what we've learned from the credit crisis - milken...

TRANSCRIPT

1

What We've Learned From the Credit Crisis

Tuesday, April 28, 200911:00 AM -

12:15 PM

Speakers:Alexander Friedman, Chief Financial Officer, Bill & Melinda Gates FoundationJames Gellert, President and CEO, Rapid Ratings InternationalBruce Kasman, Chief U.S. Economist, JPMorgan

ChaseJames McCaughan, CEO, Principal Global Investors LLCGary Shilling, President, A. Gary Shilling & Co.

ModeratorCharles Van Vleet, Director, Portfolio Investments, United Technologies Corp.

2

U.S. consumer credit trends down

Annualized percent changes in consumer credit

-10-505

1015202530

1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

Percent

Note: Shaded columns denote periods of recession.Sources: Federal Reserve, Milken

Institute.

.

3

Credit then and now

Source: Federal Reserve.

Financial Sector

3%

1958Total debt: $661.2 billion

Government44%

Nonfinancial Business sector

26%

Households27%

2008Total debt: $50,734 billion

Households27%

Financial sector34%

Government17%

Nonfinancial Business sector

22%

4

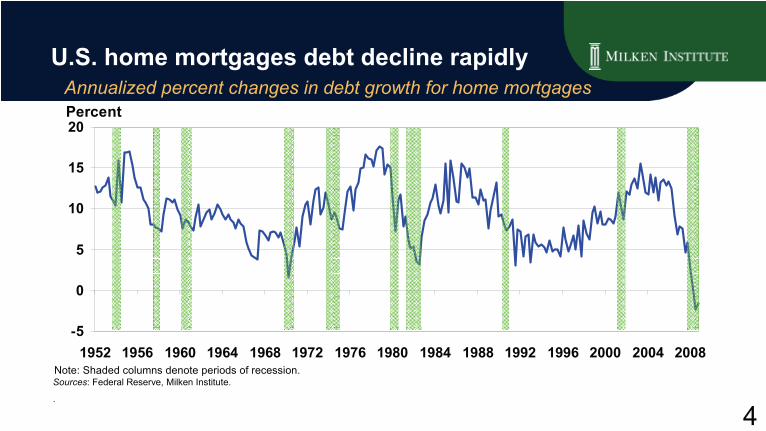

U.S. home mortgages debt decline rapidly Annualized percent changes in debt growth for home mortgages

-5

0

5

10

15

20

1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

Percent

Sources: Federal Reserve, Milken

Institute.

.

Note: Shaded columns denote periods of recession.

5

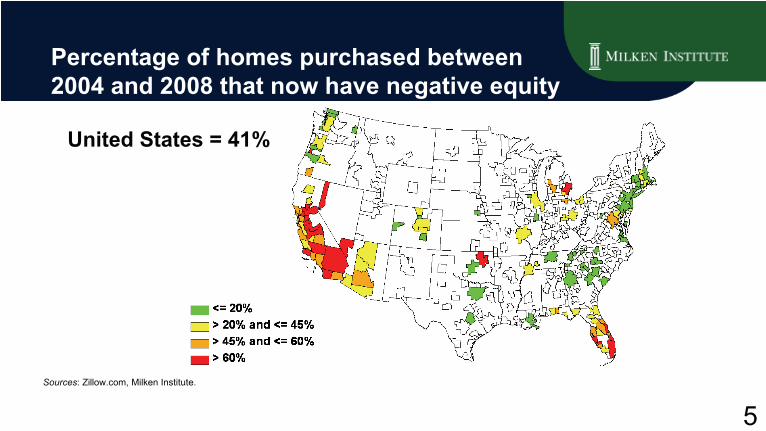

Percentage of homes purchased between 2004 and 2008 that now have negative equity

Sources: Zillow.com, Milken Institute.

United States = 41%

6

Financial stocks take big hits

Note: Bear Stearns stock price is to May 2008. Countrywide stock

price is to June 2008. Merrill Lynch and Wachovia stock prices are to December 2008.Sources: Bloomberg, Milken Institute.

-99.9-99.9-98.9-98.8-98.6

-94.3-90.3-90.0-87.5-87.2

-82.7-66.3

-60.0-46.8-45.0

Lehman BrothersWashington MutualFreddie MacFannie MaeAIGBear StearnsWachoviaCountrywideMerrill LynchBank of AmericaUBSMorgan StanleyWells FargoGoldman SachsJPMorgan & Chase

Percentage change in stock price, Dec. 2006-March 2009

1,446

1,070

461364

2006 2007 2008 2009 March

Total loss in market value: $1,081 billion from December 2006 to March 2009

Total market capitalization of these selectedfinancial institutions, US$ billions

7

Federal Reserve has little maneuvering room

Sources: Federal Reserve, Milken Institute.

0.00.51.01.52.02.53.03.54.04.5

01 02 03 04 05 06 07 08 09 10 11 12 01 02 03 04

Percent

Effective federal funds rate

Target federal funds rateApr. 30, 2008: 2%Oct. 8, 2008: 1.5%Oct. 29, 2008: 1%Dec. 16, 2008: 0-0.25%

2008 2009

8

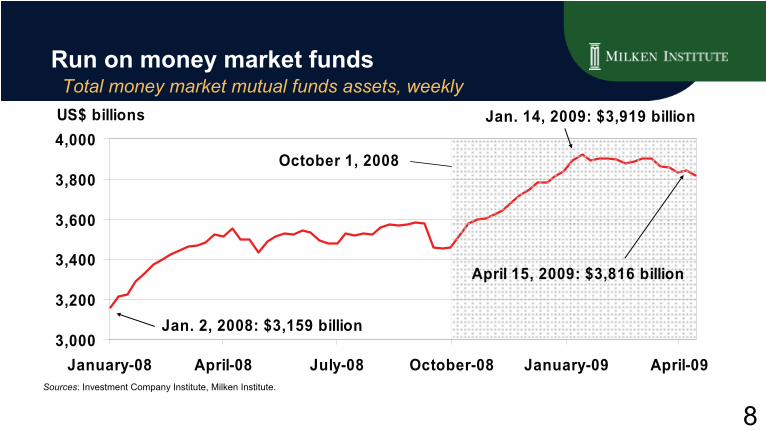

Run on money market funds

Total money market mutual funds assets, weekly

Sources: Investment Company Institute, Milken Institute.

3,000

3,200

3,400

3,600

3,800

4,000

January-08 April-08 July-08 October-08 January-09 April-09

US$ billions Jan. 14, 2009: $3,919 billion

April 15, 2009: $3,816 billion

October 1, 2008

Jan. 2, 2008: $3,159 billion

9

Market for liquidity freezes

30-day commercial paper yield spreads over 1-month Treasury

Sources: Federal Reserve, Milken Institute.

0

100

200

300

400

500

600

January-07 July-07 January-08 July-08 January-09

Asset-backed commercial paperFinancial commercial paper

AA rated, daily, basis points The Fed announced Commercial Paper Funding Facility (CPFF) on Oct. 7, 2008

10

Commercial paper outstanding declines substantially Outstanding asset-backed and unsecured commercial paper

Sources: Federal Reserve, Milken Institute.

0.5

0.7

0.9

1.1

1.3

Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09

Asset-backed commercial paperNon-asset-backed commercial paper

US$ trillions August 8, 2007: $1.2 trillion

April 15, 2009: $681 billionJan. 7, 2004: $659 billion

11Source:

Bloomberg.

Credit spreads for corporate bonds in the U.S.

Corporate bond spreads started to narrow

Credit spread for high-yield bond

Credit spread for investment-grade bond rated AAA

0

500

1,000

1,500

2,000

Mar2006

Jun2006

Sep2006

Dec2006

Mar2007

Jun2007

Sep2007

Dec2007

Mar2008

Jun2008

Sep2008

Dec2008

Mar2009

Basic points, spread over 10-year Treasury

12

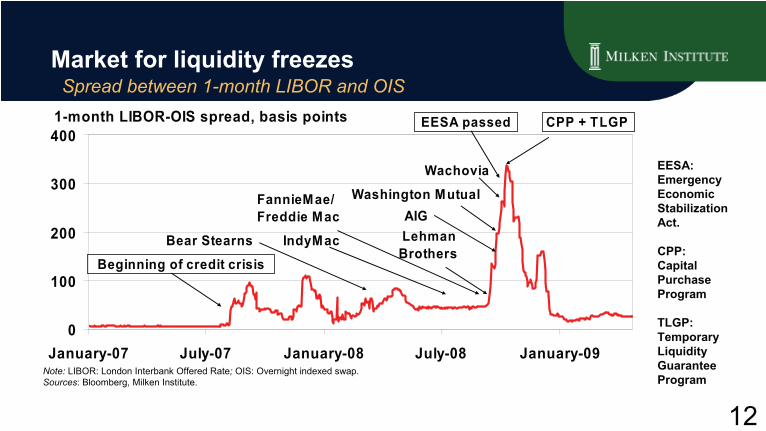

Market for liquidity freezes

Spread between 1-month LIBOR and OIS

Note: LIBOR:

London Interbank

Offered Rate; OIS: Overnight indexed swap.Sources: Bloomberg, Milken Institute.

0

100

200

300

400

January-07 July-07 January-08 July-08 January-09

1-month LIBOR-OIS spread, basis points

Bear Stearns IndyMac

FannieMae/Freddie Mac

Lehman Brothers

Wachovia

Washington Mutual AIG

CPP + TLGPEESA passed

Beginning of credit crisis

EESA: Emergency Economic Stabilization Act.

CPP: Capital Purchase Program

TLGP: Temporary Liquidity Guarantee Program

13

TED Spread reached historical high in 2008

Monthly, January 1985—March 2009

Sources: Bloomberg, Milken Institute.

0

50

100

150

200

250

300

350

1985 1988 1991 1994 1997 2000 2003 2006 2009

November 1987: 255 bps

September 2008: 315 bps

Average since 1985: 59 bps

Basis points

14

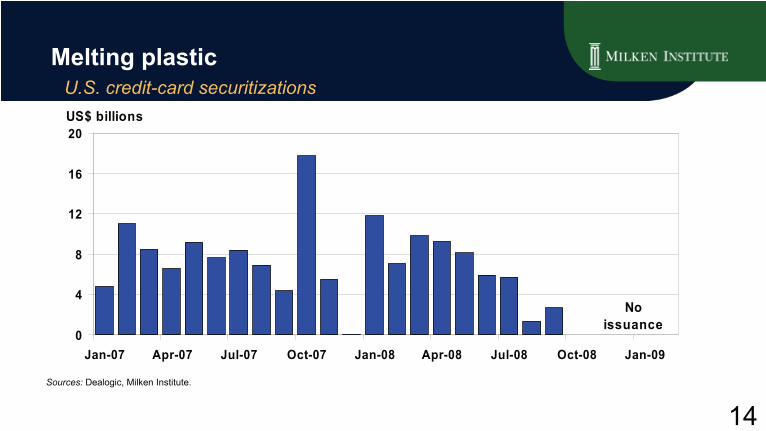

Melting plastic

U.S. credit-card securitizations

Sources:

Dealogic, Milken

Institute.

0

4

8

12

16

20

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09

US$ billions

No issuance

15

Credit drought Issuance of asset-backed securities in the U.S.

Sources:

Dealogic, Milken

Institute.*Through Mar. 5, 2009

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009*

US$ trillions

$2.1 billion

16

Comeback

U.S. corporate-bond volume, high-yield and investment-grade

Sources:

Dealogic, Milken

Institute.

0

40

80

120

160

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09

US$ billions

17

Counterparty risk increases

Note: Counterparty Risk index averages the market spreads of the

credit default swaps (CDS) of fifteen major credit derivatives dealers, including ABN Amro, Bank of America, BNP Paribas, Barclays Bank, Citigroup, Credit Suisse, Deutsche Bank, Goldman Sachs Group, HSBC, Lehman Brothers, JPMorgan Chase, Merrill Lynch, Morgan Stanley, UBS, and Wachovia. Sources:

Datastream, Milken Institute.

0

100

200

300

400

500

600

700

07/2007 09/2007 11/2007 01/2008 03/2008 05/2008 07/2008 09/2008 11/2008 01/2009 03/2009

Average CDS spread, basis points

Bear Stearns acquired

Government announces support for Fannie Mae and Freddie Mac

Lehman Brothers files for bankruptcy and Merrill Lynch acquired

AIG rescuedCitigroup agreed to buy Wachovia

October 10, 2008: 607 bps March 10, 2009: 573 bps

18

Rising risk: The credit default swap market roughly doubled each year from June 2001

through Oct. 2008

0.6 0.9 1.6 2.2 2.7 3.8 5.4 8.412.4

17.126.0

34.4

45.5

62.254.6

47.0

0

10

20

30

40

50

60

70

June2001

Dec.2001

June2002

Dec.2002

June2003

Dec.2003

June2004

Dec.2004

June2005

Dec.2005

June2006

Dec.2006

June2007

Dec.2007

June2008

Oct.2008

Notional amount of credit default swaps outstanding, US$ trillions

Source: International Swaps and Derivatives Association, Milken

Institute.

19

Participants in credit derivative market March 2007

Source: Bank for International Settlements.

CDS buyers of protection

Miscellaneous1%

Banks and dealers (Trading

portfolios)33%

Loan portfolios7%

Insurers 18%

Hedge funds31%

Mutual funds3%

Corporations2%

Pension funds5%

CDS sellers of protection

Miscellaneous1%

Banks and dealers (Trading

portfolios)39%

Loan portfolios20%

Insurers 6%

Hedge funds28%

Mutual funds2%

Corporations2%

Pension funds2%

20

Losses/write-downs, capital raised by

financial institutions worldwide

Sources: Bloomberg, Milken

Institute.

US$ billions, through April 10, 2009 Loses/Write-downs Capital raisedWachovia, United States 101.9 11Citigroup, United States 88.3 109.3AIG, United States 87.3 91.7Freddie Mac, United States 81.6 51.6Fannie Mae, United States 71.3 30.8Merrill Lynch, United States 55.9 29.9UBS, Switzerland 50.6 32.1Washington Mutual, United States 45.3 12.1Bank of America, United States 42.7 78.5HSBC, United Kingdom 42.2 23.7Others 621 633.2Grand total 1,288.1 1,103.9

21

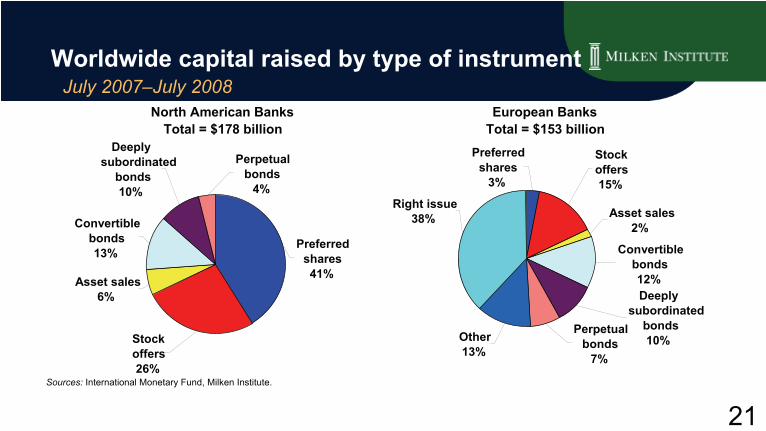

Worldwide capital raised by type of instrument

July 2007–July 2008

Sources:

International Monetary Fund, Milken

Institute.

Preferred shares

3%

Stock offers15%

Asset sales2%

Convertible bonds12%Deeply

subordinatedbonds10%

Perpetual bonds

7%

Other13%

Right issue38%

European BanksTotal = $153 billion

Preferred shares41%

Perpetual bonds

4%

Deeply subordinated

bonds10%

Convertible bonds13%

Asset sales6%

Stock offers26%

North American BanksTotal = $178 billion

22

Worldwide capital raised by source July 2007–July 2008

Sources:

International Monetary Fund, Milken

Institute.

Public investors

69%

Other institutionalinvestors

24%

Sovereign wealth funds

7%

January 2008–July 2008Total = $300 billion

Sovereign wealth funds60%

Public investors

12%

Other institutionalinvestors

28%

July 2007–December 2007Total = $56 billion

23

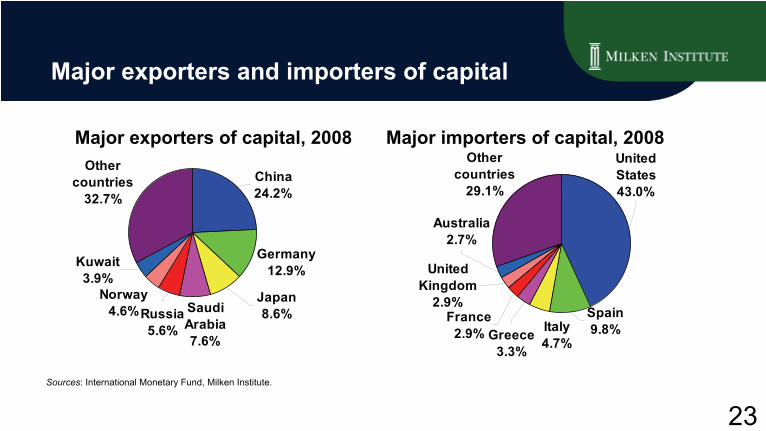

Major exporters and importers of capital

Sources: International Monetary Fund, Milken

Institute.

Major exporters of capital, 2008 Major importers of capital, 2008

Germany12.9%

Norway4.6%

Other countries

32.7%China24.2%

Saudi Arabia7.6%

Japan8.6%Russia

5.6%

Kuwait3.9%

United States43.0%

Greece3.3%

Italy4.7%

France2.9%

Australia2.7%

Spain9.8%

United Kingdom

2.9%

Other countries

29.1%

24

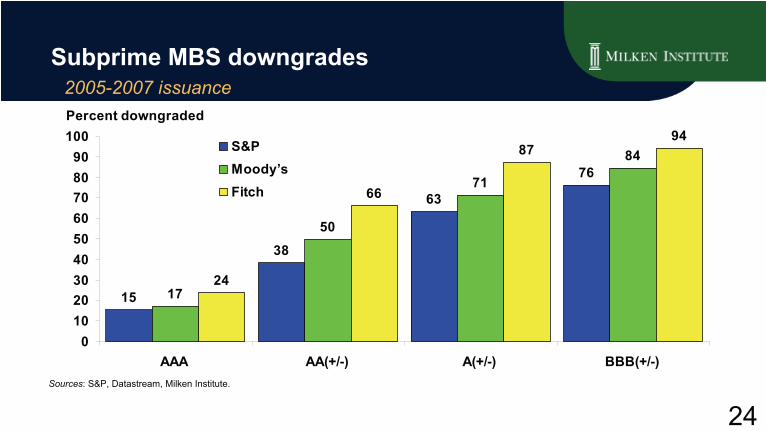

Subprime MBS downgrades

2005-2007 issuance

15

38

63

76

17

50

71

84

24

66

8794

0102030405060708090

100

AAA AA(+/-) A(+/-) BBB(+/-)

S&PMoody’sFitch

Percent downgraded

Sources: S&P, Datastream, Milken

Institute.

25

Leverage ratio for commercial banks

02468

101214161820

1896 1905 1914 1923 1932 1941 1950 1959 1968 1977 1986 1995 2004

Asset/capital ratio

Average, 1896 - 2008: 11.0x

1945: 18.2x 1979: 17.4x

1932: 6.2x

2008: 10.6x

1896: 3.6x

Sources: FDIC, Milken

Institute.

26

Leverage ratios of selected financial firms December 2008

9.3

10.6

11.1

31.6

26.2

21.5

67.9

0 10 20 30 40 50 60 70 80

Credit unions

Commercial banks

Saving institutions

Brokers/hedge funds

Federal Home Loan Banks

Fannie Mae

Freddie Mac

Leverage ratio, total assets/common equity

Note: Leverage ratios for

Freddie Mac and Fannie Mae are as of June 2008. The two institutions have negative common equities as of December 2008.Sources: FDIC, FHL Banks Office of Finance, National Credit Union Administration, Freddie Mac, Fannie Mae, Milken Institute.

(June 2008)

(June 2008)(June 2008)

27

What We’ve Learned from the Credit Crisis

James GellertPresident and CEO, Rapid Ratings

International

28

In Credit Ratings, the more things changed, the more they stayed the same…“The Commission shall conduct a study of the role and function of

credit rating agencies”

regarding “any impediments to the accurate appraisal by credit rating agencies of the financial resources and risks of issuers of securities”

–

Section 702 of Sarbanes-Oxley Act of 2002

The purpose is “to improve ratings quality for the protection of investors and in the public interest by fostering accountability, transparency, and competition in the credit rating agency industry”

–

Credit Rating Agency Reform Act of 2006

“Rating agency performance in the area of [structured products], has shaken investor confidence to its core“

–

SEC Chairman Nancy Schapiro

at the Roundtable to Examine Oversight of Credit Rating Agencies, April 15, 2009

29

Credit Ratings are woven into the fabric of the markets

“The story of the credit rating agencies is a story of a colossal

failure. The credit rating agencies occupy a special place in our financial markets. Millions of investors rely on them for

independent objective assessments. The rating agencies broke this bond of trust, and Federal regulators ignored the warning signs and did nothing to protect the public.”

--

Henry Waxman, Chairman of the House Oversight Committee, October 22, 2008

This “special place”

is:•in the Path Dependence of credit market professionals’

workflow norms •at least 8 Federal statutes, 41 regulations, over 100 state acts

and regulations, through LIBOR markets and myriad loan agreements, corporate policies, fiduciary charters, etc. •And, more recently, the Federal Reserve’s signal to the market that the Big 3 rating agencies are primus inter pares

or first among equals:“I write to express my deep concern about the ratings eligibility

criteria for the Federal Reserve’s anticipated $1 trillion lending initiative….[and] the Federal Reserve’s policy of preferring Standard & Poor’s, Moody’s Investor Services and Fitch Ratings…. The Federal Reserve should not be favoring large market participants, whose mistakes helped precipitate the current crisis…”

--

CT Attorney General Richard Blumenthal in a letter to Ben Bernanke

on April 6, 2009

30

What’s being done: more regulation –

not less

SEC, IOSCO and other international initiatives

Various bills floating through Congress

SEC review of rating agencies for transparency, conflicts, compliance, etc., and evaluation of ratings references in SEC regulations

“It is imperative that the Commission adopt its proposal to address the oligopoly in the rating industry and the overreliance

on NRSRO ratings by removing the regulatory requirements embedded in numerous SEC rules”

--

SEC Commissioner Kathleen L. Casey, Feb. 6, 2009

Nevertheless, the winds of change are for more regulation --

not less

31

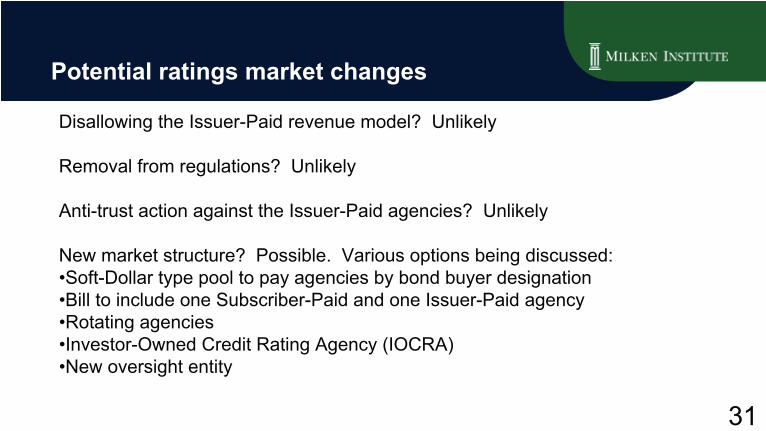

Potential ratings market changes

Disallowing the Issuer-Paid revenue model? Unlikely

Removal from regulations? Unlikely

Anti-trust action against the Issuer-Paid agencies? Unlikely

New market structure? Possible. Various options being discussed:•Soft-Dollar type pool to pay agencies by bond buyer designation•Bill to include one Subscriber-Paid and one Issuer-Paid agency•Rotating agencies •Investor-Owned Credit Rating Agency (IOCRA) •New oversight entity

32

What we’re seeing at Rapid Ratings

Buy-Side, Sell-Side and Corporations (for customer, supplier and vendor risk management) are all experiencing:

•

Dissatisfaction with the status quo –

market players have learned they cannot rely on the Big 3, but they cannot escape them completely

•

Greater openness to alternative ratings approaches and desire for “accurate”

and “actionable”

ratings

•

More focus from outside directors, audit committees, CEO/CFOs on

counterparty risk management

•

Greater desire to find uncorrelated risk management perspectives

•

All parties watching the regulatory response to ratings for guidance. And not enough concern about the pending corporate refinancings

33

What we’re seeing at rapid ratings continued

As one example of an early warning on the way down…

…but no recovery in sight…

US Homebuilders

34

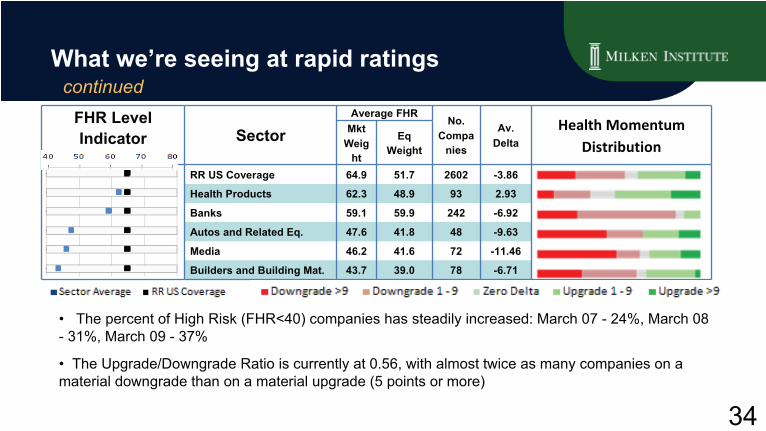

What we’re seeing at rapid ratings continued

FHR Level Indicator Sector

Average FHRNo.

Compa

nies

Av.Delta

Health Momentum

DistributionMkt

Weig

ht

Eq

Weight

RR US Coverage 64.9 51.7 2602 -3.86

Health Products 62.3 48.9 93 2.93

Banks 59.1 59.9 242 -6.92

Autos and Related Eq. 47.6 41.8 48 -9.63

Media 46.2 41.6 72 -11.46

Builders and Building Mat. 43.7 39.0 78 -6.71

•

The percent of High Risk (FHR<40) companies has steadily increased: March 07 -

24%, March 08 -

31%, March 09 -

37%

•

The Upgrade/Downgrade Ratio is currently at 0.56, with almost twice as many companies on a material downgrade than on a material upgrade (5 points or more)

35

Can the system be fixed in time?

Source: ML Indices: (1998 -

2010 Maturities calculated as at Jan 1 the prior year). (2010 -

2015 Maturities calculated as at Jan 1 2009). $ in Billions

The focus on accurate corporate ratings and information transparency for CLO and other ratings will be critical

High Yield Index Refinancing NeedsInvestment Grade Index Refinancing Needs

020406080

100120140

1998 2002 2006 2010 20140

50100150200250300350

1998 2002 2006 2010 2014

($ billion)

36

Can the system be fixed in time?

2006 & 2007 issued U.S. leverage finance peak maturity

Source:

Thomson One.

US$ billions

0

100

200

300

400

500

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

2006 2007

37

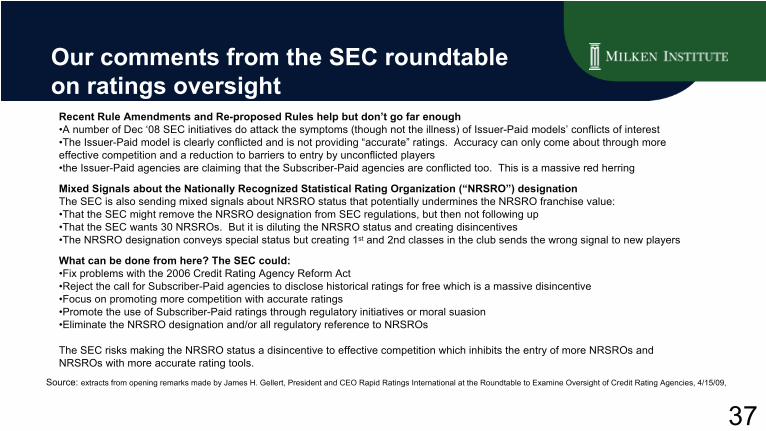

Our comments from the SEC roundtable on ratings oversight

Source: extracts from opening remarks made by James H. Gellert, President and CEO Rapid Ratings International at the Roundtable to Examine Oversight of Credit Rating Agencies, 4/15/09,

Recent Rule Amendments and Re-proposed Rules help but don’t go far enough•A number of Dec ‘08 SEC initiatives do attack the symptoms (though not the illness) of Issuer-Paid models’

conflicts of interest •The Issuer-Paid model is clearly conflicted and is not providing “accurate”

ratings. Accuracy can only come about through more effective competition and a reduction to barriers to entry by unconflicted

players•the Issuer-Paid agencies are claiming that the Subscriber-Paid agencies are conflicted too. This is a massive red herring

Mixed Signals about the Nationally Recognized Statistical Rating

Organization (“NRSRO”) designationThe SEC is also sending mixed signals about NRSRO status that potentially undermines the NRSRO franchise value:•That the SEC might remove the NRSRO designation from SEC regulations, but then not following up •That the SEC wants 30 NRSROs. But it is diluting the NRSRO status and creating disincentives•The NRSRO designation conveys special status but creating 1st

and 2nd classes in the club sends the wrong signal to new players

What can be done from here? The SEC could:•Fix problems with the 2006 Credit Rating Agency Reform Act •Reject the call for Subscriber-Paid agencies to disclose historical ratings for free which is a

massive disincentive•Focus on promoting more competition with accurate ratings•Promote the use of Subscriber-Paid ratings through regulatory initiatives or moral suasion•Eliminate the NRSRO designation and/or all regulatory reference to NRSROs

The SEC risks making the NRSRO status a disincentive to effective competition which inhibits the entry of more NRSROs

and NRSROs

with more accurate rating tools.

38

Let’s hope we can do better

“The crisis of the past 18 months has exposed critical gaps and weaknesses in our regulatory system.

As risks built up, internal risk management systems, rating agencies and regulators simply did not understand or address critical behaviors until they had already resulted in catastrophic losses.”

--

Treasury Secretary Geithner, March 26, 2009

39

What We’ve Learned from the Credit Crisis

James McCaughanChief Executive Officer

Principal Global Investors LLC

40

U.S. private debt

U.S. Private Debt% Nominal GDP

2008: 4Q: 175.5%

Source:

ISI Group.

41

U.S. private debt

Source:

ISI Group.

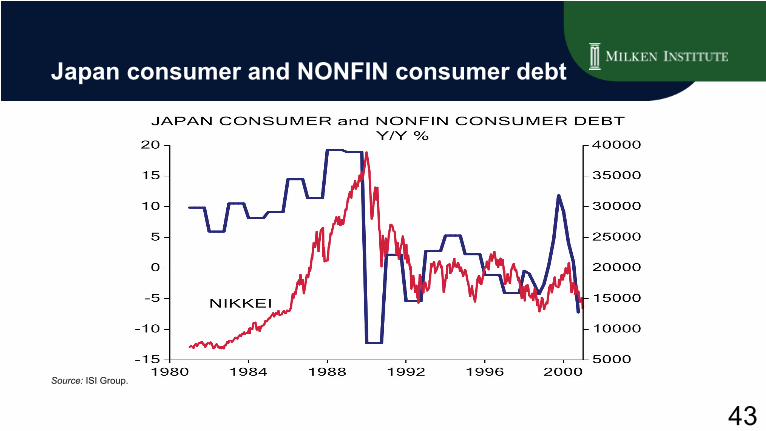

42

Japan consumer and NONFIN consumer debt

Source:

ISI Group.

43

Japan consumer and NONFIN consumer debt

Source:

ISI Group.

44

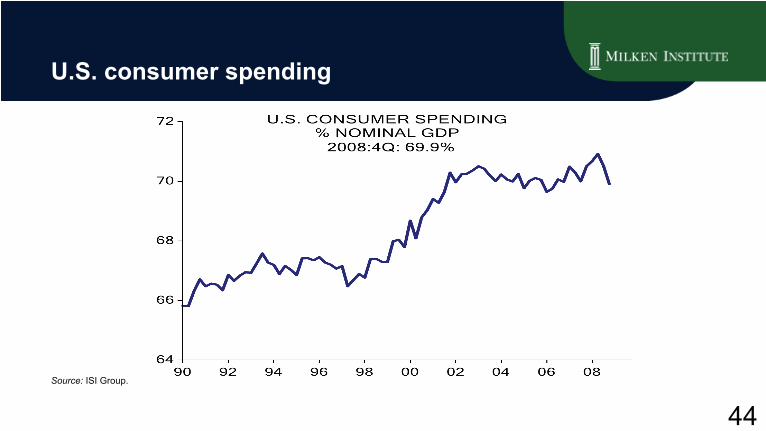

U.S. consumer spending

Source:

ISI Group.

45

U.S. saving rate

Source:

ISI Group.

46

U.S. saving rate

Source:

ISI Group.

U.S. SAVING RATEActual 2009:1Q 4.3%Forecast 2009:3Q 9.4%

-2

0

2

4

6

8

10

12

14

1965 1970 1975 1980 1985 1990 1995 2000 2005

47

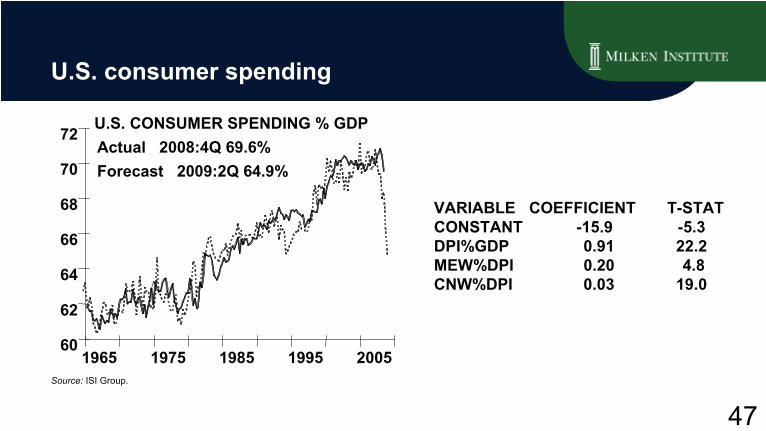

U.S. consumer spending

VARIABLE COEFFICIENT T-STAT CONSTANT

-15.9 -5.3 DPI%GDP

0.91 22.2 MEW%DPI

0.20 4.8 CNW%DPI

0.03 19.0

U.S. Consumer Spending % GDPActual 2008: 4Q 69.6%

Forecast 2009: 2Q 64.9%

Source:

ISI Group.

U.S. CONSUMER SPENDING % GDPActual 2008:4Q 69.6%Forecast 2009:2Q 64.9%

60

62

64

66

68

70

72

1965 1975 1985 1995 2005

48

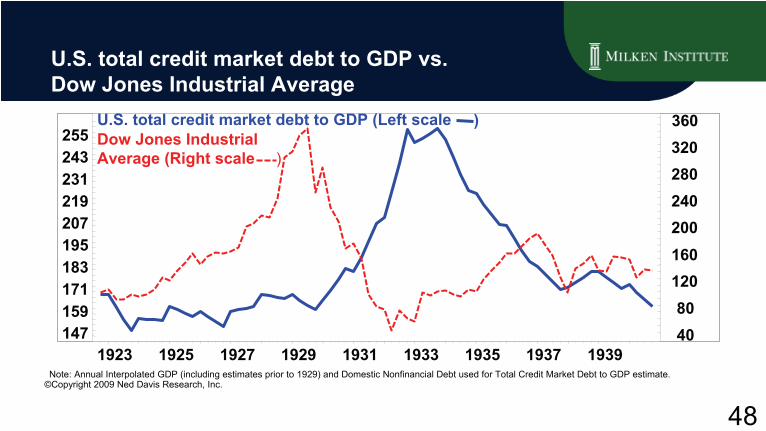

U.S. total credit market debt to GDP vs. Dow Jones Industrial Average

147 159 171 183 195 207 219 231 243 255

Note: Annual Interpolated GDP (including estimates prior to 1929) and Domestic Nonfinancial Debt used for Total Credit Market Debt to GDP estimate.

4080

120 160 200 240 280 320 360 ) U.S. total credit market debt to GDP (Left scale

Dow Jones Industrial Average (Right scale )

1923 1925 1927 1929 1931 1933 1935 1937 1939©Copyright 2009 Ned Davis Research, Inc.

49

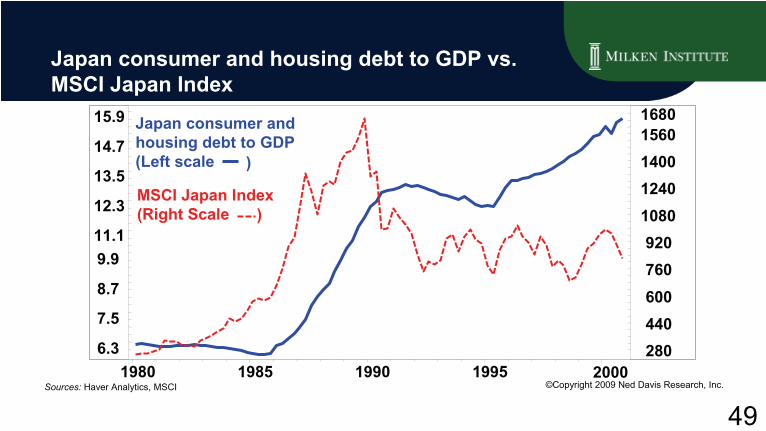

Japan consumer and housing debt to GDP vs. MSCI Japan Index

6.3

7.5

8.7

9.9 11.1

12.3

13.5

14.7

15.9

280 440 600 760 920

10801240140015601680Japan consumer and

housing debt to GDP (Left scale )

MSCI Japan Index (Right Scale )

1980 1985 1990 1995 2000©Copyright 2009 Ned Davis Research, Inc. Sources:

Haver

Analytics, MSCI

50

Private domestic non-financial debt to GDP vs. Dow Jones Industrial Average

132

140

148

156

164

172

180

188

25003500450055006500750085009500

10500 11500 12500 13500 Private domestic non-financial debt to GDP (Left Scale )

Dow Jones Industrial Average (Right scale )

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008©Copyright 2009 Ned Davis Research, Inc.

51

13500

U.S. total credit market debt to GDP vs. Dow Jones Industrial Average

228 240 252 264 276 288 300 312 324 336 348 360

25003500450055006500750085009500

10500 11500 12500

U.S. total credit market debt to GDP (Left scale ) Dow Jones Industrial Average (Right scale )

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008©Copyright 2009 Ned Davis Research, Inc.

52

Japan government debt to GDP vs. MSCI Japan Index

MSCI Japan Index (Right scale

3440465258647076828894

100

280 400 520 640 760 880

100011201240136014801600Japan government debt to GDP

(Left scale )

)

1980 1985 1990 1995 2000©Copyright 2009 Ned Davis Research, Inc. Sources:

Haver

Analytics, MSCI

53

What We’ve Learned from the Credit Crisis

Gary ShillingPresident

A. Gary Shilling & Co.

54

NASDAQ Index

Source: Yahoo Finance.

Jan-80 Dec-83 Nov-87 Nov-91 Oct-95 Oct-99 Oct-03 Oct-070500

1,0001,5002,0002,5003,0003,5004,0004,5005,0005,500

05,001,0001,5002,0002,5003,0003,5004,0004,5005,0005,500

Last Point 04/16/09: 1670

55

Real Quality-Adjusted home prices

Source:

Robert Shiller.

1890 1910 1930 1950 1970 199060

80

100

120

140

160

180

200

220

60

80

100

120

140

160

180

200

220

Avg: 1946 -1998=111

Last point 4Q 08: 137

56

ABX BBB-

Index

07-1

Source:

Markit

Ltd./UBS.

Jan-07 Jun-07 Nov-07 Apr-08 Aug-08 Jan-090102030405060708090

100

0102030405060708090100

Last point 04/16/09: 2.35

57

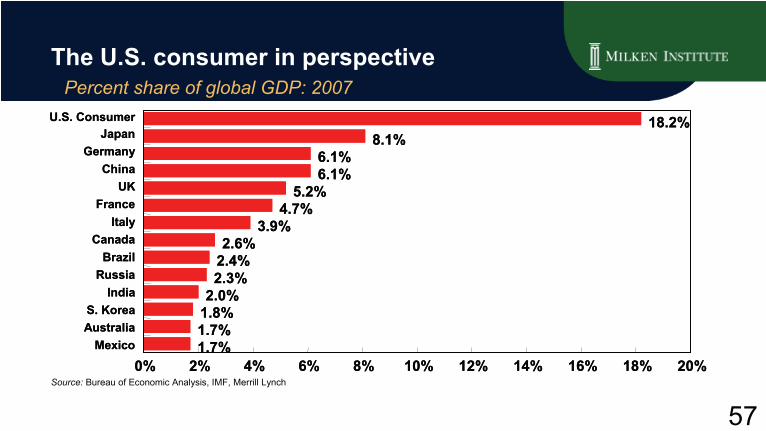

The U.S. consumer in perspective

Percent share of global GDP: 2007

Source:

Bureau of Economic Analysis, IMF, Merrill Lynch

U.S. ConsumerJapan

GermanyChina

UKFrance

ItalyCanada

BrazilRussia

IndiaS. KoreaAustralia

Mexico

18.2%8.1%

6.1%6.1%

5.2%4.7%

3.9%2.6%

2.4%2.3%

2.0%1.8%1.7%1.7%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

U.S. ConsumerJapan

GermanyChina

UKFrance

ItalyCanada

BrazilRussia

IndiaS. KoreaAustralia

Mexico

18.2%8.1%

6.1%6.1%

5.2%4.7%

3.9%2.6%

2.4%2.3%

2.0%1.8%1.7%1.7%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

58

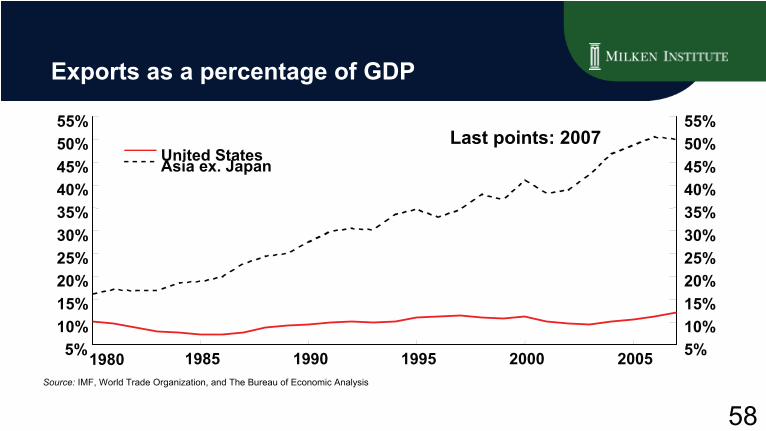

Exports as a percentage of GDP

Source:

IMF, World Trade Organization, and The Bureau of Economic Analysis

1980 1985 1990 1995 2000 2005

Last points: 2007

5%10%15%20%25%30%35%40%45%50%55%

5%10%15%20%25%30%35%40%45%50%55%

United StatesAsia ex. Japan

59

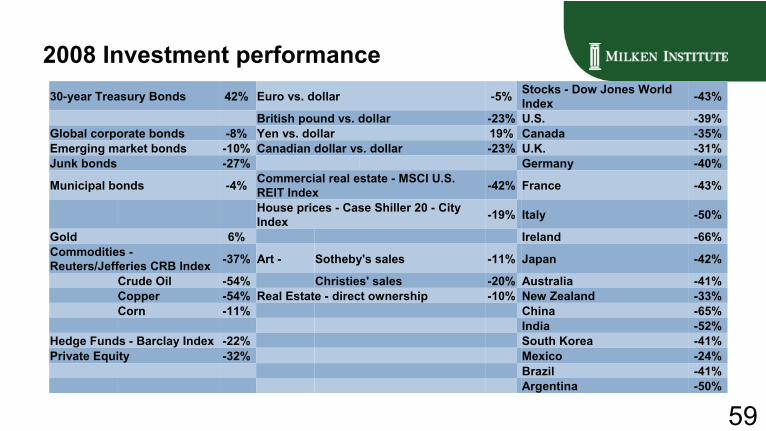

30-year Treasury Bonds 42% Euro vs. dollar -5% Stocks -

Dow Jones World Index -43%

British pound vs. dollar -23% U.S. -39%Global corporate bonds -8% Yen vs. dollar 19% Canada -35%Emerging market bonds -10% Canadian dollar vs. dollar -23% U.K. -31%Junk bonds -27% Germany -40%

Municipal bonds -4% Commercial real estate -

MSCI U.S. REIT Index -42% France -43%

House prices -

Case Shiller

20 -

City Index -19% Italy -50%

Gold 6% Ireland -66%Commodities -

Reuters/Jefferies CRB Index -37% Art - Sotheby's sales -11% Japan -42%

Crude Oil -54% Christies' sales -20% Australia -41%Copper -54% Real Estate -

direct ownership -10% New Zealand -33%Corn -11% China -65%

India -52%Hedge Funds -

Barclay Index -22% South Korea -41%Private Equity -32% Mexico -24%

Brazil -41%Argentina -50%

2008 Investment performance

60

1953 1957 1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 20050%

20%

40%

60%

80%

100%

120%

140%

0%

20%

40%

60%

80%

100%

120%

140%

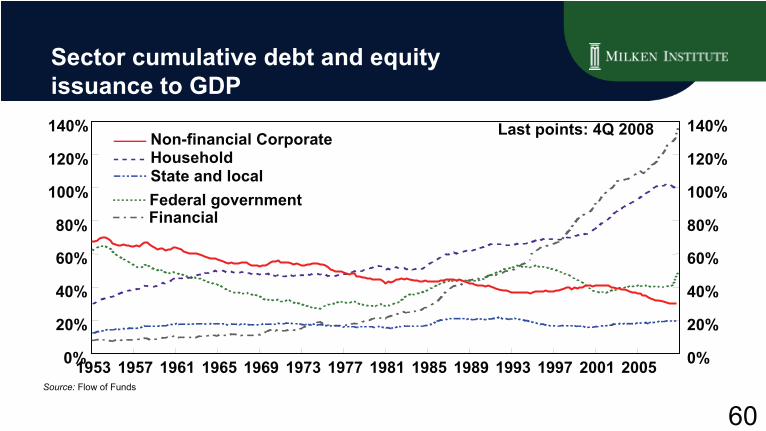

Sector cumulative debt and equity issuance to GDP

Source:

Flow of Funds

Non-financial CorporateHouseholdState and localFederal governmentFinancial

Last points: 4Q 2008

61

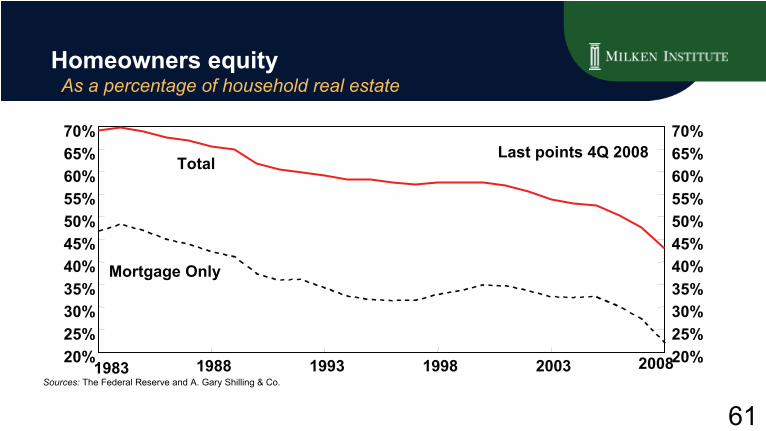

1983 1988 1993 1998 2003 200820%25%30%35%40%45%50%55%60%65%70%

20%25%30%35%40%45%50%55%60%65%70%

Total

Mortgage Only

Homeowners equity

As a percentage of household real estate

Last points 4Q 2008

Sources:

The Federal Reserve and A. Gary Shilling & Co.

62

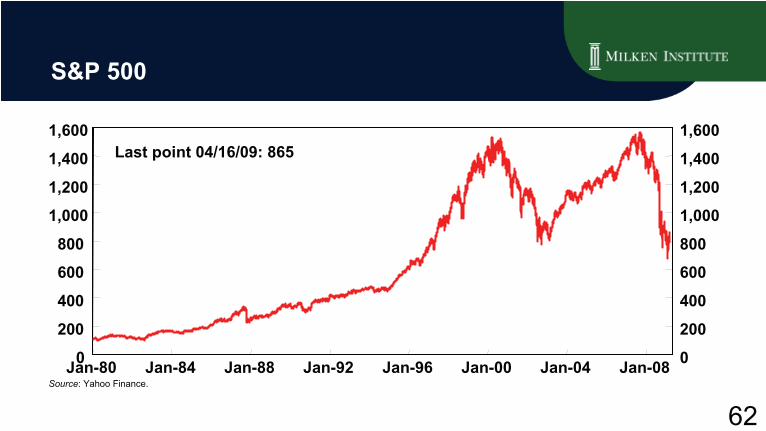

S&P 500

Source: Yahoo Finance.Jan-80 Jan-84 Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-080

200

400

600

800

1,000

1,200

1,400

1,600

0

200

400

600

800

1,000

1,200

1,400

1,600Last point 04/16/09: 865

63

Jan-59 May-67 Sep-75 Jan-84 May-92 Sep-00 Jan-09-4-202468

10121416

-4-20246810121416

U.S. personal saving rate

Seasonally adjusted annual rate

Last Point Feb. 09: 4.2%

Source:

Bureau of Economic Analysis.

64

1959 1964 1969 1974 1979 1984 1989 1994 1999 200460%

62%

64%

66%

68%

70%

72%

60%

62%

64%

66%

68%

70%

72%

Consumer spending

As a percentage of GDP

Last Point 4Q 08: 69.6%

Source:

Bureau of Economic Analysis.

65

1952-I 1964-III 1977-I 1989-III 2002-I20%

40%

60%

80%

100%

120%

140%

20%

40%

60%

80%

100%

120%

140%

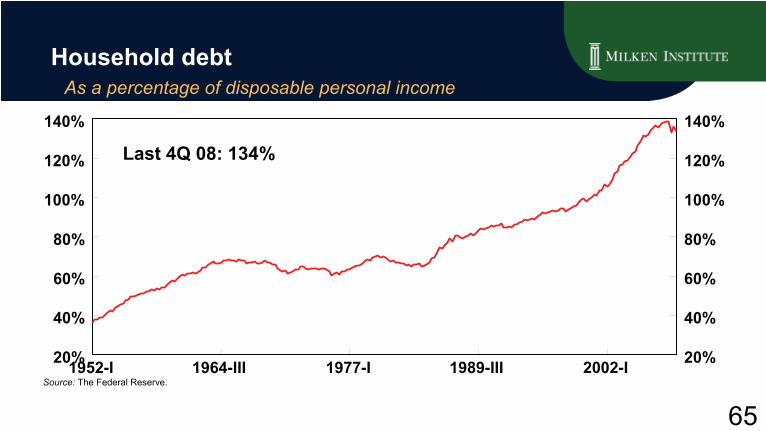

Household debt As a percentage of disposable personal income

Last 4Q 08: 134%

Source:

The Federal Reserve.