with kevin urbatsch editor of special needs trusts: planning, drafting, and administration, co-chair...

TRANSCRIPT

With Kevin Urbatsch

Editor of Special Needs Trusts: Planning, Drafting, and Administration, Co-Chair of the 2009 ASNP National Meeting

January 29, 2009

Understanding Special Needs PlanningPart One:

Overview of Special Needs Planning and Public

Benefits

The Basics ofSpecial Needs PlanningPart 1 – Overview & Public Benefits

Kevin Urbatsch

Special Needs Planning AttorneySan Francisco, California

[email protected](415) 710-7886

Overview of Special Needs Planning

Section One:Summary of Special

Needs Planning

What is Special Needs Planning?

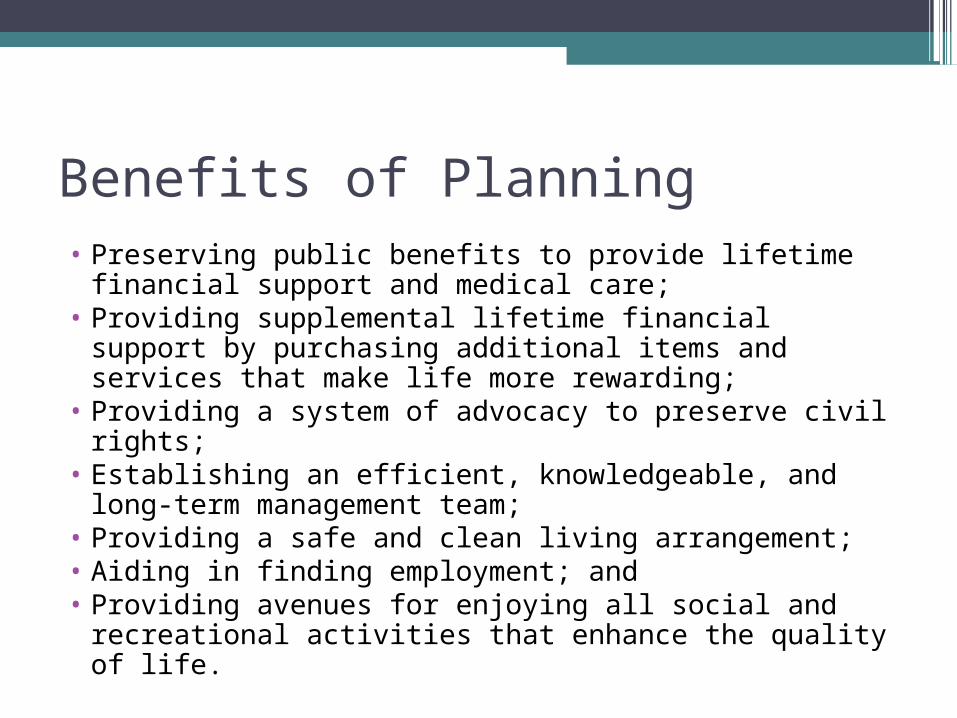

Benefits of Planning• Preserving public benefits to provide lifetime

financial support and medical care;• Providing supplemental lifetime financial support by

purchasing additional items and services that make life more rewarding;

• Providing a system of advocacy to preserve civil rights;

• Establishing an efficient, knowledgeable, and long-term management team;

• Providing a safe and clean living arrangement;• Aiding in finding employment; and• Providing avenues for enjoying all social and

recreational activities that enhance the quality of life.

Do All Persons with Disabilities Require Special Planning?•No! Persons with disabilities are each

unique and have different planning requirements Only those who are so severely disabled

that they meet the definition of disabled for public benefit programs require planning

Even if disabled and receiving public benefits only certain public benefit programs require planning

Defining Disability

•Someone could be substantially disabled in the commonly understood sense (e.g., if the person must use a wheelchair for mobility)

•However, that individual would not be considered disabled under public benefit rules if he or she holds a full-time job and earns a living wage

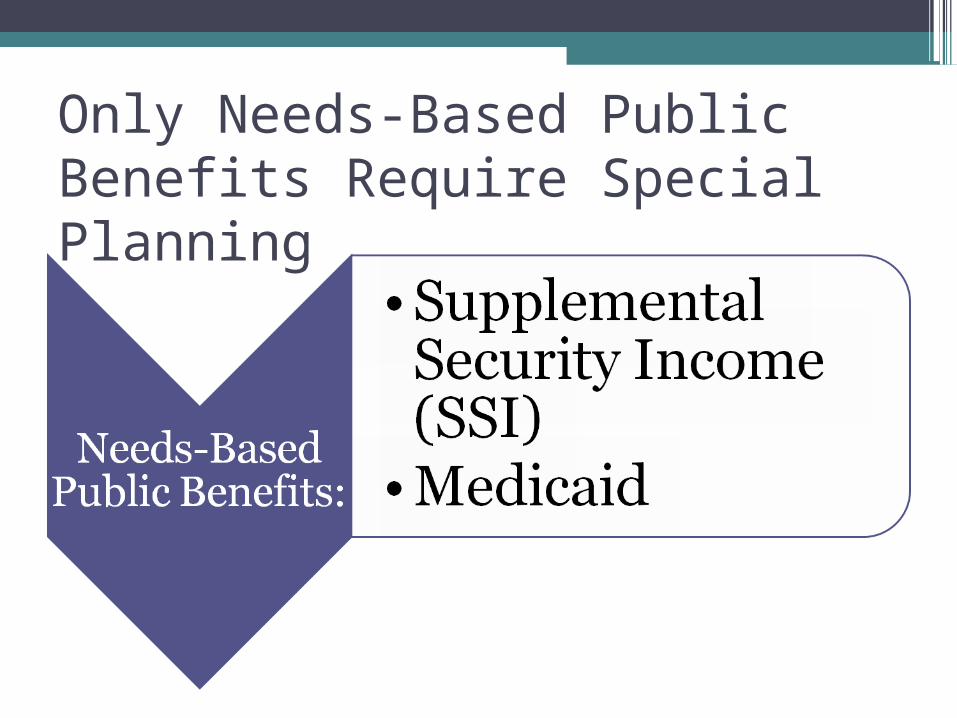

Only Needs-Based Public Benefits Require Special Planning

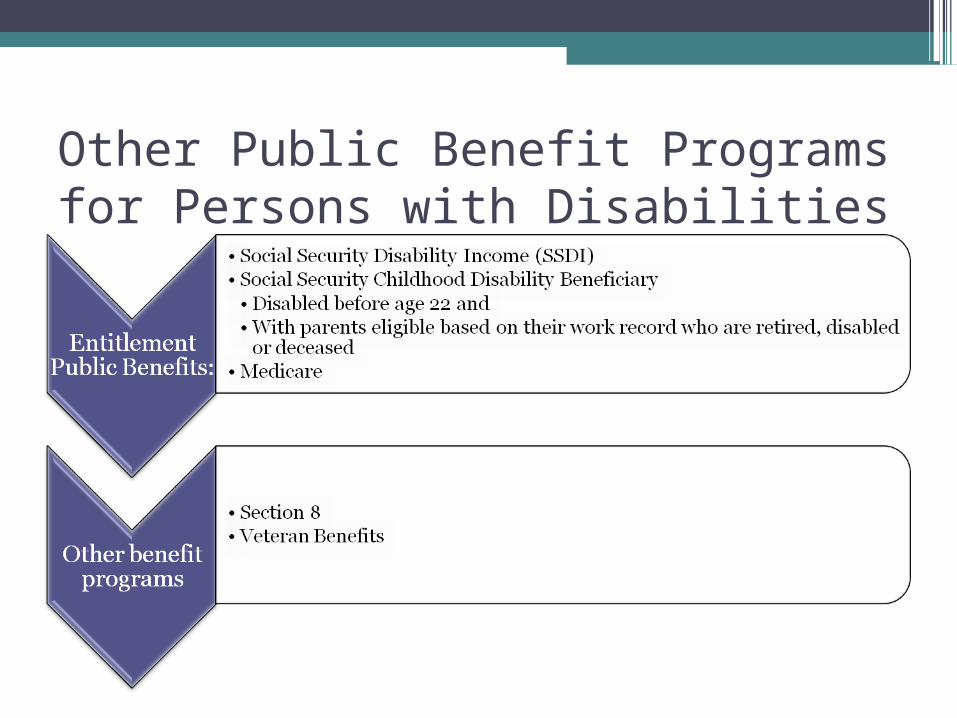

Other Public Benefit Programs for Persons with Disabilities

Dual Eligibles

Confusion of Public Benefit Programs Very Common•Often persons with disabilities, their families,

their attorneys, and others are confused about the public benefits received because: ▫Both SSI and SSDI are administered by the

Social Security Administration (SSA) and checks come from same place

▫Medicaid and Medicare are administered by the Centers for Medicaid and Medicare Services (CMS) and they are provided single card

Why “Special” Planning is Needed•If assets are in the name of a person with

a disability then would eliminate eligibility for SSI and Medicaid▫Counted as income in month of receipt▫Counted as resource first day of next

month•Loss of SSI generally acceptable, however

loss of Medicaid can be devastating

Private Paying for Medical Care

•Medical Costs are skyrocketing. For example, one coronary bypass operation in the Bay Area costs between $150,000-$330,000 or for an operation involving multiple trauma as if in an automobile accident costs between $175,000-$400,000 Prices from http://www.vimo.com/hospital/cost.php

•One trip to the emergency room could destroy a person with a disability’s inheritance if forced to privately pay for it

Special Needs Trusts

•The Special Needs Trust (SNT) is the primary tool when planning for a person with a disability

•There are various types of SNTs▫Third Party SNTs▫First Party SNTs

(d)(4)(A) SNTs or Payback SNTs Miller Trusts or Pooled SNTs or (d)(4)(C) SNTs

Special Needs Trusts

•The SNT holds title to assets owned by the needs-based public benefits recipient so that his or her eligibility is preserved

•Administration of an SNT can have an effect on eligibility if distributions are made without understanding public benefit rules

Overview of Special Needs Planning

Section Two:Public Benefit Programs for

Persons with Disabilities

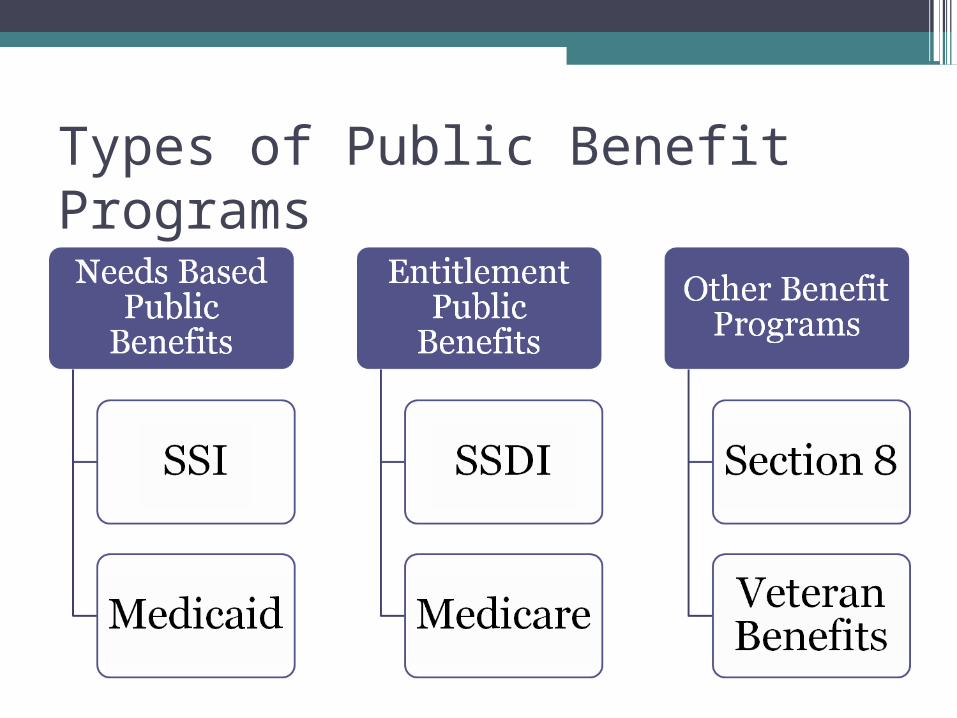

Types of Public Benefit Programs

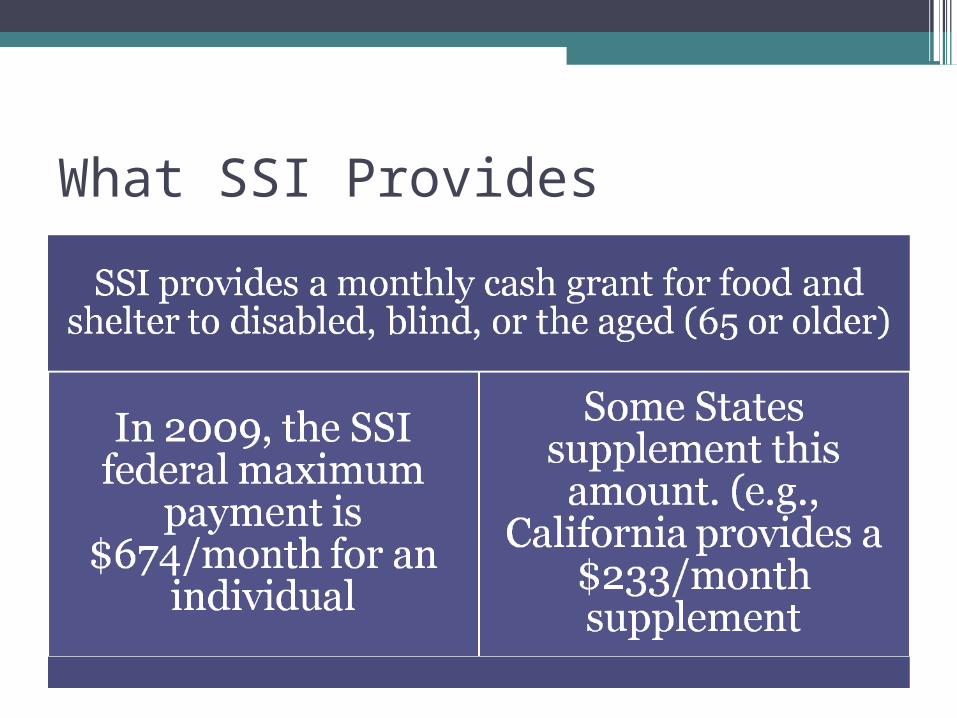

What SSI Provides

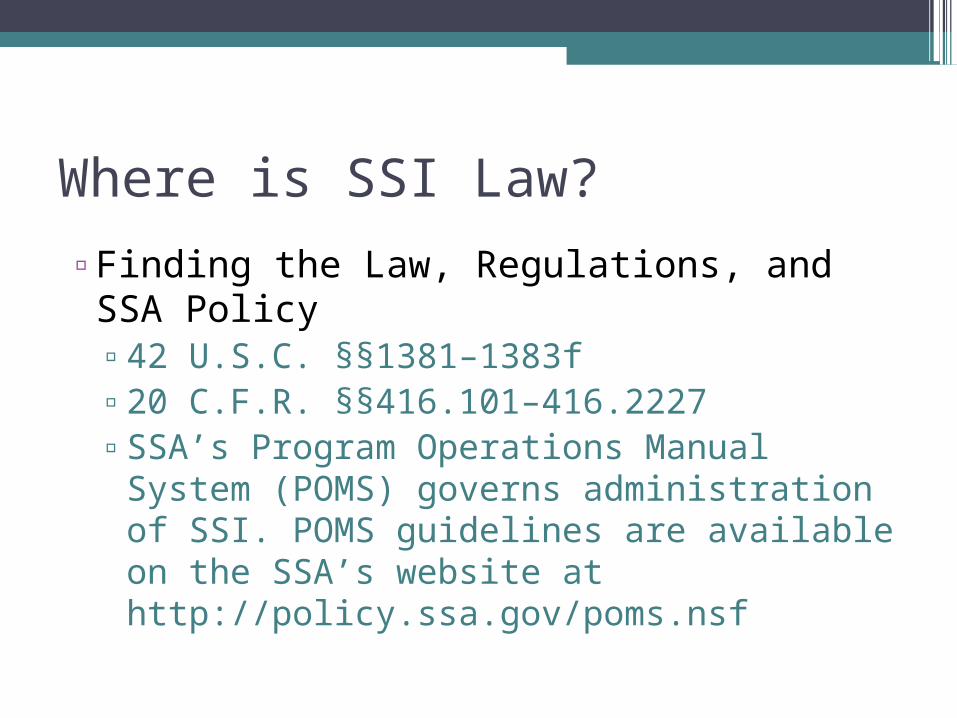

Where is SSI Law?

▫Finding the Law, Regulations, and SSA Policy▫42 U.S.C. §§1381–1383f ▫20 C.F.R. §§416.101–416.2227▫SSA’s Program Operations Manual System

(POMS) governs administration of SSI. POMS guidelines are available on the SSA’s website at http://policy.ssa.gov/poms.nsf

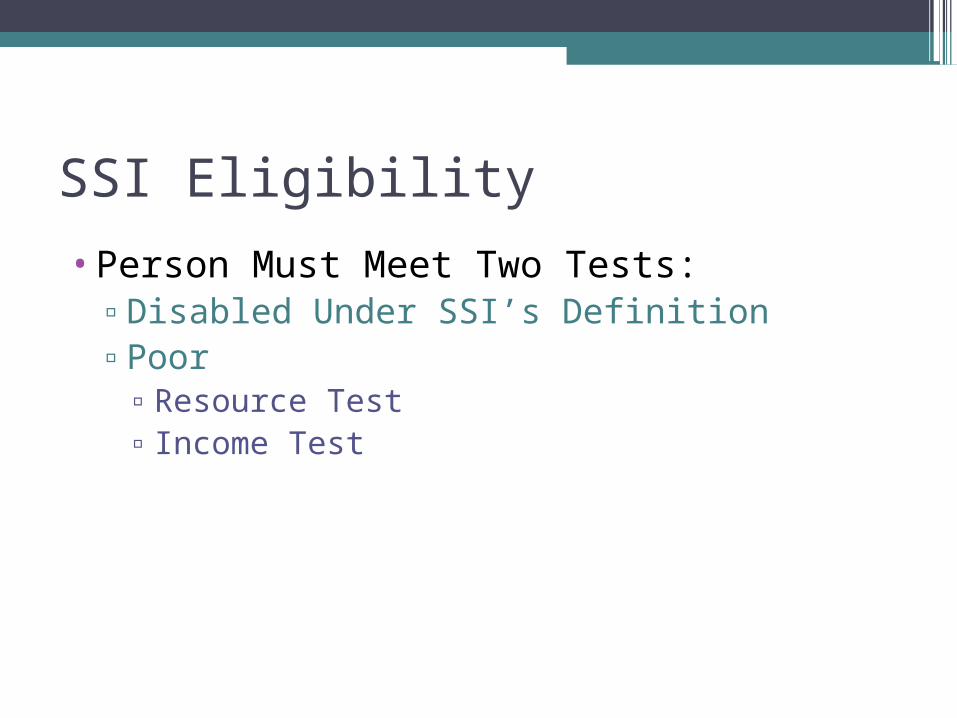

SSI Eligibility

•Person Must Meet Two Tests:▫Disabled Under SSI’s Definition▫Poor

▫Resource Test▫Income Test

SSI Definition of Disability

SSI Resource Test

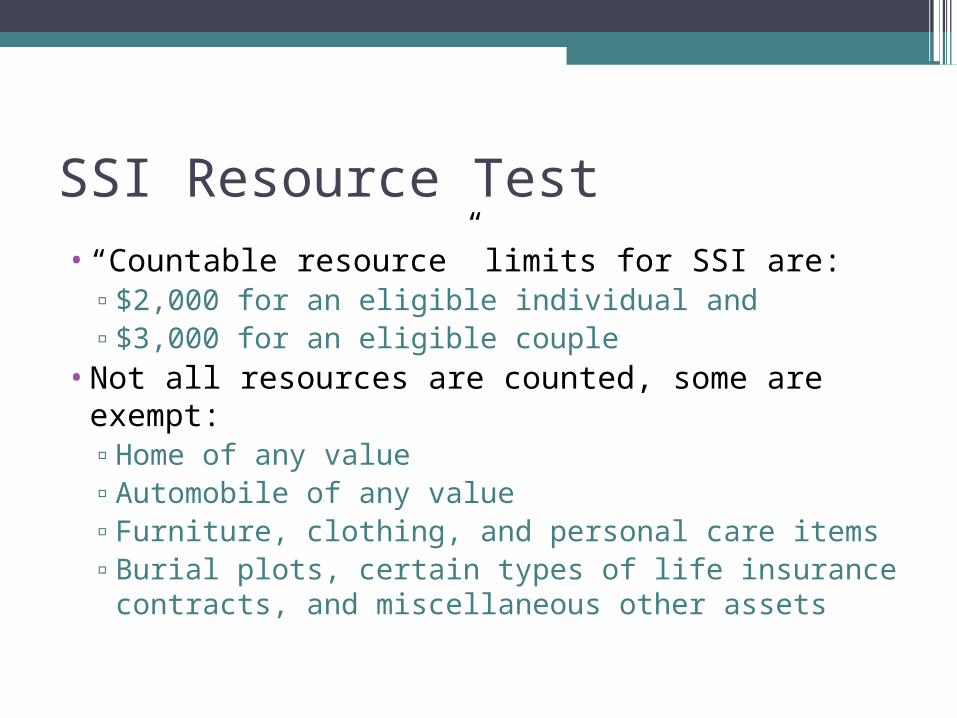

•“Countable resource” limits for SSI are:▫$2,000 for an eligible individual and ▫$3,000 for an eligible couple

•Not all resources are counted, some are exempt:▫Home of any value▫Automobile of any value▫Furniture, clothing, and personal care items▫Burial plots, certain types of life insurance

contracts, and miscellaneous other assets

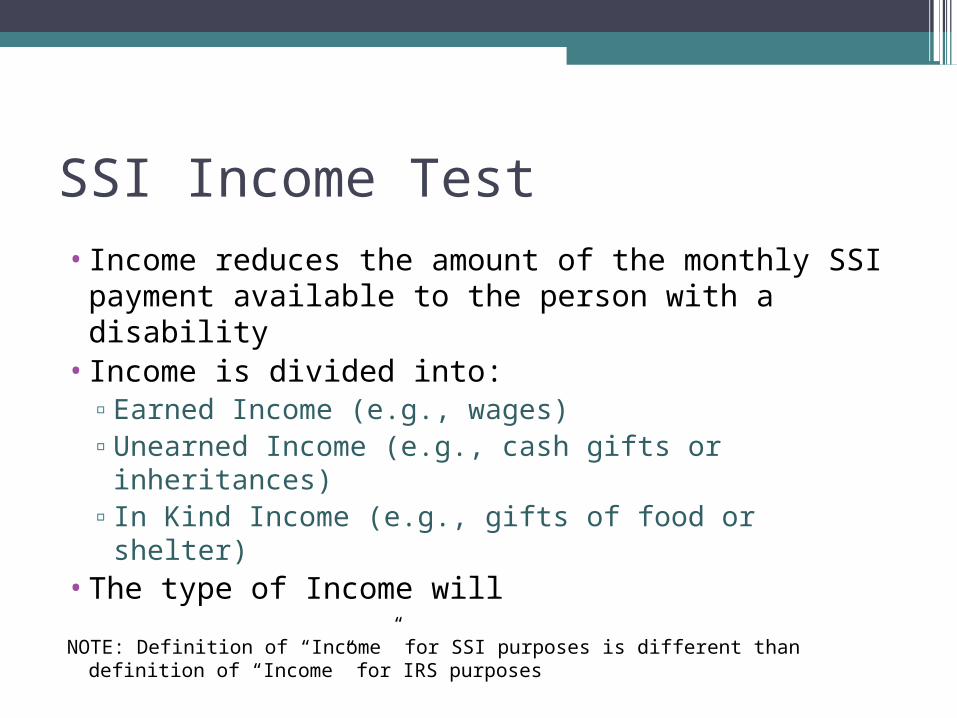

SSI Income Test• Income reduces the amount of the monthly SSI

payment available to the person with a disability

• Income is divided into:▫Earned Income (e.g., wages)▫Unearned Income (e.g., cash gifts or

inheritances) ▫In Kind Income (e.g., gifts of food or shelter)

•The type of Income will

NOTE: Definition of “Income” for SSI purposes is different than definition of “Income” for IRS purposes

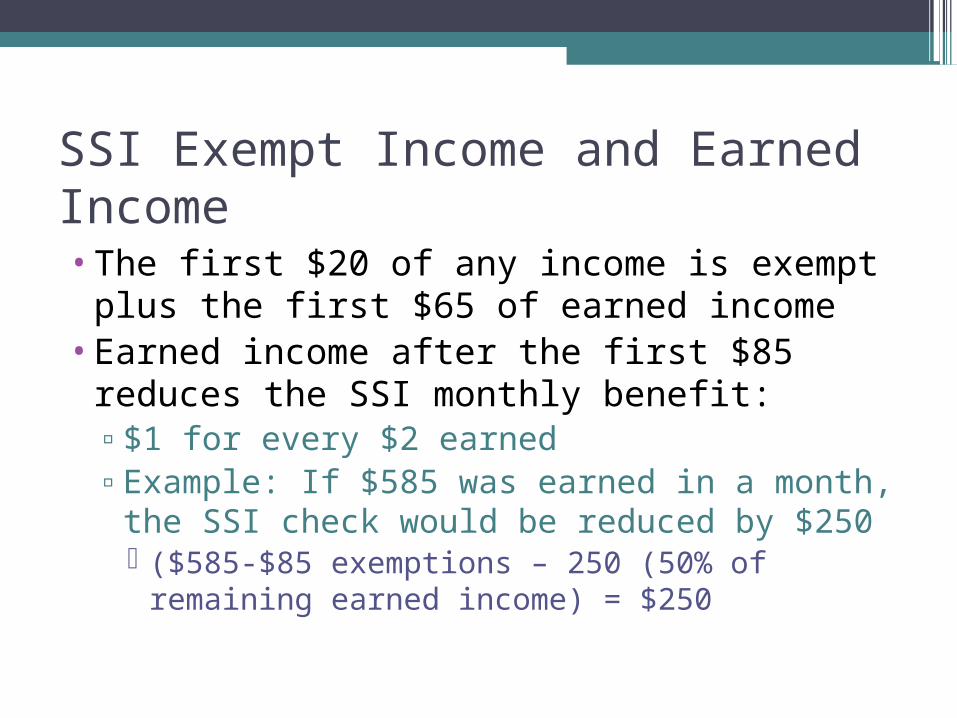

SSI Exempt Income and Earned Income•The first $20 of any income is exempt plus

the first $65 of earned income•Earned income after the first $85 reduces

the SSI monthly benefit:▫$1 for every $2 earned▫Example: If $585 was earned in a month,

the SSI check would be reduced by $250 ($585-$85 exemptions – 250 (50% of

remaining earned income) = $250

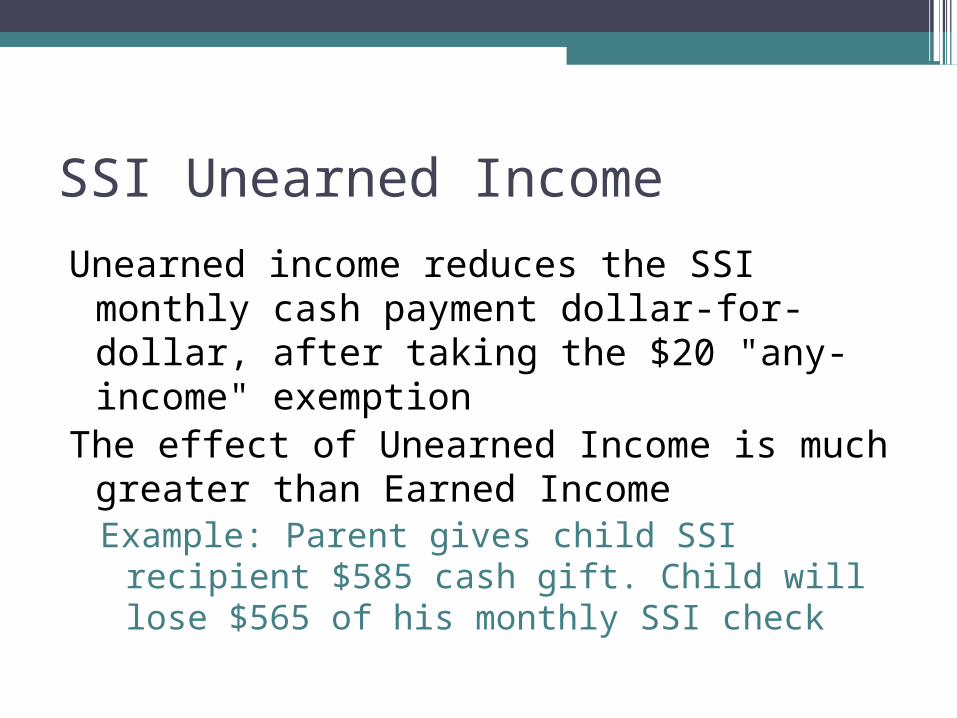

SSI Unearned Income

Unearned income reduces the SSI monthly cash payment dollar-for-dollar, after taking the $20 "any-income" exemption

The effect of Unearned Income is much greater than Earned IncomeExample: Parent gives child SSI recipient

$585 cash gift. Child will lose $565 of his monthly SSI check

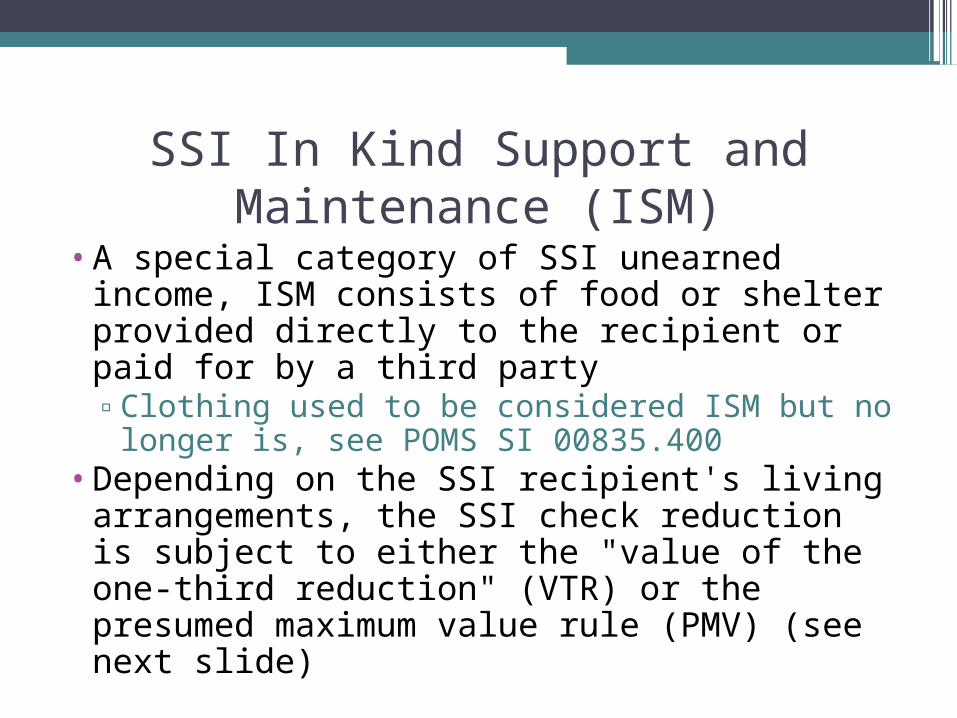

SSI In Kind Support and Maintenance (ISM)

•A special category of SSI unearned income, ISM consists of food or shelter provided directly to the recipient or paid for by a third party▫Clothing used to be considered ISM but no

longer is, see POMS SI 00835.400•Depending on the SSI recipient's living

arrangements, the SSI check reduction is subject to either the "value of the one-third reduction" (VTR) or the presumed maximum value rule (PMV) (see next slide)

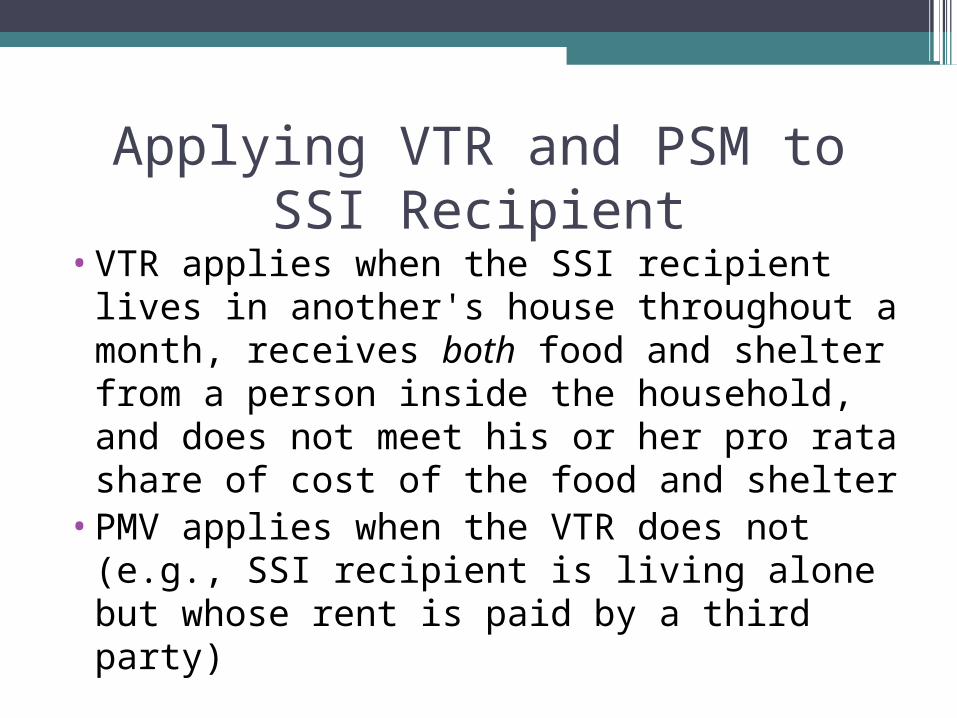

Applying VTR and PSM to SSI Recipient

•VTR applies when the SSI recipient lives in another's house throughout a month, receives both food and shelter from a person inside the household, and does not meet his or her pro rata share of cost of the food and shelter

•PMV applies when the VTR does not (e.g., SSI recipient is living alone but whose rent is paid by a third party)

Effect of VTR and PMV on SSI Recipient

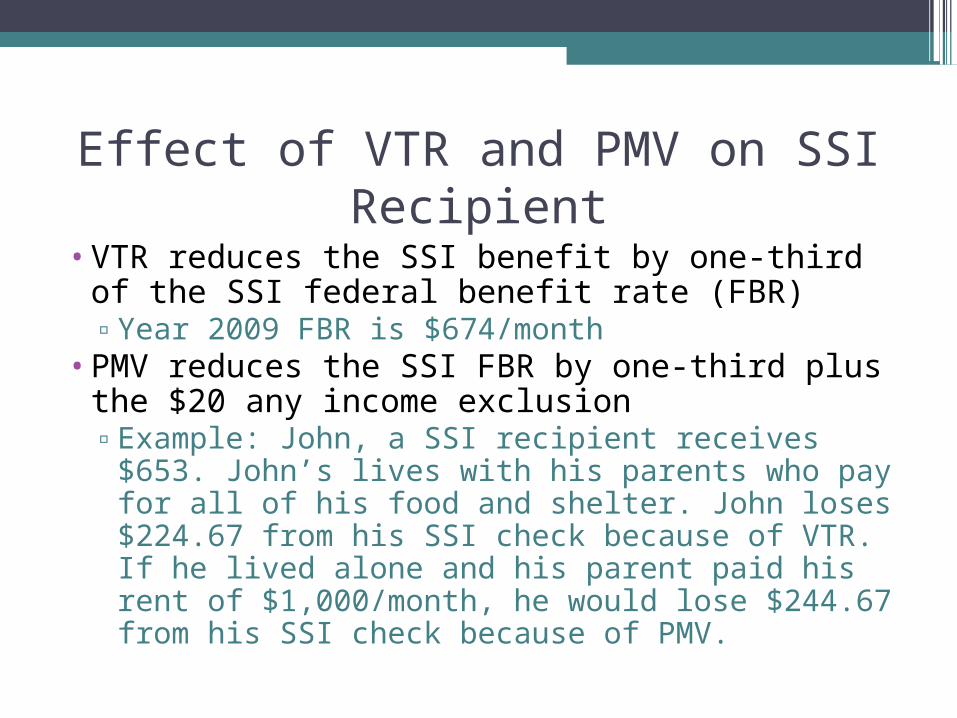

•VTR reduces the SSI benefit by one-third of the SSI federal benefit rate (FBR) ▫Year 2009 FBR is $674/month

•PMV reduces the SSI FBR by one-third plus the $20 any income exclusion▫Example: John, a SSI recipient receives $653.

John’s lives with his parents who pay for all of his food and shelter. John loses $224.67 from his SSI check because of VTR. If he lived alone and his parent paid his rent of $1,000/month, he would lose $244.67 from his SSI check because of PMV.

SSI Deeming of Income to Minor or Spouse

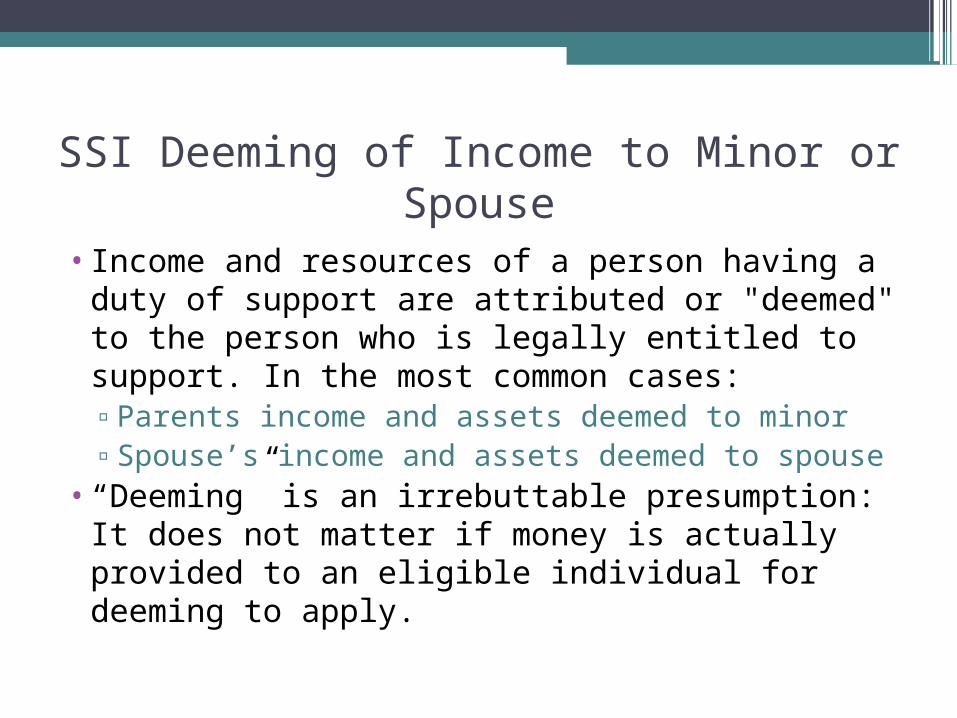

• Income and resources of a person having a duty of support are attributed or "deemed" to the person who is legally entitled to support. In the most common cases:▫Parents income and assets deemed to minor▫Spouse’s income and assets deemed to spouse

•“Deeming” is an irrebuttable presumption: It does not matter if money is actually provided to an eligible individual for deeming to apply.

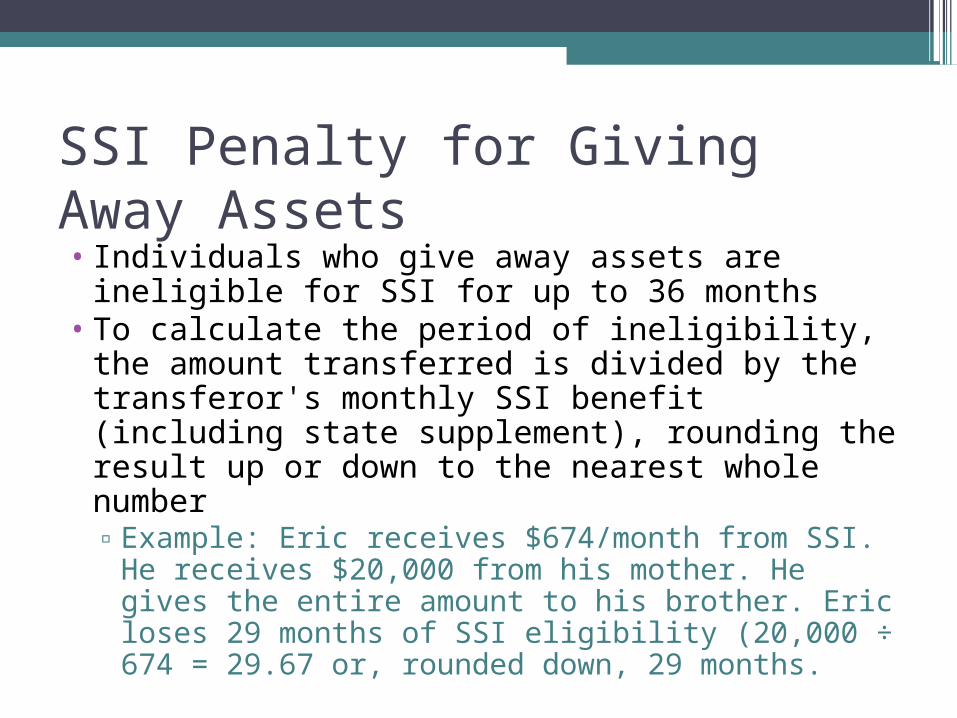

SSI Penalty for Giving Away Assets• Individuals who give away assets are

ineligible for SSI for up to 36 months• To calculate the period of ineligibility, the

amount transferred is divided by the transferor's monthly SSI benefit (including state supplement), rounding the result up or down to the nearest whole number▫Example: Eric receives $674/month from SSI.

He receives $20,000 from his mother. He gives the entire amount to his brother. Eric loses 29 months of SSI eligibility (20,000 ÷ 674 = 29.67 or, rounded down, 29 months.

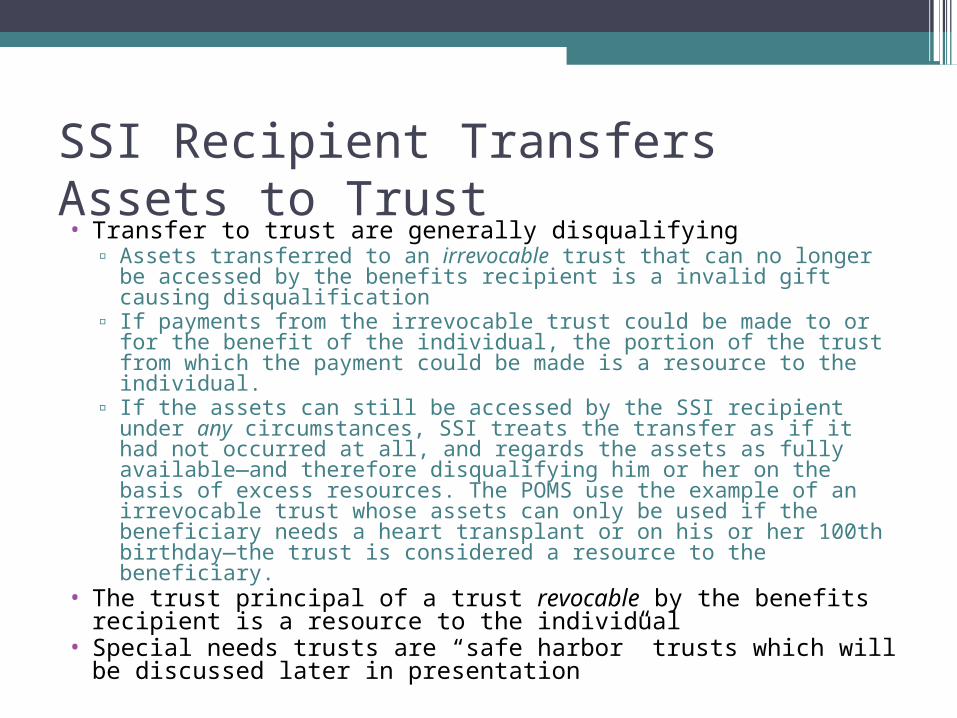

SSI Recipient Transfers Assets to Trust• Transfer to trust are generally disqualifying

▫ Assets transferred to an irrevocable trust that can no longer be accessed by the benefits recipient is a invalid gift causing disqualification

▫ If payments from the irrevocable trust could be made to or for the benefit of the individual, the portion of the trust from which the payment could be made is a resource to the individual.

▫ If the assets can still be accessed by the SSI recipient under any circumstances, SSI treats the transfer as if it had not occurred at all, and regards the assets as fully available—and therefore disqualifying him or her on the basis of excess resources. The POMS use the example of an irrevocable trust whose assets can only be used if the beneficiary needs a heart transplant or on his or her 100th birthday—the trust is considered a resource to the beneficiary.

• The trust principal of a trust revocable by the benefits recipient is a resource to the individual

• Special needs trusts are “safe harbor” trusts which will be discussed later in presentation

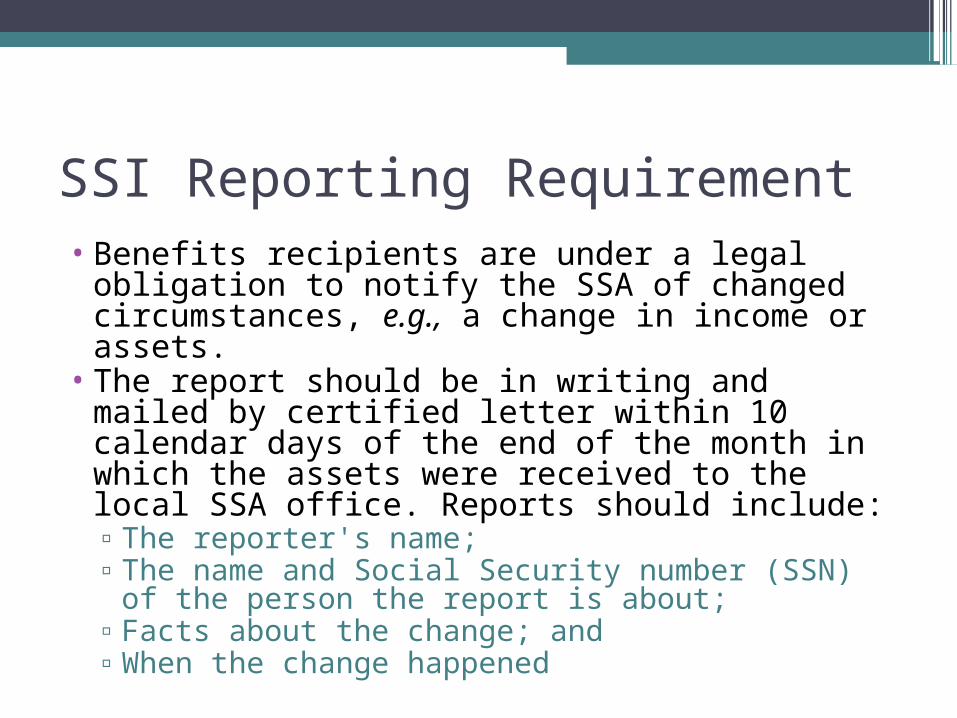

SSI Reporting Requirement• Benefits recipients are under a legal obligation

to notify the SSA of changed circumstances, e.g., a change in income or assets.

• The report should be in writing and mailed by certified letter within 10 calendar days of the end of the month in which the assets were received to the local SSA office. Reports should include:▫The reporter's name;▫The name and Social Security number (SSN) of

the person the report is about;▫Facts about the change; and▫When the change happened

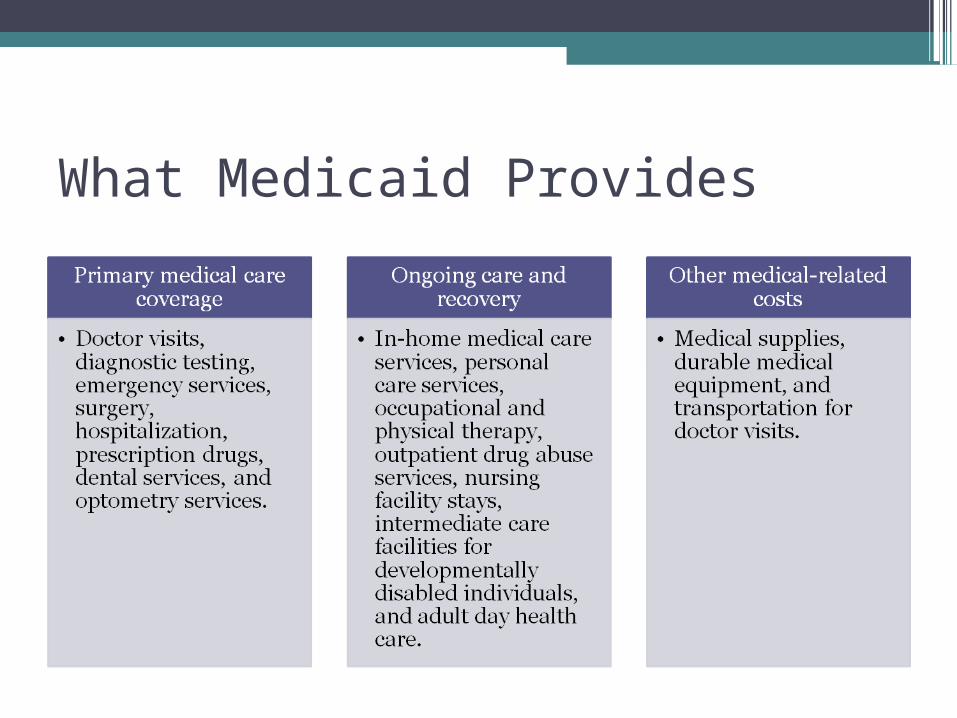

What Medicaid Provides

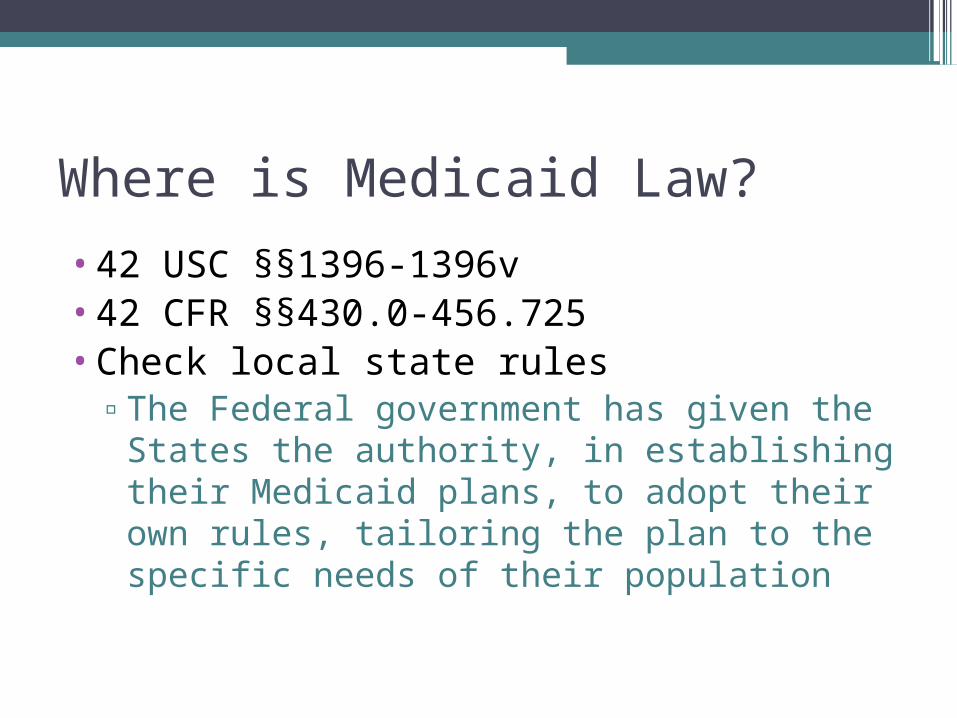

Where is Medicaid Law?

•42 USC §§1396-1396v•42 CFR §§430.0-456.725•Check local state rules

▫The Federal government has given the States the authority, in establishing their Medicaid plans, to adopt their own rules, tailoring the plan to the specific needs of their population

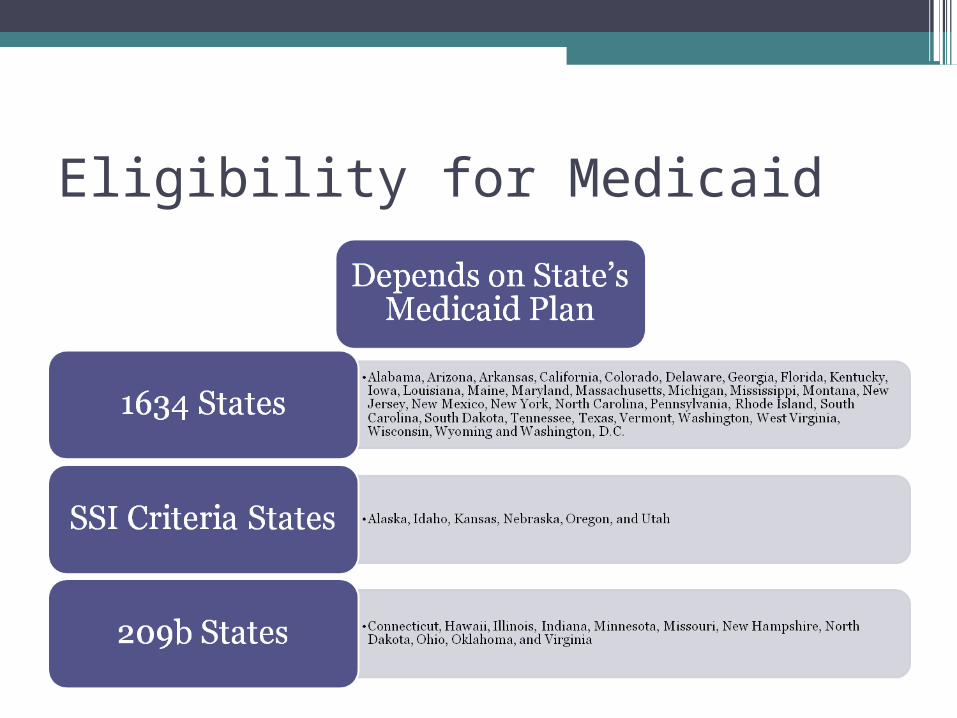

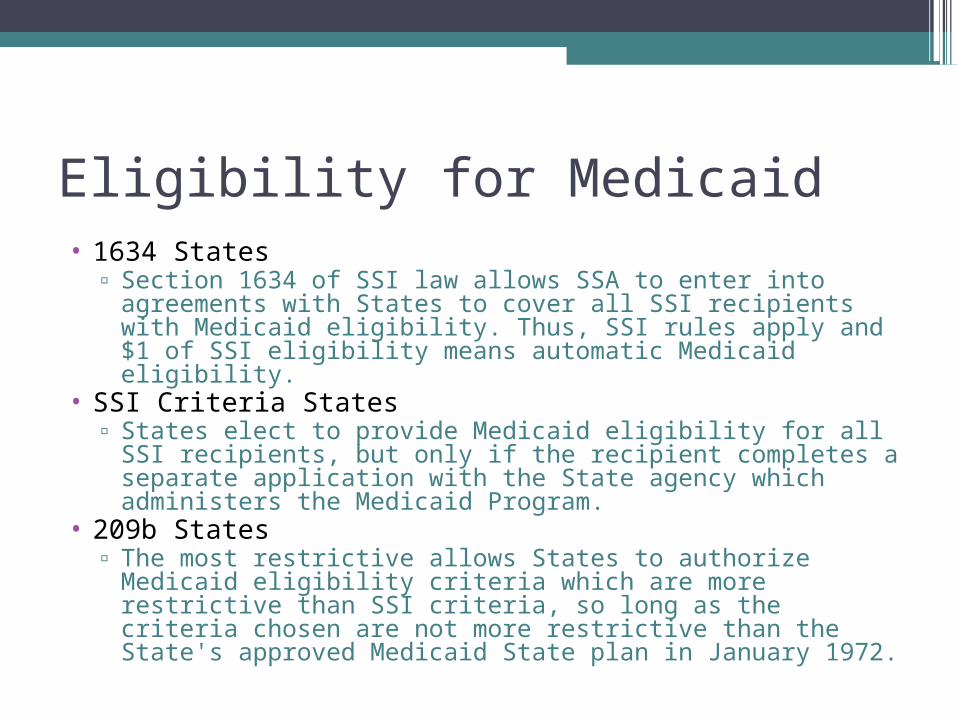

Eligibility for Medicaid

Eligibility for Medicaid• 1634 States

▫ Section 1634 of SSI law allows SSA to enter into agreements with States to cover all SSI recipients with Medicaid eligibility. Thus, SSI rules apply and $1 of SSI eligibility means automatic Medicaid eligibility.

• SSI Criteria States▫ States elect to provide Medicaid eligibility for all SSI

recipients, but only if the recipient completes a separate application with the State agency which administers the Medicaid Program.

• 209b States▫ The most restrictive allows States to authorize Medicaid

eligibility criteria which are more restrictive than SSI criteria, so long as the criteria chosen are not more restrictive than the State's approved Medicaid State plan in January 1972.

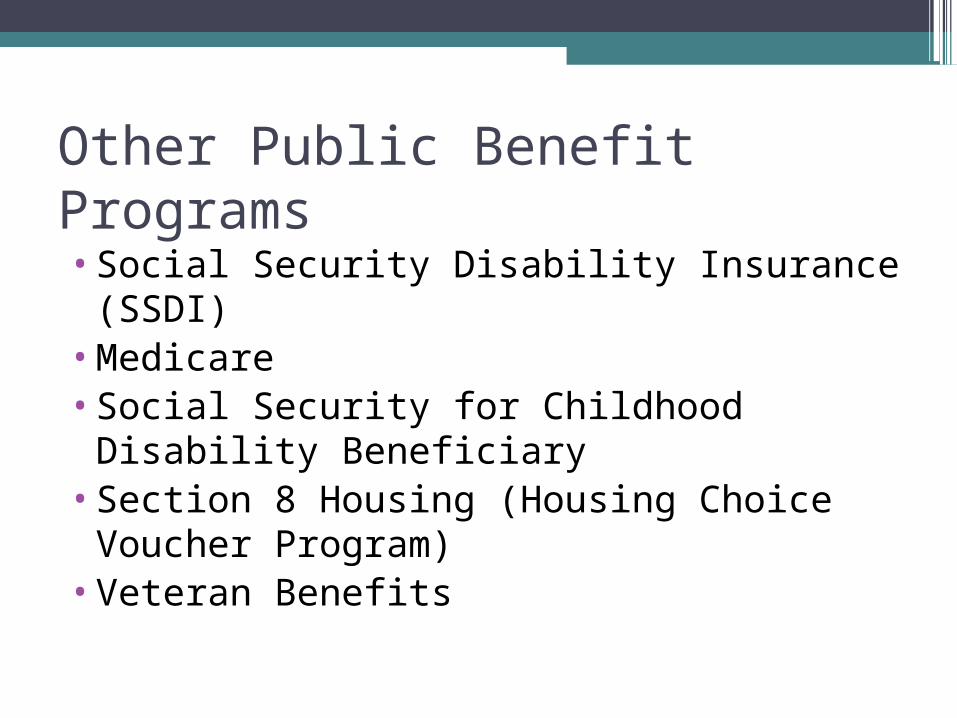

Other Public Benefit Programs

•Social Security Disability Insurance (SSDI)

•Medicare•Social Security for Childhood Disability

Beneficiary•Section 8 Housing (Housing Choice

Voucher Program)•Veteran Benefits

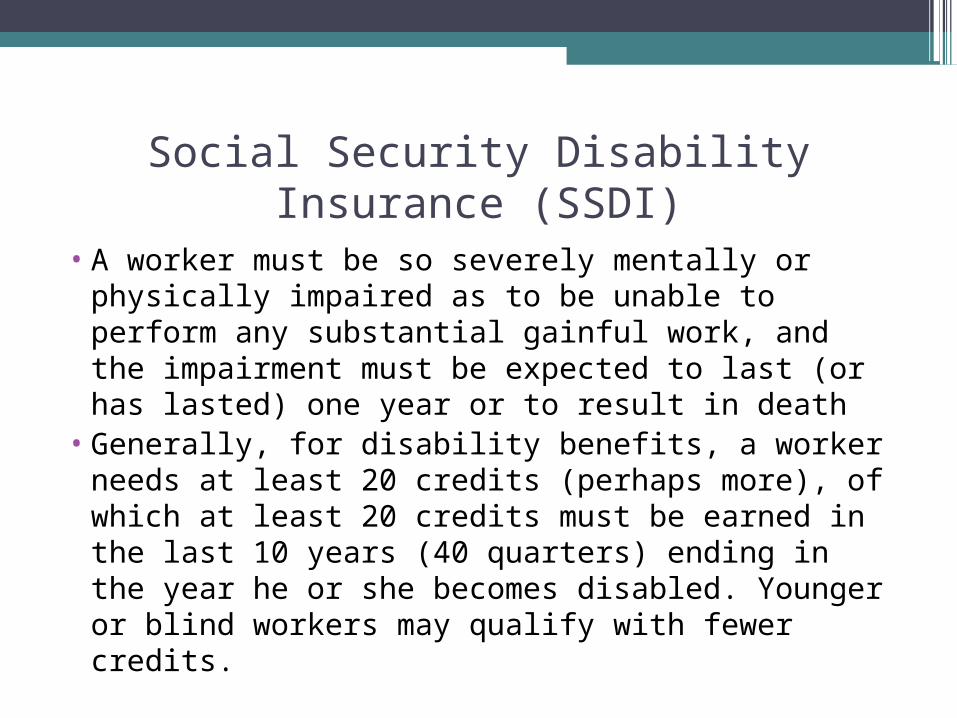

Social Security Disability Insurance (SSDI)

• A worker must be so severely mentally or physically impaired as to be unable to perform any substantial gainful work, and the impairment must be expected to last (or has lasted) one year or to result in death

• Generally, for disability benefits, a worker needs at least 20 credits (perhaps more), of which at least 20 credits must be earned in the last 10 years (40 quarters) ending in the year he or she becomes disabled. Younger or blind workers may qualify with fewer credits.

SSDI-Medicare Eligibility

A person with a disability is automatically eligible for Medicare if he or she has been receiving Social Security disability insurance or railroad retirement disability benefits for 24 months

Person with Disability May Have SSI, SSDI, Medicaid, and Medicare•Claimants may be eligible for concurrent

benefits under both SSDI and SSI, if the claimant's SSDI payments and other benefits do not exceed SSI income and asset limitations

•Claimant may also be eligible for health coverage such as Medicare, Medicaid, or private medical insurance coverage.

Social Security – Childhood Disability Beneficiary• The SSDI program pays benefits to adults

whose disability began before the age of 22.• This program is currently called the Childhood

Disability Beneficiary (CDB), formerly referred to as a Disabled Adult Child (DAC). The SSA considers this SSDI benefit as a "child's" benefit because it is paid on a parent's Social Security earnings record.

• The amount of the disabled adult child's monthly check is roughly 50 percent of the parent's monthly cash payment at retirement, and 75 percent at death.

Section 8 (Housing Choice Voucher Program)

•Section 8 programs are currently the primary vehicle for the federal government's participation in providing low-income housing to persons with disabilities

•Section 8 provides tenant based or project based assistance

•Eligibility for Section 8 is based on income•Persons with disabilities receive

accommodation•Special Needs Trusts are not designed to

assist with eligibility

Veteran Benefits

•Veterans with disabilities may receive benefits for:▫Service Connected Disabilities▫Non-Service Connected Disabilities

•Income and Resource limitations apply•Special Needs Trusts are not currently

recognized by the Veteran’s Administration

Conclusion of Public Benefits• Has this summary provided comprehensive

coverage of all public benefit programs for persons with disabilities? No.

• Public benefits laws are generally difficult to navigate because:▫The statutes, regulations, and policies are

difficult to find, are complex, and sometimes contradict each other;

▫Local program administrators cannot be relied on for authoritative advice; and

▫The law governing eligibility may change during the term of an SNT.

Special Needs Planning in the Era of Change:

New Opportunities for You and Your Clients

March 6-7, 2009Rancho Bernardo, CA

www.specialneedsplanners.com/conference2009

or call (866) 296-5509

The Urbatsch Law Firm

Special Needs Planning Attorney

101 Howard Street, Suite 490San Francisco, CA 94105

(415) 710-7886