working capital management of ual industries ltd

TRANSCRIPT

ATUAL Industries Ltd, Dhenkanal (Orissa),

SUBMITTED

AS A PARTIAL FULLMENT OF PGDM

CORPORATE GUIDE ACADEMIC GUIDEMR. S.N. BHATTACHARYA DR. U.C. PATTNAIK(ACCT. GENERAL MANAGER, (DIRECTOR OF ISBM)COMMERCIAL)

SUBMITED BY:SAUMENDRA NANDAROLL NO-MB05017

ISBM (BHUBANESWAR)

ATUAL Industries Ltd, Dhenkanal (Orissa),

SUBMITTED

AS A PARTIAL FULLMENT OF PGDM

CORPORATE GUIDE ACADEMIC GUIDEMR. S.N. BHATTACHARYA DR. U.C. PATTNAIK(ACCT. GENERAL MANAGER, (DIRECTOR OF ISBM)COMMERCIAL)

SUBMITED BY:SAUMENDRA NANDAROLL NO-MB05017

ISBM (BHUBANESWAR)

ATUAL Industries Ltd, Dhenkanal (Orissa),

SUBMITTED

AS A PARTIAL FULLMENT OF PGDM

CORPORATE GUIDE ACADEMIC GUIDEMR. S.N. BHATTACHARYA DR. U.C. PATTNAIK(ACCT. GENERAL MANAGER, (DIRECTOR OF ISBM)COMMERCIAL)

SUBMITED BY:SAUMENDRA NANDAROLL NO-MB05017

ISBM (BHUBANESWAR)

I

DECLARATION

I do here by declare that this piece of project report entitled “A Study onWorking capital Management practices in UAL INDUSTRIES LTD.” forpartial fulfilment of the requirements for the award of the degree of “POSTGRADUATE DIPLOMA IN MANAGEMENT “is a record of original work doneby me under the supervision and guidance of DR. U.C PATTNAIK, ISBM.This project work is my own and has neither been submitted norpublished elsewhere.

Place: Bhubaneswar SAUMENDRA NANDADATE: REG. NO.MB05017

ii

ACKNOWLEDGEMENTANY WORK EITHER SMALL OR BIG OWES A GREAT DEAL TO OTHERSOTHERS, MINE IS NO EXCEPTION TO ITSuccess is not destination, but a journey – it is often said. I realized it even better duringmy summer internship program at UAL INDUSTRIES LTD. I may not have come this farwithout help, guidance and support of certain people who acted as guides, friends andtorch bearers along the way.Training is an indispensable part of a person joining a company as an employee. Itprovides the students an opportunity to gain experience on the practical applications oftheir knowledge. My training at UAL INDUSTRIES has been very fruitful. I am sure thatthe hands of experience I have gained here will go a long way towards my rest of life.I specially and most sincerely acknowledge with deep sense of gratitude to thecompany’s managing director, Mr. Arun k Saraf, and the HR, Mr. Dasgupta for give methe chance to go to the Dhenkanel factory and learn, experience and gather the insightsfrom the employees at the factory /floor level which helped me to understand the entireworking capital management.I am greatly indebted to my guides DR.U.C.PATTNAIK, faculty guide for Finance(summer internship), INTERNATIONAL SCHOOL OF BUSINESS MANAGEMENT &Mr.S.N.Bhattacharya, Asst. Manager (commercial) UAL INDUSTRIES LTD.DHENKANAL for their constant guidance, advice and help which enabled me to finishthis project report properly in time.Last but not the least, I would like to forward my gratitude to my friends & other facultymembers who always endured me and stood with me and without whom I could nothave completed the project.

SAUMENDRA NANDAISBM, BBSR

iii

PREFACE

To start any business, First of all we need finance and the success of that business entirelydepends on the proper management of day-to-day finance and the management of this short-term capital or finance of the business is calledWorking capital Management.Working Capital is the money used to pay for the everyday trading activities carried out by thebusiness - stationery needs, staff salaries and wages, rent, energy bills, payments for suppliesand so on. I have tried to put my best effort to complete this task on the basis of skill that I haveachieved during the last one year study in the institute. I have tried to put my maximum effort toget the accurate statistical data. However I would appreciate if any mistakes are brought to myby the reader

TABLE OF CONTENT

CHAPTER-1

INTRODUCTIONPAGENO.

1.1 objective of study 1.11.2 Scope of the study 1.11.3 Limitation of the study 1.11.4 Research methodology 1.11.5 Methods of data collection 1.2

CHAPTER-2COMPANY PROFILE

2.1 HISTORY OF UAL INDUSTRIES LTD. 2.12.2 UNIT OF UAL INDUSTRIES LTD. 2.22.3 BORD OF DIRECTORS 2.32.4 ORGANISATION STRUCTURE OF UAL INDUSTRIES LTD. 2.42.5 VISION & MISSION OF UAL INDUSTRIES LTD. 2.52.6 MANAGEMENT INFORMATION SYTEM 2.52.7 CORPORATE SACIAL RESPONSIBILITIES 2.62.8 FACTS & MYTHS 2.72.9 PRODUCT OF UAL INDUSTRIES LTD. 2.9

2.10 INSTALLATION PROCEDURE & PROCEDURE OF MITRING 2.122.11 SERVISES 2.132.12 TRAINING 2.142.13 QUALITY POLICIES 2.152.14 ENVIRONMENT POLICIES 2.162.15 ENVIRONMENT AUDIT 2.162.16 AWARDS 2.172.17 CERTIFICATES 2.182.18 DISTRIBUTION NETWORK 2.19

CHAPTER-33.1 MEANING OF WORKING CAPITAL 3.13.2 CONCEPT OF WORKING CAPITAL 3.13.3 SIGNIFICANCE OF WORKING CAPITAL 3.23.4 CIRCULATION OF WORKING CAPITAL 3.33.5 CLASSIFICATION OF WORKING CAPITAL 3.33.6 FACTORS INFLUENCING WORKING CAPITAL REQUIREMENT 3.43.7 COMPONENTS OF WORKING CAPITAL 3.63.8 FORECASTING OF WORKING CAPITAL 3.8

3.9 CONTROL OF WORKING CAPITAL 3.83.10 SOURCES OF WORKING CAPITAL 3.93.11 STRUCTURE OF WORKING CAPITAL 3.93.12 OPERATING CYCLE 3.113.13 DURATION OF WORKING CAPITAL 3.123.14 INSTALLATION OF WORKING CAPITAL MANAGEMENT 3.133.15 MEANING OF WORKING CAPITAL MSNAGEMENT 3.133.16 CONCEPT OF WORKING CAPITAL MANAGEMENT 3.133.17 IMPORTANT OF WORKING CAPITAL MANAGEMENT 3.143.18 SIGNIFICANCE OF WORKING CAPITAL MANAGEMENT 3.153.19 THEORY OF WORKING CAPITAL MANAGEMENT 3.163.20 PRINCIPLES OF WORKING CAPITAL MANAGEMENT 3.163.21 APPROACHES OF WORKING CAPITAL MANAGEMENT 3.17

CHAPTER-4DATA ANALYSIS & INTERPRETATION

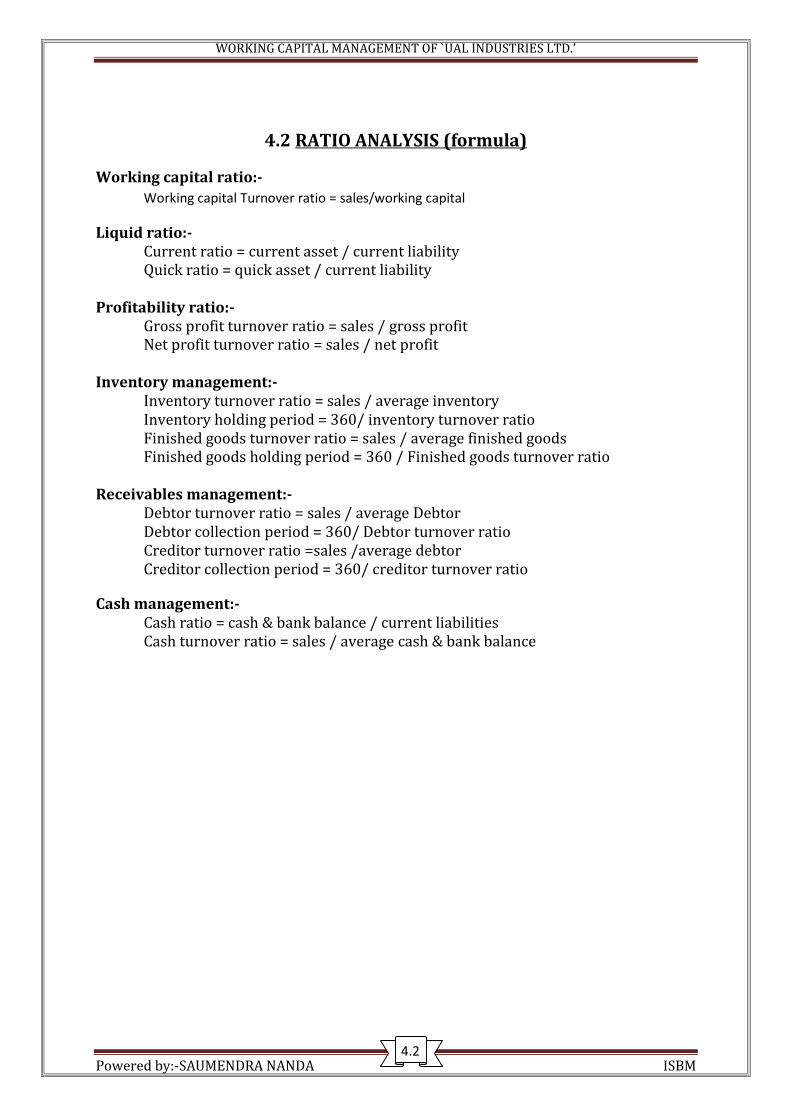

4.1 DATA ANALYSIS & INTERPRETATION 4.14.2 RATIO ANALYSIS (formula) 4.2

4.3STATEMENT SHOWING THE SCHEDULE OF CHANGING IN WORKINGCAPITAL 4.3

4.4 COMPAIRSATION SALES & WORKING CAPITAL 4.54.5 MANAGEMENT OF WORKING CAPITAL(RATIO ANALYSIS) 4.64.6 INVENTORY MANAGEMENT 4.14.7 RECEIVABLE MANAGEMENT 4.174.8 CASH MANAGEMENT 4.214.9 OPERATING CYCLE 4.25

CHAPTER-5FORECASTING

5.1 TIME SERIES ANALYSIS 5.15.2 METHOD OF LEAST SQUARES 5.15.3 FORECASTING FOR THE YEAR 2011-12 5.15.4 FORECASTING OF WORKING CAPITAL FOR THE YEAR 2011-12 5.7

CHAPTER-66.1 FINDING 6.16.2 RECOMMENDATION 6.16.3 CONCLUSION 6.36.4 BIBLIOGRAPHY 6.4

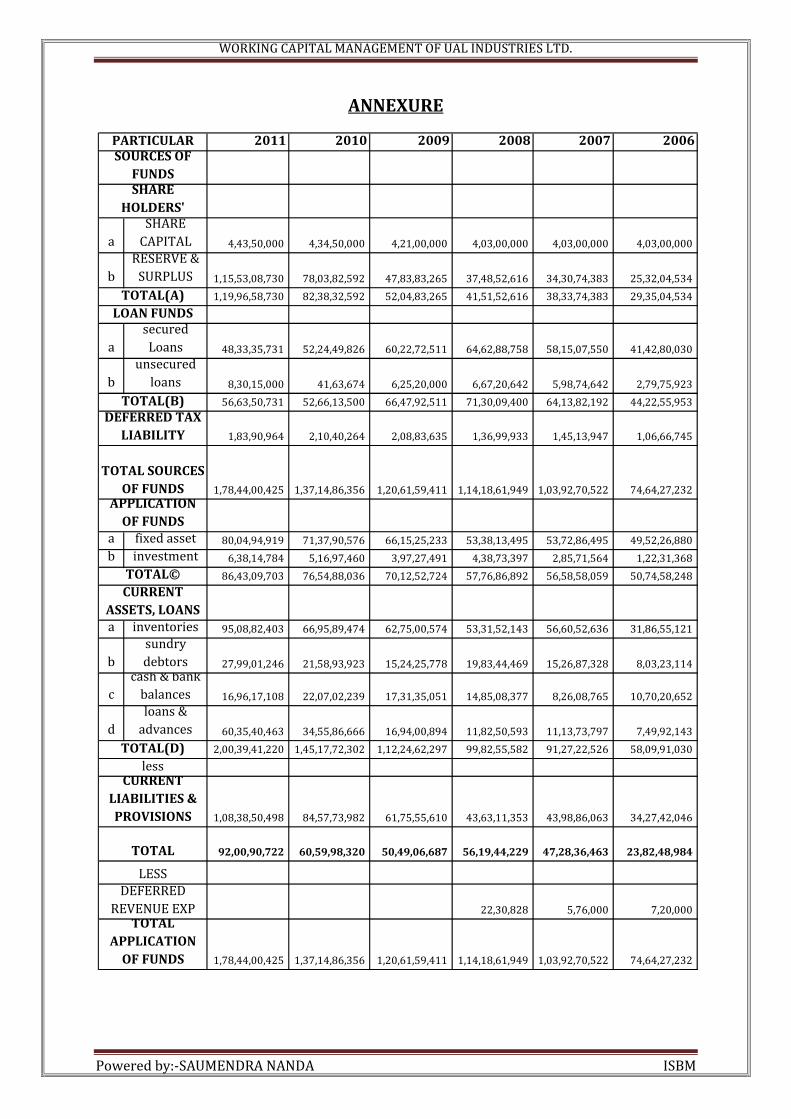

ANNEXUREANNEXURE

OBJECTIVE OF THE STUDYOBJECTIVE OF THE STUDYOBJECTIVE OF THE STUDY

P o w e r e d b y : - S A U M E N D R A N A N D A ISBM

WORKING CAPITA MANAGEMENT OF UAL INDUSTRIES LTD. 2012

1.1 OBJECTIVE OF THE STUDY:Study of the working capital management is important because unless the Working capital ismanaged effectively, monitored efficiently planed properly and reviewed periodically atregular intervals to remove bottlenecks if any the Company cannot earn profits and increaseits turnover. With this primary Objective of the study, the following further objectives areframed for a depth Analysis.

To study the working capital management of UAL INDUSTRIES LTD. To study the optimum level of current assets and current liabilities of the Company. To study the liquidity position through various working capital related Ratios. To study the working capital components such as receivables accounts, Cash

management. To estimate the working capital requirement of UAL INDUSTRIES LTD. To study the operating and cash cycle of the company

1.2 SCOPE OF THE STUDY:The scope of the study is identified after and during the study is conducted. The Study ofworking capital is based on tools like trend Analysis, Ratio Analysis, Working capitalleverage, operating cycle etc.Further the study is based on last 5 years UAL INDUSTRIES LTD.And even factors like Competitor’s analysis, industry analysis were not considered whilepreparing this project.

1.3 LIMITATIONS OF THE STUDY:Following limitations were encountered while preparing this project:

1.3.1 Limited data:-

This project has completed with annual reports; it just constitutes one part of Datacollection i.e. Secondary. There were limitations for primary data Collection because ofconfidentiality.

1.3.2 Limited period:-

This project is based on five year annual reports. Conclusions and Recommendations arebased on such limited data. The trend of last five-year May or may not reflect the realworking capital position of the company

1.3.2 Limited area:-

Also it was difficult to collect the data regarding the competitors and their financialinformation. Industry figures were also difficult to get.

1.4 RESEARCH METHODOLOGY

INTRODUCTION: Research methodology is a way to systematically solve the researchproblem. It may be understood as a science of studying now research is done systematically.In that various steps, those are generally adopted by a researcher in studying his problemalong with the logic behind them.

1.1

P o w e r e d b y : - S A U M E N D R A N A N D A ISBM

WORKING CAPITA MANAGEMENT OF UAL INDUSTRIES LTD. 2012

It is important for research to know not only the research method but also knowmethodology. The procedures by which researchers go about their work of describing,explaining and predicting phenomenon are called methodology. Methods comprise theprocedures used for generating, collecting and evaluating data. All this means that it isnecessary for the researcher to design his methodology for his problem as the same maydiffer from problem to problem. Data collection is important step in any project and successof any project will be largely depend upon now much accurate you will be able to collectand how much time, money and effort will be required to collect that necessary data, this isalso important step. Data collection plays an important role in research work. Withoutproper data available for analysis you cannot do the research work accurately.1.5 METHODS OF DATA COLLECTION:There are two types of data collection methods available.

• Primary data collection

• Secondary data collection

1.5.1 Primary Data:

The primary data is that data which is collected fresh or first hand, and for first time which isoriginal in nature. Primary data can collect through personal interview, questionnaire etc. tosupport the secondary data.

1.5.2 Secondary Data Collection Method:The secondary data are those which have already collected and stored. Secondary dataeasily get those secondary data from records, journals, annual reports of the company etc. Itwill save the time, money and efforts to collect the data. Secondary data also madeavailable through trade magazines, balance sheets; books etc.This project is based onprimary data collected through personal interview of head of account department, head ofSQC department and other concerned staff member of finance department. But primarydata collection had limitations such as matter confidential information thus project is basedon secondary information collected through five years annual report of the company,supported by various books and internet sides. The data collection was aimed at study ofworking capital management of the company.

Project is based on

Annual report of UAL INDUSTRIES LTD 2011-10

Annual report of UAL INDUSTRIES LTD 2009-10

Annual report of UAL INDUSTRIES LTD 2008-09

Annual report of UAL INDUSTRIES LTD 2007-08

Annual report of UAL INDUSTRIES LTD 2006-07

1.2

COMPANY PROFILE

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.1 HISTORY OF THE COMPANYUAL Industries Ltd., formerly known as Utkal Asbestos Limited, is in the business ofmanufacturing Fibre Cement Corrugated sheets and accessories under the brand name“Konark. The company has manufacturing units in 3 locations namely Dhenkanal (Orissa),Tungadhowa (Midnapore, West Bengal) and Baramanpur (Uttar Pradesh).The mother Plant was set up at Dhenkanal, Orissa with the initial installed capacity of30,000 MT per annum in the year 1980. To the day, in 2010, the production capacity of thecompany is 4.30 Lacs MT per annum. The company’s products are sold and distributedunder the brand name “Konark” which is synonymous with Orissa. The company maintainsits leadership in Eastern India with the “Konark” brand established as a superior Brandbased on quality, strength, and durability. The company received the ISO 9001:2008, ISO14001:2004 and OSHAS 18001:2007 certifications from Bureau Veritas QualityInternational (BVQI) and TUV which exhibit the highest quality standards.UAL Industries Ltd. is a professionally managed company. Shri S M Shroff is the non –executive Chairman and Shri A K Saraf is the Managing Director who manages overallfunctioning of the company along with Executive Director, Sri K N P Sinha and otherprofessionally qualified Non-executive Directors, unit heads and a dedicated team ofOfficers and Executives.UAL Industries Limited is the largest Fibre Cement Sheet manufacturer and marketer inEastern India with a 40% market share in East India. The National average is 10%. Thecompany provides opportunity of direct employment to more than 700 personnel andindirectly to nearly 1500 persons.It may be worthwhile to mention that after a lot of R & D the company has started using FlyAsh as a major Raw Material to the extent of 37% in the Raw Material Mix since 1992 andthereby helping in tackling the environment problem created by emission of fly ash. TheCompany is recipient of Environment Excellence Awards from Govt. of West Bengal, Orissaand TERI on various occasions.A new green field Fibre Cement Sheet manufacturing facility is being set up in the State ofBihar in the district of Vaishali near Patna. The land has been acquired and projectclearance from the Ministry of Environment & Forests, New Delhi is awaited. The Capitalinvestment in initial phase of the project shall be of the order of Rs. 30 Corers. It is likely tobe commissioned during the first quarter of next financial year 2011–12. With addition tothis plant, the total production capacity would stand enhanced to 5.50 Lacs MT per annum.

2.1

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.2 UNIT OF UAL INDUSTRIES LTD.

The mother factory was set up in the year 1980 and is located about 60 Km away from Cuttack onthe National Highway No. 42 on Cuttack-Sambalpur Road. The plant operates with a productioncapacity of 30,000MT.

ORISSA FACTORYAt+Po - KorianP.Box No - 8Dhenkanal - 759001Orissa

As a measure of expansion, Utkal Asbestos Ltd. set up its second unit at village: Tungadhowa nearGuptamani, District: Midnapore, West Bengal, under the name and style “UAL- BENGAL" in the year1999. The Midnapore unit at village Tungadhowa is located about 20 Km from the town ofKharagpur on the National Highway 6, on Kolkata - Mumbai Road. The production capacity of thePlant has gone up from 1, 40,000 TPA to 2, 50,000 TPA.

UAL Bengal, Tungadhowa Works received ISO: 9001-2008, ISO: 14001-2004 and OHSAS:18001-2008from BVQI, accredited by UKAS, London.

UAL BENGAL FACTORYKonark NagarTungadhowaWest Midnapore - 721513West Bengal

The company set up its third works at Village Baramanpur, District: Jaunpur near Varanasi in U.P. formanufacturing. A new milestone is our UAL- U.P. set up in the year 2005 at Village BaramanpurDistrict Jaunpur. The unit is about 30km away from Varanasi city. Production capacity of plant is 1,20,000 T.P.A.UAL-UP works has started the process of certification of ISO 9001-2001, 14000 OHSAS: 18001-2007

U. P. FACTORYVill - BaramanpurTeshil - KeraketDist – Jaunpur

2.2

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.3 BORD OF DIRECTORS

SHRI S.M. SHROFF – CHAIRMAN (Qualifications – B.A. (Hons.)Relevant Industry Expertise – Mr. Shroff is a Gold Medallist in Philosophy from Presidency Collegelocated at Kolkata. He started his career after leaving college as a general trader. His sharp businessacumen cultivated in him the craft of turning around sick units. An almost dying fertilizer unit inOrissa was converted into a most successful Cement plant within a period of five years. His majorinterest of business is Real Estate. The first and most fashioned Shopping Mall of Kolkata namelyForum and the first and most integrated green I. T. infrastructure building namely Technopolis goesto his credit and repute.

SHRI A.K. SARAF - MANAGING DIRECTOR ( Qualifications – B. Com. (Hons.)

Relevant Industry Expertise – He has an experience of over 30 years in the industries engaged inmanufacturing of cement and fibre cement roofing sheets and accessories. He plans, co-ordinatesand directs all the facets of the management of the company. He acts as the brain of theorganization and leads the company to success while achieving the company’s vision and objectives.

SHRI K. N. P. SINHA - EXECUTIVE DIRECTOR (Qualifications – B.E. (ChemicalEngineering)Relevant Industry Expertise – He has a long experience of 35 years in Fibre Cement Sheet Industry.His expertise includes hands on knowledge of not only plant operations but strategic planning aswell.

SHRI S.C. JAIN – DIRECTOR ( Qualifications – Master Degree in PersonnelManagement and L.L.B.)Relevant Industry Expertise – He is widely associated with various types of industries in his capacityas an Industrial Advisor in the matter of Personnel Management. He has a long experience inIndustrial Relations and Labor Laws.

SHRI G. K. TULSYAN – DIRECTOR (Qualifications – B.Sc, F.C.A.)Relevant Industry Expertise – He is a practicing Chartered Accountant and commands a wideknowledge on the subject of taxation and company law matters. He has a long experience and goodcommand over his profession.

2.3

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM2.4

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.5.1 VISION To be the country’s largest and most trusted eco friendly low cost Fibre cement

sheet manufacturer and marketer through customer satisfaction and sustainablegrowth.

2.5.2 MISSION Achieve Market Leadership in FCC Sheets Drive long term profitable growth Delight customers by providing enhanced satisfaction Adopt state of art technology to further enhance the philosophy of Zero Waste

Management and Zero Effluent Discharge from the plant. Research & Development activity is carried on a regular basis to innovate upgraded

technology to optimize the raw material mix thereby increasing product efficiency atoptimum cost.

Make UAL Industries Limited a great place to work for all its employees.

2.6 MANAGEMENT INFORMATION SYSTAMUAL Industries Ltd. runs Third Party Developed customized ERP (Enterprise

Resource Planning) Application. The Modules run are:• Financial Management• Material Management• Payroll & HR Management• Sales & Dispatch Management

All The Factories, Depot and H.O are interconnected with MPLS VPN for online data transferand connectivity. In near future, Video Conferencing and tele-communication would becharted through WAN. Special policies have been adopted for the following:

2.6.1 DATA SECURITY

Data Security has been given prime importance with introduction of Business ContinuityPlanning (BCP) and Disaster Recovery Planning (DRP) ensuring minimal downtime with datareplication methodology. Automated Backing up of user documents has been regulated.

2.6.2 NETWORK SECURITY

Internal Network of UAL Industries Ltd. has been made secured from outside threatthrough introduction of UTM at Internet Gateway Point to filter unwanted packets andinstalling Anti-Virus Software. The independent network structure is getting converted tocentrally controlled network to facilitate better network government.

2.5

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.7 CORPORATE SOCIAL RESPONSIBILITIES

Sl.No

Date Donation Made to Amount(Cash/Kind)

1 26.06.2010 Donated to the Rogikalyana Samiti Dhenkanal MainHospital

RS50,000.00

2 28.01.2010 Incurred for repairing and painting of Blind and DeafSchool, Dhenkanal Town

Rs. 84,000.00

3 NA Supply of 15 days ration to the Anathashrama, Hata RoadDhenkanal & Anathashram, Gobindapur, Dhenkanal.approx @ Rs.20, 000.00 per month

Rs.2,40,000.00

4 NA Donated to Vaniram High School Kesheria, Dhenkanal forrepairing of building

Rs. 30,000.00

5 31.07.2010 Donated Fibre Cement Corrugated sheets to GajamaraSchool, Dhenkanal

Rs. 13,592.00

6 NA Donated to Maharshi Dayananda Service MissionKathagara, Dhenkanal for accommodation of orphanChildren and help less old persons

Rs. 60,550.00

7 NA Donated to Swadhinata Sangrami Mr. Braja MohanMohapatra.Kesharia, Dhenkana

Rs. 32,000 .00

8 NA Donated Fibre cement sheets to Industrial Training Centre,Rengali Dam side Talcher.

Rs 12,000.00

9 NA Plantation at Kapilash Girls High School Deogan,Deogan High School, Deogan U.P. School,Deogan Primary School, Soraciapada Sebashram, Deogan,Deogan Medical and back side of the plant adjacement toRailway line

Rs.1,20,000.00

10 27.09.2010 Donation to Dhenkanal Mohosthab Rs. 50,000.00

11 19.09.10-20.09.10

Finance Assistanct to Saraswati Sishu Mandir for SportsFestival

Rs4,600.00

12 01.10.2010 Trophy cost provided to Mayoor Sangeet Vidyalalya ForCultural Programme

Rs. 3,000.00

13 29.09 &01.10

Provided Vehicle for Eye Camp as per direction of Collector& Dist. Magistrate

Rs. 4,000.00

2.6

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

FACTS & MYTHS

2.8.1 What is Asbestos?

Asbestos is a naturally occurring fibrous mineral commonly found in underground rockformations. For commercial purposes, it is recovered by mining and rock crushing. Fineparticles, invisible to the eye, are present in the air and water, everywhere. All of us maybe inhaling them and ingesting them through drinking water every day for our life withoutany adverse effect on health. Asbestos is commercially used since 1900 and is classifiedinto 2 groups. One category is called "Chrysotile" (white) Asbestos and the other group istermed as Amphiboles consisting of Crocidolite (blue), Amosite (brown) etc.

White asbestos (chrysotile) constitutes 98% of world production for its commercial use.Indian asbestos cement sheet and pipe manufacturers import all their requirements ofchrysotile fibres from Canada, Brazil, Russia, Zimbabwe and Kazakistan for production ofAC sheets and pipes. India imports only 20% of world production from above countries.Asbestos is also mined in India, but quantity and quality-wise it is of no relevance to ourasbestos cement production. It is generally found in large concentrations in the naturalbedrock of the earth crust.

The Chemical composition of Crocidolite, Amosite and Chrysotile are different. Asbestos fibre, (composed mainly of magnesium and silica), is a great reinforcing agent.

While its tensile strength is greater than steel, it has other rare and highly valued fireretardant, chemical resistant and heat insulating qualities. In fact it is a magic mineral andno other substitute can match its properties.

2.8.2 What are Asbestos Cement (AC) Products? Because of its exceptional strength and ability to cover inside area as reinforcement only

8.9% of chrysotile fibres are adequate to combine with cement and other raw materials.Over 90% of asbestos fibre imports of India go into AC sheet and pipe production.

AC Sheets have used in India for 70 years. Being weather proof and corrosion resistant,these sheets are practically ageless and maintenance free, whereas metal sheets corrodeand deteriorate with age and exposure.

AC Sheets have also proven to be the most cost effective, easy-to-install, strong anddurable roofing material for warehouses, factories, low-cost housing, and practically, anystructure needing a roof. Apart from India, Russia, China, Indonesia, Thailand and Brazil aresome of the largest users of AC Sheets.

AC Sheets and pipes, being corrosion and erosion-free, once properly laid and jointed,need no maintenance or replacement. They are also very cost effective.

AC products, which consume low energy in manufacture and do not in any way deplete thenatural resources, meet the needs of the country in its developing economy in the contextof rapidly rising population and limited resources.

2.7

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

AC products are manufactured under (ISI) license strictly conforming to the standards ofBureau of Indian Standards- IS 459/1992 for Corrugated Roofing Sheets, IS2098/ 1997 forFlat Sheets and IS 1626 (Part 111)/1994 for Roofing Accessories.

2.8.3 Explain the negative reports on asbestos: The bias against the use of asbestos in few countries is due to the adverse Western media

coverage relating to altogether different types and usages of asbestos in the past in thosecountries i.e. sprayed-on asbestos and friable low-density asbestos insulation used underuncontrolled conditions at that time due to lack of adequate scientific knowledge. Forexample usage of amphibole (blue) variety in such applications. Though these particularusages have since been discontinued in the West, the claims relating to the past keepappearing in the media resulting in general confusion. In India Asbestos Fibre was neverused as sprayed insulation.

But, once the scientific research into the risks of asbestos was set in motion, developmentand installation of pollution control systems took place, enabling the asbestos mining andasbestos cement industries to maintain safe and acceptable levels of dust pollution at thework places.

Once the safety fears were defined, the Governments have stepped in and laid downpollution control regulations and the mechanisms to enforce their compliance. Compliancewith these regulations and standards assured the workers in asbestos cement industries arisk free environment.

2.8

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

PRODUCT

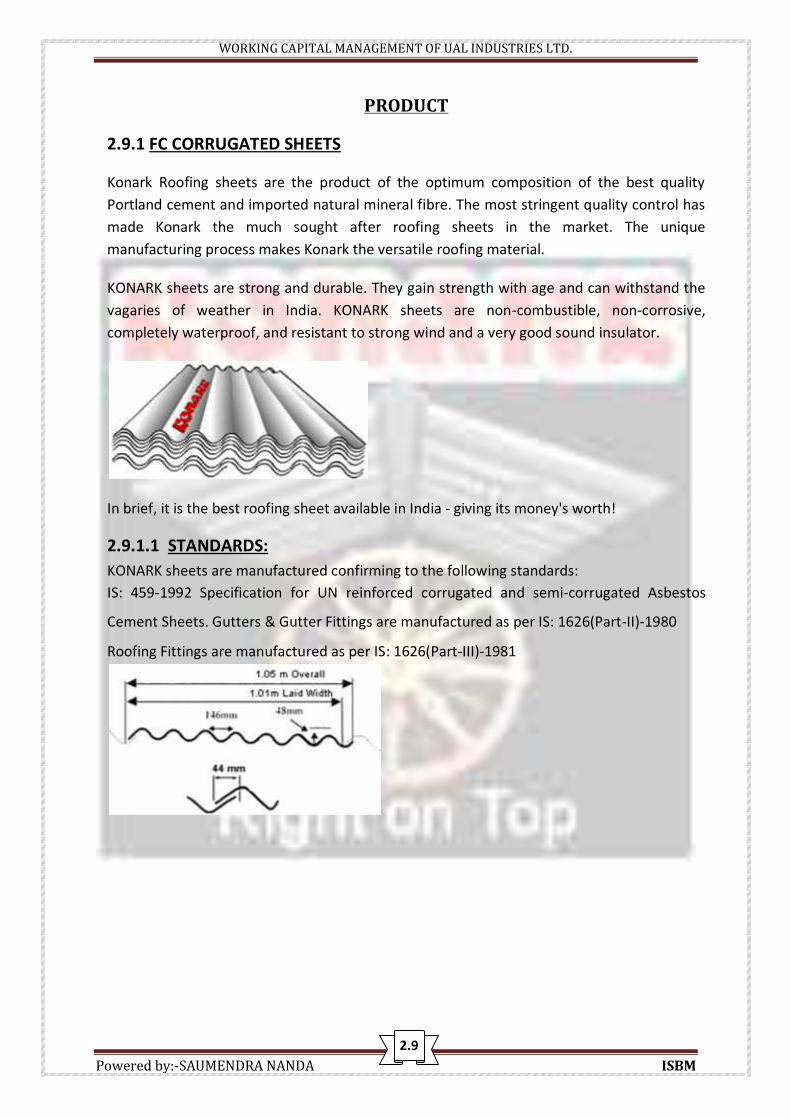

2.9.1 FC CORRUGATED SHEETS

Konark Roofing sheets are the product of the optimum composition of the best qualityPortland cement and imported natural mineral fibre. The most stringent quality control hasmade Konark the much sought after roofing sheets in the market. The uniquemanufacturing process makes Konark the versatile roofing material.

KONARK sheets are strong and durable. They gain strength with age and can withstand thevagaries of weather in India. KONARK sheets are non-combustible, non-corrosive,completely waterproof, and resistant to strong wind and a very good sound insulator.

In brief, it is the best roofing sheet available in India - giving its money's worth!

2.9.1.1 STANDARDS:KONARK sheets are manufactured confirming to the following standards:IS: 459-1992 Specification for UN reinforced corrugated and semi-corrugated Asbestos

Cement Sheets. Gutters & Gutter Fittings are manufactured as per IS: 1626(Part-II)-1980

Roofing Fittings are manufactured as per IS: 1626(Part-III)-1981

2.9

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

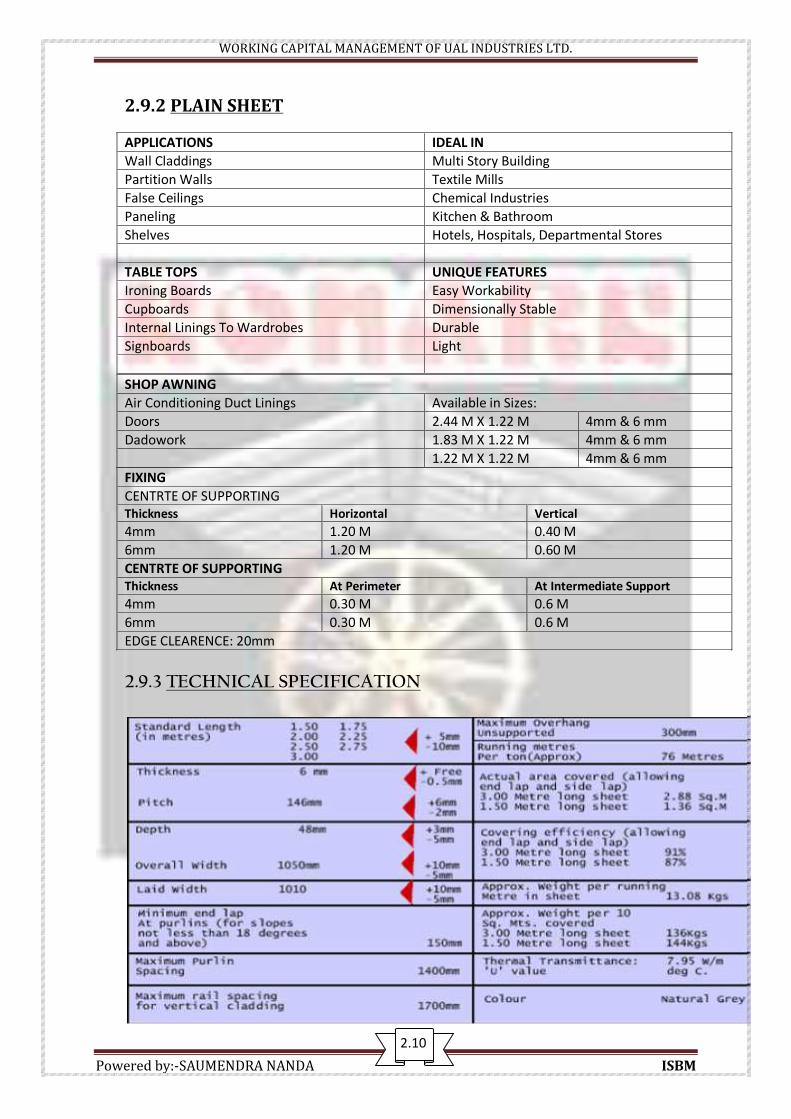

2.9.2 PLAIN SHEET

APPLICATIONS IDEAL INWall Claddings Multi Story BuildingPartition Walls Textile MillsFalse Ceilings Chemical IndustriesPaneling Kitchen & BathroomShelves Hotels, Hospitals, Departmental Stores

TABLE TOPS UNIQUE FEATURESIroning Boards Easy WorkabilityCupboards Dimensionally StableInternal Linings To Wardrobes DurableSignboards Light

FIXINGCENTRTE OF SUPPORTINGThickness Horizontal Vertical4mm 1.20 M 0.40 M6mm 1.20 M 0.60 MCENTRTE OF SUPPORTINGThickness At Perimeter At Intermediate Support4mm 0.30 M 0.6 M6mm 0.30 M 0.6 MEDGE CLEARENCE: 20mm

2.9.3 TECHNICAL SPECIFICATION

SHOP AWNINGAir Conditioning Duct Linings Available in Sizes:Doors 2.44 M X 1.22 M 4mm & 6 mmDadowork 1.83 M X 1.22 M 4mm & 6 mm

1.22 M X 1.22 M 4mm & 6 mm

2.100

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.9.4 GUTTER ACCESSERIES

2.9.5 ROOF ACCESSERIES

2.11

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.10 INSTALLATION PROCEDURE

1. Do not stack more than 150 sheets, one over the other. If possible, do not expose tosunlight.

2. To lift hold the sheets only in the places marked 'L'.3. Improper storage of sheets may result in to damage of the sheets. The damage will

be noticed only after installation.4. Always store sheets on three even level supports. Sheets of varying length should be

stacked separately.5. Always carry the sheets lengthwise, not width wise. If sheets have to be stored for

long, keep indoors.6. The distance between two purlins should not be more than 1.40 meters for roofing

and 1.70 meters for side cladding. Clamp with a purlin at the end of each sheet.7. Do not make holes in the sheet by punching, always drill holes. The drilled hole

should be 3mm. Bigger than the bolt. Use a Bitumen washer to seal holes.8. The hole should be drilled at least 2.95mm. away from the edge of the sheet. Initially

tighten nut bolts with the hand only. After 13-14 sheets are installed then all the nutbolds should be tightened together.

9. Tighten the nut in such a way that the bitumen - washer can seal the space betweenthe bolt and the hole. Do not tighten the bolt too much, otherwise the sheet willcrack. Use a spanner to tighten nut finally.

10. For a secure fitting, wherever 4 sheets have to be joined the corners should bemitred. The cut corners should be 150mm. in length and 44mm. in breadth. Use asaw to cut corners. Do not use a cutter.

11. Put bolts only in crowns, not in valleys.12. The bolt should pass through the second and the last sheet.13. Use a cat ladder for working on the roof.14. The outlet of the gutter line should not more than 15meters away.15. The length of the free overhang should more than300mm.

2.122

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.10.1 PROCEDURE OF MITRING:

For the bottom row A, the first sheet should be cut; DDG. -- Cut in the upper leftcorner.

For the second and middle rows B cut the bottom right corner of the first sheet. E--upper left-hand corners and bottom right hand corners to be cut. H--cut only upper left corner of the last sheet. For the upper row cut bottom right corners of C, F and F. Fix I without any cut.

2.11 SERVISES

In an ambition to always focus on customer needs, we provide prompt pre and post salessupport.

We also provide technical support and training to our dealers and distributors forproper handling Fibre Cement Corrugated Sheets and accessories.

Once an order is placed, it is executed within 48 hours and delivered at clients' place. We believe in quick delivery, efficient and best quality service to our customers and

dealers. Our service as a whole is also directed towards the society in creating employment

and providing high class products for creating solid housing and industrialinfrastructure.

2.13

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

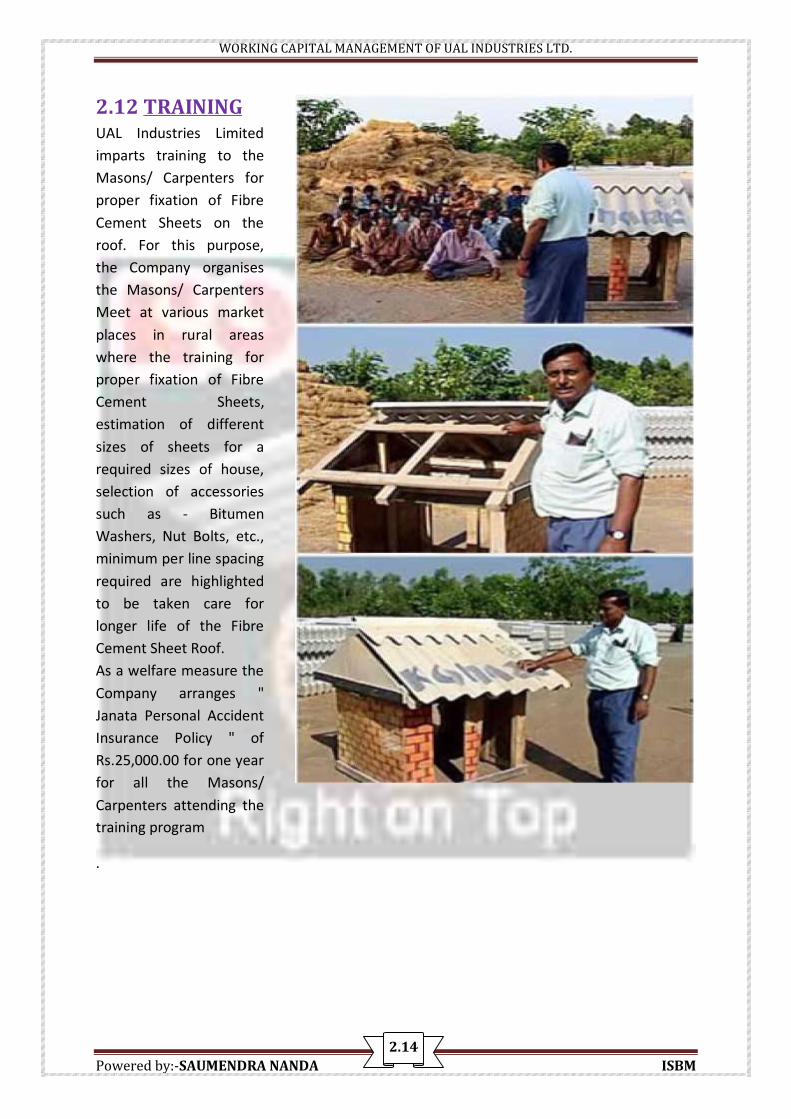

2.12 TRAININGUAL Industries Limitedimparts training to theMasons/ Carpenters forproper fixation of FibreCement Sheets on theroof. For this purpose,the Company organisesthe Masons/ CarpentersMeet at various marketplaces in rural areaswhere the training forproper fixation of FibreCement Sheets,estimation of differentsizes of sheets for arequired sizes of house,selection of accessoriessuch as - BitumenWashers, Nut Bolts, etc.,minimum per line spacingrequired are highlightedto be taken care forlonger life of the FibreCement Sheet Roof.As a welfare measure theCompany arranges "Janata Personal AccidentInsurance Policy " ofRs.25,000.00 for one yearfor all the Masons/Carpenters attending thetraining program

.

2.14

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.13 QUALITY POLICIESWe, at UAL Industries Ltd., place an identification and satisfaction of customers needs inthe field of Fibre Cement Sheets and accessories as our main goal. We shall try toachieve this by complying and reviewing Quality Management System for continualimprovement, efficient utilization of resources and involvement of people for trainingand awareness. We aim to achieve the above, by implementing a quality managementsystem conforming to ISO 9001: 2000 Standards.

Our major products, i.e., Fibre cement corrugated sheets with brand name "KONARK"are produced conforming to the BIS specification of IS 459:1992 with ISI Marking. Ourother products are: Asbestos cement building boards produced conforming to IS 2098:1997 and Fibre Cement Gutters & Roofing Accessories produced conforming to IS1626(part 2): 1994 & IS 1626(part 3): 1994. Our manufacture is based on adoptedTechnology with best usage of computer- aided programming system and the bestavailable raw materials, imported and indigenous, scientifically blended. The productsundergo strict quality control procedure in every stage of the manufacturing processuntil the product is ready for delivery.Latest Orientation Technology is applied to obtain optimum Orientation Factor for thefibres of our product matrix to make them functionally more stable. The Bureau ofIndian Standards with their Scheme of Testing & Inspection periodically verifies ourproduct quality for ISI marking.Being an ISO 9001: 2008 Company, our quality system is also periodically audited andcertified by BVQI (Bureau verities Quality International), London. All our processes andtesting equipment are periodically calibrated by accredited external agencies. Theproducts are weather resistant, maintenance free, permanent and their intrinsicproperties being appreciated further with time. Prompt customer service is our priorityand embedded in our quality system.2.15

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.14 ENVIRONMENT POLICIESWe at UAL Industries Ltd. undertake necessary measures to maintain an Eco-friendlyenvironment. We follow an effective Environment Management System.

The Thermal Power Plants emit millions of tons of fly ash annually, which are hazardous andcause a serious challenge to Ecosystem. It may be worthwhile to mention that after lot ofR&D, we are using Fly Ash as a major raw material since 1992 for safeguarding theenvironment from pollution and stop health hazards.

Manufacturing of AC Products consumes nearly 36 times less energy than its alternativemetallic substitute thereby saving environment and atmosphere from addition of moretoxins. Therefore our products are most cost effective and competitive.

We have installed pollution control devices at the plant and all our pollution controlequipment are interlocked with the plant operations. In case of failure of any pollutioncontrol devices, the process functioning will automatically stop. We have installed separateenergy meters for each and every pollution control devices.

The industry is running with the concept of "ZERO" effluent management. Processed wastewater is recycled in the manufacturing process and domestic waste is discharged throughseptic tanks and soaks pits and reused in the green belt development.

Ambient and stack air monitoring, work zone monitoring and health monitoring of allemployees are being conducted periodically. The company has well planned solid wastemanagement as all discards and rejects of sheet are pulverized and recycled back in theprocess. The company works on "ZERO" Waste Management Principle.

It is relevant to mention that our products are Eco-friendly as the company is ISO 14001:1996 certified by BVQI (Bureau verities Quality International), London for EnvironmentalManagement System under accreditation from UKAS, UK.

2.15 ENVIRONMENT AUDIT

Environmental Audit as per ISO 14001: 1996 schedule Internal Audit conducted by trained / certified officers of the company Results of environmental audit – discussed in environmental management review

meeting Appropriate action initiated.

2.16

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.16 AWARDS

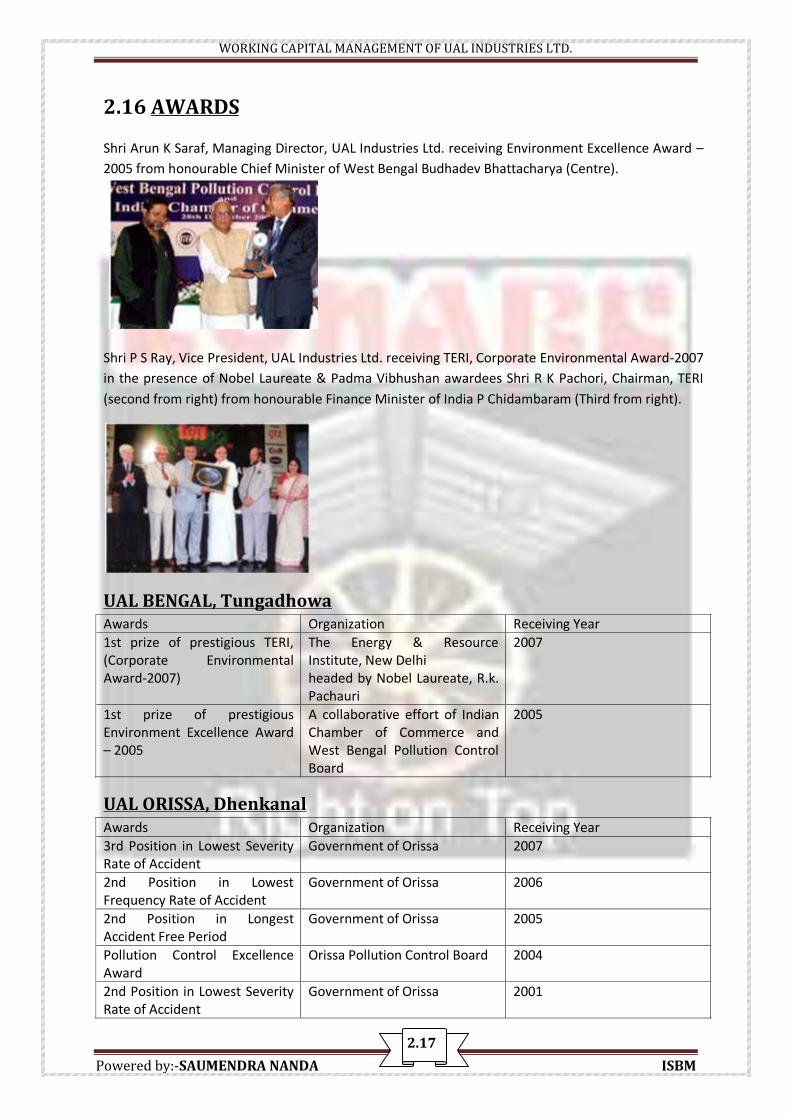

Shri Arun K Saraf, Managing Director, UAL Industries Ltd. receiving Environment Excellence Award –2005 from honourable Chief Minister of West Bengal Budhadev Bhattacharya (Centre).

Shri P S Ray, Vice President, UAL Industries Ltd. receiving TERI, Corporate Environmental Award-2007in the presence of Nobel Laureate & Padma Vibhushan awardees Shri R K Pachori, Chairman, TERI(second from right) from honourable Finance Minister of India P Chidambaram (Third from right).

UAL BENGAL, TungadhowaAwards Organization Receiving Year1st prize of prestigious TERI,(Corporate EnvironmentalAward-2007)

The Energy & ResourceInstitute, New Delhiheaded by Nobel Laureate, R.k.Pachauri

2007

1st prize of prestigiousEnvironment Excellence Award– 2005

A collaborative effort of IndianChamber of Commerce andWest Bengal Pollution ControlBoard

2005

UAL ORISSA, DhenkanalAwards Organization Receiving Year3rd Position in Lowest SeverityRate of Accident

Government of Orissa 2007

2nd Position in LowestFrequency Rate of Accident

Government of Orissa 2006

2nd Position in LongestAccident Free Period

Government of Orissa 2005

Pollution Control ExcellenceAward

Orissa Pollution Control Board 2004

2nd Position in Lowest SeverityRate of Accident

Government of Orissa 2001

2.17

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.17 CERTIFICATESUAL ORISSA, DHENKANALCertification Organization Receiving YearISO 9001:2008 TUV India Pvt. Ltd. 2008OHSAS-18001-2007 TUV India Pvt. Ltd. 2008ISO 14001-2004 TUV India Pvt. Ltd. 2004

UAL BENGAL, TUNGADHOWACertification Organization Receiving YearISO 9001:2008 & ISO14001:2004

Bureau Veritas 2008

OHSAS-18001-2007 Bureau Veritas 2008ISO 14001-2004-2008 BVQI (Bureau Veritas Quality International) accredited

by UKAS, London2008

ISO 9001:2000 BVQI (Bureau Veritas Quality International) accreditedby UKAS, London

2004

CERTIFICATES FOR CORPORATE SOCIAL RESPONSIBILITYCertification Organization Receiving YearShabujtama Silpa Pratisthan West Bengal Govt. (Aranya Saptaha) 2010Shabujtama Silpa Pratisthan West Bengal Govt. (Aranya Saptaha) 2010

2.18

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

2.18 DISTRIBUTION NETWORK

ODISHA

SALES DEPOTS

BALASORENear Assam Oil Petrol PumpNh-5, Vill- Biruan GaonP.O- Sergarh, Dist- BalasorePin-756060, ODISHA

SAMBALPURJoshi GardenCuttack RoadP.O-DhanupalliSambalpur - 768005

SALES OFFICE

DHENKANALAt+Po - KorianP.Box No - 8Dhenkanal - 759001ODISHA

BHUBANESWAR165 Cuttack RoadBomikhalBhubaneswar-751006

ASSAM

SALES DEPOTS

GUWAHATINH: 37, GorchukNear Tirupati Weigh BridgeGuwahatiAssam – 781035

BIHAR

SALES DEPOTSSIWANChap Tola, Teghra,Chhapra Road

Siwan - 841226Bihar

PATNA3 Sf -A, 5/6, Hig Bhoot NathRoadBahadurpur Housing ColonyPatna - 801505Bihar

MOTIHARIDevraha Baba ChowkKoluharawa, MotihariEast Champaran - 845401Bihar

CHATTISGARH

CHATTISGARHAman NagarMowa, RaipurChattisgarh-490023

JHARKHAND

BOKARORanchi Ramghar RoadNear- Durga Mandir, BalidihBokaro Steel City -14BokaroJharkhand

RANCHINh-33, Bargawa, NamkumRanchi, Jharkhand

TATANh-33 Pardih KumrumP.O- Kapali, JamshedpurDist- Singhbhum (East)Jharkhand

MADHYA PRADESHMADHYAPRADESHKatniMadhya Pradesh

UTTAR PRADESH

VARANASI11/4 Kuber ComplexD/58/2, Rathajatra

KOLKATA

BURDWANC/O. M/S. Nazrul Saw MillSadar Ghat RoadP.O- Sri PallyBurdwan

BARRACKPOREUAL-BengalProp. UAL Industries Ltd.Vill. KonkaporeP.O. NIlgunj Bazar,P.S. Barasat, Dist. 24 Pgs.,Kolkata-700121

RAIGANJBARODUARI, SAHARAI, NH-34(Opp- Ibp Petrol Pump)RaigunjMadhpur-733134Uttardinajpur

BARUIPURRamnagar, ShanibattalaCanning Road,24 Pgs(S)Baruipur,Kolkata-700144

2.19

WORKING CAPITAL MANAGEMENT

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

WORKING CAPITAL

3.1 MEANING OF WORKING CAPITALWorking capital (abbreviated WC) is a financial metric which represents operatingliquidity available to a business, organization or other entity, including governmentalentity. Along with fixed assets such as plant and equipment, working capital isconsidered a part of operating capital. Net working capital is calculated as currentassets minus current liabilities. It is a derivation of working capital that is commonlyused in valuation techniques such as DCFs (Discounted cash flows). If current assets areless than current liabilities, an entity has a working capital deficiency, also called aworking capital deficit.A company can be endowed with assets and profitability but short of liquidity if itsassets cannot readily be converted into cash. Positive working capital is required toensure that a firm is able to continue its operations and that it has sufficient funds tosatisfy both maturing short-term debt and upcoming operational expenses. Themanagement of working capital involves managing inventories, accounts receivable andpayable, and cash.3.2 CONCEPTS OF WORKING CAPITALThere are two concepts of working capital, namely Gross concept and Net concept.Gross Working Capital According to this concept; working capital refers to the firm’sinvestment in current assets. The amount of current liabilities is not deducted from thetotal of current assets. This concept views Working Capital and aggregate of CurrentAssets as two inter-changeable terms. This concept is also referred to as `CurrentCapital' or `Circulating Capital'.The proponents of the gross working capital concept advocate this for the followingreasons:I. Profits are earned with the help of assets, which are partly fixed and partlycurrent. To a certain degree, similarity can be observed in fixed and currentassets so far as both are partly financed by borrowed funds, and are expected toyield earnings over and above the interest costs. Logic then demands that theaggregate of current assets should be taken to mean the working capital.II. Management is more concerned with the total current assets as they constitutethe total funds available for operating purposes than with the sources fromwhich the funds come.III. An increase in the overall investment in the enterprise also brings about anincrease in the working capital.Net Working CapitalThe net working capital refers to the difference between current assets and currentliabilities. Current liabilities are those claims of outsiders, which are expected to maturefor payment within an accounting year and include creditor’s dues, bills payable, bank

3.1

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

overdraft and outstanding expenses. Net working capital can be positive or negative. Anegative net working capital occurs when current liabilities are in excess of currentassets."Whenever working capital is mentioned it brings to mind current assets and currentliabilities with a general understanding that working capital is the difference betweenthe two".‘Net working capital’ is a qualitative concept, which indicates the liquidity position ofthe firm and the extent to which working capital needs may be financed by permanentsources of finds. This needs some explanation.Current assets should be sufficiently in excess of current liabilities to constitute amargin or buffer for obligations maturing within the ordinary operating cycle of abusiness. A weak liquidity position poses a threat to the solvency of the company andmakes it unsafe. Excessive liquidity is also bad. It may be due to mismanagement ofcurrent assets. Therefore, prompt and timely action should be taken by management toimprove and correct the imbalance in the liquidity position of the firm.The net working capital concept also covers the question of a judicious mix of long-term and short-term funds for financing current assets. Every firm has a minimumamount of net working capital, which is permanent. Therefore, this portion of theworking capital should be financed with permanent sources of funds such as owners'capital, debentures, long-term debt, preference capital and retained earnings:Management must decide the extent to which current assets should be financed withequity capital and/or borrowed capital.Several economists uphold the net working capital concept. In support of their stand,they state that: In the long run what matters is the surplus of current assets over currentliabilities. It is this concept which helps creditors and investors to judge the financialsoundness of the enterprise. It is the excess of current assets over current liabilities, which can be relied uponto meet contingencies since this amount is not liable to be returned. It helps to ascertain the correct comparative financial position of companieshaving the same amount of current assets.

It may be stated that gross and net concepts of working capital are two important facetsof working capital management. Both the concepts have operational significance for themanagement and therefore neither can be ignored. While the net concept of workingcapital emphasizes the qualitative aspect, the gross concept underscores thequantitative aspect.3.3 SIGNIFICANCE OF WORKING CAPITALYou will hardly find a running business firm, which does not require some amount ofworking capital. Even a fully equipped manufacturing firm is sure to collapse without(a) An adequate supply of raw materials to process,(b) Cash to meet the wage bill,

3.2

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

(c) The capacity to wait for the market for its finished products, and(d) The ability to grant credit to its customers.Similarly, a commercial enterprise is virtually good for nothing without merchandise tosell. Working capital, thus, is the life-blood of a business. As a matter of fact, anyorganisation, whether profit-oriented or otherwise, will not be able to carry on day-to-day activities without adequate working capital.3.4 Circulation of Working CapitalAt one given time both the current assets and current liabilities exist in the business.The current assets and current liabilities are flowing round in a business like an electriccurrent. However, “The working capital plays the same role in the business as the role ofheart in human body. Working capital funds are generated and these funds arecirculated in the business. As and when this circulation stops, the business becomeslifeless. It is because of this reason that he working capital is known as the circulatingcapital as it circulates in the business just like blood in the human body.”The chart depicting ‘Working Capital Cycle’ makes it clear that the amount of cash isobtained mainly from issue of shares, borrowing and operations. Cash funds are used topurchase fixed assets, raw materials and used to pay to creditors. The raw materials areprocessed; wages and overhead expenses are paid which in result produce finishedgoods for sale.

The sale of goods may be for cash or credit. In the former case, cash is directly receivedwhile in later case cash is collected from debtors. Funds are also generated fromoperation and sale of fixed assets. A portion of profit is used for payment of interest, taxand dividends while remaining is retained in the business. This cycle continuesthroughout the life of the business firm.3.5 Classification of Working CapitalThe quantitative concept of Working Capital is known as gross working capital whilethat under qualitative concept is known as net working capital.Working capital can be classified in various ways. The important classifications are asgiven below:

3.3

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

Conceptual classification – There are two concept of working capital viz.,quantitative and qualitative. The quantitative concept takes into account as the currentassets while the qualitative concept takes into account the excess of current assets overcurrent liabilities. Deficit of working capital exists where the amount of currentliabilities exceeds the amount of current assets. The above can be summarised asfollows:(i) Gross Working Capital = Total Current Assets(ii) Net Working Capital = Excess of Current Assets over Current Liabilities(iii) Working Capital Deficit = Excess of Current Liabilities over Current Assets.Classification on the basis of financial reports – The information of working capitalcan be collected from Balance Sheet or Profit and Loss Account; as such the workingcapital may be classified as follows:(i) Cash Working Capital – This is calculated from the information contained in profitand loss account. This concept of working capital has assumed a great significance inrecent years as it shows the adequacy of cash flow in business. It is based on ‘OperatingCycle Concept’s which is explained later in this chapter.(ii) Balance Sheet Working Capital – The data for Balance Sheet Working Capital iscollected from the balance sheet. On this basis the Working Capital can also be dividedin three more types, viz., gross Working Capital, net Working Capital and WorkingCapital deficit.

Classification on the Basis of Variability – Gross Working Capital can bedivided in two categories viz., (i) permanent or fixed working capital, and (ii)Temporary, Seasonal or variable working capital. Such type of classification is veryimportant for hedging decisions.(i) Temporary Working Capital – Temporary Working Capital is also called asfluctuating or seasonal working capital. This represents additional investment neededduring prosperity and favourable seasons. It increases with the growth of the business.”Temporary working capital is the additional assets required to meet the variations insales above the permanent level.” This can be calculated as follows:Temporary Working Capital = Total Current Assets – permanent Current Assets(ii) Permanent Working Capital – It is a part of total current assets which is notchanged due to variation in sales. There is always a minimum level of cash, inventories,and accounts receivables which is always maintained in the business even if sales arereduced to a minimum. Amount of such investment is called as permanent workingcapital. “Permanent Working Capital is the amount of working capital that persists overtime regardless of fluctuations in sales.”This is also called as regular working capital.3.6 Factors Influencing Working Capital RequirementNumerous factors can influence the size and need of working capital in a concern. So noset rule or formula can be framed. It is rightly observed that, “There is no precise way todetermine the exact amount of gross or net working capital for every enterprise. Thedata and problem of each company should be analysed to determine the amount ofworking capital.Briefly, the optimum level of current assets depends upon following determinants.

Nature of business--Trading and industrial concerns require more funds forworking capital. Concerns engaged in public utility services need less working capital.For example, if a concern is engaged in electric supply, it will need less current assets,firstly due to cash nature of the transactions and secondly due to sale of services.However, it will invest more in fixed assets.3.4

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

In addition to it, the investment varies concern to concern, depending upon thesize of business, the nature of the product, and the production technique.Conditions of supply-- If the supply of inventory is prompt and adequate, lessfunds will be needed. But, if the supply is seasonal or unpredictable, more funds will beinvested in inventory. Investment in working capital will fluctuate in case of seasonalnature of supply of raw materials, spare parts and stores.Production policy-- In case of seasonal fluctuations in sales, production willfluctuate accordingly and ultimately requirement of working capital will also fluctuate.However, sales department may follow a policy of off-season discount, so that sales andproduction can be distributed smoothly throughout the year and sharp, variations inworking capital requirement are avoided.Seasonal Operations-- It is not always possible to shift the burden ofproduction and sale to slack period. For example, in case of sugar mill more workingcapital will be needed at the time of crop and manufacturing.Credit Availability- If credit facility is available from banks and suppliers onfavourable terms and conditions, less working capital will be needed. If such facilitiesare not available more working capital will be needed to avoid risk.Credit policy of enterprises-- In some enterprises most of the sale is at cashand even it is received in advance while, in other sales is at credit and payments arereceived only after a month or two. In former case less working capital is needed thanthe later. The credit terms depend largely on norms of industry but enterprise someflexibility and discretion. In order to ensure that unnecessary funds are not tied up inbook debts, the enterprise should follow a rationalized credit policy based on the creditstanding of the customers and other relevant factors. Growth and expansion-- Theneed of working capital is increasing with the growth and expansion of an enterprise. Itis difficult to precisely determine the relationship between volume of sales and theworking capital needs. The critical fact, however, is that the need for increased workingcapital funds does not follow growth in business activities but precedes it. It is clear thatadvance planning is essential for a growing concern.Price level change─ With the increase in price level more and more workingcapital will be needed for the same magnitude of current assets. The effect of risingprices will be different for different enterprises.Circulation of working capital─ Less working capital will be needed with theincrease in circulation of working capital and vice-versa. Circulation means timerequired to complete one cycle i.e. from cash to material, from material to work-in-progress, form work-in-progress to finished goods, from finished goods to accountsreceivable and from accounts receivable to cash.Volume of sale-- This is directly indicated with working capital requirement,with the increase in sales more working capital is needed for finished goods anddebtors, its vice versa is also true.Liquidity and profitability-- There is a negative relationship between liquidityand profitability. When working capital in relation to sales is increased it will reducerisk and profitability on one side and will increase liquidity on the other side.Management ability ─ Proper co-ordination in production and distribution ofgoods may reduce the requirement of working capital, as minimum funds will beinvested in absolute inventory, non-recoverable debts, etc.

External Environment ─ With development of financial institutions, means ofcommunication, transport facility, etc., needs of working capital is reduced because itcan be available as and when needed.3.5

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

3.7 COMPONENTS OF WORKING CAPITALYou have already noted that working capital has two components: Current assets andCurrent liabilities. Current assets comprise several items. The typical items are:I. Cash to meet expenses as and when they occur.II. Accounts Receivables or sundry trade debtorsIII. Inventory of:a) Raw materials, stores, supplies and spares,b) Work-in-process, andc) Finished goodsd) Advance payments towards expenses or purchases, and other short-termadvances which are recoverable.e) Temporary investment of surplus funds which could be converted intocash whenever needed.A part of the need for funds to finance the current assets may be met from supply of.Goods on credit, and deferment, on account of custom, usage or arrangement, ofpayment for expenses. The remaining part of the need for working capital may be metfrom short-term borrowing from financiers like banks. These items are collectivelycalled current liabilities. Typical items of current liabilities are:I. Goods purchased on creditII. Expenses incurred in the course of the business of the organisation (e.g.,wages or salaries, rent, electricity bills, interest etc.) which are not yetpaid for.III. Temporary or short term borrowings from banks, financial institutionsor other partiesIV. Advances received from parties against goods to be sold or delivered, oras short term deposits.V. Other current liabilities such as tax and dividends payable. Some of themajor components of current assets are explained here in brief:Cash: All of us know that the basic input to start any business is cash. Cash is initiallyrequired for acquiring fixed assets like plants and machinery which enables a firm toproduce products and generate cash by selling them. Cash is also required and investedin working capital. An investment in working capital is required, as firms have to storecertain quantity of raw materials and finished goods and also for providing credit termsto the customers.A minimum level of cash helps in the conduct of everyday ordinary business such asmaking of purchases and sales as well as for meeting the unexpected payments,developments and other contingencies. As discussed earlier cash invested at thebeginning of-the operating cycle gets released at the end of the cycle to fund freshinvestments. However, additional cash is required by the firm when it needs to buymore fixed assets, increase the level of operations or for bringing out change in workingcapital cycle such as extending credit period to the customers.The demand for cash is affected by several factors, some of them are within the controlof the managers and some are outside their control. It is not possible to operate thebusiness without holding cash but at the same time holding it without a purpose alsocosts a firm either directly in the form of interest or loss of income that could be earnedout of the cash.

3.6

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

In the context of working capital management, cash management refers to optimizingthe benefit and cost associated with holding cash. The objective of cash management isbest achieved by speeding up the working capital cycle, particularly the collectionprocess and investing surplus cash in short term assets in most profitable avenues.We will be subsequently discussing certain issues like the management of cash flowsand determination of optimal cash balance, etc.Accounts Receivable: Firms rather prefer to sell for cash than on credit, butcompetitive pressures force most firms to offer credit. Today the use of credit in thepurchase f goods and services is so common that it is taken for granted. Selling goods orproviding services on credit basis leads to accounts receivable. When consumers expectcredit, business units in turn expect credit from their suppliers to match theirinvestment in credit extended to consumers. The granting of credit from one businessfirm to another for purchase of goods and services is popularly known as trade credit.Though commercial banks provide a significant part of requirements for workingcapital, trade credit continues to be a major source of funds for firms and accountsreceivable that result from granting trade credit are major investment for the firm.Both direct and indirect costs are associated with carrying receivables, but it has animportant benefit for increasing sales. Excessive levels of accounts receivables result indecline of cash flows and much result in bad debts which in turn may reduce the profitof the firm. Therefore, it is very important to monitor and manage receivables carefullyand regularly. We would be dealing with this topic in MS-41: Working CapitalManagement.Inventory: Three things will come to your mind when you think of a manufacturingunit - machines, men and materials. Men using machines and tools convert the materialsinto finished goods. The success of any business unit depends on the extent to whichthese are efficiently managed. Inventory is an asset to the organisation like othercomponents of current assets.Inventory constitutes a very significant part of working capital or current assets inmanufacturing organisation. It is essential to control inventories (physical/quantitycontrol and value control) as these are significant elements in the costing processconstituting sometimes more than 60% of the current assets.Inventory holding is desirable because it meets several objectives and needs but anexcessive inventory is undesirable because it costs a lot to firms.Inventory which consists of raw material components and other consumables, work inprocess and finished goods, is an important component of `current assets'. There areseveral factors like nature of industry, availability of material, technology, businesspractices, price fluctuation, etc. that determines the amount of inventory holding.Holding inventory ensures smooth production process, price stability and immediatedelivery to customers. Since inventory is like any other form of assets, holding inventoryhas a cost. The cost includes opportunity cost of funds blocked in inventory, storagecost, stock out cost, etc. The benefits that come from holding inventory should exceedthe cost to justify a particular level of inventory.Marketable Securities: Cash and marketable securities are normally treated as oneitem in any analysis of current assets although these are not the same as cash they canbe converted to cash at a very short notice. Holding cash in excess of immediate

3.7

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

requirement means the firm is missing out an opportunity income. Excess cash isnormally invested in marketable securities, which serves two purposes namely, provideliquidity and, also earn a return.3.8 Forecasting of Working CapitalTo forecast the working capital requirement for the next year the followingformula may be used:(Estimated cost of goods sold x Operating Cycle) + Desired Cash Balance3.9 Control of Working CapitalWorking capital requirement depends upon the level of operation and the length ofoperating cycle. Monitoring the duration of the operating cycle is an importantingredient of working capital control. In this context, the following points should bornein mind:1. The duration of the raw material stage depends on regularity of supply,transportation time, price fluctuations and economy of bulk purchase. Forimported materials it takes a longer time.

Example – X Ltd. expects its cost of goods sold for the forthcoming year to be Rs.2 crore. The present operating cycle of the firm is 78 days. The firm plans toreduce its operating cycle to 73 days and desired cash balance is Rs. 5 lakh.The expected working capital requirement would be,2,00,00,000 x 73/365 + 5,00,000 = Rs. 45,00,0002. The duration of the work-in-process depends on the length of manufacturing cycle,consistency in capacities at different stages, and efficient coordination of variousinputs.3. The duration of the finished goods depends on the pattern of production and sales.If production is fairly uniform throughout the year but sales are highly seasonalor vice versa. The duration of finished goods tends to be long.4. The duration at the debtor’s stage depends on the credit period granted, discountsoffered for prompt payment, and efficiency and rigour of collection efforts.It is helpful to monitor the behaviour of overall operating cycle and its individualcomponents. For this purpose time series analysis and cross section analysis may bedone. In time series analysis the duration of the operating cycle and its individualcomponents is compared over a period of time for same firm. In cross section analysisthe duration of the operating cycle and its individual components is compared with thatof other firms of a comparable nature.Adequacy of Working CapitalThe importance of adequacy of working capital can hardly be over-emphasized. John L.O. Donnell and Milton S. Gladberg observe “Many a times business failure takes place due to lackof working capital.” Hence, working capital is considered as the life blood and the controllingnerve centre of a business. Inadequate working capital is business ailment. Therefore, a firm hasto maintain a sound working capital. It should be adequate foe the following reasons:(1) It protects a business form the adverse effects of shrinkage in the values of current assets.

3.8

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

(2) It is possible to pay all the current obligations promptly and to take advantage ofcash discounts.(3) It ensures, to a greater extent, the maintenance of a company’s credit standing andprovides for such emergencies as strikes, floods, fires etc.(4) It permits the carrying of inventories at a level that would enable a business to servesatisfactorily the needs of its customers.(5)` It enables a company to extend favourable credit terms to its customers.(6) It enables a company to operate its business more efficiently because there is nodelay in obtaining materials, etc., because of credit difficulties.(7) It enables a business to withstand periods of depression smoothly.(8) There may be operating losses or decreased retained earnings.(9) There may be excessive non-operating or extraordinary losses.(10) The management may fail to obtain funds from other sources for purposes ofexpansion.(11) There may be an unwise dividend policy(12) Current funds may be invested in non-current assets(13) The management may fail to accumulate funds necessary for meeting debentureson maturity.(14) Increasing price may necessitate bigger investments in inventories and fixed asset.3.10 Source of Working CapitalConventional generalizations relating to financing of working capital suggest thatan amount equal to the basic minimum of current assets should be financed from long-term source and that only seasonal needs of working capital should be financed fromshort-term sources. It is obvious that such an arrangement helps to keep the cost ofworking capital finance to the minimum for an enterprise and gives a rise to its rate ofreturn on the total funds employed. Viewed thus, the sources of working finance can beclassified into permanent and the current sources of working capital finance.3.11 Structure of Working CapitalThe study of structure of working capital is another name for the study of workingcapital cycle. In other words, it can be said that the study of structure of working capitalis the study of the elements of current assets viz. inventory, receivable, cash and bankbalances and other liquid resources like short-term or temporary investments. Currentliabilities usually comprise bank borrowings, trade credits, assessed tax and unpaiddividends or any other such things. The following points mention relating to variouselements of working capital deserves:

Inventory– Inventory is major item of current assets. The management ofinventories – raw material, goods-in-process and finished goods is an important factorin the short-run liquidity positions and long-term profitability of the company.Raw material inventories– Uncertainties about the future demand for finishedgoods, together with the cost of adjusting production to change in demand will cause afinancial manager to desire some level of raw material inventory. In the absence of such

3.9

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

inventory, the company could respond to increased demand for finished goods only byincurring explicit clerical and other transactions costs of ordinary raw material forprocessing into finished goods to meet that demand. If changes in demand are frequent,these order costs may become relatively large. Moreover, attempts to purchases hastilythe needed raw material may necessitate payment of premium purchases prices toobtain quick delivery and, thus, raises cost of production. Finally, unavoidable delays inacquiring raw material may cause the production process to shut down and then re-start again raising cost of production. Under these conditions the company cannotrespond promptly to changes in demand without sustaining high costs. Hence, somelevel of raw materials inventory has to be held to reduce such costs. Determining itsproper level requires an assessment of costs of buying and holding inventories and acomparison with the costs of maintaining insufficient level of inventories.Work-in-process inventory– This inventory is built up due to production cycle.Production cycle is the time-span between introduction of raw material into productionand emergence of finished product at the completion of production cycle. Till theproduction cycle is completed, the stock of work-in-process has to be maintained.Finished goods inventory– Finished goods are required for reasons similar tothose causing the company to hold raw materials inventories. Customer’s demand forfinished goods is uncertain and variable. If a company carries no finished goodsinventory, unanticipated increases in customer demand would require suddenincreases in the rate of production to meet the demand. Such rapid increase in the rateof production may be very expensive to accomplish. Rather than loss of sales, becausethe additional finished goods are not immediately available or sustain high costs ofrapid additional production, it may be cheaper to hold a finished goods inventory. Theflexibility afforded by such an inventory allows a company to meet unanticipatedcustomer demands at relatively lower costs than if such an inventory is not held.Thus, to develop successfully optimum inventory policies, the management needs toknow about the functions of inventory, the cost of carrying inventory, economic orderquantity and safety stock. Industrial machinery is usually very costly and it is highlyuneconomical to allow it to lie idle. Skilled labour also cannot be hired and fired at will.Modern requirements are also urgent. Since requirements cannot wait and since thecost of keeping machine and men idle is higher, than the cost of storing the material, it iseconomical to hold inventories to the required extent. The objectives of inventorymanagement are:(1) To minimize idle cost of men and machines causes by shortage of raw materials,stores and spare parts.(2) To keep down:(a) Inventory ordering cost.(b) Inventory carrying cost,(c) Capital investment in inventories.(d) Obsolescence lossesReceivables – Many firms make credit sales and as a result thereof carryreceivable as a current asset. The practice of carrying receivables has severaladvantages viz., (i) reduction of collection costs over cash collection, (ii) Reduction inthe variability of sales, and (iii) increase in the level of near-term sales. While immediate

3.104

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

collection of cash appears to be in the interest of shareholders, the cost of that policymay be very high relative to costs associated with delaying the receipt of cash byextension of credit. Imagine, for example, an electric supply company employing aperson at every house constantly reading electricity meter and collecting cash from himevery minute as electricity is consumed. It is far cheaper for accumulating electricityusage and bill once a month. This of course, is a decision to carry receivables on the partof the company. It may also be true that the extension of credit by the firm to itscustomers may reduce the variability of sales over time. Customers confined to cashpurchases may tend to purchase goods when cash is available to them. Erratic andperhaps cyclical purchasing patterns may then result unless credit can be obtainedelsewhere. Even if customers do obtain credit elsewhere, they must incur additionalcost of search in arranging for a loan costs that can be estimated when credit is given bya supplier. Therefore, extension of credit to customers may well smooth out of thepattern of sales and cash inflows to the firm over time since customers need not wait forsome inflows of cash to make a purchase. To the extent that sales are smoothed, cost ofadjusting production to changes in the level of sales should be reduced. Finally, theextension of credit by firms may act to increase near-term sales. Customers need notwait to accumulate necessary cash to purchase an item but can acquire it immediatelyon credit. This behaviour has the effect of shifting future sales close to the present time.Therefore, the extension of credit by a firm and the resulting investment in receivablesoccurs because it pays a firm to do so. Costs of collecting revenues and adapting tofluctuating customer demands may make it desirable to offer the convenienceassociated with credit to firm’s customers. To the extents that near sales are alsoincreased, extension of credit is made even more attractive for the firm.Cash and interest-bearing liquid assets– Cash is one of the most importanttools of day-to-day operation, because it is a form of liquid capital which is available forassignment to any use. Cash is often the primary factor which decides the course ofbusiness destiny. The decision to expand a business may be determined by theavailability of cash and the borrowing of funds will frequently be dictated by cashposition. Cash-in-hand, however, is a non-earning asset. This leads to the question as towhat is the optimum level of this idle resource. This optimum depends on variousfactors such as the manufacturing cycle, the sale and collection cycle, age of the bills andon the maturing of debt. It also depends upon the liquidity of other current assets andthe matter of expansion. While a liberal maintenance of cash provides a sense ofsecurity, a lack of sufficiency of cash hampers day-to-day operations. Prudence,therefore, requires that no more cash should be kept on hand than the optimumrequired for handling miscellaneous transactions over the counter and pettydisbursements etc.It has not become a practice with business enterprises to avoid too much redundantcash by investing a portion of their earnings in assets which are susceptible to easyconversion into cash. Such assets may include government securities, bonds, debenturesand shares that are known to be readily marketable and that may be liquidated at amoment’s notice when cash is needed.

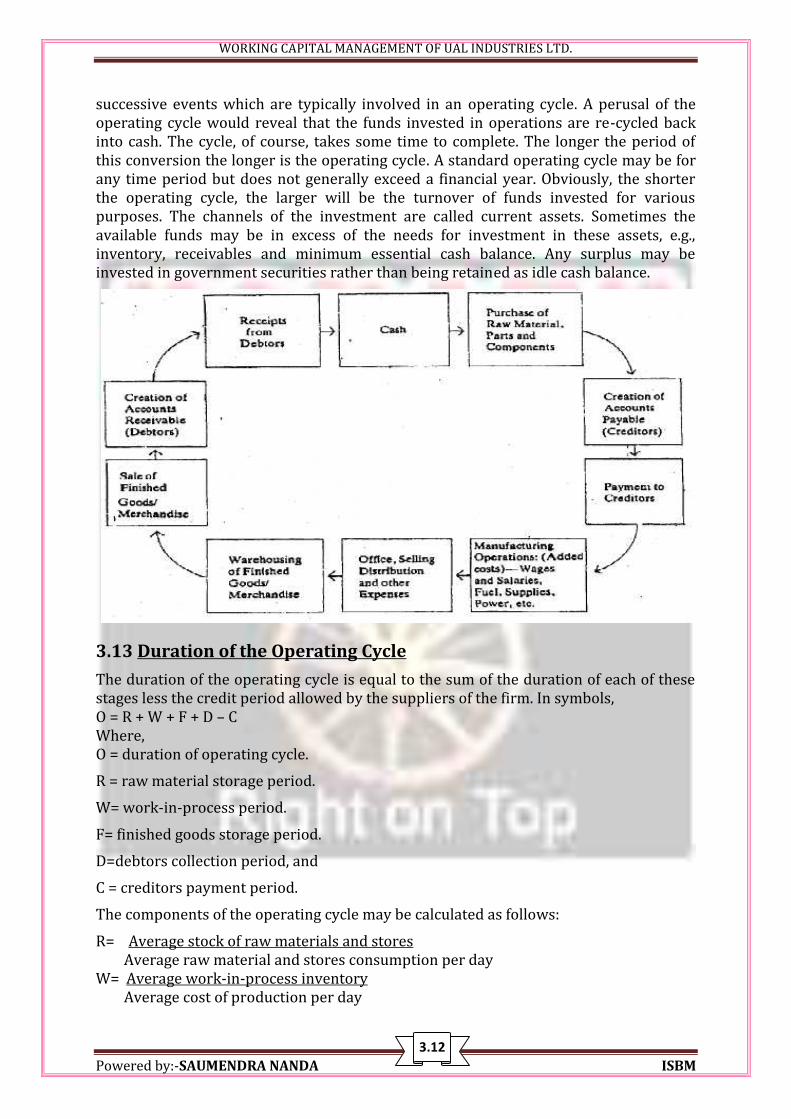

3.12 OPERATING CYCLEThe time between purchase of inventory items (raw material or merchandise) and theirconversion into cash is known as operating cycle or working capital cycle. The3.111

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

successive events which are typically involved in an operating cycle. A perusal of theoperating cycle would reveal that the funds invested in operations are re-cycled backinto cash. The cycle, of course, takes some time to complete. The longer the period ofthis conversion the longer is the operating cycle. A standard operating cycle may be forany time period but does not generally exceed a financial year. Obviously, the shorterthe operating cycle, the larger will be the turnover of funds invested for variouspurposes. The channels of the investment are called current assets. Sometimes theavailable funds may be in excess of the needs for investment in these assets, e.g.,inventory, receivables and minimum essential cash balance. Any surplus may beinvested in government securities rather than being retained as idle cash balance.

3.13 Duration of the Operating CycleThe duration of the operating cycle is equal to the sum of the duration of each of thesestages less the credit period allowed by the suppliers of the firm. In symbols,O = R + W + F + D – CWhere,O = duration of operating cycle.R = raw material storage period.W= work-in-process period.F= finished goods storage period.D=debtors collection period, andC = creditors payment period.The components of the operating cycle may be calculated as follows:R= Average stock of raw materials and storesAverage raw material and stores consumption per dayW= Average work-in-process inventoryAverage cost of production per day3.12

WORKING CAPITAL MANAGEMENT OF UAL INDUSTRIES LTD.

Powered by:-SAUMENDRA NANDA ISBM

F= Average finished goods inventoryAverage cost of goods sold per day per dayD= Average book debtsAverage credit sales per dayC= Average trade creditorsAverage credit purchase per dayWORKING CAPITAL MANAGEMENT