working together as a leadership team in a downturn - part 1

TRANSCRIPT

WORKING TOGETHER AS A LEADERSHIP TEAM IN A DOWNTURN: HR, OPERATIONAL AND BUSINESS PERSPECTIVES

Moderator: Brad MacLean Industry Culture Consultant, NOVA Cultural Improvement

Ray Gonzales VP of HR, Continental Resources

Marty Kunz VP of HR, C&J Energy

James Tastard VP of HR, Freeport LNG

Luis Jimenez HR and Total Rewards Executive

GENERAL SESSION

STRATEGIES & OPPORTUNITIES: MANAGING IN A TURBULENT OIL & GAS WORLD

HR and Business: Working Together in

a Downturn

Leading the American Energy Renaissance

April 2, 2015

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 3

Forward-Looking Information Cautionary Statement for the Purpose of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act of 1995 This presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements included in this presentation other than statements of historical fact, including, but not limited to, statements or information concerning the Company’s future operations, performance, financial condition, production and reserves, schedules, plans, timing of development, returns, budgets, costs, business strategy, objectives, and cash flow, are forward-looking statements. When used in this presentation, the words “could,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “budget,” “plan,” “continue,” “potential,” “guidance,” “strategy,” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. Forward-looking statements are based on the Company’s current expectations and assumptions about future events and currently available information as to the outcome and timing of future events. Although the Company believes the expectations reflected in the forward-looking statements are reasonable and based on reasonable assumptions, no assurance can be given that such expectations will be correct or achieved or that the assumptions are accurate. When considering forward-looking statements, readers should keep in mind the risk factors and other cautionary statements described under Part I, Item 1A. Risk Factors included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013, registration statements and other reports filed from time to time with the Securities and Exchange Commission (“SEC”), and other announcements the Company makes from time to time. The Company cautions readers these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond the Company’s control, incident to the exploration for, and development, production, and sale of, crude oil and natural gas. These risks include, but are not limited to, commodity price volatility, inflation, lack of availability of drilling, completion and production equipment and services and transportation infrastructure, environmental risks, drilling and other operating risks, lack of availability and security of computer-based systems, regulatory changes, the uncertainty inherent in estimating crude oil and natural gas reserves and in projecting future rates of production, cash flows and access to capital, the timing of development expenditures, and the other risks described under Part I, Item 1A. Risk Factors in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013, registration statements and other reports filed from time to time with the SEC, and other announcements the Company makes from time to time. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. Should one or more of the risks or uncertainties described in this presentation occur, or should underlying assumptions prove incorrect, the Company’s actual results and plans could differ materially from those expressed in any forward-looking statements. All forward-looking statements are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that the Company, or persons acting on its behalf, may make. Except as otherwise required by applicable law, the Company disclaims any duty to update any forward-looking statements to reflect events or circumstances after the date of this presentation.

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

Agenda

• Who is Continental Resources • How did we get to this latest downturn • What are we doing to address the

downturn

4

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

BAKKEN ~1.17 Million Net

Acres Leased

SCOOP ~480,000 Net Acres Leased

CLR Primary Areas of Operation

Continental Resources

Founded in 1967 by Harold Hamm

New York Stock Exchange listed, went public in 2007 at $7.50 per share (split adjusted), ticker symbol: CLR

~$20 billion enterprise value⁽¹⁾ •Market cap: ~$14B •Total debt: ~$6B

Pure play E&P: oil focused, with liquids-rich optionality •Exploration based: Organic, drill bit growth •Independent: Dedicated to finding & producing onshore light, sweet oil

Size and scalability: focused in two premier plays •The Bakken in ND & MT •The SCOOP (South Central Oklahoma Oil Province) in the Springer & Woodford • ~1,200 Employees

5 (1) Market cap and total debt as of 12/31/2014

How did we get to this latest downturn

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 7

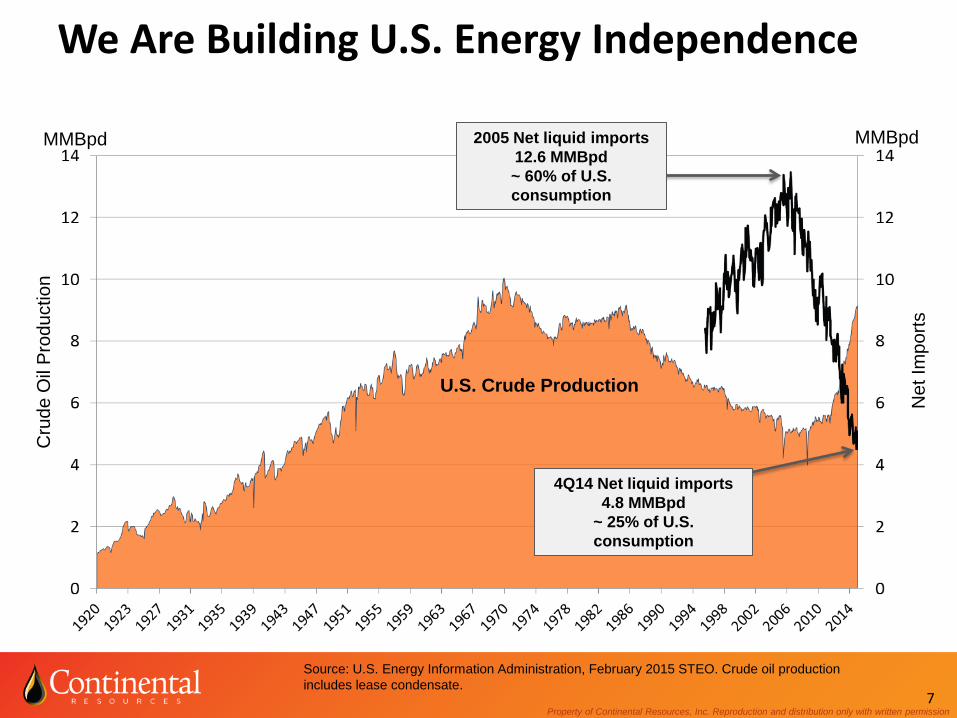

We Are Building U.S. Energy Independence

MMBpd MMBpd

Cru

de O

il P

rodu

ctio

n

Net

Impo

rts

Source: U.S. Energy Information Administration, February 2015 STEO. Crude oil production includes lease condensate.

2005 Net liquid imports 12.6 MMBpd ~ 60% of U.S. consumption

4Q14 Net liquid imports 4.8 MMBpd

~ 25% of U.S. consumption

U.S. Crude Production

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 8

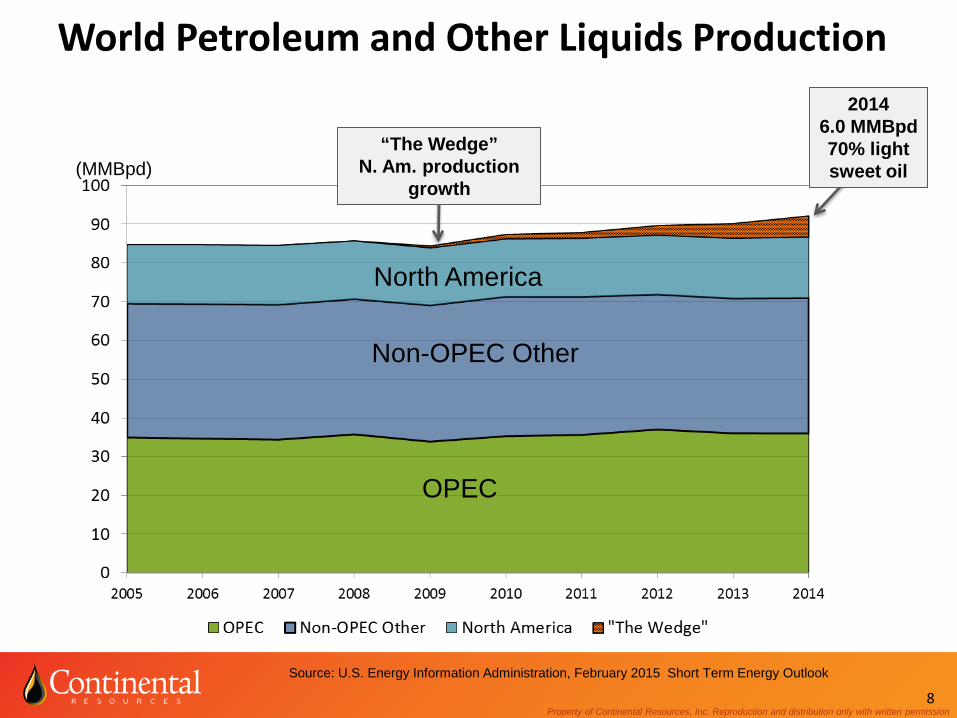

World Petroleum and Other Liquids Production

OPEC

(MMBpd)

Non-OPEC Other

North America

Source: U.S. Energy Information Administration, February 2015 Short Term Energy Outlook

“The Wedge” N. Am. production

growth

2014 6.0 MMBpd 70% light sweet oil

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

9

Bakken, Eagle Ford and “New” Permian ~ 50% of World Petroleum/Liquids Production Growth

*Source: DI Desktop (Drilling Info, Inc.) Excludes historical base production of 833,000 bopd to compare “new” Permian growth with that of Bakken & Eagle Ford

Bakken

Eagle Ford

New Permian*

MMBopd OCT 2014

~1 MMBpd of growth in the past 12 months

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

MMBopd

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 10

Cowboyistan: World’s #7 Liquids Producer 2014 Petroleum and Liquids Production

Source: U.S. Energy Information Administration, February 2015, Short Term Energy Outlook

• OPEC member

• • • • • • • • • • •

MMBpd

“New” Permian + Bakken + Eagle Ford = Cowboyistan

#7

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

Forecast

-3

-2

-1

0

1

2

3

4

5

6

78

80

82

84

86

88

90

92

94

96

2010-Q1 2011-Q1 2012-Q1 2013-Q1 2014-Q1 2015-Q1 2016-Q1

World Liquid Fuels Production and Consumption Balance million barrels per day (MMbbl/d)

Implied stock change and balance (right axis)

World production (left axis)

World consumption (left axis)

Source: Short-Term Energy Outlook, February 2015.

MMbbl/d

11

World Supply/Demand Forecast 2015-16

? ?

So what are we doing to address this

latest downturn

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 13

Current Response of U.S. Producers

• Capex cut by as much as 81%

• Drop drilling rigs • Defer well completions –

saves 60% of CWC – Avoid selling flush oil

and gas production in a poor market

– Wait for service costs to fall before completing wells

• Shut in high-cost stripper wells temporarily

• Shut in production – some operators don’t have to sell

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Emer

ald

MEG

Ene

rgy

Mag

Hunt

Halc

onN

orth

ern

Swift

Rose

tta

Tria

ngle

Goo

dric

hAp

ache

Reso

lute

Linn

Appr

oach

Penn

VA

Oas

isSa

ndRi

dge

Bill

Barr

ett

Lare

do Rex

Whi

ting

WPX

Ston

eCo

noco

Denb

ury

Mur

phy

Pion

eer

Cim

arex

QEP

Rang

eG

ulfp

ort

Ante

roCo

ntin

enta

lEO

GM

arat

hon

New

field

Nob

leCa

bot

Com

stoc

kM

atad

orSM

Ene

rgy

Sout

hwes

tern

Carr

izo

Anad

arko Oxy

Ches

apea

keBo

nanz

aSa

nche

zCo

ncho

Devo

nEc

lipse

Hess

• $61B in capital expenditure reductions already announced for 2015… as of early March.

• 73,500 layoffs

Source: Company announcements

Mid-point 46%

2014-15 Capex Reduction

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 14

U.S. Rig Count in Rapid Decline

* Continental Resources jobs estimate; rig counts Bakker-Hughes.

U.S. rig count has declined by 860 rigs, or 45%, since mid-November. One rig laydown equals the loss of 120 direct and indirect jobs. U.S. dropped 56 rigs this past week.*

?

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 15

Three Plays, Industry 50% Cut Case Industry production, excluding legacy Permian production

Note: Assumes an 8% increase in productivity due to high grading

1.55 MMBpd

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

2015: CLR - Embracing Market Change

• Revised 2015 capex and production guidance – $2.7 billion non-acquisition capex (reduced 41%) – Targeting cash flow neutrality by mid-year 2015 – 16%-20% YOY production growth

• Priorities – Maintain strong balance sheet and financial flexibility – Align capex near discretionary cash flow – Maximize returns and growth by focusing on high rate-of-return (ROR) inventory

• Opportunities – Reduce well and service costs

• Projecting 5%-10% cycle time improvements in spud to rig release by year end • Expect overall service costs to decline by at least 15% by mid-year and even more by year-end 2015

– Build efficiencies • Service quality enhancements through high-grading of service company personnel and equipment as a

result of consolidation • Lower overall industry rig count will allow advances in research and drilling and completions technologies

to emerge

– Remain opportunistic

16

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

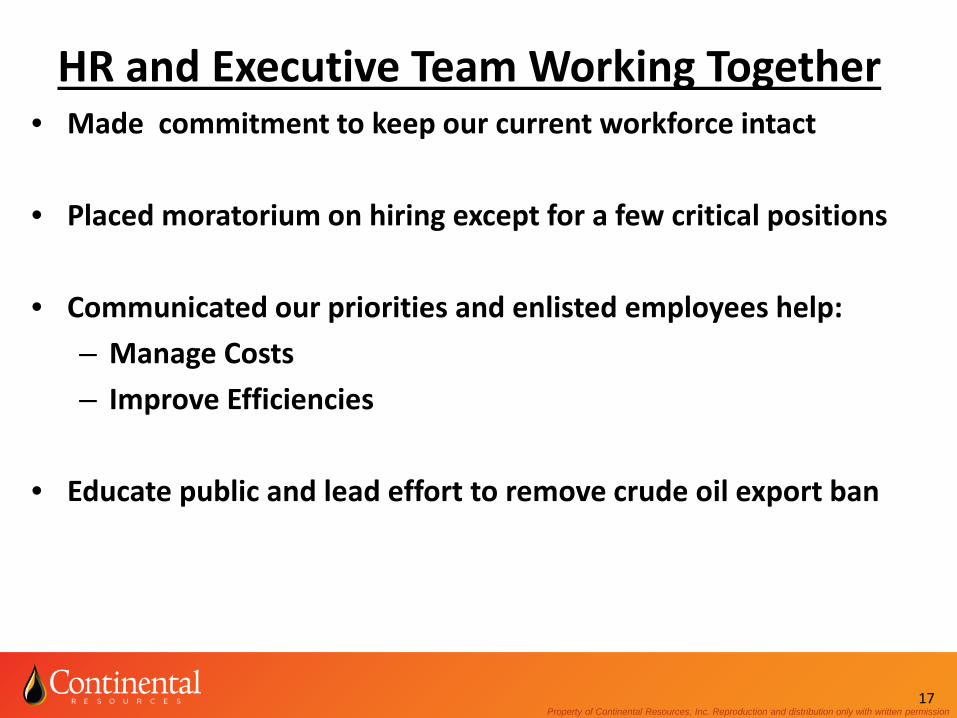

HR and Executive Team Working Together • Made commitment to keep our current workforce intact • Placed moratorium on hiring except for a few critical positions • Communicated our priorities and enlisted employees help:

– Manage Costs – Improve Efficiencies

• Educate public and lead effort to remove crude oil export ban

17

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

Most Light Sweet Refining Capacity Is Located Outside of the U.S.

18 Source: Oil & Gas Journal 2014 Refinery Survey (2013 numbers)

U.S. Refining

Since 2005 U.S. light sweet production

increased 3.8 MMBpd, while sour production

declined by 476,000 Bpd.

12 MMBpd Heavy sour

6 MMBpd Light sweet

64 MMBpd Light sweet

5 MMBpd Heavy sour

World (Non-U.S.)

Heavy sour Light sweet

Supplemental Slides

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2010 2011 2012 2013 2014

SCOOPBakkenLegacy

• Leading positions in both the Bakken and SCOOP – Scalable economics from large leasehold

and production volumes • Bakken ~1.17 million net acres • SCOOP ~480,000 net acres • Captured “core of the basin” leasehold as

an early entrant and first mover in both plays

• FY14 production totaled over 174,000

Boe per day, +28% over FY13 – Production mix:

• 70% crude oil, or ~122,000 barrels of oil per day

• 30% natural gas and NGLs, or ~313,000 Mcf per day

– Reached net production milestone of 200,000 Boe per day in December 2014

20

Two World-Class Platforms for Growth

Production Growth (Boe per Day)

174,000

20%

66%

14%

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

U.S. Energy Renaissance at Risk

1) Post-1970s consensus: America was running out of oil and natural gas, and imports would increase unabated into the future. To combat this threat:

a. President Nixon imposed price controls after the 1973 Arab oil embargo. b. U.S. later banned oil exports as an enforcement tool of this policy.

2) Given that gas production was declining, facilities were built in Texas, Louisiana, Maryland and California to import LNG from abroad.

3) U.S. oil refineries spent $85B over 25 years* to reconfigure assets to process heavy crude from Mexico, Venezuela and Canada.

4) However, we, the small U.S. Independents, developed new horizontal technologies in the 1990s and used them to discover a vast new supply of natural gas in tight rock reservoirs – 100+ years of new supply* – a real game-changer!

5) These same technologies led to the discovery of the three new crude oil resource plays, the Bakken, Eagle Ford and “new” Permian unconventional, which have generated 50% of the world’s oil production growth since 2005, represent ~40+ years of new oil supply. The U.S. accounts for 75% of world oil production growth in that decade.

Background

*Sources: PACE and USGS

21

Property of Continental Resources, Inc. Reproduction and distribution only with written permission

U.S. Energy Renaissance at Risk

1) LNG import facilities are now being retrofitted to EXPORT LNG abroad. U.S. has assured long-term self-sufficiency in natural gas.

2) Net imports of petroleum liquids have fallen to 25% of U.S. consumption, near the limit that’s difficult to exceed because 25% of U.S. refinery capacity is foreign-owned.

3) Compounding this problem, many U.S. light sweet oil refineries have been reconfigured by their foreign owners to process heavy sour/bitumen. Result: Light oil refining capacity is severely limited in the U.S.

4) The U.S. is within 5 MMBpd of being entirely self-sufficient in crude oil, which is equal to the daily capacity of foreign-owned refineries in the U.S.

5) Since 2008 the domestic energy renaissance has been the leading provider of jobs and strength to the U.S. economy.

6) A continued ban on the fair trade of domestic oil could push the country back into recession, due to mounting middle-class job losses, higher gasoline prices and reduced capital spending.

Currently

22

Property of Continental Resources, Inc. Reproduction and distribution only with written permission 23

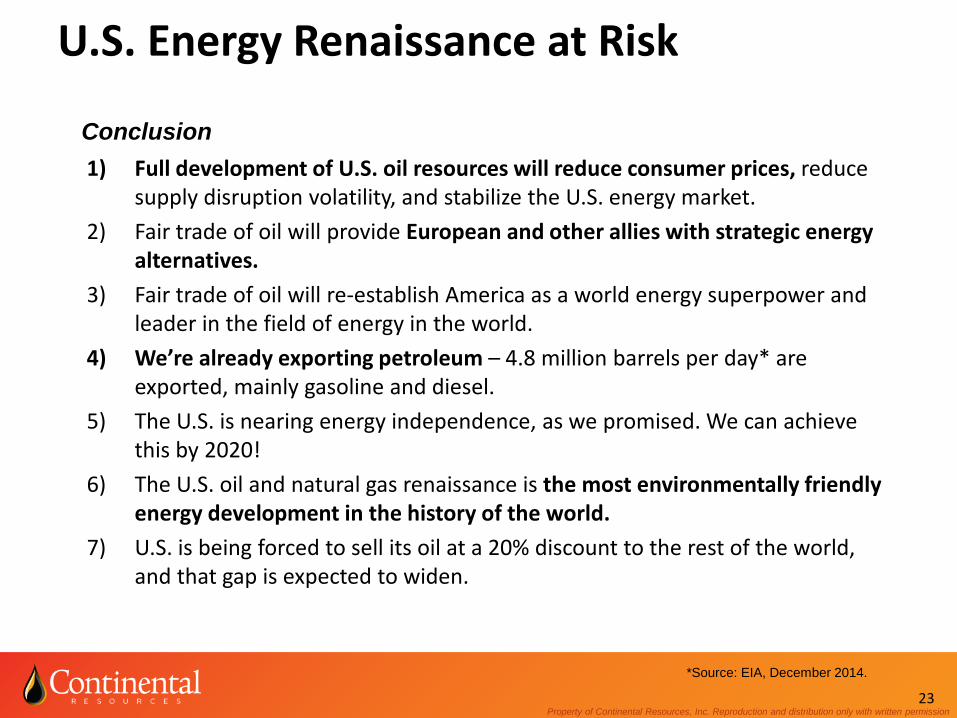

U.S. Energy Renaissance at Risk

1) Full development of U.S. oil resources will reduce consumer prices, reduce supply disruption volatility, and stabilize the U.S. energy market.

2) Fair trade of oil will provide European and other allies with strategic energy alternatives.

3) Fair trade of oil will re-establish America as a world energy superpower and leader in the field of energy in the world.

4) We’re already exporting petroleum – 4.8 million barrels per day* are exported, mainly gasoline and diesel.

5) The U.S. is nearing energy independence, as we promised. We can achieve this by 2020!

6) The U.S. oil and natural gas renaissance is the most environmentally friendly energy development in the history of the world.

7) U.S. is being forced to sell its oil at a 20% discount to the rest of the world, and that gap is expected to widen.

Conclusion

*Source: EIA, December 2014.