party transactions / excess Royalty payments

• Excess over Arm’s-length price to be taxable as per domestic provisions

Royalty Article in Indian DTAAs is mostly on above lines and in most treaties R/FTS Article common

Concept of Beneficial Ownership and Most Favored Nation Clause also relevant 14

Under DTAA, limited accrual of R/FTS for NR to NR cases except in few tax treaties e.g. India-USA

Concept of Beneficial Ownership

• OECD MC (Articles 1, 10, 11 and 12)

• Improper use of conventions (Article 1)

• Articles - BO Term not to be used in a narrow or technical sense but object and purpose of tax conventions

• Agent, nominee and conduits, etc not BOs

• OECD MC 2014 incorporates several past documents / proposals for BO

• IBFD International Tax Glossary

• Beneficial owner is a common law term whose meaning has been developed by the Courts

• The term is distinct from the term ‘Legal Owner’

• Professor Klaus Vogel

• Beneficial owner is a person who is free to decide

• Whether or not the capital / assets should be used / made available for use by others

• How the yields from them should be used

• US Model Convention

• Regards beneficial owner as a person if the income is attributable to him for tax purposes as a resident

• Article 3(2) of Model Convention

• Whether meaning as per domestic tax law to be adopted? [India – Section 2(22) , Section 79, etc.]

• BO criteria present in Indian DTAAs

• CBDT Circular 789 dt .3 April 2000 under India–Mauritius DTAA issued in the context of FIIs, etc.: Tax Residency Certificates (‘TRCs’) issued by Mauritius Tax Authorities sufficient evidence of residence status as well as BO

Note: SC in Azadi Bachao Andolan (2003) - Circular prevails even if inconsistent with the Act for DTAA purposes

• Bom HC in Universal Music (2013) – TRC sufficient evidence of Beneficial Ownership

15

Most Favored Nation Clause

Most Favored Nation Clause

– More favorable DTAA terms granted to other countries extended to existing treaty countries by Source Country

– Could be lower tax rate or narrowing the scope of income liable to tax

– Generally MFN status is contained in the protocol/ exchange of notes

– MFN Clause is generally only prospective

– Application is automatically or by negotiation and then notification

Examples of key Indian tax treaties with MFN status in the context of R/ FTS

– India - Netherlands DTAA - India – Finland DTAA - India-UK DTAA

– India - Belgium DTAA - India – Hungary DTAA

– India - France DTAA - India – Israel DTAA

– India - Sweden DTAA - India – Kazakstan DTAA

– India - Switzerland DTAA - India – Saudi Arabia DTAA

– India - Spain DTAA - India – Philippines DTAA

16

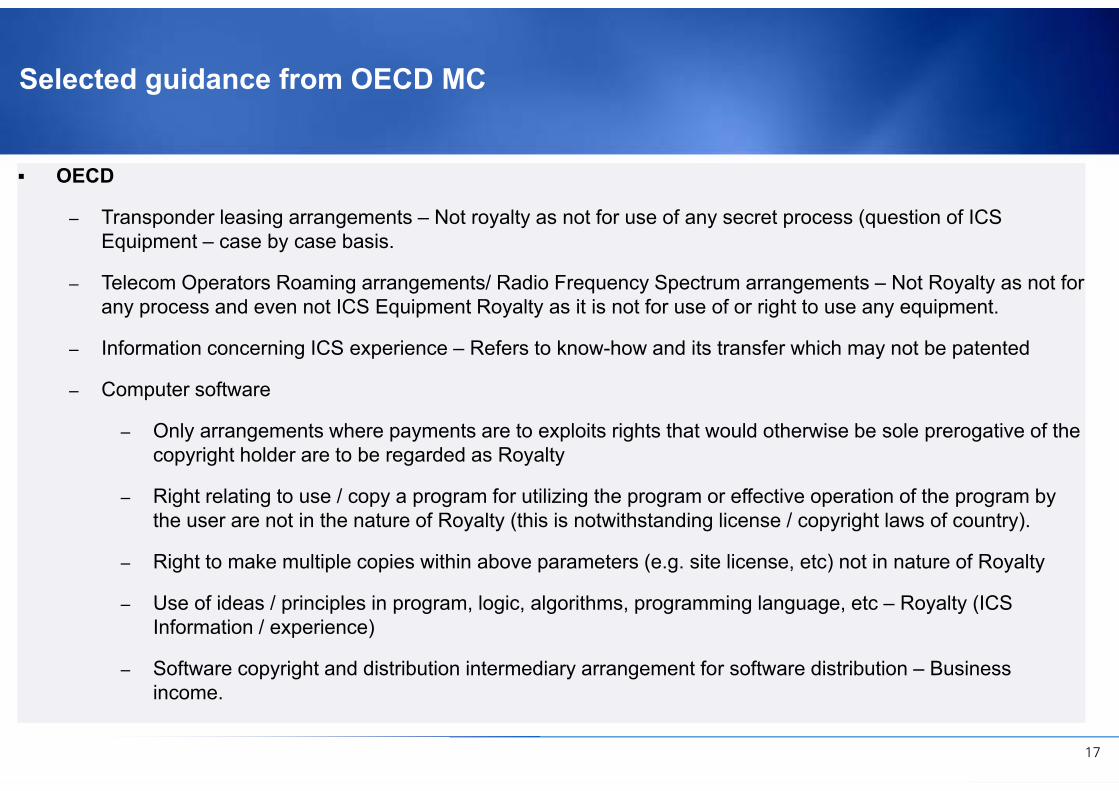

Selected guidance from OECD MC

OECD

– Transponder leasing arrangements – Not royalty as not for use of any secret process (question of ICS Equipment – case by case basis.

– Telecom Operators Roaming arrangements/ Radio Frequency Spectrum arrangements – Not Royalty as not for any process and even not ICS Equipment Royalty as it is not for use of or right to use any equipment.

– Information concerning ICS experience – Refers to know-how and its transfer which may not be patented

– Computer software

– Only arrangements where payments are to exploits rights that would otherwise be sole prerogative of the copyright holder are to be regarded as Royalty

– Right relating to use / copy a program for utilizing the program or effective operation of the program by the user are not in the nature of Royalty (this is notwithstanding license / copyright laws of country).

– Right to make multiple copies within above parameters (e.g. site license, etc) not in nature of Royalty

– Use of ideas / principles in program, logic, algorithms, programming language, etc – Royalty (ICS Information / experience)

– Software copyright and distribution intermediary arrangement for software distribution – Business income.

17

Royalty – Situations under India DTAAs (Illustrative)

• Situation 1 - Presence of Article on Royalty akin to ITA

• Taxation on gross basis

• Taxation / implications very similar to that under ITA

• Simpler method of taxation for non-residents

• Situation 2 - Scope and accrual of Royalty Article restrictive as compared to ITA

• Scope is narrower especially with respect to coverage of ICS equipments, etc.

• NR to NR payments accrual in India is generally more restrictive except in some cases e.g. India-USA DTAA

• Situation 3 – Scope / taxation rate of Royalty Article more as compared to ITA

• Scope exhaustive especially for cinematographic films, gains on alienation, etc

• Rate could be higher e.g. USA at 15% on gross basis.

• Non-Resident governed by beneficial provisions of the Act

• Situation 4 - Royalty attributable / effectively connected with PE in India

• Taxation on net basis for income attributable to the PE

• Onerous compliances / obligations / costs 18

19

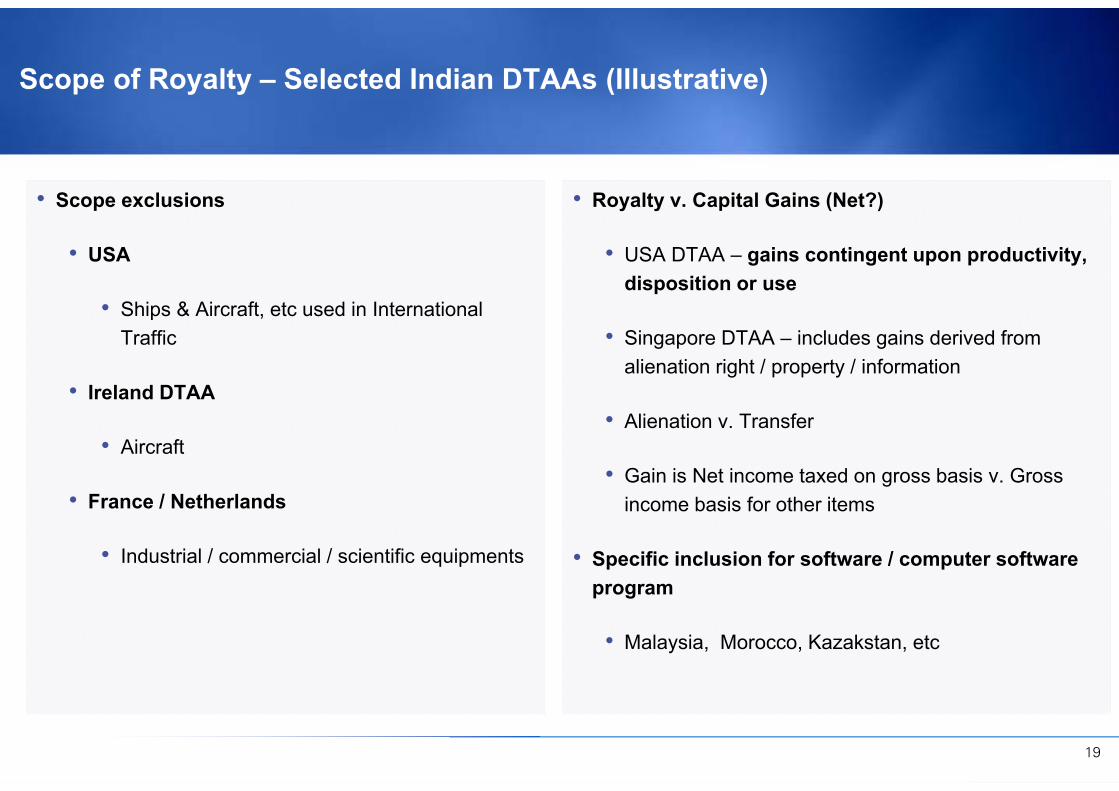

Scope of Royalty – Selected Indian DTAAs (Illustrative)

• Scope exclusions

• USA

• Ships & Aircraft, etc used in International Traffic

• Ireland DTAA

• Aircraft

• France / Netherlands

• Industrial / commercial / scientific equipments

• Royalty v. Capital Gains (Net?)

• USA DTAA – gains contingent upon productivity, disposition or use

• Singapore DTAA – includes gains derived from alienation right / property / information

• Alienation v. Transfer

• Gain is Net income taxed on gross basis v. Gross income basis for other items

• Specific inclusion for software / computer software program

• Malaysia, Morocco, Kazakstan, etc

R / FTS – meaning of ‘paid’ and impact on deemed accrual

OECD MC on Article 12

• The term ‘payment’ has a very wide meaning i.e. fulfillment of the obligation to put funds at the disposal of the creditor in the manner required by the contract or by custom

R/ FTS held to be taxable only when ‘paid’ to Non-Residents – selected decisions

• Siemens Aktiengesellschaft (2012) Bom HC: India-Germany DTAA

• Pizza Hut International (2012) – Del AT: India- USA DTAA

• CSC Technology (2012) – Del AT: India-Singapore DTAA

• Booz, Allen & Hamilton – (2013) Mum AT / others (In absence of RBI approval, no accrual of income as well)

• Johnson and Johnson v ADIT (2013) Mum AT

Paid – defined under Section 43(2) of the Income-tax Act 1961

• ‘Paid’ means actually paid or incurred according to the method of accounting

• Whether above definition relevant for Article 3(2) and can be imported for DTAAs?

20

R-FTS - Retrospective amendments

Whether impact DTAA?

• MC / DTAA Article 3(2) - Terms not defined to have meaning under the applicable tax laws of Source State (Right to tax) prevailing over a meaning given to the term under other laws of the Contracting State

• OECD / UN MC - Recommends Ambulatory approach of interpretation over static approach

• B4U International (2012) - Mum AT

• Payments for hiring of Transponder not Royalty as amendments have no affect as no change in DTAA

• WNS (Mum AT), Nokia (Del HC) and other judicial precedents support the above principles

• Adverse judicial precedents – Verizon (Mad HC / 2013) / Viacom 18 (Mum AT / 2015) / Others

Whether create retrospective withholding tax obligations or Disallowance under Section 40(a)(i)?

• No - Lex non Cogit ad impossiblia: Law cannot compel a person to do something which is impossible – a principle upheld by several decisions of the Supreme Court and several other judicial precedents

• Judicial precedents also suggest that Section 40(a)(i) refer to Explanation 2 to Section 9(1)(vi) and not the other recent Explanations and so no disallowance can be made for coverage within those Explanations

21

Royalty – selected key issues controversies -- several judicial precedents can be found on each proposition

Royalty

• Tax planning – Royalty v. Services? Reimbursements?

• Computer Software / use of other copyrighted products

• Software embedded in Hardware

• Payments for use of Satellite / Transponder

• Payments for Leased Line / Bandwidth / Circuits / Inter-connectivity

• Payments for Live Telecast

• Payments for online database access / subscription

• Accreditation arrangements (Hospitals, etc)

• Website use / hosting, advertising portal, etc

• Payments for ships – dry lease v. wet lease

• Cases of Know-How and Industrial, commercial and scientific experiences

• Cases of Business income & Cases of Capital Gains

• E-commerce payments through website using credit cards

22

Domestic TDS controversies / decisions now

also relevant as domestic

payments falling within ambit of

Section 9(1)(vi)/(vii) are liable for TDS under Section 194J of the Act w.e.f 13.7.2006

Tax Planning

Marriott International Inc., USA (2015) Mumbai ITAT

• Marriott Entities had Agreements to carry out following ‘sales and marketing services’ with Indian Hotel Entities:

• International Sales and Marketing Services;

• Reimbursement of expenses for provision of centralized and other services;

• International Sales and Marketing Fees

• Decision of the Mumbai Tribunal

• Marriott group, through inter-linkages of agreements, resorted to tax planning by dissecting one single transaction into more than one.

• All Marriott Contracting Entities have the same address and even franchise marketing / publicity support fee paid as percentage of gross revenue.

• The responsibility to maintain and / or enhance the brand value remains with the brand owner who has responsibility to incur expenditure for the same and so also the various marketing / sales services were for promotion of brands with no individual relation to the Indian Hotels

• The Tribunal treated the arrangement as colorable device, lifted the corporate veil, overruling all favourablecourt decisions for hospitality companies including in Marriott own’s entities / cases.

• The receipts from Indian hotels for various marketing/sales services and reimbursements – Royalty in nature

23

Revenue Authorities

Supply of software involves use / right to use of following:

copyright,

patent,

Invention,

process, or

scientific work

Taxable in India as royalty on gross basis

Taxpayers

Supply of software does not involve any use / right to use of copyright, patent, invention or process

It is for use of a copyrighted product / article and thus, business income, not taxable in India in the absence of any PE in India

Reliance placed on OECD and International commentaries

Software supply

Whether Royalty?

Whether Business Income?

Characterisation of receipts from software supply by foreign companies / entities / persons

Software Taxability

Issue under litigation in a number of cases pre and

post introduction of Explanation 4 to Section 9(1)(vi)

24

Recent / 2015 - Software decisions

In Favor of Assessee

• WS Atkins India (2015) – Bang AT (Section 194J)

• Purchase of software is purchase of copyrighted article and cannot be considered as payment for any commercial exploitation i.e. making copies, selling or acquiring to fall within the ambit of Royalty

• Lionbridge Technologies (2015) – Mum AT

• Purchase of standard off shelves software by overseas group entity from third party (and not developing the same on its own) and allocation of cost amongst other group entities was mere reimbursement not chargeable to tax, so no withholding tax requirement arises.

• Locuz Enterprise (2015) – Hyd AT

• NR was a reseller of software products and therefore transaction was in the nature of trade. Payments did did not fall within the ambit of Royalty

25

Against the Assessee

• Rational Software (2015) - Kar HC

• Payment for software products/purchased is in the nature of Royalty – Followed its earlier decisions in Samsung, etc

• Autodesk Asia Pte Ltd (2015) Bang AT

• Payment received for sale of software license to end user customers in India through distributors and retailers would amount to royalty.

Recent / 2015 – Software embedded in Hardware

In favor of Assessee

• Alcatel Lucent Canada (2015) – Delhi HC

• Supply of Software that is loaded on hardware as anintegral part and does not have any independentexistence.

• Software so embedded in hardware mere facilitatesfunctioning of equipment and is an integral part ofthereof.

• Supreme Court decision in TCS followed – Softwareon Media would be goods.

• Consideration for supply of software was not Royalty

• Also following previous ruling in case of Ericsson A.B.and Nokia Networks, the High court dismissed theappeal by Revenue that payments constitutedRoyalty.

26

Recent / 2015 – Software / Contents

27

Against the Assesee

• Skillsoft Ireland (2015) – AAR

• Indian Company under reseller agreement distributes skillsoft products i.e. courses as well as software through which it is delivered to customers

• Assessee argued that the payments are akin to payments for books and end-user is only granted only non-exclusive / non-transferable license and therefore not Royalty.

• AAR followed its few earlier Rulings and held that license of specially design software and simulations falls within the ambit of literary work i.e. Royalty

• CBDT Safe Harbour Notification held not applicable as construed limited to those provisions/ proceedings.

Recent / 2014 & 2015 – Live Telecast

• Delhi Race Club (1940) Limited (2014) – Delhi HC [In favor of Assesee]

• Decision in the context of Section 194J of the Act

• In clause (v) of Explanation 2 to Section 9(1)(vi) – Royalty

• “The transfer of all or any rights (including the granting of a license) in respect of any copyright , literary, artistic or scientific work including films… “

• The word ‘in’ inserted by the Court “The transfer of all or any rights (including the granting of a license) in respect of any copyright in literary, artistic or scientific work including films… “

• Reasons: copyright does not synchronize with the word literary, artistic or scientific work as they are the work in which copyright exists. Plain reading is meaningless. Court has power to add a word in the Statute in required cases.

• Live telecast is in nature of broadcast under the Copyright Act and no copyright in it subsists under Section 13 of the said Act – thus, payments for live telecast not in the nature of Royalty

• Whether the above analogy supports cases of computer software?

• IMG Media Ltd (2015 / Mum AT) – [In favor of Assessee]

• Production of program feed for live audio / video coverage of cricket matches not FIS under India-USA DTAA

• Producer has no ownership rights so it cannot give it any right to use – Therefore not Royalty

28

Recent / 2015 – Transfer v. Royalty

In favor of Assessee

• S.P. Alaguvel (2015) – Madras HC

• Payments for perpetual transfer of satellite rights for period of 99 years is Sale in terms of S. 26 of Copyright Act and thereforenot in nature of Royalty under Clause 5 of Explanation 2 of S. 9(1)(vi) of Income-tax Act.

• Andhra Petrochemicals Limited (2015) – Andhra Pradesh HC

• Payments for transfer of patent an other technical know-how not related to any particular period is not in the nature of Royaltybut business profits.

• Heubach Colour Private Limited (2015) – Ahmedabad AT

• Payment for goodwill, know-how and trademark where seller had transferred its entire right, title and interest and ownership inthe assets is not in the nature of Royalty

Against the Assessee

• HCL Limited (2015) – Delhi HC

• Payment for use of IPR’s / know-how to develop local system builders/software programmes and equipment, for five yearswith confidentiality obligation that would subsist post termination is not transfer of ownership but payment for right to use inthe nature of Royalty.

29

Recent / 2015 – Telecom

• Qualcomm Incorporated, USA (2015) – Delhi AT

• Payment for application development platform for mobiles phones that enabled mobile phone user to download application games, sending messages, sharing photos, etc. was payment for software which was for a copyrighted article and not copyright itself – Not Royalty under Section 9(1)(vi) / Article 12 of DTAA

• Royalty paid to NR by OEM manufacturing units / handset outside India which were sold in India – situs is manufacturing of products and not sales even where units / handsets were India specific.

• Flag Telecom Bermuda (2015) – Mumbai AT

• Capacity in Cable systems – Transfer of ownership rights and obligations for 25 years which coincided with the life of cables is not in the nature of payment for use or right to use capacity in cable.

• Vodafone South (2015) – Ban AT

• Carriage and Inter-connectivity charges paid to overseas telecom operators falls within Explanation 6 of Section 9(1)(vi) and in the nature of ‘process’ and taxable as Royalty

• Explanation 6 also relevant for the purpose of Tax Treaty pursuant to Article 3(2)

30

Case Study

• Facts

• AUSA is a USA Company and BIND is an Indian Company and both are engaged in Pharma Sector

• For a new Molecule under development (the Product), AUSA has agreed to grant to BIND an exclusive, worldwide, royalty bearing license with the right to grant sublicense to manufacturer, have manufactured, market, use or sell, offer to sell, import, export or otherwise dispose off the product.

• Post acquisition BIND to register or transfer the product / patent in its own name.

• BIND is obliged to make payments to AUSA towards the following:

• A lumpsum fees of USD 5 Mn and Reimbursement of certain expenses incurred by AUSa to develop the Molecule

• A Royalty equal to 2% of the sales of any commercial product manufactured by BIND or any persons authorized by BIND till the life of the patent.

• Marketing expenses on cost plus basis incurred to help BIND sale the products globally

• Questions

• Outline Indian Income-tax implications of the payments proposed and improvement opportunities, if any.

31

Questions

Answers

Presenter’s contact detailsName: Shabbir Motorwala

Email: [email protected]

THANK YOU ALL FOR YOUR ATTENTION !

The views in this presentation are personal views of the Presenter. Further, the information contained is of a general naturefor explaining the topics and issues. The presentation is not intended to serve as an advice or address the circumstances ofany particular individual or entity. Although, the endeavor is to provide accurate and timely information, there can be noguarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future.No one should act on such / this information without appropriate professional advice which is possible only after a thoroughexamination of facts / particular situation.