working with financial statements

DESCRIPTION

Chapter Three. Working With Financial Statements. Key Concepts and Skills. Understand sources and uses of cash and the Statement of Cash Flows Know how to standardize financial statements for comparison purposes Know how to compute and interpret important financial ratios - PowerPoint PPT PresentationTRANSCRIPT

© 2003 The McGraw-Hill Companies, Inc. All rights reserved.

Working With Financial Statements

Chapter

Three

3.2

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Key Concepts and Skills

• Understand sources and uses of cash and the Statement of Cash Flows

• Know how to standardize financial statements for comparison purposes

• Know how to compute and interpret important financial ratios

• Be able to compute and interpret the Du Pont Identity

• Understand the problems and pitfalls in financial statement analysis

3.3

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Chapter Outline

• Cash Flow and Financial Statements: A Closer Look

• Standardized Financial Statements

• Ratio Analysis

• The Du Pont Identity

• Using Financial Statement Information

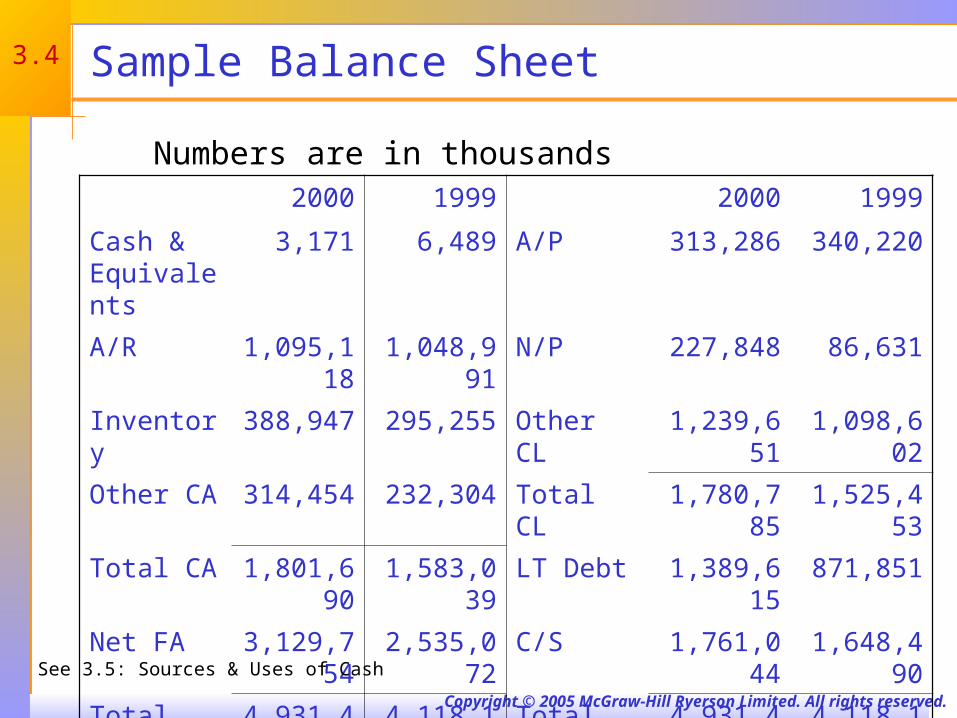

3.4

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Sample Balance Sheet

2000 1999 2000 1999

Cash & Equivalents

3,171 6,489 A/P 313,286 340,220

A/R 1,095,118 1,048,991 N/P 227,848 86,631

Inventory 388,947 295,255 Other CL 1,239,651 1,098,602

Other CA 314,454 232,304 Total CL 1,780,785 1,525,453

Total CA 1,801,690 1,583,039 LT Debt 1,389,615 871,851

Net FA 3,129,754 2,535,072 C/S 1,761,044 1,648,490

Total Assets 4,931,444 4,118,111 Total Liab. & Equity

4,931,444 4,118,111

Numbers are in thousands

See 3.5: Sources & Uses of Cash

3.5

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Sample Income Statement

Revenues 4,335,491

Cost of Goods Sold 1,762,721

Expenses 1,390,262

Depreciation 362,325

EBIT 820,183

Interest Expense 52,841

Taxable Income 767,342

Taxes 295,426

Net Income 471,916

EPS 2.29

Dividends per share 0.54

Numbers are in thousands, except EPS & DPS

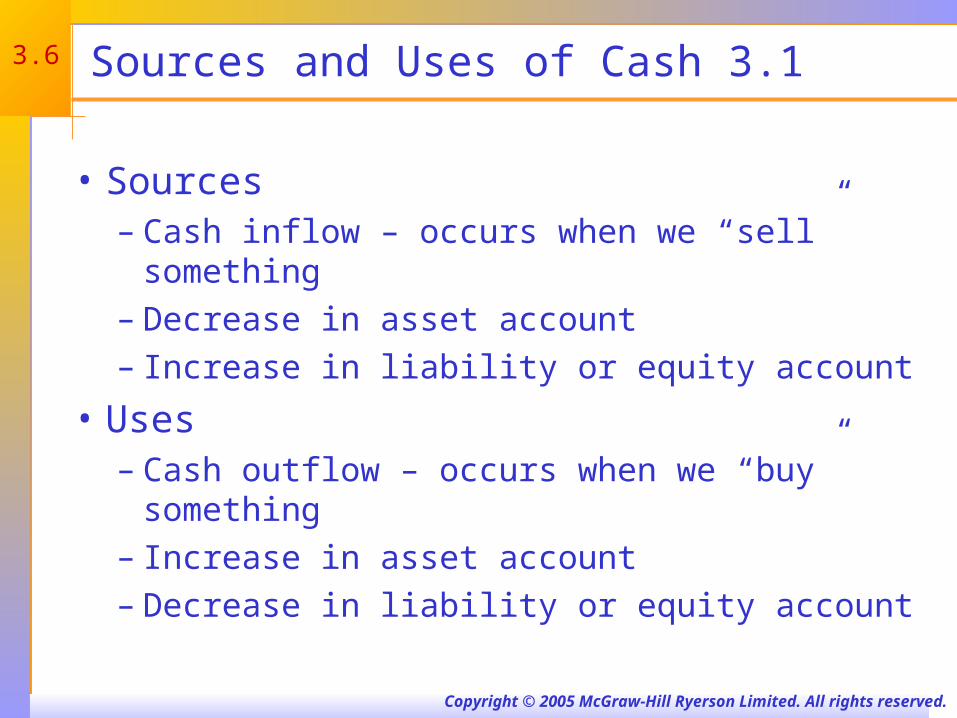

3.6

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Sources and Uses of Cash 3.1

• Sources– Cash inflow – occurs when we “sell” something– Decrease in asset account– Increase in liability or equity account

• Uses– Cash outflow – occurs when we “buy” something– Increase in asset account– Decrease in liability or equity account

3.7

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Statement of Cash Flows

• Statement that summarizes the sources and uses of cash

• Changes divided into three major categories– Operating Activity – includes net income and

changes in most current accounts– Investment Activity – includes changes in fixed

assets– Financing Activity – includes changes in notes

payable, long-term debt and equity accounts as well as dividends

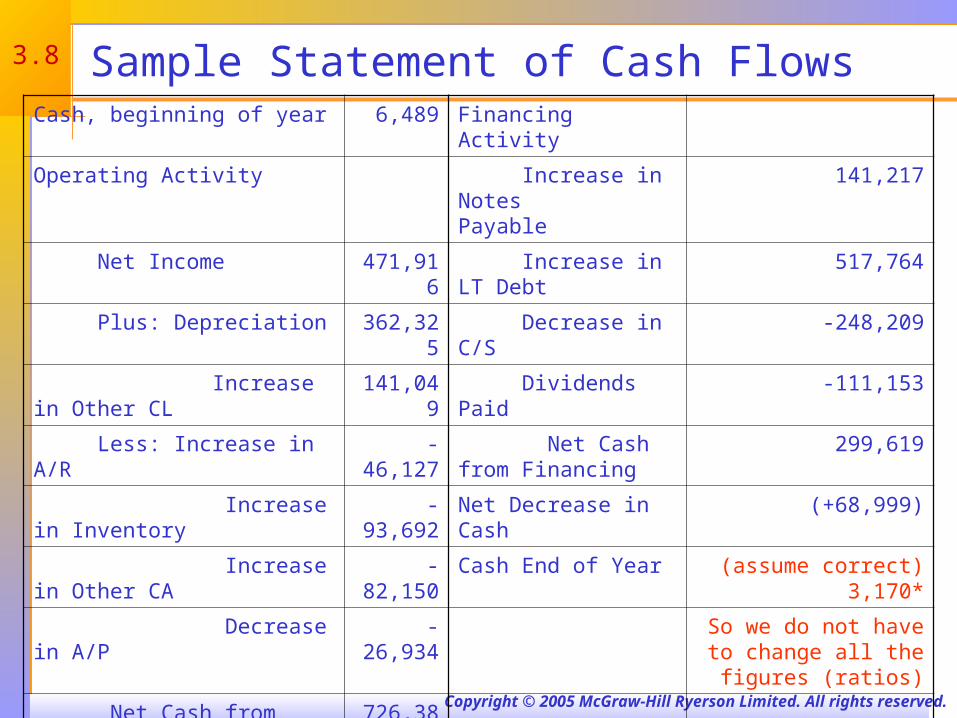

3.8

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Sample Statement of Cash FlowsCash, beginning of year 6,489 Financing Activity

Operating Activity Increase in Notes Payable

141,217

Net Income 471,916 Increase in LT Debt 517,764

Plus: Depreciation 362,325 Decrease in C/S -248,209

Increase in Other CL 141,049 Dividends Paid -111,153

Less: Increase in A/R -46,127 Net Cash from Financing

299,619

Increase in Inventory -93,692 Net Decrease in Cash (+68,999)

Increase in Other CA -82,150 Cash End of Year (assume correct) 3,170*

Decrease in A/P -26,934 So we do not have to change all the figures

(ratios)

Net Cash from Operations 726,387

Investment Activity

Fixed Asset Acquisition -957,007

Net Cash from Investments -957,007 *Difference due to rounding of dividends

3.9

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

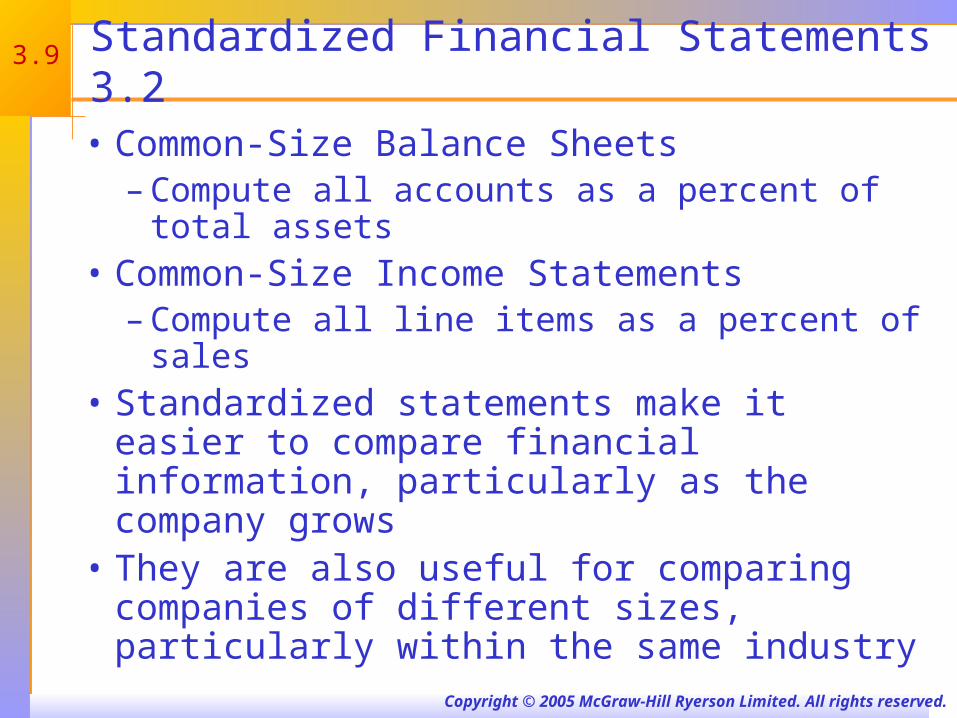

Standardized Financial Statements 3.2

• Common-Size Balance Sheets– Compute all accounts as a percent of total

assets• Common-Size Income Statements

– Compute all line items as a percent of sales• Standardized statements make it easier to

compare financial information, particularly as the company grows

• They are also useful for comparing companies of different sizes, particularly within the same industry

3.10

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Ratio Analysis 3.3

• Ratios also allow for better comparison through time or between companies

• As we look at each ratio, ask yourself what the ratio is trying to measure and why is that information important

• Ratios are used both internally and externally

3.11

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Categories of Financial Ratios

• Short-term solvency or liquidity ratios

• Long-term solvency or financial leverage ratios

• Asset management or turnover ratios

• Profitability ratios

• Market value ratios

3.12

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

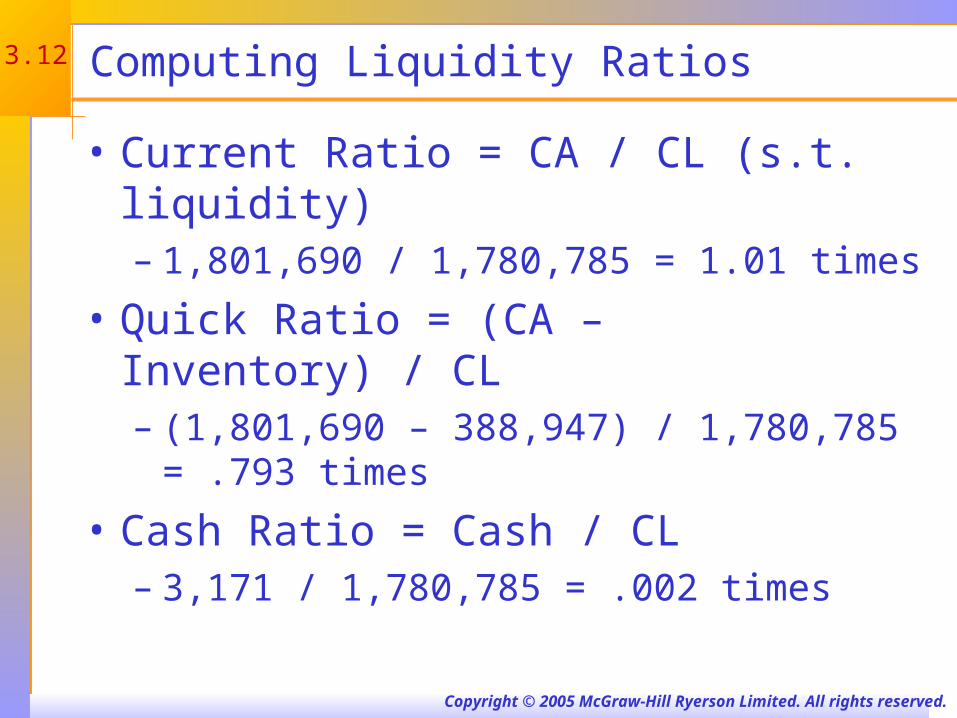

Computing Liquidity Ratios

• Current Ratio = CA / CL (s.t. liquidity)– 1,801,690 / 1,780,785 = 1.01 times

• Quick Ratio = (CA – Inventory) / CL– (1,801,690 – 388,947) / 1,780,785 = .793 times

• Cash Ratio = Cash / CL– 3,171 / 1,780,785 = .002 times

3.13

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Computing Long-term Solvency Ratios

• Total Debt Ratio = (TA – TE) / TA– (4,931,444 – 1,761,044) / 4,931,444 = .6429 times

or 64.29%– The firm finances a little over 64% of its assets

with debt.

• Debt/Equity = TD / TE– (4,931,444 – 1,761,044) / 1, 761,044 = 1.800

times

• Equity Multiplier = TA / TE = 1 + D/E– 1 + 1.800 = 2.800

3.14

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Computing Coverage Ratios

• Times Interest Earned = EBIT / Interest– 820,183 / 52,841 = 15.5 times

• Cash Coverage = (EBIT + Depreciation) / Interest– (820,183 + 362,325) / 52,841 = 22.38 times

3.15

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

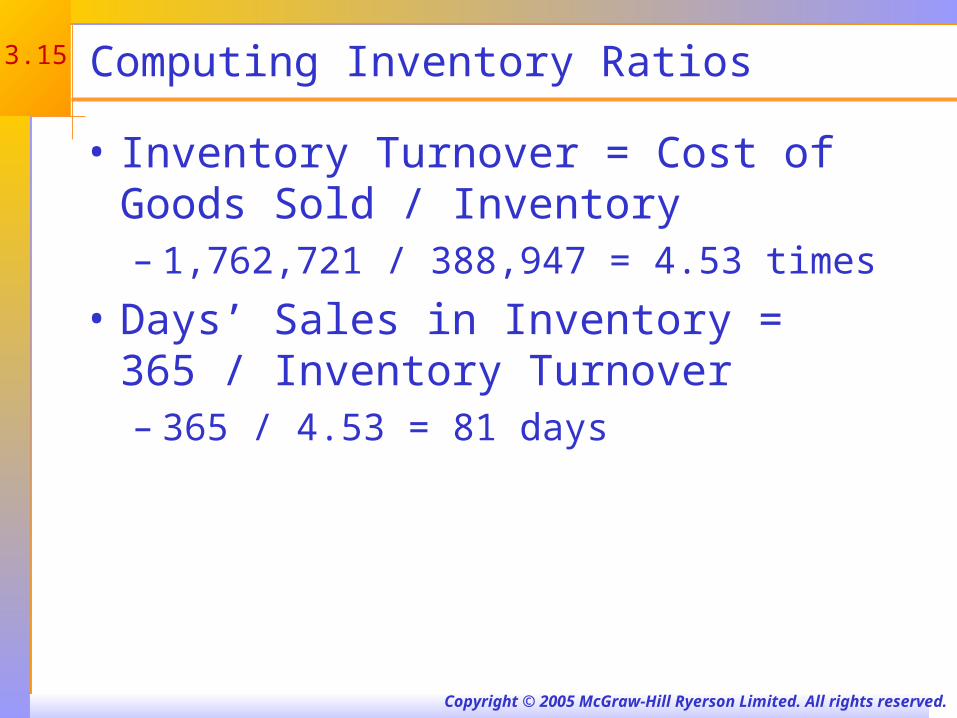

Computing Inventory Ratios

• Inventory Turnover = Cost of Goods Sold / Inventory– 1,762,721 / 388,947 = 4.53 times

• Days’ Sales in Inventory = 365 / Inventory Turnover– 365 / 4.53 = 81 days

3.16

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Computing Receivables Ratios

• Receivables Turnover = Sales / Accounts Receivable– 4,335,491 / 1,095,118 = 3.96 times

• Days’ Sales in Receivables = 365 / Receivables Turnover– 365 / 3.96 = 92 days

3.17

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Computing Total Asset Turnover

• NWC Turnover = Sales / NWC– 4,335,491 / (1,801,690 - 1,780,785) = 207.390 times

• Fixed Asset Turnover = Sales / Net Fixed Assets– 4,335,491 / 3,129,754 = 1.385 times

• Total Asset Turnover = Sales / Total Assets– 4,335,491 / 4,931,444 = .88 times

• Measure of asset use efficiency• Not unusual for TAT < 1, especially if a firm has a

large amount of fixed assets

3.18

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Computing Profitability Measures

• Profit Margin = Net Income / Sales– 471,916 / 4,335,491 = .1088 times or 10.88%

• Return on Assets (ROA) = Net Income / Total Assets– 471,916 / 4,931,444 = .0957 times or 9.57%

• Return on Equity (ROE) = Net Income / Total Equity– 471,916 / 1,761,044 = .2680 times or 26.8%

3.19

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Computing Market Value Measures

• Market Price = $60.98 per share

• Shares outstanding = 205,838,910

• PE Ratio = Price per share / Earnings per share– 60.98 / 2.29 = 26.62 times

• Market-to-book ratio = market value per share / book value per share– 60.98 / (1,761,044,000 / 205,838,910) = 7.1 times

3.20

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

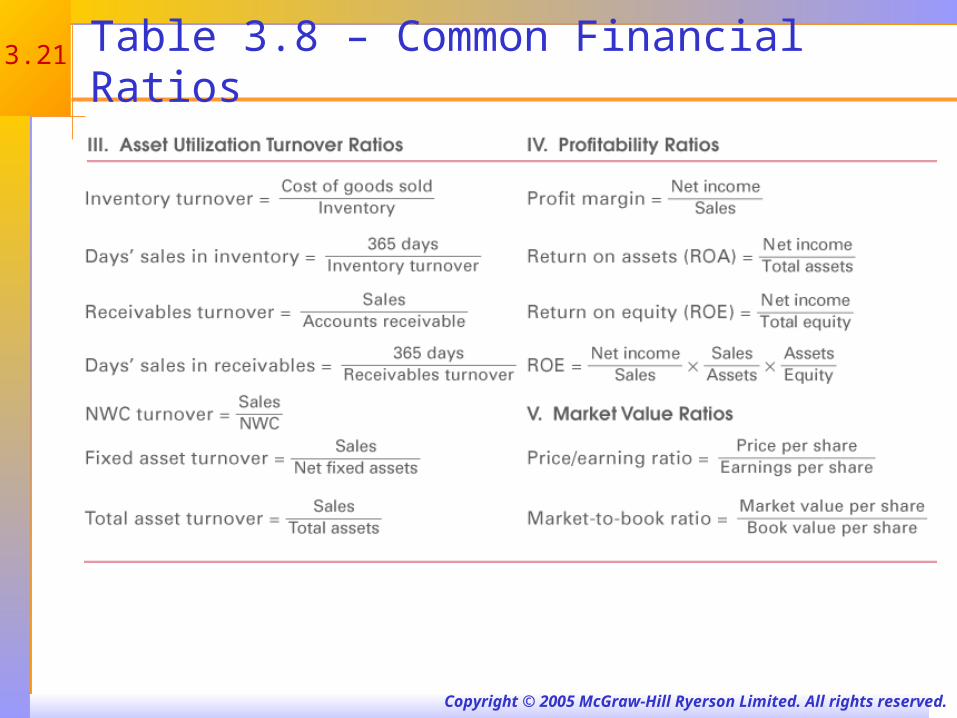

Table 3.8 – Common Financial Ratios

3.21

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Table 3.8 – Common Financial Ratios

3.22

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

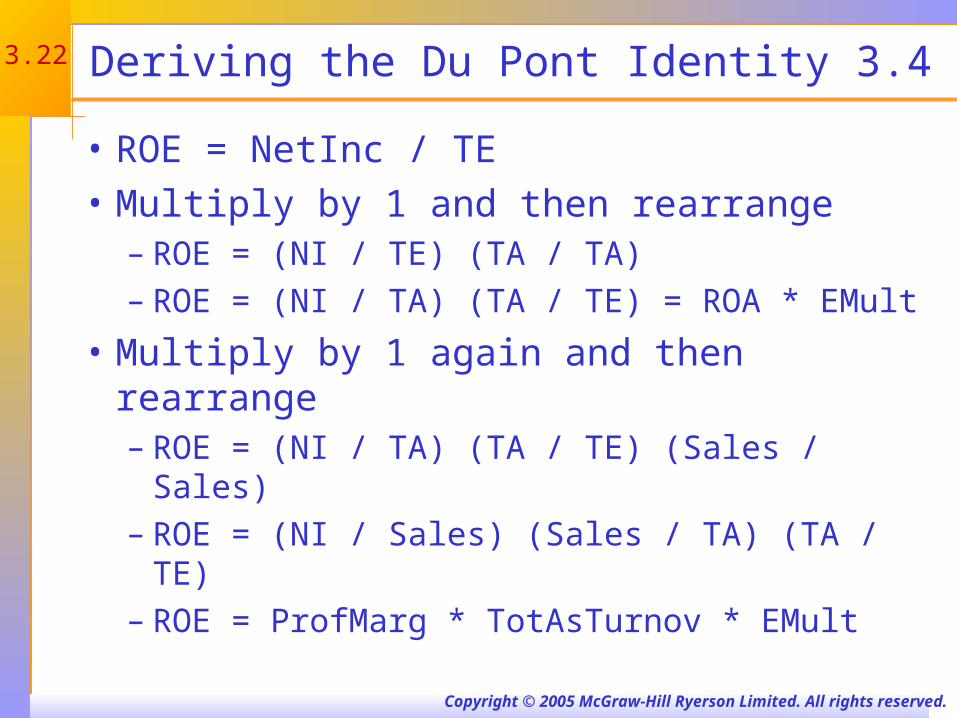

Deriving the Du Pont Identity 3.4

• ROE = NetInc / TE

• Multiply by 1 and then rearrange– ROE = (NI / TE) (TA / TA)– ROE = (NI / TA) (TA / TE) = ROA * EMult

• Multiply by 1 again and then rearrange– ROE = (NI / TA) (TA / TE) (Sales / Sales)– ROE = (NI / Sales) (Sales / TA) (TA / TE)– ROE = ProfMarg * TotAsTurnov * EMult

3.23

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

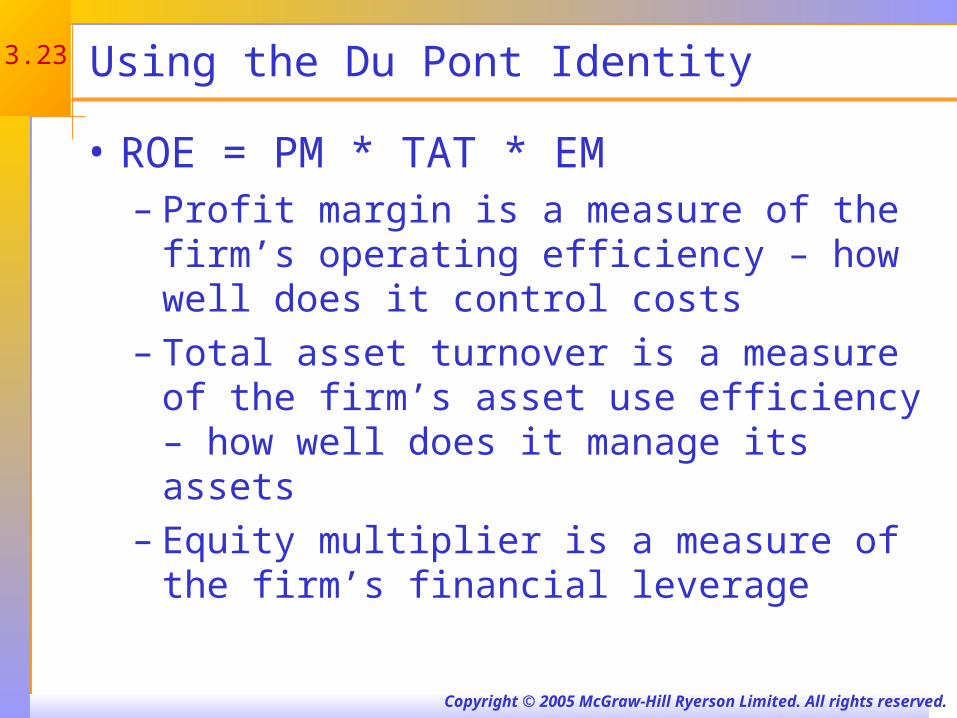

Using the Du Pont Identity

• ROE = PM * TAT * EM– Profit margin is a measure of the firm’s operating

efficiency – how well does it control costs– Total asset turnover is a measure of the firm’s

asset use efficiency – how well does it manage its assets

– Equity multiplier is a measure of the firm’s financial leverage

3.24

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

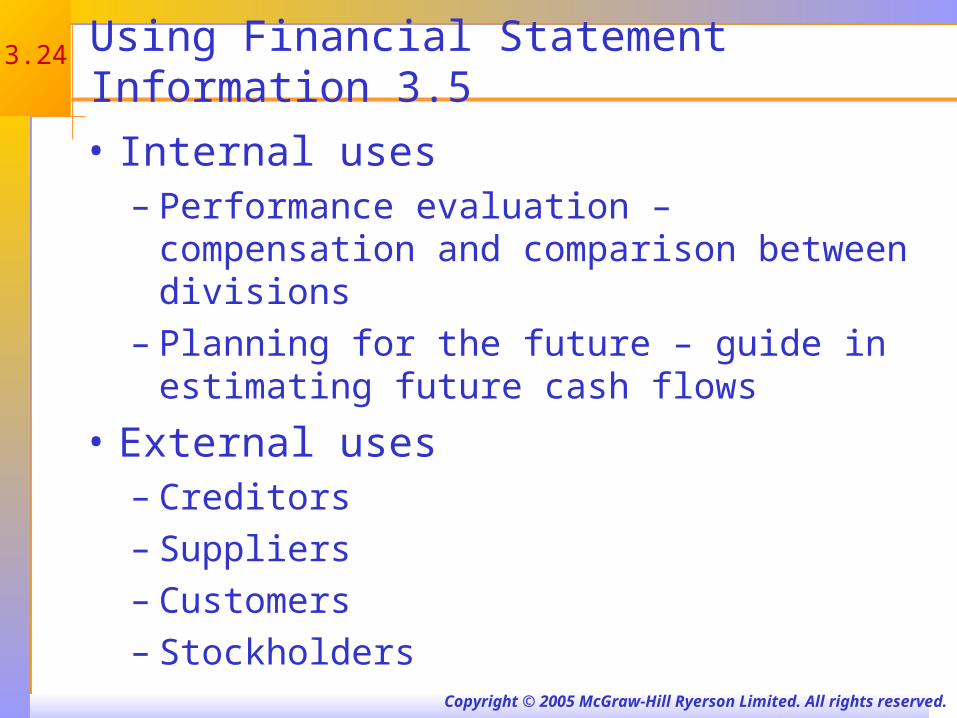

Using Financial Statement Information 3.5

• Internal uses– Performance evaluation – compensation and

comparison between divisions– Planning for the future – guide in estimating future

cash flows

• External uses– Creditors– Suppliers– Customers– Stockholders

3.25

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

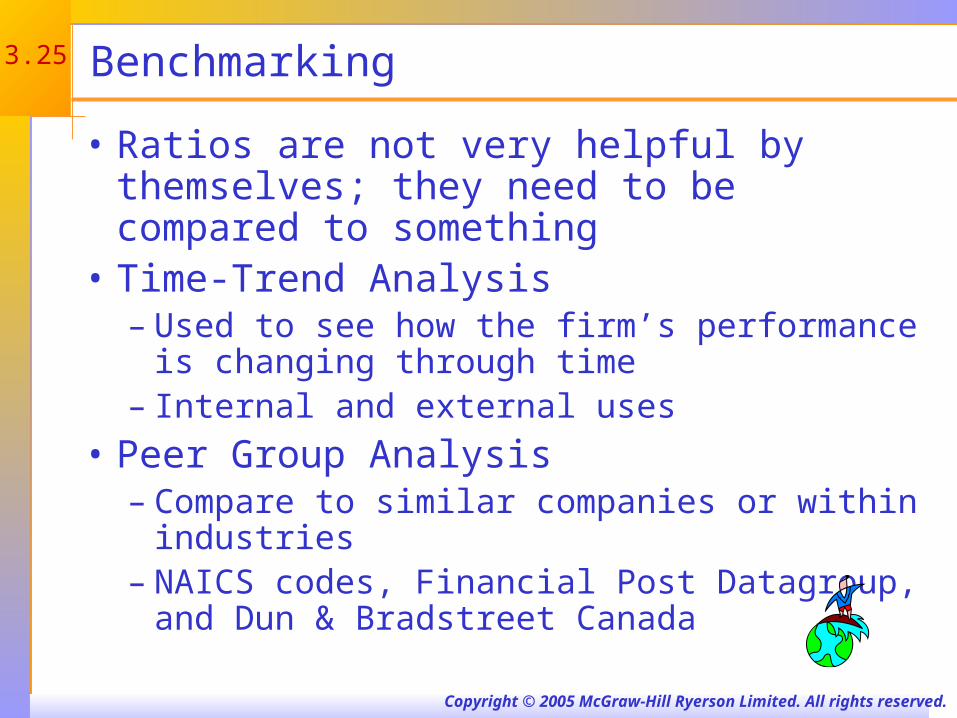

Benchmarking

• Ratios are not very helpful by themselves; they need to be compared to something

• Time-Trend Analysis– Used to see how the firm’s performance is

changing through time– Internal and external uses

• Peer Group Analysis– Compare to similar companies or within industries– NAICS codes, Financial Post Datagroup, and Dun

& Bradstreet Canada

3.26

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Potential Problems

• There is no underlying theory, so there is no way to know which ratios are most relevant

• Benchmarking is difficult for diversified firms• Globalization and international competition

makes comparison more difficult because of differences in accounting regulations

• Varying accounting procedures, i.e. FIFO vs. LIFO

• Different fiscal years• Extraordinary events

3.27

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Quick Quiz

• What is the Statement of Cash Flows and how do you determine sources and uses of cash?

• How do you standardize balance sheets and income statements and why is standardization useful?

• What are the major categories of ratios and how do you compute specific ratios within each category?

• What are some of the problems associated with financial statement analysis?

3.28

Copyright © 2005 McGraw-Hill Ryerson Limited. All rights reserved.

Summary 3.6

• You should be able to:– Identify sources and uses of cash– Understand the Statement of Cash Flows– Understand how to make standardized financial

statements and why they are useful– Calculate and evaluate common ratios– Understand the Du Pont identity– Describe how to establish benchmarks for

comparison purposes and understand some key problems that can arise