who is bypassing whom? russian, european and caspian … · who is bypassing whom? russian,...

TRANSCRIPT

1

Who is Bypassing Whom?Russian, European and Caspian Gas and Oil

32nd IAEE International ConferenceJune 21 - 24, 2009

Maureen S. Crandall, PhDProfessor of Economics

Industrial College of the Armed ForcesNational Defense University

Washington, DC

2

Agenda

• Western interest in “Southern Corridor” natural gas and oil pipelines bypassing Russia and Iran

• GasRussia trying to defeat efforts to bypass itEU interest in Nabucco diminished - not likely for another 10+ years

• OilKazakhstan progress in bypassing

Russia – by ship, to link to BTC

3

Countries Affected by Russian Gas Cutoff, 2009

Source: http://news.bbc.co.uk/2/hi/europe/7822694.stm#map, Jan 12, 2009

4

“Safety and certainty in oil lie in variety and variety alone.”

Winston Churchill, 1913

Natural Gas – Europe Searching for Diversification

5

Aftermath of 2009 Russian Gas Cutoff

• Severe damage to reputation as 40-year reliable gas supplier to Europe

• Europe looking elsewhere for new gas, but progress slow

Europeans torn between concern about over-dependence on Russian gas, and worry that it might not be there when they need itEurope will continue to be heavily dependent on Russian gas

6

Uneasy Energy Relationship• Russia-EU energy story primarily one of

gas – a wakeup call post Jan 2006Russia supplies 42% EU gas imports, 32% EU oil imports

• 2008 RU oil exports = ~ $224 billion• 2008 RU gas exports to EU = $66 billion

• In gas, Russia unlikely to be bypassed Mutual interdependence Russia cannot afford not to sell gas to Europe

• In oil, a world market• Russia is building/proposing gas pipelines

to bypass European states

7

Gas Strategy: Who is Bypassing Whom?(Gazprom 1, EU/US 0)

• Nabucco/White Stream: bypass Russia, IranRussia acting to undermine – Russian “pipes on the ground” before others move aheadPre-Caspian pipeline agreements

• Nord Stream – bypass Ukraine, Belarus & Poland

• South Stream – bypass Ukraine, Belarus & Turkey

• Blue Stream-II – bypass Ukraine & Belarus; but dependence on Turkey, a (risky) partner?

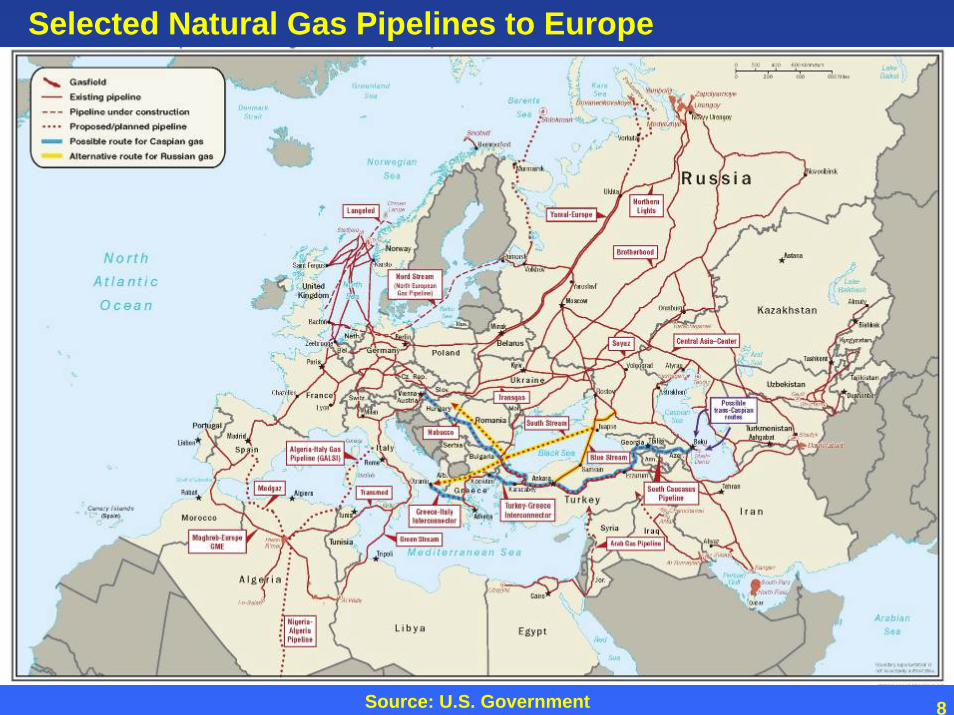

8Source: U.S. Government

Selected Natural Gas Pipelines to Europe

9

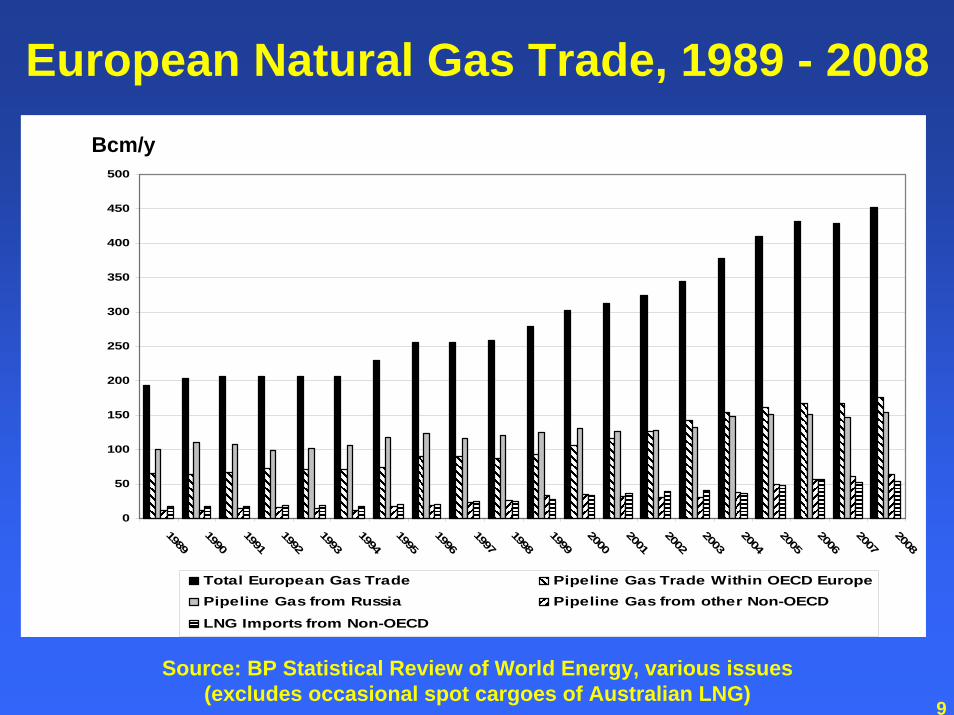

European Natural Gas Trade, 1989 - 2008

Source: BP Statistical Review of World Energy, various issues(excludes occasional spot cargoes of Australian LNG)

Bcm/y

0

50

100

150

200

250

300

350

400

450

500

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Total European Gas Trade Pipeline Gas Trade Within OECD EuropePipeline Gas from Russia Pipeline Gas from other Non-OECD

LNG Imports from Non-OECD

Bcm/y

10

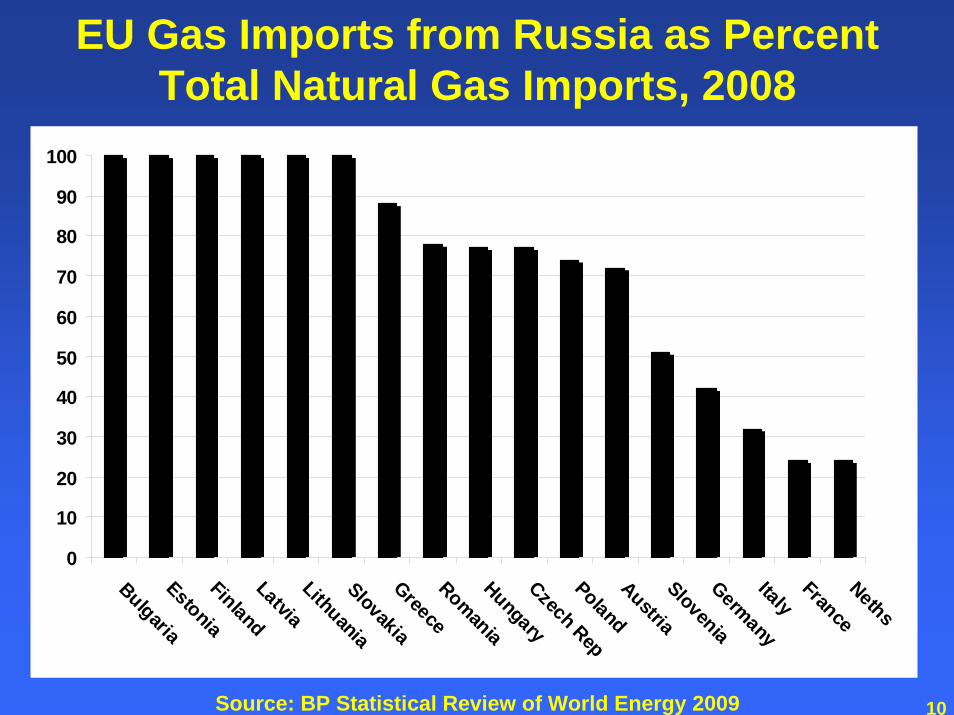

EU Gas Imports from Russia as Percent Total Natural Gas Imports, 2008

Source: BP Statistical Review of World Energy 2009

0

10

20

30

40

50

60

70

80

90

100

BulgariaEstoniaFinlandLatviaLithuaniaSlovakiaGreeceRomaniaHungaryCzech RepPolandAustriaSloveniaGermanyItalyFranceNeths

11

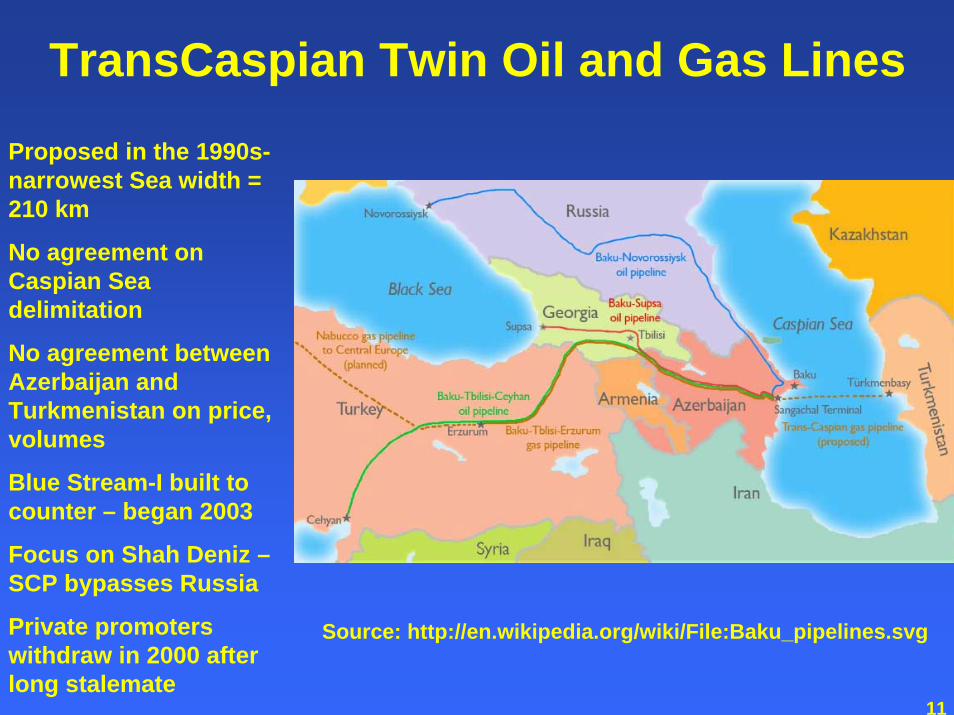

TransCaspian Twin Oil and Gas Lines

Proposed in the 1990s-narrowest Sea width = 210 km

No agreement on Caspian Sea delimitation

No agreement between Azerbaijan and Turkmenistan on price, volumes

Blue Stream-I built to counter – began 2003

Focus on Shah Deniz –SCP bypasses Russia

Private promoters withdraw in 2000 after long stalemate

Source: http://en.wikipedia.org/wiki/File:Baku_pipelines.svg

12

Blue Stream I and II

Blue Stream I = 16 bcm/y, 1,213 km, built to preclude a T-C gas pipeline, operational in 2005

Blue Stream II and South Stream competing against Nabucco

Blue Stream II proposes 24-30 bcm/y

Partnership of Italy & Russia

Issue of Turkish control of delivered gas

Source: http://www.gazprom.ru/eng/articles/article8898.shtml; http://www.petroleumiran.com/maps.html

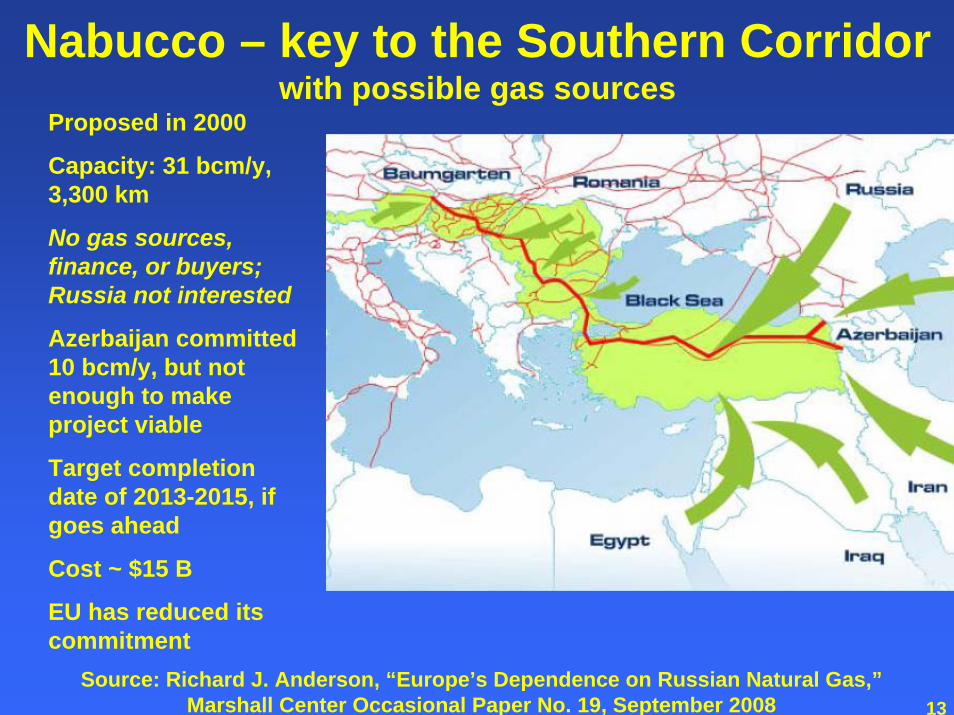

13Source: Richard J. Anderson, “Europe’s Dependence on Russian Natural Gas,”

Marshall Center Occasional Paper No. 19, September 2008

Nabucco – key to the Southern Corridor with possible gas sources

Proposed in 2000

Capacity: 31 bcm/y, 3,300 km

No gas sources, finance, or buyers; Russia not interested

Azerbaijan committed 10 bcm/y, but not enough to make project viable

Target completion date of 2013-2015, if goes ahead

Cost ~ $15 B

EU has reduced its commitment

14

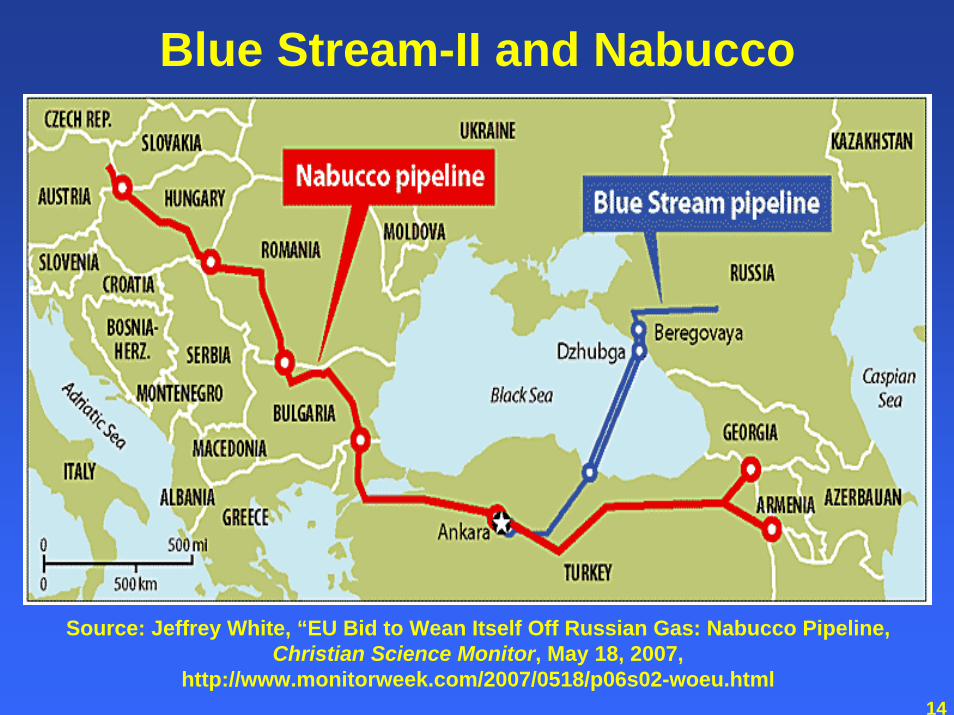

Blue Stream-II and Nabucco

Source: Jeffrey White, “EU Bid to Wean Itself Off Russian Gas: Nabucco Pipeline, Christian Science Monitor, May 18, 2007,

http://www.monitorweek.com/2007/0518/p06s02-woeu.html

15

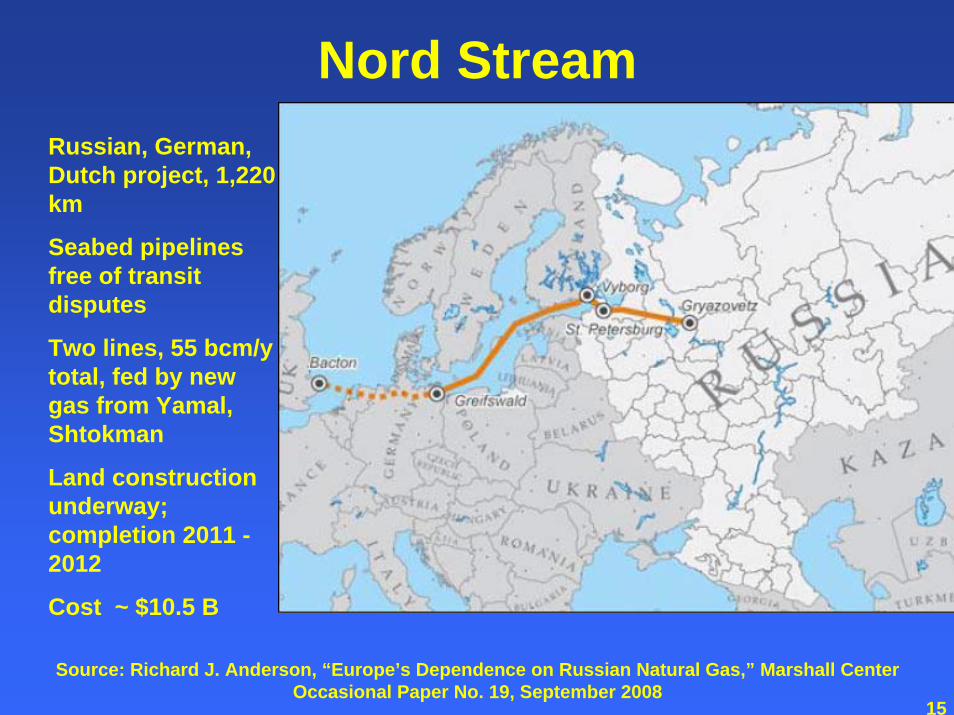

Source: Richard J. Anderson, “Europe’s Dependence on Russian Natural Gas,” Marshall Center Occasional Paper No. 19, September 2008

Nord StreamRussian, German, Dutch project, 1,220 km

Seabed pipelines free of transit disputes

Two lines, 55 bcm/y total, fed by new gas from Yamal, Shtokman

Land construction underway; completion 2011 -2012

Cost ~ $10.5 B

16

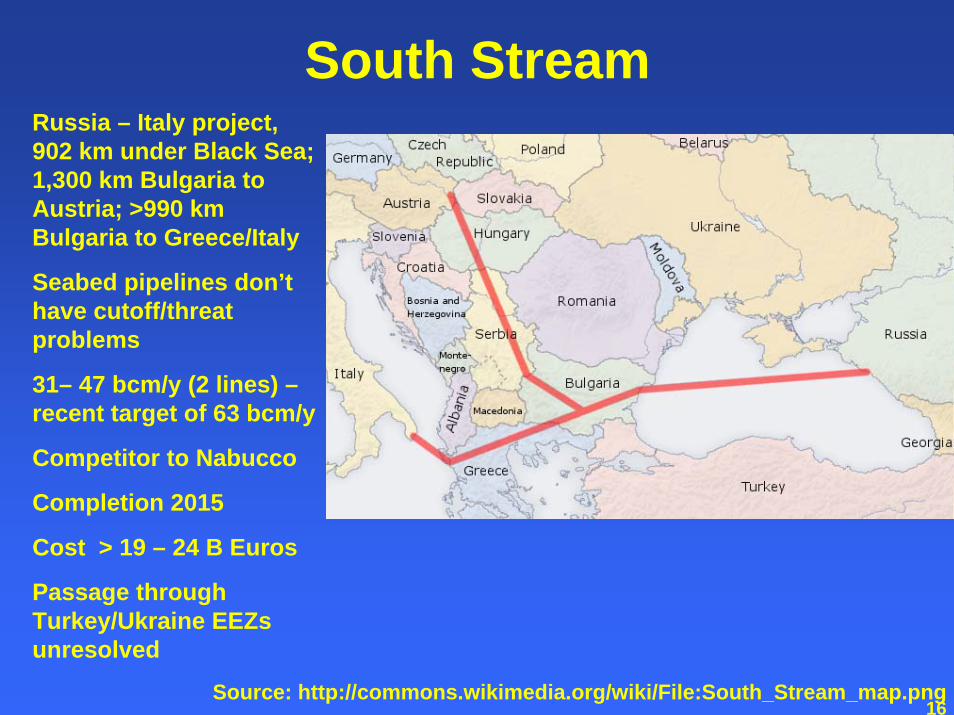

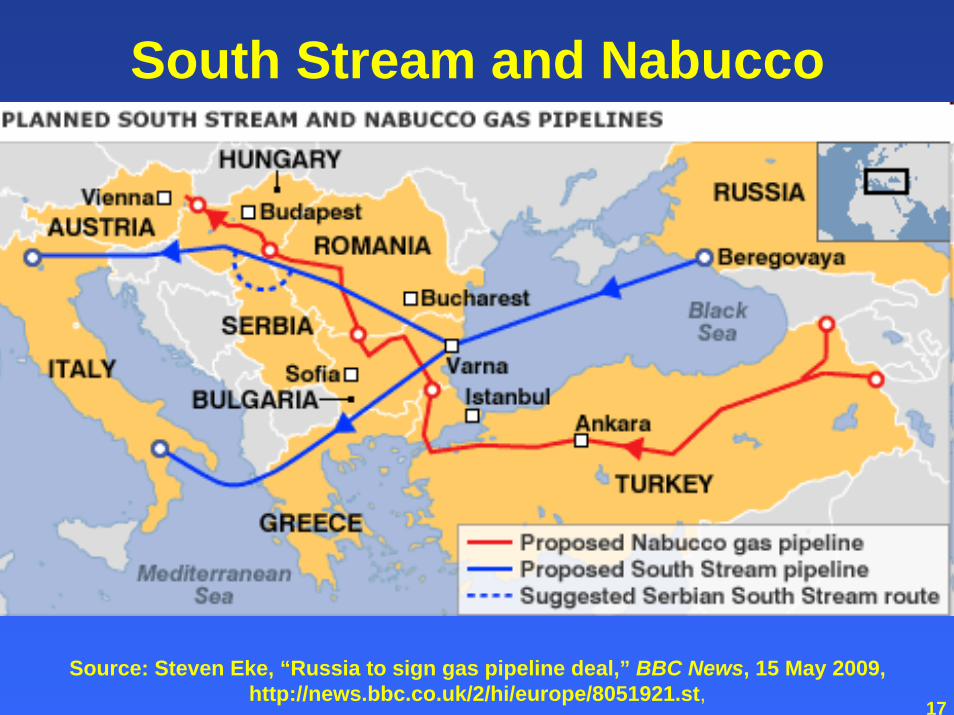

South Stream

Source: http://commons.wikimedia.org/wiki/File:South_Stream_map.png

Russia – Italy project, 902 km under Black Sea; 1,300 km Bulgaria to Austria; >990 km Bulgaria to Greece/Italy

Seabed pipelines don’t have cutoff/threat problems

31– 47 bcm/y (2 lines) –recent target of 63 bcm/y

Competitor to Nabucco

Completion 2015

Cost > 19 – 24 B Euros

Passage through Turkey/Ukraine EEZs unresolved

17

South Stream and Nabucco

Source: Steven Eke, “Russia to sign gas pipeline deal,” BBC News, 15 May 2009, http://news.bbc.co.uk/2/hi/europe/8051921.st,

18

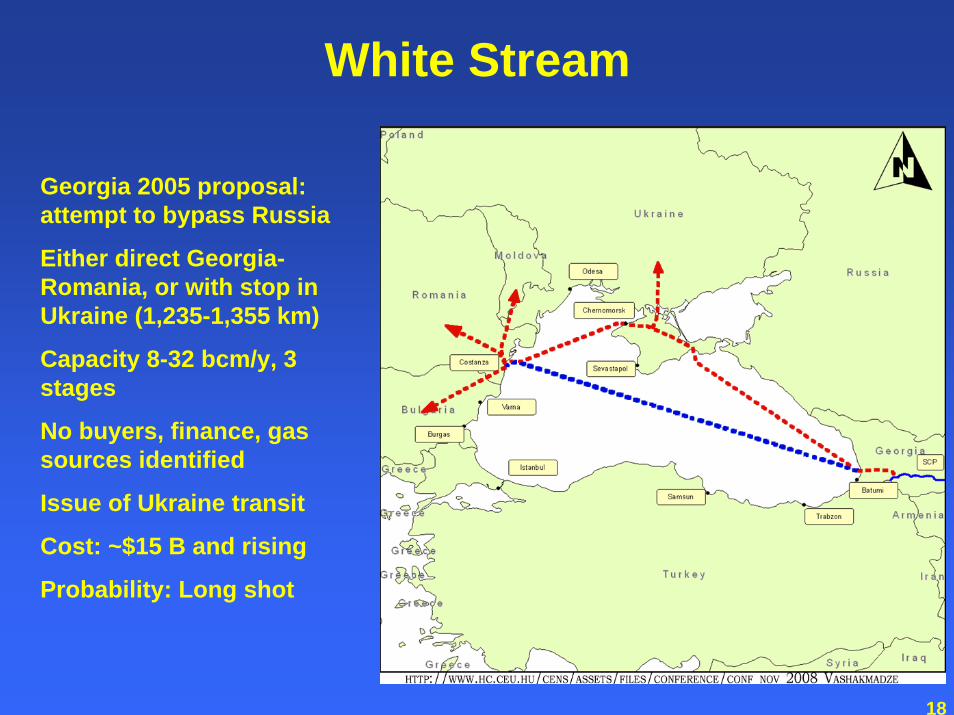

White Stream

Georgia 2005 proposal: attempt to bypass Russia

Either direct Georgia-Romania, or with stop in Ukraine (1,235-1,355 km)

Capacity 8-32 bcm/y, 3 stages

No buyers, finance, gas sources identified

Issue of Ukraine transit

Cost: ~$15 B and rising

Probability: Long shot

19

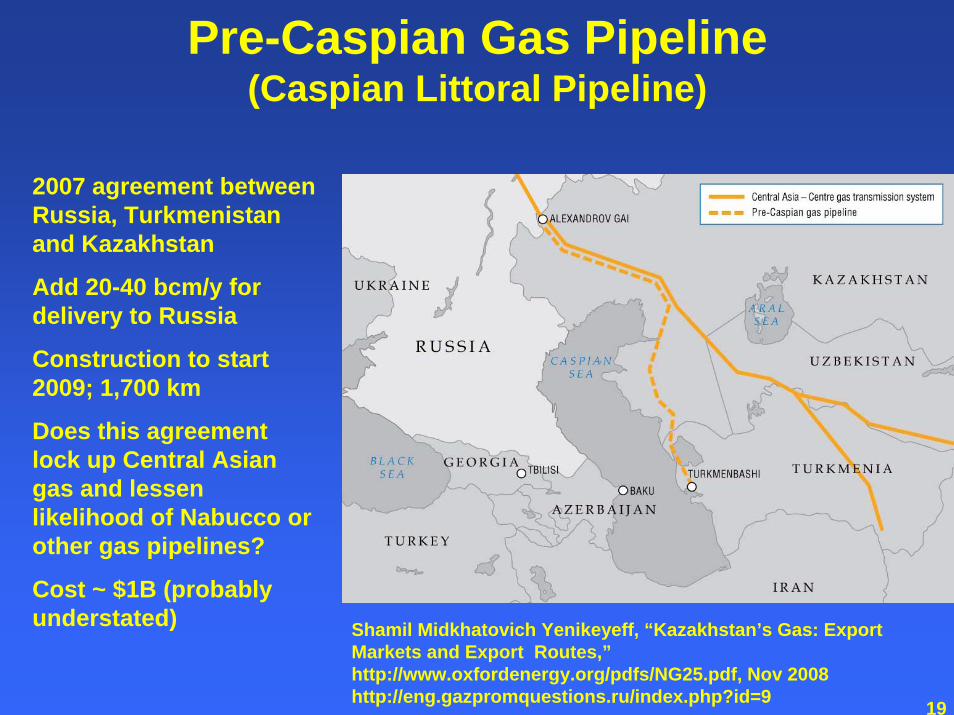

Pre-Caspian Gas Pipeline(Caspian Littoral Pipeline)

Shamil Midkhatovich Yenikeyeff, “Kazakhstan’s Gas: Export Markets and Export Routes,”http://www.oxfordenergy.org/pdfs/NG25.pdf, Nov 2008 http://eng.gazpromquestions.ru/index.php?id=9

2007 agreement between Russia, Turkmenistan and Kazakhstan

Add 20-40 bcm/y for delivery to Russia

Construction to start 2009; 1,700 km

Does this agreement lock up Central Asian gas and lessen likelihood of Nabucco or other gas pipelines?

Cost ~ $1B (probably understated)

20

Azeri Gas to Russia or Iran Rather than to Nabucco?

• Key question:Will Azerbaijan and Russia (or Iran) conclude firm gas sales/purchase agreement from 2010?

• Diversification of sales for Azerbaijan• Advances revenue stream to Baku• Pressures Turkey• Undermines Nabucco if sales to Russia

or Iran agreed

21

Wild Cards: Future Turkmenistan and Iraq Gas

• Turkmenistan: great uncertaintyRich in gas; huge Yolotan-Osman field (4 – 14 tcm); world’s 4th/5th largest fieldPetropars (Iran) likely to develop – where will gas go?

• More gas to China, Russia?• Gas for pipelines to the West?

• Iraq: new Kurdish finds, uncertainties and hurdles

Khor Mor and Chemchamal for Nabucco?• Partnership of OMV, MOL, 2 UAE firms (Crescent &

Dana)• Reserves of 100 bcm?• Kurdish-Iraqi politics and law, role of BOTAS and

Shell agreement in Iraq?

22

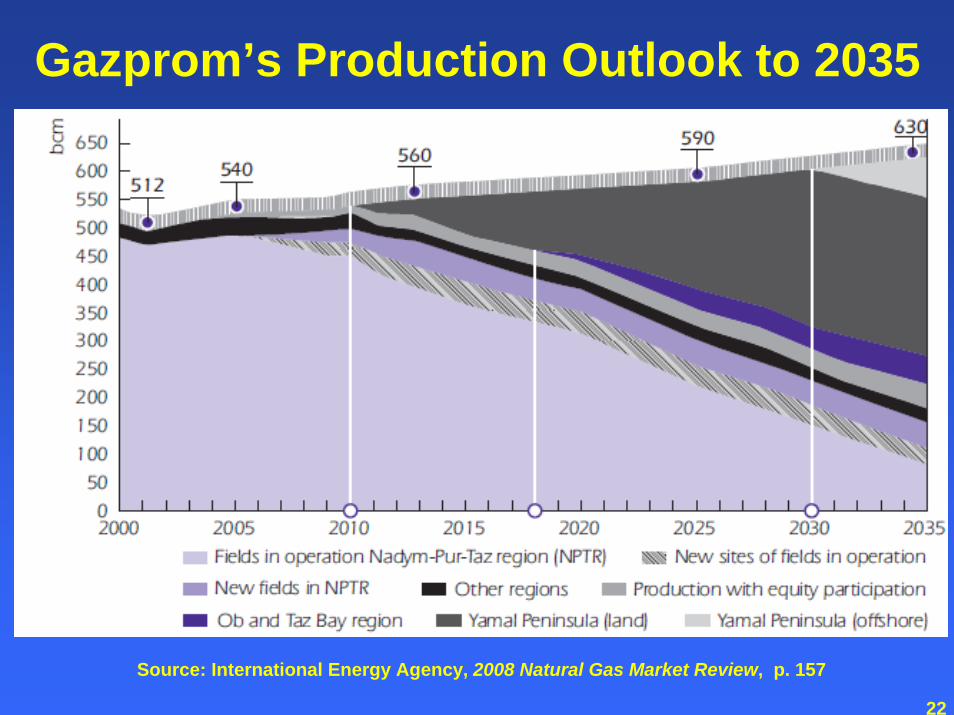

Gazprom’s Production Outlook to 2035

Source: International Energy Agency, 2008 Natural Gas Market Review, p. 157

23

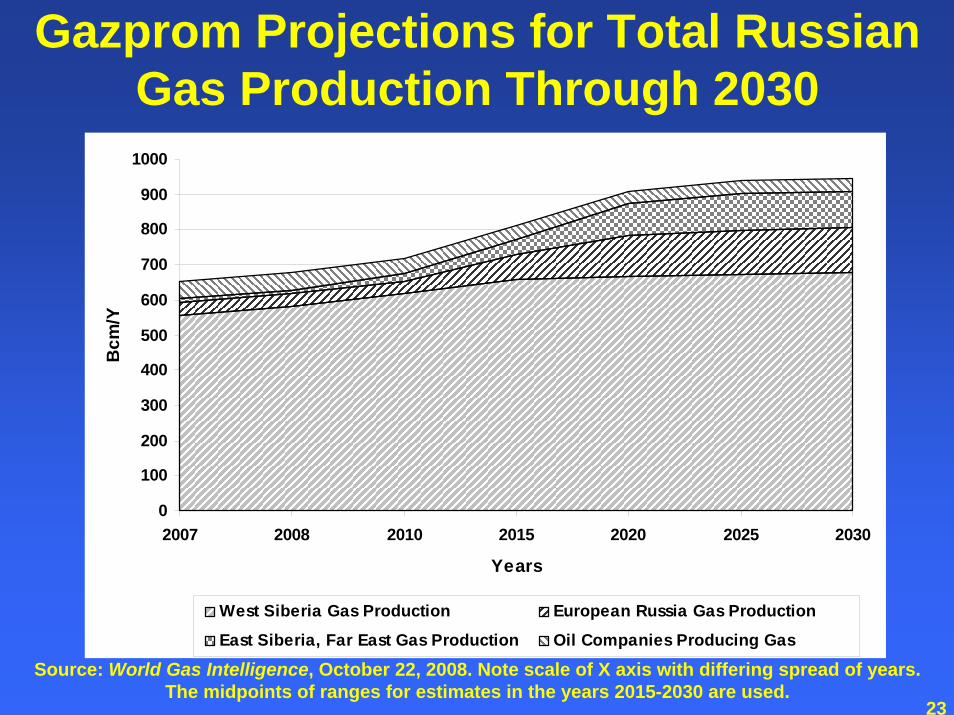

Gazprom Projections for Total Russian Gas Production Through 2030

0

100

200

300

400

500

600

700

800

900

1000

2007 2008 2010 2015 2020 2025 2030

Years

Bcm

/Y

West Siberia Gas Production European Russia Gas Production

East Siberia, Far East Gas Production Oil Companies Producing Gas

Source: World Gas Intelligence, October 22, 2008. Note scale of X axis with differing spread of years. The midpoints of ranges for estimates in the years 2015-2030 are used.

24

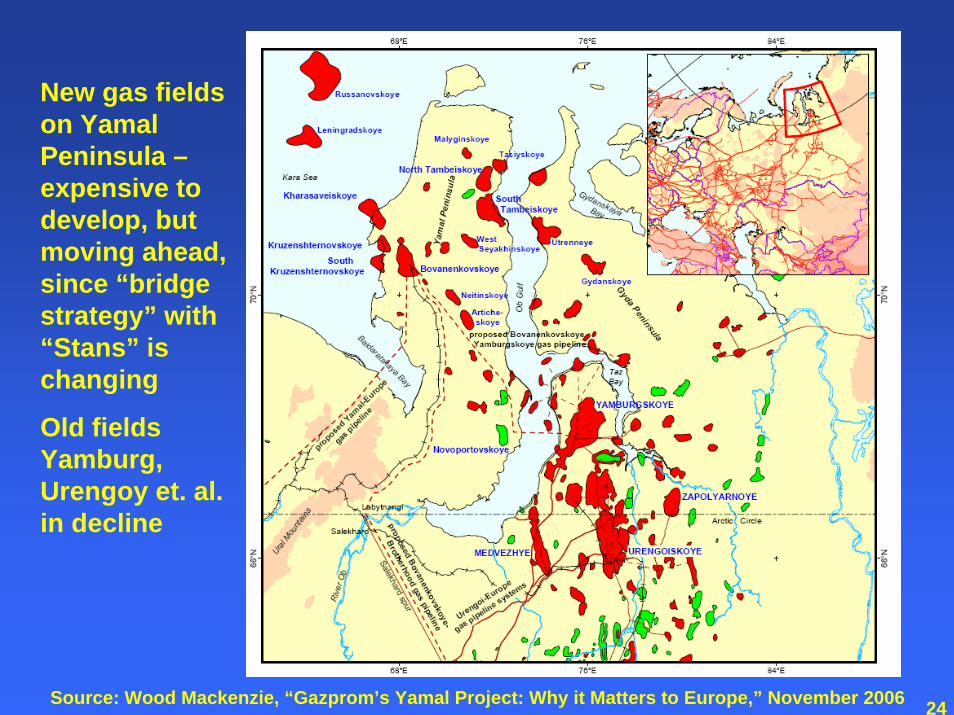

New gas fields on Yamal Peninsula –expensive to develop, but moving ahead, since “bridge strategy” with “Stans” is changing

Old fields Yamburg, Urengoy et. al. in decline

Source: Wood Mackenzie, “Gazprom’s Yamal Project: Why it Matters to Europe,” November 2006

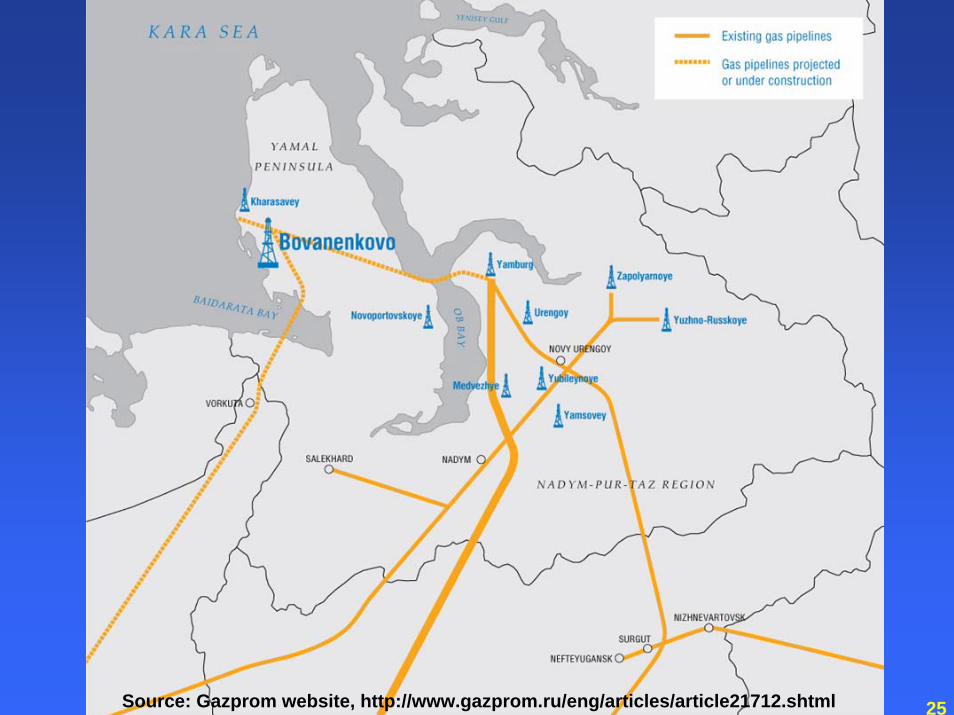

25Source: Gazprom website, http://www.gazprom.ru/eng/articles/article21712.shtml

26

Gazprom Finances & Investments

• Russian “bridge strategy” seems to be ending

Russia bought cheap Caspian gas, resold it to Europe at western prices, postponing Yamal developmentCaspian states now receiving European pricesFor Russia, may now be relatively cheaper to develop Yamal than to continue buying Caspian gas

• Will European demand for Russian gas recover?

27

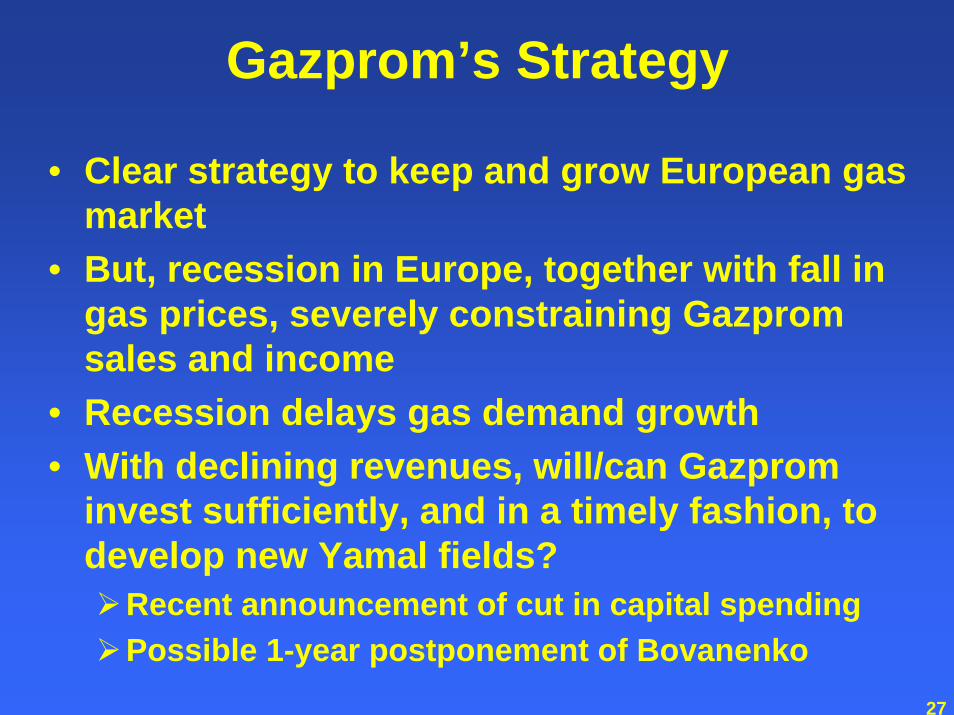

Gazprom’s Strategy

• Clear strategy to keep and grow European gas market

• But, recession in Europe, together with fall in gas prices, severely constraining Gazprom sales and income

• Recession delays gas demand growth • With declining revenues, will/can Gazprom

invest sufficiently, and in a timely fashion, to develop new Yamal fields?

Recent announcement of cut in capital spendingPossible 1-year postponement of Bovanenko

28

EU Response• Energy policy adrift

Members act in accordance with own self-interests, rather than overall EU interestsMembers cut own deals, ignore EU, and stall integration process, resulting in bottlenecks in pipelines and storageNo common regulatory regime within EU; no common regulatory regime applied equally to EU and non-EU participants

• EU dependence on Russian oil and gas imports will remain substantial

29

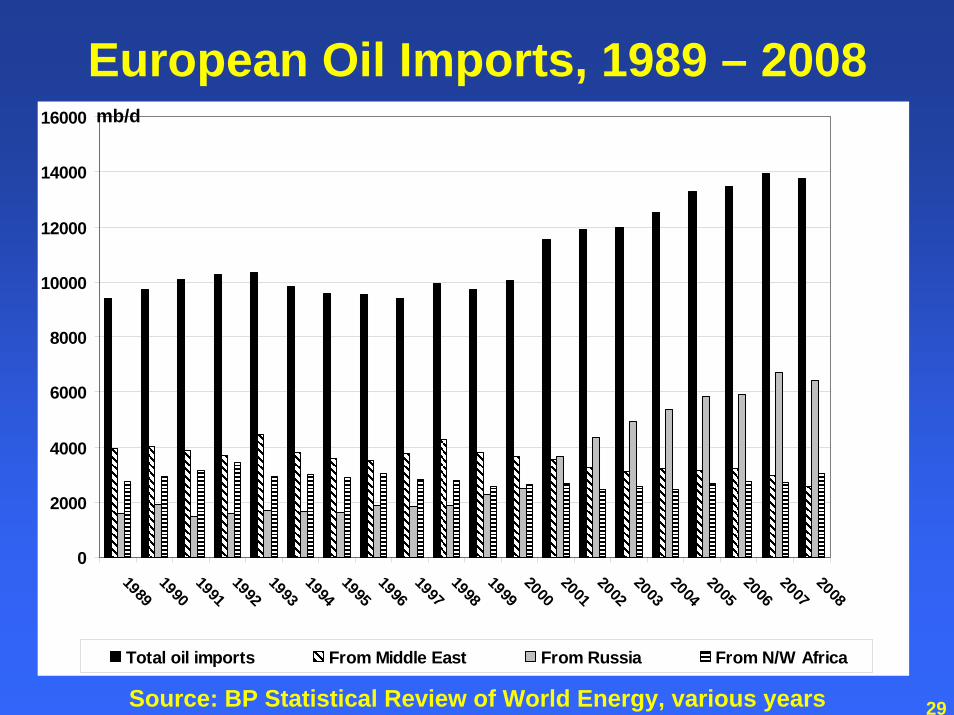

European Oil Imports, 1989 – 2008

Source: BP Statistical Review of World Energy, various years

0

2000

4000

6000

8000

10000

12000

14000

16000

19891990199119921993199419951996199719981999200020012002200320042005200620072008

Total oil imports From Middle East From Russia From N/W Africa

mb/d

30

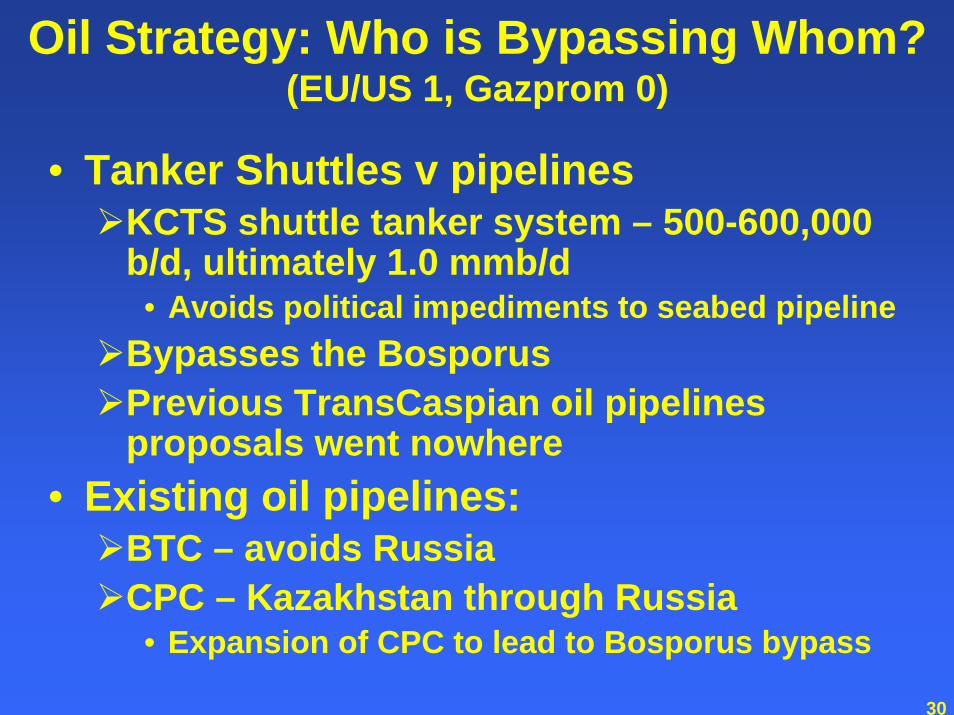

Oil Strategy: Who is Bypassing Whom?(EU/US 1, Gazprom 0)

• Tanker Shuttles v pipelinesKCTS shuttle tanker system – 500-600,000 b/d, ultimately 1.0 mmb/d

• Avoids political impediments to seabed pipelineBypasses the BosporusPrevious TransCaspian oil pipelines proposals went nowhere

• Existing oil pipelines:BTC – avoids RussiaCPC – Kazakhstan through Russia

• Expansion of CPC to lead to Bosporus bypass

31

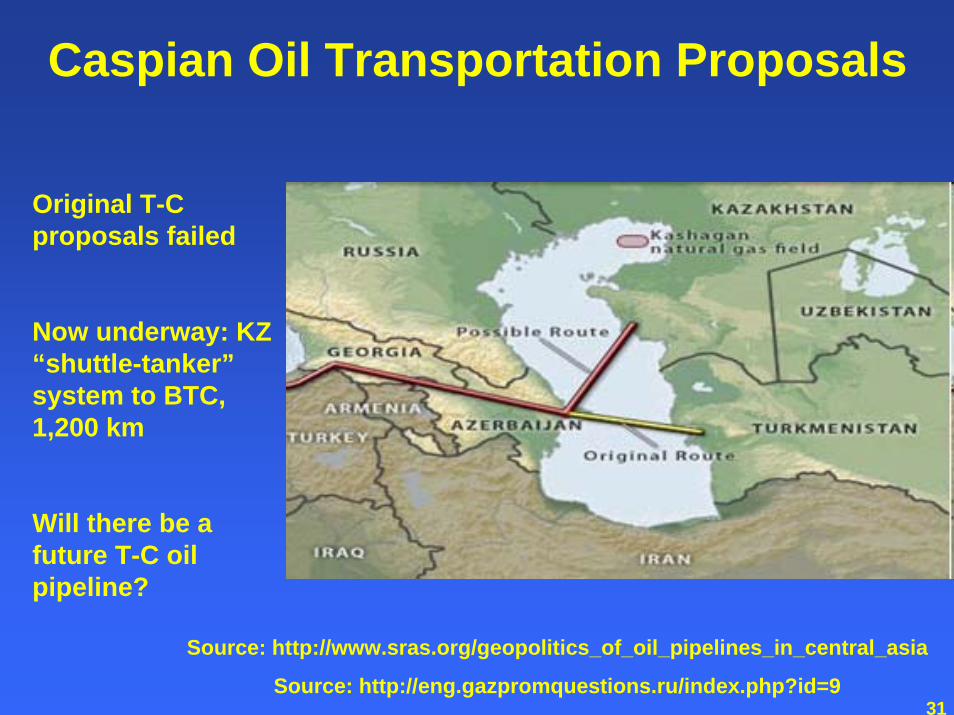

Caspian Oil Transportation Proposals

Source: http://www.sras.org/geopolitics_of_oil_pipelines_in_central_asia

Source: http://eng.gazpromquestions.ru/index.php?id=9

Original T-C proposals failed

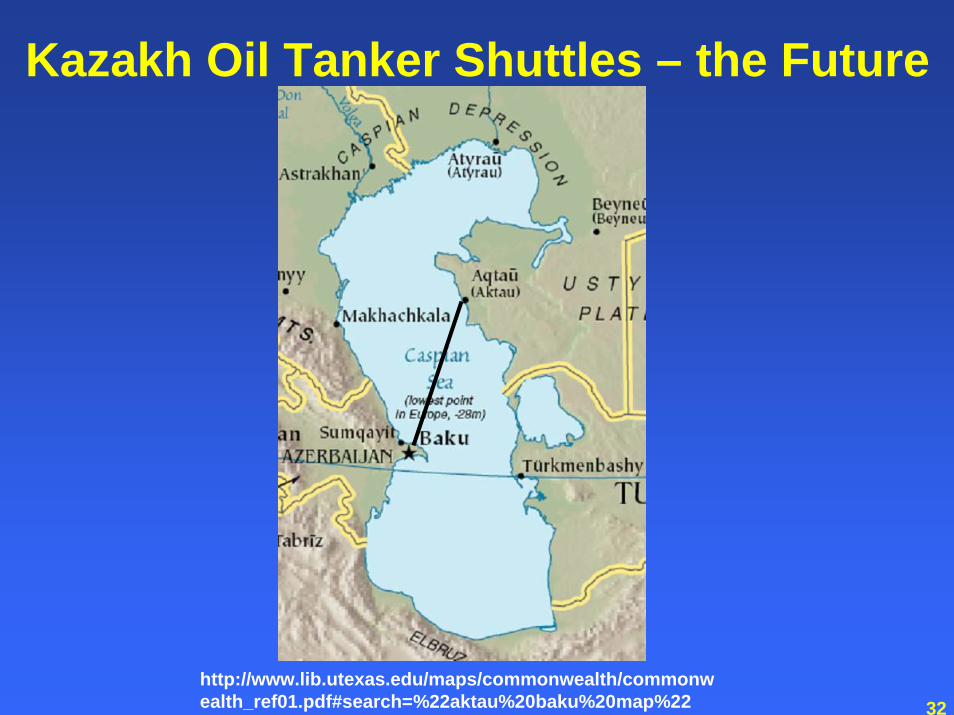

Now underway: KZ “shuttle-tanker”system to BTC, 1,200 km

Will there be a future T-C oil pipeline?

32

Kazakh Oil Tanker Shuttles – the Future

http://www.lib.utexas.edu/maps/commonwealth/commonwealth_ref01.pdf#search=%22aktau%20baku%20map%22

33

Conclusion

• Gas: Gazprom will not be bypassed for gas sales to Europe

Doubling capacity of South Stream Interested in Blue Stream-IIUndermining Nabucco’s prospectsProceeding with Pre-Caspian lineT-C gas pipeline doubtful

• Oil: Russia vulnerable to/experiencing bypassing action from KCTS

T-C oil pipeline doubtful