women's world banking presentation at 11th international microinsurance conference

TRANSCRIPT

1

Micro Insurance

Conference 2015

@womensworldbnkg

Gilles Renouil

Director, Microinsurance

2

Women account for the majority of the poor and the unbanked worldwide

60% of the working poor earning less than US$1 a day are women (ILO, 2005)

FINDEX 2014 data shows that 54% of adults in the poorest 40% households within

dev. economies remain unbanked. The gender gap remains at 9% in dev. economies.

Engaging women is key to advancement of families and societies…

Women tend to invest more of their income into the health, education and well-being

of their families (McKinsey)

…and to sustained economic growth

By 2030, the insurance industry is expected to earn up to $1.7 trillion from women

alone - with almost half coming from only 10 emerging economies (She4Shield IFC)

The global economy has missed out on 27% of GDP growth per capita due to gender

gap in the labor market (IMF, Sept 2013)

We are missing 12 trillion extra GDP growth by not achieving gender parity in a best

in region scenario (McKensey, Sept 2015)

If the credit gap for women-owned SMEs is closed by 2020, by 2030 incomes per

capita could be on average 12% higher across the BRICs and next 11 countries (Goldman Sachs, March 2014)

Why focus on women?

3

Women’s World Banking’s Global Footprint

35+ years focused on women’s access to finance

21 million active clients

68% women

40% rural

38 institutions

$8.5 billion in outstanding loan portfolio

$5.5 billion in deposits

13 banks

6 Non Banking Financial Institutions

16 NGOs

3 Cooperatives

LATIN AMERICA &

THE CARRIBEAN

Countries: 7

Institutions: 10

SUB-SAHARAN

AFRICA

Countries: 9

Institutions: 10

ASIA

Countries: 6

Institutions: 12

EUROPE

Countries: 1

Institutions: 1

MIDDLE EAST &

NORTH AFRICA

Countries: 5

Institutions: 5

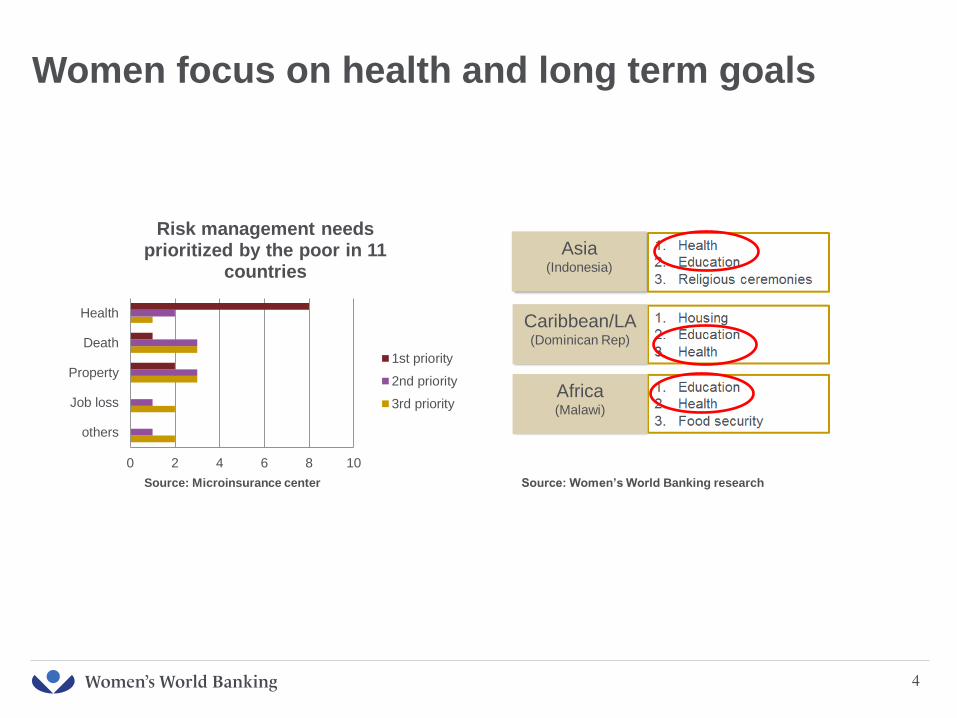

Women focus on health and long term goals

4

Source: Women’s World Banking research

Asia (Indonesia)

Caribbean/LA (Dominican Rep)

Africa (Malawi)

0 2 4 6 8 10

others

Job loss

Property

Death

Health

Risk management needs prioritized by the poor in 11

countries

1st priority

2nd priority

3rd priority

Source: Microinsurance center

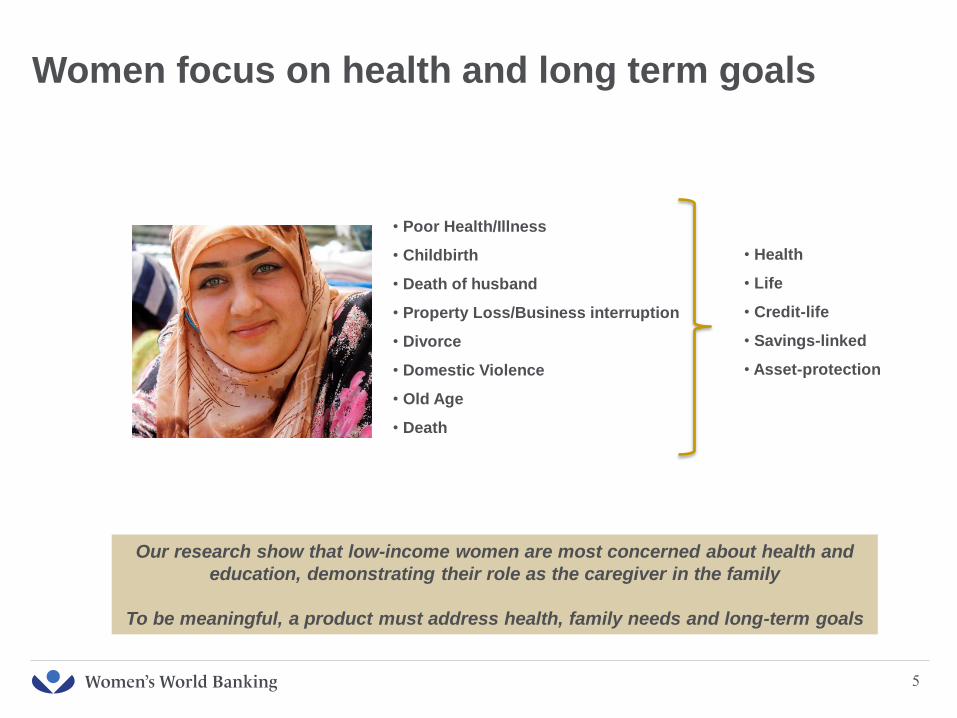

Women focus on health and long term goals

5

• Poor Health/Illness

• Childbirth

• Death of husband

• Property Loss/Business interruption

• Divorce

• Domestic Violence

• Old Age

• Death

• Health

• Life

• Credit-life

• Savings-linked

• Asset-protection

Our research show that low-income women are most concerned about health and

education, demonstrating their role as the caregiver in the family

To be meaningful, a product must address health, family needs and long-term goals

indicators

low-income populations

Gender research also made

us aware that women in

certain contexts face mobility

constraints and cannot easily

access bank branches

When we studied savings, we

learned that health is a major

area of women’s savings

and also coincides with their

role as caregivers

Gender research highlighted

women’s roles in the

household, including being

the savers and caregivers

Understanding Women’s Financial Needs

• This led us to research and develop women’s savings and insurance products

• This led us to research and develop micro-health insurance products for women

We also learned that women’s

asset building goals are for

the benefit of their families

• This led us to research and develop ways to use technology to deliver products to women

We also found that women need

health insurance not only for

their children, but for maternal

health issues

We also learned that women

value confidentiality and

convenience

6

Key customer insights

• Hospitalization due to delivery is the event that matters most to women

• Women prioritize the health of their family over their own health

• The family policy cannot exceed 5JD ($7) per month

Product Design

• Benefit at 15JD ($21.12) per day for up to 30 days, with max of 48 days in

policy period (increased from 10JD)

• No limitations for pregnancy coverage (original product had limitations)

• No exclusions (for pre-existing conditions)

• Premium at 1JD ($1.40) per month

• Mandatory enrollment for borrower only

• Voluntary coverage for spouse & full family added

Processes

• Simple claims form submitted with admission/discharge form to MFW branch

• In-house claims processing by MFW for < 6 nights hospital stay – client

receives payout faster

What is الرعاية (Ri’aya) – Caregiver?

7

Caregiver is a hospital cash product that pays a fixed per diem amount

Representing women’s roles as the caregivers of their families

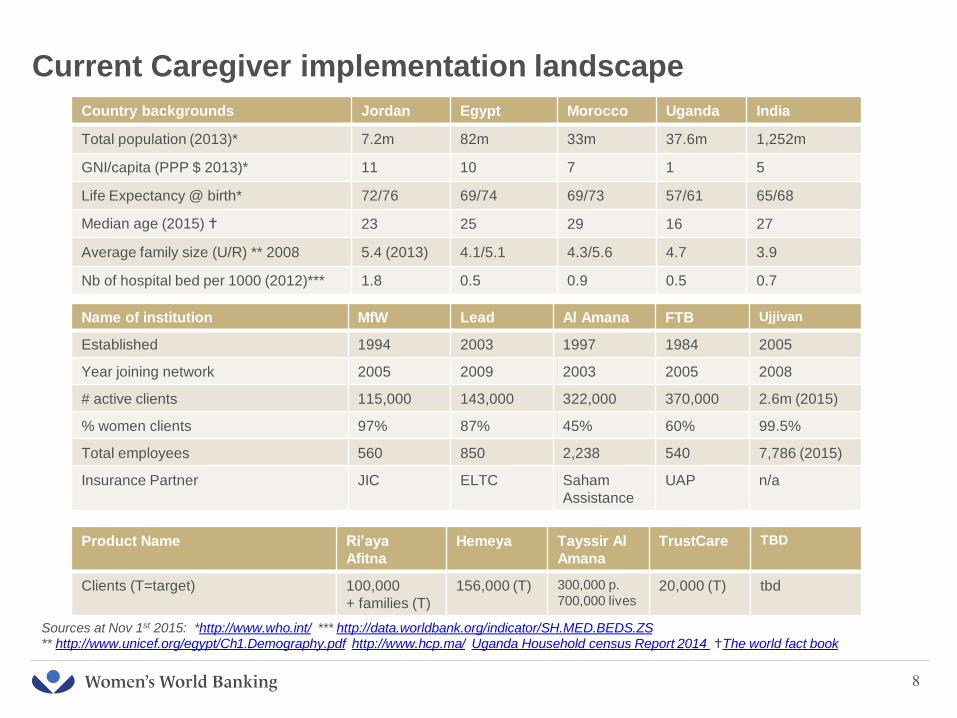

Current Caregiver implementation landscape

8

Country backgrounds Jordan Egypt Morocco Uganda India

Total population (2013)* 7.2m 82m 33m 37.6m 1,252m

GNI/capita (PPP $ 2013)* 11 10 7 1 5

Life Expectancy @ birth* 72/76 69/74 69/73 57/61 65/68

Median age (2015) 23 25 29 16 27

Average family size (U/R) ** 2008 5.4 (2013) 4.1/5.1 4.3/5.6 4.7 3.9

Nb of hospital bed per 1000 (2012)*** 1.8 0.5 0.9 0.5 0.7

Name of institution MfW Lead Al Amana FTB Ujjivan

Established 1994 2003 1997 1984 2005

Year joining network 2005 2009 2003 2005 2008

# active clients 115,000 143,000 322,000 370,000 2.6m (2015)

% women clients 97% 87% 45% 60% 99.5%

Total employees 560 850 2,238 540 7,786 (2015)

Insurance Partner JIC ELTC Saham

Assistance

UAP n/a

Product Name Ri’aya

Afitna

Hemeya Tayssir Al

Amana

TrustCare TBD

Clients (T=target) 100,000

+ families (T)

156,000 (T) 300,000 p.

700,000 lives 20,000 (T) tbd

Sources at Nov 1st 2015: *http://www.who.int/ *** http://data.worldbank.org/indicator/SH.MED.BEDS.ZS ** http://www.unicef.org/egypt/Ch1.Demography.pdf http://www.hcp.ma/ Uganda Household census Report 2014 The world fact book

9

What does it take to reach low-income women? Process model

Market understanding

Product design

Data / technical pricing

Client access / distribution

Risk bearing capacity

Regulatory Social impact

metrics

Investment for replication /

scaling

It is not enough to simply create a financial product;

clients must also know how to use it.

With which partners to team up?

10

What does it take to reach low-income women? Product development model

Target Group and Market assessment Institutional assessment

Premium

Benefits

Eligibility and Access

Insurance Partner

Product Marketing

Client education

Brand positioning

Policies and Procedures

Capacity building

IT/ MIS

Financials

Product Design Marketing and

Client Education Operating Model

With micro-insurance, low-income women can mitigate financial distress caused by

unexpected events affecting their family’s health. It can protect the first layer of assets they

have created as they move out of poverty.

We believe that Insurance products can be designed in a way that creates meaningful value

to clients and sustainable solutions to insurers.

11

Our insurance vision

Contact

12

Gilles Renouil || Director, Microinsurance

122 East 42nd Street, 42nd Floor, New York, NY 10168

Tel. 212.556.3148

Skype. gillesrenouil

www.womensworldbanking.org

Follow us @womensworldbnkg || facebook.com/womensworldbanking