will inr depreciation lead to homecoming of nri … real estate monitor - july 2013monthly real...

TRANSCRIPT

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

Will INR Depreciation Lead to Homecoming of NRI Real Estate Investors?Dubai is touted as the world-class property investment destination inthe Middle East. In 2012, real estate prices witnessed a 10% growth y-o-y, as per the Dubai Land Development (DLD) authority’s data.Also, the real estate transactions increased by 8% to AED 154 million. Interestingly, this recovery is backed by huge investments by expatriates, particularly from India as nonresident Indians (NRIs) are amongst the top five investors in the Middle East. However, with thenatural affinity towards home-biasness for India, and against the recent depreciation of the Indian rupee (INR) against the US dollar(USD), could the real estate investment decisions of the NRI community be changed in favour of India?

Indian real estate prices have increased dramatically over the last few years. Immediately following the global financial crisis (GFC),Indian property prices witnessed a significant rise averaging 40–42% across all major markets, as per the database of Real EstateIntelligence Services (REIS), Jones Lang LaSalle (refer to Figure 1). Even in cities like Mumbai, where capital values were already high,returns stood at 66% during the same period. Contrary to this,DLD’s data for Dubai suggests property prices witnessed a 65% slump in the four-year period before 2012, thereby enabling us to suspiciously ask whether a 10% rally in 2012 is all that startling.

Figure 1: Returns from Indian Residential Market

0%

10%

20%

30%

40%

50%

60%

70%

80%

Returns from Indian residential market in last four years

Capital Value % change during 2Q09-1Q13

Source: Real Estate Intelligence Services, Jones Lang LaSalle, India

More recently, INR has witnessed a significant 12% depreciation against USD since the start of May 2013 until the end of June 2013,thereby forcing its value down against all other currencies that are pegged to USD, including the UAE dirham (AED). As a consequence, INR has also depreciated against the AED by 12% during the same period.

A simple back-of-envelope calculation suggests that for instance, if a Dubai-based NRI invests AED 10 million in the Indian real estate now (INR/AED at 16.4), and assuming only a conservative 15% returns from the Indian real estate in the near term for key markets,he could expect repatriated returns of over 27% (15% of returns from real estate market plus 12% of currency appreciation),assuming that the INR returns to its pre-May mean of 14.8/AED (refer to diagram).

Merely the incremental return of 12%, owing to exchange rate fluctuation, is comparable to the 10–12% of total returns expected by DLD in the near term from the investment in Dubai real estate.Similar incremental returns can be expected from investments made by NRIs from other parts of the Middle East where the local currency is mostly pegged to USD (refer to Table-1).

Table-1: Incremental gains from INR exchange rateUAE (Dirhams) 12.5%Saudi Arabia (Rial) 12.4%Oman (Rial) 11.8%Kuwait* (Dinnar) 12.0%

*Partially pegged to the USD

Monthly Real Estate Monitor - July 2013

Pulse •Research Dynamics•2012

It could be argued that expat-Indians may be favouring Dubai over the Indian real estate on the basis of socio-economic and other factors. According to media sources, Indian investors were buying properties in Dubai as it offers relative political stability, world classinfrastructure, tax benefits, attractive prices and geographical proximity.

However, a recent survey conducted by Sumansa Exhibitions, the organiser of the Indian Property Show in UAE, portrays a different picture. The survey reveals that NRIs place a higher intrinsic value to property owned in India over that owned in Dubai or elsewhere. Apart from strict visa rules in the Middle East region along with certain regulatory obstacles in buying a property in the Emirates,critical triggers that could help sustain their interest in Indian property market include higher economic growth in India, improving infrastructure, renewed political focus on timelines for new infrastructure initiatives, rising demand for commercial space in the market (leading to job creation), social infrastructure and price trends. Putting these things into perspective, the recent fall of INR could potentially act as a trigger amongst the NRI community in the Middle East to switch their focus towards the properties back in India.

Figure 1: Financial Indicators Grade A Capital Value

Office Retail ResidentialDelhi NCR

Mumbai

Bangalore

Chennai

Pune

Hyderabad

Kolkata

Rental Value

Deal of the MonthJones Lang LaSalle’s Capital

Markets team has sold a 100% equity stake in the

holding firm of BlueRidge Special Economic Zone

(SEZ) Phase I in Punefor INR 4,500 million to IDFC

What’s New!!The Union Cabinet of India

cleared the Real Estate (Regulatory & Development)

Bill during the first week of June 2013. The bill aims to instill

transparency and maturity into the residential sector that has

been so far unregulated.

Green WallSurat is moving towards

becoming the first city in India to have a green building council (GBC) that would

ensure that the new buildings coming up will follow a green

building code.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

BangaloreBangalore office market saw improvement in transaction activity during June compared with the previous month. The combination of stable demand and restricted supply kept the city’s overall vacancy

rate low during the month. Interestingly, the IT/ITES sector accounted for the majority of leasing, with major companies taking up space in the quarter including Disney, Amazon, Honeywell, Synergy and TP Vision. The city witnessed the completion of Global Village Technology Park Phase III Tower 3, Kalyani Platina Oak, Kalyani Platina Crystal and Nagarjuna Garnet. Rents continued to remain stable across the city. However, capital values marginally appreciated because of improved demand and investor sentiments.

Bangalore’s retail market saw continued steady consumer demand in June. As a result, the vacancy in malls reduced marginally. In addition, the high streets continued to see modest absorption in the

month. Some of the major transactions in the city included leasing by Starke’s, FabIndia, McDonald’s, KFC and Pepe Jeans. Rents continued to remain stable over the month. Capital values also remain unchanged because of poor investor sentiments towards buying retail property.

Residential market saw modest absorption during June in Bangalore. The city also witnessed anincreased number of launches over the month, withthe notable ones including Prestige IVY Terraces by

Prestige Group, Sobha Santorini by Sobha Developers and DNR Atmosphere by DNR Corp. Rents remained stable over the month.However, capital values appreciated marginally across various submarkets because of increased sales volumes and marginal upsurge in price at most projects that are nearing completion.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftCBD 80-130 10,000-20,000Old Airport Road 60-75 7,000-10,000Outer Ring Road (East) 48-55 5,500-6,500Old Madras Road 45-60 5,000-6,500Electronic City 26-28 2,800-3,200

Retail Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftKoramangala 80–150 9,000–16,000Indiranagar 90–180 10,000–16,000New BEL Road 50–80 6,000–10,000Commercial Street 175–250 16,000–20,000Jayanagar 80–120 7,000–15,000

Residential Rents Capital Value

Key Precincts

INR per month for a 1,000 sq ft

two-BHK apartment INR per sq ft

Old Madras Road 15,000–25,000 5,000– 6,000Indiranagar 20,000–30,000 10,000–20,000Bellary Road 12,000–18,000 4,500–9,000Hosur Road 10,000–14,000 3,000–6,500Whitefield 18,000–25,000 4,500–8,000Tumkur Road 8,000–12,000 3,000–5,000Kanakapura Road 8,000–12,000 3,000–5,500Mysore Road 8,000–10,000 3,000–4,000

INFRASTRUCTURE ONGOING>> Having achieved considerable progress in Phase I and ready to execute Phase II of Namma Metro, Bangalore Metro Rail Corporation Ltd (BMRCL) is preparing to take up Phases II-Aand III. After completion, the proposed new network of 150 km will virtually throw a metro grid around Bangalore City besides connecting key points such as the Bengaluru International Airport, Hebbal and Magadi Road. After the completion of all the three phases, Bangalore will have a respectable 265 km of metro network. The state government’s high-power committee has already cleared a pre-feasibility study on the proposed network, said a BMRCL statement.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

ChennaiAfter a few months of slowdown, office leasing gained momentum during the month of June. The majority of supply in 2013 would be coming from the most preferred office locations of pre-toll Old

Mahabalipuram Road (OMR). Important to mention, the new office supplies such as Ramanujan IT City and SP Infocity are gaining steady demand from the occupiers. Apart from the OMR, SBD locations such as Guindy and Mount-Poonamallee Road (MPR) also witnessed healthy demand in June. Notable new occupiers in this submarket included Visionary RCM, Solartis and iGold Technologies. Average office rents in Chennai saw marginal increase on the back of improving demand.

The high streets of Chennai continued to witnesshealthy leasing activity with electronics showrooms such as Poorvika and Samsung, as well as several quick serving resturant brands that opened in June.

The city also witnessed the opening of Spencer’s hypermarket in Velachery. With the new malls operating with nearly full occupancy, retailers are chasing potential properties in the high street locations such as T Nagar, Adyar and Velachery, supporting the rental growth in the high streets.

Residential sales remained restricted in Chennai.However, the number of new launches improved during the month of June. Some of the prominent launches during the month were Prince Highlands in

Iyyapanthangal, Kgeyes Samyuktha in Madambakkam and VGN Dynasty in Melapakkam. In addition, Marutham Group launched two new projects near Tambaram and Casa Grande and added one more villa project named Avalon in Perumbakkam. Capital values and rents remained largely unaltered during the month.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftMount Road 60–90 9,000–15,000RK Salai 70–100 10,000–15,000Pre-toll OMR 40–62 5,000–6,500Post-toll OMR 25–35 3,500–5,000Guindy 40–60 6,000–9,000Ambattur 20–32 3,250–4,300

RetailRents

(High Streets) Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftT. Nagar 120–180 12,000–15,000Nungambakkam 130–150 13,000–16,000Velachery 80–120 10,000–12,000Pre-toll OMR 50–70 8,000–11,000Anna Nagar 110–140 11,000–13,000LB Road (Adyar) 110–130 10,500–13,500

Residential Rents Capital Value

Key Precincts

INR per month for a 1,000 sq ft

two-BHK apartment INR per sq ft

Adyar 20,000–30,000 11,000–17,000Medavakkam 7,000–14,000 3,600–5,250Tambaram 6,000–12,000 3,500–4,500Anna Nagar 15,000–25,000 9,000–14,000Porur 5,000–10,000 3,800–6,200Sholinganallur 9,000–12,000 4,250–5,800

INFRASTRUCTURE ONGOING>> Thirumazhisai, located along the Chennai-Bangalore Highway, will soon get a multistoreyed industrial estate at a cost of INR 200 million. In addition, the state government has also planned to create a land bank of 2,000 acres to promote the micro-industries in the state.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

DelhiThe demand for office space was showing signs of improvement in June with occupiers looking to close the transactions. The major transactions during the month included GroupM Media and Manpower

leasing space in Cyber City-Gurgaon, Samsung taking up space inNoida Expressway and SYSTRA renting space in the SBD. Unitech Infospace, Sec 48, Block 4 in Gurgaon (Sohna Road); Unitech Infospace, Gurgaon Phase II, Building Six on National Highway 8,Dundahera; and Ascendas OneHub Phase I commenced operationin June with moderate to low occupancy. Rents increased in DLF Cyber City, MG Road and Golf Course Road within the given range.However, capital values remained unaltered across all the submarkets.

The retail demand in Delhi was sluggish because of the constraints in the availability of good space.Retailers were mostly active with the pre-commitment of space in the upcoming malls that

would offer the promise of good location, design, branding and business potential. Some of the major transactions in June included Yauatcha and Burberry Brit both leasing space in Prime South, Starbucks renting space in Prime Others and Croma taking up space in the Noida suburbs. TDI Town Square Mall at Nehru Place Metro Station in Prime Others submarket commenced operation with high occupancy. On the contrary, I Mall in the Greater Noida suburbs started with moderate occupancy in June. Rents increased marginally in Prime South and Prime Others submarkets.Interestingly, capital values continued to remain stable throughout the city.

The residential demand witnessed signs of slowdown. Meanwhile, studio apartments performedwell because of the low ticket size being associated with it. Over the month, new launches were noted

only in Noida, Ghaziabad and Faridabad, while the prominent launches included ATS Pristine by ATS Infrastructure in Noida, Palm Resort by MR JKG in Ghaziabad and Aravali One by Maxheights Infrastructure in Faridabad. Rents remained stable in June. Meanwhile, capital values increased in growth corridors and the rise in values varies with projects.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftBarakhamba Road 170-400 28,000-35,000Jasola 110-170 17,000-21,000DLF Cybercity 75-78 NAMG Road 115-140 17,000-19,000Golf Course Road 85-98 12,500-15,000Sohna Road 47-55 6,500-8,000

Retail Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftSouth Delhi 180-300 24,000-32,000West and North Delhi 140-230 15,000-23,000Gurgaon-MG Road 140-270 17,500-23,000Rest of Gurgaon 60-100 8,000-14,000Noida 130-220 14,000-25,000Ghaziabad 90-150 10,500-16,000

Residential Rents Capital Value

Key Precincts

INR per month for a 1000 sq ft 2BHK

apartment INR per sq ftGolf Course Road 22,000-32,000 12,000-16,000Sohna Road 15,000-20,000 5,800-7,500Golf Course Extension Road 16,000-22,000 8,000-9,500NH 8 14,000-19,000 4,500-6,500Dwarka Expressway NA 5,500-7,500Noida-Greater Noida Expressway 12,000-14,000 4,000-6,100Noida City 12,000-14,500 4,700-6,000Indirapuram 10,000-12,000 4,200-5,000NH 24 7,000-9,000 2,400-3,200

INFRASTRUCTURE ONGOING>> The fate of the proposed metro link between the Noida City Centre and the Greater Noida Bodaki is still hanging in balance nearly after two years of its conception. With two industrial development authorities, Noida and Greater Noida are struggling to raise about INR 50 billion required to build the 29 km metro project. Important to mention that once built, this project would also be beneficial for the centres’ ambitious Delhi-Mumbai Industrial Corridor (DMIC) project.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

HyderabadLeasing volumes improved in June. Again most leases were focused on Hitec City where good quality leasable space is fast reducing. Leasing activity was more focussed in Hitec in June was

followed by CBD submarket. There were also a few leases closed in Gachibowli submarket. Interestingly, the Pocharam submarket again witnessed a marginal leasing activity as SDG Software leased space. Key transactions in June included Cytel, WHISHWORKS, Apps Associates, QSSI and PARAXEL leasing space at Hitec City, Adap.TV, NetElixir, Centrica and Metlife taking space in the CBD;and IL&FS and Biological E securing space in SBD. Salarpuria Cyber Park, which is almost fully occupied, commenced operations in June. There were many occupiers who vacated spaces either to consolidate or to relocate, increasing the overall vacancy in the city. Therefore, average market rents and capital values remained stableover the month.

Retailers continued to focus on leasing high street space for ready-to-move-in spaces while pre-committing spaces in the upcoming malls. Key transactions in June included Chhabra 555 and Axis

Bank leasing space in Banjara Hills; F Studio taking space at Nagarjuna Circle; and Pai Electronics, W, Khazana and Malabar Gold renting in Dilshuknagar. Pre-leasing continued in few upcoming malls. Rents and capital values remained stable over the month.

Residential sales remained stable in June. Newlaunches also remained stable over the month, withprojects including a villa project by Sri Srinivasa Constructions called Esmeralda Fortune in

Kondapur and an apartment project by PNR Infra called High Nest in Kukatpally. Rents and capital values continued to increasemarginally across all the submarkets as newly launched residential projects were sold at a price higher than the market average over the month.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftBegumpet 45–55 4,500–6,500

Banjara Hills 50–60 4,500–7,500Hitec City 36–42 4,000–5,200

Gachibowli 36–40 4,000–5,000Uppal 25–35 3,000–4,000

Shamshabad 20–25 3,000–4,000Retail Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftBanjara Hills 100–130 10,000–13,000Jubilee Hills 110–140 11,000–14,000

Secunderabad 80–100 8,000–10,000Hitec City 100–130 10,000–13,000Kukatpally 100–120 10,000–12,000

Dilshuknagar 100–120 10,000–12,000Residential Rents Capital Value

Key Precincts

INR per month for a 1,000 sq ft 2BHK

apartment INR per sq ftBanjara Hills 20,000–25,000 7,500–14,000Begumpet 12,000–16,000 4,000–5,500Kondapur 8,000–16,000 3,200–5,000Tellapur 6,000–12,000 2,800–3,500

Kukatpally 7,000–10,000 3,500–3,800Miyapur 5,000–8,000 2,400–3,500

INFRASTRUCTURE ONGOING>> Hyderabad Metro Rail (HMR) update in June: 28 traffic junctions will be involved in situ construction of girders to cover large spans which are more than 112 ft.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

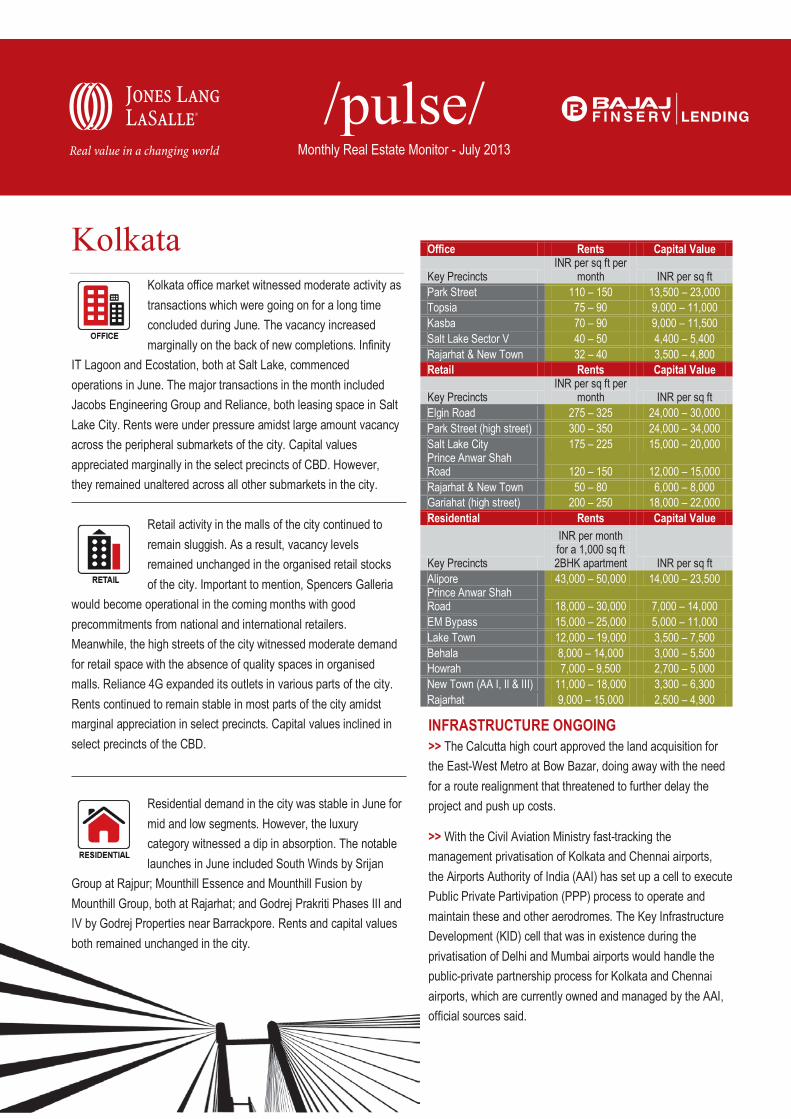

KolkataKolkata office market witnessed moderate activity as transactions which were going on for a long timeconcluded during June. The vacancy increased marginally on the back of new completions. Infinity

IT Lagoon and Ecostation, both at Salt Lake, commenced operations in June. The major transactions in the month included Jacobs Engineering Group and Reliance, both leasing space in Salt Lake City. Rents were under pressure amidst large amount vacancy across the peripheral submarkets of the city. Capital values appreciated marginally in the select precincts of CBD. However, they remained unaltered across all other submarkets in the city.

Retail activity in the malls of the city continued to remain sluggish. As a result, vacancy levelsremained unchanged in the organised retail stocks of the city. Important to mention, Spencers Galleria

would become operational in the coming months with good precommitments from national and international retailers.Meanwhile, the high streets of the city witnessed moderate demand for retail space with the absence of quality spaces in organised malls. Reliance 4G expanded its outlets in various parts of the city. Rents continued to remain stable in most parts of the city amidstmarginal appreciation in select precincts. Capital values inclined in select precincts of the CBD.

Residential demand in the city was stable in June for mid and low segments. However, the luxury category witnessed a dip in absorption. The notable launches in June included South Winds by Srijan

Group at Rajpur; Mounthill Essence and Mounthill Fusion by Mounthill Group, both at Rajarhat; and Godrej Prakriti Phases III andIV by Godrej Properties near Barrackpore. Rents and capital values both remained unchanged in the city.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftPark Street 110 – 150 13,500 – 23,000Topsia 75 – 90 9,000 – 11,000Kasba 70 – 90 9,000 – 11,500Salt Lake Sector V 40 – 50 4,400 – 5,400Rajarhat & New Town 32 – 40 3,500 – 4,800Retail Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftElgin Road 275 – 325 24,000 – 30,000Park Street (high street) 300 – 350 24,000 – 34,000Salt Lake City 175 – 225 15,000 – 20,000Prince Anwar Shah Road 120 – 150 12,000 – 15,000Rajarhat & New Town 50 – 80 6,000 – 8,000Gariahat (high street) 200 – 250 18,000 – 22,000Residential Rents Capital Value

Key Precincts

INR per month for a 1,000 sq ft 2BHK apartment INR per sq ft

Alipore 43,000 – 50,000 14,000 – 23,500Prince Anwar Shah Road 18,000 – 30,000 7,000 – 14,000EM Bypass 15,000 – 25,000 5,000 – 11,000Lake Town 12,000 – 19,000 3,500 – 7,500Behala 8,000 – 14,000 3,000 – 5,500Howrah 7,000 – 9,500 2,700 – 5,000New Town (AA I, II & III) 11,000 – 18,000 3,300 – 6,300Rajarhat 9,000 – 15,000 2,500 – 4,900

INFRASTRUCTURE ONGOING>> The Calcutta high court approved the land acquisition for the East-West Metro at Bow Bazar, doing away with the need for a route realignment that threatened to further delay the project and push up costs.

>> With the Civil Aviation Ministry fast-tracking the management privatisation of Kolkata and Chennai airports, the Airports Authority of India (AAI) has set up a cell to execute Public Private Partivipation (PPP) process to operate and maintain these and other aerodromes. The Key Infrastructure Development (KID) cell that was in existence during the privatisation of Delhi and Mumbai airports would handle the public-private partnership process for Kolkata and Chennai airports, which are currently owned and managed by the AAI, official sources said.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

MumbaiOffice leasing continued exhibiting improvement over the month of June. Projects in the advanced stage of construction recorded moderate pre-commitments. Companies were opting for consolidation and

relocation, over the expansion. Banking, financial services and insurance (BFSI) and IT industries remained the driving force behind the robust transactions in the month. Vacancy rates reduced minimally in June across select submarkets, except in the eastern suburbs. Important to mention, eastern suburbs submarket witnessed a few tenants relocating to relatively cheaper submarkets to avail lower cost advantage. Major transactions included Apple Inc leasing space in SBD Bandra Kurla Complex (BKC) and Tata AIA renting space in SBD Central. Kalpataru Prime at Thane submarket commenced operation in June. Rents and capital values in the western suburbs submarket rose slightly. However, other submarkets saw no change in either rents or capital values over the month.

Organised retailing continued to witness moderate demand over the month. Categories such as clothingand F&B remained to be the driving force behind demand generation. Interestingly, high street retail space in the suburbs, especially in Borivali and

Ghatkopar saw moderate transaction activities. A select pool of occupiers has started considering mixed-use project to open up the outlets. However, vacancy in the malls remained stable across the month. Major transactions in June included Cottonworld rentingspace at Oberoi Mall in the suburbs and Reliance Digital leasingspace at Viva City Mall in Thane. Meanwhile, Viva City Mall commenced operation in the month with healthy pre-commitment levels. It houses high-profile tenants from all the retail categories.Rents and capital values in the submarkets, such as the Prime North and the suburbs, increased marginally.

In June, the residential sector in Mumbai witnessed sluggish demand primarily because of significant increase in prices. Hence, most of the projects that were launched during the month saw smaller

configurations to improve the offtake in sales. New launches

included Acme Boulevard in Andheri by Acme Group, Bougainvillea in Kalina and Happy Homes in Vile Parle by Richa Realtors. Rents continued to remain stagnant during the month. In addition, capital values remained stable as the sales activity witnessed a slowdown with the start of the monsoon season.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftLower Parel 155–185 19,000–23,000BKC 260–360 25,000–35,000Andheri 100–150 9,000–15,000Goregaon-Malad 80–105 8,000–10,000Wagle Estate 50–65 5,000–6,000Thane-Belapur Road 45–60 5,100–6,000

RetailRents

(mall space) Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftLower Parel 260–380 22,000–32,000Malad 160–250 12,500–20,000Ghatkopar 140–225 10,100–18,000

Mulund 125–200 10,000–16,000

Thane 100–170 8,000–14,000Navi Mumbai 75–150 7,000–12,000Residential Rents Capital Value

Key PrecinctsINR per month for a

1,000 sq ft 2BHK apartment

INR per sq ft

Lower Parel 87,000–95,000 24,000–35,000

Wadala 40,000–55,000 14,500–19,100

Andheri 35,000–50,000 11,500–21,000Ghatkopar 35,000–48,000 9,500–15,000Ghodbunder Road 12,000–21,000 5,500–9,000

Kharghar 12,000–20,000 4,800–8,000

INFRASTRUCTURE ONGOING>> A signal-free drive between Chembur and South Mumbai was made possible as 14 km of the long-awaited Eastern Freeway was opened to traffic. The traffic police would have little supervision overthe 17 km long bridge (3 km to be opened in December 2013) and the freeway’s feeder and arrival routes, include roads leading to themain entrance and exit points.

Monthly Real Estate Monitor - July 2013Monthly Real Estate Monitor – July 2013

PuneThe office leasing activity in Pune increased in June,decreasing the vacancy levels marginally. Major transactions over the month included LSI Logic leasing space in Yerwada, Bajaj Finance renting

space in Viman Nagar and Amdocs taking up space in Hadapsar.The IITP Phase I located in Hinjewadi is likely to be operational in the next two—three months with good pre-commitments. Rents and capital values rose marginally in select submarkets, such as Kharadi and Hadapsar, both of which witnessed very low vacancy in most of the buildings. However, both rents and capital values remained unchanged in other parts of the city.

Leasing activity continued to be sluggish in the malls in Pune. The city’s organised retail stock also remained unchanged on the back of absence of new completions. Rents and capital values both were

stable during the month of June. It is noteworthy to mention, Season's Mall in Hadapsar and Prime Mall in Pimpri would likely to be operational by 2H13.

Demand for residential units in Pune continued to bestable in June. Major launches during the monthincluded Kumar Pinakin by KUL Group in Baner and Ayaan by Gandhi Bafna Constructions in Wagholi.

Rents and capital values both remained stable during the month of June.

Office Rents Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftHinjewadi 34–40 4,000–5,500Hadapsar 40–50 5,000–6,000Bund Garden Road 60–70 6,500–7,500Viman Nagar 50–60 6,000–7,000SB Road 55–75 6,500–7,500Koregaon Park 60–70 6,500–7,500

RetailRents

(High Streets) Capital Value

Key PrecinctsINR per sq ft per

month INR per sq ftMG Road 100–150 10,000–15,000Bund Garden Road 90–130 9,000–13,000FC Road 100–150 10,000–15,000JM Road 100–150 10,000–15,000DP Road 90–130 9,000–11,000SB Road 80–130 8,000–11,000

Residential Rents Capital Value

Key Precincts

INR per month for a 1,000 sq ft two-BHK apartment INR per sq ft

Wakad 10,000–12,000 4,500–5,500Kharadi 11,000–15,000 4,800–5,800Hadapsar 12,000–16,000 5,000–6,000Hinjewadi 9,000–11,000 4.000–5,500Undri 9,000–12,000 3,800–4,800Pimpri-Chinchwad 8,000–12,000 4,000–5,000

INFRASTRUCTURE ONGOING>> The civic administration of Pimpri Chinchwad Municipal Corporation (PCMC) would start major construction works from November onwards, while ward-level projects would begin from October onwards. The implementation of small development works in wards, such as laying drainage lines, laying footpaths and tarring of internal roads, has not started yet, despite the PCMC making budgetary provision for it.

Monthly Real Estate Monitor - July 2013

About Jones Lang LaSalleJones Lang LaSalle (NYSE:JLL) is a financial and professional services firm specializing in real estate. The firm offers integrated services delivered by expertteams worldwide to clients seeking increased value by owning, occupying or investing in real estate. With 2011 global revenue of $3.6 billion, Jones LangLaSalle serves clients in 70 countries from more than 1,000 locations worldwide, including 200 corporate offices. The firm is an industry leader in property andcorporate facility management services, with a portfolio of approximately 2.1 billion square feet worldwide. LaSalle Investment Management, the company’sinvestment management business, is one of the world’s largest and most diverse in real estate with $47 billion of assets under management.Jones Lang LaSalle has over 50 years of experience in Asia Pacific, with over 22,200 employees operating in 79 offices in 14 countries across theregion. The firm was named the Best Property Consultancy in Asia Pacific at ‘The Asia Pacific Property Awards 2012 in association with BloombergTelevision’. For further information, please visit our website, www.ap.joneslanglasalle.com

About Jones Lang LaSalle IndiaJones Lang LaSalle is India’s premier and largest professional services firm specializing in real estate. With an extensive geographic footprint across elevencities (Ahmedabad, Delhi, Mumbai, Bangalore, Pune, Chennai, Hyderabad, Kolkata, Kochi, Chandigarh and Coimbatore) and a staff strength of over 5400,the firm provides investors, developers, local corporates and multinational companies with a comprehensive range of services including research, analytics,consultancy, transactions, project and developmentservices, integrated facility management, property and asset management, sustainability, Industrial, capital markets, residential, hotels, health care,senior living, education and retail advisory. For further information, please visit www.joneslanglasalle.co.in

For more information about our research

Ashutosh Limaye Trivita RoyHead, Research and REIS Assistant Vice President, [email protected] [email protected]+91 98211 07054 +91 40 4040 9100 About Bajaj Finserv LendingBajaj Finserv Lending is one of the most diversified NBFCs in the Indian market catering to more than 5 million customers across the country. Headquartered in Pune, the company’s product offering includes Consumer Durable Loans, Personal Loans, Loan against Property, Small Business Loans, Home loans, Credit Cards, Two-wheeler and Three-wheeler Loans, Construction Equipment Loans, Loan against Securities and the recently introduced Lifestyle Finance. Bajaj Finserv Lending prides itself for holding the highest credit rating of FAAA/Stable for any NBFC in the country today.

To know more please visit www.bajajfinservlending.in or send an email to [email protected]

Research Dynamics 2013Pulse reports from Jones Lang LaSalle are frequent updates on real estate market dynamics.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent ofJones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.