whole audit note.docx

TRANSCRIPT

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 1/34

Test of controls: Income cycles:

The sales system:

Control Objectives

1. Ordering and granting of credit

a. Goods & services are only supplied to customers with good credit ratings.

b. Customers are encouraged to pay promptly.

c. Orders are recorded correctly.

d. Orders are fulfilled

2. Dispatch and Invoicing

a. All dispatches of goods are recorded.

b. All goods and services sold are correctly invoiced.

c. All invoices raised relate to goods and services that have been supplied by the

business.

d. Credit notes are only given for valid reasons.

3. Recording, accounting and credit control

a. All sales that have been invoiced are recorded in the general and sales ledger.

b. All credit notes that have been issued are recorded in the general ledger & sales

ledger.

c. All entries in the sales ledger are made to the correct sales ledger account.

d. Potentially doubtful debts are identified.

Control Activities

Ordering and credit control process:

1. Segregation of duties

a. Credit control, invoicing and inventory dispatch.

2. Authorization of credit terms to customers

a. References/credit check obtained.b. Authorization by senior staff.

c. Regular review.

3. Authorization for changes in customer data

a. Change of address supported by letterhead.

b. Requests for deletion supported by evidence balances cleared/ customer in liquidation.

4. Orders only accepted from customers who have no credit problems

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 2/34

5. Sequential numbering of blank order documents

6. Matching of customer orders with production orders & dispatch notes

Dispatches and Invoice preparation:

1. Authorization of dispatch of goodsa. Dispatch only on sales order.

b. Dispatch only to authorized customers.

c. Special authorization of dispatch of goods free of charge or on special terms.

2. Examination of goods outwards as to quantity, quality and condition

3. Recording of goods outwards

4. Agreement of goods outwards to customer records, dispatch notes and invoices

5. Pre numbering of dispatch notes and delivery notes and regular checks on sequences

6. Conditions of returns checked

7. Recording of goods returned on goods returned notes8. Signature of delivery notes by customers

9. Preparation of invoices and credit notes

a. Authorization of selling prices/ use of price lists.

b. Authorization of credit notes.

c. Checks on prices, quantities, extensions and totals on invoices and credit notes.

d. Sequential numbering of blank invoices and credit notes, and regular test on

sequence.

10. Inventory records updated

11. Matching of sales invoices with dispatch, delivery notes and sales orders.

Accounting and records:

1. Segregation of duties

a. Recording sales.

b. Maintaining customer accounts.

c. Preparing statements of accounts.

2. Recording of sales invoices sequence and control over spoilt invoices

3. Matching of cash receipts with invoices

4. Retention of customer remittance advices

5. Separate recording of sales returns, price adjustments etc.

6. Regular preparation of receivables statements

7. Authorization of writing off bad debts

8. Reconciliation of sales ledger control account

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 3/34

9. Analytical review of sales ledger and profit margins

Test of Controls

Ordering and credit control process

1. Check the references are being obtained for all new customers

2. Check that all new accounts on the sales ledger have been authorized by senior staff

3. Check that orders are only accepted from customers who are within their credit terms

and credit limits

4. Check that customer orders are being matched with production orders and dispatch

notes

Dispatch and invoice preparation

1. Verify trade sales with invoices checking

a. Quantities.

b. Prices charged with official price list.

c. Trade discounts have been properly dealt with.

d. Calculations and additions.

e. Entries in sales day book are correctly analyzed.

f. Sales tax, where chargeable, has been properly dealt with.

g. Postings to sales ledger

2. Verify details of trade sales with entries in inventory records

3. Verify non routine sales (scrap, non current asset etc)

4. Verify credit notes with:

a. Correspondence or other supporting documents/ evidence.

b. Approval by authorized officials.

c. Entries in inventory records.

d. Entries in goods returned records.

e. Calculations and additions.

f. Entries in day book, checking these are correctly analyzed.

g. Posting to sales ledger.

5. Test numerical sequence of dispatch notes and enquire into missing numbers

6. Test numerical sequence of invoices and credit notes, enquire into missing numbers and

inspect copies of those cancelled

7. Test numerical sequence of order forms and enquire into missing numbers

8. Check that dispatches of goods free of charge or on special terms have been authorized

by management

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 4/34

Accounting and records

1. Sales Day book

a. Check entries with invoices and credit notes respectively.b. Check additions and cross casts.

c. Check postings to sales ledger control account.

d. Check postings to sales ledger.

2. Sales ledger

a. Check entries in a sample of accounts to sales day book.

b. Check additions and balances carried down.

c. Note and enquire into contra entries.

d. Check that control accounts have been regularly reconciled to total of sales ledger

balances.3. Credit control

a. Scrutinize accounts to see if credit limits have been observed.

b. Check that receivables statements are prepared and sent out regularly.

c. Check that overdue accounts have been followed up.

d. Check that all bad debts written off have been authorized by management.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 5/34

TESTS ON PROVISIONS AND CONTINGENCIES

Determine whether the company has a present obligation as a result of a past

event by:

A. Review of correspondence and other documentation relating to the item.

B. Discussion with the directors. Have they created a valid expectation in other parties that they will

discharge the obligation? Review evidence of past practices, published policies and statements

made

Determine whether it is probable that an outflow of resources embodying

economic benefits will be required to settle the obligation by:

A. Checking whether any payments have been made in the post balance sheet period in respect of

the item.

B. Review of correspondence with solicitors, bank, customers, insurance company and suppliers

both pre and post year end.

C. Sending a letter to solicitor to obtain their views.(Where relevant)

D. Discussing the position with similar past provisions with the directors. Were these provisionseventually settled?

Determine whether provisions represent the best estimate of liability by:

A. Recalculating all provisions made.

B. Comparing the amount provided with any post year and payments and with any amount paid in

the past for similar items and considering opinions given by independent experts.

C.

In the event that it is not possible to estimate the amount of the provision, check that this

contingent liability is disclosed in the accounts.

1. Consider the nature of the client’s business. Would you expect to see provisions e.g. warranties.

2. For all material provisions and contingencies obtain a management representation.

3. Check that appropriate disclosures have been made in accordance with IAS 37

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 6/34

# ISA 610: Use of the internal auditors work for the external audit.

Considering the work of internal auditing sets out criteria that auditors should use when

obtaining an understanding and subsequent assessment of the internal audit function.

#General assessment includes :-

a)Organizational status i.e. degree of independence

b)Scope of function

c)Technical competence

d)Due professional care

Evaluation of internal audit work

# When the external auditor intense to use the specific work of internal auditing, the external

auditor should evaluate and perform audit procedure on that work to confirm adequacy for the

external auditor purpose.

Factors to consider include

a)Adequacy of technical training and proficiency

b)Whether work of assistant is properly supervised, reviewed and documented

c)Sufficiency and appropriateness of audit evidence to able to draw reasonable conclusions.

d) Whether conclusions are appropriate and reports are consistent with work perform.

Three approaches are available to the auditora) Review and test the process used by the management to develop the estimate

b)Use an independent estimate

c)Review of subsequent event

Where the review and tests the process made use by management, the

following steps would normally be appropriate:

a)Evaluation of data and consideration of the assumption on which the estimate is based

b)Testing of the calculation involved in the estimate

c)Comparison, where possible, of estimate made for prior with actual result of those prior

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 7/34

FINANCIAL STATEMENT ASSERTIONS

Assertions about classes of transactions and events for the period under audit:

COMPLETENESS

All transactions, events, assets, liabilities, equity interests and disclosures that should have been

recorded have been recorded.

OCCURRENCE

Transactions and events that have been recorded have occurred and pertain to the entity.

ACCURACY

Amounts and other data relating to recorded transactions and events have been recorded appropriately.

CUT OFF

Transactions and events have been recorded in the correct accounting period.

CLASSIFICATION

Transactions and events have been recorded in the proper accounts.

Assertions about account balances at the period end:

EXISTENCE

Assets, liabilities and equity interests exist.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 8/34

RIGHTS & OBLIGATIONS

The entity holds or controls the rights to assets and liabilities are the obligations of the entity.

COMPLETENESS

All assets, liabilities and equity interests that should have been recorded have been recorded.

VALUATION & ALLOCATION

Assets, liabilities and equity interests are included in the financial statements at appropriate amounts

and any resulting valuation or allocation adjustments are appropriately recorded.

Assertions about presentation and disclosure:

OCCURRENCE & RIGHTS & OBLIGATIONS

Disclosed events, transactions and other matters have occurred and pertain to the entity.

COMPLETENESS

All disclosures that should have been included in the financial statements have been included.

CLASSIFICATION & UNDERSTANDABILITY

Financial information is appropriately presented and described and disclosures are clearly expressed.

ACCURRACY & VALUATIONFinancial and other information are disclosed fairly and at appropriate amounts.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 9/34

Audit Procedures

Non-current assets

Completeness (and cut-off)

1. Obtain or prepare a summary of tangible non-current assets showing how:

a. Gross book value

b. Accumulated depreciation

c. Net book value

Reconcile with the opening position.

2. Compare non-current assets in the general ledger with the non-current assets register

and obtain explanations for differences.3. Match a sample of assets which physically exist to the non-current asset register.

Existence

1. Confirm that company physically inspects all items in the non-current asset register each

year.

2. Inspect assets, concentrating on high value items and additions in year. Confirm items

inspected:

a. Exist

b. Are in use

c. Are in good condition

d. Have correct serial numbers

3. Review records of income yielding assets.

Valuations (and allocation)

1. Verify valuation to valuation certificates

2. Consider reasonabless of valuation, reviewing:

a.

Experience of valuer

b. Scope of work

c. Methods and assumption used

3. Check revaluation surplus has been correctly calculated by recalculating it.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 10/34

Rights and Obligations

1. Verify title to land and buildings by inspection of:

a. Title deeds

b. Land registry certificates

c. Leases

2. Obtain a certificate from solicitors/bankers:

a. Stating purpose for which the deeds are being held (custody only)

b. Stating deeds are free from mortgage or lien

3. Examine documents of title for other assets (including purchase invoices, architects

certificates, contracts, hire or purchase agreements)

Additions

1. Verify additions by architects certificates, lawyers’ completion statements, vendors’invoices etc.

2. Check purchases have been authorized by directors/senior management by inspecting

Board minutes

3. Check additions have been recorded in non-current asset register and general ledger for

a sample of additions in the year.

Self constructed assets (to confirm valuation and completeness)

1. Verify material and labour costs and overheads to invoices, wage records etc.

2. Ensure expenditure has been analysed correctly and properly charged to capital

Disposals (to confirm rights and obligations, measurement completeness and

occurrence)

1. Verify disposals with supporting documentation, checking transfer of title, sales price

and dates of completion and payment

2. Check calculation of profit or loss by recalculation

3. Check that disposals have been authorized by inspection of Board minutes

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 11/34

Depreciation (to confirm valuation)

1. Review depreciation rates applied in relation to:

a. Asset lives

b. Residual values

c. Replacement policy

d. Past experience of gains and losses on disposal

e. Consistency with prior year and accounting policy

f. Possible obsolescence

2. Check depreciation has been charged on all assets with a limited useful life

3. For revalued assets, ensure that the charge for depreciation is based on the revalued

amount by recalculating it for a sample of revalued assets

4. Check calculation of depreciation rates for a sample of assets in each category

5. Compare ratios of depreciation to non-current assets (by category) with:

a. Previous years

b. Depreciation policy rates

6. Ensure no further depreciation allowed on fully depreciated assets

7. Check that depreciation policies and rates are disclosed in the accounts by inspecting

the draft financial statements.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 12/34

13

Share Capital

The following features should carry out for substantive procedures:

a. Agree the authorized share capital to the company incorporation document. Agree any

change with properly authorized resolution. File a copy of the relevant certificate on the

permanent file.

b. Verify and issue of share capital or other changes during the year with the minutes and

ensure issue or change is within the terms of the company incorporation.

c. Verify transfer of share by reference to:

1. Correspondence.

2. Completed and stamped transfer forms.

3. Cancelled share certificates.

4. Minutes of directors meeting.

d. Check the balance on the shareholders account in the registers of members and the

total list with the amount of issued share capital in the nominal ledger.

e. Agree dividends paid and declared but not paid to authorities in minute books and

check calculations with share capital issued. (e.g. returned dividends warrants )

Example: bank confirmation letter- for information purpose only.

Standard request for information#. Local practice will vary the way bank confirmations are requested and carry out. An

example is shown below which demonstrates what used to be UK practice and it covers

all the usual major areas where confirmations would be required.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 13/34

12

ISA 620 – Using the work of an expert

1. An expert means a person of firm possessing special skill, knowledge and experiences in

a particular field other than accounting and auditing.

2. When using the work performed by expert the auditors should obtain sufficient

appropriate audit evidence that such work is adequate for the purpose of audit.

3. When planning to use the work of an expert the auditor should evaluate the objectivity

and professional competence of the expert. a. Professional certification or licensing by or membership in an appropriate

professional body.

b. Experience and reputation in the field in which the auditor is seeking evidence.

4. The auditor should evaluate the appropriateness of the expert’s work on audit evidence.

This will involve evaluation of whether the substance of the expert’s finding is properly

reflected in the financial statement or supports the assertion and consideration of

a. Source data.

b. Assumption and methods used and their consistency with prior period.

c. Result of expert work in the light of the auditors overall knowledge of the business

and the result of other audit procedures.

5. Audit evidence from an expert may be obtained in the form:

a. Valuation of land and building

b. Determination of inventories quantities or physical condition

c. Legal options concerning interpretations of agreement statutes and regulation or on

the outcome of litigations or disputes.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 14/34

15.2

ISA 560 – Subsequent events

2.1 - The auditor should consider the effect of subsequent events on the financial statements

and on the auditor’s report.

Events occurring up to the date of the auditors report.

2.2 – The auditor should perform audit procedures designed to provide sufficient appropriate

audit evidence that all materials, subsequent events up to date of the auditor’s report that may

require adjustment of or disclosure in the financial statements have been identified, properly

accounted for or adequately disclosed.

Facts discovered after the date of the auditors report but before the financial

statements are issued:

2.3 – When after the date of the auditor’s report but before the financial statements are issued,

the auditor becomes adhere of a fact which may materially affect the financial statements, the

auditor should consider whether the financial statement need amendment, should discuss the

matter with management and should take the action appropriate in the circumstance.

Balance sheet anddate

Financial statementauthorized for issue

Auditors reportissued

Financial statmentissued

Financial statementapproved at general

meeting

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 15/34

2.4 – When management does not amend the financial statements in circumstances where the

auditor believes they need to be amended (and the audit report has not been released to the

entity) the auditor should express a qualified or adverse opinion.

Facts discovered after the financial statements have been issued:

2.5 – When after financial statements have been issued, the auditors becomes aware of a fact

which existed at the date of the auditors report and which, if known at the date, may have

caused the auditor to modify the auditors report, the auditor should consider whether the

financial statement need revisions, should discuss the matter with management, and should

take action appropriate to the circumstance.

2.6 – The new auditors report should include an emphasis of matter paragraph referring to a

note in the financial statements that more extensively discusses the reasons for the revision of

the reasons for the revision of the previously issued financial statements and to the earlier

report issued by the auditor.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 16/34

14.6

Inventories

The audit/review approach must consider:

#. Quantities – Normally arrived at by a year end count.

#. Valuation – Must apply IAS-2.

Attendance at the inventory count

Before

1. Planning:

a. Review working papers for previous year to identify risks and familiarize you with

the inventories.

b. Determine arrangements with management in advance.

c. For inventories held by/for third parties what arrangements have been made?

d. Review clients inventory count instructions.

e. Investigation of difference. (Where in records exist)

f. Consider the need for an expert.

2. Determine procedures to cover a representative selection of inventories.

During

Ensure staffs are following the inventory counting instructions.

1. Test counts from the inventories to the inventory sheets and from the inventory sheets

to the inventories.

2. Note damaged, old or obsolete inventories.

3. Review WIP for stage of completion.

4. Inventories held by client for third parties; ensure excluded from count.

5. Record the number of the last GRN and the last GDN.

6. Form as overall impression of inventory levels.

7. Photocopy inventory sheets.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 17/34

After

1. Check sequence of inventory sheets.

2. Check client’s computation of final figure.

3. Trace own test count items through to final inventory sheets.4. Check replies from third parties.

5. Inform management of any problem.

6. Follow up cut-off details.

7. Ensure necessary adjustments to book inventories have been made. (Where records are

maintained)

Continuous inventory counting/Perpetual inventory

4.3 - Some businesses keep inventory records and if these are reliable a year end count is notrequired. To determine the reliability of the records, it is necessary for the business to count

inventories on a regular basis. This is called continuous inventory counting or perpetual

inventory.

4.4 (a) Review Company’s procedures:

1. Independence of counters.

2. Frequency of counts.

3. Ensure all lines covered at least once per year.

4. Investigation of discrepancies.5. Updating of records.

(b) Attend at least one of the company’s counts (To observe)

(c) Review whole year’s results

1. Extent of counting

2. Accuracy of records

3. Reasons for discrepancies

4. Perform test counts at the year end.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 18/34

Inventory Valuation

4.5

a. Record basis of valuation used

b. Test material costs

1. Check to individual invoices

2. Ensure FIFO or appropriate basis being used

3. Check quantities used in WIP/FG

Test labour costs

1. Check calculations to supporting documentation.

2. Review costing against actual labour and production

Test application of overheads

1. Ensure only production overheads included

2. Ensure based on normal levels of activity

4.6 Test to determine whether NRV is lower than cost

1. Check the selling prices of goods sold after the year end against their purchase

invoices.

2. Review order book to determine at what price the goods are ordered at.3. Background knowledge

4. Write downs last year – are these items still in Inventory?

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 19/34

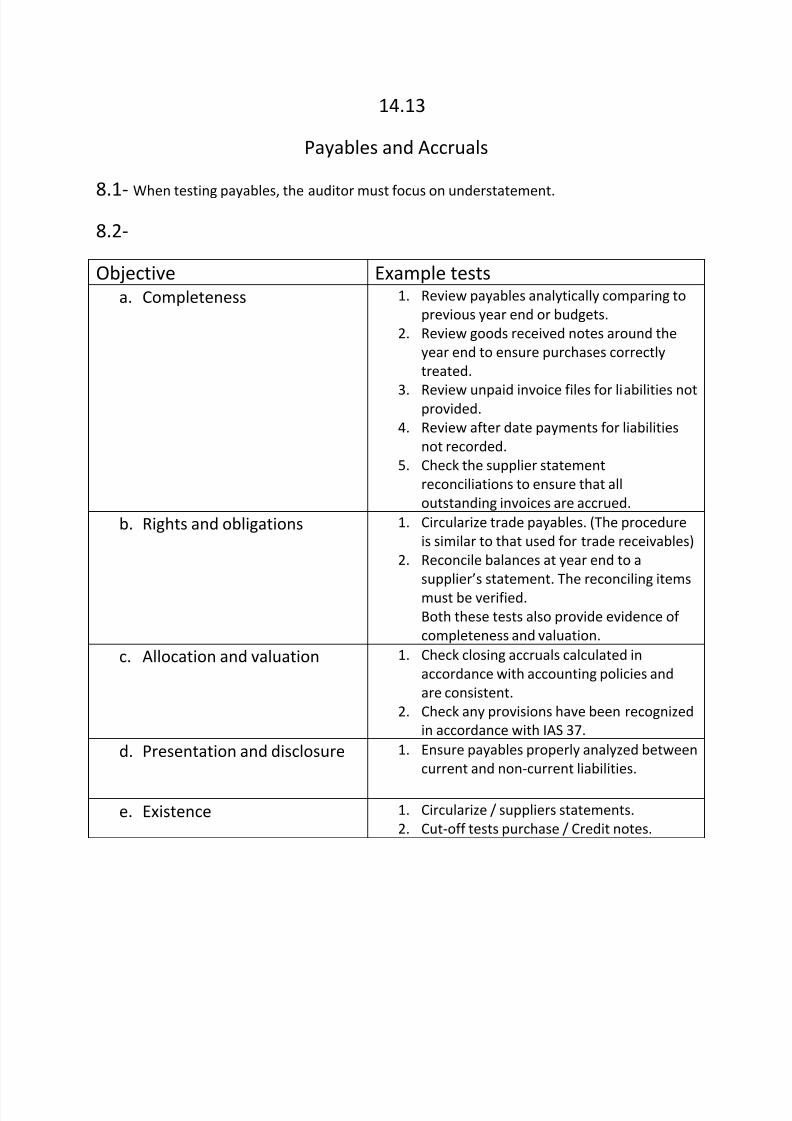

14.13

Payables and Accruals

8.1- When testing payables, the auditor must focus on understatement.

8.2-

Objective Example tests

a. Completeness 1. Review payables analytically comparing to

previous year end or budgets.

2. Review goods received notes around the

year end to ensure purchases correctly

treated.

3. Review unpaid invoice files for liabilities notprovided.

4. Review after date payments for liabilities

not recorded.

5. Check the supplier statement

reconciliations to ensure that all

outstanding invoices are accrued.

b. Rights and obligations 1. Circularize trade payables. (The procedure

is similar to that used for trade receivables)

2. Reconcile balances at year end to a

supplier’s statement. The reconciling items

must be verified.

Both these tests also provide evidence of

completeness and valuation.

c. Allocation and valuation 1. Check closing accruals calculated in

accordance with accounting policies and

are consistent.

2. Check any provisions have been recognized

in accordance with IAS 37.

d. Presentation and disclosure 1. Ensure payables properly analyzed between

current and non-current liabilities.

e. Existence 1. Circularize / suppliers statements.

2. Cut-off tests purchase / Credit notes.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 20/34

19.7

Property, plant and equipment

Audit review/ objective Example tests

a. Completeness 1. Reconcile non-current assets register to

accounts. 2. Physical verification from asset to asset

register.

b. Rights and obligations 1. Inspect invoices.

2. Buildings – title deeds and land registry

Certificates.3. Vehicles – Registration documents.

c. Presentation and disclosure 1. Check properly disclosed.

2. Capital commitments are disclosed.

3. Any leased assets disclosed.

4. Revaluations properly disclosed.

d. Existence 1. Physical verification.

2. Disposals.

19.8

Depreciation rates

The following work would be done to determine whether depreciation rates are reasonable:

a. Discuss the asset replacement policy with the directors.

b. Select some assets from the non-current assets register which are approaching the end

of their useful lives. Find these assets and note if they are still being used and their

condition. If they are not being used, then they should be written down to a nil value.

c. Check the sales and scrapping of assets over the past year. If large losses on disposal

have occurred then depreciation rates are too low; and

d. Consider technological developments in relation to the company’s assets.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 21/34

15.3

ISA 570 – Going concern

3.1 When planning and performing audit procedures and in evaluating the results there of,

the auditor should consider the appropriateness of management’s use of the going

concern assumption underlying the preparation of the financial statements.

3.2 Under the going concern assumption an entity is ordinarily viewed as continuing in

business for the foreseeable future with neither the intention nor the necessity of

liquidation, ceasing trading or seeking protection from creditors pursuant to laws or

regulations. 3.3 Management’s assessment of the entity’s ability to continue as a going concern should

cover a period of at least 12 months after period end.

3.4 In obtaining an understanding of the entity, the auditor should consider whether there

are events or conditions and related business risks which may cast significant doubt on

the entity’s ability to continue as a going concern.

3.5 Based on the audit evidence obtained, the auditor should determine if, in his

judgment, a material uncertainty exists related to events or conditions that alone or in

aggregate, may cast significant doubt on the entity’s ability to continue as a going

concern.

3.6 Examples of events or conditions, which may cast significant doubt on the going

concern assumption include:

a. Financial

1. Net liability or net current liability position.

2. Fixed-term borrowings approaching maturity without realistic prospects of

renewal or repayments; or excessive reliance on short-term borrowings to

finance non-current assets.

3.

Indications of withdrawal of financial support by debtors and other creditors. 4. Negative operations cash flows indicated by historical or prospective financial

statements.

5. Adverse key financial ratios.

6. Substantial operating losses or significant deterioration in the value of assets

used to generate cash flows.

7. Arrears or discontinuance of dividends.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 22/34

8. Inability to pay creditors on due dates.

9. Inability to comply with the terms of loan agreements.

10. Change from credit to cash-on-delivery transaction with suppliers.

11. Inability to obtain financing for essential new product development or other

essential investments.

b. Operational

1. Loss of key management without replacement.

2. Loss of a major market, franchise, license or principal supplier.

3. Labour difficulties or shortage of important supplies.

c. Other

1. Non-compliance with capital or other statutory requirements.

2. Pending legal or regulatory proceedings against the entity that may, if

successful, result in claims that are unlikely to be satisfied.

3. Changes in legislation or government policy to adversely affect the entity.

3.7 Relevant audit procedures may include:

a. Analyzing and discussing cash flow, profit and other relevant forecasts

with management.b. Analyzing and discussing the entity’s latest available interim financial

statements.

c. Reviewing the terms of debentures and loan agreements and

determining whether any have been breached.

d. Reading minutes of the meetings of shareholders, those charged with

governance and relevant committees for reference to financing

difficulties.

e. Enquiring of the entity’s lawyer regarding the existence of litigation and

claims and the reasonableness of management’s assessments of theiroutcome and the estimate of their financial implications.

f. Confirming the existence legality and enforceability of arrangements to

provide or maintain financial support with related and third parties and

assessing the financial ability of such parties to provide additional funds.

g. Considering the entity’s plans to deal with unfilled customer orders.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 23/34

h. Reviewing events after period end to identify those that either mitigate

or otherwise affect the entity’s ability to continue as a going concern.

3.8 When analysis of cash flow is a significant factor in considering the future outcome

of events or conditions the auditor considers: 1. The reliability of the entity’s information system for generating such

information, and 2. Whether there is adequate support for the assumptions underlying the forecast

In addition the auditor compares:

a. The prospective financial information for recent prior periods with historical

results. And b. The prospective financial information for the current period with results

achieved to date.

3.9 The auditor will form his opinion on the going concern status of the companybased on the outcome of the above.

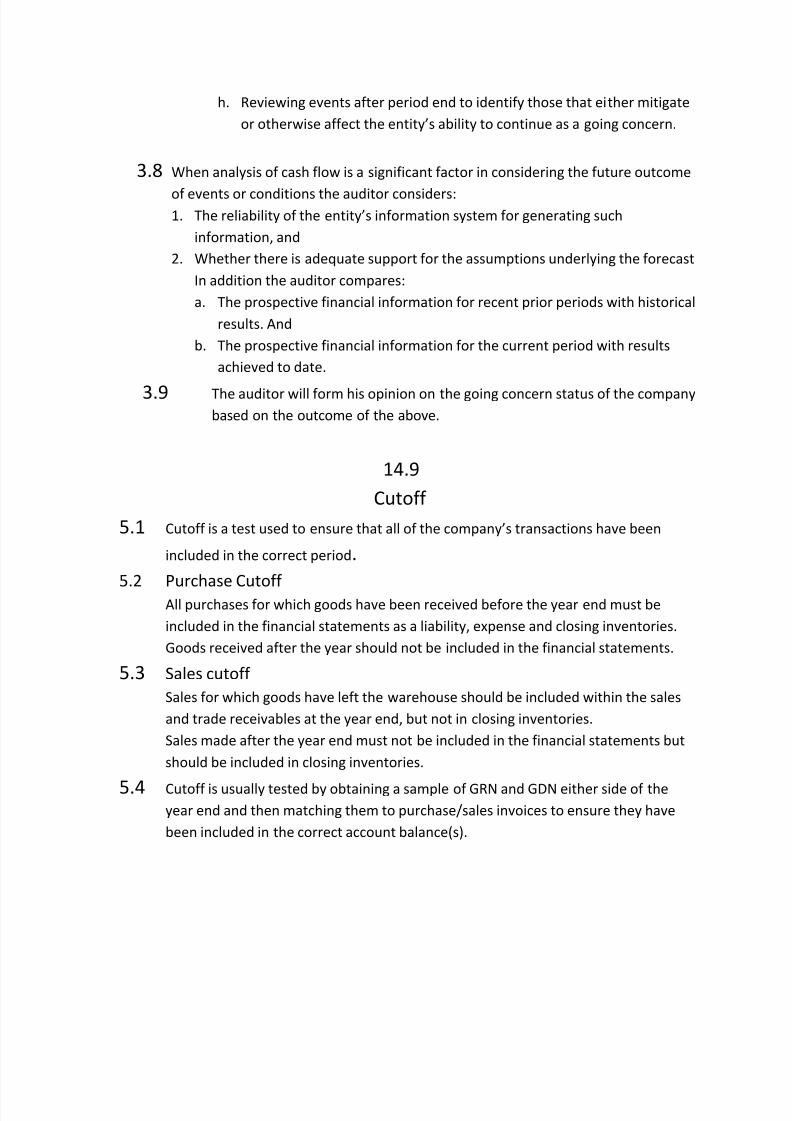

14.9

Cutoff

5.1 Cutoff is a test used to ensure that all of the company’s transactions have been

included in the correct period.

5.2 Purchase CutoffAll purchases for which goods have been received before the year end must be

included in the financial statements as a liability, expense and closing inventories.

Goods received after the year should not be included in the financial statements.

5.3 Sales cutoff Sales for which goods have left the warehouse should be included within the sales

and trade receivables at the year end, but not in closing inventories.

Sales made after the year end must not be included in the financial statements but

should be included in closing inventories.

5.4 Cutoff is usually tested by obtaining a sample of GRN and GDN either side of the

year end and then matching them to purchase/sales invoices to ensure they have

been included in the correct account balance(s).

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 24/34

14.10

Receivables

A specific technique used to test for the existence and obligation/rights of receivables as a

direct circularization. This is conducted as follows:

a. Obtain listing of trade receivables as at the confirmation date.

b. Agree total to nominal ledger.

c. Review for any obvious omissions/ misstatements by comparing this year’s list with last

year’s.

d. Select a sample of accounts for confirmation.

Select the sample from the following balances:

1. Old, unpaid amounts

2. Credit balances

3. Nil balances

4. Material balances

Letter should be on the client’s paper, signed by the client with a copy of the current

statement attached. It should request that the reply be sent direct to the auditor and

reply paid envelopes should be sent.

e. After reasonable period, send follow-up request.

f. Follow up by telephone or fax if there is no reply.

g. No reply

1. Confirmation of individual outstanding invoices.

2. Alternative procedures

A. Agree opening balance on account with last years closing balance.

B. Test casts.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 25/34

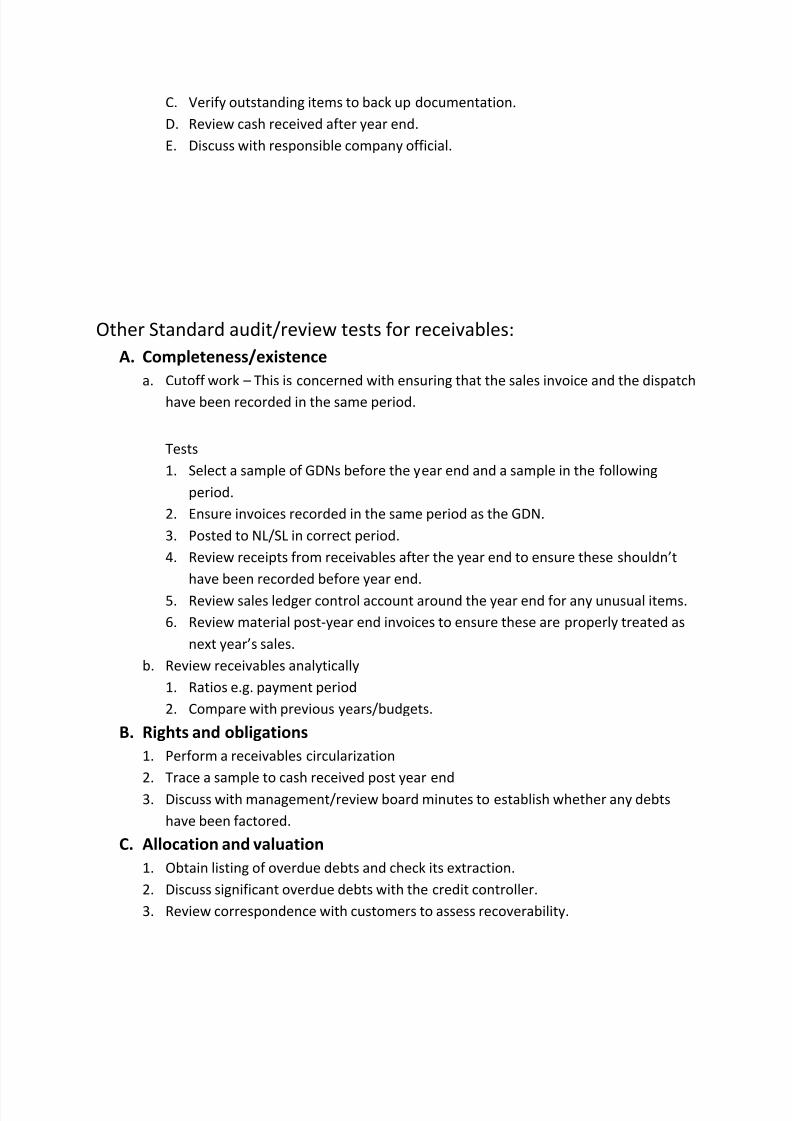

C. Verify outstanding items to back up documentation.

D. Review cash received after year end.

E. Discuss with responsible company official.

Other Standard audit/review tests for receivables:

A. Completeness/existence

a. Cutoff work – This is concerned with ensuring that the sales invoice and the dispatch

have been recorded in the same period.

Tests

1. Select a sample of GDNs before the year end and a sample in the following

period.

2. Ensure invoices recorded in the same period as the GDN.

3. Posted to NL/SL in correct period.

4. Review receipts from receivables after the year end to ensure these shouldn’t

have been recorded before year end.

5. Review sales ledger control account around the year end for any unusual items.

6. Review material post-year end invoices to ensure these are properly treated as

next year’s sales.

b. Review receivables analytically

1. Ratios e.g. payment period

2. Compare with previous years/budgets.

B. Rights and obligations

1. Perform a receivables circularization

2. Trace a sample to cash received post year end

3. Discuss with management/review board minutes to establish whether any debts

have been factored.

C. Allocation and valuation

1. Obtain listing of overdue debts and check its extraction.

2. Discuss significant overdue debts with the credit controller.

3. Review correspondence with customers to assess recoverability.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 26/34

4. Ensure all debts written off were properly authorized.

5. Review payments received after the year end.

D. Presentation and disclosure

1. Ensure receivables appropriately categorized within current assets.

14.12

Bank and Cash

Objective Example tests

a. Completeness/Allocation and

valuation

1. Review bank confirmation letter for

details of all accounts held.

2. Count petty cash balance.

3. Check cash of bank reconciliations.

4. Trace outstanding items to after date

bank statements and ensure all

subsequently cleared.

5. Review cashbook for unusual items.

b. Rights and obligations 1. Review bank letter to ensure valid title

to accounts held.

c. Presentation and disclosure 1. Ensure asset and liability balances are

disclosed separately unless there is a

right of set-off agreement.

d. Existence 1. Trace recorded assets and liabilities to

bank confirmation of balances.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 27/34

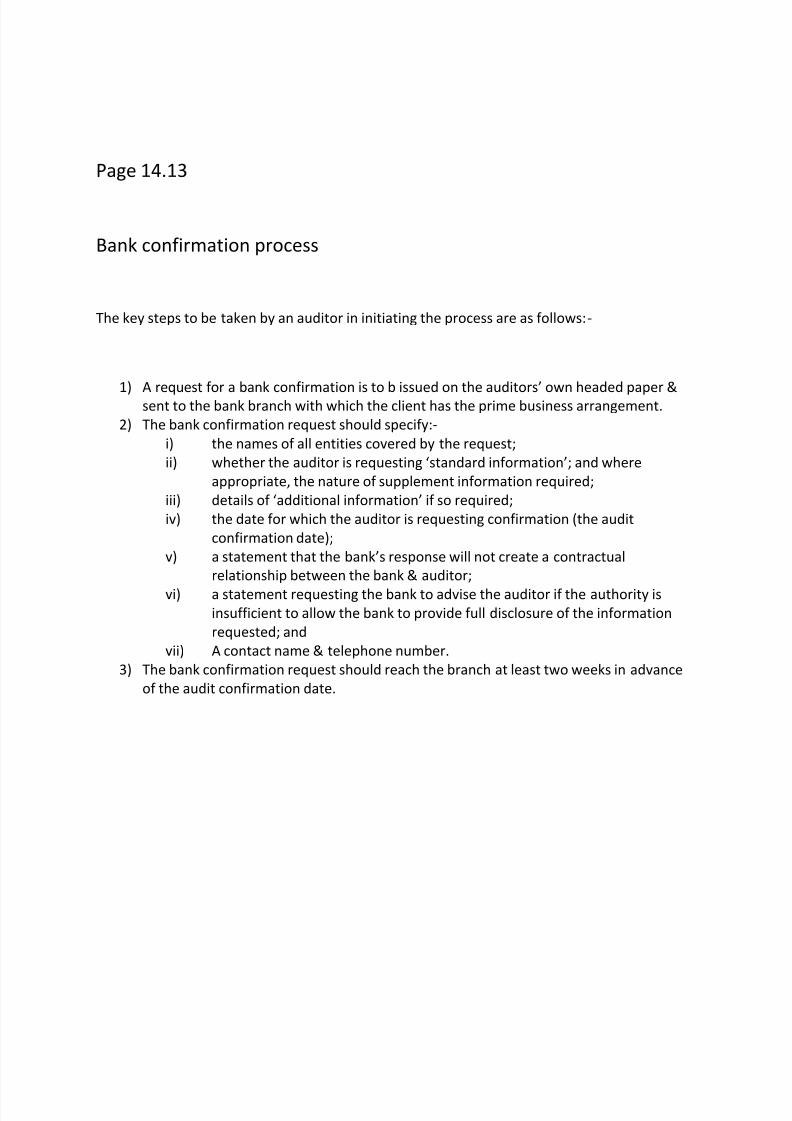

Page 14.13

Bank confirmation process

The key steps to be taken by an auditor in initiating the process are as follows:-

1) A request for a bank confirmation is to b issued on the auditors’ own headed paper &sent to the bank branch with which the client has the prime business arrangement.

2) The bank confirmation request should specify:-

i) the names of all entities covered by the request;

ii) whether the auditor is requesting ‘standard information’; and where

appropriate, the nature of supplement information required;

iii) details of ‘additional information’ if so required;

iv) the date for which the auditor is requesting confirmation (the audit

confirmation date);

v) a statement that the bank’s response will not create a contractual

relationship between the bank & auditor;

vi) a statement requesting the bank to advise the auditor if the authority is

insufficient to allow the bank to provide full disclosure of the information

requested; and

vii) A contact name & telephone number.

3) The bank confirmation request should reach the branch at least two weeks in advance

of the audit confirmation date.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 28/34

Page 15.9

ISA 250: Consideration of law & regulations in the audit of financial statements.

5.1 None-compliance with laws & regulations may have a material effect on the financial

statements, e.g. fines which are not been provided for.

5.2 The auditor is required to obtain a general understanding of the legal framework

applicable to the entity & the industry. Then the auditor should:-

I) enquire of management as to whether the entity is in compliance with such laws &

regulations;

ii) Inspect correspondence with the relevant licensing or regulatory authorities.

The auditor should obtain sufficient appropriate evidence about compliance with those laws &

regulations generally recognized by the auditor to have a material effect on the financial

statements.

5.3 Other than the above, the auditor does not perform other audit procedures on the entity’s

compliance with laws & regulation since this would be outside the scope of an audit of financial

statements.

In the absence of evidence to the contrary, the auditor is entitled to assume the entity is in

compliance with these laws & regulations.

5.4 The auditor should consider the implications of non-compliance in relation to other aspectsof the audit particularly the reliability of management representations.

Effect on the auditor’s report

5.5 Where non-compliance has a material effect on the financial statements, a qualified

(‘except for’) or adverse opinion should b expressed.

If the auditor is precluded from obtaining sufficient appropriate evidence to evaluate whether

non-compliance has occurred or is material to the financial statements, a modified opinion due

to a limitation of scope is issued.

Reporting to third parties

5.6 The auditor’s duty of confidentiality would normally preclude reporting non-compliance to a

third party.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 29/34

However, the auditor may have a legal duty to report non-compliance to regulatory or

supervisory authorities. The auditor may need to seek legal advice in such circumstances giving

due consideration to the auditor’s responsibility in the public interest.

6.7

ISA 520 Analytical procedures

7.1 – “Analytical procedures” means the analysis of relationship to identify inconsistencies and

unexpected relationships.

7.2 - The auditor should apply analytical procedures as risk assessment procedures and in the

overall review at the end of the audit.

They can also be used as a source of substantive audit evidence when their use is more

effective or efficient than tests of details in reducing detection risk for specific financial

statement assertions.

7.3 – Analytical procedures include the following type of comparisons:-

1. Prior periods

2. Budgets and forecasts

3. Industry information

4. Predictive estimates

5. Relationship between elements of financial information i.e. ratio analysis

6. Relationship between financial and non financial information e.g. payroll costs to the

number of employees.

Analytical procedures as risk assessment procedures

7.4 – The auditor should apply analytical procedures as risk assessment procedures to obtain

an understanding of the entity and its environment.

Application of analytical procedures may indicate aspects of the entity of which the auditor

unaware and will assist in assessing the risks of material misstatement in order to determine

the nature, timing and extent of further audit procedures.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 30/34

For example, the auditor could compare gross margin of a company year on year based on

interim or draft financial information. If the gross margin has increased this could indicate a

failure to include all expenses, an increase in the sales price or an error/overstatement of the

closing inventories figure.

Analytical procedures as substantive procedures

7.5 – When designing and performing analytical procedures as substantive procedures, the

auditor needs to consider the following factors:

1. The suitability of using substantive analytical procedures given the assertions.

2. The reliability of the data, whether internal or external, from which the expectation of

recorded amounts or ratios is developed.

3. Whether the expectation is sufficiently precise to identify a material misstatement atthe desired level of assurance.

4. The amount of any difference of recorded amounts from expected values that is

acceptable.

Overall review at end of the audit

7.6 – The auditor should apply analytical procedures at or near the end of the audit whenforming an overall conclusion as to whether the financial statements as a whole are consistent

with the auditor’s understanding of the entity.

7.7 – When analytical procedures identify significant fluctuations or relationships that are

inconsistent with other relevant information or that deviate from predicted amounts, the

auditor should investigate and obtain adequate corroborative audit evidence.

7.8 – Some common analytical review ratios are outlined in the Additional Notes to this

chapter.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 31/34

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 32/34

8.4 – If the auditor is unable to obtain sufficient appropriate audit evidence concerning the

opening balances a limitation on scope modification is appropriate, either qualified (‘except

for’) or a disclaimer of opinion.

8.5 – If the opening balances do contain material misstatements which affect the current

period are not corrected and adequately presented and disclosed, a disagreement modificationis appropriate, either qualified (‘except for’) or adverse.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 33/34

FOCUS OF AUDIT

The auditor can look at an operation in different ways. For example the audit can be:1 transaction oriented

2 systems oriented, or3 results oriented.In practice, most audits are a mix of these approaches but the underlying focus of these different ways ofcarrying out an audit is worthy of examination, because the approach will have implications on the type ofaudit conclusions and on the impact of the audit report.

Each of these three approaches is reviewed below.

1. Transaction oriented Audit objective:

To determine whether the operations are being carried out in compliance with the standards andprocedures as laid out in the Accounting Manual. Audit approach:

Select a representative sample of transactions and check whether they have been carried out accordingto the procedures outlined in the Accounting Manual.Follow up on any transactions that have not been properly carried out: not properly authorized / errors inamounts / indicate waste or abuse / not properly recorded / etc.Determine underlying reasons for observed findings.Form of report:

Findings: list of transactions that have not been properly carried out or recorded.

Conclusions: certain areas of the Accounting Manual are not being complied with.Recommendations: correct wrong transactions and increase compliance with certain controls as set out in

the Accounting manual.Impact of report:

With its predominant emphasis on individual transaction, there is a serious danger that this report does

not get the attention of management. In fact, it can have a negative impact. If when a manager reads it

and finds that the total impact of the weaknesses listed is small, the conclusion derived is that what the

auditor finds is not of significance.

2. Systems oriented Audit objective:

To determine whether the internal controls are adequate to ensure that operations are being carried outproperly; that assets are safeguarded; and that there is minimal waste, misuse and abuse. Audit approach:

Examine the controls in place and, on the basis of a risk assessment, professional judgement andcomparison with standards, determine whether these controls are adequate and whether, in the opinionof the auditor, any controls are missing.Select a sample of transactions to test whether the controls in place are operating as intended.Conclude on the adequacy of the internal controls.

8/14/2019 Whole Audit note.docx

http://slidepdf.com/reader/full/whole-audit-notedocx 34/34

Form of report:

Findings: List of inadequate or missing internal controls (illustrated with examples of transactions thathave not been properly carried out).

Conclusions: assessment of the strengths and weaknesses of the controls in place.Recommendations: strengthen certain controls and introduce certain additional controls.

3. Results oriented Audit objective:

To determine whether the operations are being carried out economically, efficiently and effectively andwhether the organization’s objectives are being met.

Audit approach:Identify the major expenditures, revenues, outputs and outcomes of the entity and conduct a risk

assessment.

Assess the appropriateness of management reports on expenditures, revenues and outputs. Review

studies and reports on the effectiveness of the operations and on programme performance.On the basis of these reports conclude whether managers have appropriate information to know howeconomic, efficient and effective are the operations.If these reports do not contain sufficient information to assess performance properly, the auditor candecide to conclude on the inadequacy of the measures or to determine directly whether performance isadequate.Where the auditor decides to assess performance, this can be done by:* comparing results against plans and budgets* performing analysis (such as trends in unit cost or in levels of efficiency), or* making comparisons with standards or with the performance of other organisations.

Form of report:Findings: Clarity of objectives and accountability / the extent and quality of the measurement and

reporting of performance / examples of failures in performance / trends in performance.Conclusions: Appropriateness of the performance framework / adequacy of the measurement andreporting of performance / adequacy of the internal controls / an assessment of performance or changesin performance.Recommendations: Review of programme / improve measurement and reporting of performance /improve operations / strengthen internal controls.Impact of reportBy focusing on the impact of what the auditor has observed, the message of the audit report is most likely

to capture the attention of senior management.